Natural Language Processing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

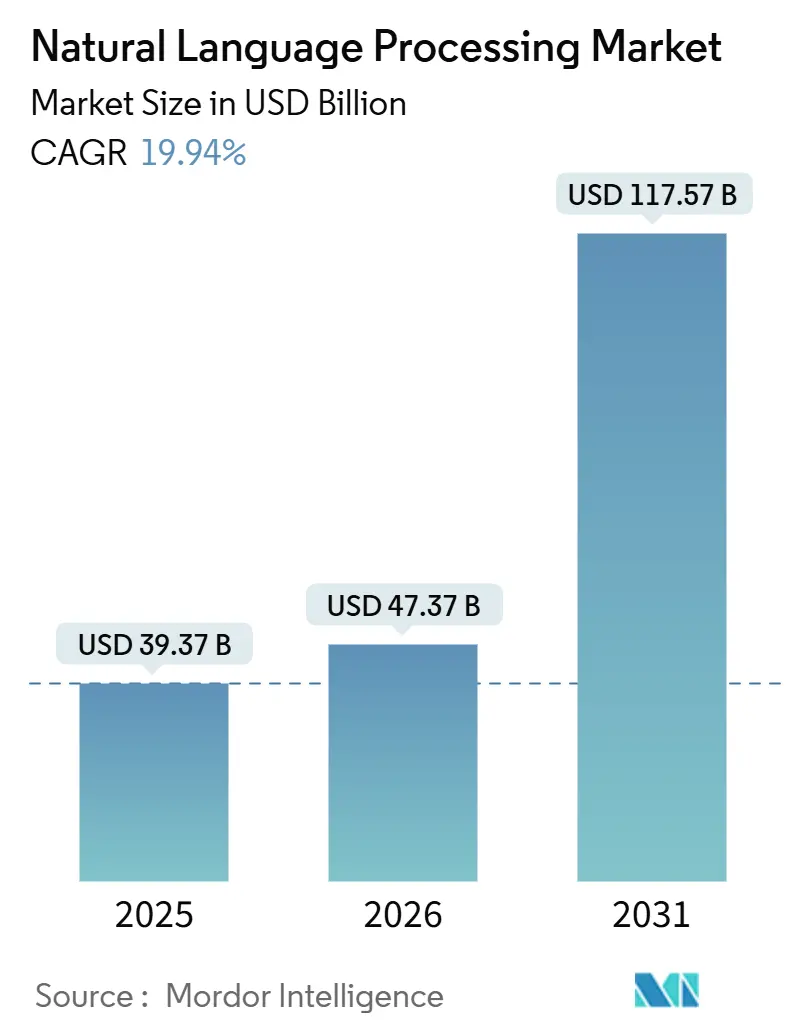

| Market Size (2026) | USD 47.37 Billion |

| Market Size (2031) | USD 117.57 Billion |

| Growth Rate (2026 - 2031) | 19.94% CAGR |

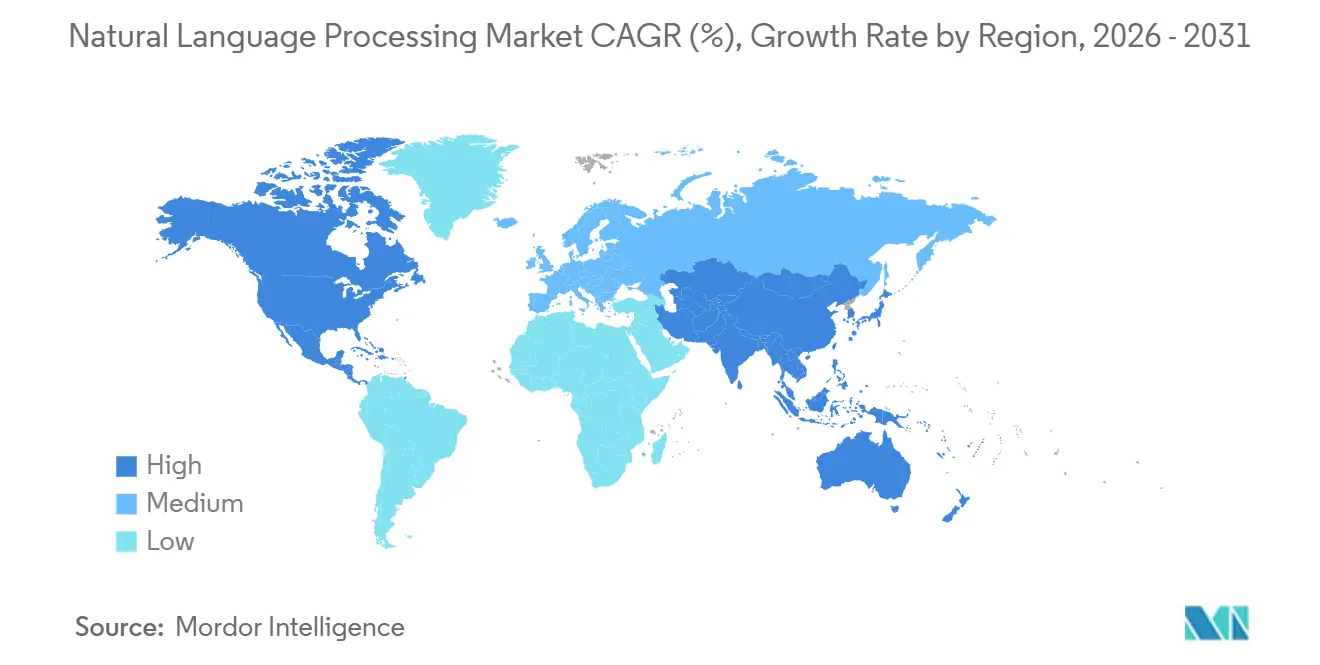

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Natural Language Processing Market Analysis by ���ϲ�����

The natural language processing market size is projected to expand from USD 39.37 billion in 2025 and USD 47.37 billion in 2026 to USD 117.57 billion by 2031, registering a CAGR of 19.94% between 2026 to 2031. The surge is anchored in transformer refinements that lift domain-specific accuracy by double-digit points, cloud–edge synergies that shrink inference latency below 100 milliseconds, and regulatory clarity that channels budget from proofs of concept into full production. Enterprise buyers now treat foundation models as core infrastructure rather than experimental add-ons, reallocating analytics budgets toward integration tooling, bias auditing, and carbon-neutral compute options. Vendor competition centers on lowering cost per token, pre-certifying high-risk modules for the EU AI Act, and winning low-resource language segments that remain underserved by English-centric systems. Capital flows mirror these priorities, with hyperscalers funneling GPU supply into managed platforms while automotive and healthcare leaders finance edge inference projects to secure deterministic latency.

Key Report Takeaways

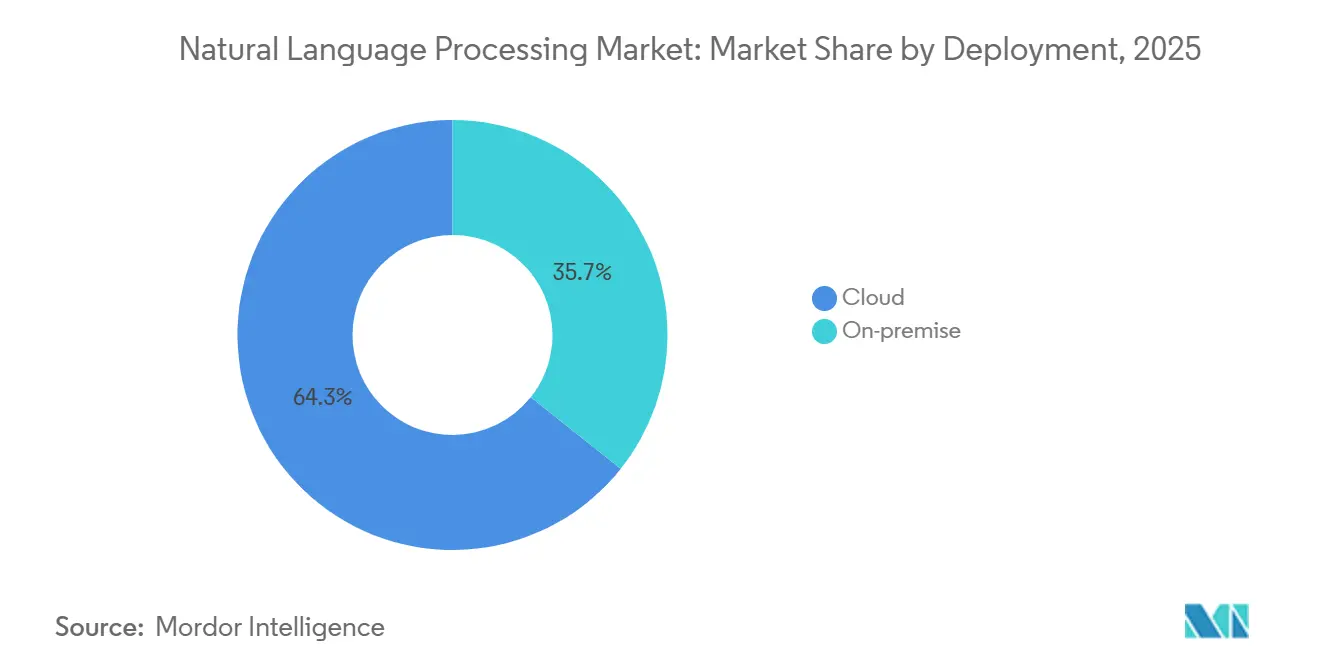

- By deployment, cloud captured 64.31% of natural language processing market share in 2025, while services recorded the fastest projected CAGR at 22.62% through 2031.

- By organization size, large enterprises held 73.13% of the natural language processing market in 2025, whereas small and medium enterprises are forecast to expand at a 19.98% CAGR to 2031.

- By component, software commanded 46.14% share of the natural language processing market size in 2025, but services are advancing at a 22.62% CAGR through 2031.

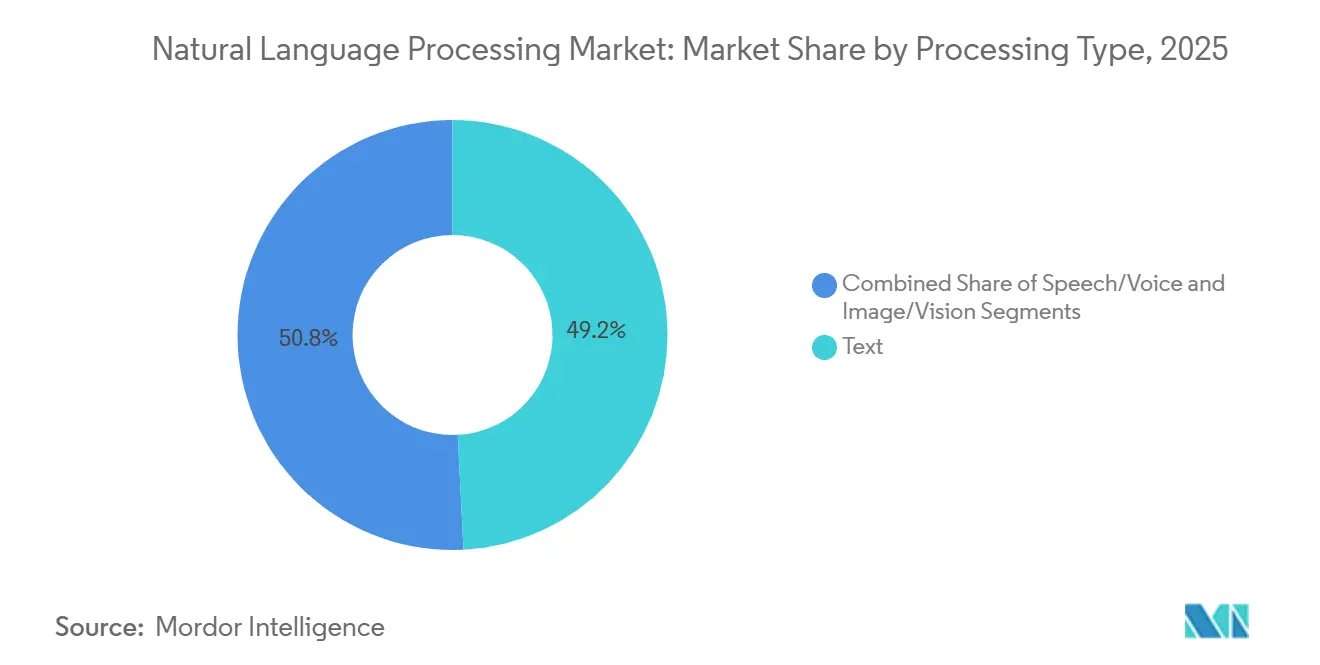

- By processing type, text processing led with 49.18% share in 2025 and speech recognition is projected to post a 22.41% CAGR between 2026-2031.

- By end-user industry, BFSI accounted for 20.13% share of the natural language processing market size in 2025, while healthcare and life sciences show the highest growth trajectory at 24.84% CAGR through 2031.

- By geography, North America retained 37.92% share in 2025 and Asia-Pacific is positioned for the quickest climb at 22.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Natural Language Processing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI-Powered Model Accuracy Gains | +4.5% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Surge in Conversational AI Adoption in Customer Support | +3.8% | Global, led by North America and Europe, expanding into Asia-Pacific | Short term (≤ 2 years) |

| Integration of NLP in Embedded or Edge Devices | +3.2% | Asia-Pacific core, spillover to North America and Europe | Medium term (2-4 years) |

| Proliferation of Domain-Specific LLMs for Regulated Industries | +2.9% | North America and Europe, gradual adoption in Asia-Pacific | Long term (≥ 4 years) |

| Rising Demand for Real-Time Speech Recognition in Automotive and Smart Devices | +2.4% | Global, early leadership in North America, Europe and China | Medium term (2-4 years) |

| Multimodal Foundation Models Unlocking New Verticals | +2.1% | Global, concentrated in North America and Asia-Pacific technology hubs | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Generative-AI-Powered Model Accuracy Gains

Foundation releases in 2025 posted 18-23 percentage-point jumps on specialist benchmarks when fine-tuned on fewer than 10,000 labels, slashing annotation budgets and opening high-liability workflows such as legal clause extraction and ICD-10 coding.[1]Nature Staff, “Large Language Models Encode Clinical Knowledge,” Nature, nature.com Google’s Gemini 2.0 Flash trimmed inference latency by 40%, enabling conversational and summarization tasks that once demanded batch processing. Mixture-of-experts routing keeps only 10-15% of a trillion parameters active per query, lowering energy draw without hurting precision. OpenAI’s o3 model logged 87.5% on ARC-AGI, signaling that multi-step reasoning is entering automated scope. Together these advances fueled board-level confidence that the natural language processing market can underpin mission-critical operations.

Surge in Conversational AI Adoption in Customer Support

Twelve-to-eighteen-percent wage inflation for tier-1 agents pushed contact centers toward automation, and retrieval-augmented generation raised first-contact resolution to 75-85% by mid-2025.[2]Salesforce Press Team, “Agentforce 2.0: Autonomous Agents for Every Business,” salesforce.comSalesforce’s Agentforce 2.0 orchestrates CRM, billing, and inventory flows without hand-offs, cutting average handle time by up to 40%. Cloud platforms bundled chat APIs into existing enterprise agreements, shrinking pilot cycles from quarters to weeks. The EU AI Act tagged most customer-service bots as limited-risk, sparing them conformity reviews and accelerating adoption across the trading bloc.[3]European Commission, “Regulatory Framework on Artificial Intelligence,” digital-strategy.ec.europa.eu

Integration of NLP in Embedded or Edge Devices

Smartphone chipsets embedding neural units now run 7-billion-parameter models locally, erasing the 200-500 milliseconds of round-trip latency tied to cloud calls and calming privacy fears. Apple’s Intelligence handles 80% of Siri requests on-device, a shift that aligns with tight data-localization rules in China and India. Mercedes-Benz integrated a 95%-accurate domain model into its MBUX cockpit, showing that edge inference can satisfy real-time automotive needs without connectivity. The natural language processing market consequently tilts toward on-device toolkits that guarantee deterministic response times and compliance with residency mandates.

Proliferation of Domain-Specific LLMs for Regulated Industries

Vertical models fine-tuned on curated corpora outperformed generic peers by 12-18 points, justifying 3-5× higher training spend in sectors where misclassification invites fines. Nuance’s DAX Copilot processed over 1 million clinical visits, trimming documentation chores by half and easing burnout. Banks adopted filings-trained models to slash false positives in anti-money-laundering from 95% to below 70%. The EU AI Act demands explainability for credit scoring, nudging vendors toward transparent architectures and certified toolchains.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of High-Quality, Bias-Free Training Data | -1.8% | Global, acute in non-English and low-resource languages | Short term (≤ 2 years) |

| Escalating Inference Costs for Large Models | -1.5% | Global, most pronounced in North America and Europe | Medium term (2-4 years) |

| Cross-Border Data Residency Compliance Barriers | -1.2% | Global, concentrated in Europe, China and India | Long term (≥ 4 years) |

| Environmental Footprint of Large-Scale Training Compute | -0.9% | Global, regulatory pressure strongest in Europe | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Shortage of High-Quality, Bias-Free Training Data

Audits showed 70-80% of corpora remain English, leading to 15-25-point drops in other languages and exposing enterprises to compliance risk in multilingual regions. Synthetic generators fill gaps yet risk mode collapse after repeated fine-tunes. Health records are siloed behind HIPAA, while PCI-DSS locks down transaction logs, fragmenting training pools. Without standardized bias tests, firms invent bespoke audits that slow procurement. The restraint weighs heavily on national markets seeking sovereign AI autonomy.

Escalating Inference Costs for Large Models

Serving 100-billion-parameter systems at sub-second latency takes 8-16 GPUs per instance, driving compute bills up to USD 100,000 per month for 1 million daily users. Quantization and pruning halve parameters but trim accuracy by several points, a hit many risk managers reject. Toolchains such as NVIDIA TensorRT-LLM triple throughput, yet steep learning curves delay deployment. Tiered cloud pricing adds volatility when traffic spikes. The cost headwind forces product teams to weigh quality against margin, restraining the natural language processing market in price-sensitive applications.

Segment Analysis

By Deployment: Cloud Dominance Masks Edge Momentum

Cloud retained 64.31% share of the natural language processing market in 2025 as enterprises favored elastic scaling and bundled AI services. Through 2031 the segment grows at 20.01% as hyperscalers lock in workloads by embedding proprietary models into broader contracts. On-premise clusters persist inside banks and hospitals that must audit every data flow, even when this choice raises cost by up to 50%. AWS Bedrock and Azure confidential enclaves now blur the line, letting clients keep sensitive payloads inside virtual private clouds while still relying on managed orchestration.

Edge adoption surges as smartphone penetration tops 70% in Asia-Pacific and automakers demand deterministic voice control. Google’s AI Edge SDK compresses Gemini Nano to under 2 GB, proving high-grade NLP can live on mid-tier handsets. Mercedes-Benz and BMW show 20-point gains in voice intent accuracy after localizing inference. Processing data in the device satisfies China’s Personal Information Protection Law with no architecture changes, and similar dynamics play out under India’s Digital Personal Data Protection Act. The dual-track evolution means the natural language processing market now values cloud and edge parity rather than single-venue supremacy.

By Organization Size: SMEs Close the Gap

Large enterprises held 73.13% of the natural language processing market share in 2025, leveraging petabytes of data and dedicated MLOps teams. Yet SMEs are projected to outpace at a 19.98% CAGR because no-code agents and pay-per-token models eliminate capital barriers. Hugging Face hubs and consumption-based cloud pricing push experimentation costs below USD 20,000, affordable even to seed-stage startups. Fast decision cycles let SMEs pilot voice commerce bots or contract analyzers in weeks, often beating slow-moving incumbents to niche opportunities.

Corporate titans keep an edge in multi-system integrations that tap ERP, CRM and supply chain feeds concurrently. They also shoulder heavier EU AI Act audits that can extend deployment by up to a year, an overhead the smallest firms avoid when their use cases fall under limited-risk classifications. Over the forecast horizon convergence is likely, with mature tooling erasing technical gaps and forcing both cohorts to differentiate on workflow intimacy rather than raw compute scale.

By Component: Services Surge as Integration Complexity Escalates

Software captured 46.14% of natural language processing market spending in 2025 through licensing of foundation models and fine-tune platforms. Yet services, forecast to grow 22.62% annually, become the fastest-rising line item as enterprises confront model drift, bias monitoring, and EU conformance audits. Accenture, Deloitte and PwC now package vendor selection, data-pipeline buildout, and 24-month MLOps support into fixed-fee bundles exceeding USD 5 million for Fortune-500 rollouts.

Hardware remains essential, with NVIDIA GPUs retaining over 80% of training chips shipped, but its share inches downward as custom ASICs from hyperscalers find traction in inference workloads. The natural language processing market size for services will likely eclipse hardware by 2028, marking a pivot from capex to opex as complexity supersedes raw silicon scarcity.

By Processing Type: Speech Recognition Gains Traction

Text processing maintained 49.18% share in 2025 thanks to mature document mining and sentiment tools. Speech recognition, however, is on track for a 22.41% CAGR because real-time transcription unlocks ambient healthcare documentation and in-car voice assistants. Ambient intelligence in clinics removes 40-50% of paperwork minutes per visit, a relief amid physician shortages. Automotive OEMs deploy fully offline assistants, eradicating coverage black spots and privacy worries.

Multimodal models such as GPT-4V cross-link images with text, widening scope to retail product search or X-ray interpretation. As vision modules mature, the natural language processing market evolves into a multimodal arena where keyboards compete with cameras and microphones for data input.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Healthcare Leads Adoption Curve

Healthcare and life sciences grow at 24.84% CAGR through 2031, propelled by ambient note-taking, coding automation, and drug-discovery literature mining. Nuance’s DAX Copilot handles over 1 million visits, granting providers capacity to see two extra patients daily without extending hours. Financial services, holding 20.13% share in 2025, focuses on fraud detection that cuts false positives by a quarter and speeds suspicious-transaction blocks to under two seconds.

Retail channels exploit visual search that turns photos into product listings, lifting conversion by double digits in pilots. Manufacturing leverages log parsing for predictive maintenance, slicing unplanned downtime by up to 30%. Across sectors, success increasingly depends on workflow integration depth and bias governance rather than vanilla text analytics.

Geography Analysis

North America kept 37.92% share in 2025, anchored by hyperscaler infrastructure and risk-tolerant early adopters. Enterprises tap generous venture funding, and regulatory sandboxes let banks trial generative models under supervisory guidance. Yet saturation and rising compliance overhead temper growth to high teens.

Asia-Pacific records the fastest climb at 22.13% CAGR as China’s USD 50 billion sovereign-AI push, India’s public digital stack, and Japan’s aging-population pressures converge. Chinese state-owned firms mandate domestic model deployment, boosting Baidu and Alibaba adoption. India’s Unified Payments Interface feeds billions of multilingual records into fraud and credit models. Japanese hospitals enjoy tax breaks when installing ambient documentation, spurring clinical NLP rollouts.

Europe benefits from the EU AI Act’s clarity, though conformity reviews add 6-12 months to high-risk launches. Germany’s automakers embed local voice assistants to satisfy GDPR. The United Kingdom encourages KYC automation to trim compliance costs. South America adopts customer-service bots tuned to regional dialects, while the Middle East funds sovereign AI as economic-diversification pillars. Africa’s uptake clusters in Nigeria and Kenya where mobile-first NLP supports fintech and ag-extension messaging. Despite disparate starting points, every region positions the natural language processing market as core digital infrastructure by decade’s end.

Competitive Landscape

Microsoft, Google, Amazon, OpenAI, and NVIDIA, the top five vendors, command about 60% of enterprise spending, indicating a moderate concentration in the natural language processing market. Hyperscalers leverage their distribution power through bundled credits and integrated MLOps. Meanwhile, open-source contenders like Meta’s Llama 3 and Mistral are narrowing accuracy gaps. This shift compels established players to prioritize latency, compliance, and domain ecosystems over mere parameter counts. Notable strategic maneuvers include Google’s latency reductions with Gemini Flash, Microsoft’s introduction of Azure AI Foundry for seamless model transitions, and NVIDIA’s H200 GPU debut, which boasts a doubled inference throughput.

Startups are finding their footing in areas like retrieval-augmented generation, synthetic data, and on-device compression. Cohere is making strides in enterprise RAG, boasting impressively low hallucination rates. Hugging Face has transformed its platform, now home to 500,000 developers, into a formidable community asset, rivaling even proprietary catalogs. A 35% year-on-year surge in patent filings underscores the escalating intellectual property skirmishes, particularly in areas like few-shot learning and bias mitigation. Regulations are being wielded as strategic tools; vendors with pre-certified high-risk modules are reaping first-mover benefits in the EU, a trend likely to echo in other regions adopting similar regulatory frameworks.

Additionally, partnerships and collaborations are shaping the competitive landscape. For instance, OpenAI’s collaboration with enterprise software providers is enabling tailored solutions for specific industries, while Amazon is integrating its NLP capabilities into AWS services to enhance accessibility for developers. These alliances are expected to drive innovation and expand the adoption of NLP technologies across diverse sectors during the forecast period.

Natural Language Processing Industry Leaders

Microsoft Corporation

SAS Institute Inc.

IBM Corporation

Google LLC (Alphabet)

NVIDIA Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft introduced Azure AI Foundry, a unified training-to-deployment suite that bundles access to OpenAI, Meta and Mistral models, letting clients switch engines without code rewrites.

- January 2026: Salesforce rolled out Agentforce 2.0, whose autonomous agents cut customer-service handle time by up to 40% in early deployments.

- December 2025: Google shipped Gemini 2.0 Flash, matching flagship multimodal accuracy while lowering response times by 40%.

- December 2025: OpenAI previewed o3, an 87.5% ARC-AGI scorer that handles multi-step reasoning for complex workflows.

Global Natural Language Processing Market Report Scope

Natural Language Processing (NLP) is a component of artificial intelligence (AI) that allows computers to assess and interpret both written and spoken human language.

The Natural Language Processing Market is Segmented by Deployment (On-premise and Cloud), Organization Size (Large Organizations and Small and Medium Organizations), Type (Hardware, Software, and Services), Processing Type (Text, Speech/Voice, and Image), End-user Industry (Education, BFSI, Healthcare, IT and Telecom, Retail, Manufacturing, Media, and Entertainment), and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle-East and Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Hardware |

| Software |

| Services |

| Text |

| Speech or Voice |

| Image or Vision |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Retail and E-Commerce |

| Manufacturing |

| Media and Entertainment |

| Education |

| Others End-User Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Deployment | On-Premise | ||

| Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Processing Type | Text | ||

| Speech or Voice | |||

| Image or Vision | |||

| By End-User Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Retail and E-Commerce | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Education | |||

| Others End-User Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is global spending on natural language processing solutions expanding?

Between 2026-2031, the natural language processing market grows at a 19.94% CAGR, lifting value from USD 47.37 billion to USD 117.57 billion.

Which region shows the strongest growth momentum?

Asia-Pacific posts a 22.13% CAGR as sovereign AI mandates in China, India’s public digital stack, and Japan’s healthcare digitization drive accelerated adoption.

Why are services outpacing software in future budgets?

Enterprises need integration, bias monitoring, and compliance audits, pushing services to a 22.62% CAGR and positioning them to overtake hardware spending by 2028.

What makes healthcare the fastest-growing end-use segment?

Ambient clinical intelligence, coding automation, and drug-discovery text mining cut paperwork by up to 50% and unlock capacity, propelling 24.84% CAGR growth.