Molded Interconnect Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

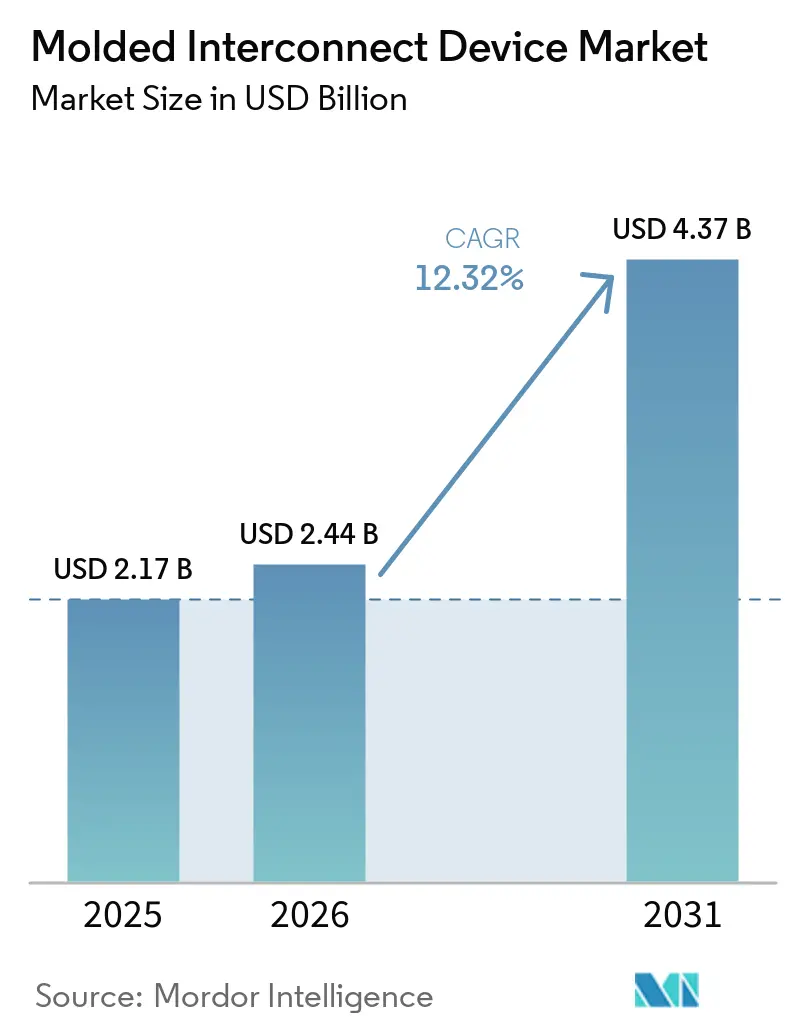

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 4.37 Billion |

| Growth Rate (2026 - 2031) | 12.32% CAGR |

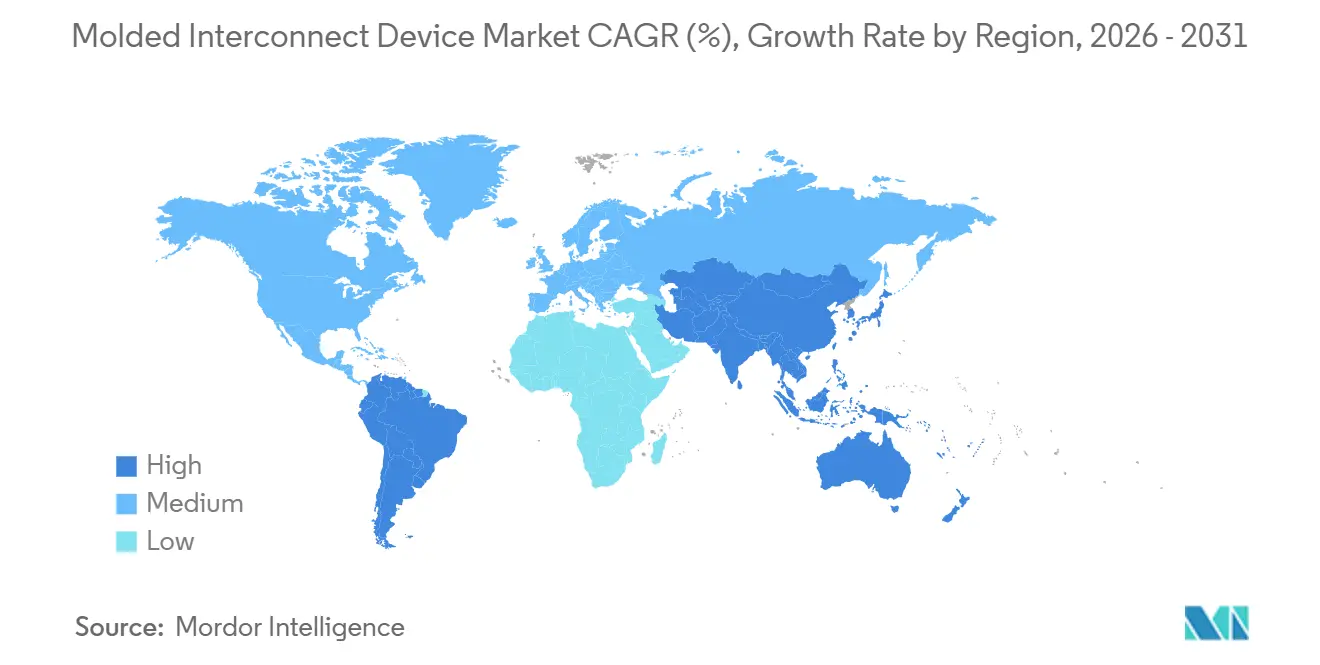

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Molded Interconnect Device Market Analysis by ���ϲ�����

The molded interconnect device market size is projected to expand from USD 2.17 billion in 2025 and USD 2.44 billion in 2026 to USD 4.37 billion by 2031, registering a CAGR of 12.32% between 2026 and 2031. Demand is rising as automotive OEMs convert bulky wiring harnesses into lightweight three-dimensional antenna modules, while smartphone makers compress multiple millimeter-wave arrays into ever-thinner housings. Growth is also propelled by premium-vehicle interiors that replace mechanical buttons with curved capacitive panels, hearing-aid miniaturization that favors liquid-crystal-polymer casings, and battery-electric-vehicle pack sensors that require 150 °C plastics able to match copper’s thermal expansion. Asia-Pacific remains the volume hub because of its printed-circuit-board base and smartphone final-assembly footprint, yet South America is accelerating nearshoring investments targeting compliance with the United States-Mexico-Canada Agreement. Meanwhile, high tooling costs and silver-price volatility temper adoption curves, although process innovation and vertical integration by leading connector suppliers continue to erode entry barriers.

Key Report Takeaways

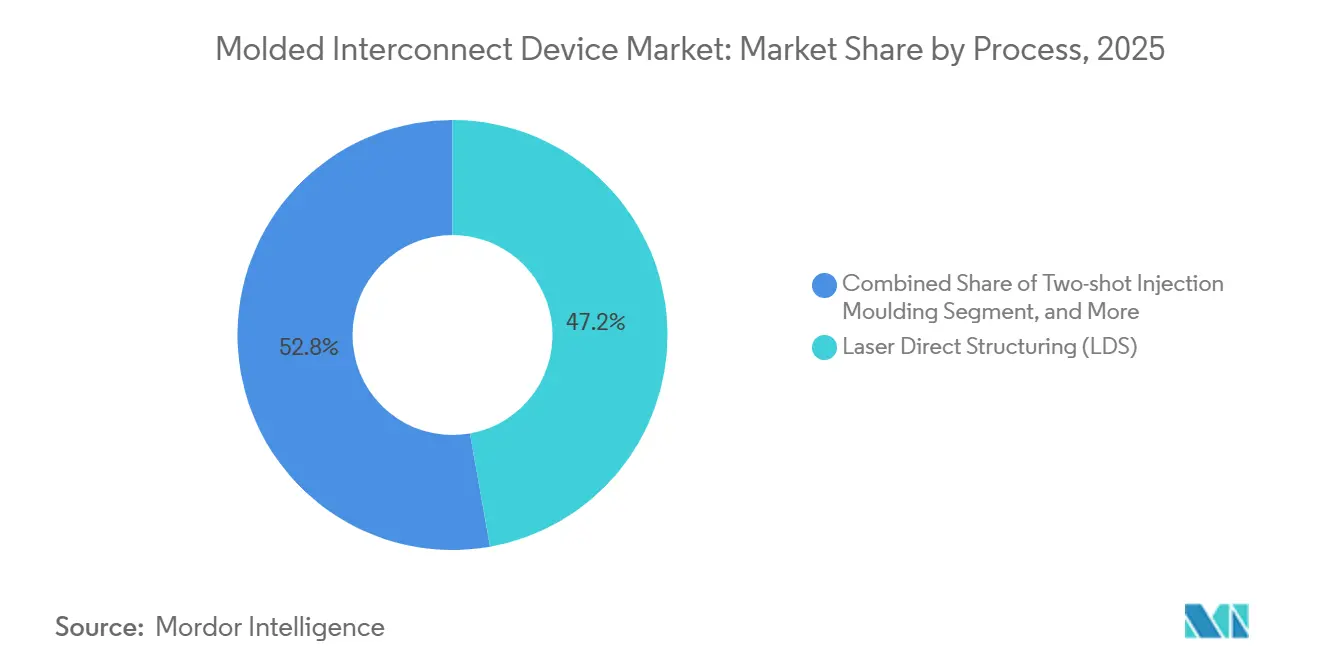

- By process, laser direct structuring led the molded interconnect device market with 47.21% revenue share in 2025, while additive and other emerging processes are forecast to grow at a 12.77% CAGR through 2031.

- By product type, antenna and connectivity modules accounted for 41.37% of the molded interconnect device market revenue share in 2025, whereas structural electronics panels are projected to expand at a 12.96% CAGR through 2031.

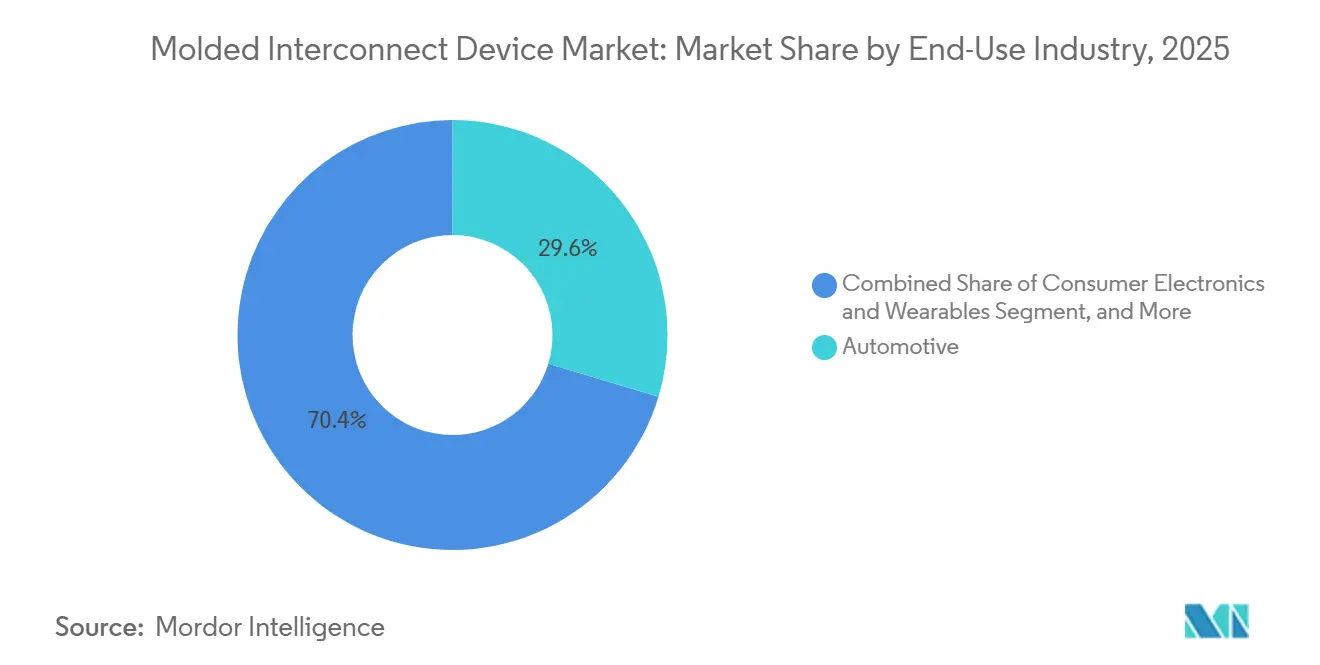

- By end-use industry, automotive applications controlled 29.63% of 2025 revenue in the molded interconnect device market, but healthcare and medical devices are expected to record the fastest growth at a 12.87% CAGR over 2026-2031.

- By material, liquid-crystal polymer held 33.47% of the 2025 revenue share in the molded interconnect device market, yet polyether ether ketone is anticipated to post a 12.84% CAGR as designers push continuous-use temperatures beyond 150 °C.

- By geography, Asia-Pacific accounted for 38.92% of 2025 revenue share in the molded interconnect device market, while South America is forecast to grow at a 13.06% CAGR as Mexican automotive suppliers add electrical component capacity.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Molded Interconnect Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive Shift to Zonal E/E Architecture Driving 3-D Antenna MID Demand | 2.80% | Global, early adoption in Germany, United States, China | Medium term (2–4 years) |

| Rapid Adoption of LDS Processing in 5G Smartphones | 2.40% | Asia-Pacific core, particularly China, South Korea, Taiwan | Short term (≤ 2 years) |

| Miniaturisation Requirements in Hearing Aids and Implantables | 1.90% | North America and Europe | Medium term (2–4 years) |

| EV-Battery Pack Sensors Needing 150 °C Plastics | 1.70% | Global EV hubs | Medium term (2–4 years) |

| Next-Gen Smart-Surface HMIs in Premium Vehicles | 1.50% | Europe and North America luxury segments, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Antenna-in-Package Integration for LEO Satellite User-Terminals | 1.30% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Automotive shift to zonal E/E architecture driving 3-D antenna MID demand

Automakers are consolidating dozens of electronic control units into regional gateways, cutting vehicle wiring mass up to 40 %. Three-dimensional molded interconnect devices integrate GPS, cellular, and vehicle-to-everything antennas onto a single liquid-crystal-polymer carrier, eliminating coax cables and improving electromagnetic isolation between bands. Zonal architectures also shorten harness lengths, allowing antenna modules to mount behind the roof liner where ambient temperatures reach 125 °C for 15 years, a condition matched by molded interconnect devices that combine mechanical and radio-frequency functions in one injection-molded part.[1]Bosch Mobility, “Zonal E/E Architecture White Paper,” bosch-mobility.com Continental, Volkswagen, and BMW programs now specify molded interconnect devices as standard, accelerating global pull-through.

Rapid adoption of LDS processing in 5 G smartphones

Smartphone OEMs increasingly employ laser direct structuring to place millimeter-wave antenna arrays on curved housings without rigid-flex or adhesive layers. A neodymium-doped laser activates copper-seed particles within liquid-crystal polymer, after which electroless plating forms lines with insertion loss below 0.5 dB/cm at 28 GHz.[2]LPKF Laser and Electronics, “Laser Direct Structuring Technology,” lpkf.com The method shaves USD 1.20-1.80 from the bill-of-materials and allows a single antenna to double as a structural rib, critical as flagship phones retail below USD 600 in India and Southeast Asia. China, South Korea, and Taiwan dominate short-term growth while Europe follows with foldable designs that need conformal radiators.

Miniaturization requirements in hearing aids and implantables

Cochlear implants must survive autoclave sterilization at 134 °C at 2.1 bar for 18 minutes. Molded interconnect devices fold stimulator, antenna, and battery contacts into one liquid-crystal-polymer shell, trimming assembly steps from 14 to 6 and reducing cycle time by 40 %.[3]Cochlear Limited, “Annual Report 2025,” cochlear.com United States FDA approval of firmware-upgradeable implants in 2025 further cements the technology, as wireless telemetry traces can now be routed along curved casings, keeping the profile below 4 mm for pediatric skull cavities.

EV-Battery Pack Sensors Needing 150 °C Plastics

Fast-charging 800-V battery packs expose voltage and temperature sense lines to 150 °C environments. Polyether ether ketone retains tensile strength above 90 MPa at that temperature and nearly matches copper’s coefficient of thermal expansion, cutting solder-joint fatigue.[4]Restraint (~) % Impact on CAGR Forecast Geographic Relevance Impact Timeline High Tooling Cost for Multi-Shot Moulds -1.80% Global, acute in North America and Europe Short term (≤ 2 years) Limited Global Capacity for LDS Polymer Compounds -1.50% Asia-Pacific and Europe polymer-compounding hubs Medium term (2–4 years) Silver Price Volatility Impacting Metallisation Chemistries -1.20% Global, pass-through pricing in Asia-Pacific contract manufacturing Short term (≤ 2 years) Reliability Gaps Above 180 °C for Aerospace Cabin Sensors -0.90% North America and Europe aerospace clusters Long term (≥ 4 years) Restraint (~) % Impact on CAGR Forecast Geographic Relevance Impact Timeline High Tooling Cost for Multi-Shot Moulds -1.80% Global, acute in North America and Europe Short term (≤ 2 years) Limited Global Capacity for LDS Polymer Compounds -1.50% Asia-Pacific and Europe polymer-compounding hubs Medium term (2–4 years) Silver Price Volatility Impacting Metallisation Chemistries -1.20% Global, pass-through pricing in Asia-Pacific contract manufacturing Short term (≤ 2 years) Reliability Gaps Above 180 °C for Aerospace Cabin Sensors -0.90% North America and Europe aerospace clusters Long term (≥ 4 years) Molded interconnect devices integrate voltage-sense foils, thermistors, and bus current shunts into snap-fit modules, eliminating hand-soldered harnesses that fail under vibration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Tooling Cost for Multi-Shot Moulds | -1.80% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Limited Global Capacity for LDS Polymer Compounds | -1.50% | Asia-Pacific and Europe polymer-compounding hubs | Medium term (2–4 years) |

| Silver Price Volatility Impacting Metallisation Chemistries | -1.20% | Global, pass-through pricing in Asia-Pacific contract manufacturing | Short term (≤ 2 years) |

| Reliability Gaps Above 180 °C for Aerospace Cabin Sensors | -0.90% | North America and Europe aerospace clusters | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Tooling Cost for Multi-Shot Moulds

Family molds with rotating cores and sequential gates cost USD 50,000-150,000 and require 6-12 weeks lead time. At volumes below 10,000 parts annually, amortization adds USD 4.00-6.00 per unit, rendering molded interconnect devices uncompetitive versus hand-assembled rigid-flex circuits in aerospace and specialty medical runs. Western labor rates, often USD 75-120 per hour for mold finishing, magnify near-term adoption hurdles.

Limited Global Capacity for LDS Polymer Compounds

Only a handful of lines operated by SABIC, Celanese, and Ticona compound copper-seeding additives into engineering resins. Batches are capped at 500-1,000 kg and must hold ±0.5 wt-% metal-oxide loading, extending supplier lead times to 16 weeks during smartphone and automotive ramps. Capacity additions require dedicated screw-barrel combinations to avoid cross-contamination, and resin buyers hesitate to sign long off-take commitments until high-volume proof emerges.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process: LDS Dominates as Additive Methods Emerge

Laser direct structuring commanded 47.21% of the 2025 revenue, underscoring its critical role in antenna miniaturization across smartphones and cars. This technology enables precise and efficient designs, meeting the growing demand for compact and high-performance devices. Two-shot molding fills niches requiring dissimilar resins and environmental sealing, offering versatility for various applications. Meanwhile, film-insert methods are gaining traction for decorative interior panels, particularly in the automotive and consumer electronics industries. Additive aerosol-jet and inkjet printing promise sub-10 µm lines without plating, presenting opportunities for intricate designs, although throughput currently lags behind mass-production benchmarks.

The molded interconnect device market continues to invest in LDS beam-steering and automated optical inspection upgrades, which have significantly improved first-pass yield to beyond 95%. These advancements enhance production efficiency and reduce waste. Meanwhile, additive approaches are increasingly attracting wearables and aerospace prototypes, where rapid iteration and customization outweigh unit cost concerns. As printhead speeds improve, these emerging technologies are expected to capture double-digit market share in molded interconnect devices by the late forecast window, reflecting their growing importance in the market.

By Product Type: Structural Panels Gain as Buttons Disappear

Antenna and connectivity modules generated 41.37% of the 2025 revenue, reflecting the high demand driven by mobile devices and telematics applications. Structural electronics panels, although currently a smaller segment, are projected to grow at a compound annual growth rate (CAGR) of 12.96%. This growth is fueled by the increasing adoption of capacitive smart surfaces, which are replacing traditional mechanical buttons, reducing wire counts, and enabling the development of curved console designs.

Lighting components are leveraging molded interconnect devices to integrate LED arrays, optics, and heat sinks into single polycarbonate carriers. This integration has significantly reduced assembly times by more than 50%, making it a preferred choice for manufacturers. Sensors and switches continue to hold a substantial market share, particularly in applications such as tire-pressure monitoring systems, inertial measurement units, and brushless motor commutation. Molded interconnect devices in these applications provide robust shielding for delicate electronics, protecting them from electromagnetic interference and moisture, thereby enhancing their reliability and lifespan.

By End-Use Industry: Healthcare Accelerates on Implantable Upgrades

Automotive accounted for 29.63% of 2025 revenue, driven by the increasing adoption of zonal gateways, electric-vehicle sensors, and vehicle-to-everything antennas. The automotive sector continues to leverage molded interconnect devices to enhance connectivity, reduce wiring complexity, and improve overall vehicle performance. Healthcare-device revenue is projected to grow at a compound annual growth rate (CAGR) of 12.87% through 2031, as advancements in medical technology drive the integration of telemetry coils and microbatteries into sterilizable polymer shells for devices such as cochlear implants and glucose monitors. This growth is further supported by the rising demand for compact, lightweight, and reliable medical devices.

Consumer electronics remain the dominant segment in terms of unit volumes; however, the sector faces increasing margin pressures as Chinese brands invest in backward integration of laser direct structuring (LDS) lines to reduce costs and enhance production efficiency. In industrial automation, molded interconnect devices are increasingly utilized for torque-sensor and encoder modules, which simplify robot-joint wiring and improve operational efficiency. Additionally, the telecom infrastructure sector is adopting molded interconnect devices to ruggedize small-cell radios, ensuring durability and reliability for outdoor deployments that are expected to last up to 20 years. This trend is driven by the growing need for robust and efficient communication networks to support expanding 5G infrastructure.

By Material: PEEK Gains on Thermal Stability

Liquid-crystal polymer led with 33.47% 2025 revenue because its 280 °C heat-deflection point and low 3.2 dielectric constant enable millimeter-wave antennas. This material is increasingly used in high-frequency applications, including 5G infrastructure and advanced driver-assistance systems (ADAS), due to its superior thermal and electrical properties. Polyether ether ketone will outpace at a 12.84% CAGR, favored for 150 °C battery-pack sensors and downhole tools needing hydrolysis and hot-glycol resistance. Its high mechanical strength and chemical resistance make it a preferred choice for demanding environments, particularly in the oil and gas sector.

Polybutylene terephthalate serves cost-sensitive switch housings below 120 °C, offering a balance of affordability and performance for applications in consumer electronics and automotive interiors. Polyamide 6T/6 balances mechanical strength with laser sensitivity, making it suitable for laser direct structuring (LDS) processes in complex 3D designs. Polycarbonate blends dominate smartphone back covers and decorative in-mold films despite their 115 °C temperature ceiling, suggesting ongoing material mix diversification as designs split between consumer and high-temperature automotive needs. These blends are also gaining traction in wearables and other portable devices due to their lightweight and aesthetic appeal.

Geography Analysis

Asia-Pacific accounted for 38.92% of 2025 revenue, driven by China’s USD 27.95 billion printed-circuit-board base and its dense network of smartphone assemblers. Japan contributed USD 11.53 billion in 2024 board revenue, with flexible substrates at 51.3%, and companies such as Ibiden applying molded interconnect devices in radar modules. South Korea followed with USD 7.86 billion in 2024 board output as Samsung Electro-Mechanics expanded its multi-layer HDI lines.

South America is the fastest-growing region, projected to grow at a 13.06% CAGR, thanks to Mexico’s USD 766.45 million fourth-quarter 2025 investment in electrical-component plants that meet USMCA local-content mandates. Suppliers face a USD 2.5 billion retooling bill to upgrade from combustion-engine parts to electric-vehicle electronics, nudging regional uptake of LDS and two-shot molding cells.

North America and Europe each controlled roughly one-fifth of 2025 revenue, anchored by medical-device contract manufacturing and aerospace sensor modules that require ISO 13485 and AS9100 certification. Germany’s labor-intensive mold finishing pushes tooling 40-50 % above Asia, yet functional-safety standards accelerate internal LDS line additions. The Middle East and Africa remain nascent, gravitating toward telecom and downhole sensors where long service life offsets higher polymer costs.

Competitive Landscape

The molded interconnect device market features moderate concentration, with the five largest suppliers holding about 35%-40% combined revenue. TE Connectivity leverages its USD 8.8 billion automotive business to cross-sell three-dimensional antenna modules alongside conventional connectors. Molex adds fiber-optic termini to liquid-crystal-polymer housings, chasing 25 Gb/s automotive camera links. LPKF supplies LDS lasers and increasingly prototyping tools priced below USD 165,000 (EUR 150,000, USD 165,000) to expand the addressable customer base.

Phillips-Medisize and Cicor Group anchor the medical-device and aerospace niches, offering ISO 13485 and AS9100 programs plus design-for-manufacturability services that OEMs struggle to replicate in-house. Regional specialists in China, Mexico, and Finland exploit lower tooling and labor costs to secure mid-volume automotive interior panels. Emerging disruptors such as Optomec advance aerosol-jet printing that removes electroless-plating chemistry, while patent activity at LPKF and others points to hybrid laser-sintering and inkjet dielectric stacking that could shorten cycle times 40 %.

Industry bodies such as IPC are drafting IPC-2291 to harmonize design rules on coating adhesion and via reliability, a move expected to lower qualification costs and encourage dual sourcing. As standards mature, tier-one connector makers may accelerate vertical integration, but high mold-cost barriers still shield smaller regional vendors serving localized programs.

Molded Interconnect Device Industry Leaders

Molex LLC

TE Connectivity Ltd.

HARTING Technology Group

LPKF Laser & Electronics SE

TactoTek Oy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: TG0 demonstrated a capacitive-touch technology at CES 2026 that converts conductive polymers, metal, and glass into pressure-sensitive automotive surfaces, cutting bill-of-materials cost about 30% compared with film-insert molding.

- October 2025: TE Connectivity expanded its Shanghai facility, adding eight LDS production cells and boosting annual capacity for three-dimensional antenna modules by 6 million units.

- August 2025: Molex introduced a Polymicro fiber-optic interconnect system that integrates molded interconnect device housings with multi-mode termini for 25 Gb/s Ethernet links.

- June 2025: LPKF launched the ProtoLaser S4 benchtop LDS platform priced at EUR 150,000 (USD 165,000), enabling SMEs to prototype molded parts in three days.

Global Molded Interconnect Device Market Report Scope

The Molded Interconnect Device Market Report is Segmented by Process (Laser Direct Structuring, Two-Shot Injection Moulding, Two-Component Selective Metallisation, Film-Insert In-Mould Electronics, Additive and Other Emerging Processes), Product Type (Antenna and Connectivity Modules, Sensors and Switches, Lighting Components, Structural Electronics Panels, Other), End-Use Industry (Automotive, Consumer Electronics and Wearables, Healthcare and Medical Devices, Industrial Automation, Telecommunications Infrastructure, Aerospace and Defence, Other), Material (Liquid-Crystal Polymer, Polybutylene Terephthalate, Polyamide, Polycarbonate and Blends, Polyether Ether Ketone, Other), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Laser Direct Structuring (LDS) |

| Two-Shot Injection Moulding |

| Two-Component (2K) Selective Metallisation |

| Film-Insert, In-Mould Electronics |

| Additive and Other Emerging Processes |

| Antenna and Connectivity Modules |

| Sensors and Switches |

| Lighting Components |

| Structural Electronics Panels |

| Other Product Type |

| Automotive |

| Consumer Electronics and Wearables |

| Healthcare and Medical Devices |

| Industrial Automation |

| Telecommunications Infrastructure |

| Aerospace and Defence |

| Other End-Use Industry |

| Liquid-Crystal Polymer (LCP) |

| Polybutylene Terephthalate (PBT) |

| Polyamide (PA 6/6T) |

| Polycarbonate (PC) and Blends |

| Polyether Ether Ketone (PEEK) |

| Other Material |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Process | Laser Direct Structuring (LDS) | |

| Two-Shot Injection Moulding | ||

| Two-Component (2K) Selective Metallisation | ||

| Film-Insert, In-Mould Electronics | ||

| Additive and Other Emerging Processes | ||

| By Product Type | Antenna and Connectivity Modules | |

| Sensors and Switches | ||

| Lighting Components | ||

| Structural Electronics Panels | ||

| Other Product Type | ||

| By End-Use Industry | Automotive | |

| Consumer Electronics and Wearables | ||

| Healthcare and Medical Devices | ||

| Industrial Automation | ||

| Telecommunications Infrastructure | ||

| Aerospace and Defence | ||

| Other End-Use Industry | ||

| By Material | Liquid-Crystal Polymer (LCP) | |

| Polybutylene Terephthalate (PBT) | ||

| Polyamide (PA 6/6T) | ||

| Polycarbonate (PC) and Blends | ||

| Polyether Ether Ketone (PEEK) | ||

| Other Material | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the molded interconnect device market expected to grow through 2031?

It is projected to register a 12.32% CAGR from 2026 to 2031, rising to USD 4.37 billion by the end of the forecast period.

Which process currently holds the largest molded interconnect device market share?

Laser direct structuring led in 2025 with 47.21% revenue share.

What is driving adoption of molded interconnect devices in electric vehicles?

Battery-pack sensors need 150 °C plastics and compact three-dimensional circuitry, requirements met by polyether ether ketone molded interconnect devices.

Which region is the fastest-growing consumer of molded interconnect devices?

South America, led by Mexicos nearshoring surge, is forecast to grow at a 13.06% CAGR through 2031.

Why are structural electronics panels gaining traction in premium vehicles?

They replace mechanical buttons with curved capacitive surfaces, lowering assembly complexity and enabling over-the-air feature activation, driving a 12.96% CAGR for the segment.

What material is expected to outpace liquid-crystal polymer in high-temperature applications?

Polyether ether ketone is forecast to grow at a 12.84% CAGR due to its superior strength retention at 150 °C and compatibility with electric-vehicle battery-pack sensors.

Page last updated on: