Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

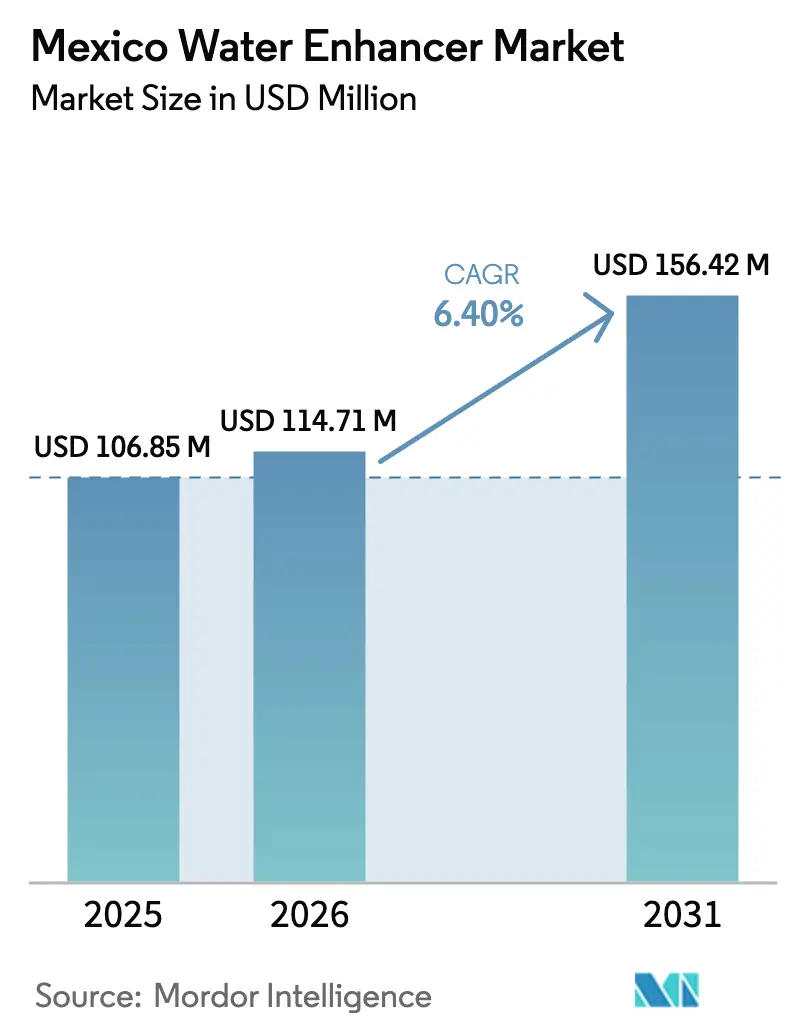

| Base Year Market Size (2025) | USD 106.85 Million |

| Market Size (2026) | USD 114.71 Million |

| Market Size (2031) | USD 156.42 Million |

| Growth Rate (2026 - 2031) | 6.40% CAGR |

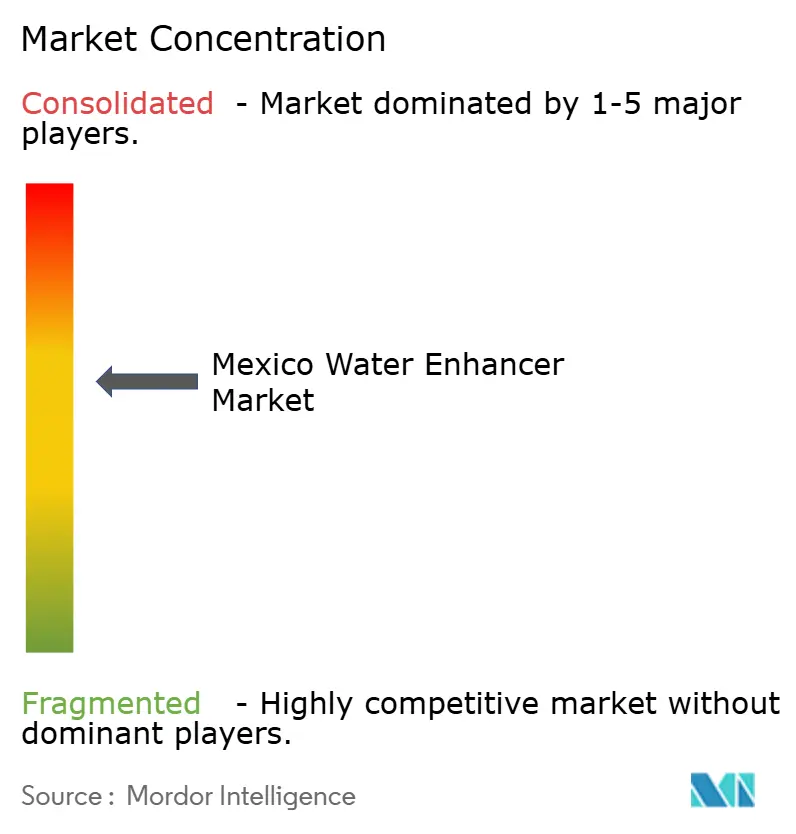

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Mexico Water Enhancer Market Analysis by ���ϲ�����

The Mexico Water Enhancer Market size is projected to be USD 106.85 million in 2025, USD 114.71 million in 2026, and reach USD 156.42 million by 2031, growing at a CAGR of 6.40% from 2026 to 2031. In key cities such as Mexico City, Guadalajara, and Monterrey, beverage purchasing habits are evolving due to factors like rising sugar taxes, the NOM-051 front-of-pack warning stamps, and an increasing urban preference for low-calorie hydration. Multinational beverage companies are responding by reformulating traditional soft drinks into zero-calorie versions. This shift not only promotes low-sugar options but also strengthens the Mexican water enhancer market, particularly in modern retail and e-commerce channels. As consumers prioritize functional benefits such as electrolytes, vitamins, and caffeine, concentrates are differentiating themselves from standard bottled water. Additionally, the use of natural sweeteners is helping products avoid warning labels and IEPS taxes. While competition in the market remains moderate, global players are capitalizing on their scale and distribution strengths, while local innovators are focusing on unique herbal flavors and direct-to-consumer strategies.

Key Report Takeaways

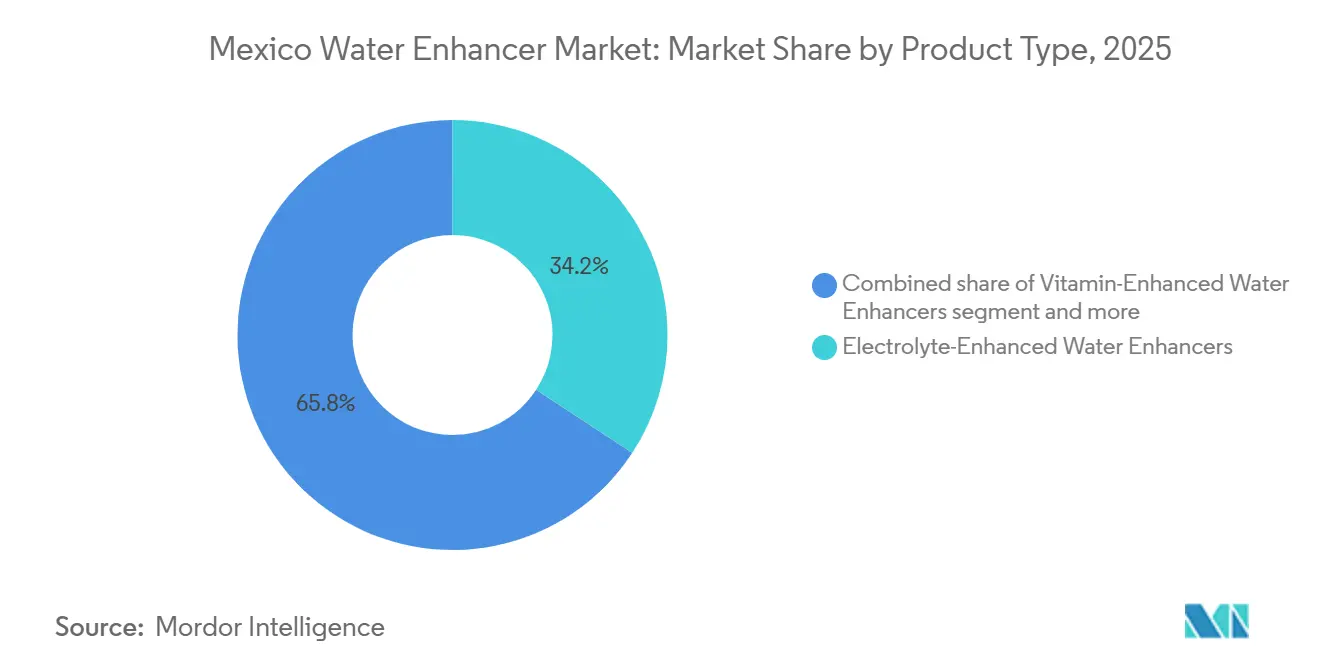

- By product type, Electrolyte-Enhanced formats captured 34.23% of Mexico water enhancer market share in 2025, and Herbal and Fruit Flavored variants are poised to grow at a 6.89% CAGR through 2031.

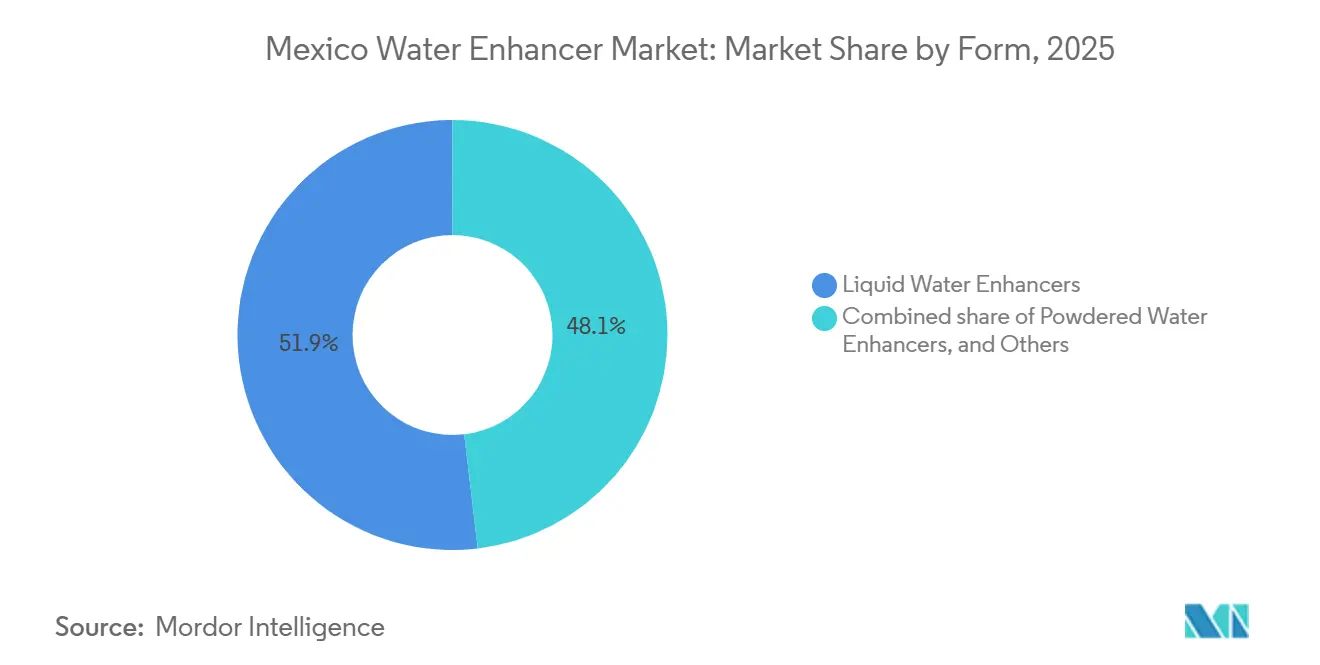

- By form, Liquid water enhancers led with 51.87% revenue share in 2025, while Powdered water enhancers are forecast to advance at a 7.12% CAGR to 2031.

- By distribution channel, Supermarkets and hypermarkets held 56.98% share of the Mexico water enhancer market size in 2025, and Online retail stores are set to register a 7.06% CAGR between 2026-2031.

- By geography, metropolitan Mexico City dominated with more than one-third of 2025 sales and is projected to retain leadership given modern retail penetration that exceeds 60%.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Water Enhancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and wellness focus among Mexican consumers | +1.2% | National, concentrated in Mexico City, Guadalajara, Monterrey metropolitan areas | Medium term (2-4 years) |

| Strong adoption of functional beverages supports the market | +1.0% | National, with early gains in urban centers and modern retail channels | Medium term (2-4 years) |

| Rising preference for natural ingredients | +0.9% | National, strongest in high-income urban segments | Medium term (2-4 years) |

| Hiking/outdoor recreation culture boosting lightweight hydration needs | +0.6% | Regional, concentrated in central highlands and northern states | Long term (≥ 4 years) |

| Sugar-sweetened beverage tax shifting demand to enhancers | +1.5% | National, immediate impact in modern retail and e-commerce | Short term (≤ 2 years) |

| Flavor innovation broadens appeal | +0.8% | National, with rapid adoption in convenience and online channels | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising health and wellness focus among Mexican consumers

In Mexico, a staggering three out of four adults grapple with being classified as overweight or obese, and diabetes cases are on the rise. In 2024, the International Diabetes Federation reported a 16.4% prevalence of diabetes among Mexican adults[1]Source: International Diabetes Federation, "Mexico", idf.org. This alarming health scenario has spurred the Mexican government to advocate for dietary reforms, inadvertently boosting the water enhancers market. The Secretaría de Salud's 2025 Dietary Guidelines not only champion plain water over sugary drinks but also promote functional hydration products enriched with electrolytes and vitamins for the active populace. Such an official nod elevates water enhancers to a health-positive status, especially those crafted with natural sweeteners like stevia or monk fruit, steering clear of the NOM-051 warning labels. The alignment of public health campaigns, regulatory nudges, and a growing consumer appetite for functional hydration signals a robust, enduring trend in consumption patterns, transcending mere cyclical health fads.

Strong adoption of functional beverages supports the market

In Mexico, the functional beverage market is primarily driven by sports drinks, energy drinks, and fortified waters. Within this market, water enhancers hold a significant position by enabling consumers to personalize their hydration needs. These enhancers allow users to add specific functional benefits, such as electrolytes for recovery after physical activity, caffeine to enhance cognitive performance, or vitamins to strengthen immune health, all at a lower cost compared to ready-to-drink functional beverages. The proposed extension of the IEPS tax to oral rehydration salts and electrolyte drinks, if implemented, could remove the current price advantage enjoyed by products like Electrolit and Pedialyte. This change would likely push cost-conscious consumers toward untaxed water enhancers, which provide similar electrolyte benefits. Consequently, this regulatory shift highlights water enhancers as a more affordable and tax-efficient alternative to traditional functional beverages, further solidifying their role in the market.

Rising preference for natural ingredients

Mexican consumers are paying closer attention to ingredient lists. In the U.S., the absence of artificial sweeteners is highly valued by consumers, a preference reinforced by NOM-051's mandatory warnings on products containing such ingredients. This growing awareness has driven a shift in formulations toward natural alternatives like stevia, monk fruit, and allulose. Suppliers such as Cargill and ADM have introduced proprietary blends, including EverSweet and SweetRight Stevia Edgility, which address stevia's bitter aftertaste and improve solubility in concentrated liquid formats. PepsiCo's Gatorade Hydration Booster, launched in September 2024, highlights this trend. The powder features electrolytes derived from watermelon juice and sea salt, delivers 100% of the daily value for vitamins A, B3, B5, B6, and C, and excludes artificial flavors, sweeteners, and added colors. The alignment between natural ingredient preferences and COFEPRIS approvals creates a supportive environment for clean-label water enhancers, particularly those targeting health-conscious consumers willing to pay a premium for transparency.

Hiking and outdoor recreation culture boosting lightweight hydration needs

As domestic tourism rebounds, Mexico's national parks and protected areas—overseen by CONANP (Comisión Nacional de Áreas Naturales Protegidas), are witnessing a surge in visitors. Urban millennials and Gen Z, drawn to experiential wellness, are increasingly embracing hiking and outdoor activities. Water enhancers resonate with the outdoor ethos: a mere 10-gram sachet or 50-milliliter liquid concentrate can substitute a bulky 500-milliliter ready-to-drink bottle, lightening the load and curbing plastic waste. Bolstered by a strong tourism infrastructure, Mexico is experiencing a boom in hiking and adventure pursuits. In 2024, Mexico's Ministry of Tourism highlighted a significant arrival of 45.05 million international tourists[2]Source: Ministry of Tourism (Mexico), "International Traveler Surveys (EVI)", datatur.sectur.gob.mx. Meanwhile, Coca-Cola's patented fast-hydration electrolyte formulations, designed for swift sodium-glucose co-transport and rapid fluid uptake, spotlight the advanced technology now integral to portable hydration. This innovation is pivotal; outdoor enthusiasts value hydration efficacy, emphasizing absorption speed, electrolyte balance, and sustained energy, over mere flavor. With the rise of outdoor activities, heightened sustainability awareness, and advancements in hydration science, water enhancers are evolving beyond urban trends, becoming integral to lifestyle and identity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety concerns over artificial sweeteners and additives | -0.8% | National, amplified by NOM-051 labeling and social media discourse | Short term (≤ 2 years) |

| Limited consumer awareness in non-urban regions | -1.0% | Regional, concentrated in rural and peri-urban areas with traditional retail dominance | Long term (≥ 4 years) |

| Competition from traditional beverages | -0.7% | National, strongest in traditional retail and lower-income segments | Medium term (2-4 years) |

| Regulatory uncertainty for novel functional ingredients | -0.5% | National, affecting product launches and import approvals | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Safety concerns over artificial sweeteners and additives

Health-conscious parents and wellness-oriented consumers have developed skepticism toward artificial sweeteners due to NOM-051's front-of-pack warning: "Contains sweeteners, not recommended for children". This labeling requirement, applicable to all sweeteners, from natural options like stevia to synthetic ones such as sucralose and acesulfame-K, has caused consumer confusion and reduced trials, particularly in households with children. COFEPRIS's increased oversight of dietary supplements, including on-site inspections and advertising monitoring, has raised compliance costs and delayed the market entry of new formulations. Manufacturers must verify that every additive is included on COFEPRIS's approved list; those not listed must navigate alternative regulatory pathways or reformulate their products. For water enhancer brands, this results in prolonged product development cycles, higher regulatory costs, and the risk of rejection or delays for new sweeteners or functional ingredients, threatening launch timelines and market competitiveness.

Limited consumer awareness in non-urban regions

Traditional retail formats, such as tiendas de abarrotes and mercados, dominate food and beverage sales in Mexico, particularly in rural and peri-urban areas. Water enhancers face challenges in these markets as they require consumer education on dosage, benefits, and usage occasions, which traditional retail formats are not equipped to provide. Additionally, cultural preferences for aguas frescas (fresh fruit waters) and refrescos (soft drinks) are deeply ingrained in non-urban regions, where water enhancers are often seen as unfamiliar or unnecessary. E-commerce has the potential to address this awareness gap through targeted digital marketing and subscription models, but its reach is largely limited to urban areas. Rural regions face infrastructure barriers, such as limited payment options and delivery logistics. Furthermore, brand growth is concentrated in metropolitan areas like Mexico City, Guadalajara, and Monterrey. This concentration restricts the addressable market and intensifies competition in urban channels, where brands compete for shelf space and invest heavily in promotional activities.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electrolyte Dominance Meets Botanical Disruption

In 2025, Electrolyte-Enhanced formats accounted for 34.23% of Mexico's water enhancer market, highlighting their connection to the country's sports-drink trend and increasing gym culture. Meanwhile, herb- and fruit-flavored enhancers, particularly those featuring hibiscus, tamarind, and guava extracts, are expected to lead the market with a strong 6.89% CAGR. COFEPRIS’ approval of plant-based additives enables manufacturers to maintain cleaner labels and avoid warning stamps. Suppliers, such as Cargill, now provide stevia blends that resolve solubility challenges, achieving taste parity with traditional sugar-sweetened beverages. Additionally, millennials are attracted to premium narratives focused on botanical origins, supporting higher price points.

Demand for Vitamin-Enhanced and Caffeine-Infused variants continues to grow, driven by the popularity of functional beverages. Vitamin products meet recommended supplement intakes and emphasize immune health, while caffeine extracts compete with energy drinks while adhering to COFEPRIS regulations. The category's growth aligns with trends such as sugar tax increases, sports nutrition crossovers, and innovations like Coca-Cola’s patented sodium-glucose co-transport method, which enhances hydration speed. This diversification in product types not only protects brands from reliance on a single use-case but also expands their audience reach.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Liquid Convenience Versus Powder Economics

In 2025, liquid concentrates emerged as the leading segment in the market, contributing 51.87% of the total revenue. This dominance is primarily driven by the convenience offered by squeeze-bottle portability, which allows easy usage and the advantage of instant dissolution, making them highly user-friendly. Additionally, high sales volumes are supported by impulse purchases at convenience stores and the growing trend of same-day online orders, which cater to consumer demand for quick and accessible options. On the other hand, powders are projected to grow at a compound annual growth rate (CAGR) of 7.12%, owing to their cost-effectiveness and shipping efficiency. These attributes make powders particularly attractive to family households, where affordability and practicality are key considerations. Furthermore, the recent authorization of polyacrylic acid has enabled the development of smoother textures in powders, enhancing their appeal and positioning them as strong competitors to liquid concentrates. A notable example of this trend is Gatorade's Hydration Booster, which highlights a strategic shift among major players to tap into the growth potential of the powder segment.

Tablet and effervescent formats, while still niche, are gaining traction in specific use cases such as outdoor recreation, where factors like lightweight portability and extended shelf life are critical. Technological advancements, such as Coca-Cola's fast-hydration electrolyte complex, indicate the possibility of innovation within this segment. This technology could potentially be adapted to dissolvable tablets, thereby revitalizing the product pipeline and expanding the subcategory's appeal. As the Mexico water enhancer market continues to evolve, the choice of product form is expected to increasingly align with specific occasions, distribution channels, and pricing strategies, reflecting the diverse needs and preferences of consumers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Modern Retail Meets Digital Disruption

In 2025, supermarkets and hypermarkets accounted for a significant 56.98% market share, driven by promotions from Walmart, Soriana, and Chedraui that bundled enhancers with bottled water. Shelf space is increasingly competitive as zero-calorie sodas and functional ready-to-drink (RTD) beverages target the same consumer base. However, eye-level placements and in-store demonstrations continue to encourage product trials. Convenience stores like OXXO capitalize on their extensive 21,970-unit network to cater to on-the-go consumption. At the same time, pharmacies market enhancers as wellness products, displaying them alongside supplements.

Online retail is the fastest-growing channel, with a projected 7.06% CAGR through 2031. This growth is supported by rising mobile adoption and increasing internet penetration. According to INEGI's 2024 data, 95.5% of cellphone users in Mexico own smartphones, and 60.8% use these devices to access the internet[3]Source: INEGI, "Instituto Federal de Telecomunicaciones (IFT)", inegi.org. Digital storefronts enable features like auto-replenishment and direct brand storytelling, eliminating the need for slotting fees. Kraft Heinz’s recent launch on AB InBev’s BEES platform highlights how brands can digitally connect with one million mom-and-pop stores. Additionally, diverse payment options, particularly OXXO Pay, are driving order growth among cash-preferencing consumers. Other channels, such as gyms, corporate cafeterias, and vending machines, provide situational opportunities but remain fragmented.

Geography Analysis

Mexico is the exclusive focus of this market, showcasing a dual opportunity landscape within its borders. Major metropolitan areas, Mexico City, Guadalajara, and Monterrey, contribute the majority of market value. This is driven by higher disposable incomes, increased health awareness, and the presence of modern retail. These urban centers also serve as innovation hubs, where new flavors and formats are tested before nationwide launches. Additionally, the urban concentration of e-commerce infrastructure, offering same-day and next-day deliveries, enhances both trial and repeat purchases. This trend is particularly evident among millennials and Gen Z, who prioritize convenience and digital engagement.

In comparison, peri-urban and rural areas present a different picture: traditional retail dominates, awareness of water enhancers is low, and cultural preferences for aguas frescas and refrescos limit category growth. However, these regions represent the largest untapped potential. With dense populations and growing smartphone penetration, conditions are favorable for mobile-commerce-driven market entry. Therefore, the geographic opportunity is less about regional differences and more about strategic channel approaches: urban growth will be fueled by modern retail and e-commerce, while rural penetration will require partnerships with traditional retailers, mobile-commerce platforms, and community-based distribution models.

Mexico's regulatory framework, governed by COFEPRIS and NOM-051, applies uniformly across the country, simplifying compliance for market entrants. However, this also means that regulatory changes, such as tax increases or labeling mandates, impact all regions simultaneously. This regulatory consistency contrasts with the fragmented retail and consumer awareness landscape. As a result, brands should adopt a dual strategy: standardizing product formulations and labeling to achieve economies of scale, while tailoring marketing and distribution strategies to address regional consumption patterns and channel preferences.

Competitive Landscape

The Mexico Water Enhancer Market is moderately fragmented, with multinational beverage companies leveraging extensive bottling networks, strong brand equity, and reformulation agility to dominate mainstream segments. Meanwhile, niche players are focusing on premium and specialty markets through direct-to-consumer channels, pharmacy placements, and subscription models. Coca-Cola's patented fast-hydration electrolyte formulation, which optimizes sodium-glucose co-transport for rapid fluid absorption, highlights how established players are incorporating technical advancements into hydration products to protect margins and support premium pricing.

Strategic approaches are centered on three key areas: reformulating products to avoid NOM-051 warning labels and IEPS taxes, innovating flavors to drive consumer trials and premiumization, and utilizing omnichannel distribution to capture both impulse purchases at convenience stores and planned replenishment through e-commerce subscriptions. Opportunities remain in functional hydration tailored to specific needs, such as post-workout recovery, cognitive performance, and immune support, as well as in sustainable packaging formats like refillable concentrates and compostable sachets that appeal to environmentally conscious consumers.

Emerging disruptors include local Mexican brands that capitalize on cultural authenticity by incorporating regional botanicals and traditional flavors. These brands use direct-to-consumer models to bypass the slotting fees and promotional expenses associated with modern retail distribution. PepsiCo's partnership with GEPP demonstrates the role of technology in gaining market share, as their nationwide reformulation spans all package types and sales channels—a supply-chain and manufacturing achievement that smaller competitors struggle to replicate. COFEPRIS's regulatory framework, which includes on-site inspections, adverse-effect monitoring, and advertising oversight, imposes compliance costs that favor established players with dedicated regulatory teams. However, it also creates opportunities for brands that prioritize transparency and proactive engagement with regulators. As a result, the competitive landscape is defined by incumbents leveraging scale and distribution advantages, while niche players focus on functional innovation, clean-label positioning, and digital-first business models to capture high-value segments.

Mexico Water Enhancer Industry Leaders

-

Kraft Heinz Company

-

Nestle SA

-

The Coca-Cola Company

-

PepsiCo Inc.

-

Wisdom Natural Brands

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: The Mexican Coca-Cola Industry (IMCC) has announced a USD 85 million investment to expand its Jugos del Valle–Santa Clara plant in Lagos de Moreno, Jalisco. This initiative will add two new production lines for non-carbonated beverages, juices, and nectars, increasing production capacity and strengthening national distribution from a strategically located facility.

- April 2025: Arca Continental and Coca-Cola have invested MXN 56.5 million to expand a PET bottle collection facility in San Luis Potos, aiming to enhance recycling efforts. This investment highlights Coca-Cola Mexico's commitment to a sustainable business model.

- January 2025: Nestlé is invested USD 1 billion to expand its production operations in Mexico. This investment focuses on increasing the capacity of plants in Veracruz, Guanajuato, Querétaro, and the State of Mexico. The company is also constructing a distribution center to strengthen its Mexican operations as a key "export hub."

- December 2024: Ocean Spray has collaborated with Dyla Brands to launch convenient on-the-go drink mixes. This partnership represents a significant step in introducing popular and delicious flavors to the powdered beverage mix market.

Mexico Water Enhancer Market Report Scope

Water enhancers, which come in concentrated liquid, powder, or tablet form, are used to enhance the taste, color, or nutritional value of plain water. The Mexican water enhancer market is segmented by product type, form, and distribution channels. By product type, the market is segmented into vitamin-enhanced, electrolyte-enhanced, caffeine-infused, herbal, and fruit-flavored. By form, the market is segmented into liquid, powdered, and others. By distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, pharmacy and drug stores, online retail, and others. For each segment, market forecasts are provided in terms of value (USD) and volume (tons).

Product Type

| Vitamin-Enhanced Water Enhancers |

| Electrolyte-Enhanced Water Enhancers |

| Caffeine-Infused Water Enhancers |

| Herbal and Fruit Flavored Water Enhancers |

By Form

| Liquid Water Enhancers |

| Powdered Water Enhancers |

| Others |

Distribution Channels

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Pharmacy and Drug Store |

| Online Retail Stores |

| Other Distribution Channels |

| Product Type | Vitamin-Enhanced Water Enhancers |

| Electrolyte-Enhanced Water Enhancers | |

| Caffeine-Infused Water Enhancers | |

| Herbal and Fruit Flavored Water Enhancers | |

| By Form | Liquid Water Enhancers |

| Powdered Water Enhancers | |

| Others | |

| Distribution Channels | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Pharmacy and Drug Store | |

| Online Retail Stores | |

| Other Distribution Channels |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What value will the Mexico water enhancer market reach by 2031?

It is forecast to reach USD 156.42 million by 2031.

How fast is the Mexico water enhancer market growing?

The market is registering a 6.40% CAGR over 2026-2031.

Which product type holds the largest share?

Electrolyte-Enhanced formats led with 34.23% market share in 2025.

Which distribution channel is expanding the quickest?

Online retail stores are projected to grow at a 7.06% CAGR through 2031.