Mexico Telecom Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

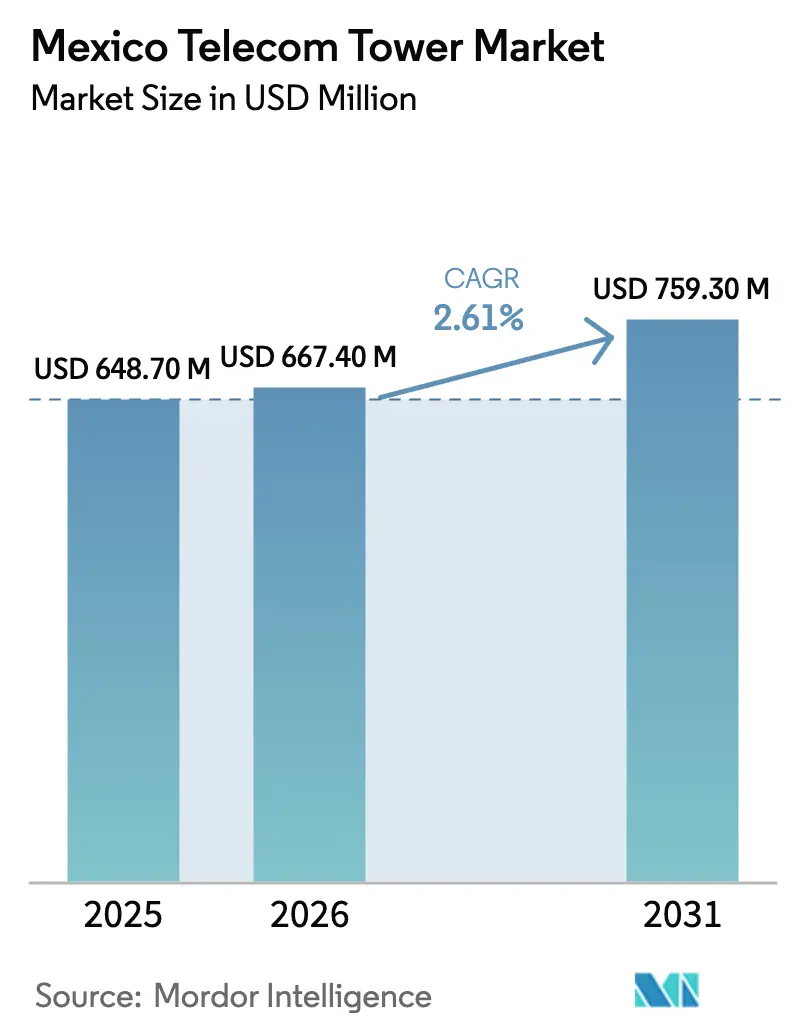

| Base Year Market Size (2025) | USD 648.70 Million |

| Market Size (2026) | USD 667.40 Million |

| Market Size (2031) | USD 759.30 Million |

| Growth Rate (2026 - 2031) | 2.61% CAGR |

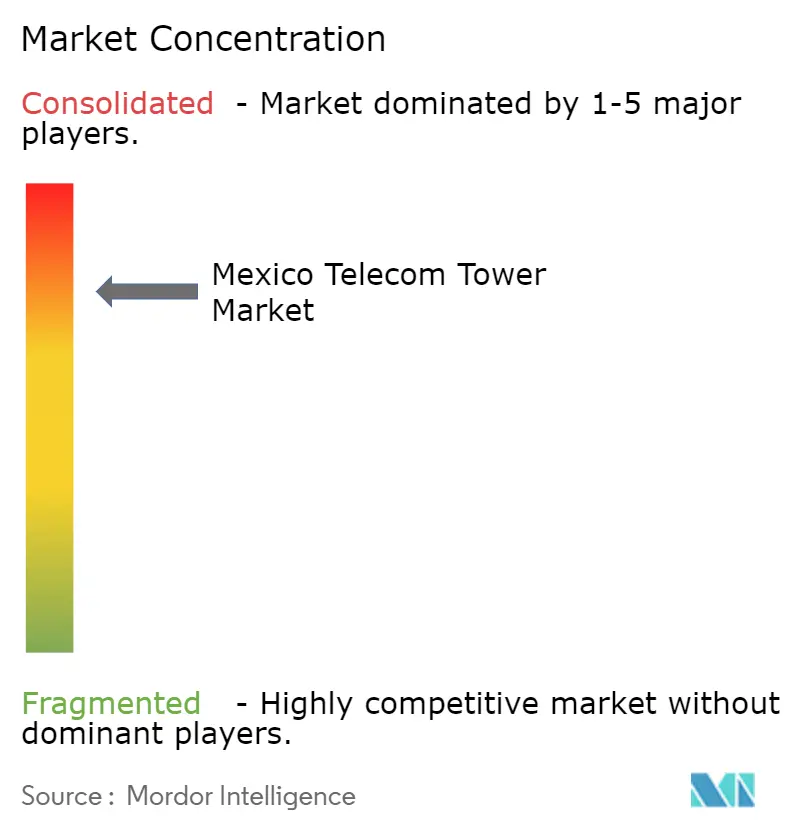

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Mexico Telecom Tower Market Analysis by ���ϲ�����

The Mexico telecom tower market size is projected to expand from USD 648.7 million in 2025 and USD 667.4 million in 2026 to USD 759.3 million by 2031, registering a 2.61% CAGR between 2026 to 2031. Rapid mobile-data traffic growth is forcing operators to densify urban coverage even as regulatory upheaval clouds investment timelines. State-backed CFE Telecom continues to build low-cost macro sites along utility rights-of-way, pressuring private lessors to shift toward premium rooftop and stealth structures in historic districts. Independent tower companies are responding with energy-as-a-service offerings, rooftop portfolios and edge-computing nodes to preserve yields as power costs rise and average tenancy ratios hover near 1.3. Exchange-rate volatility and delayed 5G spectrum auctions are tempering near-term build plans, yet long-run fundamentals remain anchored in streaming demand, industrial IoT rollouts and mandatory rural-broadband targets that together sustain moderate growth in the Mexico telecom tower market.

Key Report Takeaways

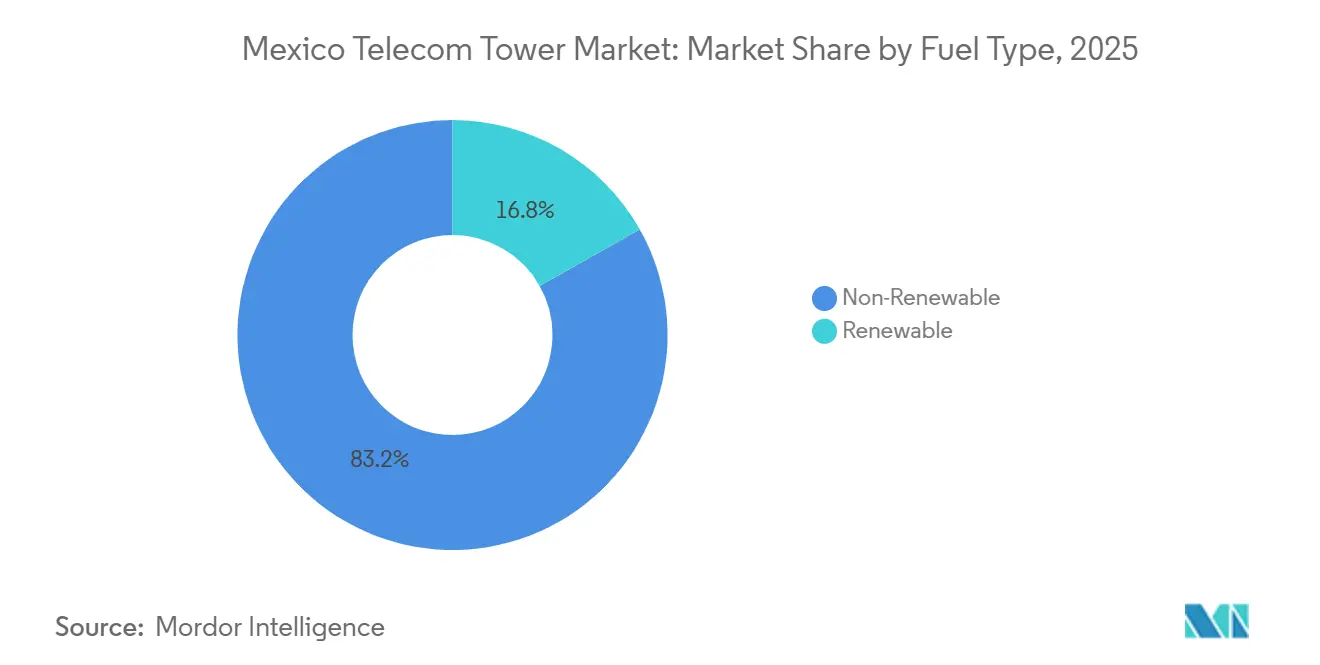

- By fuel type, non-renewable sources held 83.17% of Mexico telecom tower market share in 2025, while renewable-powered sites are advancing at a 3.26% CAGR through 2031.

- By tower type, monopoles led with 45.04% revenue share in 2025, whereas stealth designs are set to expand at a 4.12% CAGR to 2031.

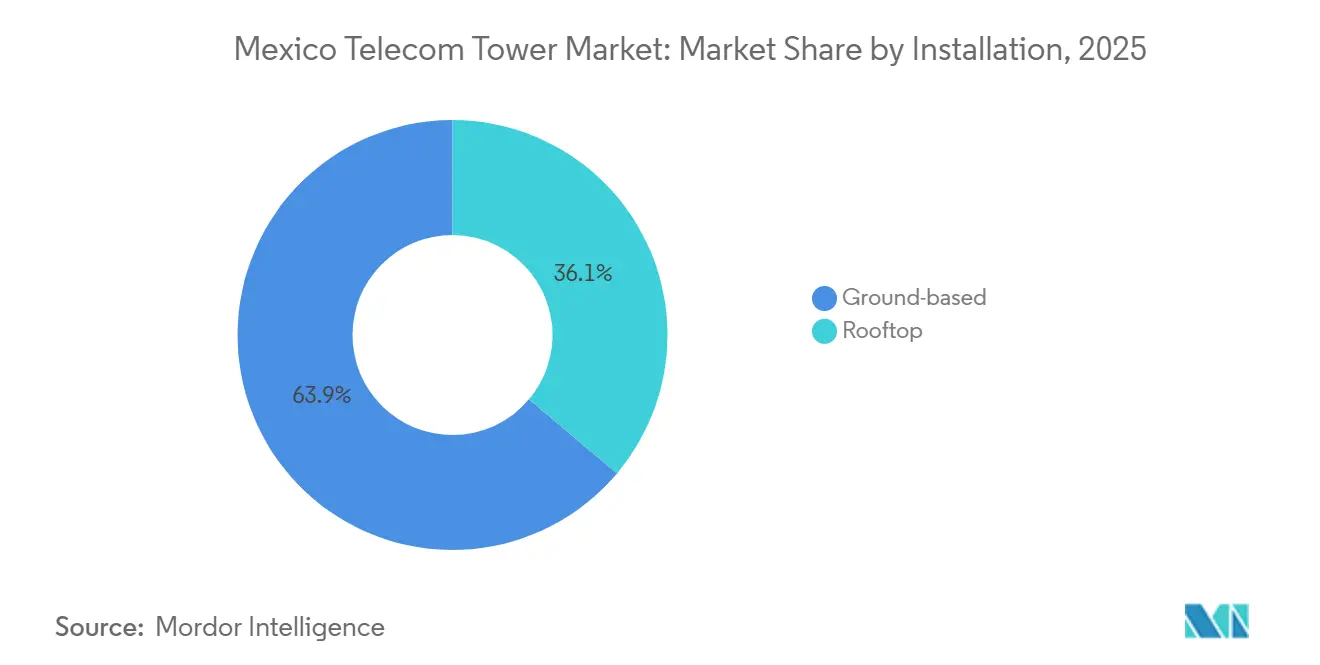

- By installation, ground-based structures accounted for 63.87% of the Mexico telecom tower market size in 2025 and rooftop sites are growing at a 3.58% CAGR to 2031.

- By ownership, private tower companies controlled 52.91% of assets in 2025 and are poised for a 2.73% growth trajectory during 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Telecom Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Mobile Data Consumption Per User | +0.9% | National, Concentrated in Mexico City Metropolitan Area, Guadalajara, Monterrey | Medium Term (2-4 Years) |

| Infrastructure-Sharing Regulations Reducing CAPEX | +0.7% | National, Particularly Central and North Mexico Industrial Corridors | Long Term (≥ 4 Years) |

| CFE Telecom Use of Utility Rights-of-Way for Low-Cost Towers | +0.6% | South Mexico, Rural Zones With Limited Private Infrastructure | Medium Term (2-4 Years) |

| Government-Funded Rural Broadband Programs | +0.5% | South Mexico, Indigenous Communities, Remote Municipalities | Long Term (≥ 4 Years) |

| Accelerated 5G Rollout Mandates | +0.4% | Mexico City Metropolitan Area, North Mexico Border Cities | Short Term (≤ 2 Years) |

| Escalating Electricity Tariffs Catalyzing Renewable Sites | +0.3% | National, Acute in Regions With Grid Instability | Medium Term (2-4 Years) |

| Source: ���ϲ����� | |||

Surging Mobile Data Consumption Per User

Telcel logged 12.8 million 5G customers by mid-2024, or 15% of its 83.4 million base, signaling a swift pivot to high-bandwidth applications that demand extra radios and fiber backhaul on each site.[1]América Móvil Investor Relations, “Financial Information,” americamovil.com Tower owners gain incremental rent from these upgrades, lifting average revenue per tenant while postponing greenfield builds in saturated districts. América Móvil earmarked USD 7 billion of 2024 capex to densify Mexico City, Guadalajara and Monterrey, adding macro and rooftop cells that ease video-streaming congestion. Yet nationwide 5G coverage reached only 37% in late 2024, far behind Chile and Brazil, keeping incremental tower demand focused on premium corridors. AT&T Mexico’s presence in 47 cities underscores the same urban skew, and its quest to monetize assets worth over USD 2 billion highlights the capital burden of competing at scale.

Infrastructure-Sharing Regulations Reducing CAPEX

A 2024 renewal of the Movistar-AT&T passive-infrastructure pact extended site pooling to 2030, trimming duplicate towers and cutting average build cost by roughly 30% for secondary operators. Originating under the now-dissolved independent regulator, these mandates stimulate tenancy ratios yet slow new-site volumes. The November 2024 shift of oversight to the Agency of Digital Transformation and Telecommunications sparked questions from United States-Mexico-Canada Agreement observers on regulator independence.[2]BNamericas Editorial, “Mexico’s Tower Market to Surpass 49,000 Sites by 2030,” bnamericas.com Still, smaller lessors such as Mexico Tower Partners, with 3,750 assets, leverage the framework to win multi-tenant contracts and scale rooftop and DAS portfolios. A 2024 Supreme Court ruling that only federal entities may tax permits further lowered site costs by removing fragmented municipal levies.[3]Center for Strategic and International Studies, “Mexico’s Telecom Sector at a Crossroads,” csis.org

CFE Telecom Use of Utility Rights-of-Way for Low-Cost Tower Deployment

By 2025, CFE Telecom had erected 5,229 LTE towers and strung 63,696 km of fiber along power lines, sidestepping land-acquisition delays that plague private rivals. Fold-in of bankrupt Altán Redes added 11,383 more towers plus a 90% discount on 700 MHz spectrum, letting the state entity undercut commercial lease rates. American Tower Corporation and Telesites argue the subsidy distorts market pricing, yet the state objective of 200,000 public Wi-Fi points by 2025 keeps momentum in underserved villages. CFE Telecom posted a MXN 9 billion (USD 460 million) 2023 loss, revealing the fiscal drag of coverage-first mandates, but military-engineer crews and utility cash flows continue to propel builds deeper into rural South Mexico.

Government-Funded Rural Broadband Programs

Federal digital-inclusion policy channels grants toward towers in settlements under 5,000 inhabitants, prompting 5,594 access points and 41,816 4G connections by 2025 in Oaxaca, Chiapas and Guerrero. Procurement favored Huawei and Nokia gear, creating parallel infrastructure that rarely interconnects with private networks, thus limiting colocation upside for independent lessors. However, by claiming loss-making terrain, CFE Telecom frees private firms to intensify focus on Mexico City and industrial corridors, sustaining double-digit returns on premium urban assets. Industry observers therefore view rural programs as both constraint and catalyst, shrinking addressable volume yet propping lease rates in core metro zones.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peso Volatility Inflating Imported Steel and RF Costs | -0.5% | National, Acute on Capital-Intensive New Builds | Short Term (≤ 2 Years) |

| Municipal Permitting Delays in Historic Zones | -0.3% | Central Mexico, Mexico City Metropolitan Area Historic Districts | Medium Term (2-4 Years) |

| Rising Urban Land-Lease Prices Amid Real Estate Boom | -0.2% | Mexico City Metropolitan Area, Monterrey, Guadalajara | Medium Term (2-4 Years) |

| Community Opposition Over RF Emissions | -0.2% | Urban Residential Zones, School Proximity Areas | Long Term (≥ 4 Years) |

| Source: ���ϲ����� | |||

Peso Volatility Inflating Imported Steel and RF Costs

BNP Paribas cut its 2025 GDP growth view to 0.5%, citing stubborn 4.7% inflation, a backdrop that drove a 10% peso slide versus the dollar in early 2025. Tower builds rely on dollar-priced steel and equipment from Ericsson, Nokia and Huawei, so depreciation lifted landed monopole costs by 8-12%, squeezing margins on peso-denominated leases. SITES LatAm spent USD 85,000 per new tower in Q4 2024, 6% above prior-year levels, and warned that further currency swings could force schedule deferrals.[4]SITES LatAm Investor Relations, “Quarterly Results,” sites.com.mx With domestic steel covering under 60% of need, hedging remains partial at best over 15-year lease horizons.

Municipal Permitting Delays in Historic Zones

Zoning boards in districts protected by the Instituto Nacional de Antropología e Historia extend approval cycles to 18 months, far beyond the six-month norm elsewhere, and often compel stealth designs that cost 20-30% more than standard monopoles. While the 2024 Supreme Court verdict stripped municipalities of fee-levying power, it left intact their aesthetic oversight, so community hearings and heritage reviews still slow activations, pushing tower firms toward costlier camouflaged poles to secure timely market entry. Advocacy groups demanding extra RF-emission studies add legal fees that chip away at internal rates of return.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Renewable Transition Accelerates Amid Grid Instability

Non-renewable generators controlled 83.17% of the Mexico telecom tower market in 2025, underscoring a legacy dependence on diesel and grid feeds. The renewables segment, though smaller, is pacing at a 3.26% CAGR through 2031, reflecting tariff hikes and blackouts that rocked the grid during 2024 heatwaves. That turmoil heightened the strategic value of hybrid solar-battery packages that satisfy stringent uptime clauses in operator leases. AT&T Mexico already powers 622 towers with on-site solar, saving roughly 3.5 million liters of diesel each year.

Transition economics remain challenging, as solar-battery capex still runs 40-50% above diesel gensets. Yet America Móvil’s pledge to cut Scope-1 and 2 emissions 52% by 2030 signals an acceleration in retrofit budgets, especially for flagship metro sites where energy bills and downtime penalties are steep. The wider Mexico telecom tower market stands to see renewable hybrid penetration expand beyond high-traffic corridors once lithium-ion prices fall and power-purchase agreements mature, an evolution that gradually narrows the operating-cost gap and raises the Mexico telecom tower market size attributable to clean-power systems.

By Tower Type: Monopole Dominance Meets Stealth Innovation

Monopole structures captured 45.04% revenue share in 2025, cementing their role as the workhorse of the Mexico telecom tower market because they fit tight footprints and rooftop slabs. Lattice frames dominate rural macro coverage thanks to superior load capacity, while guyed masts persist where land is spacious and wind loads light. The niche yet swiftly growing stealth category is forecast to record a 4.12% CAGR through 2031 as municipalities insist on visual harmony around heritage sites.

Stealth poles, disguised as flagpoles or palms, cost 20-30% more to erect, but they secure permits up to a year faster, accelerating revenue capture in dense corridors. That permit-speed advantage is compelling tower companies facing slower macro build volumes and currency-driven capex inflation. With SITES LatAm reporting an average monthly rent of USD 950 per tenant nationwide, and more than USD 1,300 in Mexico City, adding a second tenant lifts cash yields sharply. As Mexico telecom tower market share shifts toward camouflaged urban assets, operators balance upfront spend against faster time to revenue, supporting stable long-run margins.

By Installation: Rooftop Deployments Gain Traction in Dense Urban Markets

Ground-based towers still accounted for 63.87% of 2025 deployments, but rooftop nodes are expanding at a 3.58% CAGR through 2031 as operators chase small-cell density without securing fresh land parcels. Rooftop sites sidestep land rents and simplify fiber backhaul when the host building already carries Telcel or Telesites fiber.

5G millimeter-wave frequencies above 24 GHz demand tightly spaced antennas, often 200-300 meters apart, driving rooftop popularity in Mexico City, Guadalajara and Monterrey. América Móvil’s fiber-to-the-home push to 17 million premises by 2024 enriched that rooftop pipeline. Tower firms invest in structural audits and lightweight monopoles to satisfy roof-load limits, extracting high-margin leases of well above USD 2,000 per tenant on landmark properties. As a result, the Mexico telecom tower market size generated by rooftop assets is poised to outpace ground-based revenue growth even though the absolute site count remains lower.

By Ownership: Private Tower Companies Consolidate Market Share

Independent lessors held 52.91% of national sites in 2025 and are projected to grow 2.73% annually to 2031 as operators monetize non-core poles. Telefónica Movistar’s 2024 divestiture of 200 towers plus fiber routes to MX Towers typifies the trend, and AT&T Mexico’s effort to fetch more than USD 2 billion for its infrastructure signals further inventory heading to the wholesale pool.

The Mexico telecom tower market sees about 40% of sites with independents, 53% inside subsidiaries such as Telesites, and only 7% directly run by carriers, a fragmentation that leaves room for roll-ups. American Tower Corporation controls 9,702 local sites, roughly 22% of private inventory, and its tussle with AT&T Mexico over USD 300 million of delayed rent in 2025 exposed tenant-concentration risk. Yet sale-leasebacks remain attractive because they unlock cash for spectrum bids, so independent ownership is destined to climb, further increasing the Mexico telecom tower market share held by pure-play infrastructure providers.

Geography Analysis

The Mexico City Metropolitan Area and North Mexico jointly hosted close to 60% of tower assets in 2025, reflecting dense population, industrial export bases and cross-border data flow. Premium urban leases exceed USD 2,000 per tenant monthly, versus USD 800-1,200 in provincial centers, cementing metro focus for independent firms eager to protect returns. Telcel’s 5G build in 125 cities by April 2024 clustered capital in the capital, Guadalajara, Monterrey, Tijuana and Ciudad Juárez, reinforcing the urban skew of the Mexico telecom tower market.

North Mexico’s automotive and electronics corridors in Nuevo León and Chihuahua demand low-latency private networks, spurring tower collocation and edge-computing pods. Central Mexico, including Jalisco and Guanajuato, benefits from rising aerospace and EV output, prompting colocated macro and rooftop builds that widen the Mexico telecom tower market size in second-tier metros. South Mexico trails in coverage yet gains momentum from state-funded CFE Telecom rollouts that deliver service to indigenous municipalities unable to attract private capital, indirectly preserving pricing strength in core urban zones.

Regional disparity remains evident in 5G reach, just 37% population coverage nationwide by late 2024, so forthcoming spectrum auctions are crucial for stimulating expansion beyond prosperous corridors. Cancellation of the IFT-12 auction in 2025 deferred operator rollouts in secondary cities, but once clarity returns, pent-up demand in Bajío and tourist corridors should unlock a fresh wave of macro and rooftop builds. Until then, tower firms will keep channeling capex toward high-rent urban properties that underpin cash flow stability for the Mexico telecom tower market.

Competitive Landscape

Mexico’s telecom tower arena is moderately fragmented, with roughly 40% of the 44,000 structures in independent hands and the balance tied to operator affiliates. Scale matters: American Tower Corporation, Telesites and SITES LatAm each manage thousands of poles, leveraging procurement clout and multiyear master-lease agreements. American Tower’s clash with AT&T Mexico over USD 300 million in withheld rent spotlighted revenue-concentration risks where three carriers generate over 90% of demand.

Government intervention adds complexity. The 2024 absorption of Altán Redes into CFE Telecom, complete with a 700 MHz discount and army-built towers, injects a subsidized rival that can under-price private leases, challenging neutrality clauses in the United States-Mexico-Canada Agreement. Independent lessors warn that market-based incentives erode if state players distort returns, yet investors still fund newcomers: QMC Telecom raised USD 115 million in May 2024 to target secondary cities.

Consolidation is gathering pace. Telefónica Movistar exited ownership via a tower-and-fiber sale to MX Towers, while AT&T Mexico scopes a multibillion-dollar divestiture. Such deals free capital for spectrum and software while enlarging the inventory pool available to independents, subtly lifting tenancy ratios and reinforcing the Mexico telecom tower market’s gradual shift toward professionally managed, multi-tenant portfolios.

Mexico Telecom Tower Industry Leaders

American Tower Corporation (ATC Mexico)

Telesites, S.A.B. de C.V.

Mexico Tower Partners (MTP)

SBA Communications Corporation (SBA Mexico)

Phoenix Tower International (PTI)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: American Tower Corporation resumed receiving lease payments from AT&T Mexico after a USD 300 million dispute earlier in the year, with arbitration scheduled for Aug 2026 to finalize terms.

- January 2025: The Instituto Federal de Telecomunicaciones cancelled the IFT-12 5G spectrum auction, handing oversight to the newly formed Agency of Digital Transformation and Telecommunications, which immediately slowed tower deployment plans.

- November 2024: The Mexican government dissolved the independent telecom regulator and installed the Agency of Digital Transformation and Telecommunications under presidential control, sparking trade-compliance concerns.

Mexico Telecom Tower Market Report Scope

Telecom towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The Mexico Telecom Tower Market Report is Segmented by Fuel Type (Renewable, and Non-Renewable), Tower Type (Lattice Tower, Guyed Tower, Monopole Tower, and Stealth Tower), Installation (Rooftop, and Ground-based), Ownership (Operator-owned, Joint Venture, Private-owned, and MNO Captive), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Renewable |

| Non-Renewable |

| Lattice Tower |

| Guyed Tower |

| Monopole Tower |

| Stealth Tower |

| Rooftop |

| Ground-based |

| Operator-owned |

| Joint Venture |

| Private-owned |

| MNO Captive |

| By Fuel Type | Renewable |

| Non-Renewable | |

| By Tower Type | Lattice Tower |

| Guyed Tower | |

| Monopole Tower | |

| Stealth Tower | |

| By Installation | Rooftop |

| Ground-based | |

| By Ownership | Operator-owned |

| Joint Venture | |

| Private-owned | |

| MNO Captive |

Key Questions Answered in the Report

How large will the Mexico telecom tower market be by 2031?

It is expected to reach USD 759.3 million by 2031, expanding at a 2.61% CAGR from 2026.

Which tower type is growing fastest in Mexico?

Stealth towers are projected to grow at a 4.12% CAGR through 2031 as cities enforce stricter aesthetic rules.

Why are rooftop installations gaining momentum?

Rooftop nodes avoid land rents, speed permitting and enable dense 5G millimeter-wave coverage in Mexico City, Guadalajara and Monterrey.

What share of towers do independent companies control?

Independent lessors managed 52.91% of structures in 2025 and are set to increase that share as operators pursue sale-leasebacks.

How is currency volatility affecting tower construction?

A weaker peso raises imported steel and equipment costs by up to 12%, prompting some firms to delay new builds or renegotiate contracts.

What role does CFE Telecom play in rural coverage?

CFE Telecom leverages power-line rights-of-way and spectrum discounts to deploy thousands of subsidized towers in underserved South Mexico communities.

Page last updated on: