Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

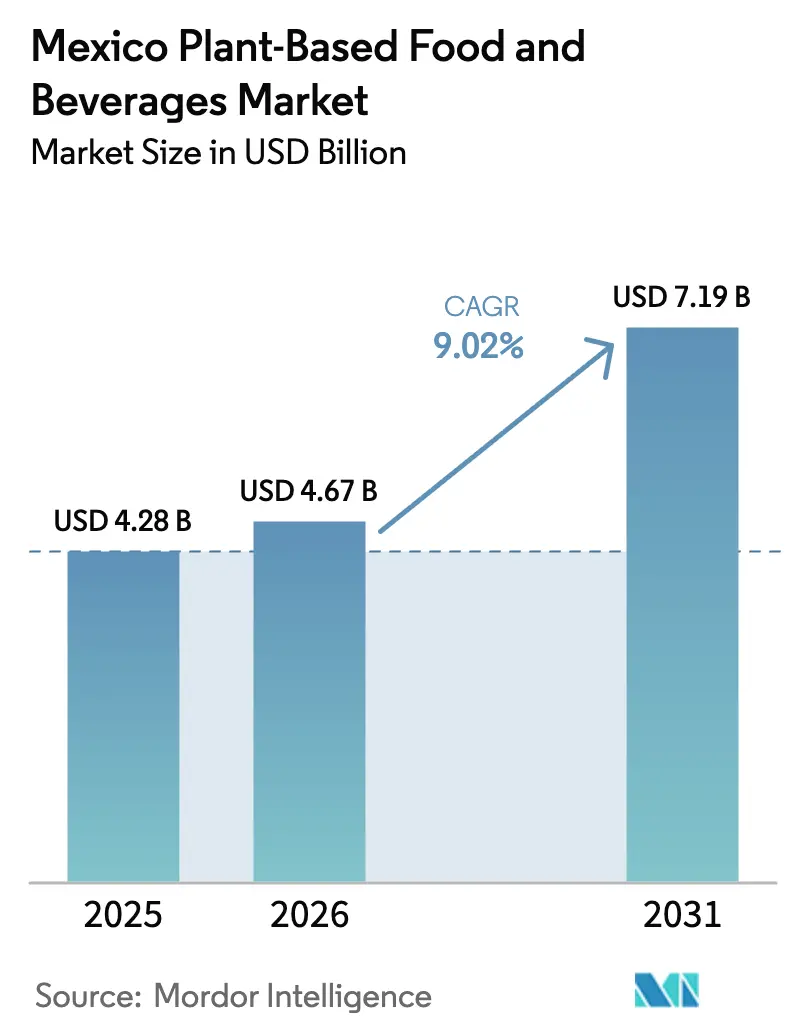

| Base Year Market Size (2025) | USD 4.28 Billion |

| Market Size (2026) | USD 4.67 Billion |

| Market Size (2031) | USD 7.19 Billion |

| Growth Rate (2026 - 2031) | 9.02% CAGR |

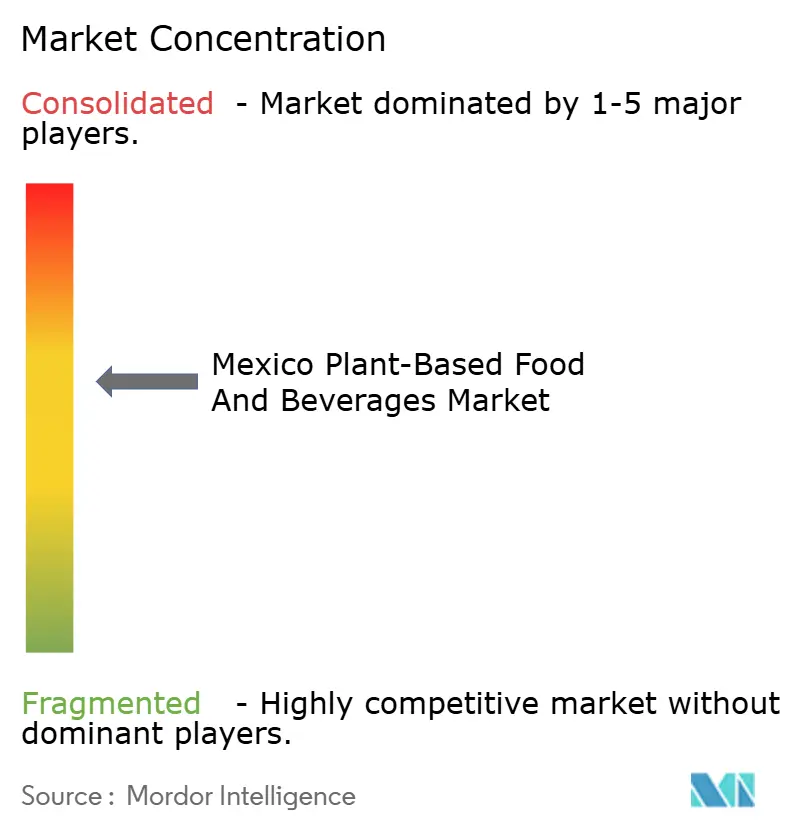

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Mexico Plant-Based Food And Beverages Market Analysis by ���ϲ�����

Forecasts indicate that the Mexico Plant-Based Food and Beverages market size, valued at USD 4.28 billion in 2025 and USD 4.67 billion in 2026, is set to reach USD 7.19 billion by 2031, marking a CAGR of 9.02% from 2026 to 2031. Despite limited purchasing power hindering frequent shifts to premium plant-based brands, policy measures—such as front-of-package warning labels, a nationwide ban on junk food in schools, and the introduction of Healthy and Sustainable Dietary Guidelines—have nudged households towards healthier food choices, as highlighted by WORLDOBESITY.ORG. In 2024, Mexico reported an alarming 73.4% obesity rate among adults and a diabetes mortality rate of 71.4 per 100,000, underscoring the urgent need for diet-driven preventive measures from both public and private sectors. While modern retailers dominate, accounting for nearly half of the nation's food sales and serving as primary gatekeepers for imported plant-based SKUs, traditional outlets face challenges. These outlets grapple with cold-chain deficiencies, limiting rural access. As a result, the Mexico Plant-Based Food and Beverages market is witnessing a transformation, driven by strategic pricing, partnerships for rural distribution, and a focus on clean-label reformulation.

Key Report Takeaways

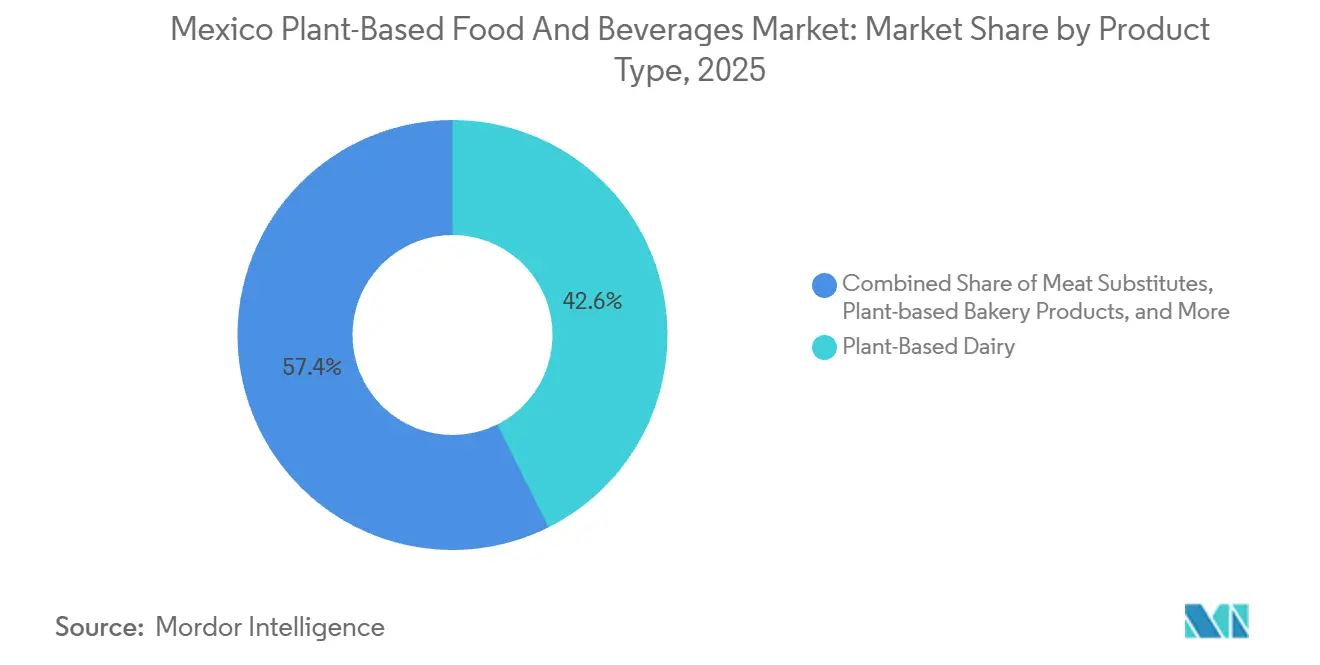

- By product type, Plant-based Dairy led with 42.63% of the Mexico Plant-Based Food and Beverages market share in 2025.

- Meat Substitutes are forecast to advance at a 7.75% CAGR through 2031, the fastest among product categories.

- By ingredient, Soy accounted for 45.05% of the Mexico Plant-Based Food and Beverages market size in 2025, while Rice-based formulations are set to grow at 9.42% CAGR to 2031.

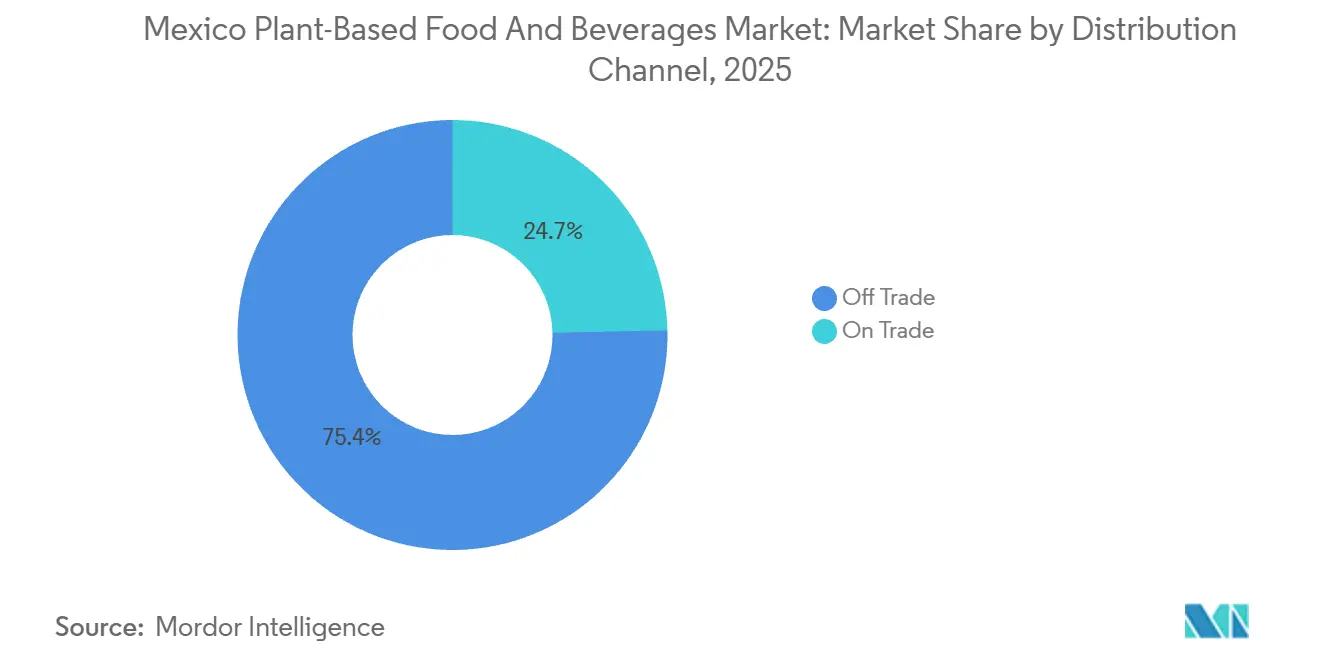

- Off-Trade channels captured 75.35% of the 2025 value, but On-Trade is projected to clock a 10.31% CAGR through 2031 on tourism recovery and menu diversification.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Plant-Based Food And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and lactose intolerance prevalence | +2.1% | National, concentrated in urban centers (Mexico City, Guadalajara, Monterrey) | Medium term (2-4 years) |

| Demand for functional, fortified plant-based beverages | +1.8% | National, with premium segment growth in northern states | Long term (≥ 4 years) |

| Shift toward vegan, vegetarian, and flexitarian diets | +1.5% | Urban Mexico, tourist regions (Cancún, Playa del Carmen) | Medium term (2-4 years) |

| Government health programs recommending reduced meat consumption | +1.3% | National, institutional channels (schools, Liconsa programs) | Long term (≥ 4 years) |

| Expanded retail and e-commerce availability | +1.0% | Urban centers, northern border regions | Short term (≤ 2 years) |

| Influence of urban millennials and Gen Z wellness trends | +0.9% | Mexico City, Monterrey, Guadalajara metropolitan areas | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising Health Consciousness and Lactose Intolerance Prevalence

In Mexico, the rising prevalence of cardiometabolic diseases is driving a growing demand for healthier diets. Studies show that adopting better eating habits could prevent 74,396 to 92,540 deaths annually from cardiovascular diseases, cerebrovascular diseases, type 2 diabetes, and colorectal cancer. The 2023 Mexican Healthy and Sustainable Dietary Guidelines, developed with input from the Secretaría de Salud, Instituto Nacional de Salud Pública, and UNICEF, recommend diets that are 21% more affordable and produce 34% fewer carbon emissions compared to current consumption patterns. These improvements focus on reducing red meat and ultra-processed food intake, especially in urban areas where dietary changes are more evident. Most Mexican adults are biochemically lactose intolerant when consuming 12-18 grams of lactose (about one glass of milk), though fewer than 15% experience symptoms. This has fueled the demand for dairy alternatives, which manufacturers are actively promoting. Urban households are increasingly replacing fluid milk with plant-based beverages made from soy, almond, and oat. USDA agricultural attachés have noted this shift in dairy consumption. With clinical evidence, government support, and wider retail availability, plant-based products are moving into mainstream markets, particularly among middle- to upper-income households willing to pay premiums for healthier, sustainable food options.

Demand for Functional, Fortified Plant-Based Beverages

Mexicans are increasingly choosing nutritious products, prompting manufacturers to fortify plant-based milks with essential vitamins and minerals like calcium, vitamin D, and B12 to address nutrient deficiencies caused by reduced dairy consumption. Regulatory guidelines from COFEPRIS allow brands to highlight these health benefits on packaging. However, NOM-051 front-of-package warning labels penalize products high in added sugars or sodium, pushing manufacturers to reformulate products with cleaner labels, natural sweeteners, and enhanced protein content. In 2024, the hotel-restaurant-institutional (HRI) sector grew by 4.5%, reaching approximately 490,000 establishments[1]Source: USDA Foreign Agricultural Service (FAS), "Report Name: Dairy and Products Annual", apps.fas.usda.gov. This sector is increasingly incorporating fortified plant-based beverages into breakfast buffets and wellness menus to cater to international tourists and health-conscious domestic consumers. Ingredient suppliers are leveraging this trend by offering ready-to-use fortification solutions, such as pea protein isolates enriched with iron and zinc or oat bases with added prebiotic fiber. These solutions enable Mexican food processors to launch functional products without significant research and development costs. The growing demand for fortified plant-based beverages indicates they will not only compete with traditional dairy products but also with sports drinks and meal-replacement options in convenience stores and modern retail channels, further expanding their market presence.

Shift Toward Vegan, Vegetarian, and Flexitarian Diets

Mexico is the second-largest adopter of plant-based diets globally, with a rising number of individuals identifying as vegan or vegetarian. This trend is primarily driven by younger, higher-income consumers in urban hubs like Mexico City, Monterrey, and Guadalajara. However, rural and lower-income populations largely stick to traditional, meat-based diets due to cultural habits and limited access to alternatives. Flexitarianism, where people reduce meat consumption occasionally, is also gaining momentum, creating a growing market for plant-based products that prioritize taste, convenience, and affordability. Restaurants nationwide are increasingly offering plant-based options, signaling the normalization of this lifestyle in the foodservice sector. Social media platforms like Instagram, TikTok, and YouTube are amplifying this trend, particularly among Gen Z and millennials, with micro-influencers driving product awareness and trials. Furthermore, the Asociación de Empresarios Veganos de México (AEVM) is collaborating with Mexico City's Ministry of Economic Development to support vegan entrepreneurs by enhancing funding, visibility, and accessibility.

Government Health Programs Recommending Reduced Meat Consumption

The Mexican government's 2025-2030 Healthy and Sustainable Dietary Guidelines recommend reducing meat consumption and focusing on plant-based proteins like beans and lentils, with moderate inclusion of eggs, poultry, and fish. This policy significantly impacts institutional procurement, including schools, Liconsa (a state-run milk distribution program for low-income groups), and public hospital cafeterias. A national junk-food ban, effective March 2025, requires schools to serve natural, minimally processed foods, such as seasonal fruits, vegetables, and meals with limited sugar and oil. This creates opportunities for plant-based snacks and beverages that meet nutritional standards. Profeco, the federal consumer protection agency, increases transparency through product quality assessments, such as its 2026 yogurt review, which exposed adulteration and non-compliance with NOM-181. The 2024 General Law on Adequate and Sustainable Food promotes nutrition education and sustainable food production, supporting plant-based systems. However, Liconsa's 2024 purchase of 618 million liters of fortified milk highlights the challenge for plant-based alternatives to match dairy's nutritional value and cost-effectiveness in social programs.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from established animal-based products | -1.7% | National, strongest in rural and low-income segments | Long term (≥ 4 years) |

| Supply chain disruptions and raw material price fluctuations | -1.2% | National, import-dependent manufacturers | Short term (≤ 2 years) |

| Consumer skepticism and negative perception | -0.9% | National, particularly among older and rural demographics | Medium term (2-4 years) |

| Allergen issues with soy and tree nuts | -0.5% | National, regulatory compliance under COFEPRIS | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Competition from Established Animal-Based Products

In 2025, Mexico's dairy sector produced 14.1 million metric tons of milk and is projected to grow steadily. This growth is fueled by strong domestic demand, lower input costs, and government support through subsidies like Liconsa distribution, alongside the widespread availability of dairy products in retail markets[2]Source: USDA Foreign Agricultural Service (FAS), "Report Name: Dairy and Products Annual", apps.fas.usda.gov. Conventional dairy products are priced 20-40% lower than plant-based alternatives due to economies of scale, a well-established cold-chain infrastructure, and the absence of import tariffs on U.S. dairy ingredients. However, plant-based dairy alternatives face significant challenges in replicating the taste, texture, and protein content of traditional dairy. Consumer studies reveal dissatisfaction with current options, highlighting the need for advanced R&D in precision fermentation and plant-protein texturization. Furthermore, only 6% of Mexicans follow traditional plant-based diets, while 68% consume meat-heavy Western diets. Dietary transitions are slow, particularly in rural and low-income areas where animal proteins are culturally significant and affordable. Additionally, animal-based products benefit from larger marketing budgets, creating substantial barriers for plant-based competitors.

Supply Chain Disruptions and Raw Material Price Fluctuations

Mexico's plant-based protein sector relies heavily on U.S. imports, making it vulnerable to exchange-rate fluctuations, rising freight costs, and trade policy changes. The peso's depreciation through 2025 has significantly increased the cost of importing essential ingredients like soy protein isolates, pea protein concentrates, and specialty oils (such as almond and oat). This has tightened manufacturers' margins, as many cannot pass these costs to price-sensitive consumers. Furthermore, global vegetable oil prices rose 24.2% year-on-year from January to May 2025, driven by palm oil supply shortages in Indonesia and Malaysia, biodiesel mandates, and shipping disruptions in the Red Sea and Suez Canal. These rising costs have directly impacted the production of plant-based dairy and meat alternatives, which depend on oils like coconut, sunflower, and canola. Mexico, expected to import 22.0 million metric tons of maize in 2025/26, remains highly exposed to global grain market volatility. While manufacturers are exploring local sourcing opportunities in citrus (3.5 million metric tons) and sorghum (4.2 million metric tons), the country’s underdeveloped processing capacity for protein fractionation and oil extraction continues to hinder growth[3]Source: USDA Foreign Agricultural Service (FAS), "Production - Mexico", apps.fas.usda.gov.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dairy Alternatives Dominate, Meat Substitutes Accelerate

In 2025, plant-based dairy accounted for 42.63% of the market value, driven by the increasing demand for soy, almond, and oat milks in urban areas. However, only 15% of Mexican households purchased plant-based milk at least once, compared to the near-universal consumption of traditional dairy milk. This highlights significant growth opportunities if pricing and distribution barriers are addressed. Yogurt and cheese alternatives are gaining traction, with brands like Del Bosque (soy yogurt), Violife (imitation Manchego), and Q-Veggie (mozzarella-style) expanding their presence in specialty stores and supermarkets. In April 2025, La Michoacana introduced its first dairy-free paletas line, featuring flavors like Coconut & Strawberries 'N Cream and Piña Colada, made with coconut cream and distributed through Costco, Walmart, and Albertsons in Mexico and the U.S. Plant-based beverages, including packaged milk, smoothies, coffee, and tea, dominate the segment, supported by trends in functional fortification.

Meat substitutes are expected to grow at a 7.75% CAGR through 2031, driven by product innovation and foodservice adoption. Tofu and tempeh are becoming more popular in cities, while textured vegetable protein (TVP) is increasingly used in institutional kitchens. Nestlé’s 2024 launch of plant-based ground meat products across Latin America, including Mexico, reflects strong multinational interest. Local startups like Plant Squad (seitan-based tenders) and Maika (veggie burgers) are targeting flexitarians through e-commerce and specialty stores. Regulatory scrutiny, including NOM-051 labeling, emphasizes the need for reformulation to meet health-conscious consumer demands. Clean-label formulations and transparent supply chains remain critical to overcoming these challenges.

By Ingredient: Soy Dominance Faces Allergen and Diversification Pressures

In 2025, soy is projected to hold a significant 45.05% share of the ingredient market, reflecting its long-standing supply-chain development, agronomic efficiency, and versatility. It is widely used in dairy alternatives, meat substitutes, and baked goods due to its functional benefits in emulsification, protein fortification, and texturization. Soy protein isolate imports reached 2,708.8 metric tons, emphasizing its importance in industrial formulations. However, soy faces challenges, including rising allergen concerns and sustainability issues linked to deforestation in South America. Retailers and brands are increasingly sourcing certified deforestation-free soy or exploring alternative proteins. Ingredients like Almond, Pea, and Oat are gaining popularity as manufacturers aim for allergen-free and diverse formulations. However, almond and oat ingredients remain import-dependent, with products like Yumma Avocado Almond Milk priced at MXN 151.80 for 450 ml, reflecting premium costs.

Rice-based ingredients are expected to grow at a 9.42% CAGR through 2031, driven by their hypoallergenic properties, neutral flavor, and lower costs compared to tree nuts. Rice milk appeals to consumers with multiple food sensitivities and parents seeking allergen-free options, supported by the 2024 General Law on Adequate and Sustainable Food, which prioritizes school nutrition. Coconut-based ingredients, used in premium products like Walrus Code ice cream (MXN 61.60) and Gud Vegan Cream (MXN 88.00 for 500g), occupy a niche but profitable segment. Functional flours from pea, lentil, chickpea, and fava bean are emerging as dual-purpose ingredients for protein fortification and gluten-free baking. The ingredient market is shifting towards diversification and local sourcing. Mexico’s maize diversity, with 64 native races documented by CONABIO, offers potential for functional corn-based beverages like pozol and tejuino, blending traditional appeal with modern nutritional benefits, though commercialization remains limited to artisanal producers.

By Distribution Channel: Off-Trade Scale Meets On-Trade Growth

In 2025, Off-Trade channels accounted for 75.35% of sales, led by supermarkets and hypermarkets such as Walmart Mexico, Soriana, Chedraui, and La Comer. These retailers, which represent 72.4% of health and wellness packaged food sales, play a key role in listing plant-based products. Modern retail offers advantages like centralized procurement, cold-chain logistics, and private-label development, with retailers expanding their plant-based private-label lines to boost margins and stand out from national brands. However, smaller producers face challenges due to high volume and compliance requirements. Convenience stores, like OXXO with over 20,000 outlets, are emerging as key points for single-serve plant-based snacks and beverages aimed at on-the-go consumers. Online platforms, including retailer websites like Walmart.com.mx and Soriana.com, and delivery apps like Rappi and Uber Eats, are growing rapidly among urban, high-income consumers who value convenience and variety. Specialty retailers like Veggicano cater to vegan and health-conscious customers, offering premium-priced imported brands such as Tofutti and Gud.

On-Trade channels are projected to grow at a 10.31% CAGR through 2031, driven by menu innovation and tourism. In 2024, Mexico’s restaurant industry grew by 4.5% to 490,000 establishments, while international tourist arrivals reached 45 million. This growth supports plant-based menu options in hotels, resorts, and quick-service restaurants. Companies like Unilever are partnering with chains like Burger King to introduce plant-based items. However, challenges such as limited cold-chain infrastructure, high ingredient costs, and chef training requirements persist. Overcoming these barriers will require price parity with animal-based items, expanded distribution in domestic markets, and leveraging social media to boost demand for plant-based offerings.

Geography Analysis

Mexico's plant-based food and beverage market shows clear differences between urban, rural, and regional areas. Consumption is concentrated in major cities like Mexico City, Monterrey, and Guadalajara, which together account for 40% of the population and dominate modern retail and foodservice sales. Mexico City, with over 21 million people in its metropolitan area, is the leading market for imported and premium plant-based products. This is due to higher disposable incomes, diverse consumer preferences, and a strong retail network, including Walmart, Costco, La Comer, and specialty stores like Veggicano. Northern states such as Nuevo León, Chihuahua, and Baja California are early adopters of U.S. plant-based products, influenced by their proximity to the border, cross-border shopping, and cultural exchanges. USDA reports indicate that northern consumers prefer imported U.S. products and shop online, creating opportunities for cross-border brands. Tourist destinations like Cancún, Playa del Carmen, and Los Cabos are also seeing growth in plant-based options as hotels and restaurants cater to international visitors, with 32 million tourists in 2023 driving demand.

In contrast, rural and southern regions like Oaxaca, Chiapas, and Tabasco rely on traditional diets of maize and beans. Processed plant-based products have low penetration here due to affordability issues, limited cold-chain logistics, and a preference for local ingredients. ENSANUT data shows only 6% of Mexicans follow a "staple" diet, mainly in rural and southern areas, while 68% follow Western diets, indicating a decline in traditional plant-based eating. Urban and northern regions will drive market growth due to higher purchasing power and openness to innovation. However, rural areas require strategies like lower prices, partnerships with local markets, and culturally adapted products like plant-based chorizo or tamales. The 2023 dietary guidelines highlight that southern rural diets already meet meat consumption recommendations, so plant-based strategies must align with regional habits.

COFEPRIS ensures consistent labeling and health claims nationwide, but enforcement and awareness vary. Urban consumers are more familiar with NOM-051 labels, while rural consumers prioritize affordability. The 2024 General Law on Adequate and Sustainable Food promotes nutrition education and sustainable food production, offering long-term potential for change in underserved areas. Brands must balance short-term urban opportunities with long-term rural growth by leveraging government programs, local partnerships, and culturally relevant products.

Competitive Landscape

The Mexico plant-based food and beverages market exhibits a moderately concentrated structure, characterized by the presence of a few dominant multinational companies alongside a growing number of regional and niche players. Large global manufacturers leverage established distribution networks, strong brand recognition, and diversified product portfolios to maintain a competitive advantage. Their scale enables consistent product innovation, competitive pricing strategies, and broad retail penetration across supermarkets, hypermarkets, and convenience stores.

At the same time, domestic brands and emerging startups are strengthening their presence by targeting evolving consumer preferences, particularly among health-conscious, lactose-intolerant, and flexitarian populations. These players often focus on differentiated offerings such as locally sourced ingredients, clean-label formulations, and culturally adapted flavors that resonate with Mexican consumers. This dynamic has led to increased product diversification across categories including plant-based dairy alternatives, meat substitutes, and functional beverages.

Competitive intensity in the market is driven by continuous product innovation, strategic partnerships, and expansion into modern retail and e-commerce channels. Companies are investing in marketing initiatives to build awareness around sustainability, health benefits, and ethical consumption. While market entry barriers such as supply chain integration and brand loyalty favor established players, the evolving consumer landscape continues to create opportunities for smaller brands to gain traction, reinforcing the market’s moderately concentrated nature.

Mexico Plant-Based Food And Beverages Industry Leaders

-

Danone SA

-

Nestle SA

-

Heartbest Foods

-

Grupo Bimbo SAB de CV

-

NotCo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Silk has introduced a new plant-based beverage formula in Mexico, expanding its presence in the country’s growing market for dairy alternatives. According to the brand, the newly launched Silk formula includes six essential nutrients and offers an improved texture, alongside a neutral flavor that can be used in a variety of settings, from morning coffee to post-workout smoothies.

- August 2025: Silk introduced its new plant-based beverage formula in Mexico, aiming to strengthen its position in the growing market for dairy alternatives. Silk’s new formula was designed to integrate easily into daily routines, offering six essential nutrients, an improved texture, and a neutral flavor profile adaptable to various consumption moments, from morning coffee to post-workout smoothies.

- February 2025: Spanish plant-based meat brand Heura has launched its first Mexican-style product, Tex Mex Chunks. According to the brand, the launch is an expansion of the Chunks range, available in Original and Mediterranean varieties.

Mexico Plant-Based Food And Beverages Market Report Scope

Plant-based food and beverages are produced from various plant sources such as fruits, vegetables, nuts, oils, whole grains, and legumes, among others. Being plant-based these products contain no components derived from animals and use only plant-sourced ingredients. Mexico plant-based food and beverages market is segmented by product type and distribution channel. By product type, the market is segmented into meat substitutes, dairy alternative beverages, non-dairy ice cream, non-dairy cheese, non-dairy yogurt, non-dairy spreads, and other plant-based products that include non-dairy chocolates, milk powders, etc. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. The report offers market size and forecasts in value (USD million) for the above segments.

By Product Type

| Plant-based Dairy | Yogurt |

| Cheese | |

| Frozen Desserts and Ice-Cream | |

| Other Plant-based Dairy | |

| Meat Substitutes | Tofu |

| Tempeh | |

| Textured Vegetable Protein | |

| Other Meat Substitutes | |

| Plant-based Nutrition/Snack Bars | |

| Plant-based Bakery Products | |

| Plant-based Beverages | Packaged Milk |

| Packaged Smoothies | |

| Coffee | |

| Tea | |

| Other Plant-based Beverages | |

| Other Food and Beverages |

By Ingredient

| Soy |

| Almond |

| Pea |

| Oat |

| Rice |

| Coconut |

| Other Sources |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Stores | |

| Other Off-Trade Channels |

| By Product Type | Plant-based Dairy | Yogurt |

| Cheese | ||

| Frozen Desserts and Ice-Cream | ||

| Other Plant-based Dairy | ||

| Meat Substitutes | Tofu | |

| Tempeh | ||

| Textured Vegetable Protein | ||

| Other Meat Substitutes | ||

| Plant-based Nutrition/Snack Bars | ||

| Plant-based Bakery Products | ||

| Plant-based Beverages | Packaged Milk | |

| Packaged Smoothies | ||

| Coffee | ||

| Tea | ||

| Other Plant-based Beverages | ||

| Other Food and Beverages | ||

| By Ingredient | Soy | |

| Almond | ||

| Pea | ||

| Oat | ||

| Rice | ||

| Coconut | ||

| Other Sources | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Stores | ||

| Other Off-Trade Channels | ||

Key Questions Answered in the Report

What is the current value of the Mexico Plant-Based Food and Beverages market?

The market was valued at USD 4.67 billion in 2026 and is on track to reach USD 7.19 billion by 2031.

How fast is category value growing?

It is projected to register a 9.02% CAGR from 2026 to 2031.

Which product segment leads sales?

Plant-based Dairy held 42.63% of 2025 value, making it the largest segment.

Which distribution channel is expanding the fastest?

On-Trade outlets, spurred by tourism and menu innovation, are expected to post a 10.31% CAGR to 2031.

Page last updated on: