Metal Replacement Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 171.35 Billion |

| Market Size (2030) | USD 253.29 Billion |

| Growth Rate (2025 - 2030) | 8.13% CAGR |

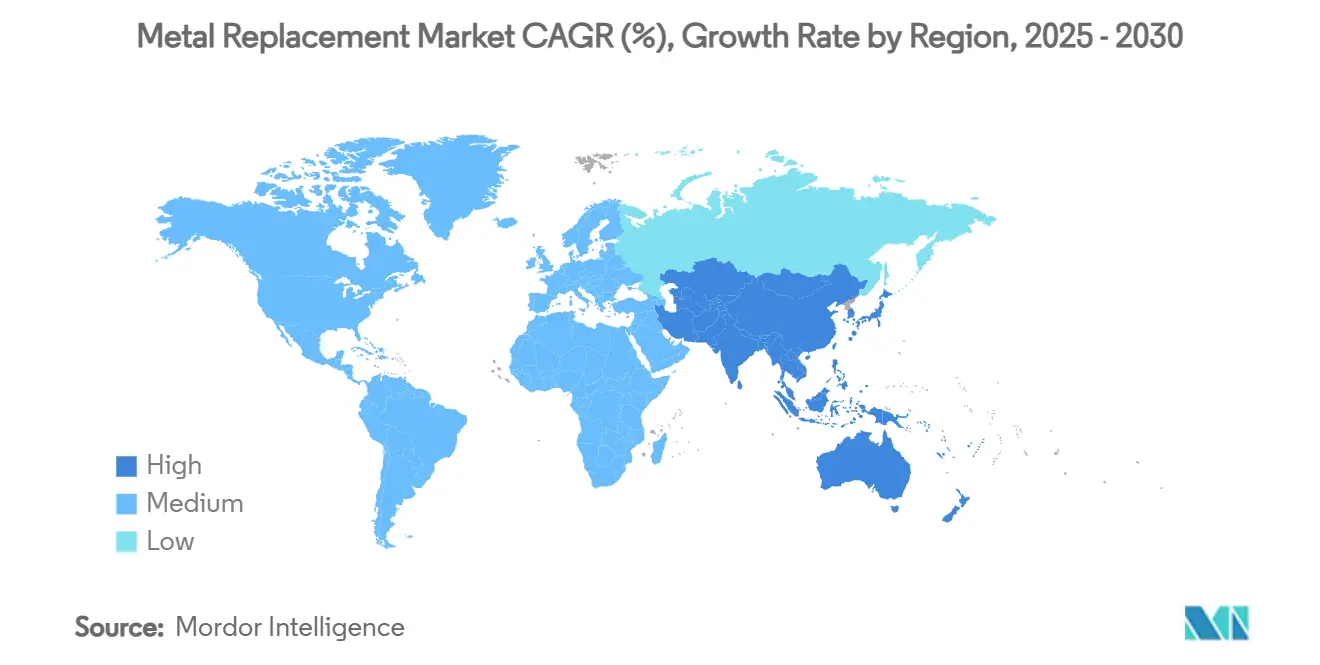

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

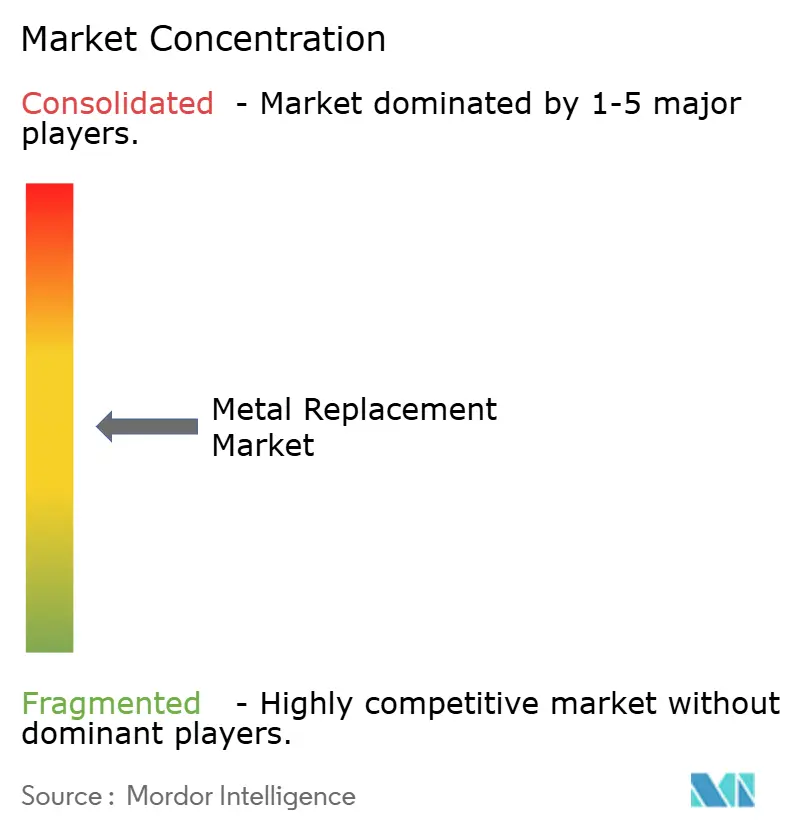

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Metal Replacement Market Analysis by ���ϲ�����

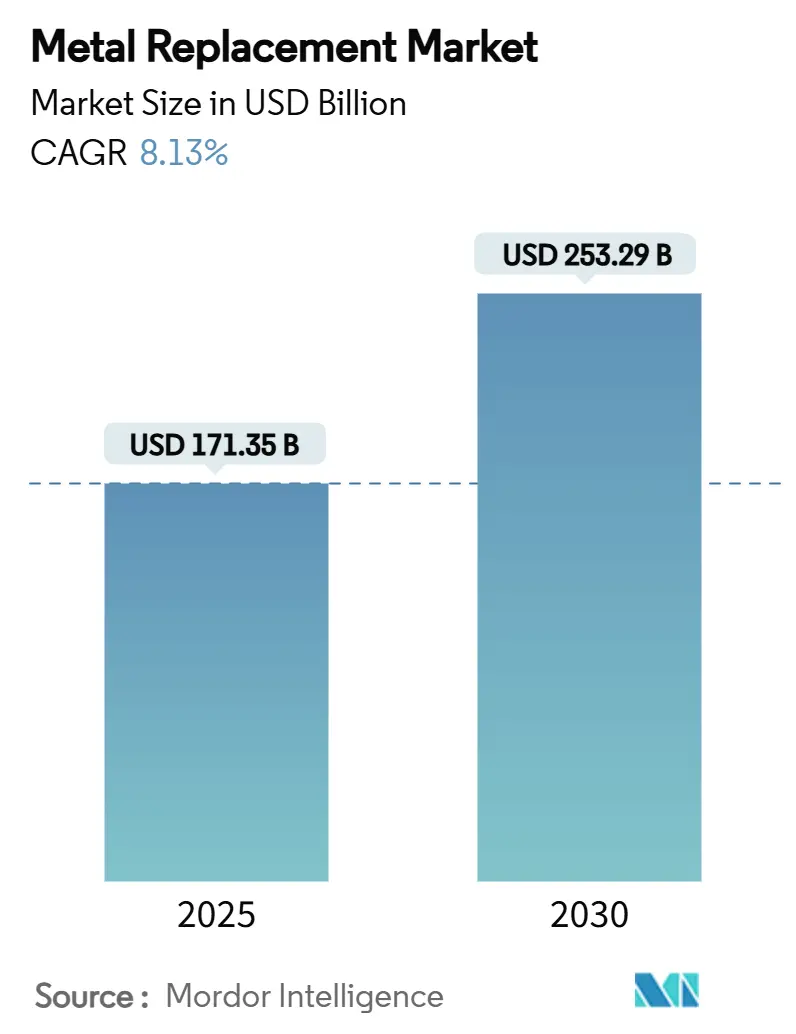

The Metal Replacement Market size is estimated at USD 171.35 billion in 2025, and is expected to reach USD 253.29 billion by 2030, at a CAGR of 8.13% during the forecast period (2025-2030), propelled by tightening lightweighting mandates and continuous material innovations. The value gap between high-performance polymers and traditional metals is narrowing as engineering plastics deliver metal-equivalent strength while enabling complex part geometries, corrosion resistance, and faster production cycles. Automotive OEMs remain the largest consumers because every 10% reduction in vehicle mass translates into a 6-8% fuel-efficiency gain. Healthcare device makers are rapidly shifting from titanium implants to biocompatible polymers such as PEEK to avoid stress shielding and to leverage 3D printing for patient-specific designs. Regional demand concentrates in Asia-Pacific where large-scale investments in engineering-plastic and composite lines meet growing electric-vehicle and infrastructure needs.

Key Report Takeaways

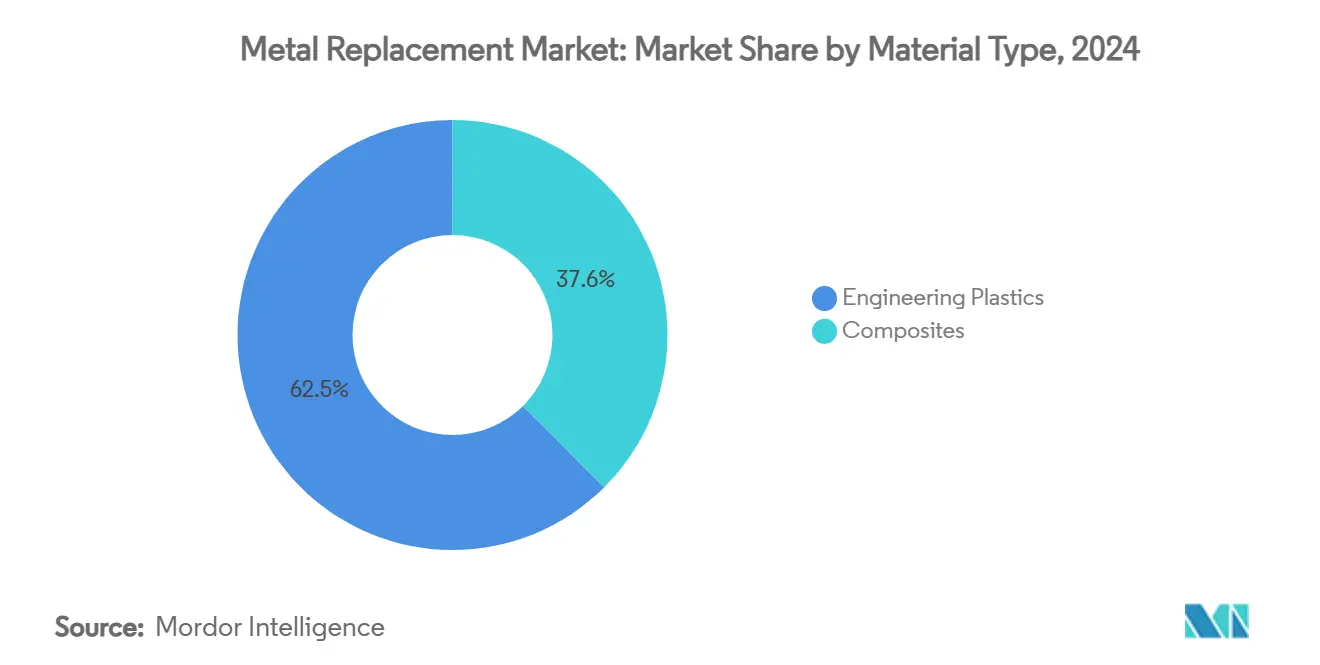

- By material type, engineering plastics held 62.45% of the metal replacement market share in 2024, while composites posted the fastest 8.81% CAGR through 2030.

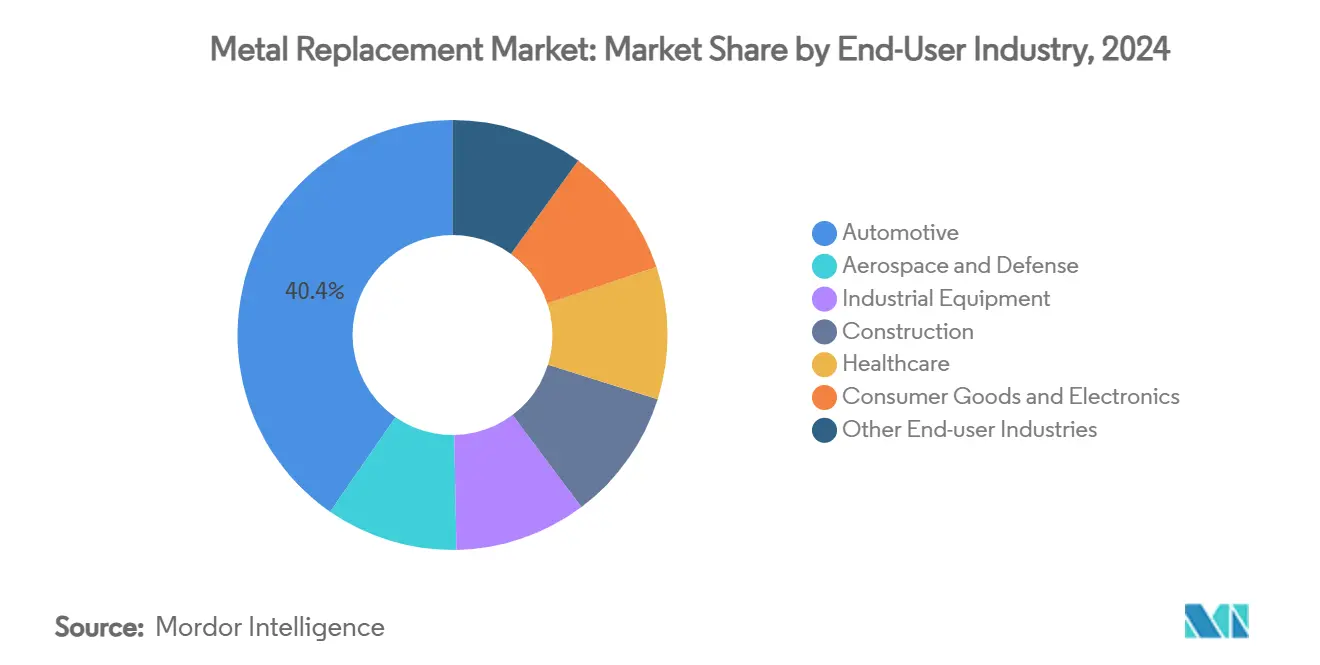

- By end-user industry, automotive commanded 40.35% share of the metal replacement market size in 2024, whereas healthcare is advancing at an 8.78% CAGR to 2030.

- By geography, Asia-Pacific accounted for a 47.34% share of the metal replacement market size in 2024 and is forecast to grow at a 9.12% CAGR over 2025-2030.

Global Metal Replacement Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in automotive and aerospace lightweighting trends | +2.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Increasing use of engineering plastics & composites in place of metals | +2.1% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Rapid expansion of electric-vehicle component manufacturing | +1.9% | Global, led by China and expanding to North America & EU | Short term (≤ 2 years) |

| Additive manufacturing of reinforced polymers enabling small-batch metal replacement | +1.2% | North America & EU, emerging in Asia-Pacific | Medium term (2-4 years) |

| Regulatory push for micro-mobility device lightweighting | +0.8% | EU & North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Growth in Automotive and Aerospace Lightweighting

Stringent emission norms are pushing automakers toward plastics and composites that shave kilograms without compromising crashworthiness. The United States targets 85 g/mile CO₂ for light-duty vehicles by 2032, forcing OEMs to substitute heavy steel parts with glass-fiber-reinforced polyamide modules that deliver 30% weight savings[1]Federal Register, “Multi-Pollutant Emissions Standards 2027-2032,” federalregister.gov. In aerospace, the Boeing 787 moved from 2% to nearly 80% composite content across five decades, cutting airframe mass by 20% and boosting fuel efficiency by more than 10%[2]SAE International, “Composite Adoption in Commercial Aircraft,” sae.org. The global CFRP market is expected to reach USD 41.4 billion in 2025, underscoring the steady transition away from aluminum skins. Thermoplastic composite aircraft ribs developed by Arkema and Hexcel now offer recyclability alongside structural integrity, marking a pivotal sustainability milestone.

Increasing Use of Engineering Plastics & Composites in Place of Metals

Continuous-fiber-reinforced thermoplastics provide higher stiffness-to-weight ratios than many ferrous alloys while retaining impact toughness and fatigue life. CF-PEEK, for instance, posts tensile strength of 425 MPa versus 311 MPa for conventional CF-epoxy while achieving flame-retardant LOI scores of 47. Automated fiber placement and stamp-forming lines introduced by Mitsubishi Chemical reduce cycle time and part cost, broadening uptake in EV battery trays and structural cross-members.

Rapid Expansion of Electric-Vehicle Component Manufacturing

A typical Chinese new-energy vehicle already incorporates 40 kg of advanced compounds, and thermoplastic composite battery enclosures now weigh 10 kg versus 80 kg for earlier metal designs. Covestro’s polycarbonate inverters meet high-heat and dimensional-stability needs while allowing LiDAR transparency required for advanced driver-assistance systems. India’s EV ecosystem is on track for a 90% CAGR that could generate USD 150 billion in annual value by 2030, magnifying regional polycarbonate and polyamide demand.

Additive Manufacturing of Reinforced Polymers Enabling Small-Batch Metal Replacement

Continuous-fiber FDM printers achieve 540 MPa flexural strength, surpassing 6061-T6 aluminum and enabling localized production of drone airframes and surgical tools. PEEK cranial implants gained FDA clearance in 2024, validating additive manufacturing for load-bearing medical components. Machine-learning-based deposition control now minimizes voids, improving quality consistency and widening certification pathways in aerospace and defense.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced polymers & composites | -1.4% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Performance limitations in high-stress applications | -0.9% | Aerospace & Defense, Industrial Equipment sectors | Long term (≥ 4 years) |

| Supply-chain volatility for specialty additives & resins | -0.7% | Global, with acute impact in Asia-Pacific supply chains | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

High Cost of Advanced Polymers & Composites

BASF lifted North American PA66 compound prices by USD 0.15/lb in 2024 as feedstock costs climbed. Carbon fiber remains 45 times more expensive than aluminum, straining adoption in cost-sensitive segments. US import tariffs on plastic resins introduced in 2025 are set to inflate domestic part costs by up to 20%. Volatility in specialty additive supply chains keeps engineering-plastic pricing unpredictable, although bio-based routes such as BASF’s 40% biomass-balanced ethyl acrylate demonstrate long-run cost-carbon relief.

Performance Limitations in High-Stress Applications

Operating temperatures above 572 °F and cyclic loads in turbine hardware still favor nickel or titanium alloys, limiting the scope of polymer substitution. Earlier EU proposals to curb carbon-fiber use over recyclability concerns, though shelved, signal regulatory scrutiny of composite end-of-life pathways. Additive-manufactured polymer parts face certification hurdles due to variable porosity and bonding, requiring tighter process windows and digital-thread traceability before full aerospace qualification.

Segment Analysis

By Material Type: Engineering Plastics Dominate While Composites Accelerate

Engineering plastics captured 62.45% of the metal replacement market in 2024, anchored by high-volume polyamide, polycarbonate, and POM formulations validated for power-train and medical housings. Celanese’s Zytel XMP70G50 PA66 replaces steel cross-members in EV chassis, cutting 25% weight and improving fatigue life. The segment benefits from mature global supply chains and drop-in processing on injection and blow-molding lines.

Composites are posting the fastest 8.81% CAGR, driven by carbon-fiber-reinforced thermoplastics that combine rapid processing with recyclability. Global demand for carbon fiber is projected to hit 450,000 tonnes by 2030, up from 25,000 tonnes in 2005. Glass-fiber laminates maintain volume leadership due to cost advantages, but novel hybrid fabrics now generate 1.8× higher specific strength than stamped steel in pump housings. Intelligent composite systems outfitted with embedded sensors report real-time strain, allowing predictive maintenance and broader adoption in high-value industrial equipment.

By End-user Industry: Automotive Leadership Meets Healthcare Innovation

The automotive domain anchored 40.35% of the global metal replacement market size in 2024. Fiber-reinforced plastics reduce vehicle mass by 30%, enhance corrosion resistance, and lower tooling costs compared with stamped steel. Electric-vehicle platforms increasingly integrate polypropylene copolymer front wing plates and polycarbonate structural cross-beams, displacing traditional metal stampings while improving design freedom. BMW’s use of recycled carbon-fiber composites in mass-market models further underscores sustainability alignment.

Healthcare devices represent the fastest-growing 8.78% CAGR segment. PEEK’s elastic modulus closely matches cortical bone, minimizing stress shielding, while its radiolucency enables clear postoperative imaging. Device firms achieve up to 80% weight reduction and 30% cost savings by switching from stainless steel to single-use polymer instruments that cut sterilization expenses. Emerging orthopedic applications incorporate continuous-fiber-reinforced PEEK screws that equal titanium pull-out strength yet avoid metal artifacts in MRI scans.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific held a 47.34% share of the metal replacement market in 2024 and is forecast to grow at a 9.12% CAGR through 2030. China leads with large-scale ABS, polyamide, and CFRP capacity expansions that reduce import reliance while supporting domestic EV output averaging 40 kg advanced compounds per vehicle. Government incentives prioritize upstream material sovereignty, and local suppliers like Hengli and Wanhua invest in lithium-battery polymers and high-temperature resins to meet next-generation battery-housing specs.

India is gaining momentum as a polymer manufacturing hub. Deepak Nitrite’s USD 1.1 billion investment in methyl methacrylate, polymethyl methacrylate, and polycarbonate complexes at Dahej will come online by 2027, feeding appliance, automotive, and solar end markets. Toray’s 93,000-square-foot R&D facility in Japan focuses on nano-filler composites for autonomous-vehicle lidar housings, while Sekisui Chemical targets growth in hot-water and industrial piping through CPVC compounds that replace copper and galvanized steel.

North America and Europe maintain sizable demand bases driven by stringent emission policies and reshoring strategies. The US Inflation Reduction Act accelerates domestic EV production, prompting supply-chain localization for polymer components. LEGO’s USD 1 billion Virginia plant exemplifies onshoring for energy-efficient molding with renewable electricity. In Europe, Euro 7 tailpipe and brake-dust regulations stimulate investment in flame-retardant polycarbonate and glass-fiber-nylon brake-backing plates, displacing cast iron.

Competitive Landscape

Global competition in the metal replacement market is intensifying as incumbents pursue acquisitions, divestitures, and ecosystem partnerships. Celanese’s USD 11 billion takeover of DuPont Mobility & Materials doubled its engineered-materials revenue and is projected to yield USD 450 million in annual synergies. BASF segregated commodity chemicals from high-growth specialties, carving out the Metal Solutions unit to streamline decision-making and unlock capital efficiency.

LANXESS exited urethane systems in a EUR 460 million sale to UBE Corporation, channeling proceeds into battery-grade specialty additives with lower CO₂ footprints. Arkema invested in Heartland Industries to integrate kenaf-fiber additives, driving Scope 3 emission cuts in high-volume plastics for sports and infrastructure. Evonik collaborates with BASF on biomass-balanced ammonia, delivering a 65% product-carbon-footprint reduction for nylon intermediates.

Market leaders prioritize circular-economy credentials alongside mechanical performance. Celanese’s paint-grade carbon-capture polymer uses 2 million lb captured CO₂ annually. Mitsubishi Chemical diverts PET bottle waste into CFRP precursors, reinforcing the sustainability narrative. Despite consolidation, niche innovators remain competitive by specializing in high-thermal-conductivity polyimides and electrically conductive carbon-nanotube composites, addressing white-space needs in 800-V EV powertrains and wind-turbine lightning strike protection.

Metal Replacement Industry Leaders

SABIC

BASF

DuPont

Solvay

TORAY INDUSTRIES INC.,

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: BASF introduced a portfolio of polyamide (PA) and polyphthalamide (PPA) blends for advanced metal replacement in structural parts. These blends offer superior and consistent mechanical properties compared to PA66. Ultramid T7000 exceeds PA66 in stiffness and strength, both in dry and humid conditions, with reduced water absorption ensuring excellent dimensional stability.

- October 2024: SABIC advanced metal replacement in transportation and medical devices with innovative materials. Their LNP ELCRES FST copolymer resins for train interiors provide design flexibility, weight reduction, recyclability, and compliance with fire safety standards. SABIC also showcased 3D-printed rail parts using LNP THERMOCOMP compounds for faster replacements.

Global Metal Replacement Market Report Scope

| Engineering Plastics | Polyamide (PA) |

| Polycarbonate (PC) | |

| Acrylonitrile-Butadiene-Styrene (ABS) | |

| Polyethylene Terephthalate (PET) | |

| Polyphenylene Sulfide (PPS) | |

| Other Engineering Plastics | |

| Composites | Glass Fiber Reinforced Plastics (GFRP) |

| Carbon Fiber Reinforced Plastics (CFRP) | |

| Other Composites |

| Automotive |

| Aerospace and Defense |

| Industrial Equipment |

| Construction |

| Healthcare |

| Consumer Goods and Electronics |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Engineering Plastics | Polyamide (PA) |

| Polycarbonate (PC) | ||

| Acrylonitrile-Butadiene-Styrene (ABS) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyphenylene Sulfide (PPS) | ||

| Other Engineering Plastics | ||

| Composites | Glass Fiber Reinforced Plastics (GFRP) | |

| Carbon Fiber Reinforced Plastics (CFRP) | ||

| Other Composites | ||

| By End-user Industry | Automotive | |

| Aerospace and Defense | ||

| Industrial Equipment | ||

| Construction | ||

| Healthcare | ||

| Consumer Goods and Electronics | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the metal replacement market in 2030?

The metal replacement market is forecast to reach USD 253.29 billion by 2030 at an 8.13% CAGR.

Which material type currently dominates sales?

Engineering plastics lead with 62.45% share in 2024 due to their versatility across automotive, electronics, and healthcare uses.

Why is Asia-Pacific the largest regional consumer?

The region combines high manufacturing capacity, expanding electric-vehicle output, and major investments in engineering-plastic and composite production lines.

How fast is healthcare demand growing?

Healthcare applications are expanding at an 8.78% CAGR as PEEK and other biocompatible polymers replace titanium and stainless steel implants.