Market Overview

| Study Period | 2020 - 2031 |

|---|---|

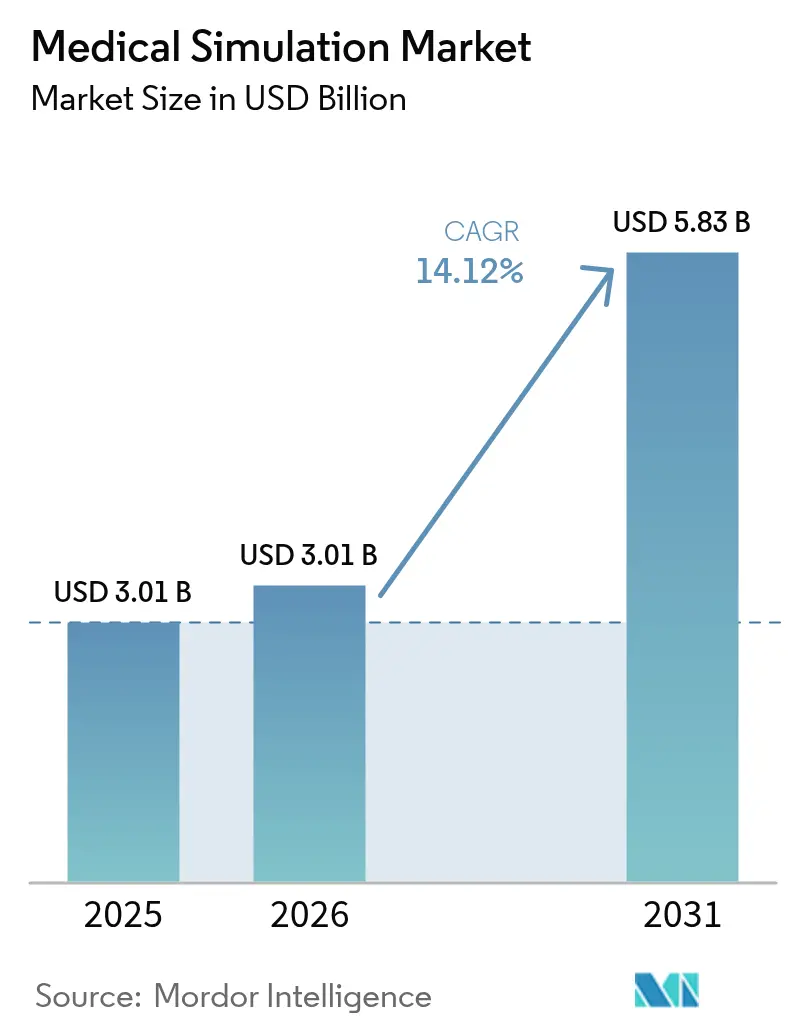

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 5.83 Billion |

| Growth Rate (2026 - 2031) | 14.12% CAGR |

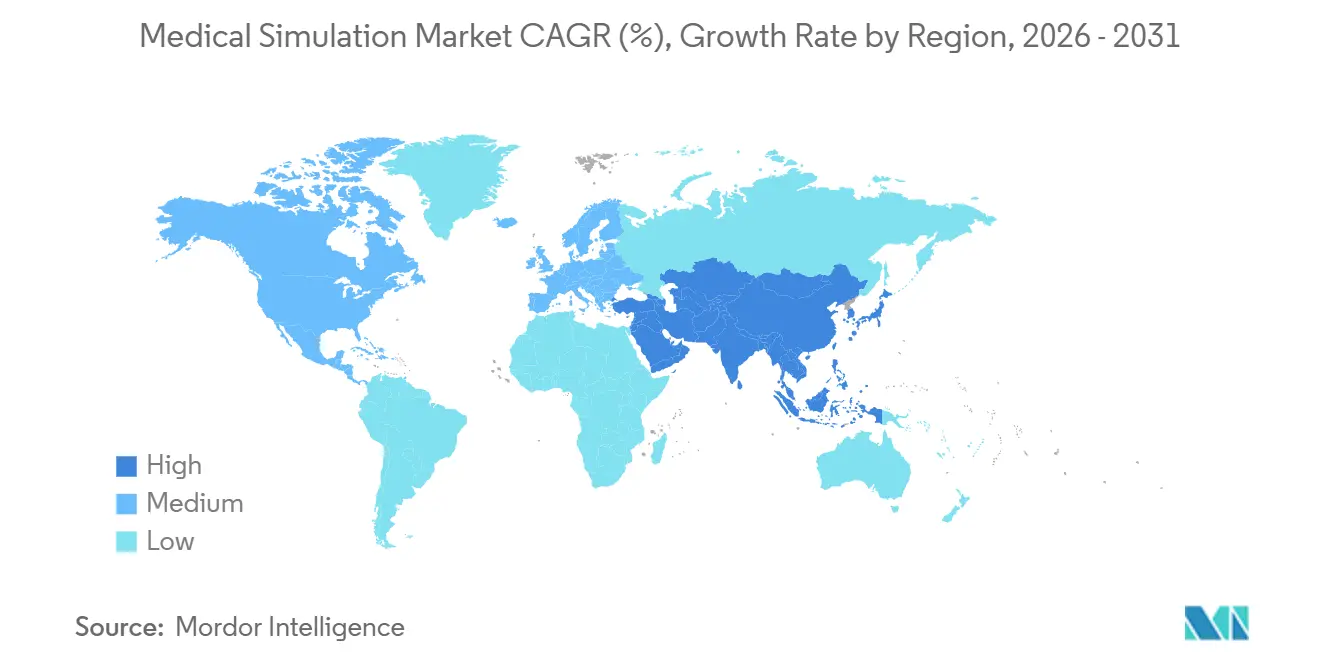

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Medical Simulation Market Analysis by ���ϲ�����

The medical simulation market size expanded from USD 2.64 billion in 2025 to USD 3.01 billion in 2026 and is projected to reach USD 5.83 billion by 2031, registering a CAGR of 14.12% over 2026-2031. Rising global zero-harm mandates, rapid growth in minimally invasive surgery, and AI-based analytics that quantify learner gaps in real time are reshaping how hospitals, academic centers, and defense forces verify clinical competency. By late 2025, more than 450 accredited simulation centers were active worldwide, and 72% of them embedded AI debriefing tools that parse eye-tracking, haptic force, and verbal cues to produce individualized remediation plans[1]Society for Simulation in Healthcare, “Accreditation,” ssih.org. Mandatory documentation of simulation hours, required under the WHO Global Patient Safety Action Plan 2021-2030, has made continuing education a credentialing gate for many procedural specialties[2]World Health Organization, “Global Patient Safety Action Plan 2021-2030,” who.int. Purchasers now favor flexible subscription platforms over capital equipment because cloud analytics link training outcomes to e-credentialing systems, thereby reducing upfront spending. Regionally, North America led with a 43.52% revenue share in 2025, yet Asia-Pacific is the fastest riser, with a forecast 16.12% CAGR, driven by China’s domestic haptic‐simulator approvals and India’s rapid expansion of medical colleges.

Key Report Takeaways

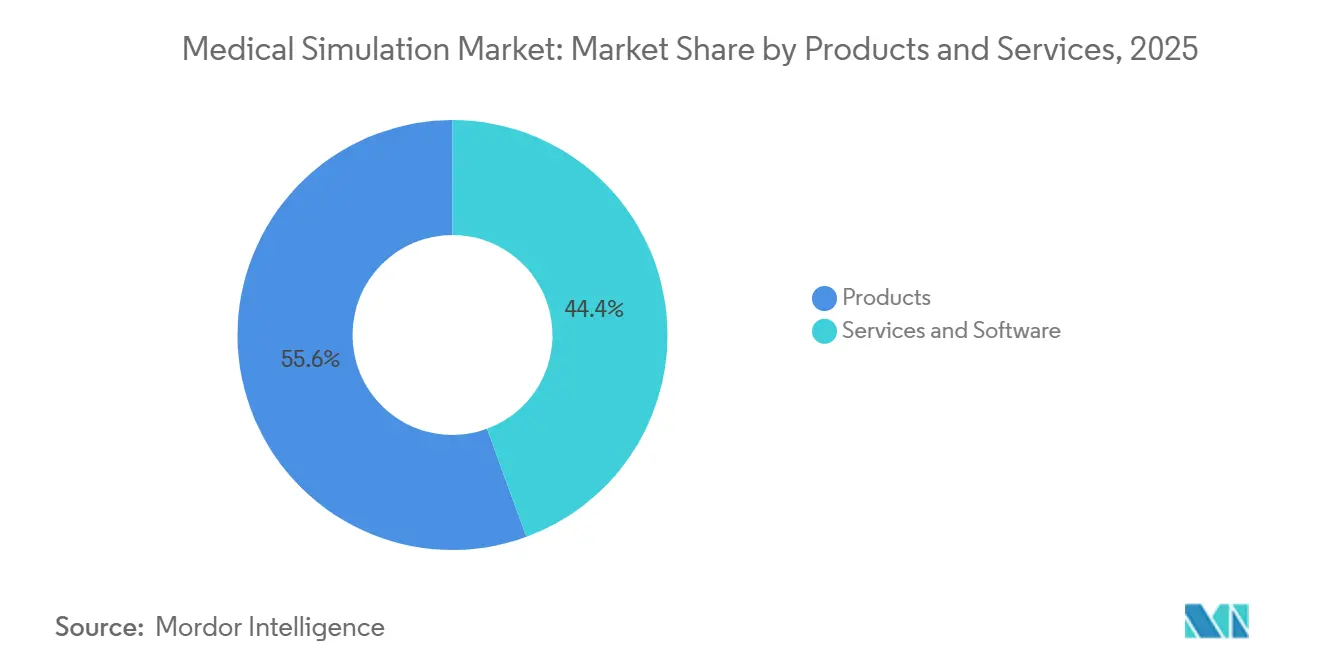

- By products and services, hardware commanded 55.55% revenue share in 2025 while services and software are projected to advance at a 17.85% CAGR through 2031, reflecting the pivot toward subscription-based competency platforms.

- By fidelity, low-fidelity simulators held 44.53% of the medical simulation market share in 2025, whereas high-fidelity systems are forecast to grow at a 15.75% CAGR through 2031.

- By end user, hospitals and surgical centers led with 42.15% revenue in 2025; academic and research institutes are expected to expand at 15.82% CAGR to 2031 as licensure exams embed simulation components.

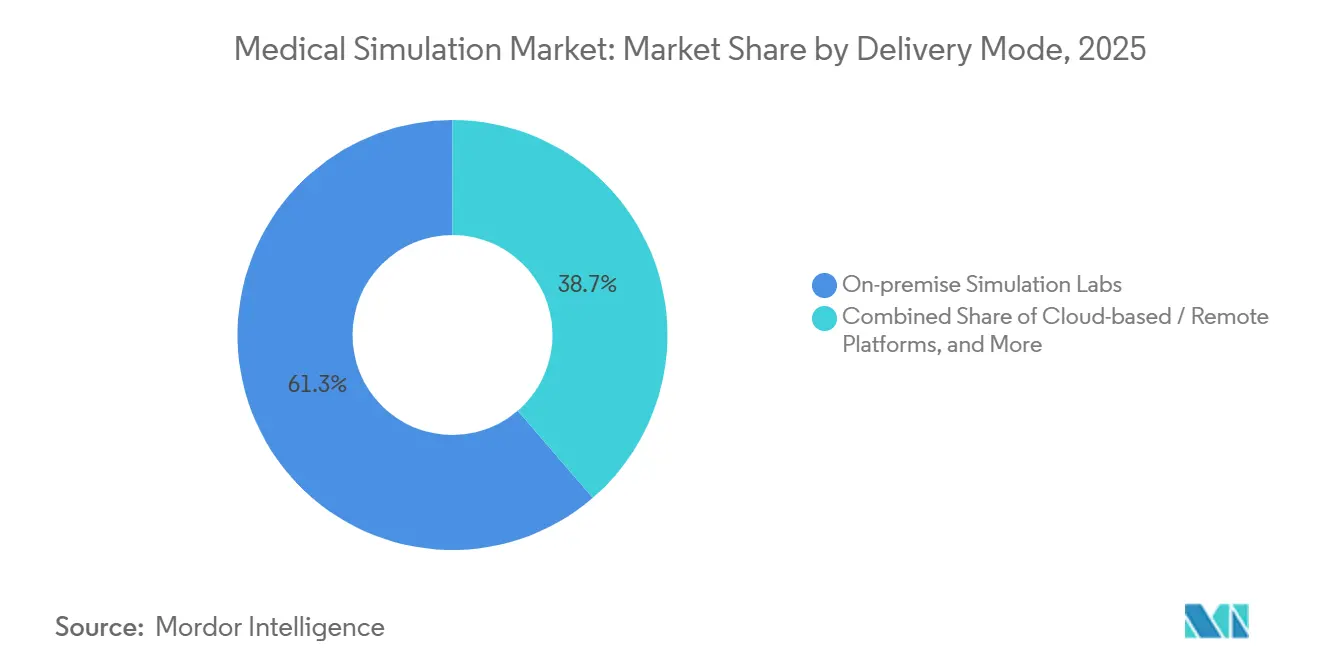

- By delivery mode, on-premises labs captured 61.32% of 2025 spending, yet cloud platforms will surge at an 18.19% CAGR through 2031, as federated learning preserves privacy while benchmarking performance.

- By geography, North America retained leadership with 43.52% share in 2025, but Asia-Pacific will post the fastest 16.12% CAGR through 2031 due to expanded regulatory approvals and new training centers.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Simulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological Advances in Haptics & XR Simulators | +3.2% | Global, with early adoption in North America, Europe, and APAC urban centers | Medium term (2-4 years) |

| Global "Zero-Harm" Patient-Safety Mandates & Reporting Standards | +2.8% | Global, led by WHO member states and Joint Commission-accredited facilities | Long term (≥ 4 years) |

| Growth in Minimally-Invasive & Robotic Procedures | +2.5% | North America, Europe, and APAC (China, India, Japan) | Medium term (2-4 years) |

| Expansion of Simulation Accreditation (SSH, ASPIRE, SESAM) | +1.9% | Global, with concentration in North America, Europe, and Middle East | Long term (≥ 4 years) |

| AI-Driven Competency Analytics Linked to e-Credentialing Systems | +2.3% | North America, Europe, and APAC advanced markets | Short term (≤ 2 years) |

| Carbon-Neutral Remote Simulation Labs Incentivized by Green-Funding Credits | +0.8% | Europe (EU Green Deal), North America (select states), and Oceania | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Technological Advances in Haptics and XR Simulators

Haptic fidelity now reproduces tissue texture and thermal cues, enabling trainees to detect pathologic anatomy during palpation and enhancing the realism of surgical rehearsal. A 2025 controlled study showed residents who practiced on VirtaMed’s ArthroS hip-arthroscopy platform completed their first ten live cases 23% faster and with 31% fewer instrument collisions than peers trained only on videos[3]VirtaMed AG, “ArthroS Hip Arthroscopy Simulator Study,” sciencedirect.com. Mentice’s VIST G7 system, cleared by the FDA in 2024, adds real-time computational fluid dynamics to approximate blood-flow resistance during catheter procedures, helping interventional cardiologists cut fluoroscopy time by 18% after training[4]Mentice AB, “VIST G7 FDA Clearance,” mentice.com. CAE Healthcare and GigXR partnered in 2024 to overlay holographic organs onto physical manikins, creating mixed-reality scenarios that merge tactile cues with CT imaging. These improvements address a long-standing gap in traditional screen-based trainers that lack proprioceptive feedback, enabling deeper muscle memory encoding for surgeons and interventionalists.

Global Zero-Harm Patient-Safety Mandates and Reporting Standards

Patient-safety regulators now treat simulation as risk-mitigation infrastructure rather than an educational luxury. The Joint Commission’s 2024 update requires U.S. hospitals to run quarterly high-fidelity drills for sepsis and code-blue events and to upload performance metrics to an auditable registry[5]Joint Commission, “National Patient Safety Goals 2024,” jointcommission.org. A 2024 ASHRM study linked accredited simulation programs to a 27% reduction in malpractice claims related to procedural errors. In January 2025, 38 national societies signed an SSH consensus committing to make simulation at least 20% of competency assessments for procedural specialties by 2028. Europe follows suit as SESAM and ASPiH published ISO-aligned quality standards that the EU Commission may adopt as prerequisites for device reimbursement. These mandates will keep the medical simulation market on a structural growth path that is less exposed to discretionary budget swings.

Growth in Minimally Invasive and Robotic Procedures

Intuitive Surgical reported an installed base of 11,040 da Vinci systems in Q3 2025, enabling 2.68 million robotic procedures in 2024, outpacing open and laparoscopic volumes combined. The SAGES-endorsed RoSTraC curriculum now mandates 40 hours of simulator training before console use, making simulators gatekeepers for robotic-surgery credentials. ARPA-H launched a USD 150 million Autonomous Implantable Robotics program in November 2025, funding hybrid simulators that teach surgeons to supervise AI-assisted suturing. Fellowship bodies recommend dedicating 25% of operative time to simulation, which drives demand for institution-owned devices versus shared regional centers. As robotic platforms proliferate, hospitals and training centers must scale up simulation capacity, further boosting the medical simulation market.

Expansion of Simulation Accreditation

Global accreditation has moved from voluntary to strategic. SSH listed more than 450 labs in 2025, up 18% from 2024, and its accredited seal is now a differentiator in hospital marketing. SESAM and ASPiH rolled out pan-European quality schemes that tie simulator fidelity to summative assessment validity. The Middle East follows, with ISO 9001:2015-certified centers in Riyadh and Dubai funded under Saudi Vision 2030. Academic programs chase accreditation to strengthen grant applications, creating another pull for high-quality simulation solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Lifecycle Costs of Full-Mission Simulators | -2.1% | Global, with acute impact in LMIC and small-to-midsize hospitals | Short term (≤ 2 years) |

| Funding Gaps in Low-/Middle-Income Countries' Training Budgets | -1.7% | Sub-Saharan Africa, South Asia, and Latin America (excluding Brazil) | Long term (≥ 4 years) |

| Faculty-Training & Curriculum-Integration Complexity | -1.3% | Global, particularly in newly established medical schools | Medium term (2-4 years) |

| Cyber-Security & Learner-Data Privacy Risks in Cloud Platforms | -0.9% | North America, Europe (GDPR jurisdictions), and APAC (China, South Korea) | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

High Capital and Lifecycle Costs of Full-Mission Simulators

Acquisition prices range from USD 250,000 to USD 500,000, plus annual maintenance equal to 12%–15% of the purchase outlay, limited to tertiary centers. Surgical Science disclosed an average price of SEK 1.8 million, yet 40% of prospects deferred purchases for more than 1 year during the 2024 capital freezes. Recurring consumables such as synthetic skin can exceed USD 15,000 per year and are often underestimated at procurement, adding hidden strain to budgets. SaaS alternatives like Mentice’s cloud VIST cost USD 3,500 per user annually but still require reliable broadband, which 35% of rural U.S. counties and 70% of sub-Saharan facilities lack. Leasing spreads payments over five years, but adoption remains below 20%, suggesting that financial innovations alone cannot eliminate sticker shock.

Funding Gaps in Low and Middle-Income Countries

LMICs allocate an average of 1.2% of health budgets to workforce training versus 3.8% in high-income settings, relegating simulation to donor pilots. A 2024 survey of 142 African medical schools found only 18% owned equipment beyond basic CPR manikins, with 62% citing absent budget lines. India mandated labs for every medical college, yet 43% of institutions lacked functional simulators in 2024 audits despite the rule. Currency depreciation raises import costs, as seen when the South African rand dropped in 2024, forcing Cape Town University to postpone a high-fidelity purchase. Maintenance contracts denominated in hard currency intensify the burden and cause equipment to lapse once warranties end.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products and Services: Subscription Software Gains Momentum

Services and software revenues are expected to grow at 17.85% CAGR through 2031, nearly three points faster than the overall medical simulation market. Products accounted for 55.55% of 2025 revenue, led by interventional and surgical simulators. Patient simulators, such as Gaumard HAL S5301, held a minor share, driven by weekly code-blue rehearsals in emergency residencies. Low-cost task trainers serve as entry points for resource-constrained institutions, while VR and haptic devices make up a minor share but will scale as broader adoption of immersive curricula increases.

Moving to services, simulation software licenses accounted for a minor portion of 2025 revenues but face downward pressure from open-source projects such as MedSimAI. Training and consulting services address the faculty gap by certifying instructors in SSH-aligned debriefing. AI-based competency analytics, currently small, are projected to post a greater CAGR through 2031 as hospitals link dashboards to e-credentialing platforms. Accessories and consumables generate sticky recurring income through bundled service contracts. This subscription pivot suggests that revenue composition will tilt toward data and content, reshaping competitive strategy across the medical simulation market.

By Fidelity: High-Fidelity Adoption Accelerates

Low-fidelity simulators accounted for 44.53% in 2025, a sign that affordable task trainers remain indispensable. Medium-fidelity units accounted for a significant share as interim solutions for institutions upgrading capabilities. High-fidelity systems forecast a 15.75% CAGR to 2031 as accreditation bodies require real-time physiologic feedback. The NAEMSP position statement calling for high-fidelity training in every paramedic program will force more than 5,000 U.S. EMS agencies to modernize equipment.

High-fidelity adoption also increases because European standards require summative assessments to use simulators capable of physiologic deterioration. A March 2025 study found that residents trained on high-fidelity devices had 34% higher retention of crisis resource management skills at six months than those trained on medium-fidelity devices. While low-fidelity remains vital in LMICs, the global push for quality and accreditation will continue to pull demand toward advanced platforms, increasing the medical simulation market for premium systems.

By End User: Academic Demand Surges

Hospitals and surgical centers led with a 42.15% share in 2025, anchored by the Joint Commission drill mandates that tie performance to accreditation. Academic and research institutes are the fastest risers at a projected 15.82% CAGR. India’s directive that 15% of final-year MBBS marks be derived from simulation OSCEs forces 706 colleges to rapidly add equipment and services. China’s authorization of domestically built haptic units lowered prices by 40% and enabled 230 universities to purchase laparoscopic trainers.

Military and defense organizations held a minor share in 2025, driven by the U.S. Department of Defense, which trained 1.2 million personnel using high-fidelity manikins for Tactical Combat Casualty Care. Device and pharma firms accounted for 6% as FDA usability rules require human-factors validation. EMS agencies owned 4% but will expand with NAEMSP guidance. These dynamics point to sustained growth across user categories and will more evenly distribute medical simulation market revenues over time.

By Delivery Mode: Cloud Platforms Scale Quickly

On-premise labs accounted for 61.32% of spending in 2025 because tactile feedback remains critical for many surgical skills. Hybrid deployments synchronize manikins with cloud dashboards; CAE Healthcare’s Caesar uploads session data to a HIPAA-compliant cloud while the device stays local. Pure-cloud solutions like SIIM’s browser-based Virtual Hospital cut per-learner costs to USD 150 per year and remove IT overhead, driving an 18.19% CAGR forecast for remote platforms.

Federated environments such as SimulaFed prove that European schools can train shared AI models without transferring raw data, satisfying GDPR constraints. Google Cloud’s Isolator sandbox lets device makers test against synthetic patients in a secure container, accelerating FDA validation work. Latency and privacy remain challenges, yet the efficiency and scale of remote solutions will continue to reallocate spending within the medical simulation market.

Geography Analysis

North America commanded a 43.52% share in 2025 due to 1,200 accredited residency programs and strong defense spending on Tactical Combat Casualty Care that relies heavily on high-fidelity manikins. The Joint Commission’s quarterly drill mandate forces more than 6,200 acute-care hospitals to own or access simulation labs, anchoring steady hardware refresh cycles. Canada integrated simulation into 14 specialty exams in 2024, boosting domestic simulator purchases by 22% year over year.

Asia-Pacific will post the fastest CAGR of 16.12% through 2031. China approved fourteen domestic haptic simulators, which cut unit prices and reduced import barriers. India opened 157 new medical colleges between 2014 and 2024, each required to build simulation facilities, and Japan’s work-style reforms cap resident hours, which incentivizes simulator hours over bedside apprenticeship. Australia and South Korea launched funding to equip regional hospitals, broadening demand beyond capital cities.

Europe benefits from the EU Medical Device Regulation 2017/745, which obliges device makers to conduct human-factors tests using simulators, lifting orders from manufacturers. Germany’s Charité opened a EUR 12 million center with 18 bays and a da Vinci robot, while France’s health authority asked surgical residents to log 60 simulation hours, which 28 medical schools quickly adopted. Middle East and Africa investments top USD 4.2 billion under Vision 2030 plans with newly certified labs in Riyadh and Dubai. Latin America centers on Brazil’s BRL 450 million public-sector program though private schools, which train most physicians, still lack access.

Competitive Landscape

The medical simulation market remains moderately concentrated. The top five vendors, such as Laerdal Medical, CAE Healthcare, Surgical Science, Gaumard Scientific, and Mentice, held a meaningful combined share in 2025, yet specialized niches stay open for new entrants. Laerdal acquired SIMCharacters in February 2025, adding generative-AI virtual patients that improve conversational realism. CAE Healthcare, under Madison Industries since 2024, accelerated its cloud pivot and now sells hybrid deployment packages that link Caesar manikins to remote dashboards.

Surgical Science derived 35% of 2024 revenue from software subscriptions, insulating margins from capital budget cycles. Gaumard continues to upgrade physiologic modeling in its HAL series, while Mentice pushes cloud-native vascular simulation to reach smaller hospitals. White-space innovators such as Inovus Medical and Medical-X offer portable kits priced 50% below incumbents, pursuing volume in cost-sensitive LMICs.

Technology competition concentrates on analytics. TeamVision combines multimodal sensor streams to auto-score non-technical skills and reduce debrief time. Open-source frameworks like MedSimAI lower entry barriers for academic spin-offs. Regulatory moats also matter. Vendors with validated 21 CFR Part 11 workflows win contracts from device makers because they can support FDA submissions. Intuitive Surgical patented machine-learning haptic calibration in 2024 which could differentiate its simulators in a tightening market. Competitive intensity therefore balances between scale advantages of incumbents and agile innovation from newcomers.

Medical Simulation Industry Leaders

Gaumard Scientific Company Inc.

Laerdal Medical

CAE Healthcare

Surgical Science

Mentice

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Chennai-based MediSim VR launched Uttarakhand’s first center of excellence in AI and VR medical simulation at the Himalayan Institute of Medical Sciences, Dehradun.

- March 2025: NVIDIA and GE HealthCare began co-developing autonomous imaging solutions using the new NVIDIA Isaac for Healthcare simulation platform, which blends physics-based sensor models with pretrained anatomy AI.

Global Medical Simulation Market Report Scope

As per the scope of the report, medical simulation is the modern-day methodology for training healthcare professionals through advanced educational technology. Medical simulation is experiential learning that every healthcare professional may need but cannot consistently engage in during real-life patient care.

The segmentation for the medical simulation market includes products and services, fidelity levels, end users, delivery modes, and geographical distribution. The product segment comprises interventional or surgical simulators, including laparoscopic, robotic and endoscopic, and orthopedic simulators. It also includes patient simulators, task trainers, VR, MR, and haptic devices, along with accessories and consumables. The services and software segment covers web-based simulation platforms, simulation software licenses, training and consulting services, and AI-driven competency analytics. Fidelity levels are categorized into high-fidelity, medium-fidelity, and low-fidelity simulations. The end-user segment includes academic and research institutions, hospitals and surgical centers, military and defense entities, medical device and pharmaceutical firms, and emergency medical services (EMS). Delivery modes are segmented into on-premise simulation labs, cloud-based or remote platforms, and hybrid deployments. Geographically, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers the value (in USD) for the above segments.

By Products & Services

| Products | Interventional / Surgical Simulators | Laparoscopic |

| Robotic & Endoscopic | ||

| Orthopaedic | ||

| Patient Simulators | ||

| Task Trainers | ||

| VR / MR & Haptic Devices | ||

| Accessories & Consumables | ||

| Services & Software | Web-based Simulation Platforms | |

| Simulation Software Licences | ||

| Training & Consulting Services | ||

| AI-based Competency Analytics |

By Fidelity

| High-Fidelity |

| Medium-Fidelity |

| Low-Fidelity |

By End User

| Academic & Research Institutes |

| Hospitals & Surgical Centres |

| Military & Defence Organisations |

| Medical-Device & Pharma Companies |

| Emergency Medical Services (EMS) |

By Delivery Mode

| On-premise Simulation Labs |

| Cloud-based / Remote Platforms |

| Hybrid Deployments |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Products & Services | Products | Interventional / Surgical Simulators | Laparoscopic |

| Robotic & Endoscopic | |||

| Orthopaedic | |||

| Patient Simulators | |||

| Task Trainers | |||

| VR / MR & Haptic Devices | |||

| Accessories & Consumables | |||

| Services & Software | Web-based Simulation Platforms | ||

| Simulation Software Licences | |||

| Training & Consulting Services | |||

| AI-based Competency Analytics | |||

| By Fidelity | High-Fidelity | ||

| Medium-Fidelity | |||

| Low-Fidelity | |||

| By End User | Academic & Research Institutes | ||

| Hospitals & Surgical Centres | |||

| Military & Defence Organisations | |||

| Medical-Device & Pharma Companies | |||

| Emergency Medical Services (EMS) | |||

| By Delivery Mode | On-premise Simulation Labs | ||

| Cloud-based / Remote Platforms | |||

| Hybrid Deployments | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large will the medical simulation market be by 2031 ?

Forecasts point to USD 5.83 billion at a 14.12% CAGR from 2026 to 2031, reflecting strong uptake of cloud platforms and high-fidelity devices.

Which segment is growing fastest within medical simulation ?

Services and software subscriptions show the highest 17.85% CAGR as institutions shift from hardware ownership to data-rich competency platforms.

Why is Asia-Pacific posting the quickest growth in medical simulation ?

Domestic manufacturing approvals in China and mandatory labs in India reduce costs and expand capacity, driving a 16.12% regional CAGR.

What limits wider adoption of high-fidelity simulators ?

Capital costs up to USD 500,000 plus recurring consumables and limited faculty skills remain the main constraints, especially in LMICs.

How are AI analytics changing simulation training ?

Multimodal engines now auto-score skills, cut instructor debrief time, and link results to credentialing databases, shifting demand toward software services.

Page last updated on: