Liquor Confectionery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

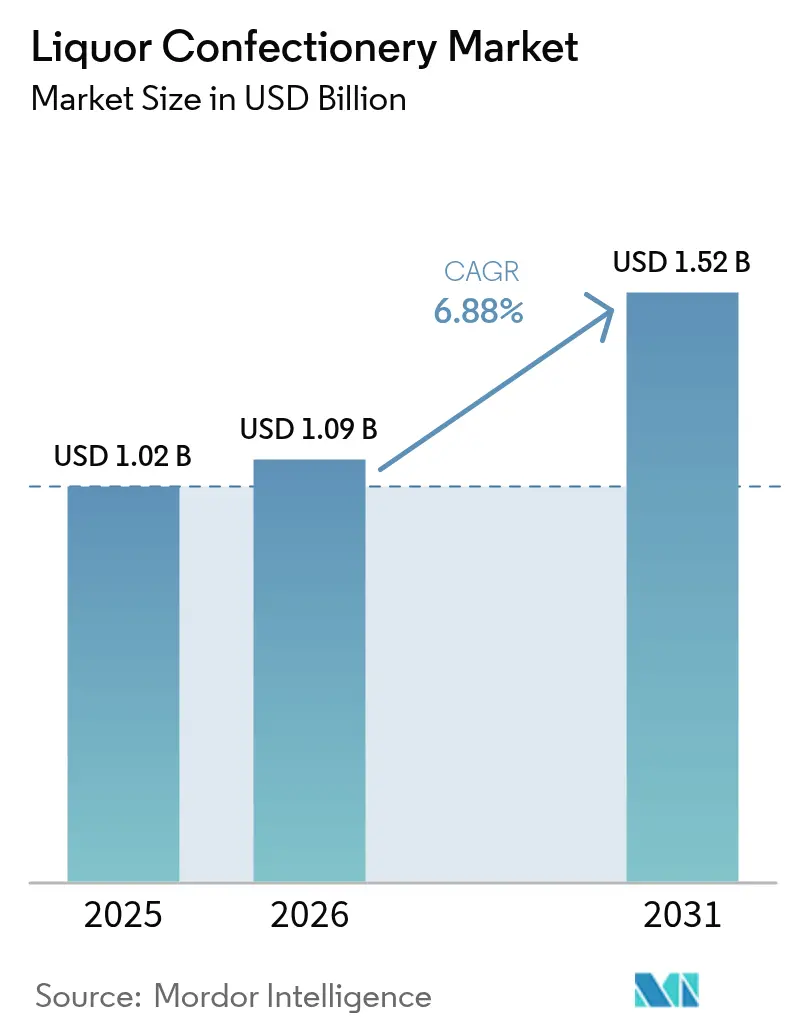

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Liquor Confectionery Market Analysis by ���ϲ�����

The Liquor confectionery market size is expected to increase from USD 1.02 billion in 2025 to USD 1.09 billion in 2026 and reach USD 1.52 billion by 2031, growing at a CAGR of 6.88% over 2026-2031. This growth highlights a transition from niche gifting to more widespread premium indulgence. Consumers are increasingly choosing spirit-infused chocolates, which command higher prices compared to traditional assortments. The integration of craft-spirits culture with artisanal chocolate-making strengthens demand and provides resilience against declines in mass-market volumes. Additionally, the expansion of e-commerce has improved visibility for small-batch product launches. Specialty retailers and direct-to-consumer platforms are driving market engagement by hosting tasting events and offering subscription boxes that emphasize product provenance. Manufacturers are protecting their margins through strategic collaborations that distribute marketing costs and by utilizing barrel-aged cocoa techniques, ensuring compliance with alcohol-label standards while preserving flavor quality.

Key Report Takeaways

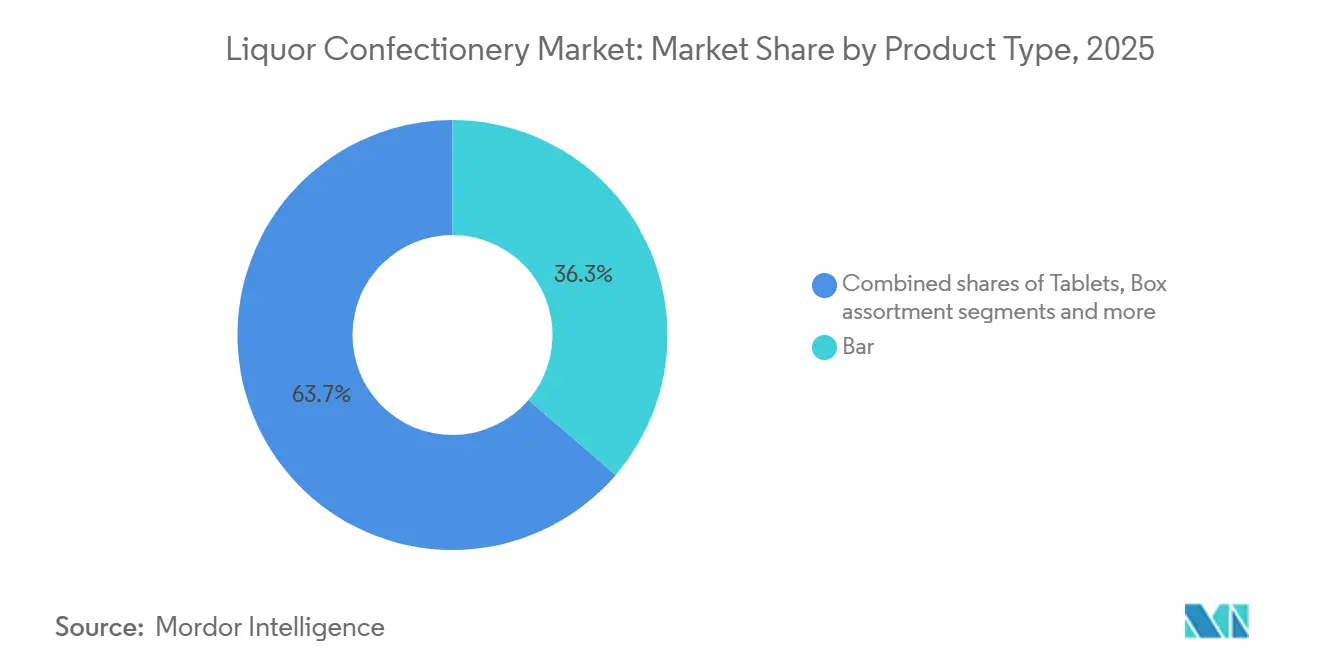

- By product type, bar formats captured 36.28% Liquor confectionery market share in 2025 and are on track for an 8.11% CAGR through 2031.

- By alcohol base, whisky and bourbon led with 38.12% revenue share in 2025, while tequila and mezcal are projected to expand at a 7.41% CAGR over 2026-2031.

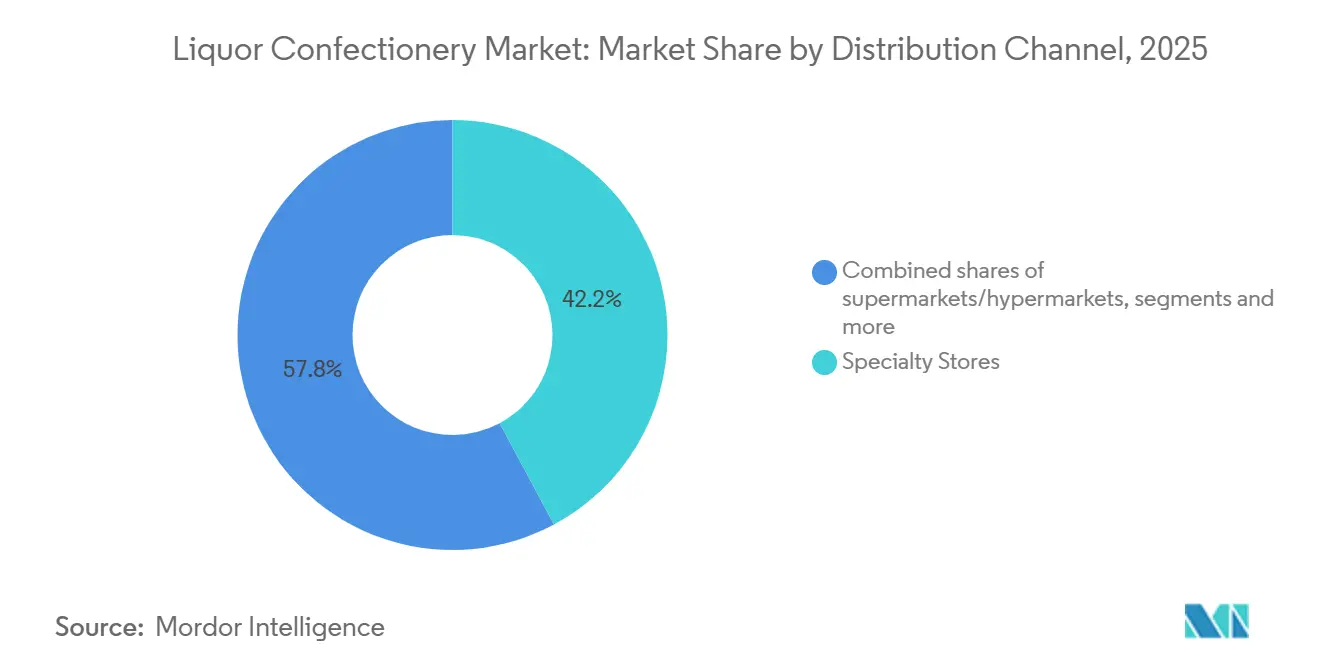

- By distribution channel, specialty stores held 42.18% of the Liquor confectionery market size in 2025, and online retail is the fastest-growing route at 8.36% CAGR to 2031.

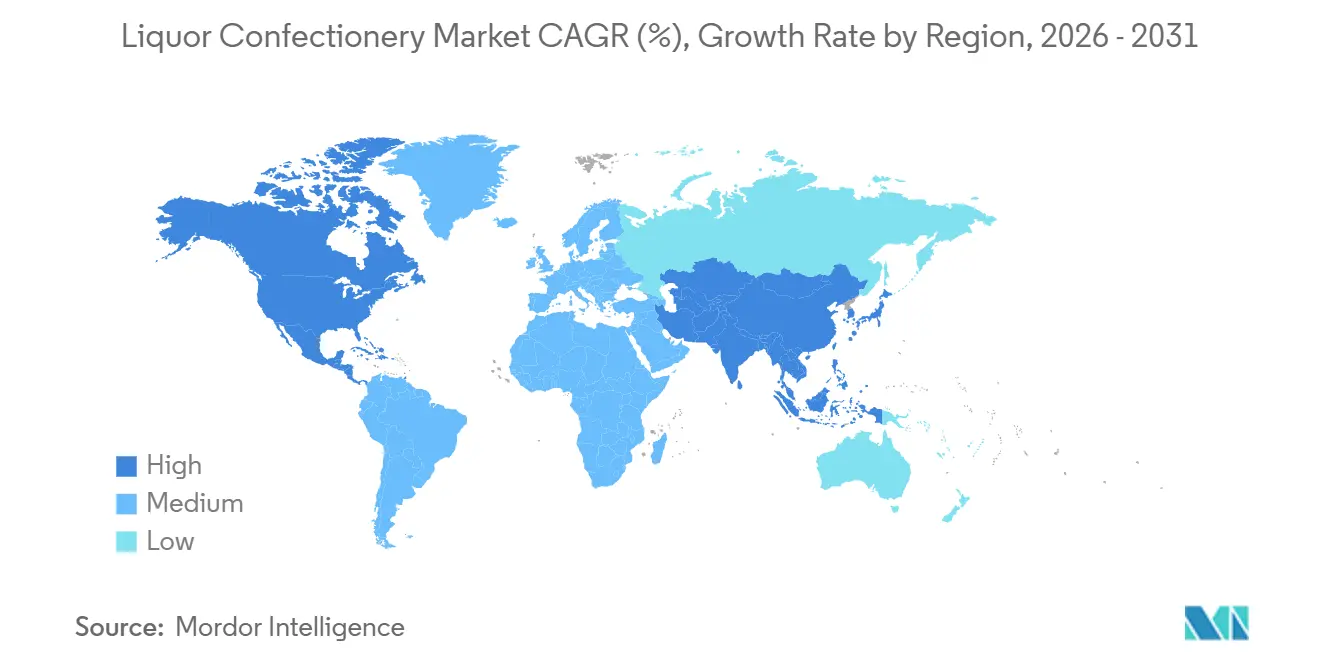

- By geography, Europe accounted for 45.22% of 2025 demand, whereas North America is advancing at an 8.24% CAGR across the same forecast window.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liquor Confectionery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for premium and luxury confectionery products | +1.8% | Global, with concentration in Europe and North America | Medium term (2-4 years) |

| Increasing popularity of gourmet chocolates and artisanal confectioneries | +1.5% | Europe, North America, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Growing demand for unique and innovative liquor-infused flavors | +1.3% | North America, Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Expansion of the gifting culture and luxury gifting occasions | +1.2% | Global, particularly Middle East, Asia-Pacific, Europe | Short term (≤ 2 years) |

| Increasing availability of liquor confectionery in specialty retail outlets | +0.9% | North America, Europe, select Asia-Pacific cities | Medium term (2-4 years) |

| Collaborations between chocolatiers and liquor manufacturers for new offerings | +0.7% | North America and Europe, with spillover to South America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising consumer preference for premium and luxury confectionery products

Spending on premium confectionery has remained strong, even as other luxury categories experience a slowdown. Consumers increasingly perceive high-quality chocolate as an affordable indulgence, particularly during periods of economic uncertainty. Liquor-infused chocolates are enhancing this trend by combining the distinct characteristics of spirits with chocolate's unique flavors. This allows manufacturers to price these products between EUR 50-80 per kilogram, significantly higher than the EUR 25-35 range for non-alcoholic premium assortments. This willingness to pay a premium reflects a shift in consumer preferences, with buyers, especially millennials and Gen Z, prioritizing sensory complexity and storytelling over quantity. Social media has further accelerated this trend by spotlighting artisanal brands. For these younger generations, confectionery has transitioned from being a simple snack to a lifestyle statement. Additionally, rising disposable incomes are driving the demand for premium and luxury confectionery products. According to the U.S. Bureau of Economic Analysis (BEA), the annual total value of disposable personal income in the United States reached USD 21,917.7 billion[1]Source: U.S. Bureau of Economic, "National Income and Product Accounts", bea.gov.

Increasing popularity of gourmet chocolates and artisanal confectioneries

As consumers increasingly prioritize transparency and craftsmanship, artisanal production methods, such as single-origin cocoa sourcing, small-batch tempering, and hand-finishing, have evolved from niche practices to widely adopted industry standards. This growing demand for authenticity and quality has significantly benefited the liquor confectionery segment. The infusion of alcohol into chocolate requires precise techniques, including meticulous moisture control and careful flavor balancing, which only highly skilled chocolatiers can consistently execute. In regions like North America and Europe, the rise of bean-to-bar producers has further strengthened the supply ecosystem. This ecosystem now enables the creation of exclusive, limited-edition spirit collaborations. These collaborations often involve small production runs, typically yielding only 500-1,000 units, yet they generate substantial brand visibility and appeal to collectors, driving demand for such premium offerings.

Growing demand for unique and innovative liquor-infused flavors

Flavor innovation has expanded from traditional whisky and rum ganaches to include tequila, mezcal, amaro, and barrel-aged spirits, reflecting the influence of cocktail culture trends. Alcohol consumption is increasing globally among both men and women, supporting market growth. The World Health Organization reports that men consumed an average of 8.2 liters per capita, while women consumed 2.2 liters[2]Source: World Health Organization, "Alcohol", who.int. . Tequila-infused chocolates are gaining popularity as agave spirits grow their presence in premium on-premise channels. Manufacturers are utilizing añejo and reposado expressions to incorporate oak, vanilla, and caramel notes that pair well with dark chocolate. Mezcal variants attract adventurous consumers with their smoky, earthy profiles, offering a distinct alternative to conventional options. This diversification reduces dependence on whisky-focused SKUs and enables brands to meet occasion-specific demand, such as mezcal chocolates for experiential gifting and bourbon variants for traditional holidays. Additionally, the trend supports geographic customization, with European producers focusing on cognac and armagnac infusions, while North American brands highlight bourbon and rye.

Expansion of the gifting culture and luxury gifting occasions

Liquor confectionery sales experience a significant surge during Q4, driven by heightened demand associated with holidays, year-end celebrations, and the Lunar New Year. These occasions play a pivotal role in boosting annual revenue for the category. In Middle Eastern markets, gifting during Ramadan and Eid is particularly prominent; however, the presence of alcohol in such products creates challenges. To address this, manufacturers often develop non-alcoholic flavor variants or face import restrictions in these regions. Additionally, the premiumization of corporate gifting has gained momentum, with businesses allocating larger budgets per recipient to enhance client relationships. This shift has elevated liquor confectionery from being a novelty item to a strategic gifting option, particularly within the financial services and professional services sectors, where fostering strong client connections is a priority.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory constraints on alcohol in food | -1.4% | Global, particularly stringent in Middle East, parts of Asia, and select US states | Long term (≥ 4 years) |

| Limited consumer awareness or acceptance in certain conservative markets | -0.9% | Middle East, South Asia, parts of Southeast Asia | Medium term (2-4 years) |

| Health concerns related to alcohol consumption affecting buying behavior | -0.7% | North America, Europe, health-conscious urban centers globally | Short term (≤ 2 years) |

| Volatility and fluctuation in raw material prices such as cocoa and alcohol | -1.1% | Global, with acute impact in regions dependent on imported cocoa | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Regulatory constraints on alcohol in food

Multinational brands face compliance challenges due to differing alcohol content thresholds for food products across jurisdictions. In the U.S., the Food and Drug Administration permits alcohol in confectionery products without specific labeling if the content is below 0.5% by weight. However, many liquor-infused chocolates exceed this limit, requiring compliance with Alcohol and Tobacco Tax and Trade Bureau (TTB) regulations, including age verification at the point of sale. In the European Union, Regulation (EC) No 1169/2011 requires allergen labeling and alcohol content disclosure for products with more than 1.2% ABV. This increases labeling complexity and restricts product placement in certain retail environments. In contrast, Middle Eastern markets either ban or heavily restrict foods containing alcohol, effectively excluding conventional liquor confectioneries from these regions. As a result, brands must develop alcohol-free variants that replicate traditional spirit profiles. These regulatory challenges fragment product portfolios and drive up SKU management costs, as brands must create region-specific formulations and packaging.

Limited consumer awareness or acceptance in certain conservative markets

Cultural and religious norms in regions such as Asia, the Middle East, and North Africa restrict the growth of liquor confectionery, even in areas where regulations technically permit low-alcohol food products. Educating consumers is crucial in these markets, as many are unaware that chocolates typically contain only 2-5% alcohol by weight, far lower than alcoholic beverages. Additionally, processes like cooking or ganache preparation can further reduce the active alcohol content. Brands entering these conservative markets often adopt a premium positioning strategy, focusing on gifting occasions to avoid associations with casual alcohol consumption. However, this approach limits their volume potential. The challenge becomes even greater in markets where chocolate is still a developing category, as the inclusion of alcohol introduces an additional layer of unfamiliarity, slowing adoption.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bar Formats Lead Premium Convenience

In 2025, bar formats represented 36.28% of total revenue and are anticipated to grow at a CAGR of 8.11% through 2031. This growth highlights the increasing consumer preference for single-serve convenience and portion control in the premium confectionery market. Bars, with their familiar formats, are especially popular in specialty retail and airport duty-free settings. Here, shoppers are attracted to the perceived quality conveyed through weight, packaging, and highlighted ingredients. Compared to box assortments, bars have a less complex production process. This enables manufacturers to achieve economies of scale in molding and wrapping while incorporating features like alcohol-infused ganache centers or liqueur-soaked inclusions. Tablets, while holding a smaller market share, appeal to consumers looking for shareable formats for social occasions. Box assortments, despite slower growth, continue to be a key choice for gifting occasions. Other formats, such as truffles, pralines, and seasonal novelties, address niche demands but face higher production costs and shorter shelf life.

Recent advancements in bar formats emphasize dual-texture designs. These combine crunchy elements, such as caramelized nuts and toffee, with liquor-infused ganache, enhancing sensory appeal and supporting a price range of EUR 8-12 for a 100-gram bar. Additionally, manufacturers are exploring barrel-aged chocolate. This process involves storing cocoa nibs in used whisky or rum casks, allowing them to absorb residual spirit flavors without adding liquid alcohol. This technique effectively navigates regulatory challenges while delivering an authentic spirit profile. Initially popular in craft chocolate circles, this method is now expanding into premium mass-market products. Meanwhile, tablets and box assortments continue to dominate holiday sales.

By Alcohol Base: Whisky Dominance Meets Agave Disruption

In 2025, whisky and bourbon infusions represented 38.12% of the revenue, leveraging consumers' familiarity with these spirits and their complementary pairing with dark chocolate. Rum-based variants, associated with tropical flavors and holiday traditions, held a secondary share. Liqueur infusions, such as amaretto, Grand Marnier, and Baileys, appeal to consumers seeking a sweeter option compared to straight spirits. Wine and champagne chocolates, positioned as premium celebratory or romantic gifts, face challenges in standing out from non-alcoholic fruit ganaches due to their lower alcohol content and delicate flavors.

Tequila and mezcal variants are growing at a 7.41% CAGR, the fastest among alcohol bases, driven by younger consumers' increasing interest in the cultural significance and complex flavors of agave spirits. Premium tequila shipments to the U.S. have risen, with añejo and extra-añejo varieties driving value growth as consumers transition from mixto to 100% agave products. This premiumization trend in spirits is directly influencing the confectionery market. Brands are utilizing tequila's earthy and peppery notes to create dark chocolate pairings that appeal to adventurous consumers. Mezcal, with its smoky profile, enables even bolder flavor combinations, often paired with chili, sea salt, or citrus to enhance complexity. The growth of the agave category is further supported by successful collaborations, where craft chocolatiers partner with boutique tequila producers to launch limited-edition releases, generating social media buzz and collector interest.

By Distribution Channel: Specialty Stores Anchor Experience, E-commerce Scales Reach

In 2025, specialty stores represented 42.18% of sales, providing curated selections, knowledgeable staff, and engaging experiences. These attributes support premium pricing and enhance customer education. These channels are essential for liquor confectionery, offering opportunities for sampling, storytelling, and personalized recommendations, services that mass-market retailers find challenging to replicate. Additionally, specialty stores function as brand-building platforms, enabling manufacturers to introduce limited editions and collect feedback before broader market launches. Although supermarkets and hypermarkets hold a smaller share due to limited shelf space and difficulties in highlighting premium products in competitive pricing environments, some are adapting by creating specialized sections like "world foods" or "premium gifting" to target higher-margin confectionery.

Online retail channels are growing at the fastest rate among distribution methods, with a CAGR of 8.36%. This growth is driven by direct-to-consumer subscription models and the ability to offer a wider variety of products than physical stores. E-commerce allows brands to collect customer data, personalize marketing, and reduce dependence on wholesale margins. However, it requires investments in fulfillment infrastructure and temperature-controlled shipping to prevent chocolate from melting. Increasing internet penetration further supports online sales. By 2025, approximately 6 billion people, or about three-quarters of the global population, were using internet, according to the International Telecommunication Union (ITU)[3]Source: International Telecommunication Union (ITU), "ITU's Facts and Figures 2025", itu.int . E-commerce is particularly effective for limited-edition collaborations and seasonal launches, using scarcity messaging and countdown timers to create urgency. While other channels, such as duty-free shops, hotel minibars, and corporate gifting platforms, cater to specific occasions, they lack the scale of specialty retail or the rapid growth of online sales.

Geography Analysis

In 2025, Europe accounted for 45.22% of the market share, driven by the long-standing chocolate-making traditions of Belgium, Switzerland, Germany, and France, along with a cultural acceptance of alcohol-infused confections. Belgian pralines with liqueur centers, a staple since the early 20th century, have fostered strong consumer familiarity, encouraging trials and supporting premium pricing. The region benefits from its proximity to premium spirit producers such as Scotch whisky, cognac, and Irish whiskey, as well as regulatory frameworks that allow alcohol in food with minimal restrictions. However, growth is slowing as the market matures and younger Europeans consume less confectionery, leading to a decline in per capita consumption.

North America is experiencing the fastest regional growth, with an 8.24% CAGR, fueled by the expansion of craft spirits, premiumization trends, and increasing consumer interest in flavor pairings. As of 2024, the United States hosts over 2,600 craft distilleries, offering chocolatiers ample opportunities for authentic local collaborations. While Mexico's rich chocolate heritage and tequila production suggest strong potential for liquor-infused confections, the market remains underdeveloped. In the Asia-Pacific region, countries like China, Japan, and Singapore are leading the adoption of luxury confections. However, cultural unfamiliarity with alcohol-infused sweets and regulatory challenges are slowing market penetration. The Middle East and Africa show contrasting trends: the UAE and Saudi Arabia are driving demand for luxury gifting with non-alcoholic premium variants, while alcohol-containing products face distribution restrictions.

South America is an emerging market for liquor confectionery. Urban centers in Brazil and Argentina, influenced by European culinary traditions and supported by a growing middle class, are showing early signs of growth. The region's rum and cachaça production presents collaboration opportunities. However, local chocolate manufacturing infrastructure remains underdeveloped compared to Europe and North America, leading to a reliance on imports that increase retail prices. Additionally, regulatory frameworks vary significantly, with some countries imposing high tariffs on alcohol-infused imports, while others maintain more open policies.

Competitive Landscape

The liquor confectionery market is moderately fragmented, with established premium brands such as Lindt and Sprüngli, Toms Gruppen, and Neuhaus dominate the market by leveraging their strong brand equity, extensive distribution networks, and vertical integration into retail operations. These companies capitalize on decades of expertise in chocolate-making and utilize global supply chains to ensure consistent product quality across various regions. This consistency is particularly critical due to the technical precision required for infusing alcohol into chocolates and managing their shelf life effectively. On the other hand, smaller entrants in the market often collaborate with well-known spirit brands to enhance their credibility and gain access to broader distribution channels. This collaborative approach creates a unique ecosystem that contrasts with the highly competitive, zero-sum dynamics typically observed in the mass-market confectionery segment.

Strategic trends within the sector reveal a clear bifurcation. Some players treat liquor confectionery as a premium extension of their existing product lines, focusing on volume and scalability. Meanwhile, craft producers position alcohol infusion as a central element of their brand identity, emphasizing artisanal quality and niche appeal. Prominent industry players like Mars and Ferrero have chosen to enter the liquor confectionery market selectively through acquisitions rather than organic development. This strategy reflects their acknowledgment of the distinct challenges associated with this segment, including the complexities of formulation, adherence to regulatory requirements, and the need for specialized channel management.

Technology adoption is a key driver of innovation in the liquor confectionery market. Companies are increasingly utilizing blockchain technology to ensure transparency in cocoa sourcing and provenance, while IoT sensors are being deployed to maintain temperature-controlled logistics, ensuring product integrity throughout the supply chain. Additionally, e-commerce platforms are being leveraged to deliver personalized customer experiences. Brands are using consumer data to recommend tailored spirit-chocolate pairings and to predict gifting occasions, enhancing customer engagement. Emerging disruptors in the market include subscription box services that curate monthly selections from multiple artisanal producers. These services aggregate demand, making it easier for small-batch chocolatiers to reach a broader audience while significantly reducing their customer acquisition costs, which is a critical advantage for producers with limited marketing resources.

Liquor Confectionery Industry Leaders

-

Toms Gruppen

-

Ferrero Group

-

Neuhaus

-

Mars Inc.

-

Lindt and Sprüngli

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ferrero has committed an investment of USD 445 million in Ontario as part of its global expansion strategy. This significant financial commitment will support the introduction of a new product, which will be produced on the company’s first manufacturing line established in the province. This initiative underscores Ferrero's dedication to strengthening its presence in the region and expanding its global footprint.

- October 2024: Swiss Miss collaborated with Hotel Tango Distillery to introduce Cocoa-infused Toasted Marshmallow Bourbon, priced at USD 27.99, demonstrating cross-category innovation between confectionery and spirits brands to create premium limited-edition offerings.

- October 2024: Manchester Distillery launched Sweetie Chocolate Liqueur, expanding their portfolio into confectionery-inspired spirits that bridge traditional liqueur categories with modern flavor preferences and premium positioning strategies.

Global Liquor Confectionery Market Report Scope

Liquor confectionery refers to sweet treats infused with alcohol. The liquor confectionery market report is segmented by product type, alcohol base, distribution channel, and geography. By product type, the market is segmented into bar, tablets, box assortment, and others. By alcohol base, the market is segmented into whisky/bourbon, rum, liqueurs, tequila/mezcal, and wine/champagne. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail, and others. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market forecasts are provided in terms of value (USD) and volume (Tons).

| Bar |

| Tablets |

| Box Assortment |

| Others |

| Whisky / Bourbon |

| Rum |

| Liqueurs |

| Tequila / Mezcal |

| Wine / Champagne |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Bar | |

| Tablets | ||

| Box Assortment | ||

| Others | ||

| By Alcohol Base | Whisky / Bourbon | |

| Rum | ||

| Liqueurs | ||

| Tequila / Mezcal | ||

| Wine / Champagne | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast will premium liquor chocolates grow in North America by 2031?

The segment is projected to post an 8.24% CAGR between 2026 and 2031 on the back of craft-distillery collaborations and rising e-commerce reach.

Which alcohol base is expanding most rapidly in liquor chocolates?

Tequila and mezcal variants are advancing at a 7.41% CAGR, outpacing traditional whisky options as agave spirits gain popularity.

Why are specialty stores critical for liquor-infused confectionery sales?

They deliver curated experiences, sampling, and education that justify premium prices and currently account for 42.18% of global sales.

What is the biggest regulatory hurdle for international expansion?

Divergent alcohol-in-food thresholds force brands to manage multiple recipes and labels, raising compliance costs and slowing rollouts.

Page last updated on: