Lip Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.55 Billion |

| Market Size (2031) | USD 4.62 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

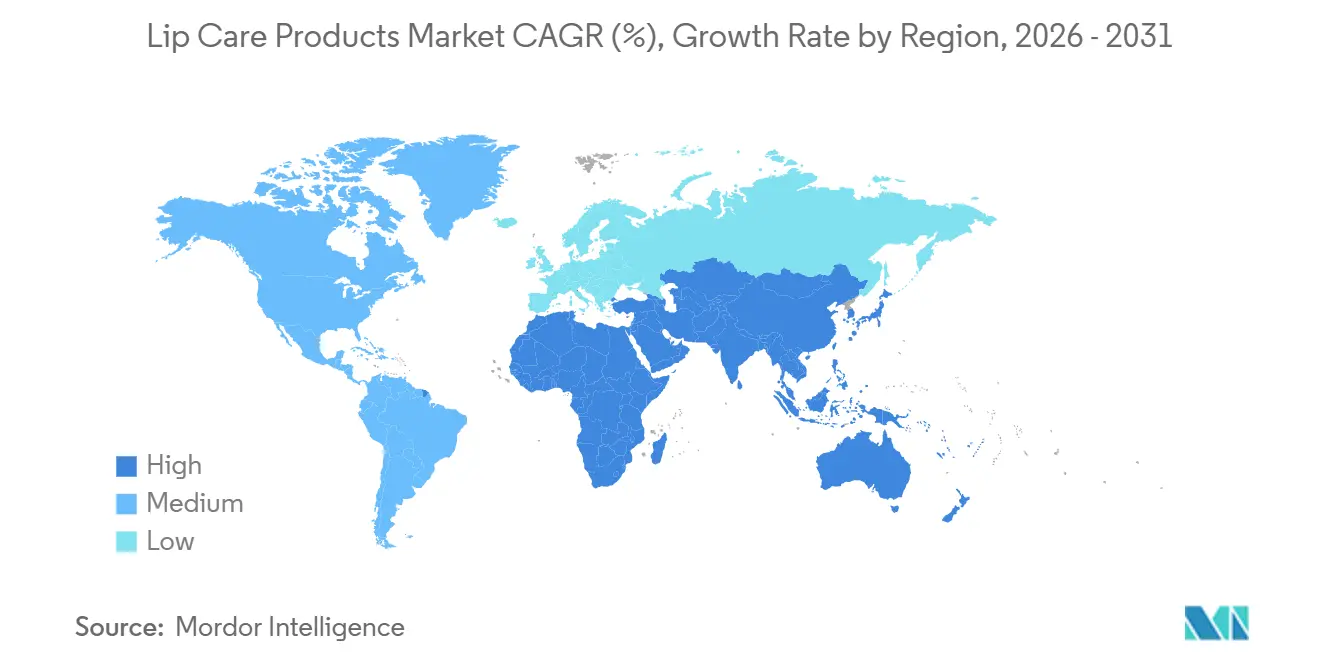

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Lip Care Products Market Analysis by ���ϲ�����

The lip care products market size is expected to increase from USD 3.38 billion in 2025 to USD 3.55 billion in 2026 and reach USD 4.62 billion by 2031, growing at a CAGR of 5.41% over 2026-2031. The sector is shifting from basic balms toward multifunctional treatments that mix hydration, sun protection, anti-aging actives, and color in formats that range from sticks to overnight masks. Consumers favor exfoliating scrubs and tinted hybrids that create a “skincare-for-lips” routine, a pattern reinforced by K-beauty influences and dermatologist advocacy. Clean-beauty demands are accelerating natural and organic launches, while tariff pressure and raw-material swings push brands to optimize costs through vertical integration. Digital commerce, refillable packaging, and halal certification together reshape competitive strategies as incumbents adopt omnichannel playbooks and indie labels harness social media to gain reach.

Key Report Takeaways

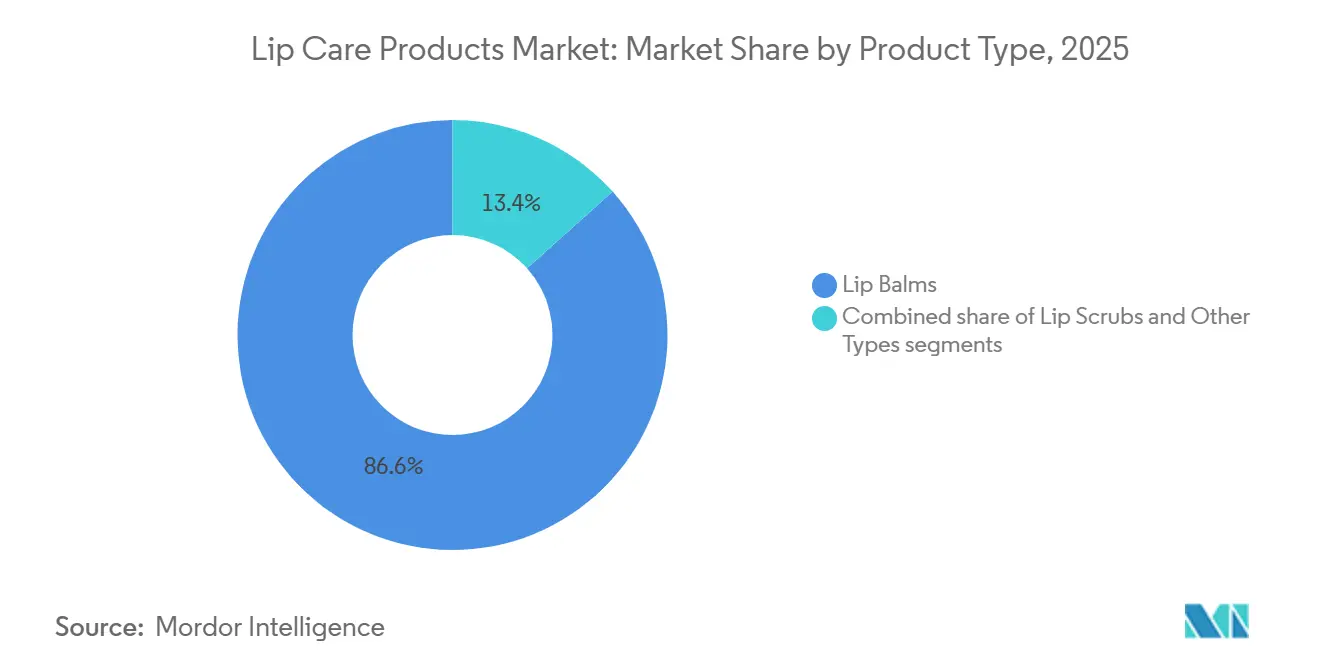

- By product type, lip balms held 86.62% of the lip care products market share in 2025, whereas lip scrubs are forecast to grow at a 7.16% CAGR through 2031.

- By nature, conventional items commanded 84.66% revenue in 2025, yet natural and organic formats are advancing at a 6.90% CAGR to 2031.

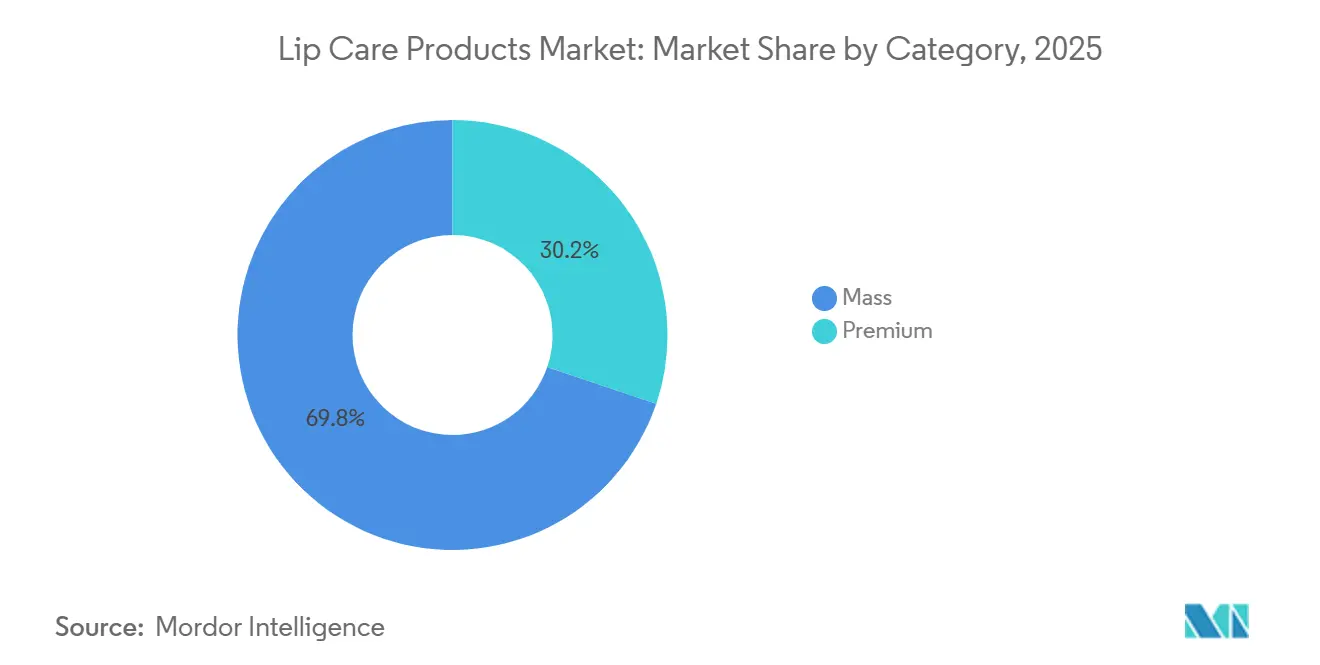

- By category, mass-market lines captured 69.81% of 2025 sales, while premium offerings are projected to expand at a 6.72% CAGR to 2031.

- By packaging, tubes contributed 45.93% of sales in 2025, whereas jars are on track for a 6.59% CAGR owing to overnight masks and refill systems.

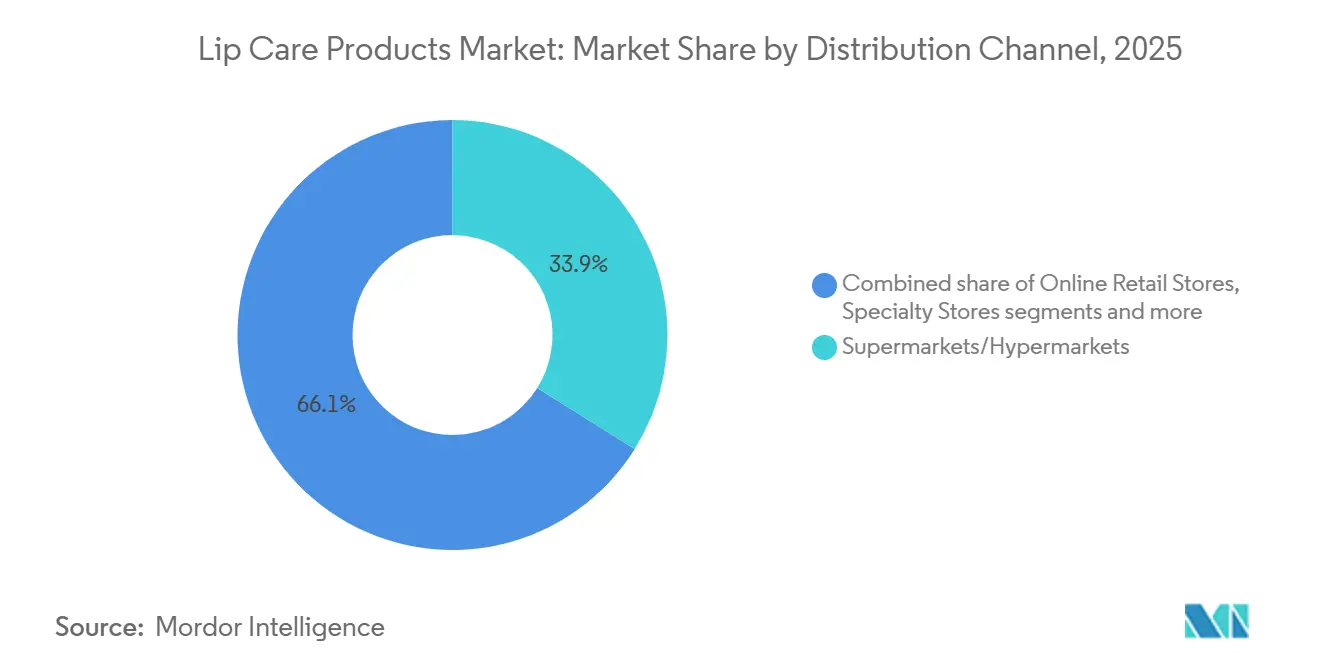

- By distribution channel, supermarkets and hypermarkets delivered 33.90% of the 2025 volume, but online retail is rising at a 6.18% CAGR on the back of direct-to-consumer brands.

- By geography, Asia-Pacific generated 36.89% of 2025 revenue, and the Middle East and Africa segment is set to grow at a 6.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lip Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on lip health, appearance, and everyday grooming routines | +1.2% | Global, with pronounced uptake in Asia-Pacific and North America | Medium term (2-4 years) |

| Strong demand for multifunctional lip products offering hydration, SPF protection, and anti-aging benefits | +1.0% | Global, particularly North America, Europe, and Middle East and Africa | Medium term (2-4 years) |

| Growing preference for natural, organic, vegan, and cruelty-free formulations | +0.9% | North America, Europe, and urban centers in Asia-Pacific | Long term (≥ 4 years) |

| Rapid adoption of hybrid "care-meets-color" balms, oils, and tinted treatments | +0.8% | Asia-Pacific (K-beauty influence), North America, Europe | Short term (≤ 2 years) |

| Expanding male grooming segment boosting demand for men-specific lip care solutions | +0.5% | Asia-Pacific (Singapore, South Korea, Japan), North America, Middle East | Medium term (2-4 years) |

| Increasing interest in customized and personalized lip care products | +0.4% | North America, Europe, and affluent urban markets in Asia-Pacific | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising consumer focus on lip health, appearance, and everyday grooming routines

Consumer emphasis on lip health, appearance, and grooming routines is reshaping the lip care products market, as lips become integral to daily skincare and beauty regimens. In 2024, according to the Office for National Statistics (UK), UK households allocated approximately GBP 37.9 billion to personal care products and services, reflecting a readiness to invest in grooming essentials [1]Source: Office for National Statistics (UK), "Consumer Trends: Q4 2024," ons.gov.uk . This trend has elevated products like lip balms, scrubs, and tinted treatments from occasional use to everyday necessities. Established brands such as Vaseline and Nivea have diversified their offerings to include targeted repairing and moisturizing sticks, embedding lip care into daily skincare routines. Concurrently, beauty-focused companies like Fenty Beauty and Maybelline are integrating conditioning ingredients into glosses and tinted balms, addressing consumer demand for both aesthetic enhancement and long-term lip health. Rising awareness of environmental factors, including sun and pollution, has further driven demand for SPF and barrier-protective formats, emphasized by brands like La Roche-Posay and Aquaphor. Social media trends promoting multi-step lip routines and innovations in clean, multifunctional formulations, such as Burt’s Bees’ natural wax-based balms and Laneige-style overnight masks, are also contributing to market growth. North America and Europe, with their advanced beauty markets, continue to lead in premiumization trends, influencing global adoption and product positioning.

Strong demand for multifunctional lip products offering hydration, SPF protection, and anti-aging benefits

Consumer demand for multifunctional lip products that combine hydration, SPF protection, and anti-aging benefits is reshaping the lip care market. This shift reflects a preference for streamlined solutions addressing multiple concerns, driven by daily exposure to environmental stressors. Basic lip balms are evolving into advanced formulations incorporating ingredients like hyaluronic acid and ceramides for intense hydration, alongside broad-spectrum UV filters to combat dryness, chapping, and premature aging. Brands such as Cetaphil Protective Lip Balm exemplify this trend with SPF 50 lip balms formulated with Ethylhexyl Methoxycinnamate, meeting regulatory standards while aligning with minimalist skincare routines. Anti-aging actives, including peptides, are increasingly incorporated to target fine lines and improve elasticity, appealing to consumers seeking products that deliver visible results. For example, Lotus Herbals offers peptide-infused balms that strengthen the skin barrier while providing hydration and protection against pollution and sun damage. Social media and the "skinification" trend further amplify the adoption of products like Laneige's lip serums and overnight treatments, which repair and rejuvenate during sleep. Additionally, clean formulations using natural waxes instead of petrolatum enhance ingredient bioavailability without compromising texture. Regional climates, particularly in the Middle East and Africa, are influencing the development of climate-adaptive, multifunctional products designed for year-round use.

Growing preference for natural, organic, vegan, and cruelty-free formulations

Consumer demand for natural, organic, vegan, and cruelty-free formulations is reshaping the lip care market, as individuals prioritize ethical sourcing and skin-safe ingredients over synthetic alternatives. This shift aligns with a growing focus on lip health, supported by 2024 data from the National Sanitation Foundation, which indicates that 74% of buyers prefer organic ingredients in personal care products [2]Source: National Sanitation Foundation, "74% of Consumers Consider Organic Ingredients Important in Personal Care Products," nsf.org. As a result, there is a notable transition from petrolatum-based balms to plant-derived options that deliver effective hydration. Brands such as Hurraw! are capitalizing on this trend with premium vegan balms made from organic raw materials like sunflower seed oil and candelilla wax, addressing consumer demand for cruelty-free and long-lasting moisture solutions. Multifunctional formulations incorporating hydration, SPF protection, and natural antioxidants like non-GMO vitamin E are gaining traction, particularly among consumers seeking anti-aging benefits and bee-free waxes. Social media further amplifies this trend, showcasing self-care routines with products like Pacifica’s vegan tinted balms, which combine organic shea butter with color. Innovations such as Ethique’s home-compostable vegan lip balms with jojoba and cocoa butter address climate-adaptive needs while reducing plastic waste. Regional premiumization in North America and Europe is driving global adoption, blending natural efficacy with luxury textures to meet the expectations of organic-conscious consumers.

Expanding male grooming segment boosting demand for men-specific lip care solutions

The male grooming segment is witnessing significant growth, driving demand for lip care products tailored specifically for men. As men increasingly incorporate lip health into their daily skincare and grooming routines, the focus on hydration, protection, and clean formulations is extending to gender-specific solutions. Products such as matte, unscented balms are gaining traction, addressing urban pollution and outdoor exposure while prioritizing functionality over aesthetic shine. For instance, Jack Black's Intense Therapy Lip Balm combines shea butter and vitamin E to deliver repair, anti-aging benefits, and SPF protection, appealing to men seeking alternatives to generic options. In Japan, data from Hot Pepper Beauty Academy highlights a rise in average monthly spending on skincare cosmetics among men, from JPY 1,344 in 2022 to JPY 1,586 in 2024, reflecting a growing willingness to invest in specialized lip care [3]Source: Hot Pepper Beauty Academy, "Beauty Census Second Half of the Year 2024," hba.beauty.hotpepper.jp . Social media influencers are normalizing these routines, particularly among younger demographics, linking preferences for vegan and organic products to men's skincare lines like Brickell Men's Products. Additionally, innovations such as peptide-infused balms from brands like Patricks LB1 Matte-Finish Hydrating Lip Balm address climate-adaptive protection and active lifestyles. Regional premiumization in Asia-Pacific and North America is further driving global launches, fostering masculine branding that integrates clean ingredients with functionality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Difficulties in sourcing consistent-quality natural and organic ingredients | -0.6% | Global, with acute pressure in North America and Europe | Medium term (2-4 years) |

| Consumer concerns over irritation, allergies, and product sensitivity risks | -0.5% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Raw material supply chain volatility affecting costs and availability | -0.7% | Global, with spillover from West Africa (shea, cocoa) to all regions | Short term (≤ 2 years) |

| Rising sustainability requirements driving higher packaging and compliance expenses | -0.6% | Europe (EU PPWR mandates), North America, and multinational brands globally | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Difficulties in sourcing consistent-quality natural and organic ingredients

Sourcing consistent-quality natural and organic ingredients presents significant challenges for the lip care industry, as fluctuating availability and variability disrupt the production of clean beauty formulations. Consumers increasingly demand vegan and cruelty-free options, driven by trends in everyday grooming and multifunctional products. Brands like Burt’s Bees face difficulties due to reliance on organic beeswax and peppermint sourced from regions prone to seasonal shortages, leading to formulation changes that may compromise hydration and SPF performance. Climate variability and regional biodiversity limitations further complicate the supply chain for natural actives such as shea butter and jojoba, delaying the introduction of anti-aging peptides and barrier-protective hybrids sought after in men’s grooming products. Ethical sourcing requirements for alternatives like candelilla wax add regulatory complexities, slowing innovation in climate-adaptive solutions for pollution-exposed routines. Social media-driven consumer expectations amplify scrutiny, as variability in plant chemistry impacts product texture and efficacy, challenging brands to maintain premium quality without synthetic stabilizers. Diversifying suppliers mitigates single-source risks but increases costs for organic certifications, pressuring price-sensitive male consumers expanding beyond basic balms. Additionally, regulatory measures like the European Union Deforestation Regulation (EUDR) on palm derivatives limit ingredient options, further restraining the shift from petrolatum-based products to natural, multifunctional solutions.

Consumer concerns over irritation, allergies, and product sensitivity risks

Concerns over irritation, allergies, and product sensitivity risks are impacting consumer trust in lip care products, particularly as even natural and multifunctional formulations can cause adverse reactions. For example, organic lip balms from brands like EOS, containing ingredients such as limonene and castor oil, have been linked to allergic contact dermatitis, resulting in swelling, redness, and cracking, which discourages repeat purchases despite hydration and SPF benefits. Sourcing challenges for consistent organic ingredients and variability in plant extracts, such as propolis or balsam of Peru, further heighten sensitivity risks, especially in vegan and cruelty-free options. These issues complicate the development of men’s grooming products that prioritize matte, unscented formats for pollution-exposed skin. Additionally, flavorings and preservatives in tinted balms and overnight masks exacerbate irritation, slowing the adoption of anti-aging peptides and barrier hybrids amid heightened scrutiny on social media. Chemical sunscreens in SPF-infused products also provoke contact cheilitis, conflicting with premiumization trends in North America and Europe, where ethical sourcing already strains formulation stability. While innovations like fragrance-free petrolatum alternatives are gaining traction, rigorous patch-testing is essential to rebuild consumer confidence. Overall, allergy concerns and supply inconsistencies are limiting experimentation with multifunctional naturals, constraining growth in the lip care category.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Scrubs and Masks Carve Niche Beyond Balm Dominance

Lip balms represent the largest share of the lip care products market, accounting for 86.62% of the projected 2025 revenue. These products are widely recognized as daily-use essentials, addressing consumer needs for hydration, SPF protection, and overall lip health. Their affordability and availability through supermarkets, pharmacies, and convenience stores drive broad adoption, including among male grooming segments and clean beauty consumers. Despite challenges in sourcing natural ingredients, lip balms remain integral to everyday grooming routines. Brands like Carmex, offering medicated relief in classic stick formats, further reinforce their role in routine integration while minimizing irritation risks for most users.

Lip scrubs, with a projected annual growth rate of 7.16% through 2031, are emerging as a fast-growing segment. These products complement lip balms by enabling multi-step care routines inspired by facial skincare practices. They address dryness and flakiness, preparing lips for the application of masks or tints, and appeal to consumers seeking vegan and organic formulations. Products like Fresh Sugar Lip Polish exemplify this trend, offering gentle exfoliation that smooths lips and enhances the absorption of anti-aging serums. This segment is also contributing to premiumization while addressing consumer concerns about allergies and synthetic irritants.

By Nature: Organic Variants Gain Share Amid Clean-Beauty Momentum

Conventional formulations are expected to account for the largest share, commanding 84.66% of the revenue in 2025. This is driven by mass-market brands focusing on cost efficiency, shelf stability, and broad retail distribution, catering to everyday grooming needs and the growing male consumer segment. These products rely on synthetic emollients like dimethicone and phenyl trimethicone, preservatives such as phenoxyethanol and approved parabens, and petroleum-derived waxes including petrolatum and microcrystalline wax. These ingredients ensure reliable hydration, SPF integration, and consistent texture, making them widely available in supermarkets and pharmacies. The stability of these formulations supports multifunctional demands, enabling brands like ChapStick to deliver consistent performance in tinted sticks that minimize irritation risks for regular users while addressing sourcing challenges in organic alternatives.

Natural and organic variants are projected to grow at a CAGR of 6.90% through 2031, driven by increasing demand for ingredient transparency, allergen avoidance, and environmental sustainability. These products align with consumer preferences for vegan, cruelty-free options and multi-step skincare routines. Despite challenges such as price volatility for shea butter and cocoa butter, higher organic certification costs, and extended lead times, these products command higher per-unit prices and foster loyalty among consumers upgrading to premium offerings like scrubs and masks. Brands such as Lush exemplify this trend with 100% natural lip scrubs and balms, addressing sensitivity concerns while offering premium formulations for daytime protection and overnight recovery.

By Category: Premium Segment Expands as Consumers Trade Up for Efficacy

Mass-market products accounted for the largest share, capturing 69.81% of the projected 2025 revenue. These products dominate through supermarkets, hypermarkets, pharmacies, and drugstores, offering price points below USD 5 per unit. Their accessibility and high replenishment frequency cater to everyday grooming routines. Lip balms contributed 86.62% of revenue, while conventional formulations accounted for 84.66%. Broad distribution supports the expansion of male grooming products and multifunctional hydration solutions without premium costs. Brands like Blistex leverage this trend with medicated sticks containing cooling menthol, strategically placed at checkout counters to encourage impulse purchases and address routine protection needs against pollution and dryness. Mass-market brands sustain their leadership through aggressive promotional pricing, impulse-purchase placement, and a wide range of SKUs, including flavor variants and seasonal packaging. These strategies help counteract margin pressures from tariff-driven cost inflation and economic trade-down risks, ensuring product availability in pharmacies for men-specific matte balms and basic SPF hybrids.

Premium offerings are projected to grow at a CAGR of 6.72% through 2031, driven by consumer preferences for dermatologist-endorsed formulations, luxury heritage branding, and clinically substantiated claims, with price points ranging from USD 15 to USD 50 per unit. This growth aligns with the organic segment, expected to grow at 6.90%, and the scrub segment, forecasted to expand at 7.16%. These categories appeal to clean-beauty consumers prioritizing natural ingredients, anti-aging peptides, and intensive masks over synthetic alternatives. Brands such as La Mer and Sisley Paris exemplify this trend with high-end products that integrate seamlessly into multi-step skincare routines, promoting long-term lip health and addressing allergen concerns.

By Packaging Type: Jars Gain Traction as Masks and Refills Proliferate

Tubes held the largest share, accounting for 45.93% of the projected 2025 revenue, driven by their portability, hygienic no-finger application, and squeeze-and-twist dispensing that minimizes product waste. Their slim design fits easily into handbags and travel kits, supporting convenience-focused purchases in mass-market and pharmacy channels. Meanwhile, jars are anticipated to grow at an annual rate of 6.59% through 2031, fueled by the rising popularity of overnight lip masks and refillable premium systems that emphasize intensive care routines. Scoopable textures in jars convey indulgence and treatment efficacy, encouraging consumers to associate this format with deeper performance benefits. Brands like Laneige have popularized jar-based lip sleeping masks, reinforcing the connection between packaging, sensory appeal, and perceived premium value. Additionally, refillable concepts align jars with sustainability trends by promoting reuse over single-use disposables.

Tins and alternative formats, such as sticks and compacts, cater to niche markets shaped by lifestyle positioning and impulse buying. Metal tins offer durability and portability, particularly for balms marketed to outdoor enthusiasts who value rugged packaging. Stick formats enable one-handed application and high visibility at checkout, supporting convenience-driven purchases in supermarkets and travel retail. Regulatory changes, such as the European Union Packaging and Packaging Waste Regulation, are driving brands to adopt mono-material tubes made from polypropylene or polyethylene, simplifying recycling and reducing contamination risks. Packaging innovation is increasingly influenced by hygiene preferences, indulgence cues, refill systems, and regulatory compliance.

By Distribution Channel: Online Retail Surges as DTC Brands Bypass Traditional Gatekeepers

Supermarkets and hypermarkets held the largest share of distribution in 2025, accounting for 33.90%. These channels benefit from high foot traffic, strategic impulse placement near checkouts, and extensive geographic reach, supporting mass-market volume. Their scale advantages make them essential for mainstream lip balms and entry-level treatments aimed at convenience-driven purchases. Pharmacies and drugstores also play a significant role by reinforcing clinical credibility, positioning medicated and dermatologist-recommended lip treatments alongside skincare and over-the-counter products to appeal to efficacy-focused shoppers. Specialty beauty stores, including Ulta Beauty, provide curated discovery spaces with testers and advisors, attracting consumers willing to pay premiums for prestige products and exclusive launches.

Online retail channels are projected to grow at an annual rate of 6.18% through 2031, driven by direct-to-consumer expansion, social commerce integration, and influencer-led discovery on platforms such as TikTok, Instagram, and YouTube. Digitally native brands increasingly leverage these platforms to build community trust before expanding offline. For instance, Rhode entered Sephora in autumn 2025, showcasing a hybrid omnichannel strategy where prestige retail partnerships enhance reach while direct-to-consumer channels maintain margin control and access to first-party customer data. In the Middle East and North Africa, a strong mall culture coexists with rapid e-commerce growth, particularly in the United Arab Emirates and Saudi Arabia, where online content significantly influences purchasing decisions. Distribution strategies are evolving toward omnichannel models, where digital discovery, clinical credibility, and experiential retail work in tandem.

Geography Analysis

Asia-Pacific held the largest share of 36.89% in the projected 2025 revenue for lip care products. This dominance is attributed to humid climates that drive product usage and encourage repeat purchases, alongside rising disposable incomes in India and Southeast Asia. Urbanization and the growth of digital commerce in India have improved access to both mass-market and premium lip care products, while regulatory frameworks are enhancing quality standards. The influence of K-beauty trends has accelerated the adoption of hybrid products that combine hydration, tint, and gloss in a single offering. Brands like Innisfree have capitalized on this trend by aligning their multifunctional lip balms with regional preferences. In China, compliance requirements from the National Medical Products Administration, including pre-market registration and ingredient safety assessments, add complexity but reinforce consumer trust. The ASEAN Cosmetic Directive simplifies market entry across key countries, though halal certification requirements from bodies like JAKIM and Majelis Ulama Indonesia provide access to ethically conscious consumers.

The Middle East and Africa region is expected to grow at the fastest annual rate of 6.47% through 2031. This growth is driven by increasing demand for halal-certified cosmetics, rapid urbanization in GCC states, and climate extremes that necessitate barrier-repair formulations. Hot and arid conditions, coupled with prolonged sun exposure, have increased the demand for long-wear lip products with SPF and hydration-locking ingredients such as hyaluronic acid and ceramides. In markets like the United Arab Emirates, a strong mall culture coexists with growing digital adoption, supporting omnichannel distribution for both premium and mass-market brands. Climate-induced dryness from air-conditioning has further amplified the preference for occlusive and moisture-sealing formulations, while halal certification enhances trust by aligning ingredient transparency with religious compliance.

North America and Europe remain significant markets due to their mature retail infrastructure and stringent regulatory standards, which often set global benchmarks. The European Union Cosmetics Regulation (EC) No 1223/2009 mandates comprehensive safety assessments, restricts over 1,600 substances, and requires the disclosure of 26 fragrance allergens, increasing formulation complexity while bolstering consumer confidence. In North America, brands like Burt's Bees leverage their natural product positioning within this regulatory framework to build trust and loyalty. South American markets, including Brazil, Argentina, and Colombia, benefit from rising middle-class incomes and deeper digital commerce penetration, though regulatory fragmentation and import tariffs pose challenges. In Africa outside MENA, urbanization and mobile commerce are creating long-term potential in countries like South Africa and Nigeria, though infrastructure gaps and currency volatility currently temper growth prospects.

Competitive Landscape

The global lip care products market exhibits moderate consolidation, with multinational corporations utilizing their scale, distribution networks, and substantial research and development budgets to maintain their positions in both mass-market and premium segments. Companies such as Unilever, L'Oréal, Beiersdorf, Kenvue, and EOS capitalize on extensive retail partnerships and global supply chains to ensure widespread product availability, catering to diverse consumer demographics. Their advanced research and development capabilities enable them to adapt swiftly to regulatory changes, sustainability requirements, and emerging trends like tinted oils and hybrid care-plus-color balms, fostering both brand loyalty and innovation within the category.

Digitally native and direct-to-consumer brands complement this competitive landscape by utilizing social commerce, influencer collaborations, and ingredient transparency to attract younger consumers, particularly millennials and Gen Z. Brands such as Rhode and Bite Beauty demonstrate the effectiveness of influencer-driven storytelling, online-first product launches, and community engagement in building trust around functional benefits, natural ingredients, and clean-label claims. By bypassing traditional retail channels, these brands reduce operational costs, reinvest in digital marketing, and retain first-party consumer data, enabling them to respond more quickly to evolving preferences, such as refillable systems and care-plus-color innovations.

Growth opportunities are particularly evident in hybrid product formats and regionally tailored offerings, including halal-certified products targeting consumers in the Middle East and Southeast Asia. Premium refillable systems appeal to sustainability-conscious consumers seeking reduced waste and extended product lifecycles, while tinted care formulations combine functional performance with cosmetic appeal. Brands that successfully integrate multifunctional benefits with ethical certifications can achieve differentiation in mature markets and drive adoption in emerging regions with stringent compliance requirements. The interplay of conglomerate scale, digital agility, and innovative product formats continues to shape competitive advantage in the global lip care products market.

Lip Care Products Industry Leaders

-

Unilever PLC

-

L’Oréal SA

-

Beiersdorf AG

-

Kenvue Inc.

-

EOS Products LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Reliance Retail's beauty platform, Tira, expanded into the color cosmetics segment with the launch of its first makeup product, the Tira Lip Plumping Peptint. The product was formulated with shea butter, murumuru butter, a peptide complex, hyaluronic acid, and vitamins C and E. The Peptint was offered in nine shades and featured Tira's signature packaging, a soft applicator, and a collectible charm. The range was vegan, cruelty-free, and free from parabens and mineral oils.

- October 2025: Bath & Body Works expanded its beauty product range with the introduction of a new Lip Oil collection. The available shades included Crystal Clear, Bubblegum Pink, Honey Glaze, and Rosy Cheeks. This lightweight, non-sticky lip oil provided a tinted, sheer shine with buildable color. Each product was enriched with coconut oil to nourish and condition the lips.

- September 2025: Suroskie, a prominent brand in the self-care and beauty industry, announced the launch of its new product, Dessert Drip Lip Oils. This product provided a subtle tint with each application while nourishing the lips with a blend of carefully selected ingredients. The formulation included Shea Butter, Turmeric Oil, Sepilift DPHP, Almond Oil, and Jojoba Oil, designed to deliver effective lip care.

Global Lip Care Products Market Report Scope

Lip care products refer to the different sets of products that are primarily used to treat chapped and dried lips and moisturize them. Along with this, these products are also used to lighten dark lips.

The global lip care products market is segmented by type, distribution channel, and geography. By type, the market is segmented into lip balms, lip scrubs, and other types. Lip balms are further segmented into lip masks and lip salves. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies/drug stores, specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, South America, Asia-Pacific, the Middle East, and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Lip Balms | Lip Masks |

| Lip Salve | |

| Lip Scrubs | |

| Other Types (Lip Serums, Oils, Powders, Creams) |

| Conventional |

| Natural/Organic |

| Mass |

| Premium |

| Tubes |

| Tins |

| Jars |

| Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Lip Balms | Lip Masks |

| Lip Salve | ||

| Lip Scrubs | ||

| Other Types (Lip Serums, Oils, Powders, Creams) | ||

| By Nature | Conventional | |

| Natural/Organic | ||

| By Category | Mass | |

| Premium | ||

| By Packaging Type | Tubes | |

| Tins | ||

| Jars | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies/Drug Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the lip care products market be by 2031?

The market is projected to reach USD 4.62 billion by 2031, expanding at a 5.41% CAGR from 2026 to 2031.

Which product type leads sales in lip care?

Lip balms dominate with 86.62% of 2025 revenue, though lip scrubs are the fastest-growing subsegment.

Which region is the fastest-growing for lip products?

The Middle East and Africa are forecast to grow at a 6.47% CAGR through 2031, driven by halal demand and climate needs.

Why are premium lip products gaining share?

Consumers pay for proven efficacy, cleaner ingredients, and luxury packaging, pushing premium sales to grow at a 6.72% CAGR through 2031.

Page last updated on: