Lice Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 1.65 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

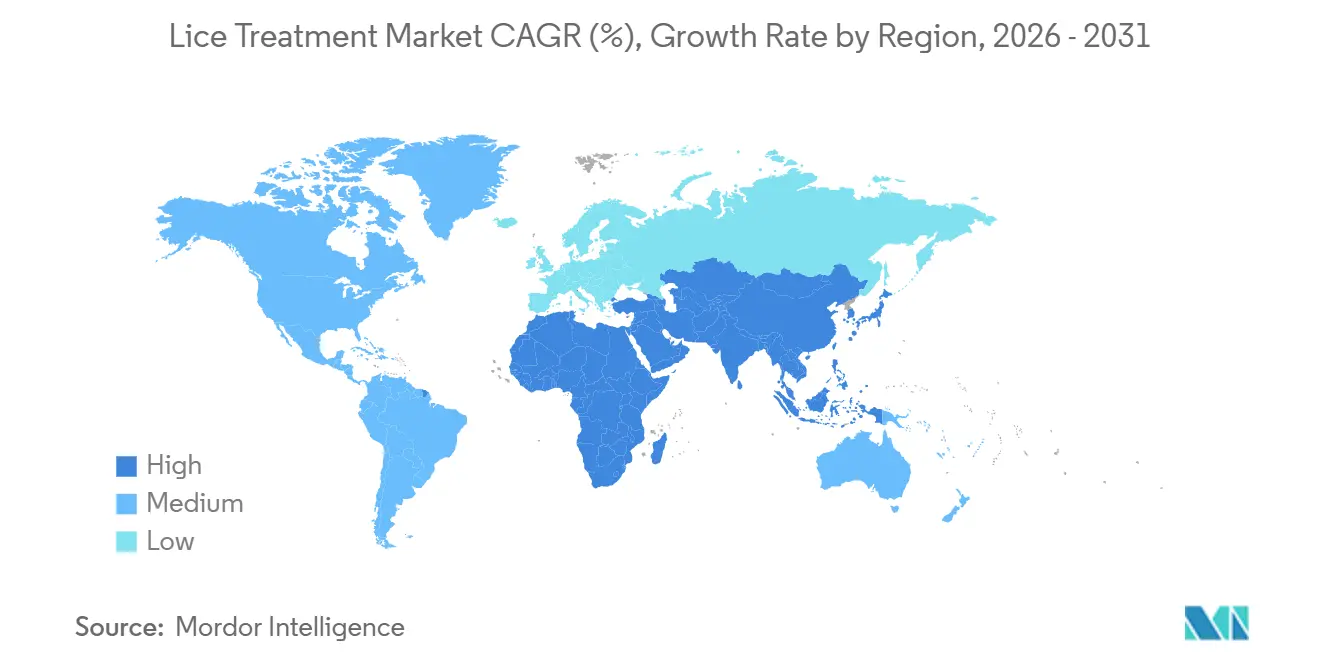

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Lice Treatment Market Analysis by ���ϲ�����

The Lice Treatment Market size is expected to increase from USD 1.15 billion in 2025 to USD 1.21 billion in 2026 and reach USD 1.65 billion by 2031, growing at a CAGR of 6.34% over 2026-2031.

Demand is propelled by the collapse of pyrethroid efficacy, tightening neurotoxic-active regulations, and an accelerated consumer pivot toward botanical or device-based alternatives. North America anchors spending because of branded over-the-counter (OTC) franchises and a dense network of professional removal clinics, yet Asia-Pacific contributes most incremental volume as e-commerce bypasses pharmacy gatekeepers. The lice treatment market is also shaped by subscription models that shift costs from families to schools and by heated-air or AI-enabled comb devices that promise chemical-free eradication. Competitive intensity remains moderate because low barriers invite private-label and generic entrants, while no vendor holds more than a 15% stake in the lice treatment market.[1]Centers for Disease Control and Prevention, “Parasites – Lice – Head Lice,” CDC, cdc.gov

Key Report Takeaways

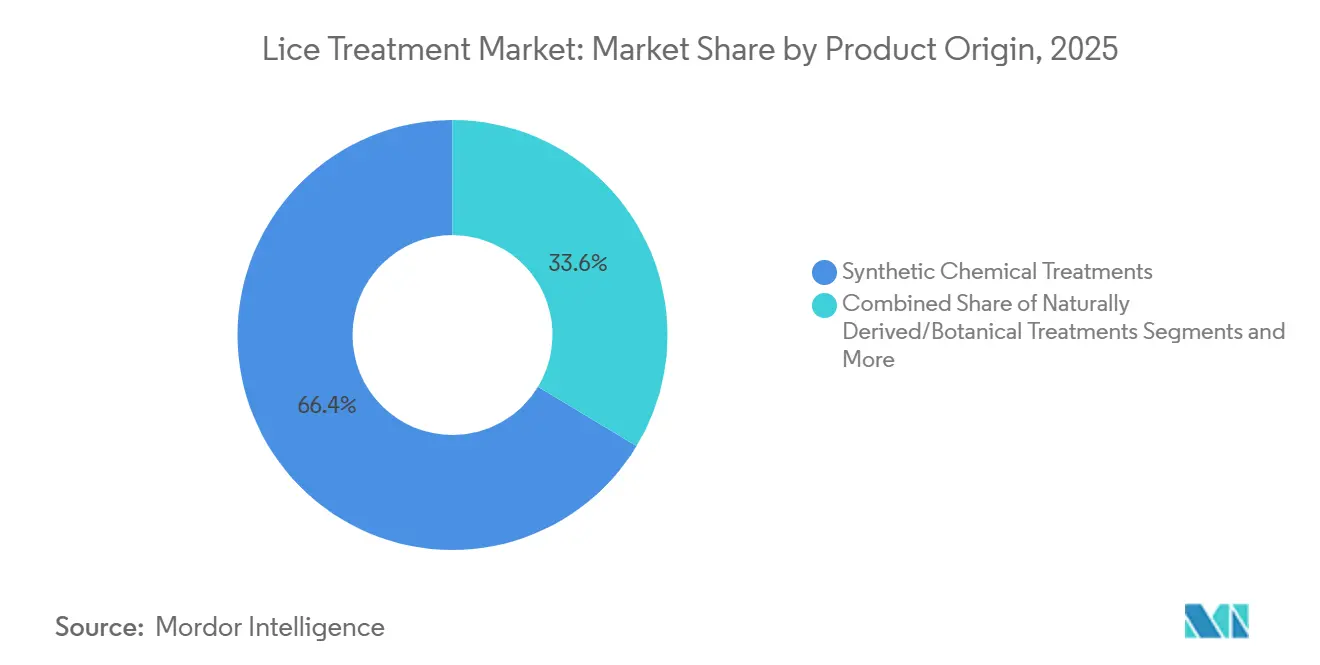

- By product origin, synthetic treatments held 66.36% of lice treatment market share in 2025, while botanical formulations are advancing at a 10.37% CAGR through 2031.

- By age group, the pediatric segment accounted for 53.62% of the lice treatment market size in 2025, and adolescents are projected to expand at an 8.63% CAGR to 2031.

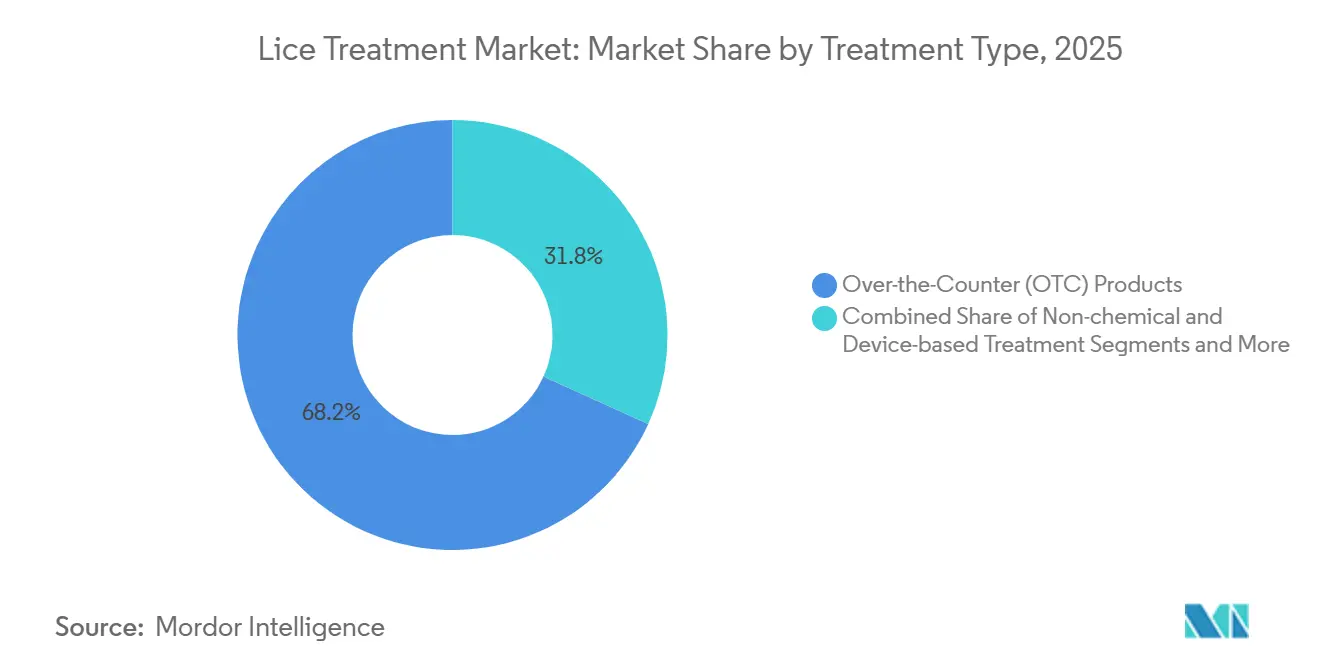

- By treatment type, OTC products led with 68.21% lice treatment market share in 2025, whereas non-chemical platforms are forecast to grow at a 9.52% CAGR between 2026-2031.

- By product type, shampoos controlled 44.14% of lice treatment market revenue in 2025, yet devices are rising at a 10.24% CAGR through 2031.

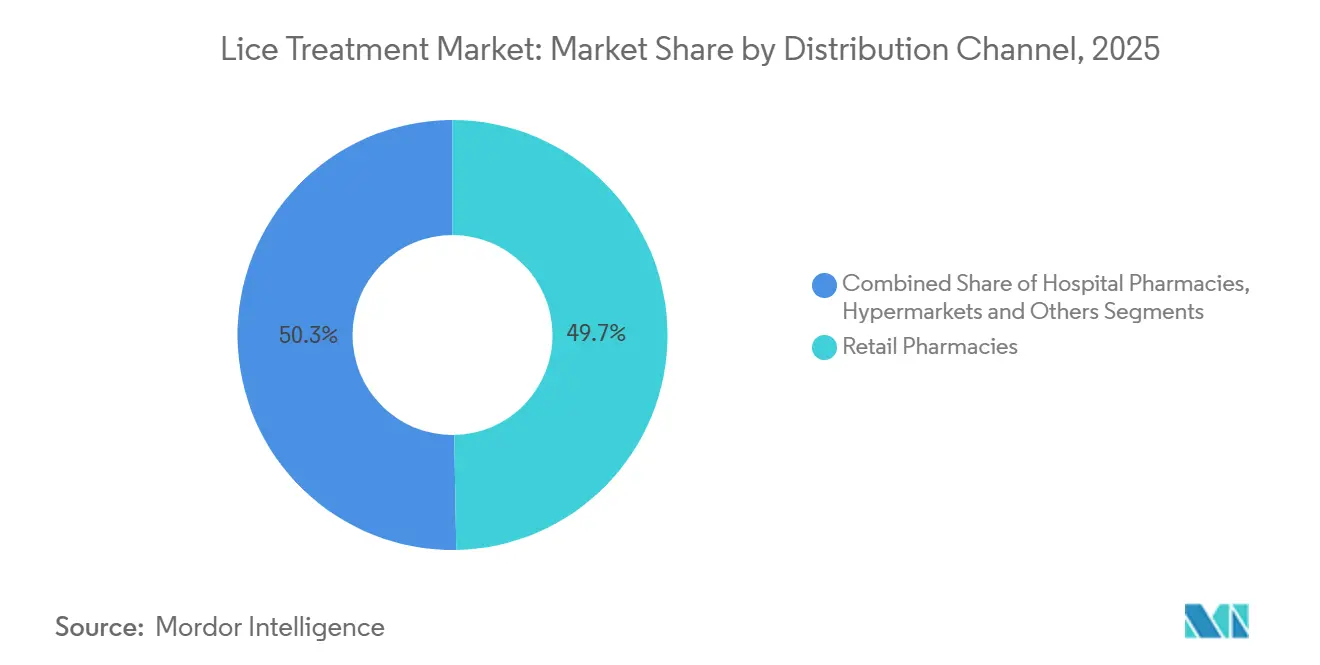

- By distribution channel, retail pharmacies distributed 49.72% of sales in 2025, and online pharmacies plus e-commerce are expanding at a 10.63% CAGR during 2026-2031.

- By geography, North America captured 33.25% of 2025 revenue, while Asia-Pacific is the quickest‐growing region at an 8.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lice Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of treatment-resistant “super lice” | +1.2% | North America, Europe | Medium term (2-4 years) |

| Wider availability of generic ivermectin 0.5% lotion | +0.9% | North America, Europe, select Asia-Pacific | Short term (≤ 2 years) |

| Heightened parental awareness via school e-health portals | +0.7% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of OTC permethrin bans in Europe | +0.6% | European Union member states | Long term (≥ 4 years) |

| Retail launch of AI-enabled lice detection combs | +0.5% | North America, Western Europe, Japan | Short term (≤ 2 years) |

| Growth of “lice-free school” subscription contracts | +0.4% | United States, Canada, Australia | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising Prevalence of Treatment-Resistant “Super Lice”

Pyrethroid-resistant lice now dominate infestations across most U.S. states, and kdr mutations appear in European samples as well. Clinical literature published in 2025 reported that 98% of North American specimens carried at least one resistance allele, driving caregivers toward ivermectin, spinosad, or device solutions.[2]Yuyi Gao, “Prevalence of Knockdown-Resistance Alleles in North-American Head Lice, 2025,” Journal of Medical Entomology, pubmed.ncbi.nlm.nih.gov Multiple treatment cycles inflate per-episode spending and erode loyalty to legacy OTC shampoos. Manufacturers still dependent on pyrethroid chemistry face margin pressure unless they diversify into next-generation actives or non-chemical devices.

Growing Availability of Prescription Sklice (Ivermectin 0.5%) Generics

After the FDA moved ivermectin 0.5% lotion from prescription to OTC status in 2020, generic launches by Amneal, Teva, and Perrigo cut average retail prices by about 45%. Medicaid formularies favor these lower-cost options, expanding access for lower-income families.[3]Food and Drug Administration (authoring agency), “FDA Reclassifies Sklice (Ivermectin 0.5%) Lotion to Over-the-Counter Status,” U.S. Food and Drug Administration, fda.gov Although adoption remains uneven in Asia-Pacific and Latin America, the price drop reshapes pharmacy shelf economics in the United States and Europe.

Heightened Parental Awareness Through School E-Health Portals

Digital class portals alert parents within hours of an outbreak, link to evidence-based treatment guides, and schedule automated reminders for follow-up checks. A 2025 Ontario pilot showed a 30% cut in repeat infestations once the system was live. These platforms drive product selection toward clinically validated brands and reinforce early purchasing behavior.

Expansion of OTC Permethrin Bans in Europe

Denmark, Sweden, and other EU members have shifted permethrin to prescription-only channels under the Biocidal Products Regulation. Brands must either invest in expensive dossiers to stay on shelves or pivot into botanical lines regarded as cosmetics. That regulatory tension steers families into dimeticone or device alternatives, reshaping the lice treatment market long term.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising safety concerns about neuro-toxic pediculicides | -0.8% | North America, Europe | Medium term (2-4 years) |

| Growing use of “no-poison” home remedies | -0.6% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Strict EU biocide rules delaying novel actives | -0.5% | European Union member states | Long term (≥ 4 years) |

| Grey-market generics in price-sensitive economies | -0.4% | South Asia, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Increasing Safety Concerns Around Neuro-Toxic Pediculicides

Pediatric societies now advise parents to avoid neuro-toxic shampoos when alternatives exist, citing developmental-toxicity signals from animal studies. Label warnings in Europe intensify risk perception, pushing families toward botanical or device platforms and shrinking demand for permethrin lotions.

Rising Preference for “No-Poison” Home Remedies Impacting Product Uptake

DIY methods such as wet-combing or olive-oil suffocation circulate widely on social media. Although a 2025 Cochrane analysis placed wet-combing success at only 38%, wellness-centric parents still embrace non-commercial tactics. This behavioral shift siphons volume away from formal retail channels.

Segment Analysis

By Product Origin: Botanical Alternatives Challenge Synthetic Dominance

Synthetic formulas captured 66.36% of 2025 revenue, a share built on long-standing pharmacist trust and clinical validation. Yet botanical solutions are scaling at 10.37% as parents seek “clean-label” reassurance. The lice treatment market size for botanicals is projected to expand steadily because essential-oil brands navigate lighter regulatory paths. Synthetic players now hedge with combination kits that bundle a nit comb to boost perceived value. Underlying fragility persists: rampant resistance forces a pivot toward costlier ivermectin and spinosad, while European rules squeeze pyrethroids. Tea-tree and neem products win shelf space despite lower eradication rates, thanks to rapid cosmetic registration. Device vendors, exempt from drug dossiers, present a longer-run disruptive threat.

Second-order effects shape future margins. Tea-tree suppliers skirt pharmacovigilance, but inconsistent kill rates spark repeat infestations that may erode consumer trust. Dimeticone gels, acting via suffocation not neuro-toxicity, bridge the performance gap and qualify as Class I devices in several markets, accelerating approvals. Electronic-vacuum comb makers aim to halve unit prices, positioning reusable hardware as the logical escape from resistance loops in the lice treatment market.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Adolescent Growth Outpaces Pediatric Core

Children aged 0-11 generated 53.62% of 2025 sales, reflecting playground transmission intensity. Adolescents aged 12-17 now expand at 8.63% because middle- and high-school screenings catch silent carriers, and teens value discreet, rapid fixes. The lice treatment market size for the adolescent cohort is forecast to widen as social stigma fuels willingness to pay for single-session devices. Adults represent secondary household cases and often secure insurance-covered prescriptions, while geriatric demand stays negligible.

Digital commerce reorders purchase journeys. Teens, browsing via smartphones, buy ivermectin lotions or smart combs without parental mediation, forcing brands to optimize TikTok and Instagram storefronts. Pediatric purchases still favor multi-dose shampoo packs, though rising clinical failures nudge families toward professional franchises. Adult cases gravitate to dermatology offices, where oral ivermectin fills the refractory niche. For marketers, distinct channels and messaging are mandatory across age bands inside the lice treatment market.

By Treatment Type: Non-Chemical Platforms Accelerate

OTC products led with 68.21% lice treatment market share in 2025, courtesy of easy pharmacy access. Still, non-chemical options climb at 9.52% as resistance spreads and EU rules pinch neuro-toxic actives. Prescription ivermectin and spinosad cover severe cases but face access hurdles.

Dimeticone products, labeled as medical devices, bypass drug requirements and retain efficacy against resistant strains. Heated-air systems dehydrate lice in one visit, luring parents averse to chemicals. Hybrid offerings emerge: OTC kits including a chemical shampoo plus an AI comb for verification. Pharmacy closures during the COVID-19 era pushed households to e-commerce, shrinking the pharmacist’s gatekeeper role in the lice treatment market.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Devices Rise as Shampoos Plateau

Shampoos maintained 44.14% share in 2025 because of habit and convenience. Devices now advance at 10.24% CAGR; families justify a USD 40-80 smart comb versus multiple USD 20 shampoo cycles. Lotions and creams appeal to dense or curly hair where shampoo foams poorly, while sprays target hard-to-reach nape zones. Ivermectin tablets remain a niche but indispensable option for chronic infestations.

The lice treatment market share held by devices stands to climb once unit prices drop and retailers bundle financing. FDA Class II clearance focuses on safety, enabling annual model improvements without multi-year trials. As shampoo efficacy wanes, devices or dimeticone gels become first-line in affluent segments, pushing chemical shampoos toward commodity status.

By Distribution Channel: E-Commerce Chips Away at Pharmacy Dominance

Retail pharmacies accounted for 49.72% of sales in 2025, benefiting from pharmacist recommendations and instant availability. Yet online pharmacies and general e-commerce are surging at 10.63% CAGR as same-day delivery spreads. Parents value discretion and review aggregation, and telemedicine links let physicians e-prescribe ivermectin directly to mail-order pharmacies.

Brick-and-mortar outlets still capture panic purchases discovered after school pickup, but planned replenishment migrates online. Amazon Pharmacy and CVS.com streamline insurance adjudication, undercutting local pharmacy margins. Hospital pharmacies serve prescription niches, while hypermarkets appeal to bulk shoppers. Omnichannel consistency—pricing, pack sizes, brand voice—is now a gating factor for growth inside the lice treatment market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated 33.25% of 2025 revenue, buoyed by high insurance penetration and professional franchise density. Pyrethroid resistance makes treatment episodes costlier, lifting average selling prices. Mandatory screenings in 40+ U.S. states sustain repeat demand despite flat incidence. Canadian provinces increasingly reimburse prescription ivermectin for low-income families, softening price sensitivity. Mexican urban centers mirror U.S. brand preferences, but rural areas still rely on under-regulated sachets, limiting formal-channel opportunity.

Asia-Pacific expands at 8.22% CAGR through 2031, with India and China driving absolute volume. Grey-market generics hijack 30-40% of unit sales, though rising urban incomes and smartphone adoption push parents toward branded devices. Japan and South Korea favor botanical lotions and AI combs that align with tech and clean-beauty trends. Australia, while small in population, exhibits North American dynamics: franchise clinics, insurance coverage, and e-commerce uptake. Localized strategies are imperative—low-price sachets in South Asia, premium unboxing experiences in East Asia, and pharmacy focus in Oceania.

Europe sits mid-pack, its growth dampened by biocide stringency. Germany, France, and the United Kingdom anchor demand and reimburse prescription pediculicides for children. Southern Europe leans on OTC shampoos, whereas Eastern Europe still trusts generic permethrin despite falling cure rates. Nordic countries push botanical transitions, having curtailed OTC permethrin. Beyond Europe, Middle East & Africa and South America remain formative. Brazil’s health-tech startups pilot tele-consult + delivery bundles, and South African chains test heated-air service booths, yet weak logistics and limited insurance curb mass uptake. Growing but fragmented, these regions require tailored channel blends to unlock the lice treatment market.

Competitive Landscape

The lice treatment market has a moderate fragmentation. Kenvue, Reckitt, and Perrigo defend legacy permethrin lines using retailer incentives and brand familiarity, though efficacy erosion dilutes loyalty. Amneal, Teva, and Dr. Reddy’s win on price after launching generic ivermectin lotions post-2024. Device-centric firms such as Larada Sciences and Hair Fairies monetize high-margin heated-air treatments through franchise models and institutional contracts.

Innovation migrates to engineering and digital platforms rather than chemistry. The FDA’s 510(k) route lets AI comb makers iterate annually. Patent data shows progress in plasma-ionization tips, machine-vision nit counters, and slow-release botanical microcapsules. E-commerce-native brands exploit Instagram for story-driven marketing, bypassing shelf fees. Subscription-based school contracts give service vendors predictable cash flows, a structural advantage over one-off product sales. Future competitive edges will hinge on omnichannel reach, bundled service propositions, and region-specific regulatory mastery.

Lice Treatment Industry Leaders

Prestige Consumer Healthcare Inc

Reckitt Benckiser Group plc

Bayer AG

Sanofi S.A

Kenvue

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Pelthos Therapeutics acquired Xeglyze (abametapir) for USD 1.8 million, adding a single-application pediculicide to its dermatology portfolio.

- January 2026: Health Canada accepted Cipher Pharmaceuticals’ NDS for Natroba (spinosad) to treat head lice and scabies, advancing the product’s launch timeline.

- January 2026: Lice Happens celebrated assisting 10,000 Georgia families with its mobile, non-toxic lice-removal service during its first decade of operation.

Global Lice Treatment Market Report Scope

As per the scope of this report, lice treatment refers to the process of removing parasitic lice and their eggs (nits) from hair, body, or clothing using specialized methods.

The Lice Treatment Market Report is segmented by Product Origin, Age Group, Treatment Type, Product Type, Distribution Channel, and Geography. By Product Origin, the market is segmented into Synthetic, Botanical, Device, and Combination products. By Age Group, the market is segmented into Pediatric, Adolescents, Adults, and Geriatric. By Treatment Type, the market is segmented into OTC, Prescription, and Non‑chemical treatments. By Product Type, the market is segmented into Shampoos, Lotions, Sprays, Devices, and Others. By Distribution Channel, the market is segmented into Retail, Hospital, Online, and Hypermarkets. By Geography, the market is segmented into North America, Europe, Asia‑Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Synthetic Chemical Treatments |

| Naturally Derived / Botanical Treatments |

| Device-based / Mechanical Treatments |

| Combination Kits (chemical + device / comb) |

| Pediatric (0-11 years) |

| Adolescents (12-17 years) |

| Adults (18-64 years) |

| Geriatric (65 years & above) |

| Over-the-Counter (OTC) Products |

| Prescription Treatments |

| Non-chemical and Device-based Treatments |

| Shampoos |

| Lotions & Creams |

| Sprays |

| Serums & Gels |

| Oral Tablets |

| Devices |

| Others |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies & E-commerce |

| Hypermarkets & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Origin | Synthetic Chemical Treatments | |

| Naturally Derived / Botanical Treatments | ||

| Device-based / Mechanical Treatments | ||

| Combination Kits (chemical + device / comb) | ||

| By Age Group | Pediatric (0-11 years) | |

| Adolescents (12-17 years) | ||

| Adults (18-64 years) | ||

| Geriatric (65 years & above) | ||

| By Treatment Type | Over-the-Counter (OTC) Products | |

| Prescription Treatments | ||

| Non-chemical and Device-based Treatments | ||

| By Product Type | Shampoos | |

| Lotions & Creams | ||

| Sprays | ||

| Serums & Gels | ||

| Oral Tablets | ||

| Devices | ||

| Others | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies & E-commerce | ||

| Hypermarkets & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big will the lice treatment market be in 2031?

It is forecast to reach USD 1.65 billion by 2031, reflecting a 6.34% CAGR from 2026.

Which product origin grows fastest?

Botanical formulations are set to rise at a 10.37% CAGR, the quickest among all origins.

Why are devices gaining traction over shampoos?

Parents value reusable, chemical-free eradication; smart combs and heated-air kits grow at 10.24% CAGR, outpacing plateauing shampoos.

Which region offers the highest growth momentum?

Asia-Pacific leads with an 8.22% CAGR thanks to e-commerce access, urban school enrollment, and rising disposable incomes.

What drives the switch from permethrin to ivermectin?

Near-universal pyrethroid resistance and lower-cost generics have shifted demand toward ivermectin 0.5% lotions.