Leptospirosis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

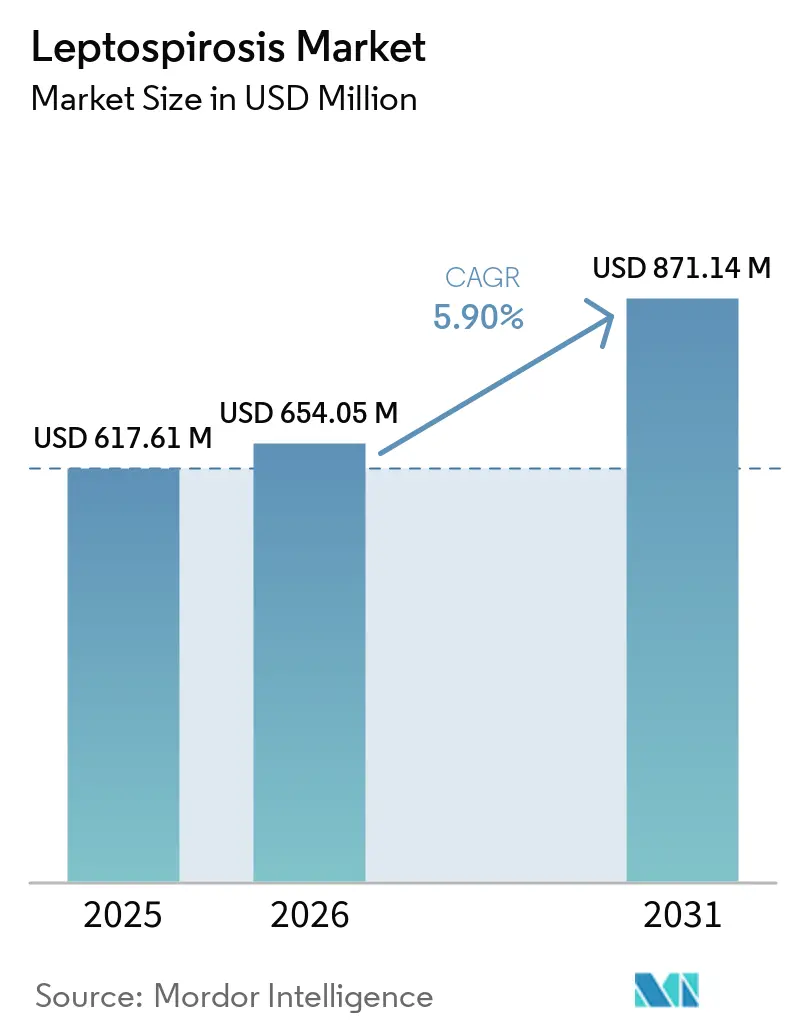

| Market Size (2026) | USD 654.05 Million |

| Market Size (2031) | USD 871.14 Million |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Leptospirosis Market Analysis by ���ϲ�����

The Leptospirosis Market size is expected to grow from USD 617.61 million in 2025 to USD 654.05 million in 2026 and is forecast to reach USD 871.14 million by 2031 at 5.90% CAGR over 2026-2031.

Climate change-induced flooding is accelerating shifts in the disease landscape, outpacing traditional surveillance systems. In response, tertiary hospitals are adopting isothermal amplification platforms that can confirm Leptospira infections in under an hour. This technological shift is driving growth in the leptospirosis market as clinicians transition from empirical treatments. Notification mandates in various regions have exposed significant under-reporting of leptospirosis cases, resulting in a compliance-driven increase in diagnostic orders and reinforcing the central role of diagnostics in market revenue. Simultaneously, disaster-response agencies are stockpiling doxycycline and ceftriaxone, redirecting therapeutic demand from retail channels to bulk public procurement. This transition is stabilizing supply volumes and maintaining price levels in the leptospirosis market.

Key Report Takeaways

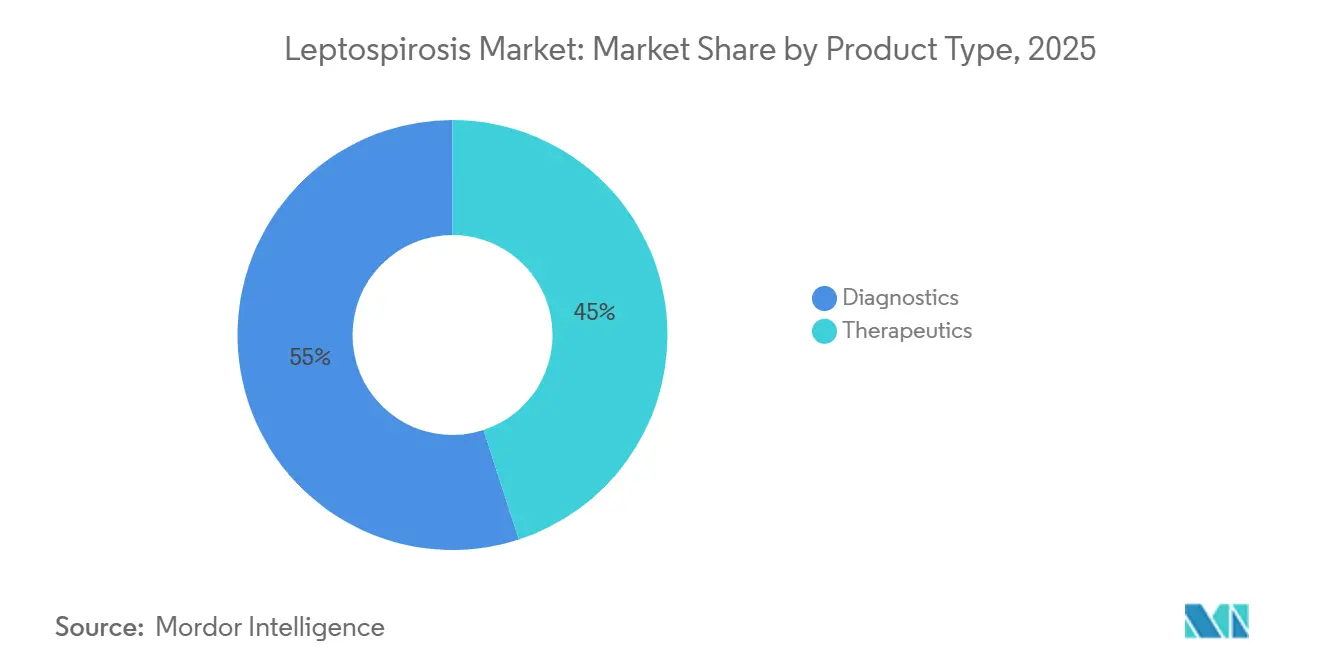

- By product type, diagnostics led with 55.0% of the leptospirosis market share in 2025, while therapeutics are projected to expand at a 6.35% CAGR through 2031.

- By end user, hospitals and specialty clinics held 48.0% of the leptospirosis market size in 2025, whereas diagnostic reference laboratories are forecast to record a 7.55% CAGR over 2026-2031.

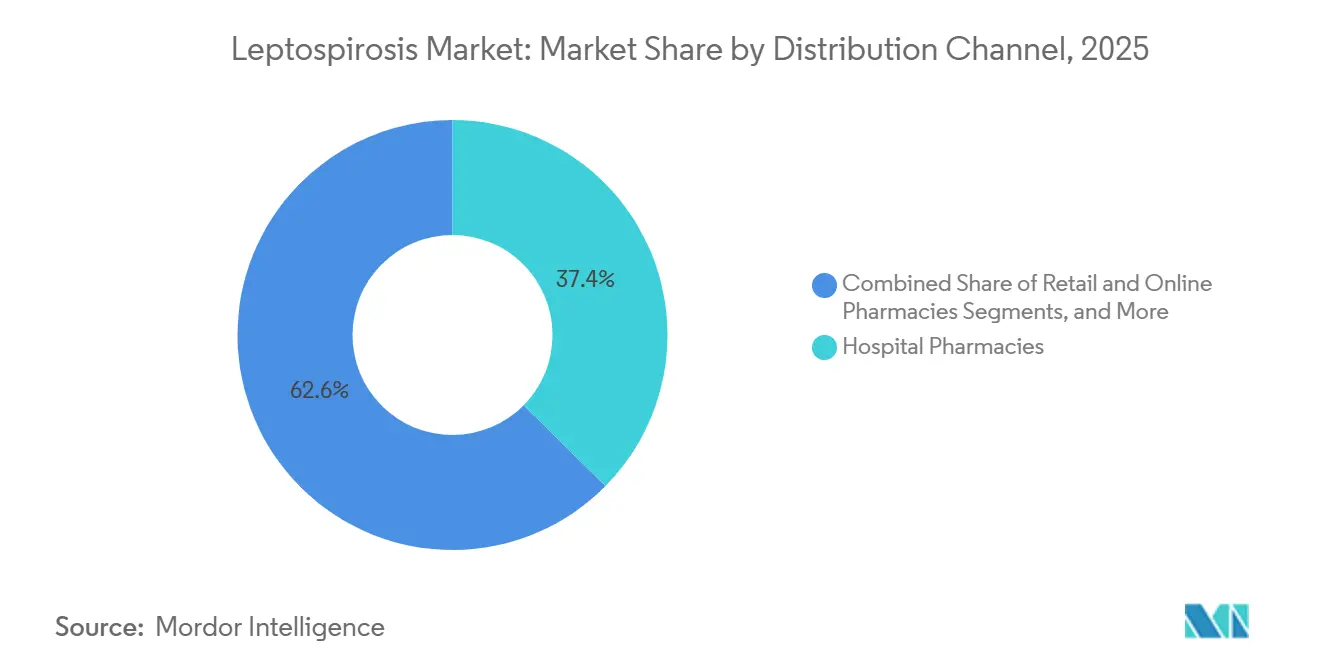

- By distribution, hospital pharmacies held 37.39% of the leptospirosis market size in 2025, whereas retail and online pharmacies are forecast to record a 7.15% CAGR over 2026-2031.

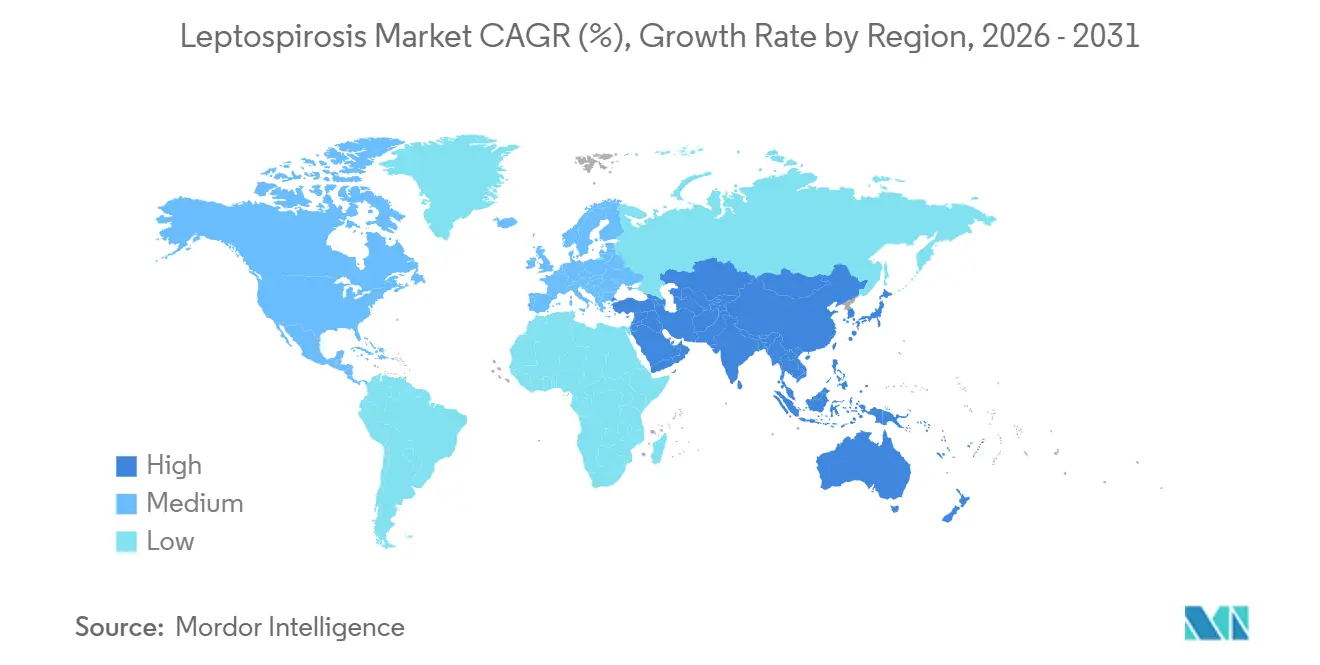

- By geography, North America commanded 40.40% of the leptospirosis market share in 2025, but Asia-Pacific is advancing at a 6.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Leptospirosis Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Flooding and extreme rainfall driven by climate change | 1.2% | Global, concentrated in South America (Brazil, Argentina), Asia-Pacific (Philippines, India), and Oceania (New Zealand, Australia) | Medium term (2-4 years) |

| Reinstating leptospirosis as a notifiable disease | 0.9% | Europe (France, Netherlands), South America (Argentina), Oceania (Australia, New Zealand) | Short term (≤ 2 years) |

| Public-sector stockpiling of doxycycline and ceftriaxone for disaster response | 0.7% | South America (Brazil), Asia-Pacific (Philippines), North America (FEMA regions) | Medium term (2-4 years) |

| Tertiary hospitals adopting multiplex febrile-illness PCR panels | 1.1% | North America, Europe, Asia-Pacific urban centers (India, China, Thailand) | Short term (≤ 2 years) |

| Adventure tourism driving prophylactic antibiotic use | 0.5% | Central America (Costa Rica), Southeast Asia (Thailand, Vietnam), South America (Peru) | Long term (≥ 4 years) |

| Affordable nanoparticle-LAMP lateral-flow combo tests enabling community screening | 1.0% | Asia-Pacific (India, Philippines, Indonesia), Sub-Saharan Africa, South America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Flooding And Extreme Rainfall Driven By Climate Change

In May 2024, flooding in Brazil’s Rio Grande do Sul resulted in 1,314 reported cases and 55 fatalities, increasing the incidence rate to 12.1 per 100,000, significantly higher than the national average of 1.9 per 100,000. Concurrently, surveillance efforts identified 958 lab-confirmed infections, marking a 10.3-fold increase and prompting swift actions for procuring rapid tests and preventive antibiotics.[1]Ministry of Health Brazil, “Technical Note on Leptospirosis Management During Floods,” gov.br In the Philippines, the first seven months of 2025 recorded 3,037 cases, reflecting a 121% increase from the previous year, attributed to Typhoon Hagupit. This surge led to the transition of LAMP testing to community clinics. New Zealand experienced its highest case load in 20 years following Cyclone Gabrielle, while the Netherlands saw a 4.1-fold rise in local infections in 2024, coinciding with intensified precipitation extremes.[2]Department of Health Philippines, “Leptospirosis Surveillance Report January–July 2025,” doh.gov.ph Such climatic events are transforming leptospirosis from a seasonal ailment, primarily affecting farm workers, to a pressing year-round public health concern, driving increased investments in diagnostics and treatments within the leptospirosis market.

Reinstating Leptospirosis As A Notifiable Disease

In August 2023, France reinstated mandatory reporting for leptospirosis. By 2024, 886 cases were recorded, with a notable 74% hospitalization rate. This data highlights the disease's burden and aids in setting procurement budget baselines.[3]Santé Publique France, “Leptospirosis Surveillance 2024,” santepubliquefrance.fr Following a 2023 decree in Argentina, confirmed cases increased 3.8-fold by epidemiological week 34 of 2025, emphasizing the need for rapid molecular assays. In January 2026, Australia expanded its national case definition to include PCR-positive results, broadening the range of reimbursable tests and boosting diagnostic demand. In the United States, weekly publications under the National Notifiable Diseases Surveillance System ensure hospitals remain vigilant, stabilizing order volumes for multiplex panels. Such regulatory measures are transforming previously latent testing demands into quantifiable, budgeted needs, thereby expanding the leptospirosis market.

Public-Sector Stockpiling Of Doxycycline And Ceftriaxone For Disaster Response

In May 2024, Brazil promptly dispatched 400 rapid tests and supplies of doxycycline to the flood-affected Rio Grande do Sul within 48 hours, demonstrating how emergency protocols can bypass standard tender processes. During the 2025 typhoon season, the Philippines provided doxycycline prophylaxis to first responders. At the same time, the WHO formalized the inclusion of doxycycline in its 2025 emergency list, integrating leptospirosis treatment into global disaster response strategies. In the United States, FEMA has begun storing doxycycline alongside tetanus vaccines in regional warehouses, ensuring immediate availability during hurricane emergencies. Additionally, bulk contracts at the state level are insulating generic suppliers from the usual retail price drops, establishing a consistent revenue stream in the leptospirosis market.

Tertiary Hospitals Adopting Multiplex Febrile-Illness PCR Panels

bioMérieux’s BioFire Global Fever Panel delivers a 93.8% accuracy rate for detecting Leptospira and provides results in approximately one hour. This rapid turnaround enables clinicians to differentiate leptospirosis from dengue or malaria in a single test. In 2024, a consortium in Colombia enhanced a three-pathogen multiplex by adding Rickettsia and Borrelia. With a detection limit of 159.5 copies/µL, this advancement is critical for Andean regions where overlapping zoonotic diseases complicate treatment. In March 2025, HiMedia introduced the Hi-PCR Acute Fever Panel, featuring a 1-copy/µL detection threshold. This panel offers Asian hospitals a cost-effective alternative, priced at roughly half the cost of imported systems. These advanced platforms are replacing multiple singleplex assays with a singular syndromic panel, optimizing reagent usage and reducing time-to-therapy—benefits that are directly strengthening the leptospirosis market.

Restraint Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented product reimbursement pathways for neglected tropical diseases | -0.8% | Global, acute in Sub-Saharan Africa, South Asia, and parts of Latin America | Long term (≥ 4 years) |

| Dependence on generic, low-margin antibiotics limiting private R&D investment | -0.6% | Global, especially impacting pharmaceutical innovation in North America and Europe | Long term (≥ 4 years) |

| Supply-chain bottlenecks in rabbit-serum–based EMJH culture reagents | -0.3% | Global, concentrated in diagnostic reference laboratories in Asia-Pacific and South America | Medium term (2-4 years) |

| Possible efflux-pump–mediated reduced susceptibility in Pomona serovar strains | -0.4% | Asia-Pacific (Philippines, Thailand), Oceania (Australia), South America (Brazil) | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Fragmented Reimbursement Pathways Hinder Progress on Neglected Tropical Diseases

Between 2018 and 2023, the World Health Organization reported a 41% decline in official development assistance for neglected tropical diseases, significantly reducing financial resources for new diagnostic developments. In India, Indonesia, and the Philippines, health insurance plans exclude coverage for leptospirosis tests, requiring patients to pay out of pocket amounts ranging from USD 15 to 40, which can represent up to a week's wages in rural areas. In Brazil, reimbursement is provided for outdated microscopic agglutination tests but not for advanced PCR tests. This policy directs laboratories toward slower, traditional technologies, even as the market shifts toward rapid molecular platforms for leptospirosis. These inconsistencies limit economies of scale for advanced assays, delaying price reductions and restraining the growth of the leptospirosis market.

Reliance on Low-Margin Generic Antibiotics Stifles Private R&D Investment

A 2024 review classified the evidence supporting current antibiotics as having very low certainty. Additionally, the low pricing of generic doxycycline, which sells for pennies per pill, leaves minimal room for pricing innovative therapies. While small grants have been secured for vaccine development, the industry predominantly views prevention as the only commercially viable approach, slowing the introduction of new molecules into the leptospirosis market. The absence of premium-priced drugs discourages venture investments, limiting advancements in therapeutic solutions.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diagnostics Lead, Therapeutics Accelerate

Diagnostics, contributing 55% of 2025 revenue, emphasize the transition of laboratory confirmation from an optional service to a clinical requirement. While serological ELISA and MAT kits remain dominant in reference labs, molecular assays now account for nearly one-third of diagnostic sales due to reagent prices dropping below USD 5 per run. The multiplex category is experiencing the fastest growth, with products like bioMérieux’s BioFire Global Fever Panel and HiMedia’s Acute Fever Panel delivering results in under an hour, enabling physicians to reduce broad-spectrum antibiotic therapy. Although smaller in size, therapeutics are projected to surpass diagnostics with a 6.35% CAGR through 2031. This growth is driven by the expansion of disaster-response stockpiles in Asia-Pacific and South America, ensuring consistent orders for generic manufacturers and strengthening the overall resilience of the leptospirosis market.

By End User: Reference Labs Outpace Hospitals

In 2025, hospitals and specialty clinics accounted for 48% of spending, driven by the adoption of syndromic PCR panels that consolidate febrile-illness testing. However, growth is expected to slow as most tertiary facilities have already upgraded their equipment. On the other hand, diagnostic reference laboratories are anticipated to achieve a 7.55% CAGR. This growth is supported by national public-health institutes deploying portable LAMP systems for district-level screening, shifting volumes to centralized networks and increasing the market share captured by reference labs.

By Distribution Channel: Emergency Procurement Reshapes Flows

In 2025, hospital pharmacies captured 37.39% of distribution revenue, supported by steady intravenous ceftriaxone usage in ICUs. Retail and online pharmacies are expected to grow at 7.15% annually, driven by adventure-tourism prophylaxis packs and the increasing trend of tele-consultations issuing electronic doxycycline prescriptions. Government and emergency procurement, which already accounts for approximately one-quarter of sales, is expanding as ministries formalize climate-disaster response strategies, redirecting significant volumes of diagnostics and medications outside routine tender processes.

Geography Analysis

In 2025, North America accounted for 40.40% of global revenue, supported by mandatory weekly reporting by health authorities and government stockpiles, which established a consistent baseline for test and drug consumption in the regional leptospirosis market. Hospital formularies now predominantly feature multiplex panels, and reimbursement policies have evolved to tie payouts to documented etiology, steering practitioners away from broad-spectrum regimens. The United States operates over 50 state public-health laboratories equipped for same-day Leptospira PCR testing, ensuring sustained demand even in non-flood seasons.

Asia-Pacific is projected to grow at a compound annual growth rate (CAGR) of 6.95% through 2031, driven by the Philippines reporting significant case numbers in the first half of 2025 and India's substantial annual infections, many of which remain undiagnosed. Affordable LAMP tests, priced at approximately USD 3.50, are enabling mass screenings in community clinics, broadening the leptospirosis market's reach beyond urban tertiary centers. Australia's decision in early 2026 to include PCR in its case definition provides a boost from high-income regions, while Indonesia and Malaysia are expected to implement similar policy changes within the next two years.

In South America, demand is episodic, often spiking in response to floods. For example, Brazil's severe flooding in May 2024 led to a significant surge in confirmed cases within two months, prompting emergency purchases of rapid tests and large quantities of doxycycline. Meanwhile, Argentina's notification law highlighted diagnostic gaps, with the majority of 2025 cases concentrated in three provinces, a void that suppliers are now working to address. Europe experiences steadier growth but faces challenges due to varied reimbursement policies across its member nations. In Africa, while the burden of the disease remains largely uncharted, there is potential for significant growth once financial support improves.

Competitive Landscape

The global leptospirosis market is moderately fragmented. Abbott, bioMérieux, and Roche offer ELISA and multiplex PCR products but generate less than 1% of their total infectious-disease revenue from Leptospira, indicating a limited strategic focus. These companies, which dominate premium markets, face competition from HiMedia and BioPerfectus. The latter's LAMP assays, priced 40-60% lower, have already secured significant market shares in India and the Philippines. Additionally, university spin-outs in Argentina and the United States have developed lateral-flow innovations with 100% sensitivity. However, licensing challenges leave the annual point-of-care niche, valued at USD 50-80 million, largely untapped.

Supply dynamics vary by product category. Diagnostics, particularly multiplex tests that combine pathogens, achieve moderate gross margins. As a result, portfolio players use revenues from high-volume viruses like influenza to support leptospirosis R&D. In contrast, therapeutics, dominated by doxycycline and ceftriaxone, operate as commodity products with single-digit margins. This margin structure restricts market entry to high-efficiency generic manufacturers, primarily in India and China. Disaster-response agencies prioritize shelf life and availability over brand recognition, shifting procurement competition from molecular innovation to manufacturing capacity.

Regulatory processes remain slow. Fewer than 20% of endemic countries automatically recognize WHO prequalification, requiring companies to submit separate dossiers, which fragments budgets and extends launch timelines. While increasing notification mandates may create latent demand and attract new entrants, stringent scale requirements and low drug margins are likely to maintain the leptospirosis market in a moderately concentrated state, with the top five vendors accounting for approximately 45-50% of global revenue.

Leptospirosis Industry Leaders

Abbott

F. Hoffmann-La Roche Ltd

Pfizer Inc.

Thermo Fisher Scientific Inc.

BioMerieux Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Australia updated its national leptospirosis surveillance case definition to include PCR-confirmed infections, immediately expanding reimbursable molecular testing.

- September 2025: The University of Connecticut filed U.S. patent US20250152689A1 for a multirecombinant protein vaccine that achieved 100% hamster survival, signaling renewed interest in prophylactic pipelines.

- September 2025: Yale School of Medicine researchers unveiled a diagnostic method targeting virulence-modifying proteins, opening a path to earlier human detection.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the leptospirosis market as global sales of human and veterinary vaccines, antibiotics, supportive therapeutics, and commercial diagnostic kits that reach patients or animals through hospitals, veterinary clinics, public-health programs, and licensed distributors. According to ���ϲ�����, grouping treatment and test revenues in one pool mirrors real-world budget decisions and gives buyers a complete spending view.

Scope exclusion: research-only reagents and lab-developed tests that lack clinical clearance are left out.

Segmentation Overview

- By Product Type

- Diagnostics

- Serological Assays (ELISA, MAT-based)

- Molecular Assays (qPCR, LAMP, CRISPR)

- Rapid Immunochromatographic Tests (Lateral Flow, DPP)

- Multiplex Syndromic Panels

- Therapeutics

- Beta-lactams (IV Penicillin G, Ampicillin)

- Tetracyclines (Doxycycline, Omadacycline)

- Macrolides (Azithromycin)

- Third-Generation Cephalosporins (Ceftriaxone, Cefotaxime)

- Others (Supportive Care Adjuncts)

- Diagnostics

- By End User

- Hospitals & Specialty Clinics

- Diagnostic Reference Laboratories

- Point-of-Care / Primary-Care Settings

- Public-Health Agencies & NGOs

- By Distribution Channel

- Hospital Pharmacies

- Retail & Online Pharmacies

- Government & Emergency Procurement

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed infectious-disease physicians, field veterinarians, procurement officers, and diagnostics distributors across North America, Brazil, India, Thailand, and Kenya. These conversations clarified the true treatment mix, seasonality spikes after floods, typical test panels ordered, and price bands, letting us challenge desk estimates and firm up incidence-to-demand ratios.

Desk Research

We began with open data sets such as WHO Global Health Observatory, OIE animal-health reports, FAOSTAT livestock counts, and UN Comtrade vaccine trade codes, which gave broad incidence, herd size, and shipment clues. Peer-reviewed journals (The Lancet, PLOS NTDs), national outbreak dashboards, and patent abstracts from Questel helped track strain diversity and pipeline assets. SEC filings and 10-Ks of listed drug makers supplied average selling prices. Dow Jones Factiva and D&B Hoovers supplemented revenue splits. This list is illustrative; many other credible sources fed our desk review.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-case model converts reported human and animal infections into doses and test volumes; selective bottom-up supplier roll-ups validate totals. Key variables include annual infection incidence, livestock vaccination coverage, share of severe cases needing IV antibiotics, average test panels per suspected case, and regional purchasing power parity for price spreads. Multivariate regression with weather-linked flooding events and livestock population shifts projects demand, while scenario analysis vets high and low paths. Data gaps, especially in under-reported regions, were bridged with expert-agreed correction factors anchored to comparable diseases.

Data Validation & Update Cycle

Outputs pass variance checks against trade flows and hospital procurement logs before senior review. Reports refresh annually, with interim updates triggered by material events such as a major vaccine approval or an El Niño flood surge. A final analyst pass ensures clients receive the latest view.

Why Mordor's Leptospirosis Baseline Is Dependable

Published figures often diverge because firms choose different product baskets, incidence multipliers, or refresh cadences. We disclose scope up front and revise each year, so planners can trace every assumption.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 529.3 M (2025) | ���ϲ����� | - |

| USD 556.3 M (2025) | Global Consultancy A | excludes diagnostics price erosion, applies uniform CAGR to all regions |

| USD 501.0 M (2023) | Trade Journal B | older base year and no veterinary channel adjustment |

| USD 447.8 M (2021) | Industry Association C | uses seven-year-old incidence data and omits currency inflation restatement |

The comparison shows that scope clarity, up-to-date incidence inputs, and yearly recalibration let ���ϲ����� deliver a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

How big is the leptospirosis market in 2026 and how fast will it grow?

The leptospirosis market size reached USD 654.05 million in 2026 and is projected to expand at a 5.9% CAGR to USD 871.14 million by 2031.

Which segment holds the largest share of spending?

Diagnostics captured 55% of global revenue in 2025, reflecting hospitals shift toward laboratory confirmation required by new notification laws.

What region offers the fastest growth opportunity?

Asia-Pacific leads with a 6.95% CAGR through 2031, buoyed by flood-related outbreaks in the Philippines and improved testing access in India.

Why are therapeutics still attractive despite low margins?

Public-sector stockpiling for disaster response locks in multi-year doxycycline and ceftriaxone contracts, creating stable volumes that offset thin per-unit margins.

Which technology is transforming hospital diagnostics?

Multiplex febrile-illness PCR panels, such as the BioFire Global Fever Panel, deliver sub-one-hour results for Leptospira alongside dengue and malaria, improving patient triage and antibiotic stewardship.

Page last updated on: