Laser Welding Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.77 Billion |

| Market Size (2031) | USD 5.06 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

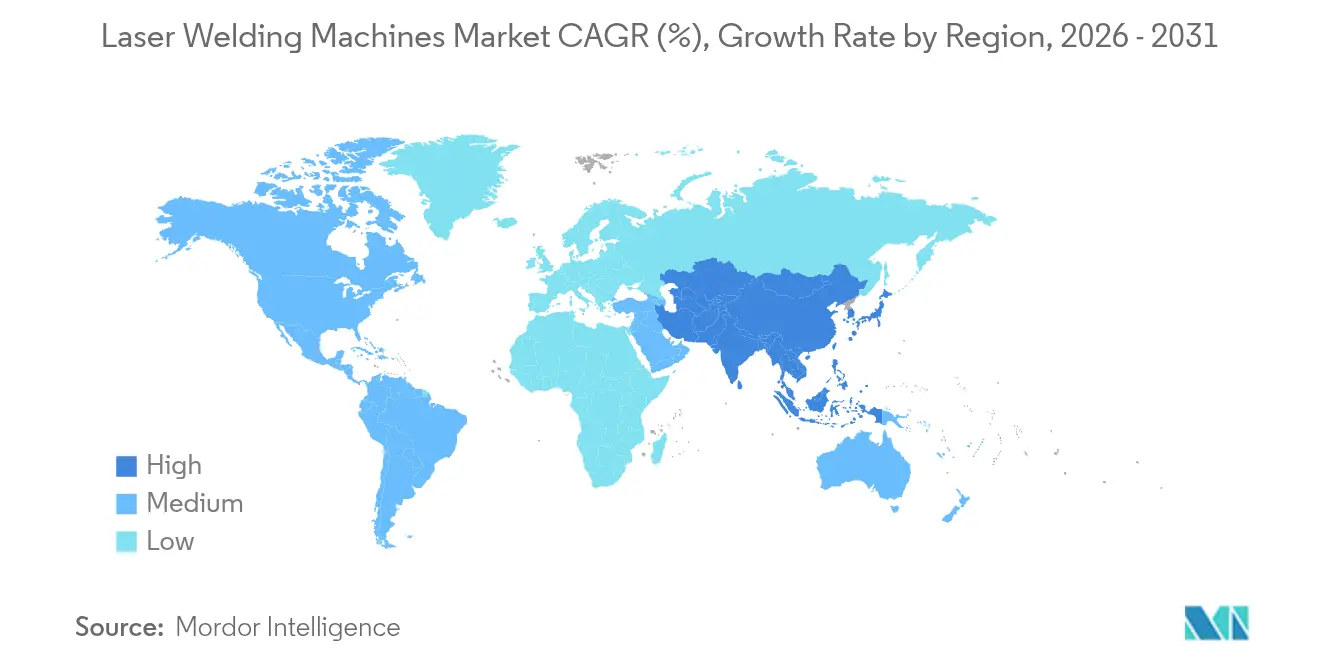

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

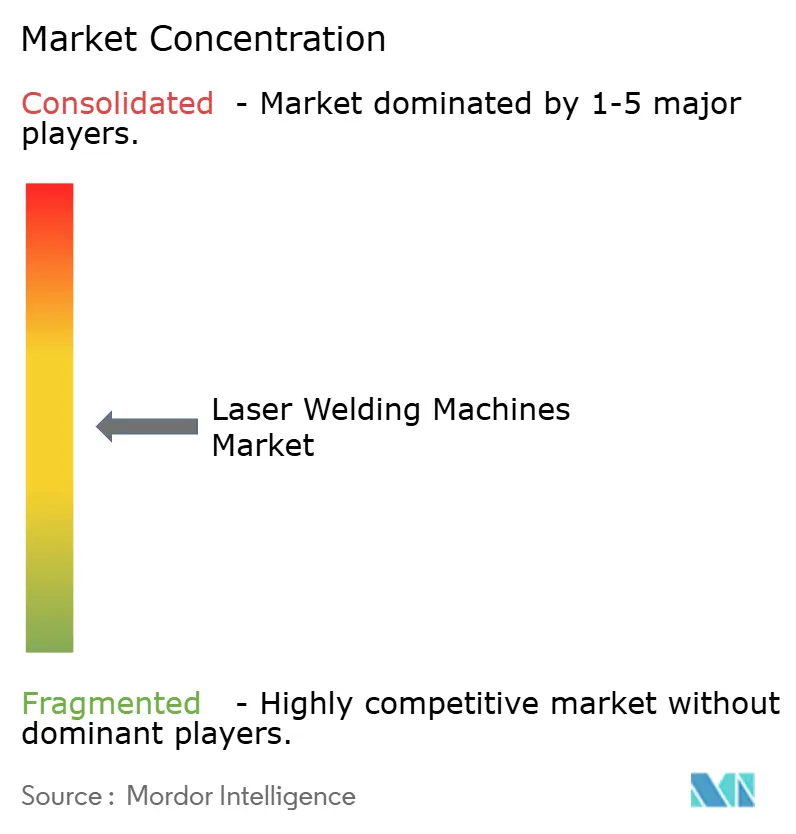

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Laser Welding Machines Market Analysis by ���ϲ�����

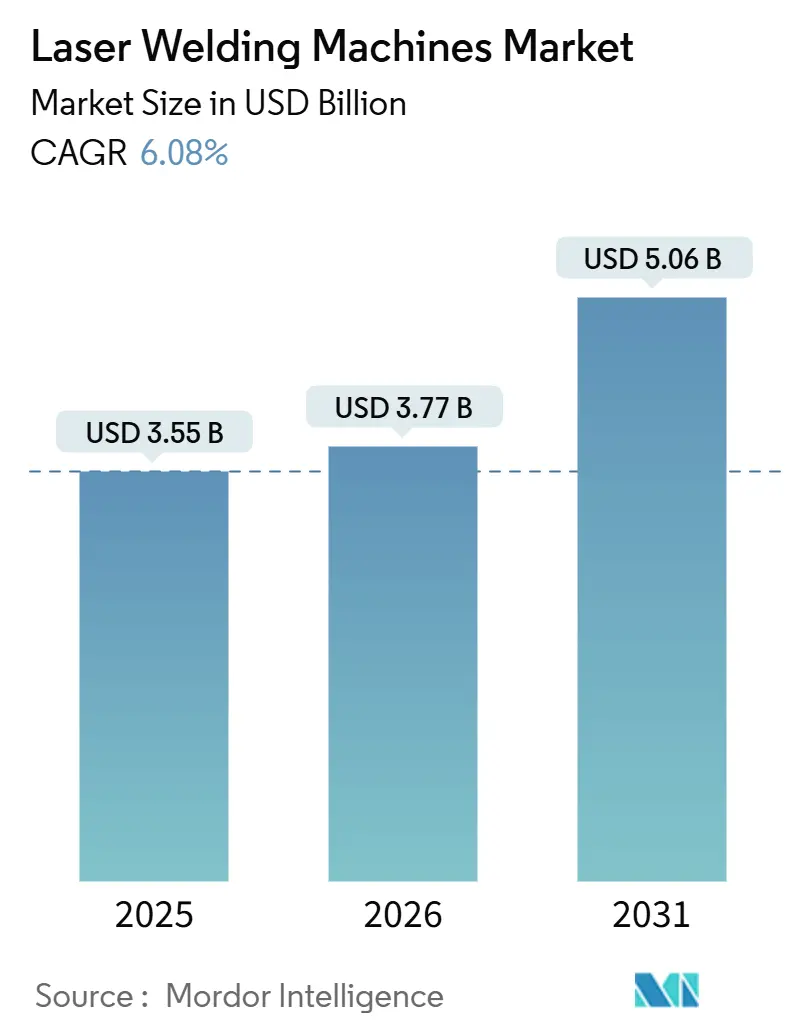

The Laser Welding Machines Market size is projected to expand from USD 3.55 billion in 2025 and USD 3.77 billion in 2026 to USD 5.06 billion by 2031, registering a CAGR of 6.08% between 2026 to 2031.

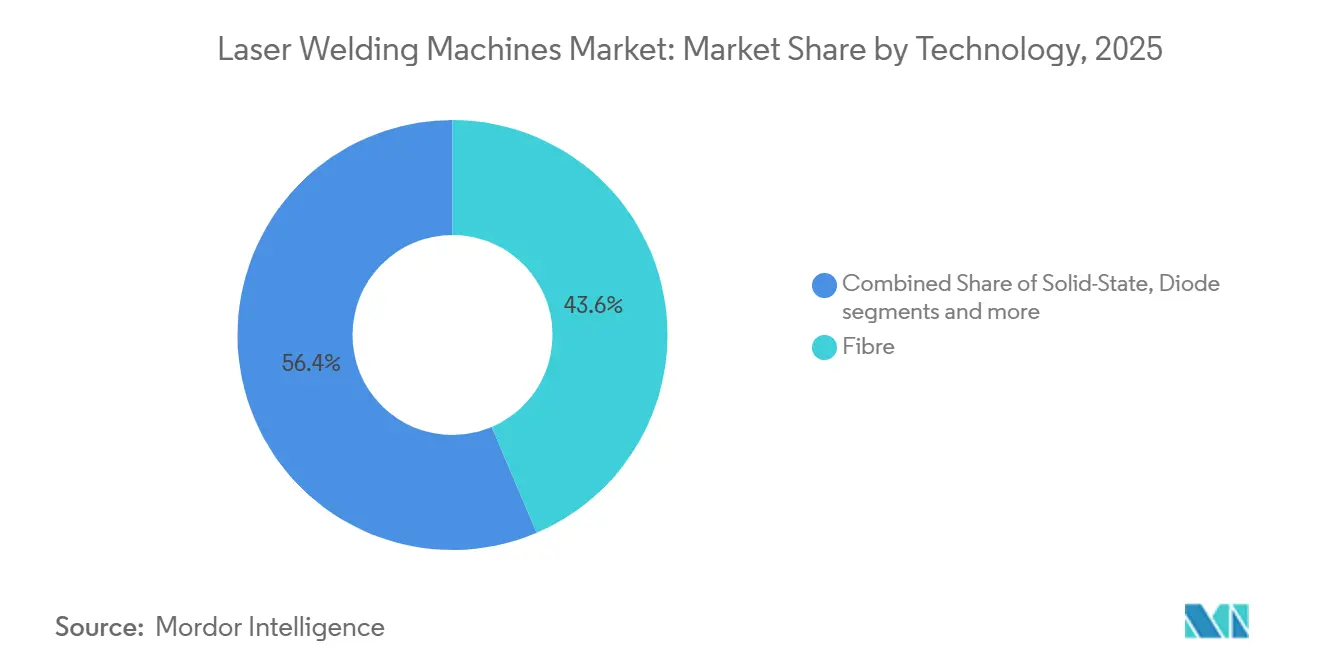

Demand is shifting from metal-inert-gas and tungsten-inert-gas methods toward non-contact joining because electric-vehicle battery enclosures, miniaturized printed-circuit-board assemblies, and implantable medical devices all specify tighter heat-input limits. Fiber technology led in 2025, yet solid-state platforms are gaining as pulsed control handles dissimilar metals required in battery tabs. Handheld fiber units priced below USD 20,000 are widening access for job shops that cannot justify a robotic cell, while artificial-intelligence seam tracking is lifting first-pass yields above 98% and shortening payback periods.[1]Lincoln Electric, “PythonX Handheld Launch,” lincolnelectric.com Asia-Pacific remains the volume center due to China’s gigafactory build-out, but green and blue lasers for copper welding are anchoring the next growth wave in Europe’s 800-volt automotive programs.

Key Report Takeaways

- By technology, fiber lasers accounted for 43.68% of the laser welding machines market share in 2025, while solid-state lasers are likely to register the fastest growth at a 6.43% CAGR by 2031.

- By system type, robotic-integrated cells represented 41.85% of the laser welding machines market share in 2025, whereas handheld and portable systems are poised to grow at an 8.39% CAGR during the forecast period.

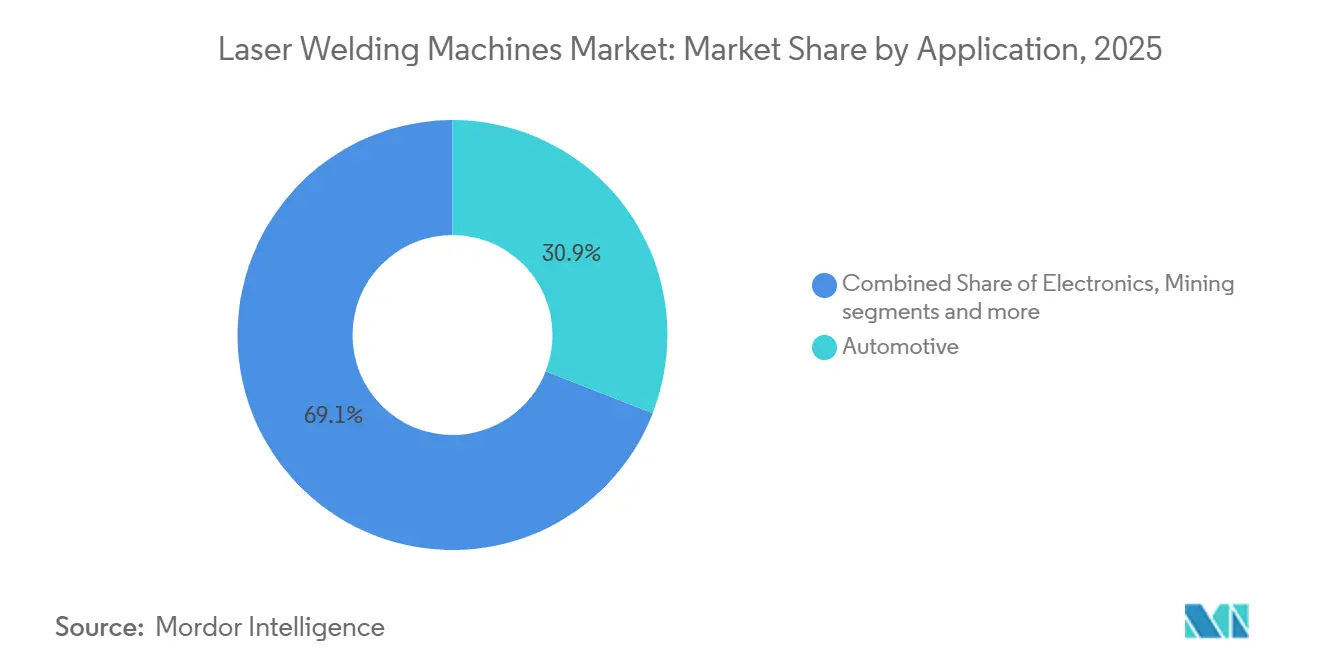

- By application, automotive generated 30.92% of the 2025 value within the laser welding machines market size, while the others segment, including medical devices and battery energy storage, is expected to witness a 6.43% CAGR over the forecast period.

- By material, aluminum contributed 26.52% of the laser welding machines market share in 2025, while titanium is set to record the fastest expansion at a 6.72% CAGR by 2031.

- By geography, Asia-Pacific generated 49.35% of the 2025 value within the laser welding machines market size and is anticipated to maintain the strongest regional growth at a 7.62% CAGR through the forecast period.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laser Welding Machines Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven seam tracking improves weld accuracy and first-pass yield in smart factories | +1.2% | Global; early use in Germany, Japan, South Korea | Medium term (2-4 years) |

| Automakers mandate laser welding for next-generation EV battery enclosures | +1.1% | China and South Korea, spreading to North America | Short term (≤ 2 years) |

| Green and blue lasers enable spatter-free copper welding in e-mobility components | +0.9% | Germany and China | Medium term (2-4 years) |

| Electronics OEMs require micro-joint precision for miniaturized PCB assemblies | +0.8% | Taiwan, South Korea, Vietnam | Short term (≤ 2 years) |

| Portable handheld fiber laser systems expand adoption in job shops and field repairs | +0.7% | North America, Europe, emerging South America | Long term (≥ 4 years) |

| Medical-device manufacturers adopt low-heat fiber welding for stents and catheters | +0.6% | North America, Europe, India | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

AI-driven seam tracking improves weld accuracy and first-pass yield in smart factories

Real-time seam-tracking fuses charge-coupled-device cameras, laser-triangulation sensors, and convolutional-neural-network software to correct part-placement errors during multi-pass welds. First-pass yields have climbed from roughly 88% to above 98% on German body-in-white lines, cutting scrap by 40% and trimming return-on-investment periods for robotic cells to under two years. Fanuc integrates edge inference that recalibrates focus within 50 milliseconds, while Panasonic reports similar gains on battery-tray lines. As labor costs rise in Eastern Europe and Southeast Asia, manufacturers view these accuracy improvements as an equalizer that justifies the up-front premium of Laser-welding machine market equipment. Broader deployment beyond premium cars into commercial vehicles is now underway as component variation declines and software tools mature.

Automakers Mandate Laser Welding for Next-Generation EV Battery Enclosures

Electric-vehicle batteries need hermetically sealed aluminum housings that arc welding cannot supply without porosity or spatter. Catl’s Ningde plant welded 3-mm aluminum enclosures in under 10 seconds per module using multi-kilowatt fiber lasers, achieving leak rates better than 1 × 10⁻⁵ mbar-L/s. Tesla and BYD have issued similar specifications for cell-to-pack joints, causing a single EV battery line to budget USD 30-50 million for Laser welding machines, market cells, even though legacy resistance welding costs one-fifth as much because the laser process eliminates expensive post-weld inspection at high volume. These directives explain why automotive accounts for the largest slice of current revenue and why Asia-Pacific still absorbs half of all new installations.

Green and Blue Lasers Enable Spatter-Free Copper Welding in E-Mobility Components

Copper reflects up to 95% of standard 1,070-nanometer fiber-laser energy, leading to unstable keyholes and metal expulsion. Operating at 515 nanometers, TruDisk green lasers push absorptivity toward 50%, enabling single-pass welds of 1.5-mm busbars at 4 m/min without pre-heat. Coherent’s 450-nanometer blue-diode system delivers comparable quality and is now on German hairpin lines for 800-volt inverters requiring resistance below 0.5 milliohms. Although these sources cost 50-70% more per watt and last only 10,000-15,000 hours, they unlock use cases that standard fiber lasers cannot reach, advancing the Laser welding machines market in Europe and China.

Electronics OEMs Require Micro-Joint Precision for Miniaturized PCB Assemblies

Smartphone and wearable brands are abandoning solder reflow for laser micro-welding as component pitch narrows below 0.3 millimeters and assemblies cannot tolerate temperatures above 200 °C. Hgtech’s scanner-equipped fiber systems weld nickel-plated steel tabs to copper foils in 100 milliseconds, erasing fatigue failures in devices tested to 1,500 g impacts. Apple’s 2025 titanium-frame iPhone used pulsed lasers that limited heat-affected zones to under 200 micrometers, preserving tensile strength above 900 megapascals. Contract manufacturers in Vietnam now switch between product codes in under 15 minutes, proving that laser flexibility offsets its capital premium at scale.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment compared with conventional MIG and TIG welding systems | -0.9% | Global; especially South America and MEA | Medium term (2-4 years) |

| Shortage of skilled laser-welding operators limits industrial adoption | -0.7% | North America, Europe; and emerging in APAC | Long term (≥ 4 years) |

| Reflective non-ferrous metals create process-stability challenges | -0.5% | Global, acute in e-mobility and aerospace | Short term (≤ 2 years) |

| Export restrictions on high-power laser systems disrupt supply chains | -0.4% | China, Russia, the Middle East | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High Capital Investment Compared With Conventional MIG and TIG Welding Systems

A turnkey robotic laser cell costs USD 150,000-500,000 versus USD 5,000-20,000 for a comparable metal-inert-gas station.[2]IEEE Editors, “AI Seam-Tracking for Automotive Welding,” ieee.org Small and medium enterprises, which make up over 60% of fabrication shops in North America and Europe, require three-year paybacks but need volumes above 10,000 parts annually to meet that hurdle. Duties of 15-35% on imported lasers inflate prices in Brazil, Nigeria, and Argentina, widening the gap. Germany’s Digital Now program offsets as much as 50% of qualified Industry 4.0 spending, but few similar subsidies exist elsewhere, so many firms keep buying arc gear despite higher consumables and rework costs over time.

Shortage of Skilled Laser-Welding Operators Limits Industrial Adoption

Fewer than 15% of the American Welding Society’s certified welders hold laser endorsements, and training demands 200-400 practical hours. Germany’s DVS pathway requires 400 hours, yet enrollment is falling as younger workers choose software careers. The median welder age in the United States topped 55 in 2025, with retirements outpacing entrants 3:1 across Midwestern hubs. High-volume auto plants counter with automation, but low-volume aerospace and medical shops still need skilled programmers to set weld schedules, creating a labor bottleneck that tempers the Laser welding machines market growth.

Segment Analysis

By Technology: Solid-state Lasers Widen Capability for Mixed-Metal Joints

Fiber platforms captured 43.6% of 2025 revenue, making them the largest technology slice of the laser welding machines market share. Buyers favor their 30–40% wall-plug efficiency and diode life that tops 30,000 hours, advantages that keep three-shift automotive plants productive. Solid-state lasers, chiefly neodymium-doped disk and Neodymium-doped Yttrium Aluminum Garnet, are the fastest risers, advancing at a 6.43% CAGR to 2031 as pulsed-waveform control produces splash-free aluminum-to-steel battery-tab welds in fewer than two pulses per joint. Carbon-dioxide units, once the default for 6-mm steel plate, now struggle because aluminum and copper absorb under 5% at 10.6 µm, a mismatch with e-mobility needs.

Disk lasers dominate high-peak-power micro-welding, joining pacemaker leads where heat-affected‐zone widths must stay under 100 µm. Diode lasers operating at 808–980 nm have niche applications in plastic welding for battery enclosures, remaining steady as transparent polymer joints prevent particulate contamination. Hybrid programmable sources, typified by nLight’s API-driven Corona family, let process engineers tune pulse shapes on the fly, shortening qualification cycles from six weeks to one. That flexibility is luring aerospace primes that must shift rapidly between titanium Grade 5 and Inconel 718 brackets without swapping optics.

Note: Segment shares of all individual segments available upon report purchase

By System Type: Portables Erode Robotic Dominance

Robotic-integrated cells generated 41.85% of 2025 revenue and still anchor high-volume Electric Vehicle (EV) battery lines running under ±0.5 second takt-time dispersion. These multi-kilowatt stations cost USD 200,000–400,000 apiece yet deliver 98% first-pass yield and embedded AI seam tracking that trims rework to single-digit parts per million. Handheld/Portable units under USD 20,000 are growing quickest at an 8.39% CAGR to 2031 as they remove the need for safety light curtains and fixed gantries on job-shop floors.

Pipeline contractors have cut field-repair times by 70% on API-grade X70 steel, and Chilean mine operators overlay wear plates on excavator buckets without hauling 15-ton assemblies to workshops. Stationary bench-top rigs remain vital in medical-device cleanrooms, where microscope eyepieces and foot-pedal triggers let technicians weld 10-100 pacemaker cans per shift with Cp k values above 1.67. Dual-purpose platforms that swap welding, cutting, and surface-cleaning heads claim less share, but their 15% price premium confines uptake to aerospace depots handling diverse alloys on a single line.

By Application: Automotive Leads, but Medical and BES Outpace

Automotive retained 30.92% of 2025 revenue, the largest among all uses, as body-in-white seam welding and aluminum battery enclosures demanded zero-defect joints under Verband der Automobilindustrie rules. Catl, LG Energy Solution, and Tesla consumed more than 2,000 robotic cells last year to hermetically seal packs at leak rates below 1 × 10⁻⁵ mbar-L/s. Yet the diversified others bucket, such as medical, jewelry, and battery-energy-storage (BES), is expanding at a 6.43% clip to 2031, making it the fastest cohort.

International Organization for Standardization (ISO) 13485 approvals push stent makers toward fiber lasers that keep Nitinol super-elasticity above 95% of virgin strain limits. Home-and-commercial BES suppliers such as Enphase, BYD, SolarEdge specify laser joining for 20,000-cycle battery modules where resistance must stay under 0.3 milliohms. Electronics micro-welding remains robust as smartphone flex boards drop below 0.3 mm pitch, while aerospace contracts for titanium airframe skins require keyhole welds no wider than 400 µm and porosity under 0.5% by volume.

Note: Segment shares of all individual segments available upon report purchase

By Material Type: Titanium Climbs on Airframe Adoption

Aluminum delivered 26.52% of 2025 revenue, the single-largest material slice, because electric vehicle battery housings and lightweight auto panels dominate annual tonnage. Titanium is the sprinter, growing 6.72% a year to 2031 as Airbus and Boeing shift wing ribs and fuselage frames from riveted to laser-welded Grade 5 sheets, eliminating post-weld heat treatment. Aluminum will continue to anchor high-volume welding demand as automakers accelerate lightweighting programs and battery-enclosure production scales with EV adoption. Its excellent thermal conductivity and compatibility with high-power fiber lasers make it the preferred material for automated welding lines in automotive and battery manufacturing.

Steel remains the volume workhorse for agricultural and construction machinery, yet its relative weight slips as carbon-fiber hybrids proliferate. Plastics, welded in transmission-mode setups with diode sources, keep niche relevance for sensor housings that need IP67 ratings across –40 °C to +125 °C thermal excursions.

Geography Analysis

Asia-Pacific owned 49.35% of 2025 revenue and is set to grow at 7.62% through 2031, sustaining the largest regional slice of the laser welding machines market share. Chinese hubs in Wuhan and Shenzhen shipped more than 3,000 multi-kilowatt fiber cells in 2025, while Han’s Laser and Raycus now manufacture diodes, fibers, and beam optics on the same campuses, shrinking lead times to four weeks. Japan’s precision electronics clusters favor pulsed solid-state tools that hit sub-100 µm spots for smartwatch battery tabs, and South Korea mandates green-laser copper welding on 800-V e-axle hairpins to curb electrical losses to under 0.5 milliohms. India, buoyed by Production-Linked Incentive subsidies, is ramping contract assembly of smartphones and EV power electronics, though import duties of 10–20% on laser sources still damp small-shop uptake.

North America is supported by approximately USD 8 billion in EV gigafactory investments made between 2024 and 2025 across Nevada, Texas, and Georgia. Tesla, General Motors, and Ford require hermetically sealed structural packs that integrate into the chassis and demand laser inline leak-testing at 100% throughput. Canada’s aerospace suppliers in Quebec weld titanium fuel tanks to AS9100D quality, but only 12% of national welders carry laser certificates, prolonging new-line commissioning to six months. Mexico absorbs spill-over work under United States-Mexico-Canada Agreement (USMCA), yet Small and Medium-sized Enterprises (SMEs) still lean on Middle Income Group (MIG) because average payback horizons exceed three years without vendor financing.

Europe grows more slowly but commands high-spec niches. German tier-ones deployed 800 robotic cells in 2025 alone, each running AI seam tracking to meet VDA zero-defect mandates on galvanized steel. France and Spain secured a USD 38 million Jenoptik deal for titanium wing boxes, aiming for 20% lighter airframe modules. Export licensing under the European Dual-Use Regulation tightens supply of >6 kW lasers to China and Russia, pushing EU vendors to co-engineer indigenous gallium-nitride diodes for copper busbars. South America and the Middle East & Africa remain nascent; Volkswagen’s Brazilian plant added four cells in 2025, yet capital outlay five to ten times higher than MIG limits broader regional spread.

Competitive Landscape

Competition remains moderate, with major companies such as Trumpf Group, IPG Photonics, Han’s Laser, Coherent, and Raycus shaping the competitive landscape. Trumpf deepened vertical integration by buying EHRT Maschinenbau in February 2025, pairing ultrasonic and laser heads in a single station for aluminum-to-copper joints that cut contact resistance to below 0.3 milliohms. IPG, after a 12% revenue dip in 2024, diverted USD 90 million into blue-diode R&D to reclaim copper-welding share from Coherent, whose 450 nm modules already run on German e-motor hairpin lines.

Chinese suppliers undercut Western prices by 30–40% through local diode fabs and in-house optics. Raycus opened a 50,000 m² Wuhan campus in August 2024 capable of 30,000 sources a year, while Huagong Tech (HGTECH) bundles robots, vision systems, and warranty service into all-Chinese packages attractive to Southeast-Asian tiers. Han’s Laser formed a joint R&D center with BYD that tunes 515 nm pulse sequences for 5 m/min copper busbar lines; early trials cut spatter to near zero.

Emerging disruptors aim at software openness and portability. NLight’s Corona platform lets customers change peak-power duration and pulse repetition via API calls, accelerating golden-joint transfer across global plants. Lincoln Electric’s PythonX handheld laser weighs 18 kg including a fume-extractor backpack, turning oil-pipeline repair crews into one-person operations that finish a crack fix in two hours instead of ten.[3]Lincoln Electric, “PythonX Handheld Launch,” lincolnelectric.com European startups such as Synova pitch laser-microjet hybrids that fire a water-confined beam, preventing oxidation on titanium orthopedic screws without inert gas shielding.

Laser Welding Machines Industry Leaders

TRUMPF Group

IPG Photonics Corporation

Han’s Laser Technology Group

Coherent Corp.

Jenoptik AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Lincoln Electric rolled out the PythonX portable 1.5 kW laser with four-hour battery runtime.

- February 2025: Amada Miyachi secured ISO 13485:2016 certification for its micro-welding systems used in implantables.

- February 2025: Trumpf Group acquired EHRT Maschinenbau, adding ultrasonic capability for hybrid aluminum-to-copper battery tabs.

- January 2025: Coherent Corp. committed USD 50 million to double Saxonburg's output of multi-kilowatt lasers by 2026.

Global Laser Welding Machines Market Report Scope

| Fiber |

| CO2 |

| Solid-State |

| Diode |

| Others (Hybrid, Green) |

| Hand-held/Portable |

| Stationary Bench-top |

| Robotic-Integrated Cell |

| Hybrid Multi-Function (Weld-Cut-Clean) |

| Automotive |

| Electronics |

| Aerospace & Defense |

| Mining |

| Oil & Gas |

| Others (medical, jewelry, BES, etc.) |

| Steel |

| Aluminum |

| Titanium |

| Copper |

| Plastics & Polymers |

| Others (other metals nickel, nickel alloys, precious metals, magnesium & alloys, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Technology | Fiber | |

| CO2 | ||

| Solid-State | ||

| Diode | ||

| Others (Hybrid, Green) | ||

| By System Type | Hand-held/Portable | |

| Stationary Bench-top | ||

| Robotic-Integrated Cell | ||

| Hybrid Multi-Function (Weld-Cut-Clean) | ||

| By Application | Automotive | |

| Electronics | ||

| Aerospace & Defense | ||

| Mining | ||

| Oil & Gas | ||

| Others (medical, jewelry, BES, etc.) | ||

| By Material Type | Steel | |

| Aluminum | ||

| Titanium | ||

| Copper | ||

| Plastics & Polymers | ||

| Others (other metals nickel, nickel alloys, precious metals, magnesium & alloys, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global spending on laser welding machines be by 2031?

The laser welding machines market size is projected to reach USD 5.06 billion by 2031, up from USD 3.77 billion in 2026.

Which technology is growing fastest within these machines?

Solid-state lasers lead growth at a 6.43% CAGR because their pulsed output welds dissimilar metals used in EV batteries and medical implants.

Why are blue and green lasers important for EV manufacturing?

They raise copper absorptivity to 40–60%, enabling spatter-free welds on 800-V busbars that must keep joint resistance below 0.5 milliohms.

What keeps small fabricators from buying robotic laser cells?

A turnkey system costs USD 150,000–500,000, five to ten times more than a comparable MIG setup, and many SMEs need paybacks inside three years.

Which region accounts for the biggest share today?

Asia-Pacific holds 49.35% of 2025 revenue thanks to China’s gigafactories and electronics contract manufacturers.