Ketogenic Diet Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13.77 Billion |

| Market Size (2031) | USD 17.88 Billion |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

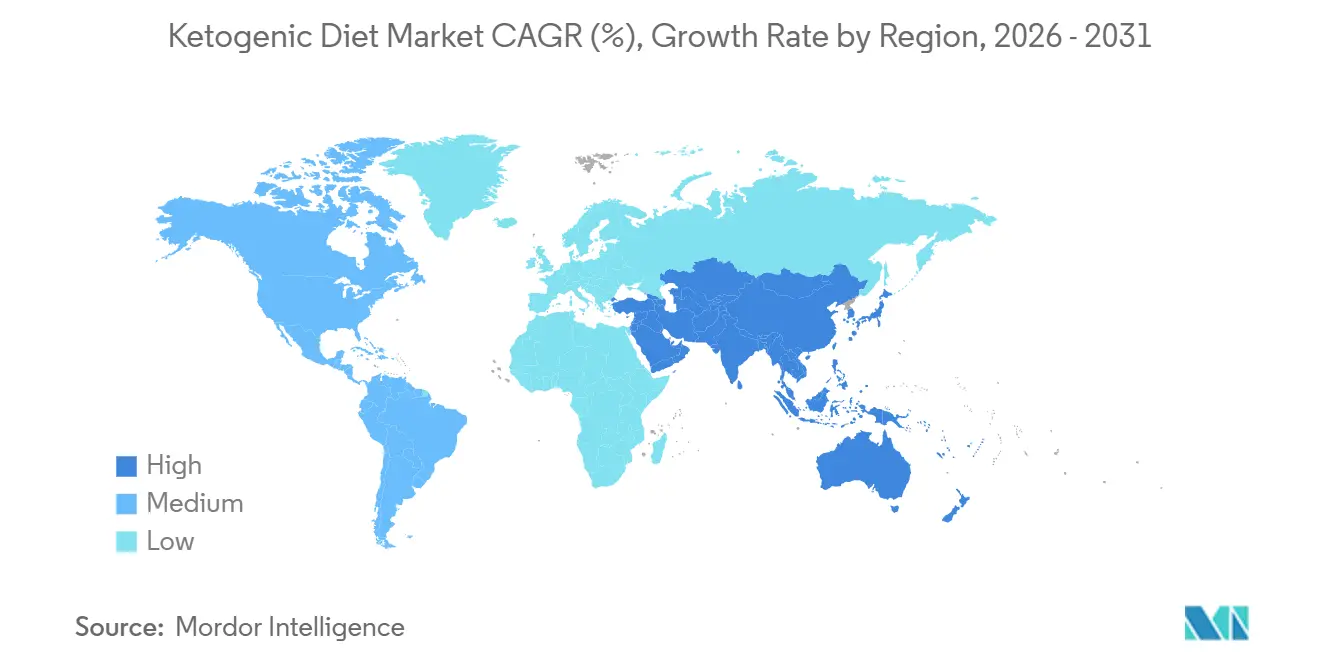

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Ketogenic Diet Market Analysis by ���ϲ�����

The Ketogenic Diet Market size was valued at USD 13.08 billion in 2025, increased to USD 13.77 billion in 2026, and is projected to reach USD 17.88 billion by 2031, registering a compound annual growth rate (CAGR) of 5.37% during the forecast period. The market's growth is primarily driven by the increasing global emphasis on metabolic health, weight management, and structured nutritional approaches aimed at mitigating lifestyle-related health risks. Rising awareness of carbohydrate reduction strategies, along with growing concerns about obesity and insulin resistance, has bolstered consumer interest in ketogenic dietary patterns as a structured eating approach. Additionally, market growth is supported by ongoing product innovation that improves taste, texture, and convenience, making keto-friendly options more accessible to a broader consumer base.

Key Report Takeaways

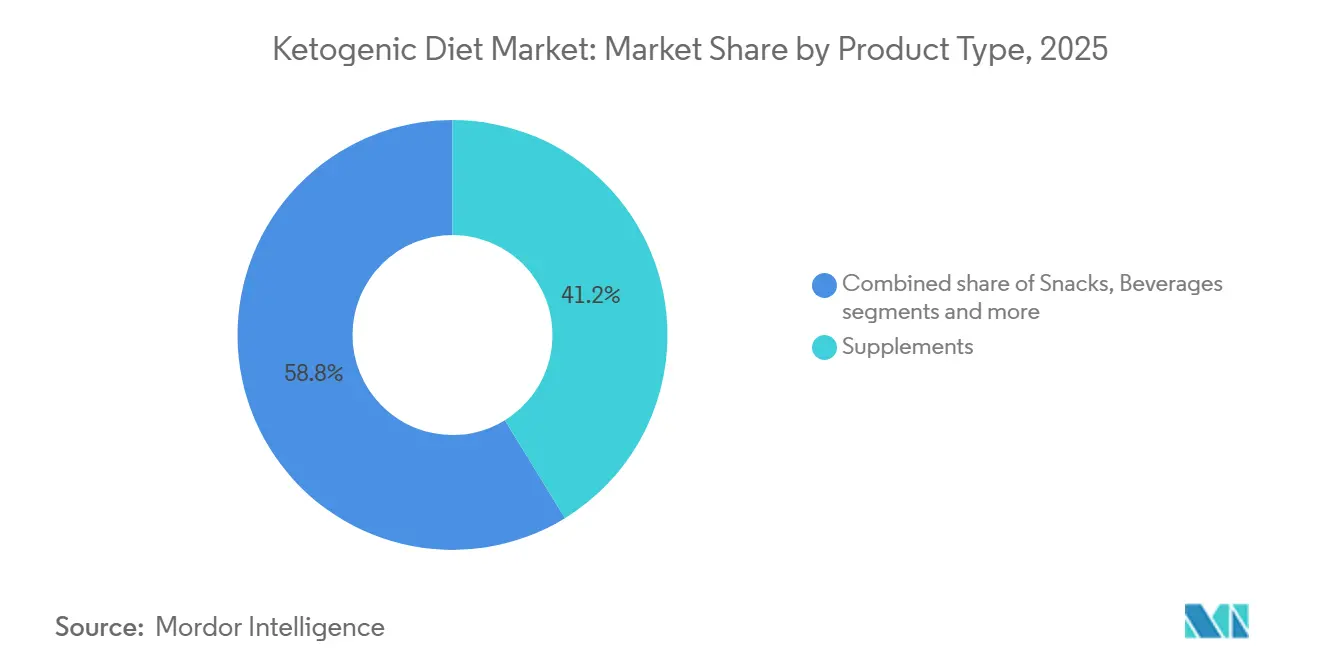

- By product type, supplements led with 41.23% of the ketogenic diet market share in 2025, whereas beverages are forecast to expand at a 5.87% CAGR through 2031.

- By nature, conventional products held 81.23% of the ketogenic diet market size in 2025, while organic offerings are projected to advance at a 6.56% CAGR to 2031.

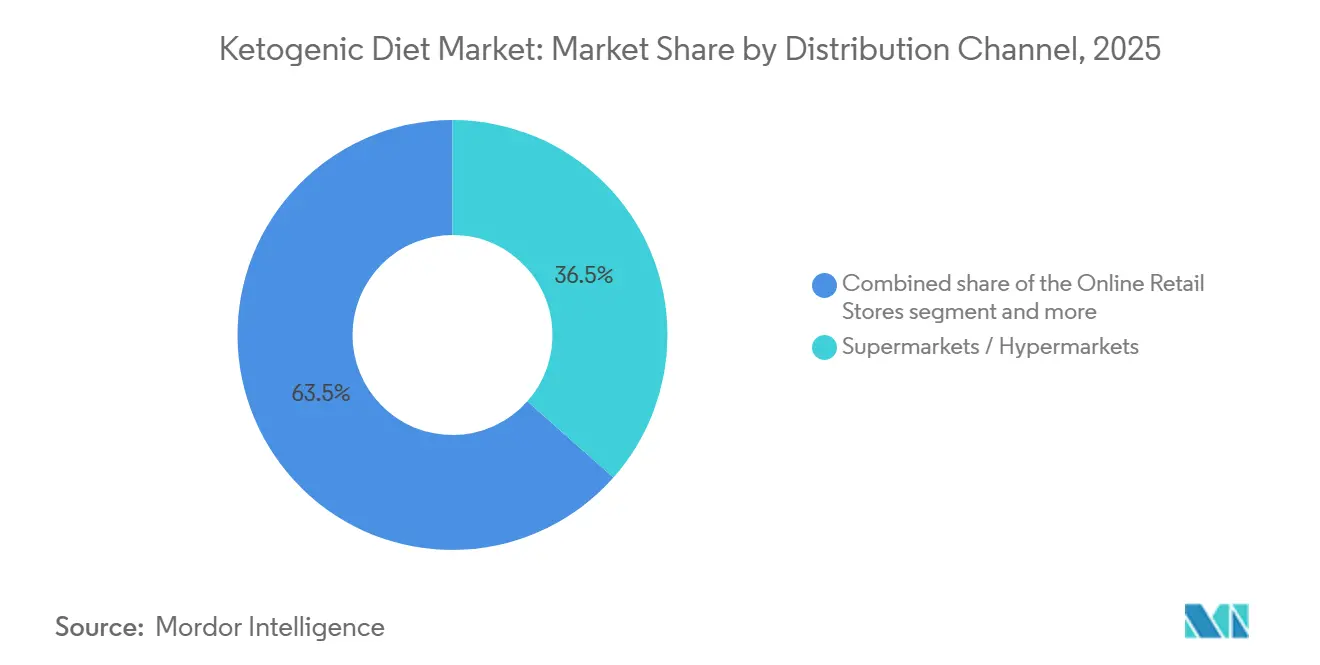

- By distribution channel, supermarkets/hypermarkets commanded 36.54% share of the ketogenic diet market size in 2025, yet online retail is set to grow fastest at 6.81% CAGR through 2031.

- By geography, North America captured 38.87% ketogenic diet market share in 2025; Asia-Pacific is forecast to post the strongest regional CAGR at 5.65% to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ketogenic Diet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in obesity and metabolic disorders | +0.9% | Global, with acute pressure in North America, Middle East, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Surge in fitness enthusiasm and athletic performance | +0.7% | North America, Europe, Australia; emerging in urban Asia-Pacific | Short term (≤ 2 years) |

| Product innovation in taste/texture and ready-to-eat formats | +0.8% | Global, led by North America and Europe innovation hubs | Medium term (2-4 years) |

| Development of plant-based keto options | +0.5% | North America, Europe, with spillover to Asia-Pacific vegetarian segments | Long term (≥ 4 years) |

| Social media and influencer impact | +0.6% | Global, strongest in North America, Europe, and digitally connected Asia-Pacific markets | Short term (≤ 2 years) |

| Rising interest in therapeutic uses beyond weight loss | +0.7% | North America, Europe (clinical adoption); Asia-Pacific (emerging awareness) | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rapid rise in obesity and metabolic disorders

The rising prevalence of obesity and related metabolic conditions is driving market growth. As consumers increasingly prioritize dietary interventions for weight management, glycemic control, and metabolic health, low-carbohydrate and ketogenic diets are gaining popularity as structured nutritional solutions. The ketogenic diet's focus on carbohydrate restriction and metabolic flexibility aligns with consumer objectives such as fat reduction, appetite regulation, and improved insulin sensitivity. Additionally, growing medical discussions around lifestyle-related disorders have heightened interest in controlled dietary strategies as preventive and complementary health measures. For example, the World Obesity Federation estimates that by 2025, approximately 1.6 million premature deaths from non-communicable diseases, including diabetes, cancer, heart disease, and stroke, will be linked to overweight and obesity [1]Source: World Obesity Federation , "World Obesity Atlas 2025", worldobesity.org. This statistic highlights the critical need for effective dietary management approaches.

Surge in fitness enthusiasm and athletic performance

The increasing global focus on fitness, body composition, and athletic performance is driving demand in the ketogenic diet market. As consumers adopt structured workout routines, strength training, endurance sports, and physique enhancement practices, dietary strategies that promote fat adaptation and sustained energy release are becoming more popular. The ketogenic diet is associated with improved metabolic efficiency and controlled carbohydrate intake, appealing to individuals aiming to optimize training outcomes, manage body fat, and maintain lean muscle mass. For example, according to the Health and Fitness Association, gyms, studios, and other fitness facilities in the United States recorded 77 million members in 2024, reflecting a significant level of active health engagement [2]Source: Health and Fitness Association, "How 77 Million Fitness Members Work Out", healthandfitness.org. This growing participation in fitness activities increases awareness of structured dietary approaches, including ketogenic diets, as individuals seek nutritional strategies to support performance and recovery.

Product innovation in taste/texture and ready-to-eat formats

Continuous innovation in taste enhancement, texture improvement, and ready-to-eat convenience formats is driving growth in the global ketogenic diet market. A key challenge for ketogenic diets has been the limited variety and reduced sensory appeal compared to traditional carbohydrate-rich foods. Manufacturers are addressing this issue by creating products that replicate conventional flavors and textures while adhering to strict low-carbohydrate requirements. Advances in food processing technologies, alternative binding systems, and reformulation techniques are improving consistency, creaminess, and overall palatability. For example, Keto Chow offers a Hearty Beef Single Meal Soup Base pouch, packaged in brown and white, featuring a bowl of soup with beef and herbs, labeled as Ultra Low-Carb. This shelf-stable, portion-controlled format illustrates how brands are expanding beyond powders and supplements to provide complete meal solutions that combine convenience with sensory satisfaction.

Development of plant-based keto options

The growth of plant-based keto options is influencing the market as manufacturers adapt to changing consumer preferences for sustainable, ethical, and plant-focused nutrition. Traditionally, ketogenic diets have depended heavily on animal-based fats and proteins, limiting their appeal to vegan, vegetarian, and flexitarian consumers. The introduction of plant-based low-carbohydrate protein sources and fat alternatives has broadened the consumer base by merging ketogenic and plant-based dietary approaches. This combination enables brands to address two growing lifestyle trends simultaneously: low-carb nutrition and plant-based eating. Furthermore, plant-based keto products often align with clean-label standards and environmentally conscious branding, enhancing their premium market positioning. As sustainability and ingredient transparency become increasingly significant factors in purchasing decisions, the availability of credible plant-based keto snacks, meal replacements, and functional foods improves inclusivity within the category.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict dietary restrictions and sustainability challenges | -0.3% | Global, acute in Europe and environmentally conscious North American segments | Medium term (2-4 years) |

| Limited product variety and availability | -0.3% | Asia-Pacific, Latin America, Middle East and Africa (distribution gaps); rural North America and Europe | Short term (≤ 2 years) |

| Cultural and dietary preferences | -0.2% | Asia-Pacific (rice-centric diets), Latin America (corn/beans), Mediterranean Europe, Middle East | Medium term (2-4 years) |

| Challenges in balanced nutrition | -0.2% | Global, with heightened scrutiny in North America and Europe from health authorities | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Strict dietary restrictions and sustainability challenges

Strict carbohydrate restrictions and rigid macronutrient requirements pose a significant challenge for the global ketogenic diet market. The diet necessitates maintaining a very low carbohydrate intake while consuming high levels of fat, which many consumers find difficult to sustain over the long term. This restrictive approach limits food variety, reduces flexibility in social and cultural eating contexts, and complicates meal planning. Consequently, long-term adherence becomes challenging for many individuals, resulting in higher dropout rates after initial trials. Sustaining ketosis requires consistent dietary discipline, careful label reading, and structured eating habits, which may not align with dynamic lifestyles or traditional dietary practices in various regions. Furthermore, the limited range of permissible food options can lead to monotony, discouraging repeat engagement with keto-specific products.

Limited product variety and availability

Limited product variety and inconsistent availability serve as significant restraints in the market. Despite advancements in innovation, the range of keto-compliant products remains narrower compared to conventional food categories. Many mainstream food items exceed permissible carbohydrate levels, limiting consumer options and making adherence to the diet reliant on a smaller selection of specialized products. This limited variety can result in taste fatigue and decreased long-term commitment, particularly among new users seeking more diverse flavors and meal options. In many regions, keto-specific products are primarily available in specialty health stores or select retail chains, restricting broader accessibility. Smaller markets often lack locally produced keto products, leading to a reliance on imports and reduced consistency in product availability.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beverages Propel RTD Shift

The supplements segment accounted for a remarkable 41.23% share in 2025, propelled by its unparalleled convenience, highly advanced functionality, and strong alignment with rapidly transforming consumer performance goals. The escalating demand for revolutionary metabolic health support, accelerated weight management solutions, sustained energy release, and enhanced cognitive performance firmly established supplements as indispensable performance-oriented tools rather than traditional dietary aids. The segment also experienced unprecedented advancements through transformative innovations in clean-label formulations, sugar-free sweeteners, plant-based keto proteins, and flavored ready-to-mix formats that significantly elevated palatability.

The beverages segment, anticipated to grow at a CAGR of 5.87% through 2031, is driven by advantages specific to liquid product formats rather than factors associated with supplements. Beverages benefit from higher consumption frequency compared to other keto categories, as they are incorporated into daily hydration and refreshment routines, leading to stronger repeat purchase cycles. The segment also gains from prominent shelf visibility in retail coolers and functional drink aisles, which boosts impulse purchases and facilitates brand discovery. Additionally, beverage products offer smooth, ready-to-consume textures that eliminate preparation barriers, simplifying adoption for first-time keto consumers. Flavor diversification and premium positioning have further broadened the category's appeal, attracting health-conscious consumers seeking low-carb alternatives to traditional soft drinks and sugary beverages.

By Nature: Organic Gains Clean-Label Premium

The conventional segment, projected to hold an 81.23% market share in 2025, dominates due to its broader ingredient flexibility, scalable manufacturing processes, and stronger price competitiveness compared to organic alternatives. Conventional keto products enable manufacturers to source a wider range of approved low-carb ingredients without the certification constraints associated with organic production. This allows for faster product development and portfolio expansion. Additionally, this flexibility supports mass-market distribution across supermarkets, convenience stores, pharmacies, and online platforms, enhancing accessibility to a broader consumer base. Conventional products also typically offer longer shelf stability and more consistent supply availability, strengthening retail partnerships and global export potential.

The organic segment is projected to grow at the fastest CAGR of 6.56% through 2031, driven by increasing consumer preference for clean-label, minimally processed, and certification-backed food products within the ketogenic category. As keto consumers increasingly associate dietary discipline with overall wellness and ingredient transparency, demand for products free from synthetic additives, pesticides, artificial sweeteners, and genetically modified components is accelerating. Organic certification enhances trust and perceived product integrity, particularly among premium and health-conscious buyers who closely scrutinize ingredient sourcing and production methods. For example, according to the German Federation of Organic Food Producers (BÖLW), organic food revenues in Germany reached EUR 16.99 billion in 2024, reflecting strong and sustained consumer demand for certified organic products [3]Source: German Federation of Organic Food Producers (BÖLW), "Revenue from organic food in Germany", boelw.de.

By Distribution Channel: Online Retail Disrupts Traditional

Supermarkets and hypermarkets are projected to account for a 36.54% market share in 2025, dominating the distribution landscape due to their broad product assortment, high consumer footfall, and strong shelf visibility. These retail formats offer centralized access to various keto product categories, enabling consumers to compare brands, review nutritional labels, and make informed purchasing decisions in one location. Large-format retailers benefit from established supply chain networks and bulk procurement capabilities, ensuring consistent stock availability and competitive pricing. Additionally, impulse purchasing behavior is more prevalent in physical retail environments, particularly for newly launched or promotional keto items strategically placed in high-traffic areas. The expansion of private-label products within supermarkets has further contributed to their dominance, as retailers introduce affordable keto alternatives under their own brands, increasing accessibility for mainstream consumers.

The online retail segment is projected to grow at the fastest CAGR of 6.81% through 2031, driven by its structural advantages in product variety, targeted marketing, and consumer education within the ketogenic diet market. Online platforms provide access to a significantly broader assortment of niche and specialty keto products that may not be available in traditional stores. This extensive catalog supports the discovery of emerging brands, premium formulations, and newly launched innovations. Digital retail also offers detailed product descriptions, nutritional transparency, ingredient breakdowns, and verified consumer reviews, which are essential for keto consumers who carefully evaluate carbohydrate counts and formulation quality. Subscription models and auto-replenishment options further enhance repeat purchase behavior, particularly for staple keto products.

Geography Analysis

North America is projected to hold a 38.87% market share in 2025, dominating the global ketogenic diet market. This leadership is attributed to strong consumer awareness of low-carbohydrate lifestyles, the widespread availability of keto-labeled products, and a mature functional food ecosystem. The region benefits from the early adoption of ketogenic protocols within weight management and wellness communities, coupled with extensive product penetration in mainstream retail and specialty nutrition stores. Robust product innovation pipelines, intense brand competition, and strategic marketing efforts have further consolidated the market. Additionally, the presence of large-scale manufacturers and well-developed distribution networks ensures high product visibility and consistent supply across supermarkets, pharmacies, and digital platforms.

Asia-Pacific is expected to grow at the fastest CAGR of 5.65% through 2031, emerging as a high-potential region. This growth is driven by shifting dietary patterns, increasing health consciousness, and the rapid expansion of modern retail infrastructure. Urbanization and the adoption of westernized eating habits have fueled interest in weight management solutions, encouraging the uptake of low-carb dietary alternatives. The region is also experiencing rising demand for functional and fortified foods, creating opportunities for keto-compatible innovations. The expansion of e-commerce ecosystems, particularly in major Asian economies, has improved access to both imported and domestic keto brands. Furthermore, younger consumer demographics are actively engaging with digital health trends and lifestyle-based diets, accelerating regional adoption.

Europe, South America, and the Middle East & Africa collectively represent steadily expanding markets, supported by evolving dietary awareness and increasing penetration of specialty health foods. Europe benefits from strong clean-label preferences and regulatory clarity regarding nutritional labeling, which supports the growth of keto-aligned product formulations. In South America, gradual adoption is driven by rising interest in weight control and premium functional foods, although market maturity remains moderate. Meanwhile, the Middle East & Africa region is experiencing early-stage growth, supported by expanding retail modernization and the emergence of health-focused consumer segments.

Competitive Landscape

The global ketogenic diet market is moderately fragmented, with competition spanning multinational food corporations and specialized keto-focused brands. Key players in the market include Nestlé S.A., Perfect Keto LLC, Bulletproof 360 Inc., Ancient Brands LLC, and Dang Foods Co. Large multinational companies utilize robust Research and Development (R&D) capabilities, extensive global supply chains, and established retail networks to expand their keto-aligned product offerings. Meanwhile, niche players differentiate themselves through specialized formulations, direct-to-consumer strategies, and strong brand recognition within low-carb consumer communities. The competitive landscape is dynamic, driven by frequent product launches, reformulations, and portfolio diversification that influence market positioning.

Companies are increasingly focusing on therapeutic applications, particularly medically supervised ketogenic solutions aimed at supporting metabolic and neurological health. Additionally, there is a growing emphasis on plant-based formulations as manufacturers seek to cater to vegan and flexitarian dietary preferences while maintaining keto compatibility. Innovation efforts prioritize clean-label ingredients, sugar-free alternatives, and improved taste profiles to broaden the appeal of ketogenic products. Firms are also investing in localized product development to align with regional taste preferences and regulatory requirements, especially in high-growth emerging markets where dietary habits differ significantly from those in Western markets.

Disruptors in the ketogenic diet market are increasingly leveraging personalized nutrition platforms that utilize digital diagnostics, biomarker tracking, and algorithm-driven diet customization to enhance consumer engagement. These platforms go beyond standardized keto meal plans by offering tailored macronutrient ratios, individualized product recommendations, and real-time metabolic feedback. By integrating wearable health devices, glucose monitoring systems, and AI-powered dietary analytics, personalized nutrition companies are developing adaptive keto programs that respond to user-specific metabolic needs, moving away from one-size-fits-all approaches.

Ketogenic Diet Industry Leaders

-

Nestlé S.A.

-

Perfect Keto LLC

-

Bulletproof 360 Inc.

-

Ancient Brands LLC

-

Dang Foods Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Ghodawat Consumer Limited (GCL) has introduced Coolberg Diet, India's first zero-sugar malt beverage. It contains less than 5 kcal per 100 ml, no added sugar, and no caffeine, making it suitable for gym-goers, diabetics, and individuals following a keto diet.

- April 2025: The low-carb brand HeyLo! has introduced new brownie bars in Choco, Ginger, and Orange flavors to address the increasing demand in the keto and low-carb market. These bars are fudgy, vegan, gluten-free, and high in fiber, made with almond flour, chicory root fiber, and natural sweeteners.

- January 2025: Chunk Foods has achieved the distinction of being the first plant-based meat producer to receive Ketogenic Certified status. This certification was awarded for its vegan steak, which is formulated using soy protein.

Global Ketogenic Diet Market Report Scope

Keto is short for ketogenic, referring to a diet or food that is low in carbohydrates but high in protein. While originating as a medical diet, it is popularly associated with weight loss. It also helps in boosting metabolism, reducing appetite, and improving the balance of the gut. The report on ketogenic diet food is segmented by product type into supplements, beverages, snacks, and other product types. By Nature, the market is segmented into conventional and organic. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty nutrition stores, pharmacy/drug stores, convenience stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Supplements | Ketone Salts |

| Ketone Esters | |

| MCT Oil | |

| Others | |

| Snacks | Bars |

| Nuts and Seed Mixes | |

| Cookies and Brownies | |

| Meat and Cheese Snacks | |

| Beverages | Ready-To-Drinks |

| Shakes | |

| Coffee and Creamers | |

| Dairy and Dairy Alternatives | |

| Others |

| Conventional |

| Organic |

| Supermarkets/Hypermarkets |

| Specialty Nutrition Stores |

| Pharmacy/Drug Stores |

| Convenience Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Supplements | Ketone Salts |

| Ketone Esters | ||

| MCT Oil | ||

| Others | ||

| Snacks | Bars | |

| Nuts and Seed Mixes | ||

| Cookies and Brownies | ||

| Meat and Cheese Snacks | ||

| Beverages | Ready-To-Drinks | |

| Shakes | ||

| Coffee and Creamers | ||

| Dairy and Dairy Alternatives | ||

| Others | ||

| By Nature | Conventional | |

| Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Nutrition Stores | ||

| Pharmacy/Drug Stores | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global ketogenic diet market in 2031?

The ketogenic diet market size is forecast to reach USD 17.88 billion by 2031.

Which product type is expected to grow fastest through 2031?

Ready-to-drink beverages show the highest CAGR at 5.87%, driven by flavor innovation and convenience.

Why is Asia-Pacific considered the most attractive growth region?

Urbanization-led obesity spikes and rising middle-class spending push Asia-Pacific to a leading 5.65% CAGR despite distribution hurdles.

Which sales channel offers the strongest growth outlook?

Online retail is expanding at 6.81% CAGR thanks to subscription bundles and data-driven personalization.

Page last updated on: