Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

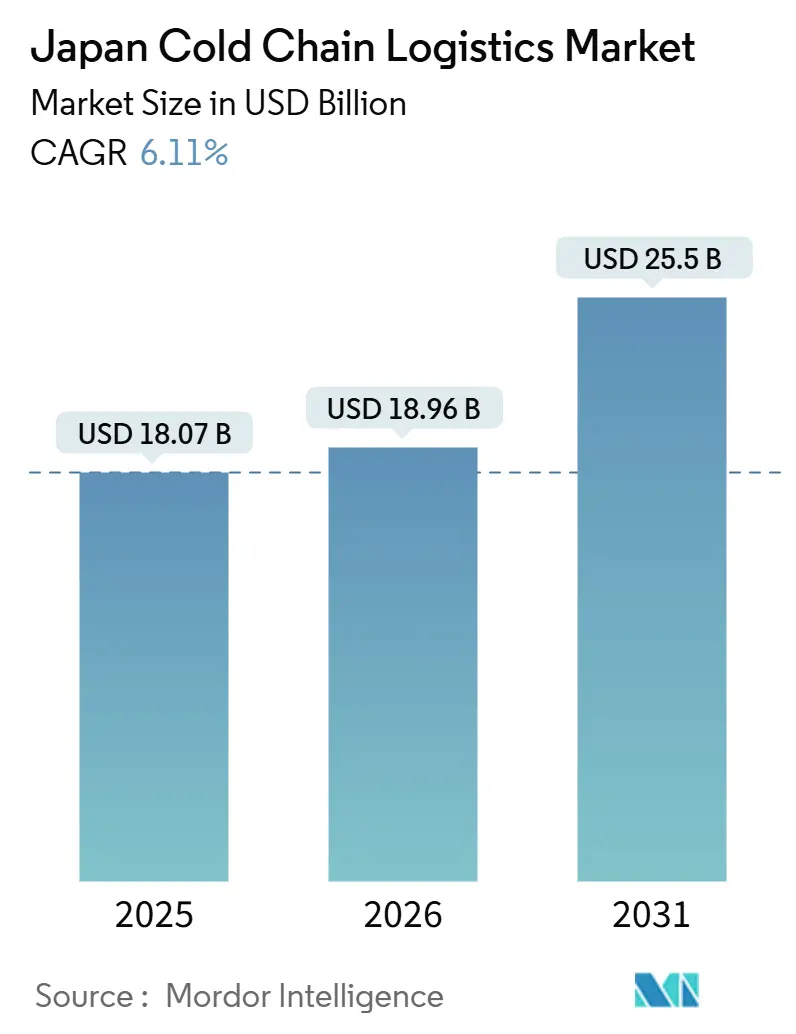

| Base Year Market Size (2025) | USD 18.07 Billion |

| Market Size (2026) | USD 18.96 Billion |

| Market Size (2031) | USD 25.5 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

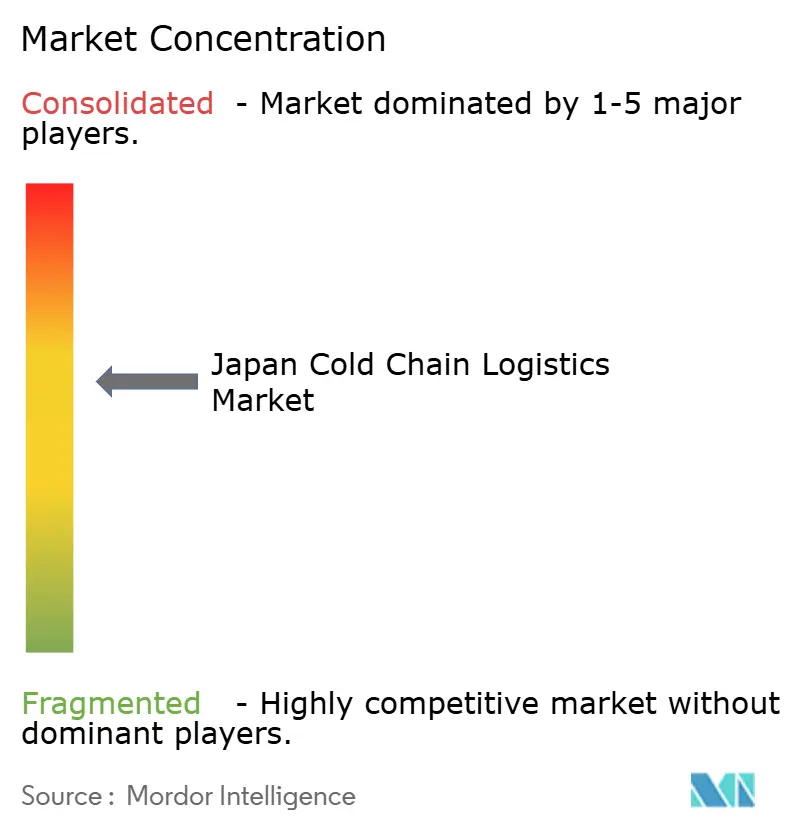

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Japan Cold Chain Logistics Market Analysis by ���ϲ�����

The Japan cold chain logistics market size is expected to increase from USD 18.07 billion in 2025 to USD 18.96 billion in 2026 and reach USD 25.5 billion by 2031, growing at a CAGR of 6.11% over 2026-2031.

Continued urbanization, population aging, and dietary shifts toward convenience products are fueling steady volume growth, encouraging operators to replace reactive expansion with long-range infrastructure planning. Investments in automated storage, hydrogen or battery-electric reefer fleets, and low-GWP refrigeration systems advance operational resilience while reducing emissions. Retailers convert thousands of convenience stores into micro-fulfillment nodes, shrinking last-mile distances for chilled groceries and pharmaceuticals. Rising biologic and vaccine pipelines add premium 2-8 °C cargo, widening profit margins and spurring carrier upgrades in documentation and monitoring capabilities. Simultaneously, trade agreements under the Regional Comprehensive Economic Partnership strengthen export incentives for seafood, meat, and fresh produce, reinforcing the Japan cold chain logistics market as a gateway between Northeast Asia and global demand centers.

Key Report Takeaways

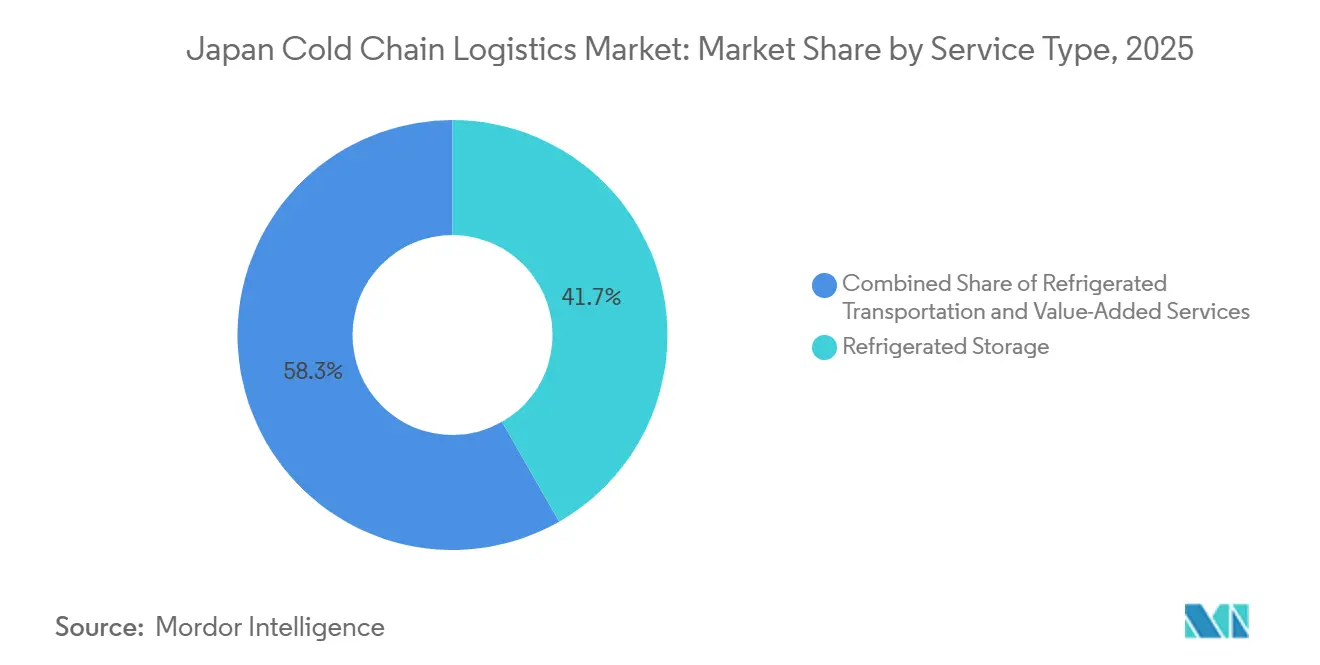

- By service type, refrigerated storage led with 41.74% of Japan cold chain logistics market share in 2025, while Value-added Services is forecast to expand at an 8.25% CAGR through 2031.

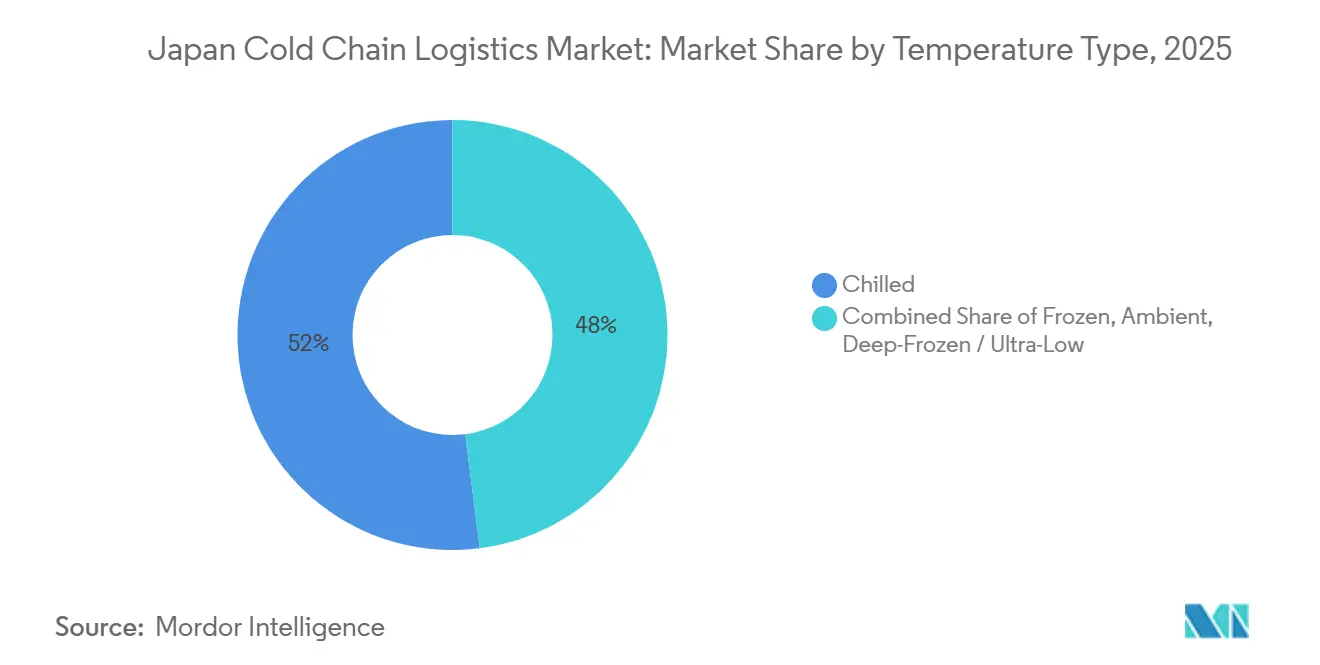

- By temperature type, the chilled segment commanded 52.02% of the Japan cold chain logistics market size in 2025; the frozen segment is projected to advance at a 7.01% CAGR between 2026 and 2031.

- By application, meat and poultry accounted for a 22.54% share of the Japan cold chain logistics market size in 2025, and vaccines & clinical trial materials are moving at a 7.36% CAGR through 2031.

- By geography, Kanto held 27.97% of Japan cold chain logistics market share in 2025, whereas Kyushu & Okinawa recorded the highest projected 8.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid take-up of e-grocery platforms demanding chilled last-mile fulfilment | +1.4% | Metropolitan areas, Kanto and Kansai concentration | Short term (≤ 2 years) |

| Rising pipeline of biologics and cell-/gene-based medicines needing 2-8°C transit | +1.0% | National pharmaceutical corridors, urban medical centers | Medium term (2-4 years) |

| State-backed vaccine reserve programs expanding cold-warehouse leasing | +0.7% | Strategic national distribution hubs | Medium term (2-4 years) |

| Frozen seafood exports accelerating under new free-trade concessions | +0.9% | Coastal processing zones, Hokkaido, Kyushu export gateways | Long term (≥ 4 years) |

| Vision-guided AS/RS robotics increasing pallet throughput per m² | +0.8% | Major logistics parks, automated warehouse clusters | Long term (≥ 4 years) |

| Roll-out of zero-emission electric reefer fleets supported by green incentives | +0.5% | Urban delivery zones, government pilot corridors | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rapid Take-Up of E-Grocery Platforms Demanding Chilled Last-Mile Fulfillment

Rakuten Mart, launched in 2024, now processes about 70,000 daily orders and serves 12 million households, relying on micro-fulfillment centers with multi-temperature automation[1] Rakuten Group, “Rakuten Mart Launch,” rakuten.com . Seven-Eleven’s 7NOW app connects roughly 20,000 stores to same-hour delivery, converting convenience outlets into distributed cold chain nodes. Retailers leverage these networks to monetize excess cold storage and shorten inventory cycles, challenging pure-play logistics specialists to match their consumer reach. Aeon equips delivery crews with fan-integrated uniforms and heat-wave allowances to protect labor productivity in peak summers. Reducing the density of urban drop points reduces truck kilometers per order, cutting emissions and reinforcing Japan's cold chain logistics market as an urban service benchmark

Rising Pipeline of Biologics and Cell or Gene Therapies Needing 2-8 °C Transit

New piperidine-based lipid carriers extend mRNA shelf life at standard refrigeration, redirecting infrastructure spending from -80 °C freezers toward precision 4 °C facilities[2]Nature Communications, “mRNA Lipid Thermostability,” nature.com . The Tsukuba Medical Logistics Center Phase 2, inaugurated in 2025, illustrates investment in triple-zone warehouses with redundant power that meet PMDA audit trails. Concentrated production clusters around Tsukuba and Kobe magnify regional capacity imbalances, prompting service providers to build satellite depots in underserved prefectures. Regulatory familiarity becomes a key differentiator as operators embed electronic batch-release records into transport management systems.

State-Backed Vaccine Reserve Programs Expanding Cold-Warehouse Leasing

Long-term leasing agreements under government vaccine stockpiling schemes guarantee throughput for specialized -70 °C chambers, moving cold storage from a commercial asset to a national security utility. Operators such as Sagawa Express deploy real-time temperature and GPS telemetry that allows ministries to audit the chain of custody within minutes. Standardized protocols harmonize regional depots, boosting demand for interoperable IoT platforms. Lease stability lowers financing costs for new builds yet concentrates competition among firms with proven compliance credentials. The emphasis on redundant cooling and backup generators accelerates the rollout of on-site solar and battery systems that cushion grid interruptions.

Frozen Seafood Exports Accelerating Under New Free-Trade Concessions

Japan’s exports of agricultural, forestry, fishery products, and food reached about JPY 1.70 trillion (USD 10.9 billion) in 2025, even as seafood volumes fell due to China’s import ban. Maritime cold chain innovations, therefore, extend the Japan cold chain logistics market beyond domestic shorelines. In response to shifting trade flows, exporters are investing in higher-spec reefer containers, real-time temperature telemetry, and shock-resistant packaging to safeguard premium seafood over longer transit routes. Shipping lines are upgrading port-side plug-in capacity and pre-cooling infrastructure to minimize temperature deviations during dwell time. Meanwhile, insurers and buyers increasingly require end-to-end digital traceability, pushing logistics providers to integrate IoT monitoring with customs documentation. These enhancements not only protect cargo integrity but also elevate Japan’s reputation as a reliable supplier in high-value global food markets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking pool of certified refrigerated-vehicle drivers | -1.2% | National, acute in rural and inter-regional corridors | Short term (≤ 2 years) |

| High metropolitan land and construction costs curbing new cold-depot builds | -0.9% | Tokyo, Osaka, Nagoya metropolitan zones | Medium term (2-4 years) |

| Summer grid brownouts threatening integrity of ultra-low-temperature storage | -0.5% | Urban centers during peak demand periods | Short term (≤ 2 years) |

| Mandatory HFC refrigerant phase-down driving costly system retrofits | -0.7% | National, affecting legacy infrastructure | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Shrinking Pool of Certified Refrigerated-Vehicle Drivers

Cold chain fleets face deeper gaps because drivers need extra handling credentials. Nippon Express invested in Gatik AI to fast-track autonomous middle-mile trucks and joined a Tokyo-Osaka automated corridor scheduled for trial runs in 2027, signaling multi-modal solutions to the labor crunch. Hybrid truck-rail pilots already move temperature-sensitive cargo from Hokkaido to Kansai, showcasing interim fixes while full automation matures. Rural areas suffer the sharpest shortages, forcing network consolidation and higher last-mile fees that can erode product freshness windows.

High Metropolitan Land and Construction Costs for New Depots

Record land prices around Tokyo Bay and Osaka’s waterfront are pushing investors into peripheral prefectures such as Ibaraki and Chiba, where Sankei Building is developing three multi-temperature warehouses. The Okayama CONNECT Logistics Center, opened in 2025, became the Chugoku region’s largest cold store by exploiting lower land costs while installing large-scale solar and lithium batteries to curb energy bills. Vertical AS/RS designs help recoup the cost of expensive plots by increasing pallet density, but steep capex requirements lock out small operators and accelerate mergers. Peripheral builds lengthen delivery runs into central business districts, increasing fuel-cost exposure and delivery uncertainty during peak traffic.

Segment Analysis

By Service Type: Shifting to Value-Creation Beyond Basic Storage

Value-added Services is projected to grow at an 8.25% CAGR through 2031, while Refrigerated Storage accounted for 41.74% of Japan's cold chain logistics market share in 2025, supporting inventory buffers for approximately 56,054 convenience stores that collectively generated roughly USD 75.8 billion in annual sales. Underlying sales volume will keep cold warehouses full, yet margins increasingly hinge on integrated inspection, kitting, and data-reporting capabilities that protect cargo value and compliance.

Clients now ask third-party logistics providers to manage import duty refunds, barcode translation, and temperature audit packages, driving deeper service. Refrigerated Transportation diversifies as Kuribayashi’s Ro-Ro solution cuts Osaka-Sendai lead times to 3 hours while lowering emissions, illustrating modal realignment. Private warehousing is gaining ground among pharma firms that build bespoke cleanrooms, whereas public multi-client depots still dominate fast-moving consumer goods. Technology tiering intensifies: operators offering IoT, blockchain traceability, and under-2-hour recall-readiness capture premium contracts, magnifying differentiation in the Japan cold chain logistics market.

Note: Segment shares of all individual segments available upon report purchase

By Temperature Type: Frozen Gains Momentum, Chilled Retains Scale

The chilled band (0-5 °C) maintained a 52.02% share of the Japan cold chain logistics market size in 2025 because it handles dairy, meat, and vaccines, which are daily necessities across more than 50,000 retail outlets. Frozen cargo (-18 °C to 0 °C) is slated for a 7.01% CAGR through 2031, driven by quick-service restaurants that will adopt frozen side dishes and by Daibreak’s Art-Lock technology that allows sushi to reach United States supermarkets without textural loss. Deep-frozen chambers below -50 °C are expanding across Hokkaido fisheries and radiopharma labs, yet they continue to remain a niche segment.

Electricity intensity drives innovation; Mitsubishi Heavy’s R32 LXZ units deliver a 6.4 COP even under -25 °C loads, trimming energy per pallet. Demand response programs show ultra-low depots can earn grid fees, potentially offsetting higher energy bills. As refrigerant rules tighten, many mid-life -10 °C rooms will leapfrog to natural CO₂ or ammonia systems that future-proof assets and accelerate carbon reporting gains.

Note: Segment shares of all individual segments available upon report purchase

By Application: Pharma Logistics Outpaces Food Staples

Meat & Poultry remains the largest line item, accounting for 22.54% of the Japan cold chain logistics market share in 2025, propelled by convenience meal kits and active trade with Southeast Asia. Yet vaccines & clinical trial materials are forecast to grow at a 7.36% CAGR, driven by mRNA platforms and state reserve programs that ensure consistent throughput. Fish & Seafood reorients toward North American customers, with Aomori salmon consolidation enabling a stable year-round supply.

Pharmaceuticals & Biologics rise on surging GLP-1 exports and on economic incentives for cell and gene therapy manufacturing. Ready-to-Eat meals benefit from dual-income households and e-grocery services' call for 20-minute deliveries. Specialty chemicals, especially temperature-sensitive photoresists for chips, are expanding alongside Hokkaido semiconductor fabs, demanding customized hazard-class segregation in multi-chamber warehouses.

Geography Analysis

Kanto anchored 27.97% of Japan cold chain logistics market share in 2025 thanks to Narita and Haneda air gateways and the Tokyo Bay port cluster that funnels imports to 37 million residents. The Goka Hub Center provides 18,891 m² of chilled and frozen space with backup generators that ensure 120-hour autonomy, yet land scarcity pushes new builds into Ibaraki and Chiba, where highway access offsets longer urban runs. Rising congestion charges and labor shortages erode cost advantages, prompting interest in rail shuttles to inner-city depots.

Kyushu & Okinawa outpaces every other region with a forecast CAGR of 8.13%, leveraging direct shipping lanes to ASEAN under RCEP. Kitakyushu’s 24-hour marine airport serves as a multimodal hub for seafood, flowers, and biologics that require same-day delivery to Seoul or Shanghai[3]Kitakyushu City, “National Strategic Special Zone Outline,” tokku-kitakyushu.jp . Lower wage and land costs lure depot investors, and prefectural grants subsidize solar rooftops that cushion subtropical power spikes.

Kansai merges Expo 2025 showmanship with pragmatic logistics upgrades, such as Nippon Express’s Protect Box Thermal, which eliminates the need for gel packs. Chubu links east and west with Nagoya rail junctions; it gains share as automotive and food processors co-locate distribution in integrated parks. Hokkaido & Tohoku intensify seafood and produce exports via new cold piers, while Chugoku and Shikoku close historic capacity gaps through Okayama CONNECT’s high-density build. Together, these regions demonstrate Japan’s polycentric pattern, where each prefecture adds a unique specialization that lifts the resilience of the entire Japan cold chain logistics market.

Competitive Landscape

Japan’s cold chain logistics market is moderately concentrated, with a few leading firms controlling a significant share of capacity while smaller regional and niche operators continue to compete. Strategic consolidation reshapes competition yet leaves ample room for niche operators. Mitsui’s 2025 acquisition of HAVI sealed access to multinational QSR clients, reinforcing its end-to-end foodservice vertical. Asahi Logistics absorbed Rainbow Logistics, expanding Kanto-Kansai line-haul coverage and announcing a 22,000 m² Ibaraki depot that opens in 2026[4].Asahi Logistics, “Rainbow Logistics Integration,” asahi-logistics.co.jp

Nippon Express partners with Gatik AI for autonomous middle-mile routes and unveiled Protect Box Thermal, signaling technology as a key differentiator. Market share dispersion persists because regional specialists hold entrenched contracts with prefectural cooperatives and fisheries. Family-owned cold stores in Tohoku and Shikoku survive by offering custom fish fillet processing or rice-cake shock-freezing services, niches unattractive to conglomerates.

Sustainability promises, such as DHL’s hydrogen trucks or Bushu Ice’s solar microgrid, influence bid evaluations as shippers chase Scope 3 reductions. Equipment makers like Mitsubishi Heavy Industries and Mayekawa profit from retrofit mandates and step-change refrigeration technologies, reinforcing upstream-downstream interdependencies within Japan's cold chain logistics industry.

Japan Cold Chain Logistics Industry Leaders

Nippon Express

Kintetsu World Express

Yamato Holdings

Nichirei Logistics Group

Mitsubishi Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Nippon Express Holdings Co., Ltd. launched a new digital platform to enhance real‑time tracking and visibility of temperature‑controlled shipments. This marks a push toward digital cold chain transparency and improved operational reliability.

- October 2025: Kuehne + Nagel entered into a dedicated cold chain logistics partnership with a major biopharmaceutical firm in Japan, strengthening its healthcare logistics footprint and tailored temperature‑sensitive handling services.

- August 2025: Nippon Express launched a new cross‑border e‑commerce logistics service for overseas sellers targeting Japan using its DCX (Digital Commerce Transformation) platform, improving digital cold logistics integration for imports.

- May 2025: Kuhene+Nagel Signed a lead logistics provider (LLP) agreement with Evonik covering Asia‑Pacific, including Japan. This broadens integrated logistics responsibilities that can include temperature‑controlled freight in the region.

Japan Cold Chain Logistics Market Report Scope

By Service Type

| Refrigerated Storage | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0-5 °C) |

| Frozen (-18-0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

By Application

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Applications |

By Region (Domestic)

| Kanto |

| Kansai |

| Chubu |

| Kyushu and Okinawa |

| Hokkaido and Tohoku |

| Rest of Japan |

| By Service Type | Refrigerated Storage | |

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5 °C) | |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Applications | ||

| By Region (Domestic) | Kanto | |

| Kansai | ||

| Chubu | ||

| Kyushu and Okinawa | ||

| Hokkaido and Tohoku | ||

| Rest of Japan | ||

Key Questions Answered in the Report

What is the projected value of Japan’s cold chain logistics sector by 2031?

It is forecast to reach USD 25.50 billion, expanding at a 6.11% CAGR from 2026 to 2031.

How fast is the frozen logistics segment growing compared with chilled operations?

Frozen operations are advancing at a 7.01% CAGR through 2031, while the chilled segment retains scale with 52.02% share but grows more slowly.

Which region is expected to post the strongest growth to 2031?

Kyushu & Okinawa lead with an 8.13% CAGR thanks to RCEP-linked trade corridors and expanding agri-food output.

Why are value-added services gaining traction among shippers?

Customers increasingly pay for labeling, kit assembly, and compliance documentation, driving this segment’s 8.25% CAGR and lifting margins beyond basic storage fees.

What technologies are firms adopting to cut carbon from refrigerated transport?

Operators are testing battery-electric and hydrogen-powered reefers, shifting long hauls to Ro-Ro ferries, and installing solar-plus-battery systems at depots to curb emissions.

How severe is Japan’s refrigerated-truck driver shortage?

Government data point to a potential 34% capacity gap by 2030, spurring investment in autonomous truck pilots and intermodal rail solutions.

Page last updated on: