Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

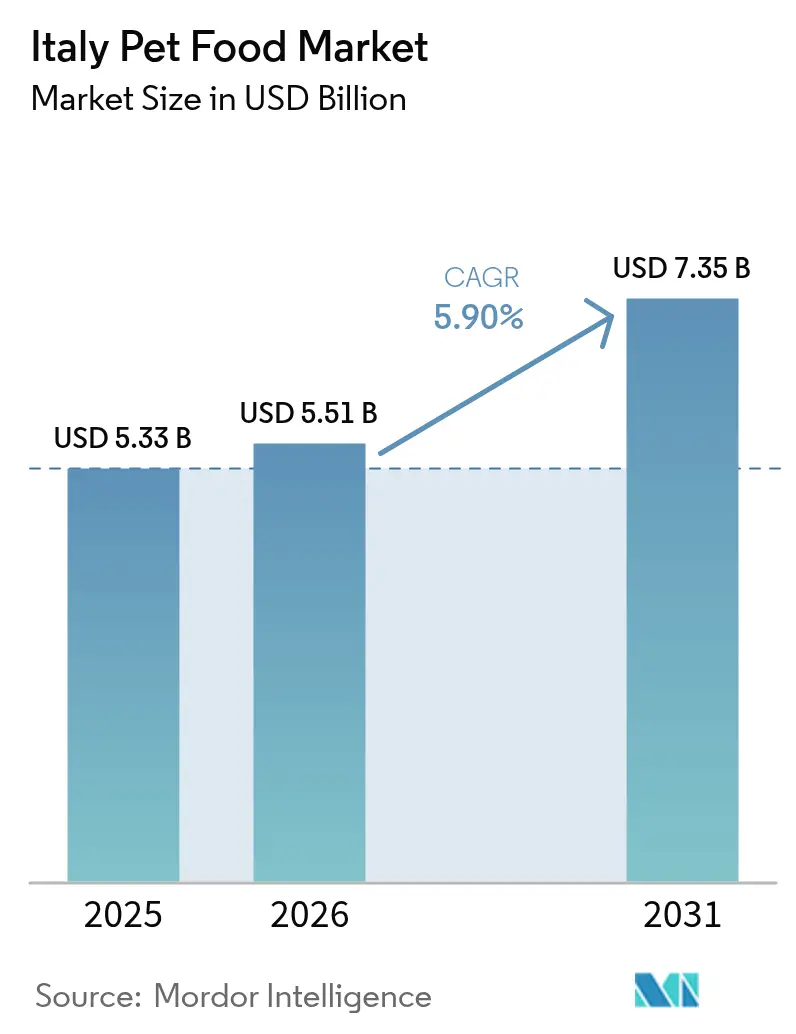

| Base Year Market Size (2025) | USD 5.33 Billion |

| Market Size (2026) | USD 5.51 Billion |

| Market Size (2031) | USD 7.35 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

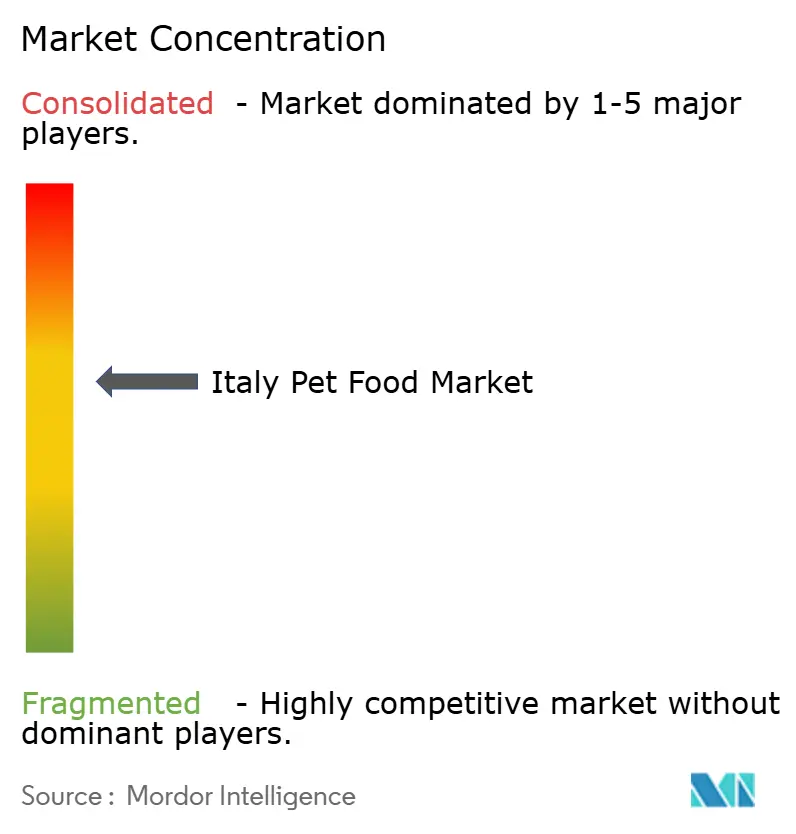

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Italy Pet Food Market Analysis by ���ϲ�����

The Italy pet food market size is expected to increase from USD 5.33 billion in 2025 to USD 5.51 billion in 2026 and reach USD 7.35 billion by 2031, growing at a CAGR of 5.90% over 2026-2031. Demand is buoyed by pet humanization, single-serve convenience, and the rapid adoption of online subscription models, which lift premium price realization. Dry formulations still anchor volume, but wet pouches and trays are capturing value as urban households prioritize palatability and portion control. Domestic capacity scale-ups, notably Nestlé Purina PetCare’s new Campania plant, shorten lead times and enable regional customization. Structural demographic shifts—aging owners, smaller households, and fewer births temper unit growth but simultaneously raise per-person expenditure, helping producers preserve margins despite inflation shocks.

Key Report Takeaways

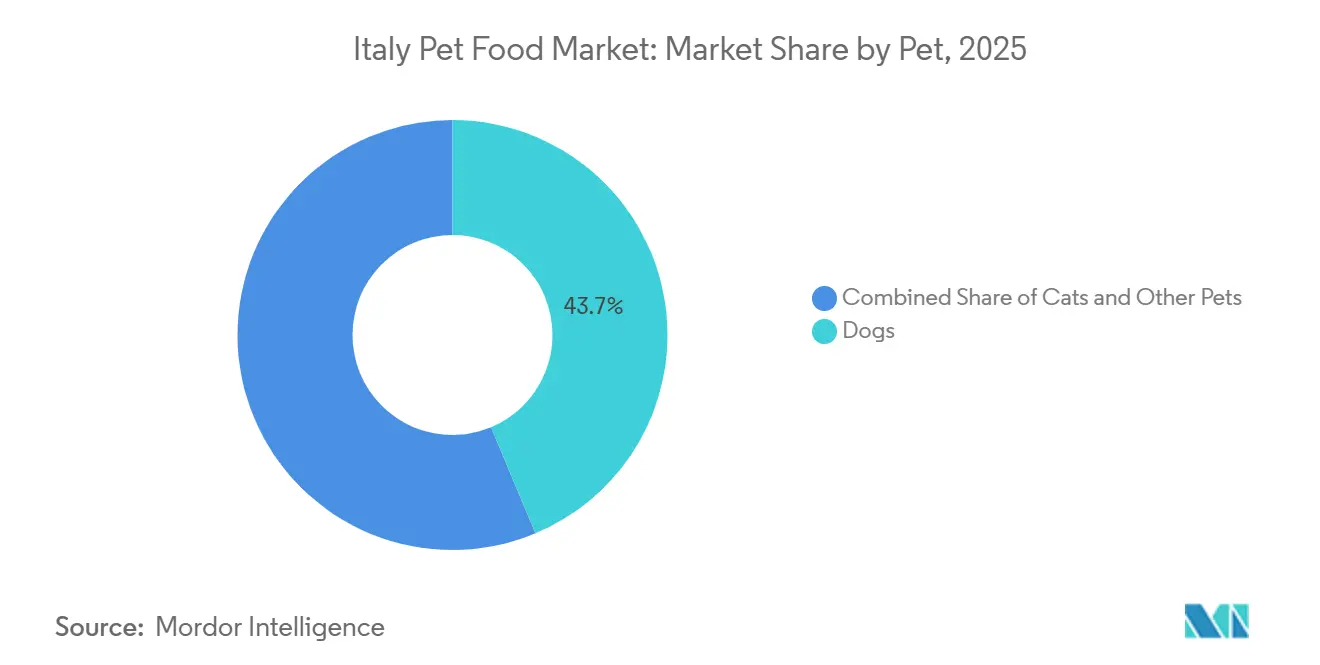

- By pet type, dogs accounted for 43.7% of the Italy pet food market share in 2025 and are projected to record the fastest growth, expanding at a CAGR of 6.8% through 2031.

- By pet food type, food commanded 67.4% of Italy pet food market size in 2025, while pet nutraceuticals/supplements are projected to grow at the highest CAGR of 10.8% to 2031.

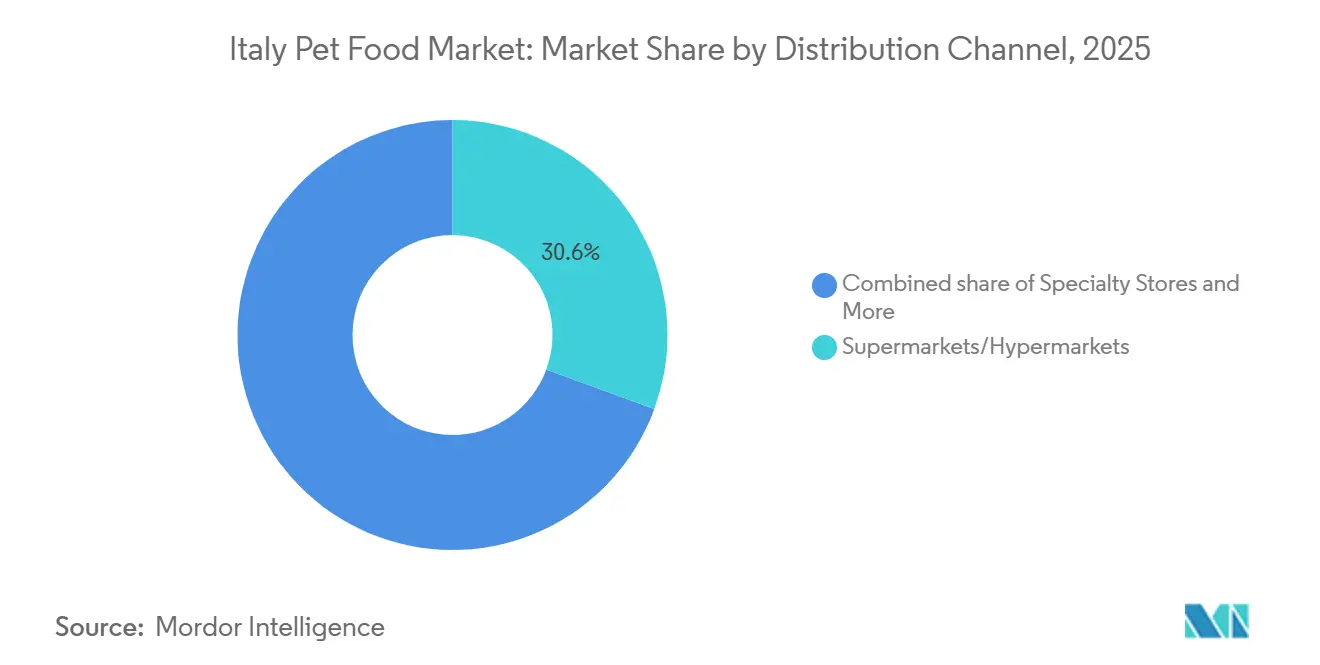

- By distribution channel, supermarkets and hypermarkets accounted for a 30.6% share of Italy pet food market in 2025, while the Online Channel is forecast to log the strongest 6.5% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Pet Food Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization driven by pet-humanization | +1.2% | Nationwide, the highest in Milan, Turin, and Bologna | Medium term (2-4 years) |

| Supermarket private-label rollouts are expanding volume | +0.8% | Nationwide, led by Coop, Conad, and Esselunga | Short term (≤ 2 years) |

| Veterinary endorsement of functional diets | +0.6% | Metro areas with dense vet networks | Medium term (2-4 years) |

| Rapid growth of e-commerce channels | +1.0% | Accelerating in Campania, Sicily, and Calabria | Short term (≤ 2 years) |

| Domestic single-serve wet-food capacity scale-up | +0.5% | Campania hub with national spillover | Medium term (2-4 years) |

| European Union (EU) approval of insect protein for pets | +0.4% | Early uptake in premium outlets | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Premiumization Driven by Pet-Humanization

Italian owners increasingly treat dogs and cats as family members, choosing human-grade recipes, single-source proteins, and functional add-ons. Single-person households now represent 36.2% of all residences, fueling discretionary spending per pet[1]Source: European Food Safety Authority, “Insect Protein Approval,” efsa.europa.eu . In April 2024, Nestlé Purina PetCare announced an investment of EUR 472 million (USD 508 million) to establish a new wet pet food manufacturing facility and logistics hub in Mantua, northern Italy, scheduled for completion in 2027. Companies such as Nestlé Purina PetCare, Farmina Pet Foods, and Monge and C. S.p.A. are strengthening premium portfolios through science-backed formulations, transparent sourcing, and sustainability positioning, supporting higher value growth in the market.

Supermarket Private-Label Rollouts Expanding Volume

Coop Italia’s 2024 launch of Gli Spesotti shows how retailers monetize aisle control, while own brands already account for more than 40% of Coop's turnover. Conad and Esselunga are replicating the strategy, offering 15-25% discounts that resonate with inflation-sensitive consumers. Contract producers such as Partner in Pet Food and United Petfood Producers supply bespoke recipes that keep formulations on trend while preserving retailer margins. Branded leaders respond with in-store promotions and loyalty programs to defend shelf real estate. The tug-of-war fragments the middle tier and widens the gap between value and premium propositions.

Veterinary Endorsement of Functional Diets

Clinics recommend life-stage and disease-specific feeds for conditions like renal insufficiency, diabetes, and allergies. Hill’s Pet Nutrition earns the bulk of its Italian sales from these channels, where medical trust outweighs price concerns. Royal Canin distributes breed-specific therapies through a similar network, while Dechra Pharmaceuticals offers vet-exclusive menus that personalize nutrition. The European Food Safety Authority (EFSA) has cleared insect proteins such as Tenebrio molitor for pet use, enabling hypoallergenic options[2]Source: Council Regulation (EU) 2025/219, “Mediterranean Fishing Quotas,” eur-lex.europa.eu . Functional treats fortified with omega-3s and probiotics are now outpacing conventional snacks, underscoring the blurring line between food and preventive care.

European Union Approval of Insect Protein for Pets

European Food Safety Authority (EFSA) green light for Tenebrio molitor and Acheta domesticus unlocks a low-carbon protein that emits significantly fewer greenhouse gases than poultry[3]Source: Council Regulation (EU) 2025/219, “Mediterranean Fishing Quotas,” eur-lex.europa.eu . Italian start-ups are piloting wet and dry recipes for pets with chicken or fish allergies, pricing them 20-30% above mainstream equivalents. Early adopters cluster in specialty stores and e-commerce, where shoppers actively seek sustainable labels. As insect farms scale and automation cuts costs, parity with meat proteins is anticipated by 2028-2029. The move dovetails with European Green Deal targets, positioning Italy as a potential hub for circular-economy feed substrates.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-linked down-trading to economy brands | −0.9% | Strongest in the southern and rural zones | Short term (≤ 2 years) |

| Declining birth rate limiting new pet adoption | −0.7% | Structural nationwide trend | Long term (≥ 4 years) |

| Compounding pharmacies cannibalizing veterinary diet demand | −0.3% | Urban centers with many pharmacies | Medium term (2-4 years) |

| Omega-3 supply gaps from Adriatic fishing quotas | −0.4% | Impacts manufacturers using seafood inputs | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Inflation-Linked Down-Trading to Economy Brands

Food inflation slowed to 3.6% in May 2025, but cumulative price hikes since 2021 still squeeze lower-income households. Coop’s Gli Spesotti moves nearly 10 million packs a month, proving the magnetism of 15-25% discounts. Southern and rural buyers exhibit the highest price elasticity, prompting branded giants to bolster couponing, which erodes margins. While trading down constrains short-term value growth, it increases household penetration, creating a future upsell base once real wages normalize. The tension forces producers to refine cost structures without sacrificing recipe quality.

Compounding Pharmacies Cannibalizing Veterinary Diet Demand

Urban pharmacies now prepare custom diets that swap allergens, tailor macronutrient ratios, and include supplements not found in packaged therapeutic SKUs. The practice exploits a regulatory gray zone overseen by regional health boards, raising questions about consistency but attracting owners seeking bespoke solutions. Clinics sometimes collaborate with pharmacists, diverting purchases away from brands like Hill’s and Royal Canin. Though still below 5% of therapeutic diet volume, compounding’s momentum is pressuring incumbents to accelerate the expansion of formulation variety and subscription convenience. Over time, tighter oversight may cap the trend, yet for now it trims high-margin vet-channel sales.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pets: Dogs Lead Market Expansion

Dogs captured 43.7% of the Italy pet food market share in 2025, making them the largest segment, supported by high dog ownership, strong spending on premium dry kibble, and wide availability across supermarkets and pet specialty stores. Dogs are also projected to register the fastest growth at a 6.8% CAGR through 2031, driven by premiumization, functional nutrition demand, and sustained humanization trends.

Other pets, including birds, rabbits, and small mammals, remain niche but are gaining traction in specialty outlets. Manufacturers such as Monge and Affinity Petcare are expanding tailored recipes and smaller pack sizes suited to lower consumption volumes. These categories command higher per-kilogram prices due to specialized ingredients and shorter production runs. Although their contribution to the Italy pet food market size remains limited, their growth provides incremental upside without significant capital investment.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download Sample Report

By Pet Food: Food Maintains Market Leadership

Food held 67.4% of the Italy pet food market share in 2025, making it the largest segment, primarily supported by the affordability, long shelf life, and widespread consumption of dry kibble that meets established nutritional standards. Nutraceuticals and supplements represent the fastest-growing niche, projected to advance at a 10.8% CAGR through 2031. Their rapid expansion is driven by increasing veterinary prescriptions of glucosamine, omega-3 fatty acids, and probiotics for aging pets, along with rising owner awareness of preventive health benefits. Subscription-based e-commerce models further strengthen repeat purchases, increasing customer lifetime value and boosting the premium tier’s contribution to the Italy pet food market size.

Wet meals, freeze-dried formats, and fresh-prepared recipes cater to owners seeking higher palatability and minimally processed options. Wet food is expanding particularly quickly, supported by convenient single-serve pouches that command per-kilogram prices up to 80% higher than bulk kibble. Emerging freeze-dried and fresh segments currently account for a moderate share but offer margins of 30–40%, positioning them as future growth drivers as production costs gradually decline.

By Distribution Channel: Supermarkets Lead yet Online Surges

Supermarkets and hypermarkets held 30.6% of the Italy pet food market share in 2025, making them the largest distribution channel, supported by prominent in-store displays, loyalty programs, and competitive private-label pricing. Coop’s Gli Spesotti brand alone sells around 10 million units monthly, highlighting the strength of brick-and-mortar retail. Specialty chains such as Arcaplanet increase average transaction values through curated assortments and trained staff, particularly in northern and central Italy. Veterinary clinics remain essential for therapeutic diets, where professional endorsement drives higher willingness to pay.

Online channels are the fastest-growing distribution segment, projected to expand at a 6.5% CAGR through 2031, nearly double the pace of store-based outlets, as consumers increasingly prefer home delivery convenience. Platforms such as Zooplus, Amazon, and Arcaplanet’s webstore account for a rising share of digital sales, leveraging scale efficiencies in last-mile logistics. Southern regions are growing 2–3 percentage points above the national average as broadband access improves. Direct-to-consumer platforms from Farmina and Almo Nature capture first-party consumer data, strengthening loyalty programs and enabling personalized product offerings.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download Sample Report

Geography Analysis

Northern Italy, encompassing Lombardy, Piedmont, Emilia-Romagna, and Veneto, accounts for the largest share of the Italy pet food market and shows premium penetration above 50%. Milan, Turin, and Bologna neighborhoods exhibit high demand for grain-free and functional formulations, helped by dense veterinary networks that endorse therapeutic lines. Monge’s Piedmont hub and Nestlé’s historical northern footprint facilitate efficient distribution and export logistics. Supermarket chains such as Esselunga dominate shelf space, reinforcing the region’s volume leadership.

Central Italy, Lazio, Tuscany, and Umbria deliver balanced growth as Rome’s urban pet base and Florence’s specialty boutiques nurture both value and premium tiers. Coop’s value range resonates with middle-income families, while e-commerce logistics hubs in Rome enhance online penetration. Veterinary channels distribute Hill’s, Royal Canin, and Dechra therapies, maintaining strong prescription sales. Despite lower disposable incomes than in the north, brand loyalty remains solid in high-tourism Tuscany, where expatriate residents favor premium imports.

Southern Italy and the islands Campania, Sicily, Calabria, Puglia, and Sardinia represent the fastest-growing region, outpacing the national CAGR by roughly two percentage points. Nestlé’s USD 496 million Campania facility anchors regional supply, building wet-food capacity that addresses local demand and export prospects across the Mediterranean. Online adoption is growing rapidly as improved logistics are narrowing delivery lead times, especially in Naples, Palermo, and Bari. Although private-label still captures a significant share due to higher price sensitivity, premiumization momentum is visible in affluent coastal towns and tourist hubs.

Competitive Landscape

Nestlé Purina PetCare, Mars Petcare Italy, Monge and C. S.p.A., Affinity Petcare, and Hill’s Pet Nutrition together account for the majority of the Italy pet food market in 2025, lending scale advantages in procurement, advertising, and veterinary outreach. Nestlé’s new Campania plant underscores long-term commitment, while Mars pursues regenerative agriculture contracts covering 20,900 hectares across Europe. Both giants have redesigned packaging to improve recyclability and meet circular-economy rules. Their innovation pipelines and omnichannel presence sustain their dominance.

Monge leverages vertical integration and renewable energy to sharpen cost positions and Environmental, Social, and Governance (ESG) credentials. Affinity Petcare focuses on specialty stores with Mediterranean diet-inspired ranges, while Hill’s secures vet-channel volumes via clinical backing. Each counters multinational firepower with agility, sustainability marketing, and niche targeting. Private-equity funded challengers such as Partner in Pet Food and United Petfood Producers provide white-label capacity to retailers, eroding incumbent shelf space.

Fressnapf’s acquisition of Arcaplanet cements an omnichannel platform that blends 500-plus stores with digital outreach, raising competitive pressure on both grocery and online specialists. Start-ups exploring insect proteins, fresh-prepared meals, and data-driven personalization chip away at category edges. As Environmental, Social, and Governance (ESG) compliance tightens, players able to certify traceable supply chains and low-carbon inputs will capture disproportionate growth. Furthermore, integrating high-margin veterinary and grooming services into physical retail hubs is creating "pet ecosystems" that insulate market leaders from pure-price competition from digital-only platforms.

Italy Pet Food Industry Leaders

Nestlé Purina PetCare (Nestlé S.A.)

Mars Petcare Italy (Mars, Incorporated)

Monge & C. S.p.A.

Affinity Petcare S.A. (Agrolimen S.A.)

Hill’s Pet Nutrition, Inc. (Colgate-Palmolive Company)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download Sample Report

Recent Industry Developments

- December 2025: Romanian poultry group Transavia revealed plans to invest EUR 150 million (USD 157.5 million) in a fully automated pet-food plant in Ciugud, Alba county, designed to supply dry and wet formulas for more than 11 million dogs and cats annually from the second half of 2026.

- November 2025: The European Bank for Reconstruction and Development, along with Turkven and the International Finance Corporation, acquired a minority stake in Türkiye-based Çağatay Pet Food to finance a new production site and technology upgrades that will lift the company’s 45,000-metric-ton annual capacity.

- April 2024: Nestlé Purina PetCare invested EUR 472 million (USD 495 million) to build a 180,000-square-meter wet pet food factory in Mantua, Italy, scheduled for completion in 2027 and anticipated to create 300 jobs.

Italy Pet Food Market Report Scope

Pet food is specially formulated to meet the nutritional needs of domesticated animals, such as dogs, cats, and other companion pets, supporting their growth, health, and overall well-being.

The Italy Pet Food Market Report provides a detailed analysis based on pet type, covering dogs, cats, and other companion animals. It further evaluates the market by product category, including standard pet food, treats, veterinary diets, and nutraceuticals and supplements. The study also assesses performance across key distribution channels such as supermarkets and hypermarkets, specialty pet stores, convenience stores, online platforms, and other retail formats. Market size and forecasts are presented in both value terms in USD and volume in metric tons.

By Pets

| Dogs |

| Cats |

| Other Pets |

By Pet Food Product

| Food | Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||

| Wet Pet Food | ||

| Pet Treats | Dental Treats | |

| Crunchy Treats | ||

| Soft & Chewy Treats | ||

| Freeze-dried and Jerky Treats | ||

| Other Treats | ||

| Pet Veterinary Diets | Urinary tract disease | |

| Diabetes | ||

| Renal | ||

| Digestive Sensitivity | ||

| Oral Care Diets | ||

| Derma Diets | ||

| Obesity Diets | ||

| Other Veterinary Diets | ||

| Pet Nutraceuticals/Supplements | Milk Bioactives | |

| Omega-3 Fatty Acids | ||

| Probiotics | ||

| Proteins and Peptides | ||

| Vitamins and Minerals | ||

| Other Nutraceuticals |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Convenience Stores |

| Online Channel |

| Other Channels |

| By Pets | Dogs | ||

| Cats | |||

| Other Pets | |||

| By Pet Food Product | Food | Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||

| Wet Pet Food | |||

| Pet Treats | Dental Treats | ||

| Crunchy Treats | |||

| Soft & Chewy Treats | |||

| Freeze-dried and Jerky Treats | |||

| Other Treats | |||

| Pet Veterinary Diets | Urinary tract disease | ||

| Diabetes | |||

| Renal | |||

| Digestive Sensitivity | |||

| Oral Care Diets | |||

| Derma Diets | |||

| Obesity Diets | |||

| Other Veterinary Diets | |||

| Pet Nutraceuticals/Supplements | Milk Bioactives | ||

| Omega-3 Fatty Acids | |||

| Probiotics | |||

| Proteins and Peptides | |||

| Vitamins and Minerals | |||

| Other Nutraceuticals | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Specialty Stores | |||

| Convenience Stores | |||

| Online Channel | |||

| Other Channels | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Need More Details on Market Definition?

Ask a Question

Research Methodology

���ϲ����� follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download Sample Report