Isoflavones Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

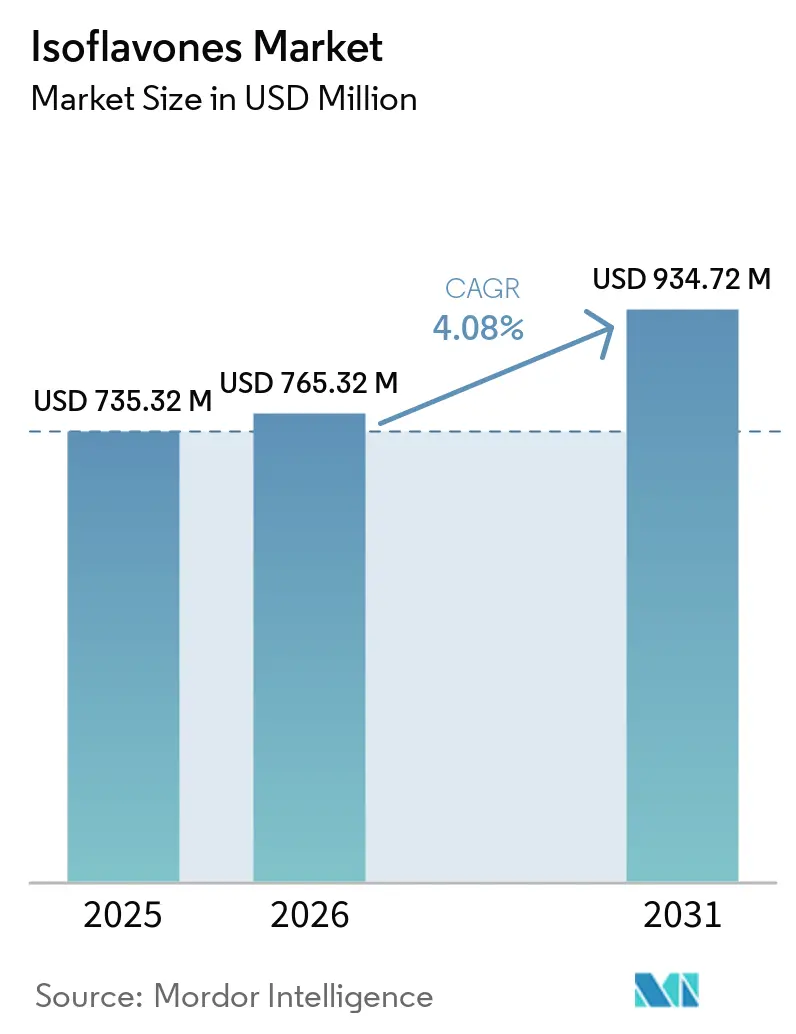

| Market Size (2026) | USD 765.32 Million |

| Market Size (2031) | USD 934.72 Million |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

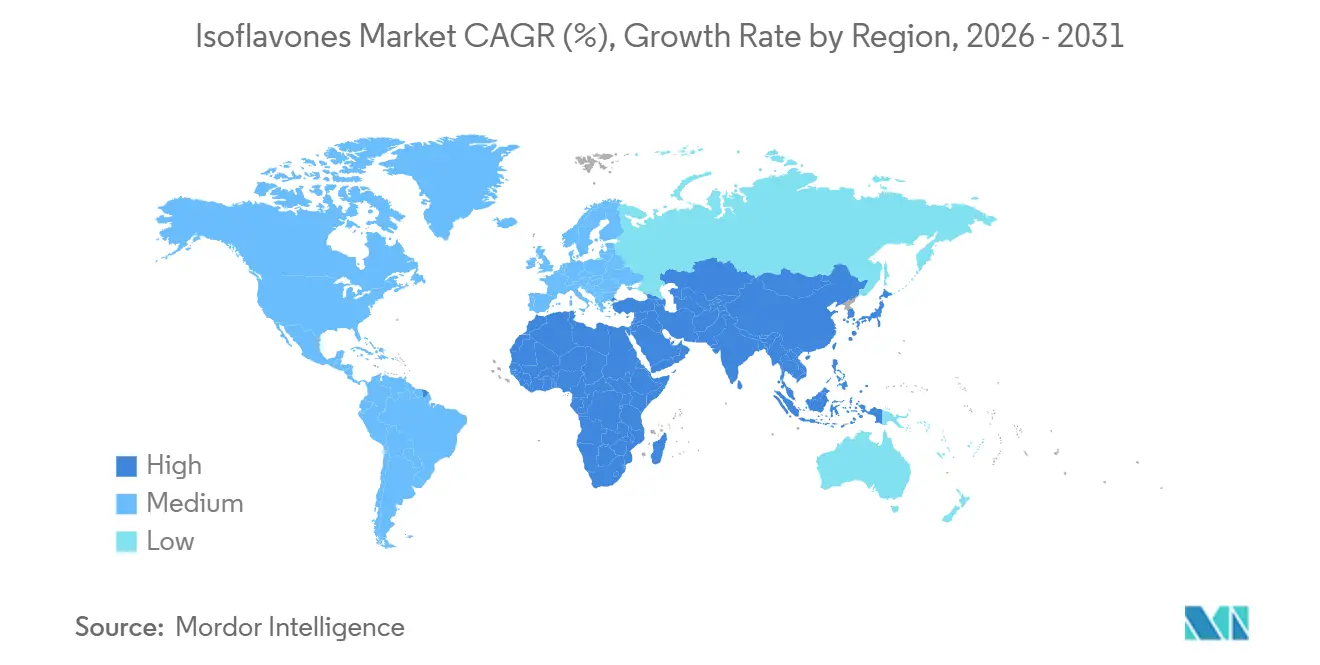

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Isoflavones Market Analysis by ���ϲ�����

The global isoflavones market size is expected to grow from USD 735.32 million in 2025 to USD 765.32 million in 2026 and is forecast to reach USD 934.72 million by 2031 at 4.08% CAGR over 2026-2031. As consumer preferences shift towards plant-based solutions and clinical validations of health benefits expand, the global isoflavones market is carving out a significant niche within the broader functional ingredients arena. Isoflavones uniquely straddle the realms of nutraceuticals, pharmaceuticals, and cosmetics. This multi-sector presence not only shields them from the cyclical nature of any single sector but also paves the way for diversified growth. Regulatory bodies are showing greater acceptance of plant-based bioactive ingredients, and substantial improvements in extraction technologies that have enhanced both the bioavailability and commercial viability of isoflavone products [1]Source: European Food Safety Authority, "Regulation (EU) 2015/2283," efsa.onlinelibrary.wiley.com. With advancements in extraction technologies and improved bioavailability, product efficacy is on the rise. Demographic trends, especially the aging populations in North America and the Asia Pacific, are propelling the adoption of isoflavones in applications ranging from cardiovascular and bone health to menopausal wellness. Meanwhile, the cosmetics industry and functional beverages are becoming fertile ground for innovation, with both powder and liquid formats being tailored to diverse workflows. The competitive landscape is moderately fragmented, enabling mid-tier specialty extractors to carve out and defend their niche.

Key Report Takeaways

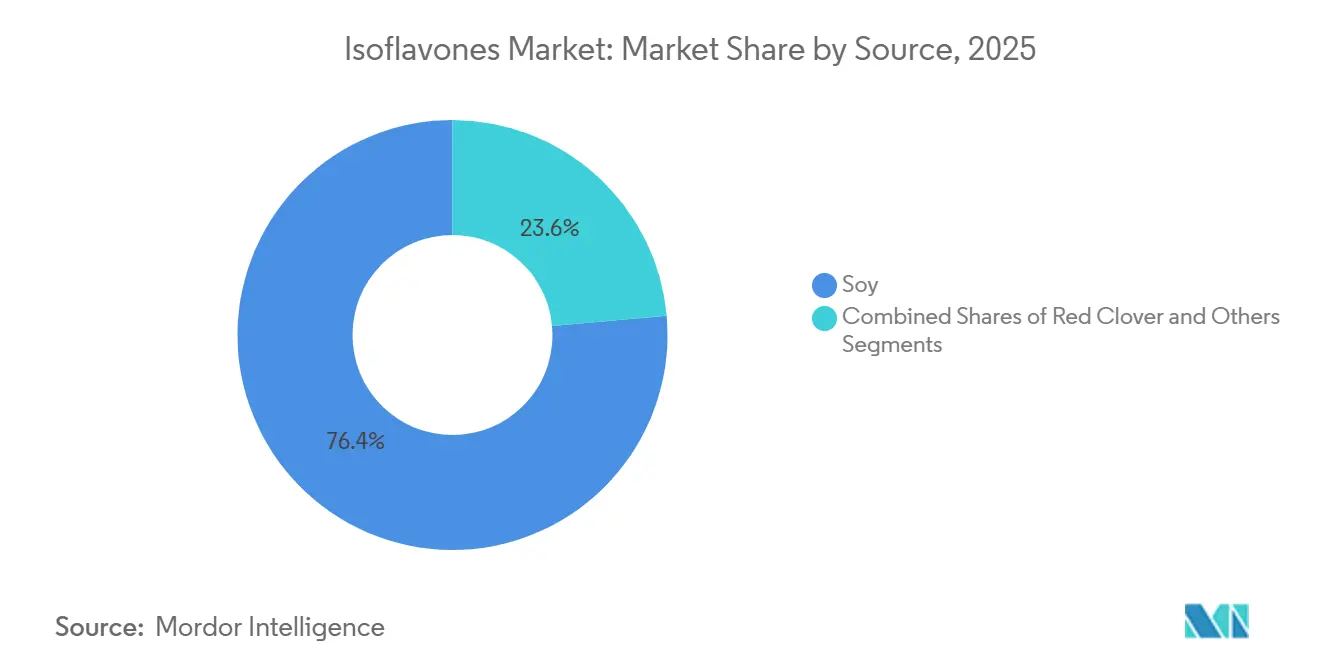

- By source, soy captured 76.43% of the 2025 isoflavones market share, whereas red clover leads growth at 5.33% CAGR through 2031.

- By form, powder held 63.21% share in 2025, while liquid formats are set to expand at a 5.11% CAGR through 2031, particularly in Asia-Pacific.

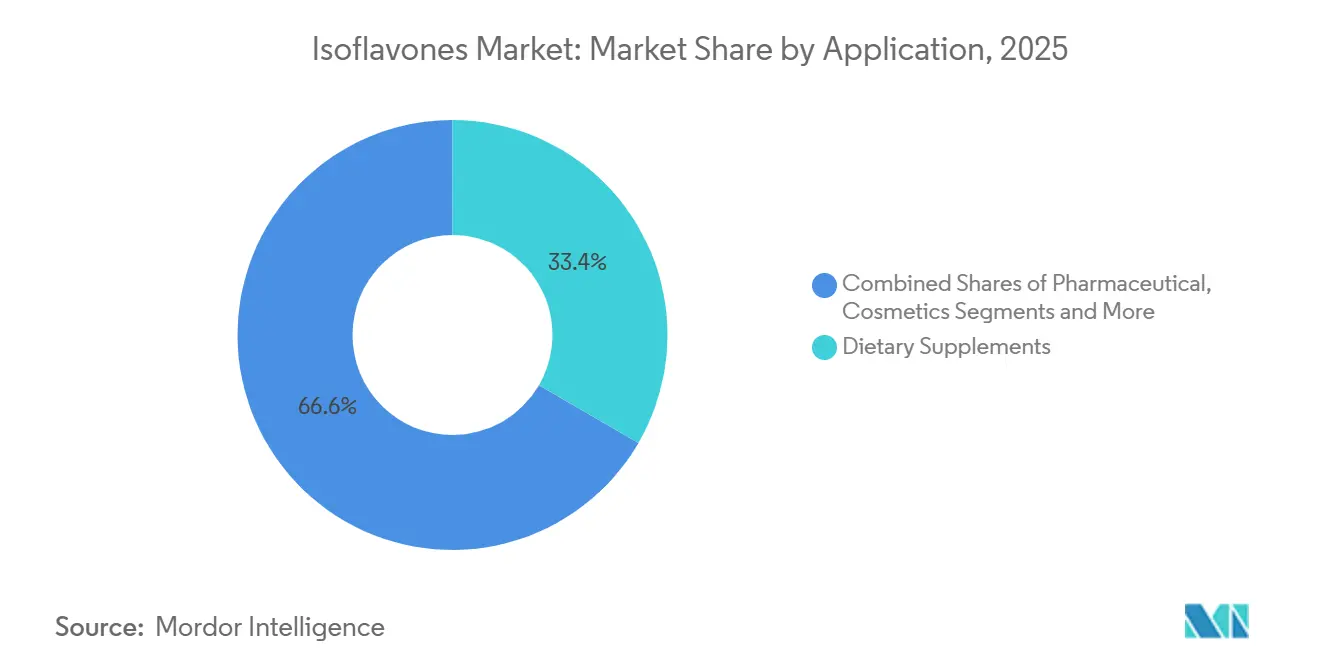

- By application, dietary supplements commanded 33.37% of the 2025 value, yet cosmetics exhibit the fastest pace at 5.33% CAGR over 2026-2031.

- By geography, North America led with 32.45% share in 2025, but Asia-Pacific is poised for the swiftest climb at 5.01% CAGR through 2031, fueled by rising middle-class demand and domestic production in China and India.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Isoflavones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for natural, plant-based ingredients | +1.2% | Global, with concentrated demand in North America and Northern Europe | Medium term (2–4 years) |

| Growing demand for isoflavones in nutraceuticals and preventive healthcare products | +1.5% | Global; strongest in North America, Japan, and Germany | Long term (≥ 4 years) |

| Advancements in extraction techniques, increasing purity and bioavailability | +0.9% | Global, with research and development hubs in Brazil, China, and South Korea | Medium term (2–4 years) |

| Use in cosmetics for anti-aging, skin firming, wrinkle reduction, and sun protection | +0.8% | Asia-Pacific and Western Europe | Medium term (2–4 years) |

| Fueling demand for isoflavone-enhanced animal feed to improve livestock health | +0.5% | Asia-Pacific, North America, spill-over to South America | Short term (≤ 2 years) |

| Influence of traditional Asian dietary patterns | +0.6% | Asia-Pacific core; diaspora-driven spill-over to North America and Europe | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising consumer preference for natural, plant-based ingredients

Driven by a growing consumer preference for natural, plant-based ingredients, the global isoflavones market is experiencing a surge in demand, particularly in supplements and functional foods. Clinical studies reinforce the importance of isoflavones in supporting cardiovascular health, enhancing bone strength, and addressing menopausal symptoms. Additionally, dietary guidelines in key markets, such as the United States, are promoting soy-based foods as essential components of healthier eating habits. This support is strengthened by the extensive scale of global soybean production, which ensures a reliable and cost-effective feedstock, a capability unmatched by competing plant sources. The combination of increasing consumer health awareness, well-established agricultural supply chains, and growing scientific validation positions isoflavones as a significant contributor to the transition toward plant-based nutrition and functional wellness. Importantly, this trend is not solely driven by consumer demand but is also supported by policy initiatives, with governments advocating plant-forward diets as part of public health strategies. As a result, isoflavones are establishing themselves as a critical ingredient in the evolving landscape of functional nutrition and wellness innovation.

Growing demand for isoflavones in dietary supplements and preventive healthcare products

Driven by an aging population's quest for natural remedies, the global isoflavones market is experiencing significant growth, particularly in dietary supplements and preventive healthcare. These remedies address menopausal health, bone protection, and cardiometabolic management. Clinical research is expanding the application scope for isoflavones. Notably, studies by the National Institute of Health link soy consumption to a reduced risk of neurocognitive disorders. Furthermore, fermented soy demonstrates even more pronounced protective benefits, indicating new opportunities in brain health that extend beyond its traditional applications. The vast size of Europe's preventive health market highlights the commercial potential of isoflavones. However, the challenge posed by inconsistent equol conversion rates across different populations is driving innovation toward personalized, microbiome-focused formulations. These trends emphasize isoflavones' critical role in the future of preventive healthcare, combining scientific validation with increasing consumer demand for plant-based wellness. This momentum is further supported by the alignment of clinical findings and growing consumer awareness, accelerating product development. As companies incorporate personalization into their supplement strategies, isoflavones are positioned to transition from specialized botanical extracts to widely adopted functional health solutions.

Advancements in extraction techniques, increasing purity and bioavailability

Advancements in extraction techniques are reshaping the isoflavones market, reducing production costs while enhancing ingredient functionality. Breakthroughs such as multi-enzyme catalysis and microwave-assisted extraction are delivering superior conversion rates and faster processing times, making industrial-scale production more efficient and commercially viable. Circular economy innovations that preserve protein content while extracting high-quality isoflavones are further strengthening sustainability credentials and creating dual revenue streams. These developments not only improve aglycone purity and bioavailability but also sharpen product differentiation in the dietary supplement channel, positioning isoflavones as a more effective and competitive solution. As technology continues to raise the performance bar, companies that invest in advanced extraction platforms will secure stronger market positioning. This innovation-driven momentum is setting the stage for isoflavones to evolve into a premium, science-backed ingredient across preventive healthcare and functional nutrition.

Use in cosmetics for anti-aging, skin firming, wrinkle reduction, and sun protection

Isoflavones are gaining prominence in the cosmetics industry, transitioning from their traditional phytoestrogenic roles to advanced applications such as anti-aging, skin firming, wrinkle reduction, and sun protection. Clinical studies highlight the effectiveness of equol production, a key metabolite of isoflavones, in improving skin hydration and reducing visible signs of aging, making it highly appealing to consumers. Notably, equol prevalence varies geographically, with East Asian populations exhibiting higher rates compared to Western markets. This demographic insight is critical for brands, influencing both product development and marketing strategies. These factors have driven the shift toward microbiome-aware and personalized skincare solutions, positioning isoflavones as a unique ingredient in the beauty and wellness sector. As cosmetic companies integrate clinical validation with consumer-focused innovation, isoflavones are establishing themselves as a cornerstone of premium skincare portfolios, offering scientifically validated solutions that meet the growing demand for natural, functional, and customized beauty products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergic reactions and sensitivities linked to soy-based isoflavones | -0.4% | Global; higher impact in North America and Europe where soy allergy reporting is systematic | Short term (≤ 2 years) |

| Stringent and varying regulatory barriers for isoflavone-containing products | -0.6% | Europe (particularly France, Germany); spill-over effect to other export markets | Medium term (2–4 years) |

| Limited awareness in emerging geographies | -0.3% | Middle East, Africa, and parts of Latin America | Long term (≥ 4 years) |

| Sensory challenges in isoflavone integration | -0.2% | Global, most acute in food and beverage applications | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Allergic reactions and sensitivities linked to soy-based isoflavones

In the global market, soy-based isoflavones face challenges due to their association with allergen sensitivities. The Food and Drug Administration (FDA) classifies soy among the "Big 9" food allergens. Although the actual prevalence of soy allergies is low, increased consumer awareness of soy's allergenic status creates a perception challenge. This is particularly evident in mainstream food and beverage applications, where formulators must balance functionality with the risk of consumer avoidance. Regulatory authorities have implemented strict requirements for allergen labeling and risk assessments on soy-containing products, increasing operational costs and potentially discouraging smaller manufacturers from entering the market [2]Source: Food and Drug Administration, “FDA’s GRAS Rule Reform,” fda.gov. Consequently, red clover isoflavones are gaining traction as a soy-free alternative in dietary supplements, appealing to consumers with sensitivities. Simultaneously, emerging analytical methods, such as component-resolved diagnostics, are beginning to differentiate between allergenic soy proteins and non-allergenic isoflavone fractions. This development offers potential for more precise product claims. However, this differentiation has not yet been fully utilized in consumer communications, presenting an opportunity for ingredient manufacturers to reshape narratives and address allergen-related challenges.

Stringent and varying regulatory barriers for isoflavone-containing products

The global isoflavones market faces challenges from stringent and inconsistent regulatory barriers, creating a fragmented environment that complicates product development and distribution. In Europe, national standards vary significantly: France enforces conservative toxicological thresholds, while Germany imposes restrictive intake recommendations. These differences require manufacturers to frequently reformulate products and revise labeling strategies, increasing compliance costs and hindering innovation. The absence of unified European Union-level positive lists for botanical substances, along with unresolved health claims, adds further uncertainty. Companies must navigate a complex regulatory framework, which limits scalability. Outside Europe, regulatory scrutiny is intensifying globally. The upcoming FDA policy change in March 2025, which will eliminate self-affirmed GRAS determinations, introduces additional burdens by requiring enhanced safety documentation and extending product development cycles by 12-18 months [3]Source: U.S. Department of Health and Human Services, “Red Clover,” nccih.nih.gov. This policy shift is expected to extend product development timelines by 12 to 18 months, creating significant challenges for ingredient suppliers. These regulatory complexities constrain market growth, elevate operational risks, and prevent isoflavone producers from fully capitalizing on the growing consumer demand for plant-based functional ingredients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Soy's Scale Advantage Contrasted by Red Clover's Functional Appeal

In 2025, soy is expected to maintain its dominance in the global isoflavones market, commanding a substantial 76.43% share. This stronghold is supported by a well-established global supply chain and decades of clinical endorsements, particularly in areas such as cardiovascular health, bone metabolism, and managing menopausal symptoms. Regulatory endorsements, such as the Food and Drug Administration's approval of a soy protein-related health claim concerning coronary heart disease, further strengthen soy's credibility and market position. The three core isoflavones in soy, genistein, daidzein, and glycitein, possess a well-defined bioactivity profile, instilling confidence in formulators regarding their consistent efficacy. Additionally, advanced biotechnological methods, including CRISPR-associated protein 9 and marker-assisted selection, are enhancing isoflavone concentrations in soybean varieties, highlighting soy's entrenched yet dynamically evolving leadership through innovation.

In contrast, red clover is rapidly gaining traction, with projections indicating a robust 5.33% compound annual growth rate expansion through 2031. Its superior isoflavone density, when compared with soy, makes it a prime candidate for supplement formulations that prioritize efficient dosing and animal feed applications. While regulatory uncertainties persist, particularly with intake ceilings being set lower than soy, consumer demand remains strong. This is especially evident among those seeking soy-free options for menopausal health. Manufacturers, aiming to diversify their ingredient portfolios and mitigate allergen-related challenges, are increasingly supporting red clover. This momentum is further driven by a growing interest in diversified supply chains. Meanwhile, other sources such as kudzu, chickpeas, and legume blends, though still niche, are receiving increased research and development focus, positioning red clover at the forefront of a broader shift toward functional, non-soy isoflavone innovations.

By Form: Powder's Versatility Leads While Liquid Formats Gain Commercial Traction

In 2025, powder form is set to dominate the global isoflavones market, holding a commanding 63.21% share. This supremacy stems from its adaptability; powders meld effortlessly into tablets, capsules, protein fortifications, cosmetic actives, and animal feed premixes. The rising preference for aglycone-enriched soy isoflavone powders is transforming the premium segment of the dietary supplement market, boasting enhanced absorption and elevated plasma concentrations over traditional glycoside powders. While challenges like elevated enzymatic costs and intricate purification processes persist, innovations in multi-enzyme systems are progressively alleviating these issues. Furthermore, heightened purity levels bolster the powder's standing in pharmaceuticals, where consistency and compliance are paramount, cementing its status as the most commercially entrenched format.

On the other hand, liquid formulations are on the rise, with a forecasted compound annual growth rate of 5.11% extending to 2031. They are making inroads in functional beverages and topical cosmetics. In the realm of supplements, the "beauty-from-within" trend is propelling demand for ready-to-drink formats, particularly among postmenopausal women. Meanwhile, in cosmetics, liquid serums and emulsions harness isoflavones for their benefits on hydration and skin elasticity. Challenges like oxidative degradation in water-based solutions are being tackled with advanced encapsulation methods, such as nanocarrier systems and cyclodextrin complexes. These innovations not only prolong shelf life but also maintain bioavailability. Such advancements position liquid formats as a burgeoning category, broadening the commercial landscape of isoflavones beyond their traditional powder-centric applications.

By Application: Dietary Supplements Anchor Demand, Cosmetics Accelerate

In 2025, dietary supplements led the charge for isoflavones, commanding a dominant 33.37% share of the application market. This prominence is bolstered by robust clinical evidence supporting isoflavones in managing menopausal symptoms, preventing osteoporosis, promoting cardiovascular health, and their potential neuroprotective benefits. Pharmaceuticals trailed as the second-largest application, harnessing the selective estrogen receptor modulator properties of isoflavones for targeted therapeutic outcomes, further validated by professional guidelines in Europe. However, a notable challenge in the supplement realm is the limited equol conversion in Western populations, diminishing the bioactive benefits for many. This shortfall has paved the way for commercial ventures, particularly probiotic-co-formulated products aimed at boosting equol production, underscoring the trend of personalization in supplement innovation.

On another front, cosmetics are emerging as the fastest-growing application, with projections indicating a 5.33% CAGR through 2031. This uptick is fueled by accumulating evidence highlighting isoflavones’ benefits in anti-aging, skin firming, wrinkle reduction, and photoprotection, with both topical and ingestible forms gaining popularity. Beyond the beauty realm, isoflavones find significance in animal feed, especially red clover isoflavones, which enhance nitrogen utilization and fiber digestion in dairy cattle. While the food and beverage sector sees a gradual adoption with soy-based protein drinks, soy milk, and bakery items reaping benefits from dietary endorsements, sensory challenges and stability concerns hinder wider acceptance. In summary, while dietary supplements remain a cornerstone for isoflavones, the cosmetics sector is rapidly emerging as the most vibrant growth area, positioning isoflavones at the confluence of health, wellness, and beauty advancements.

Geography Analysis

In 2025, North America dominated the global isoflavones market, capturing a 32.45% share. This stronghold is supported by robust regulatory endorsements and a well-established retail framework. The Food and Drug Administration's endorsement of soy protein as a health asset serves as a potent marketing tool. Coupled with widespread access through mainstream pharmacies and retail outlets, this endorsement amplifies its reach. Dietary trends in the United States and Canada, with a surge in vegetarian, vegan, and flexitarian choices, are driving the integration of soy-based ingredients in both dietary supplements and food items. The United States leads, accounting for over 75% of the regional demand, but Canada and Mexico are not far behind, experiencing growth spurred by dietary guidelines promoting soy as a healthy protein alternative. This blend of regulatory backing, evolving consumer habits, and a solid distribution framework solidifies North America's dominant stance in the global arena.

Asia-Pacific is on a rapid ascent, with projections indicating a 5.01% CAGR through 2031. This growth trajectory is anchored in traditional soy consumption, a higher prevalence of equol production in Asian demographics, and a burgeoning nutraceutical market in nations like China, Japan, South Korea, and India. Japan stands as a beacon of soy innovation, with its demand stretching from conventional foods to supplements and beverages. South Korea is riding the wave of sustainability and plant-based trends, further expanding its soy food market. China's vast processing capabilities and increasing soy product consumption bolster the region's upward momentum. Meanwhile, India's middle-class and Southeast Asian markets are gradually increasing their soy intake, driven by a growing affinity for functional ingredients. This blend of cultural ties to soy and a modern wellness push positions Asia-Pacific as the most vibrant growth hub for isoflavones.

Europe presents a market of strategic importance, yet it is intricately woven with regulatory nuances. These regulations not only limit high-dose supplement usage but also catalyze innovation at food-equivalent dosages. Germany epitomizes this balance: while it enforces strict intake guidelines, there is a notable consumer enthusiasm for soy-based foods and a thriving pharmacy sector for compliant supplements. The European Food Safety Authority provides a scientific backbone for market stability, even as individual nations adopt more stringent stances. While South America primarily serves as a soy-origin center, it is not a dominant consumption market. However, Brazil's research institutions are pioneering extraction technologies with global implications. The Middle East and Africa, though currently the smallest market segment, are witnessing a budding interest in premium supplements, especially in Gulf regions. This trend hints at a promising future, contingent on heightened consumer awareness and a matured retail landscape.

Competitive Landscape

In the global isoflavones market, major agricultural processors like Archer Daniels Midland and Cargill find themselves in competition with specialty phytochemical firms such as Tokiwa Phytochemical and Bio-gen Extracts. They are also up against emerging Asian producers, including Bio Actives Japan Corporation and Shanghai Honovo Chemical. Companies are increasingly setting themselves apart through proprietary extraction technologies, producing product-specific clinical evidence, and catering to diverse applications ranging from dietary supplements and cosmetics to animal feed, thanks to their integrated manufacturing infrastructures. A clear trend towards consolidation is evident, underscored by Bunge’s 2026 acquisition of International Flavors & Fragrances’ soy protein concentrate and soy crush operations. This move signals a strategic alignment of commodity-scale infrastructure with the ambitions of specialty ingredients.

There is untapped potential at the crossroads of precision nutrition and isoflavone delivery. Companies are venturing into formulations that blend standardized isoflavones with probiotic strains, boosting equol production. This strategy offers a unique differentiation that is yet to be fully realized. Major players like DSM-Firmenich, armed with microbiome expertise and a diverse bioactive portfolio, stand poised to seize this opportunity. Meanwhile, nimble firms such as FutureCeuticals and NutriScience Innovations can swiftly adapt with agile clinical study designs. The uptick in patent activity surrounding microbial fermentation and enzyme-based synthesis of equol precursors hints at a burgeoning momentum for biotransformation-based isoflavone products, heralding a new wave of innovation.

In Europe, regulatory compliance is becoming a pivotal competitive edge. The evolving botanical framework by the European Food Safety Authority and Regulation (EC) No 1924/2006 on health claims poses significant entry hurdles. Larger firms, with their established regulatory affairs teams, have a leg up in navigating these challenges. In contrast, smaller entities grapple with scaling across diverse jurisdictions. This landscape is reshaping competitive dynamics, favoring those who meld scientific credibility with regulatory savvy and versatility across applications. As the market evolves, success will be determined by the ability to fuse innovative extraction and biotransformation methods with distinct product claims and solid compliance strategies.

Isoflavones Industry Leaders

-

Archer Daniels Midland

-

Cargill, Incorporated

-

DSM-Firmenich

-

International Flavors & Fragrances Inc.

-

Solbar Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: In a strategic move to bolster its manufacturing prowess, DSM-Firmenich kicked off the construction of a new facility in Parma, Italy. This state-of-the-art plant will specialize in crafting flavors and functional blends.

- February 2025: In a bid to boost production capacity for its TAURA fruit-based ingredients, IFF is set to enlarge its Cedar Rapids, Iowa facility by an additional 47,000 square feet. The revamped facility aims to commence operations by the end of 2026.

- June 2024: Otsuka Pharmaceutical Co., Ltd. rolled out its SOYJOY soy bar in South Korea, harnessing the power of whole soybeans to deliver nutrients like plant-based protein and soy isoflavones.

Global Isoflavones Market Report Scope

Isoflavones are plant-derived compounds classified as phytoestrogens, primarily found in soybeans, red clover, and other legumes, that mimic estrogen activity in the human body.

The global isoflavones market is segmented by source, application, form, and geography. By source, the market is segmented into soy, red clover, and others. By form, the market is segmented into powder and liquid. By application, the market is segmented into Dietary Supplements, pharmaceuticals, cosmetics, animal feed, and food and beverages. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Soy |

| Red Clover |

| Others |

| Powder |

| Liquid |

| Dietary Supplements |

| Pharmaceutical |

| Cosmetics |

| Animal Feed |

| Food and Beverages |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Source | Soy | |

| Red Clover | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Dietary Supplements | |

| Pharmaceutical | ||

| Cosmetics | ||

| Animal Feed | ||

| Food and Beverages | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the isoflavones market be by 2031?

The isoflavones market size is projected to reach USD 934.72 million by 2031 on the back of a 4.08% CAGR.

Which source dominates supply?

Soy accounts for 76.43% of 2025 value, leveraging well-established crop and extraction infrastructure.

Why is Asia-Pacific growing fastest?

Rising middle-class health spending, traditional soy diets, and expanding extraction capacity drive a 5.01% CAGR through 2031.

What’s the key growth segment beyond nutraceuticals?

Cosmetics leads with a 5.33% CAGR through 20231, as clinical evidence of anti-aging benefits underpins premium positioning.

How will new FDA rules affect suppliers?

Elimination of self-affirmed GRAS in 2025 will lengthen approval times and favor firms with robust regulatory capabilities.

Page last updated on: