Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

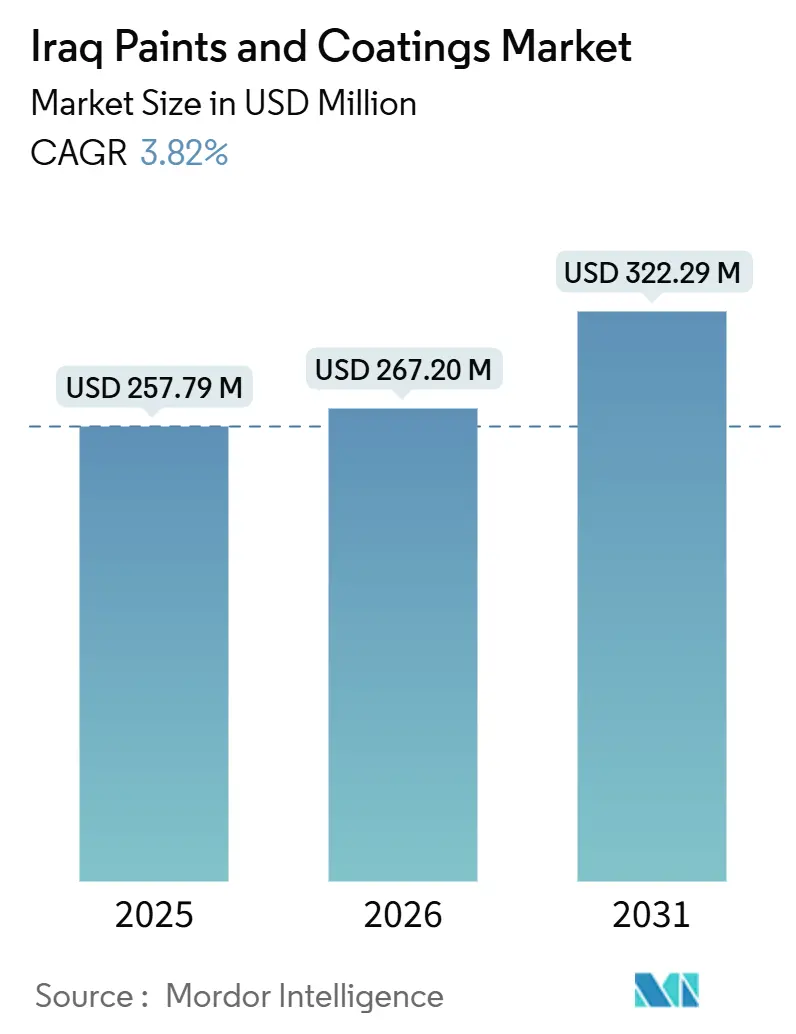

| Base Year Market Size (2025) | USD 257.79 Million |

| Market Size (2026) | USD 267.20 Million |

| Market Size (2031) | USD 322.29 Million |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

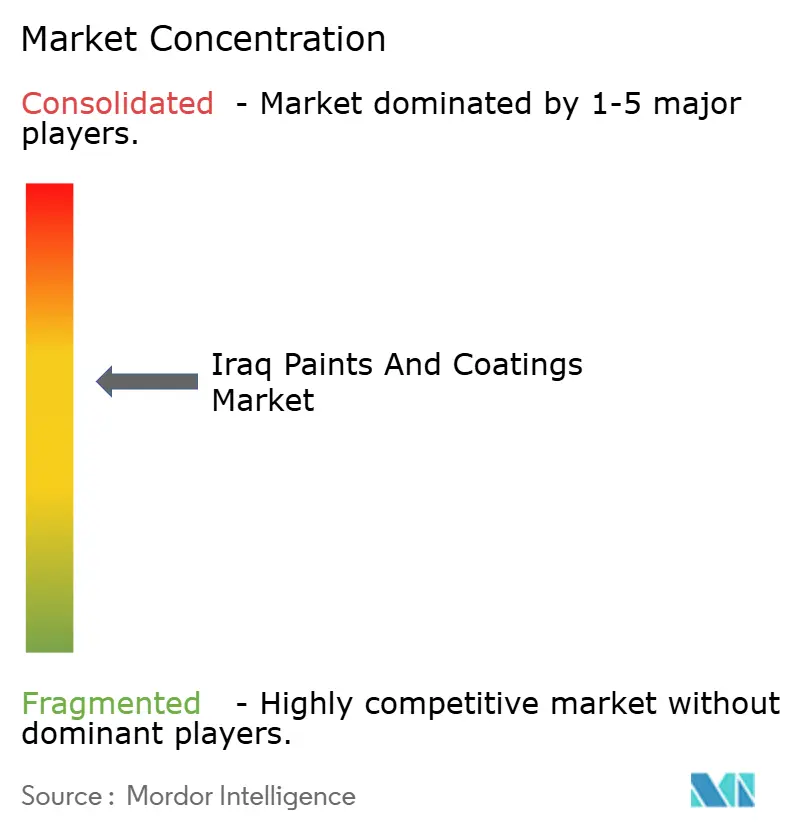

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Iraq Paints And Coatings Market Analysis by ���ϲ�����

The Iraq Paints And Coatings Market size is projected to expand from USD 257.79 million in 2025 and USD 267.20 million in 2026 to USD 322.29 million by 2031, registering a CAGR of 3.82% between 2026 to 2031. Post-conflict reconstruction programs, increased capital expenditure in downstream oil and gas projects, and a government-supported affordable housing pipeline are key drivers of demand for architectural and protective coatings. Private developers and international contractors prefer branded emulsions that comply with Iraq Quality Mark performance standards, while state-owned megaprojects require epoxy, polyurethane, and high-build systems capable of withstanding extreme temperature variations and saline conditions. However, political deadlocks delaying public tenders, resin price fluctuations tied to crude oil benchmarks, and distribution challenges in rural governorates are constraining short-term revenue growth. Multinational suppliers maintain a competitive advantage in high-performance segments, but local producers are increasingly differentiating themselves with fire-resistant and tint-on-demand products, intensifying competition in mid-tier price categories.

Key Report Takeaways

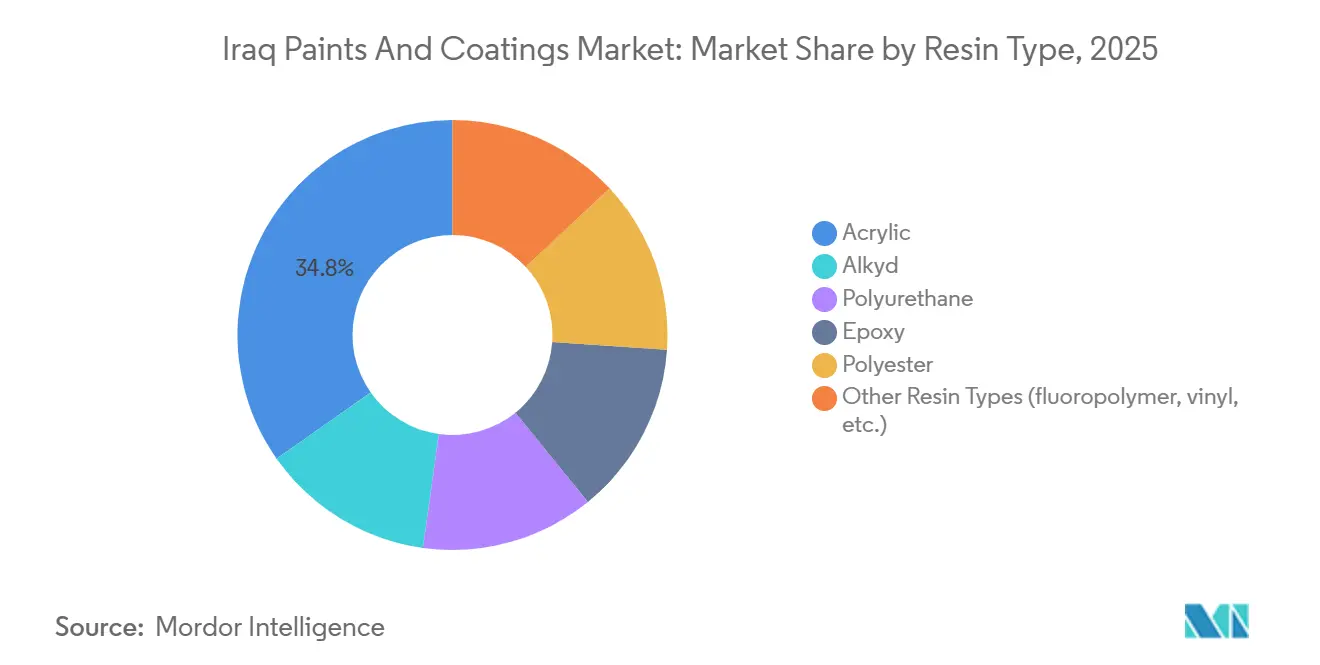

- By resin type, acrylic captured 34.75% of Iraq paints and coatings market share in 2025, while polyurethane is forecast to post the fastest 4.02% CAGR through 2031.

- By technology, solvent-borne commanded 68.44% of the Iraq paints and coatings market share in 2025, whereas water-borne technology is projected to climb at a 4.22% CAGR through 2031.

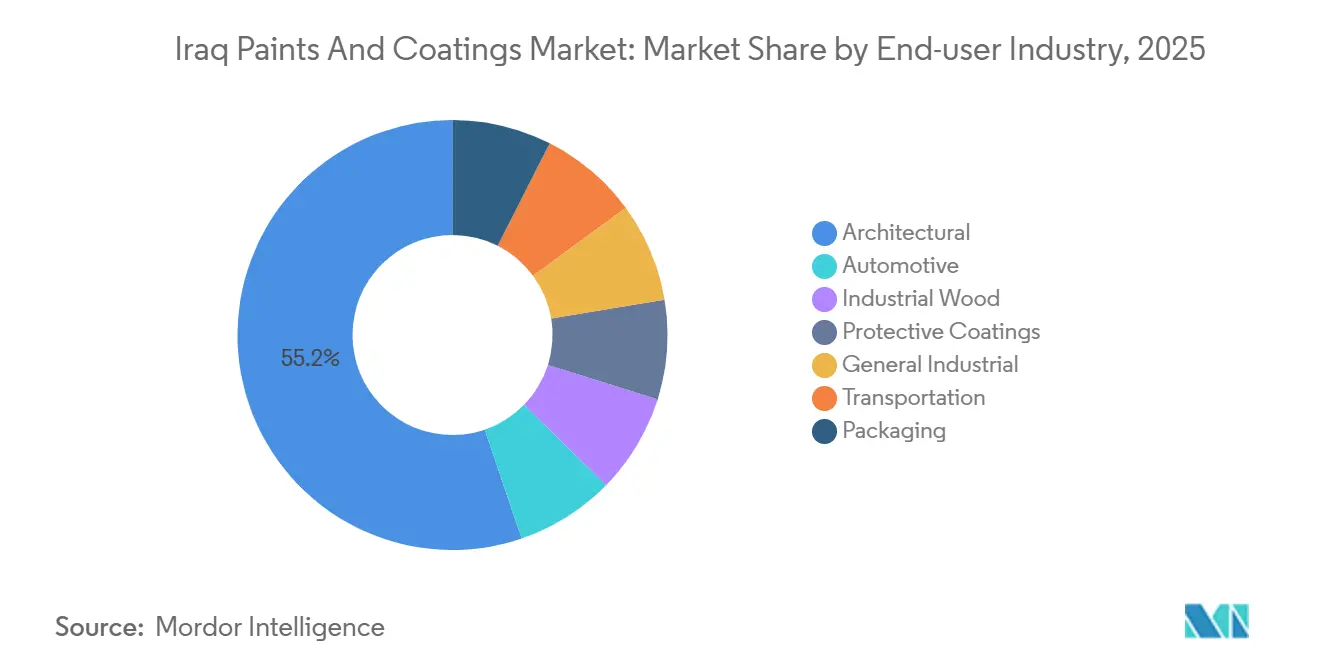

- By end-user industry, architectural industry held 55.22% of the Iraq paints and coatings market share in 2025, while protective coatings are advancing at a 4.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Iraq Paints And Coatings Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust post-ISIS reconstruction spend | +0.9% | National, concentrated in Anbar, Ninewa, Salah ad-Din | Medium term (2–4 years) |

| Elevated CAPEX in downstream oil and gas | +1.1% | South Iraq (Basra, Maysan, Dhi Qar) | Long term (≥ 4 years) |

| Government-backed affordable housing push | +0.8% | National, early gains in Baghdad, Basra | Medium term (2–4 years) |

| Shift toward low-VOC and water-borne systems | +0.5% | National, led by multinational contractor projects | Long term (≥ 4 years) |

| On-premise tinting kiosks enabling mass customization | +0.3% | Urban centers (Baghdad, Erbil, Basra) | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Understand The Key Trends Shaping This Market

Download PDF

Robust Post-ISIS Reconstruction Spend

The United Nations Funding Facility for Stabilization has allocated over USD 1.5 billion across 3,436 projects by 2025, focusing on rebuilding schools, hospitals, and water networks in liberated governorates[1]United Nations Development Programme, “Funding Facility for Stabilization,” undp.org. Reconstruction efforts are shifting from emergency repairs to aesthetic improvements, as demonstrated by a 24% year-over-year increase in decorative-paint imports into Anbar during the first half of 2025. The enforcement of IQS 1101 standards by COSQC for road-marking paints ensures durability, favoring branded acrylic emulsions. Medium-term impacts remain significant, with multi-year contracts under REFAATO extending through 2028. Demand is moving toward color-matched and washable finishes, creating opportunities for premium products.

Elevated CAPEX in Downstream Oil and Gas

Since 2024, TotalEnergies, BP, and Shell have collectively announced over USD 46 billion in downstream projects, each requiring multi-layer epoxy and polyurethane coatings to withstand salinity and high-temperature hydrocarbons. Shell’s USD 11 billion Nibras petrochemical complex, signed in January 2026, alone demands fire-retardant linings for six million tons per year of process capacity. Local steel fabricators upgrading to ISO 12944 compliance further expand the addressable market. Supplier partnerships offering specification support and on-site inspections are gaining a competitive advantage.

Government-Backed Affordable Housing Push

The National Housing Policy aims to deliver five million units by 2030, with the 60,000-unit New Sadr City project leading initial deliveries. Each unit's average consumption of 20 liters of interior emulsion and 8 liters of exterior masonry paint establishes a substantial baseline for architectural coatings. Reflective-roof and heat-shield coatings are now mandatory for public housing to reduce cooling loads in temperatures exceeding 50°C, driving demand for silicone-modified acrylics. Retail expansions, such as Jazeera Paints’ showroom opening in Ranya in February 2026, cater to homeowners seeking personalized color options.

Shift Toward Low-VOC and Water-Borne Systems

Bureau Veritas introduced a third-party VOC certification in 2024, aligning with EU limits of 30 g/L for interior matte finishes. COSQC is drafting solvent-emission thresholds for IQS 1101, set to take effect by 2027, encouraging a shift to water-borne binders. Innovations such as Lubrizol’s 2025 launch of acrylic-polyurethane hybrids and Covestro’s NeoPac PU-485 provide contractors with solvent-like durability at reduced emissions. International EPC firms are increasingly incorporating water-borne requirements into tender specifications, accelerating long-term adoption of these systems.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political instability and delayed public tenders | -0.6% | National, acute in disputed territories | Short term (≤ 2 years) |

| Volatility in crude-linked raw material prices | -0.5% | National, supply-chain dependent | Medium term (2–4 years) |

| Under-developed distribution logistics | -0.4% | Rural governorates, secondary cities | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Political Instability and Delayed Public Tenders

The IMF reported a slowdown in non-oil GDP growth to 1.0% in 2025 due to stalled capital spending. Approximately 40,000 state-enterprise projects remain on hold amid budget disputes and ministerial turnover. Brent crude prices declined from USD 80 per barrel in 2024 to USD 74 in 2025, with projections of USD 66 in 2026, further constraining fiscal resources. Protective-coating projects tied to refinery upgrades or rail rehabilitation are delayed whenever tenders are postponed, reducing supplier revenue visibility. Security premiums in regions like Kirkuk and Diyala inflate contractor bids, exacerbating delays and increasing project costs.

Volatility in Crude-Linked Raw Material Prices

Acrylic monomer prices declined by only 8% in 2025, despite a 17.5% two-year drop in Brent crude prices, reflecting the oligopolistic nature of feedstock supply. Iraq imports 90% of its resins, exposing local producers to exchange-rate risks as the dinar depreciated from 1,460 to 1,520 per USD between 2024 and 2025. Manufacturers have passed some cost increases to distributors, reducing volume elasticity, while tender bidders include price-escalation clauses that limit competitiveness. With limited hedging options, margin compression is expected to persist until contract cycles reset in 2027.

Segment Analysis

By Resin Type: Polyurethane Growth Driven by Durability and Performance

Acrylic resins accounted for 34.75% of Iraq's paints and coatings market share in 2025, supported by their cost-effective washability and color retention for residential interiors. Polyurethane is projected to grow at a 4.02% CAGR through 2031, driven by demand from oil and gas operators for high-build systems that withstand saline mist and desert heat. Covestro’s water-borne polyurethane dispersion meets sub-30 g/L VOC requirements, offering a compliant solution for industrial wood and packaging applications. Alkyd resins are losing market share as reconstruction projects funded by donors prioritize lifecycle costs over initial expenses, requiring ten-year warranties. Epoxy resins remain essential for acid-resistant linings in projects such as Shell’s Nibras complex.

Lubrizol’s hybrid technology combines the UV stability of acrylics with the toughness of polyurethane, aligning with Iraq’s high solar exposure of 11 hours daily. Polyester powder coatings remain niche due to limited domestic appliance production but could expand if investments in white goods materialize. Specialty applications include fluoropolymer additives for road-marking reflectivity and vinyl coatings for swimming pool waterproofing, highlighting the diversity in formulations. Asian Paints’ 55% solids emulsions, sourced from its UAE plant since 2024, reduce labor time by minimizing the number of coats required, appealing to contractors facing skilled labor shortages.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: Water-Borne Coatings Gain Momentum Amid Solvent-Borne Dominance

Solvent-borne technology dominated the Iraq paints and coatings market in 2025, holding a 68.44% share due to its rapid curing under high temperatures (up to 50°C) and its ability to adhere to minimally prepared substrates. However, water-borne technology is growing at the fastest rate, with a 4.22% CAGR projected through 2031, driven by upcoming national VOC regulations and contractor preferences for interior projects catering to international clients. TotalEnergies has specified water-borne coatings for indoor applications in its Gas Growth project, fostering normalized demand among local subcontractors.

Powder, high-solids, and UV-cure technologies remain limited due to the scarcity of application equipment, curing ovens, and skilled applicators. Frequent power outages force manufacturers to rely on diesel generators, adding USD 0.15 per kilogram to powder-coating costs. Architectural coatings are transitioning to water-borne formulations due to health concerns related to occupant exposure, while protective coatings continue to rely on solvent-borne systems for performance. Axalta’s dual-base tinting kiosks enable retailers to cater to both solvent-borne and water-borne demands without increasing inventory, addressing challenges in managing technology transitions.

By End-user Industry: Protective Coatings Drive Growth in Petrochemical Projects

The architectural segment accounted for 55.22% of revenue in 2025, supported by government and private sector efforts to achieve a five-million-unit housing target. Protective coatings are expected to grow at a 4.12% CAGR through 2031, fuelled by over USD 40 billion in downstream investments requiring chemically resistant systems. Hempel’s revenue decline in the Middle-East in 2025 highlights timing risks, but order backlogs suggest future growth as EPC contracts progress to the painting phase.

General industrial and packaging coatings remain underdeveloped due to the manufacturing sector’s limited contribution to GDP. However, new cement and rebar plants commissioned in 2025 indicate incremental volume growth. Automotive refinish demand is rising, driven by a 75% increase in Chinese light-vehicle imports, with BYD’s entry in December 2025 expanding specifications to include OEM-grade finishes. Transportation coatings are seeing modest growth from rail and port infrastructure projects under the USD 17 billion Development Road initiative, creating niche demand for anti-corrosion coatings for rolling stock and bridge components.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

South Iraq accounted for majority of the market size in 2025, with Basra hosting most refineries, petrochemical facilities, and port expansions. Ongoing EPC activities are driving sustained demand for epoxy and polyurethane coatings. Marine coating volumes are increasing as construction at Grand Faw Port accelerates. Gulf port import routes enhance supply reliability, reducing lead times by up to 15 days compared to landlocked regions.

Baghdad and central governorates represent a balanced architectural market, driven by projects such as the New Sadr City development and public-sector office renovations. Retail chains have positioned tint-on-demand kiosks within five kilometers of major housing clusters, improving convenience for homeowners. However, periodic budget freezes have slowed ministry refurbishments, moderating growth compared to the south.

North Iraq, led by Erbil and Sulaymaniyah, is expected to achieve the fastest regional growth through 2031. A favorable business environment, formalized land-lease regulations, and lower perceived corruption are attracting light manufacturing investments, boosting demand for general industrial coatings. Cooler winters in the region support the adoption of water-borne formulations with reduced freeze-thaw risks. However, unresolved fiscal transfers from Baghdad and security concerns in Kirkuk continue to limit growth potential until the northern segment of the Development Road is completed after 2028.

Competitive Landscape

The competitive landscape features a mix of multinational, regional, and local brands competing across various price tiers. Jotun, Akzo Nobel, and Asian Paints leverage regional facilities and technical service teams to maintain their presence in high-value projects. Jazeera Paints is expanding its showroom network, adding a sixth outlet in Ranya in February 2026, offering 16,000 color options from 12 bases[2]Jazeera Paints, “Ranya Showroom Opening,” jazeerapaints.com . Nasr Paint introduced Iraq’s first civil-defense-approved fire-resistant coating in 2025, establishing a niche in safety-compliant high-rise projects.

Regional players benefit from proximity advantages, while local producers focus on smaller contracts where price outweighs warranty considerations. Hempel’s revenue decline in the Middle-East in 2025 reflects volatility in Iraq’s tender pipeline. Technology partnerships, such as Axalta’s Irus Mix, enable distributors to expand product offerings cost-effectively, enhancing service differentiation.

Underserved segments include industrial wood and packaging coatings. The Ministry of Industry’s 2025 investment plan includes a USD 50 million wood-processing complex in Anbar, which could drive demand for UV-cured coatings if funded. Suppliers offering scalable hybrid water-borne systems can secure early specifications. Compliance with COSQC regulations remains a critical requirement for public tenders, increasing pressure on smaller operators to certify their formulations.

Iraq Paints And Coatings Industry Leaders

Jazeera Paints

Jotun

Akzo Nobel N.V.

Caparol Paints

NATIONAL PAINTS FACTORIES CO. LTD.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: Iraq commenced full-capacity operations at the Salah al-Din-3 and North Refinery-2 facilities in Kirkuk, each with a processing capacity of 70,000 barrels per day (bpd), contributing a total of 140,000 bpd. These advancements, which focused on enhancing the production of high-quality, Euro 5 compliant fuel, heightened the demand for specialized, high-performance industrial coatings to support essential infrastructure maintenance.

- September 2024: Iraq introduced its National Strategy for Environmental Protection for the period 2024-2030, assigning the Ministry of Environment to monitor industrial emissions and ensure environmental compliance. The strategy emphasized the implementation of stricter regulations on low-VOC coating formulations and the promotion of sustainable manufacturing practices.

Iraq Paints And Coatings Market Report Scope

Paints and coatings are specialized materials in liquid, gas, or solid form, applied to surfaces to offer protection, decoration, and enhanced functionality. They play a vital role in preventing corrosion, resisting moisture, and increasing the durability of substrates such as metal, wood, and concrete.

The Iraq paints and coatings market is segmented by resin type, technology, and end-user industry. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types (fluoropolymer, vinyl, etc.). By technology, the market is segmented into water-borne, solvent-borne, and other technologies. By end-user industry, the market is segmented into architectural, automotive, industrial wood, protective coatings, general industrial, transportation, and packaging. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types (fluoropolymer, vinyl, etc.) |

By Technology

| Water-borne |

| Solvent-borne |

| Other Technologies |

By End-user Industry

| Architectural |

| Automotive |

| Industrial Wood |

| Protective Coatings |

| General Industrial |

| Transportation |

| Packaging |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types (fluoropolymer, vinyl, etc.) | |

| By Technology | Water-borne |

| Solvent-borne | |

| Other Technologies | |

| By End-user Industry | Architectural |

| Automotive | |

| Industrial Wood | |

| Protective Coatings | |

| General Industrial | |

| Transportation | |

| Packaging |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Iraq paints and coatings market?

The Iraq paints and coatings market stands at USD 267.20 million in 2026 and is projected to reach USD 322.29 million by 2031.

Which resin type is growing fastest through 2031?

Polyurethane resins are forecast to expand at a 4.02% CAGR through 2031 as oil and gas operators specify high-durability coatings.

Why did solvent-borne technology dominate in 2025?

Protective coatings for pipelines and tanks need quick cure and temperature resilience that water-borne systems cannot yet match, preserving a 68.44% share of solvent-borne technology in 2025.

What is the main distribution challenge for coating suppliers?

Limited warehousing, unreliable grid power, and fragmented retail channels raise logistics costs and cause stock-outs, especially in rural governorates.