IoT Microcontroller Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 6.11 Billion |

| Market Size (2030) | USD 13.28 Billion |

| Growth Rate (2025 - 2030) | 16.81% CAGR |

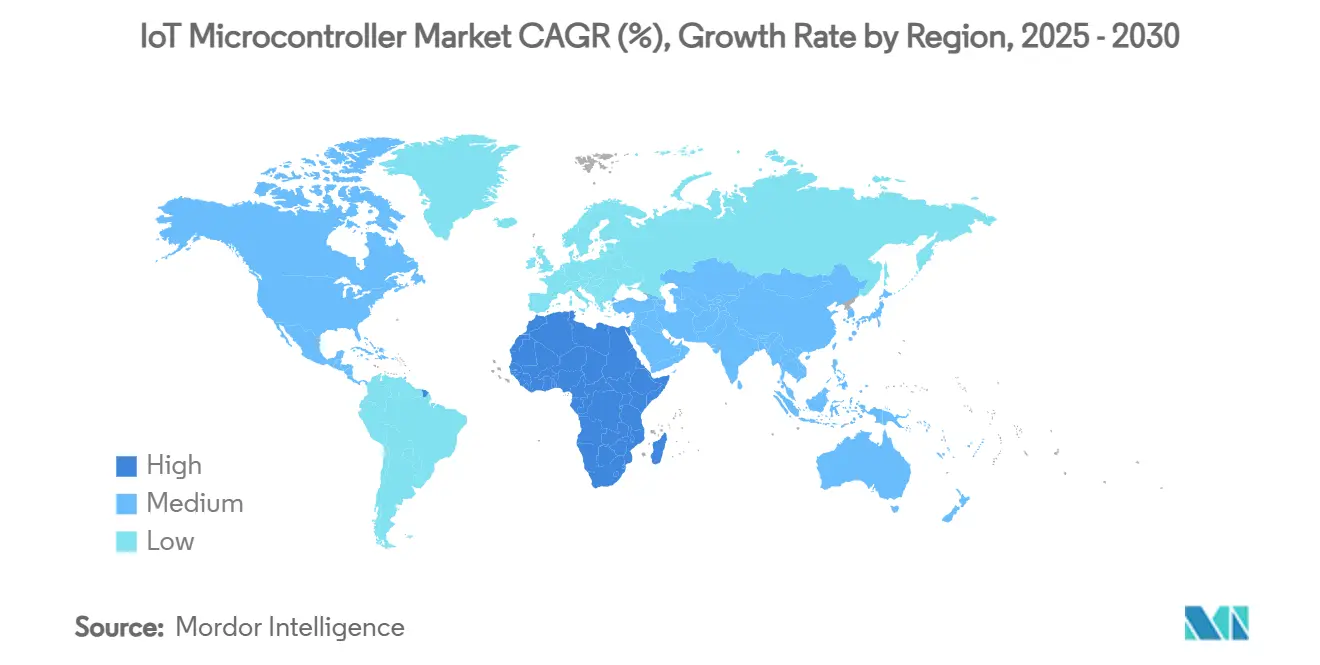

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

IoT Microcontroller Market Analysis by ���ϲ�����

The IoT Microcontroller Market size is estimated at USD 6.11 billion in 2025, and is expected to reach USD 13.28 billion by 2030, at a CAGR of 16.81% during the forecast period (2025-2030).

Underpinned by the fusion of edge-AI engines with ultra-low-power processing cores. Automotive electrification, smart-city infrastructure roll-outs, and the ubiquity of connected consumer devices underpin today’s demand curve, while the shift toward 64-bit and RISC-V architectures signals the next performance leap for intelligent edge nodes.[1]Sally Ward-Foxton, “STMicro Launches NPU-Equipped Microcontroller,” EE Times, eetimes.com Increasing regulatory scrutiny—most notably the EU Cyber Resilience Act—raises the security baseline and compels suppliers to embed hardware-root-of-trust functions as standard. Supply-chain realignment continues, with mature-node capacity and advanced packaging investments shaping where the IoT microcontroller market sources wafers over the medium term. Competitive intensity is rising as ARM incumbents defend share against RISC-V challengers, even as start-ups leverage open-source IP to undercut royalty-based business models.[2]Martin Lesund, “Cellular IoT Dominates LPWANs,” Wevolver, wevolver.com

Key Report Takeaways

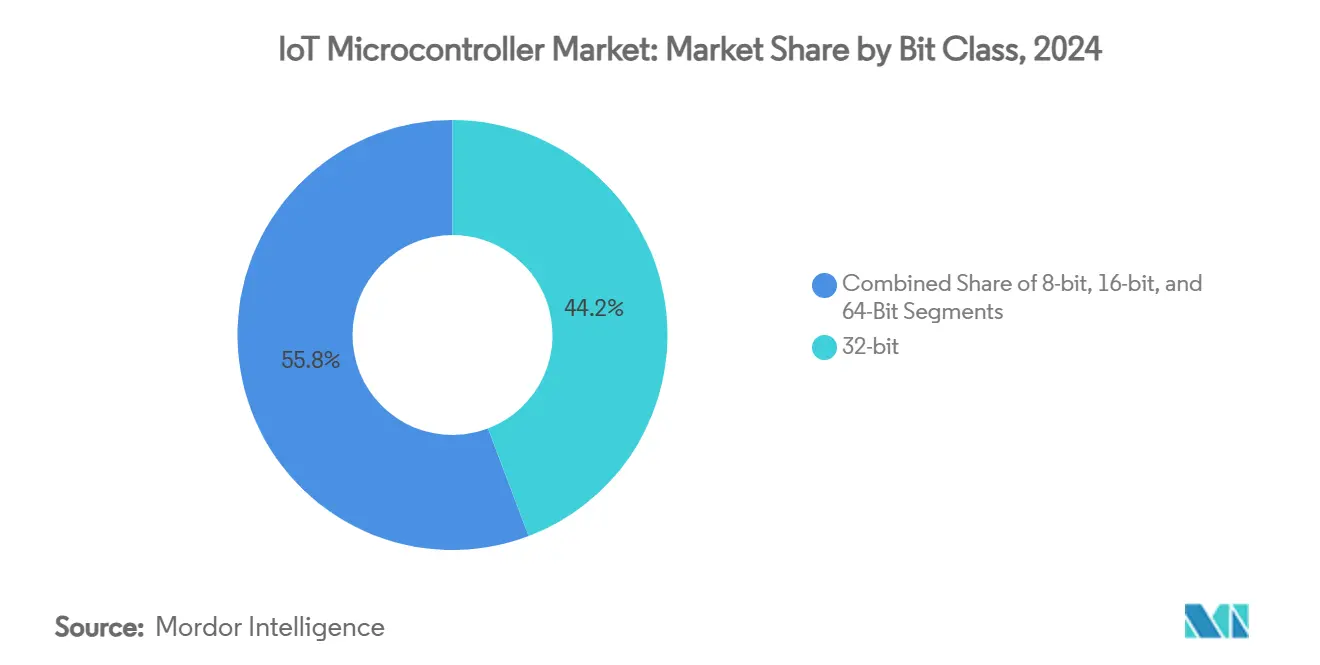

- By bit class, 32-bit devices led with 44.23% of IoT microcontroller market share in 2024 while 64-bit units are forecast to expand at a 17.23% CAGR through 2030.

- By connectivity, Wi-Fi held 34.54% of the IoT microcontroller market size in 2024, whereas cellular NB-IoT/LTE-M is set to grow at a 19.45% CAGR to 2030.

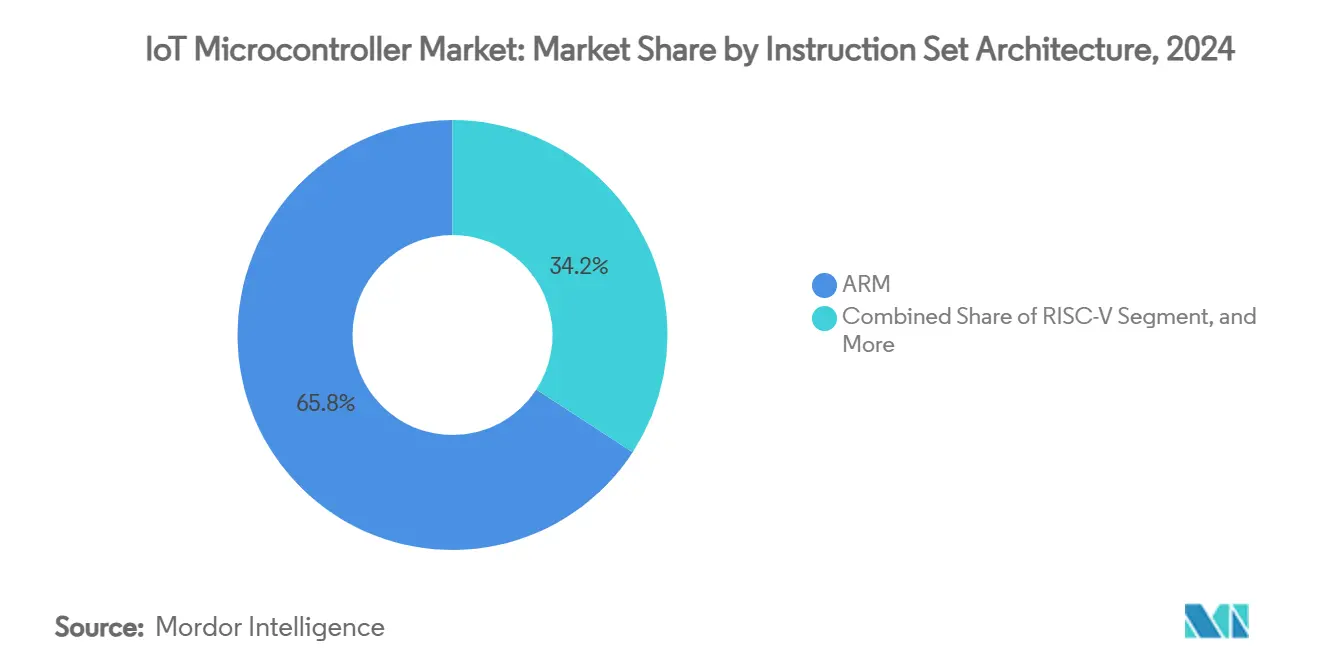

- By instruction-set architecture, ARM commanded 65.81% share of the IoT microcontroller market in 2024; RISC-V exhibits the fastest trajectory at 22.65% CAGR through 2030.

- By application, automotive and transportation captured 36.23% of the IoT microcontroller market size in 2024, but smart-city infrastructure is advancing at an 18.92% CAGR through 2030.

- By geography, Asia-Pacific dominated with 41.87% IoT microcontroller market share in 2024, while Africa is expected to post a 20.53% CAGR, the highest regionally, during the forecast period.

Global IoT Microcontroller Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of connected consumer devices | +3.2% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Rising demand for automotive electronics | +2.8% | Global, led by Europe & North America regulatory push | Long term (≥ 4 years) |

| Transition to cost-efficient 32-bit MCUs | +2.1% | APAC manufacturing hubs, expanding to MEA | Short term (≤ 2 years) |

| Open-source RISC-V customization boom | +1.9% | Global, early adoption in China & Europe | Medium term (2-4 years) |

| Edge-AI accelerators on IoT MCUs | +2.4% | North America & EU innovation centers | Long term (≥ 4 years) |

| Green procurement favouring ultra-low-power MCUs | +1.7% | EU regulatory leadership, spreading globally | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Proliferation of Connected Consumer Devices

More than 2.57 billion IoT terminals were active in China by August 2024, underscoring how smart-home ecosystems catalyze silicon demand in the IoT microcontroller market. MCUs now bundle multi-protocol radios—NXP’s RW612 supports simultaneous Wi-Fi 6 and Bluetooth LE 5.4—to meet Matter-compliant interoperability requirements. Lifecycle-management tool chains are becoming purchase criteria, evidenced by Nordic Semiconductor’s June 2025 acquisition of Memfault to unify silicon, firmware, and cloud services. Subscription-based device services now demand robust OTA update pipelines, pushing vendors to integrate secure boot, encrypted storage, and cloud hooks at minimal energy budgets. As cross-brand interoperability matures, suppliers that streamline software complexity while sustaining low power win mindshare among appliance makers.

Rising Demand for Automotive Electronics

Per-vehicle semiconductor spend is projected to rise to USD 1,200 by 2030, doubling 2024 levels as EV adoption and ADAS penetration grow. Infineon captured 29% global automotive MCU share in 2023 on the back of its AURIX and TRAVEO portfolios. NXP’s S32K5, the first 16 nm FinFET automotive MCU with embedded MRAM, illustrates how zonal architectures consolidate ECUs while lifting functional-safety ceilings. Battery-management systems and sensor-fusion workloads increasingly need integrated ML accelerators and time-sensitive networking support, expanding silicon content per chassis. As over-the-air software upgrades become routine, rigorous cybersecurity mandates such as UNECE R155 push hardware-root-of-trust requirements deeper into the bill of materials.

Transition to Cost-Efficient 32-bit MCUs

Accelerated migration away from 8-bit and 16-bit architectures reflects system-level cost savings that offset higher die area. STMicroelectronics reported a 46% YoY revenue drop in legacy MCU lines by Q2 2024 as design-ins shifted toward higher-value 32-bit offerings.[3]“Best Microcontrollers for Machine Learning,” STMicroelectronics, st.com Microchip now derives 53% of FY 2025 revenue from IoT verticals built on 32-bit cores, confirming mainstream acceptance in cost-sensitive segments. Higher peripheral integration eliminates external components—such as discrete ADCs and RF front-ends—cutting total BOM despite richer functionality. Process shrinkage pushes 32-bit pricing to historic 16-bit levels, widening the adoption funnel in wearables and industrial sensors accelerating growth in the IoT microcontroller market.

Open-Source RISC-V Customization Boom

Royalty-free licensing and geostrategic autonomy fuel a 22.65% CAGR for RISC-V cores through 2030. Microchip’s parallel 64-bit RISC-V and ARM roadmaps exemplify supplier hedging strategies. Custom implementations achieve 17% lower power draw than Cortex-M0 equivalents by pruning unused opcodes and inserting DSP extensions. China’s SOPHGO SG2380 stacks 32 TOPS into a 16-core SiFive design as Beijing’s import-substitution agenda accelerates homegrown ISA uptake. However, immature tool chains and fragmented middleware ecosystems lengthen learning curves for resource-constrained teams, tempering near-term volume.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor supply-chain constraints | -2.1% | Global, acute in automotive & industrial segments | Short term (≤ 2 years) |

| Stringent IoT security compliance costs | -1.8% | EU leadership, expanding to North America & APAC | Medium term (2-4 years) |

| Protocol-stack fragmentation complexity | -1.5% | Global, particularly challenging in multi-vendor ecosystems | Medium term (2-4 years) |

| Patent litigation over low-power wireless IP | -1.2% | North America & Europe primary litigation venues, global impact | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Semiconductor Supply-Chain Constraints

Lead times have compressed from 2022 crisis peaks but still exceed pre-pandemic norms for mature-node MCUs, as foundries prioritize AI accelerators on advanced nodes. Industry-wide 300 mm capacity investments exceed USD 400 billion through 2027, yet only a fraction targets 90 nm–180 nm processes central to the IoT microcontroller market. Texas Instruments’ USD 60 billion domestic wafer plan aims to control 95% of internal output by 2030, signaling a strategic pivot toward vertical integration for supply resilience in the IoT microcontroller market. Export-control frictions between the United States and China inject risk premiums, prompting OEMs to qualify second-source silicon in parallel to primary suppliers.

Stringent IoT Security Compliance Costs

The EU Cyber Resilience Act, effective December 2024, mandates secure-by-design principles, pushing non-compliant vendors out of regulated markets. Microchip’s CRA reference stack shows the added bill of materials: hardware security modules, isolated key storage, and encrypted OTA workflows. Penalties of up to EUR 15 million (USD 16.5 million) or 2.5% of global revenue elevate cybersecurity from feature to compliance cost center, especially for SMEs with limited engineering headcount. Parallel frameworks in the United States and Japan heighten the need for a “design-once, certify-everywhere” approach, extending development schedules and budgets.

Segment Analysis

By Bit Class: 64-bit Builds Momentum Beyond 32-bit Leadership

The 32-bit tier maintained 44.23% IoT microcontroller market share in 2024, an anchor across home automation and industrial sensing. However, 64-bit units are forecast to compound at 17.23% CAGR through 2030 as edge-AI inference moves on-die. ST’s STM32N6 packs 600 GOPS in a microcontroller power envelope, exemplifying how 64-bit cores stretch compute density without resorting to application processors. Legacy 8-bit and 16-bit devices retreat to ultra-low-cost lighting and appliance controllers, but cost-down trends in 32-bit silicon narrow price gaps, accelerating obsolescence. Code-porting hurdles remain a friction point; however, vendor-supplied migration libraries and abstraction layers soften switching costs.

Edge-centric datasets-from voice to vibration signatures-require 64-bit address spaces for low-latency analytics. Early adopters in industrial vision and predictive maintenance are willing to pay premiums for on-chip inference to avoid cloud round-trips. In response, roadmap disclosures from Microchip and Renesas outline 64-bit RISC-V SoCs with optional AI coprocessors due 2026. The emergent sweet-spot positions 64-bit MCUs as gateways bridging sensor networks and mid-tier application processors, an architectural middle ground poised for rapid scaling.

Note: Segment shares of all individual segments available upon report purchase

By Connectivity Type: Cellular IoT Upshifts Growth Curve

Wi-Fi remained the largest slice at 34.54% of the IoT microcontroller market in 2024, serving bandwidth-hungry cameras and smart-home hubs. Cellular NB-IoT/LTE-M, however, accelerates at 19.45% CAGR, powered by municipal roll-outs and nationwide meter readings. Nordic’s nRF9160-based street-light controllers illustrate how battery-optimized LTE links enable infrastructure assets without local gateways. Multi-protocol SoCs blend Wi-Fi 6, BLE, and Thread in a single die, mitigating fragmentation risk and future-proofing against evolving standards like Matter.

Bluetooth/BLE’s pervasive install base keeps it entrenched in wearables, whereas Thread and Zigbee gain new life as low-latency backbones for interoperable lighting ecosystems. The “no-radio” MCU niche shrinks as connectivity becomes a default expectation; silicon vendors unable to integrate RF blocks face ASP erosion. Long-range sub-GHz and proprietary LoRa variants still serve agriculture and remote asset tracking, but integration trends favor universal chipsets supporting multiple stacks under one secure boot architecture.

By Instruction Set Architecture: RISC-V Steps Out of Niche Territory

ARM’s 65.81% share reflects three decades of ecosystem investment, yet rising license fees and export-control uncertainties propel designers toward RISC-V, expanding at 22.65% CAGR. China’s 14th Five-Year Plan explicitly references open ISA adoption, fast-tracking local 32-bit and 64-bit derivatives. Infineon’s proposal to standardize RISC-V safety extensions for automotive indicates that Tier 1s value architectural optionality. x86 variants, though niche, persist where legacy software stacks dictate continuity.

RISC-V’s modular instruction sets allow custom AI and crypto extensions unmatched in fixed ISAs, yielding differentiated power-performance points. Yet tool-chain fragmentation and quality-of-service variability among IP providers remain barriers. ARM counters with low-touch licensing for Cortex-M-class cores and ecosystem bundles, buying time while it readies v9 security and ML features tuned for cost-sensitive IoT workloads.

Note: Segment shares of all individual segments available upon report purchase

By Application: Smart-City Infrastructure Outpaces Legacy Segments

Automotive retained 36.23% IoT microcontroller market size in 2024, propelled by zonal architectures, battery-management units, and ADAS domain controllers. Smart-city projects, though smaller today, are forecast to grow at an 18.92% CAGR, leveraging energy-saving street lighting, adaptive traffic control, and environmental sensing platforms. Connected lighting alone cuts municipal electricity usage by 30%, creating self-funding deployment models. Industrial automation sustains double-digit momentum as predictive maintenance reduces unplanned downtime by up to 50%. Healthcare’s regulated slope slows volume growth but boosts ASPs; medical device OEMs demand long-term software support and cryptographic authenticity.

Wearables and smart-home appliances benefit from Matter’s brand-agnostic ecosystem, tilting MCU selection toward multi-protocol SoCs with secure OTA frameworks. Agriculture-particularly in South America-experiences steady sensorization to optimize irrigation and crop yields, albeit tempered by connectivity gaps. Across segments, AI-capable MCUs redefine value propositions, shifting competition from MHz and flash to TOPS/W and DevOps tool-chain breadth.

Geography Analysis

Asia-Pacific commanded 41.87% of IoT microcontroller market share in 2024 on the back of integrated manufacturing clusters spanning wafers, OSAT, and EMS services. China targets USD 295 billion domestic semiconductor revenue by 2030, supported by sovereign-fund injections and preferential tax credits. Taiwan’s foundry leadership, Korea’s memory depth, and Japan’s material science prowess sustain the region’s supply-chain gravity. Yet export-license headwinds spur “China-plus-one” strategies, redirecting some assembly activity to Southeast Asia and India.

Europe wields regulatory influence through the Cyber Resilience Act, effectively setting global security baselines that ripple across product roadmaps. The EUR 43 billion (USD 47.4 billion) Chips Act seeks to elevate regional fab share to 20% by 2030, creating grant-funded opportunities for 28 nm MCU lines. Germany’s automotive OEM cluster drives high-ASP microcontroller demand for zone controllers, while the Nordics innovate around ultra-low-power wireless solutions.

Africa registers the highest regional CAGR at 20.53% as mobile-first economies leapfrog fixed infrastructure, adopting cellular IoT and satellite backhaul for agriculture, logistics, and utilities, accelerating adoption in the IoT microcontroller market. Limited legacy systems allow clean-sheet smart-city designs, although currency volatility and import duties challenge supply. North America enjoys automotive electronics tailwinds and IIoT retrofits in brownfield factories but competes with cost-optimized Asian imports. South America shows mid-single-digit growth amid macroeconomic swings, with agritech as a bright spot; the Middle East funnels petro-dollars into energy management and urban digitization pilots, serving as early references for desert-climate IoT deployments.

Competitive Landscape

IoT microcontroller market structure tilts toward moderate concentration: top five vendors command just over 60% combined revenue, leaving space for design-win upsets. Incumbents STMicroelectronics, NXP, Infineon, Renesas, and Microchip scale wafer volumes and furnish extensive SDK ecosystems, forming a defensive moat. Yet RISC-V start-ups and Chinese IDMs enter with price-aggressive, customizable chips, prompting incumbents to adopt architectural agnosticism. Platform strategies dominate: Nordic’s acquisition of Memfault bundles device analytics with silicon, moving revenue mix beyond hardware. STMicroelectronics and Qualcomm’s collaboration integrates STM32 compute with Wi-Fi/BT/Thread combo radios, aiming for turnkey industrial modules.

Technology differentiation centers on edge-AI acceleration. NXP’s MCX N series touts 30× ML uplift and 3× power savings, positioning it for voice-command endpoints. Patent filings from Meta signal cross-industry entrants who could license ML accelerators to MCU makers, blurring traditional boundaries. Supply-chain ownership is emerging as strategic leverage; Texas Instruments’ fab expansion and Infineon’s partnership with Flex for modular zone controllers underscore the race to secure capacity and shorten design-to-production cycles.

IoT Microcontroller Industry Leaders

NXP Semiconductors N.V.

Renesas Electronics Corporation

STMicroelectronics N.V.

Microchip Technology Inc.

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nordic Semiconductor acquired Memfault, creating a chip-to-cloud lifecycle-management platform that deepens customer lock-in and opens recurring-revenue streams.

- April 2025: NXP launched MCX L14x/L25x ultra-low-power MCUs and reported USD 2.835 billion Q1 revenue, reinforcing its strategy to pair dual-core heterogeneous compute with power-optimized sensor domains.

- March 2025: NXP introduced S32K5 automotive MCUs on 16 nm, embedding MRAM for instant-on code execution to support software-defined vehicles, positioning itself ahead in zonal-controller design cycles.

- February 2025: STMicroelectronics unveiled STM32N6 with Neural-ART accelerator delivering 600 GOPS, signaling a tactical move to embed AI in MCU price points and defend against edge-SoC encroachment.

Global IoT Microcontroller Market Report Scope

| 8-bit |

| 16-bit |

| 32-bit |

| 64-bit |

| No Integrated Connectivity |

| Wi-Fi |

| Bluetooth / BLE |

| Zigbee / Thread |

| Cellular NB-IoT / LTE-M |

| Multi-protocol SoC |

| ARM |

| RISC-V |

| x86 |

| Proprietary / Others |

| Smart Home and Wearables |

| Industrial Automation and IIoT |

| Automotive and Transportation |

| Healthcare and Medical Devices |

| Smart City Infrastructure |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Bit Class | 8-bit | ||

| 16-bit | |||

| 32-bit | |||

| 64-bit | |||

| By Connectivity Type | No Integrated Connectivity | ||

| Wi-Fi | |||

| Bluetooth / BLE | |||

| Zigbee / Thread | |||

| Cellular NB-IoT / LTE-M | |||

| Multi-protocol SoC | |||

| By Instruction Set Architecture | ARM | ||

| RISC-V | |||

| x86 | |||

| Proprietary / Others | |||

| By Application | Smart Home and Wearables | ||

| Industrial Automation and IIoT | |||

| Automotive and Transportation | |||

| Healthcare and Medical Devices | |||

| Smart City Infrastructure | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the IoT microcontroller market?

The IoT microcontroller market size is USD 6.11 billion in 2025 and is forecast to reach USD 13.28 billion by 2030.

Which architecture is growing fastest in IoT microcontroller market?

The IoT microcontroller market is experiencing its fastest architectural growth in RISC-V cores, projected to expand at a 22.65% CAGR through 2030 as developers increasingly adopt royalty-free, customizable designs.

Why are 64-bit MCUs gaining traction?

Edge-AI workloads and large-dataset processing require 64-bit addressing and higher compute density, driving a 17.23% CAGR for 64-bit devices.

How will the EU Cyber Resilience Act affect suppliers?

The Act enforces secure-by-design mandates and hefty penalties, elevating development costs and favoring vendors with integrated security IP.

Which region is the fastest-growing IoT microcontroller market?

Africa leads regional growth at a 20.53% CAGR as mobile-first infrastructure supports leapfrog IoT deployments.

What is the key competitive differentiator today?

Integrated AI acceleration and comprehensive chip-to-cloud tool chains now outweigh raw MHz, shaping supplier roadmaps and buyer criteria.