Industrial Fabric Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

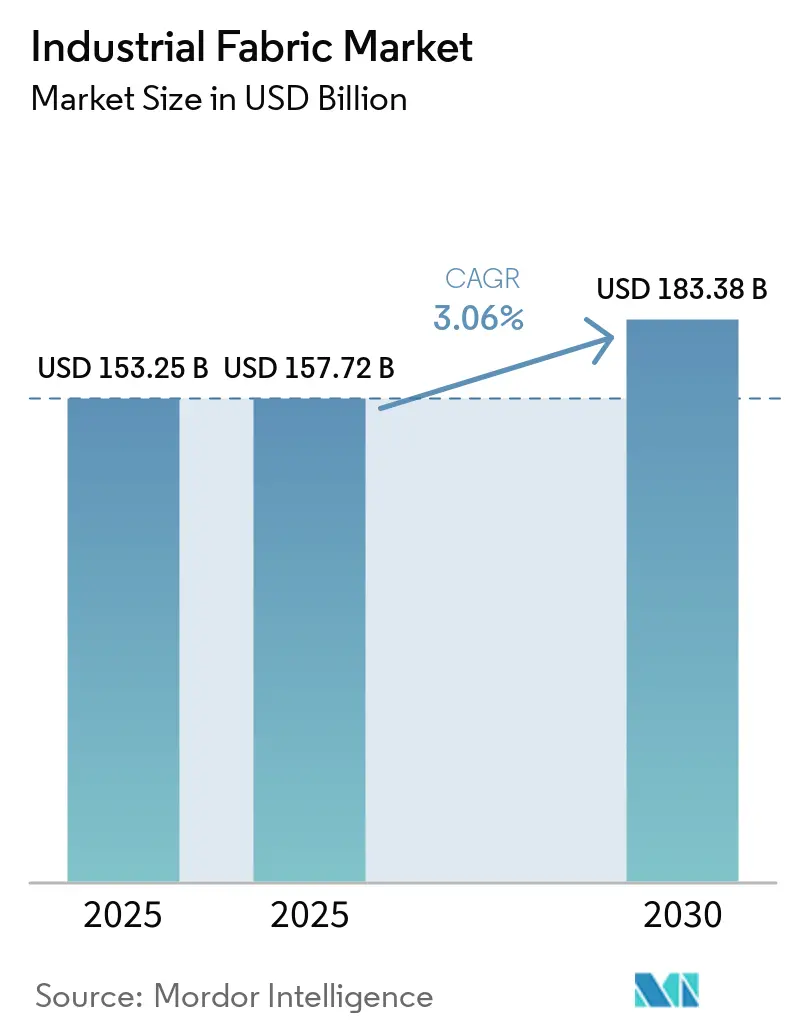

| Market Size (2025) | USD 157.72 Billion |

| Market Size (2030) | USD 183.38 Billion |

| Growth Rate (2025 - 2030) | 3.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Industrial Fabric Market Analysis by ���ϲ�����

The Industrial Fabric Market size was valued at USD 153.25 billion in 2025 and is estimated to grow from USD 157.72 billion in 2025 to reach USD 183.38 billion by 2030, at a CAGR of 3.06% during the forecast period (2025-2030). Industries are shifting from commodity polyester to specialized materials, including aramid, carbon, and hybrid fibers, leading to widening price bands. This transition is paving the way for premium applications, such as crash-absorbing auto parts, ISO 8 gigafactory cleanrooms, and 100-meter wind-blade spar caps. Demand is further strengthened by the record installation of conveyor belts in mining and logistics, the widespread adoption of NFPA 2112 flash-fire apparel, and the Asia-Pacific's dominant polyester capacity, which reinforces its global cost leadership. Concurrently, recycled-content mandates from China and the EU are reshaping feedstock flows and increasing quality-control overheads for converters in Southeast Asia. The competitive landscape increasingly favors vertically integrated fiber giants like Toray, DuPont, and Freudenberg. These industry leaders are pushing downstream into finishing, coating, and cleanroom non-wovens, aiming to protect their margin spreads.

Key Report Takeaways

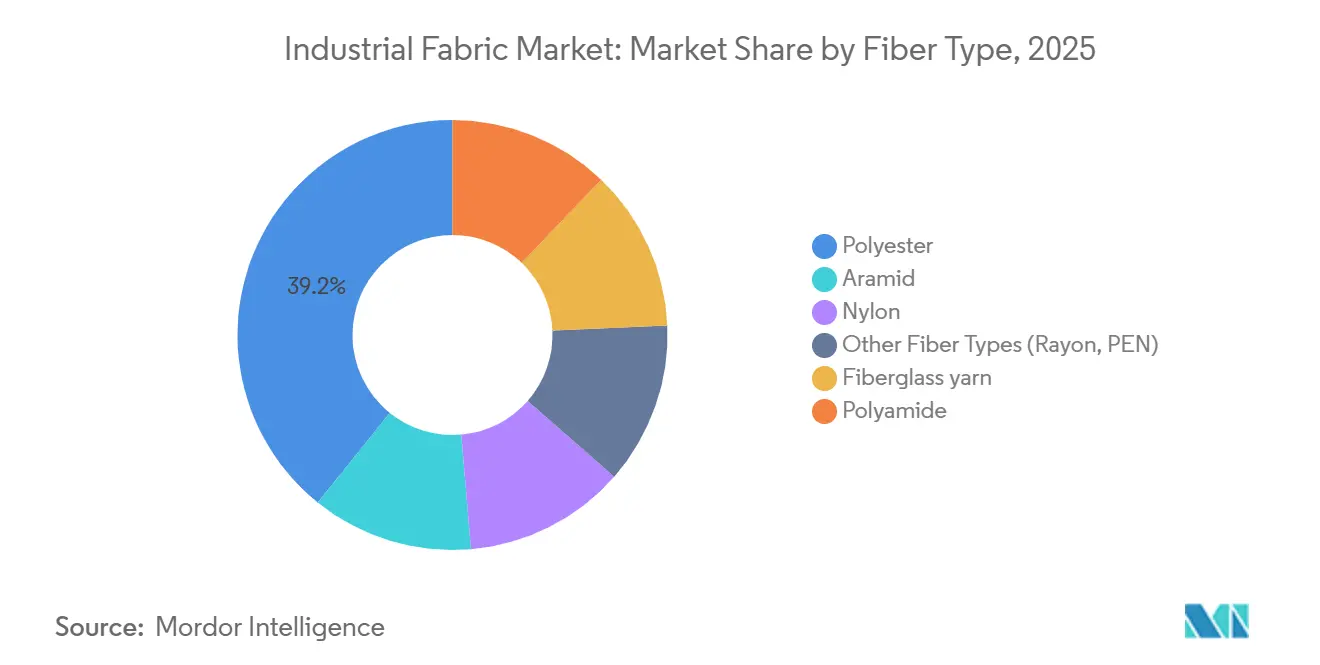

- By fiber type, polyester led with 39.22% of the industrial fabric market share in 2025, while aramid recorded the highest projected CAGR at 5.89% through 2031.

- By fabric construction, woven fabrics accounted for 45.28% of the industrial fabric market size in 2025 and are advancing at a 4.21% CAGR through 2031.

- By application, conveyor belts held 28.09% revenue share in 2025; fire-protective apparel is forecast to expand at a 5.14% CAGR to 2031.

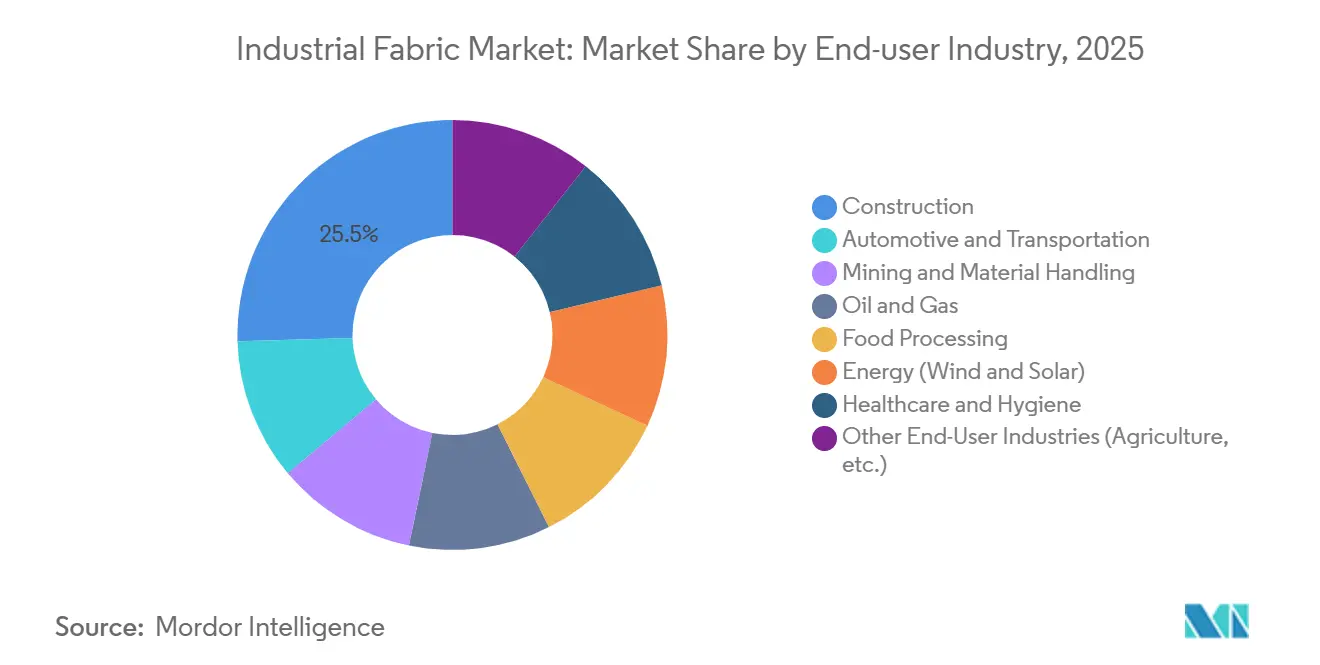

- By end-user industry, construction captured 25.46% of 2025 revenue, while automotive and transportation are the fastest-growing segments at 5.55% CAGR to 2031.

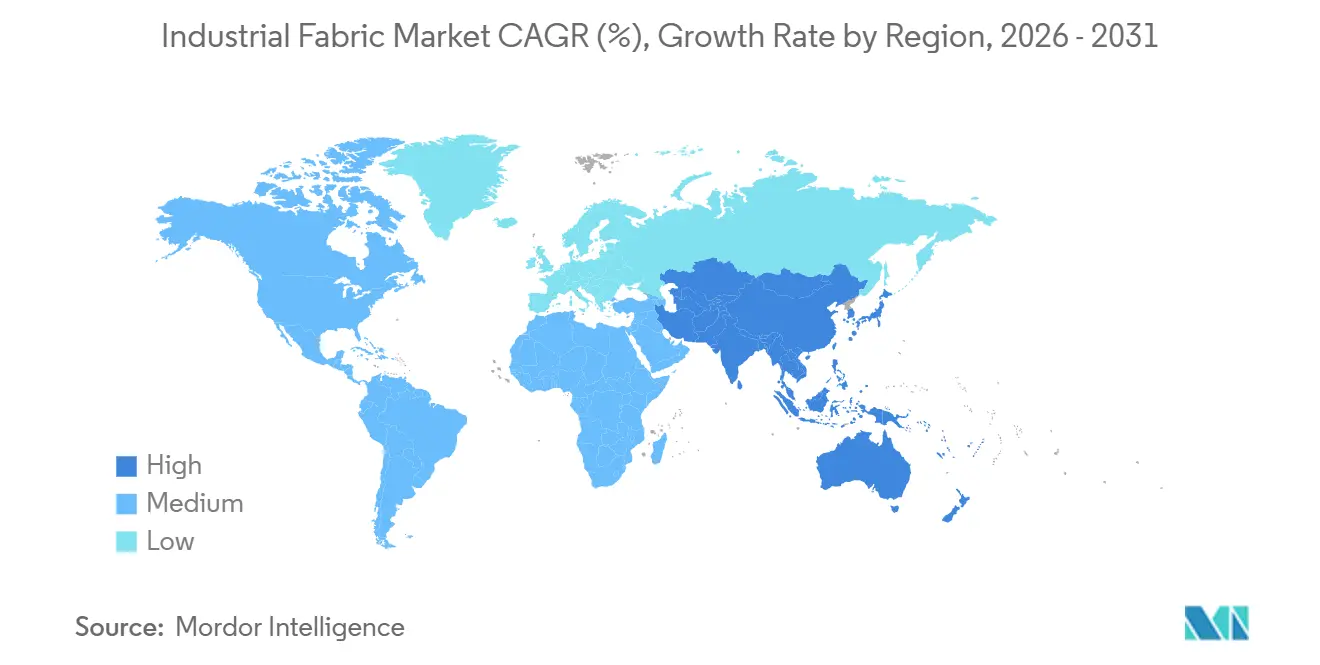

- By geography, Asia-Pacific commanded 41.14% of global revenue in 2025 and is projected to grow at a 5.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Fabric Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly growing application in automotive lightweighting | +0.80% | Global, with concentration in Europe, North America, and China | Medium term (2-4 years) |

| Rising demand for conveyor and transmission belts in intralogistics | +0.60% | Asia-Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Infrastructure push for on-shore and off-shore wind-turbine blades | +0.70% | Europe, North America, and coastal Asia-Pacific | Long term (≥ 4 years) |

| High-temperature filtration upgrades in cement and metal plants | +0.40% | Asia-Pacific, Middle-East, and South America | Medium term (2-4 years) |

| Shift to advanced geotextiles for climate-resilient infrastructure | +0.50% | North America, Europe, and coastal regions globally | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Demand for Conveyor and Transmission Belts in Intralogistics

Global e-commerce fulfillment centers are processing a record number of daily orders, underscoring the need for high conveyor uptime. This surge in demand has spurred unprecedented belt installations across megawarehouses in the Asia-Pacific region. At Chile’s Chuquicamata copper mine, Kevlar-reinforced belts, which are lighter and more energy-efficient than their steel-cord counterparts, are enjoying an extended service life. Continental’s CONTIFLEX series, crafted from polyester-nylon, features wide widths and high tensile ratings, making them reliable for transporting coal[1]Continental, “CONTIFLEX Textile Conveyor Belts,” continental.com . Semperit’s Transoil covers, which are oil-resistant and FDA-compliant, are making inroads in food and chemical plants. Concurrently, robust capital expenditure programs at Asian express-parcel hubs are fueling the growth of the industrial fabric market.

Infrastructure Push for On-Shore and Off-Shore Wind-Turbine Blades

GE Vernova’s blades, which heavily utilize glass and carbon fiber, are driving a surge in material demand, capturing a significant slice of the global E-glass output. By incorporating carbon in spar caps and glass in shells, hybrid lay-ups achieve weight reductions, enabling taller hub heights and enhanced annual energy capture. Thermoplastic roots, when paired with steel inserts through induction welding, eliminate the need for adhesive inspections and reduce assembly time. Furthermore, the strategic use of basalt and aramid fibers in trailing edges targets fatigue-critical zones, which endure millions of load cycles.

High-Temperature Filtration Upgrades in Cement and Metal Plants

Cement kilns and steel furnaces now face stringent regulations, limiting particulates to specific levels. This regulatory push is spurring the retrofitting of advanced filter fabrics, such as ceramic-fiber and expanded-PTFE. These fabrics not only withstand high exhaust temperatures but also boast impressive capture efficiency. Gore’s ePTFE membranes stand out by resisting sulfuric-acid condensation, a challenge that quickly degrades polyester felts. Bekaert’s sintered metal fibers, designed for high-pressure endurance, are crucial for catalytic crackers.

Shift to Advanced Geotextiles for Climate-Resilient Infrastructure

Highways and levees are grappling with intensified freeze-thaw cycles and unprecedented floods. In Saskatchewan, Highway 7, enhanced with GEOWEB geocells, saw a boost in resilient modulus, leading to reduced rut depth post-winter[2]Saskatchewan Ministry of Highways, “Highway 7 Geocell Trial,” saskatchewan.ca . The Texas Department of Transportation's use of wicking fabrics effectively drained moisture, cutting down subgrade moisture and preventing costly repairs. In Louisiana, coastal deployment of Secutex achieved commendable vegetation survival rates over time.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock price volatility | -0.50% | Global, with acute impact in Asia-Pacific and Middle-East | Short term (≤ 2 years) |

| Transition toward bio-based technical textiles cannibalizing synthetics | -0.30% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Self-healing elastomer power-transmission belts | -0.20% | Global, with early adoption in mining and heavy industry | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Petrochemical Feedstock Price Volatility

In February 2026, Northeast Asia's naphtha prices surged past Middle-Eastern benchmarks. This uptick, coupled with PTA prices lagging behind crude fluctuations, squeezed polyester-staple margins. A mid-2025 dip in PTA prices led to diminished earnings for Chinese mills, falling short of their five-year average. Concurrently, geopolitical tensions curtailed Gulf naphtha exports, prompting Asian buyers to procure European cargoes at a premium. Furthermore, when price spreads tighten, smaller mills in India and Indonesia scale back loom utilization, tempering short-term fiber demand.

Transition Toward Bio-Based Technical Textiles Cannibalizing Synthetics

From 2016 to 2024, bio-composites derived from flax, hemp, and PLA witnessed robust growth, spurred by OEMs' push to curb lifecycle CO₂ emissions. For instance, flax fabric door panels boast significant mass savings over traditional glass mat versions. Hemp stands out, offering high modulus and strength that competes with E-glass, yet at a lighter weight and lower cost. The EU's directive to boost recycled polyester content by 2030 amplifies this momentum, with brands keenly adopting low-carbon narratives. Although bio-based matrices face a heat-deflection ceiling, their potential to substitute in certain applications might slightly temper the industrial fabric market's growth rate during the forecast period of 2026-2031.

Segment Analysis

By Fiber Type: Specialty Aramid Accelerates While Polyester Anchors Volume

Aramid is projected to expand at a CAGR of 5.89% through the forecast period of 2026-2031, driven by its high tensile strength and decomposition thresholds. These characteristics not only meet the NFPA 2112 standards for flash-fire apparel but also serve as a substitute for steel-cord belts. In Chilean copper mines, the adoption of Kevlar belts has led to reduced energy consumption and an extended lifespan, translating to notable savings in total cost-of-ownership. Twaron's lightweight properties are being leveraged to reduce weight in automotive reinforcements and blade trailing edges.

Polyester commands a 39.22% share of the industrial fabric market in 2025, thanks to its competitive pricing and China's strong production capabilities. Polyamide finds its niche in high-modulus applications such as airbags, while fiberglass is utilized for wind-blade shells. Additionally, emerging PEN fibers, known for their high glass-transition points, are carving a space in capacitor-film applications.

By Fabric Construction: Woven Leads Through Non-Crimp Upgrades

In 2025, woven architectures accounted for 45.28% of the industrial fabric market and are projected to grow at a CAGR of 4.21% during the forecast period of 2026-2031. This growth is largely attributed to multiaxial non-crimp fabrics, which not only reduce resin usage but also enhance stiffness. SAERTEX's non-crimp fabrics (NCFs) have become the preferred choice for spar caps, while Continental's Plylon Plus belts, with their rip-resistant dual-twill weaves, boast impressive tensile ratings.

Non-woven fabrics are capturing a significant revenue share, thanks to ISO 8 cleanroom fabrics that play pivotal roles in gigafactory walls and coveralls. Melt-blown polypropylene, the gold standard for surgical masks due to its high sub-micron capture rates, commands a premium over its spunbond counterpart. Knitted textiles, though a smaller market segment, provide stretch benefits for seat covers but lack the tensile strength of woven fabrics.

By Application: Fire-Protective Apparel Overtakes Commodity Segments

Fire-protective apparel is witnessing a 5.14% CAGR during the forecast period of 2026-2031, bolstered by updates from NFPA 2112 and NFPA 1977. These updates now encompass battery-assembly lines, which are vulnerable to thermal-runaway flames reaching extreme temperatures. Nomex IIIA has distinguished itself by achieving high HTI-24 ratings with a brief after-flame duration and demonstrating resilience through extensive industrial launderings.

Conveyor belts held a 28.09% market share in 2025. However, with the introduction of Kevlar reinforcements, which significantly cut down downtime, the replacement cycle dynamics are evolving. Leading the charge are Continental, Semperit, and ASGCO, providing wide-width conveyor belts with oil-resistant covers, all adhering to FDA regulations. For high-RPM drives, there is a growing reliance on polyamide cords in transmission belts, ensuring commendable efficiency rates.

By End-User Industry: Automotive and Transportation Delivers Highest Growth

The automotive and transportation sectors are on track to grow at a 5.55% CAGR through 2026-2031. This growth is fueled by ambitious goals, including notable reductions in component weight and carbon emissions. In a strategic move, Toray is significantly expanding its carbon fiber production, targeting the needs of crash-zone structures that demand high strength and elongated blades.

The construction sector, buoyed by a steady demand for geotextiles, held a 25.46% market share in 2025. Major projects, spanning highways, levees, and railways, have reported enhanced performance metrics when advanced fabrics supplanted traditional granular fills. The mining, oil and gas, and energy sectors are major players in this demand landscape. Highlighting the industry's technical requirements, Saudi Aramco showcases aramid hoses designed for high temperatures, while GE Vernova presents large fiber blades.

Geography Analysis

In 2025, the Asia-Pacific region commanded a dominant 41.14% share of the industrial fabric market revenue, with projections indicating a rise at a 5.67% CAGR through the forecast period of 2026-2031. China's polyester-staple capacity, a linchpin in the global supply chain, firmly anchors the region's cost curves. Bolstering feedstock security, six gigascale projects came online in 2025. Companies such as Hengyi, Tongkun, and Sinopec are diversifying their portfolios, ramping up production lines for airbags and cleanroom non-wovens, highlighting the region's pivot towards specialty products.

North America and Europe, while absorbing a significant portion of the demand, wield considerable strategic importance. This is underscored by the fact that battery gigafactories in Virginia, Michigan, and Germany, which require ISO 8 cleanrooms, consume a substantial volume of non-woven panels. DuPont's Tyvek 400 Dual TG coveralls, adhering to EN 1149-5 antistatic codes, are tailored for lithium-handling areas. Volkswagen's Salzgitter plant, which is augmenting cell capacity, also has a pronounced demand for dry-room fabrics.

In South America, driven by the mining activities in Chile and Peru, there is a notable revenue contribution. These mines, leveraging Kevlar belts for reduced energy consumption and extended lifespan, underscore the trend. In the Middle-East and Africa, where the market sees significant contributions, Saudi Aramco and ADNOC have made specifications for aramid hoses and offshore geotextiles, emphasizing UV stability. Moreover, South African platinum and coal pits have an annual demand for belts that surpasses millions, further driving the consumption of woven polyester.

Competitive Landscape

The industrial fabric market is moderately consolidated. A discernible trend of vertical integration is emerging, with fiber majors venturing into finishing and coating processes to capture added margins. Toray's ambitious carbon-tow initiative in South Carolina, set to amplify global capacity by 2030, is targeting structural applications in both the automotive and wind sectors. DuPont's strategic expansions in Tennessee, particularly at Cooper River for Kevlar and the Tyvek HomeWrap line, underscore a pronounced focus on protective apparel and building envelopes. Freudenberg's microfilament setup in Germany, serving medical filtration and battery separators, highlights the industry's gravitation towards premium fabrics in regions demanding high skill.

With recycled-content mandates looming in China and the EU, companies like Hengyi and Indorama, bolstered by their chemical-recycling assets, are poised to navigate the complexities of rising feedstock challenges. Cleanroom non-wovens emerge as a golden opportunity, with Ahlstrom and Freudenberg reaping benefits through their dedicated ISO 8 lines. New players like Bcomp, supplying ampliTex flax fabrics to automotive stalwarts Volvo and Porsche, and Microporous, making a significant investment in Virginia for battery separators and cleanroom media, are reshaping the industry's dynamics. The competitive landscape is heating up, driven by technological strides in plasma surface treatment, nano-scale coatings, and digital weaving.

Industrial Fabric Industry Leaders

Ahlstrom

Albany International Corp.

Amcor

Continental AG

DuPont

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Kornit Digital launched the Presto MAX PLUS roll-to-roll printing system at the Texprocess 2026 event in Frankfurt. The system expanded digital textile production into demanding industrial applications, including footwear uppers, automotive interiors, military camouflage, and high-performance sportswear.

- April 2026: The LYCRA Company introduced its new LYCRA ANTISTATIC fiber at Techtextil 2026. The fiber is designed for professional workwear and protective apparel (PPE) in industries such as petrochemicals, electronics, pharmaceuticals, medicine, and aerospace, where static electricity presented significant challenges.

Global Industrial Fabric Market Report Scope

Industrial fabrics are durable, engineered textiles designed to withstand rigorous commercial and industrial environments. Unlike standard fabrics used in consumer goods, these materials are developed to emphasize protection, containment, and long-term durability over aesthetics. Industrial fabrics are specifically created for use in products, processes, or services where functionality is the primary requirement. They are employed by non-apparel industry professionals for demanding and high-performance applications.

The industrial fabrics market is segmented by fiber type, fabric construction, application, end-user industry, and geography. By fiber type, the market is segmented into fiberglass yarn, polyamide, polyester, aramid, nylon, and other fiber types. By fabric construction, the market is segmented into woven, non-woven, and knitted. By application, the market is segmented into automotive interior trim, conveyor belts, transmission belts, fire protective apparel, and other application. By end-user industry, the market is segmented into automotive and transportation, mining and material handling, oil and gas, construction, food processing, energy, Healthcare and Hygiene, and other end-user industries. The report also covers the market size and forecasts for industrial fabric in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Fiberglass yarn |

| Polyamide |

| Polyester |

| Aramid |

| Nylon |

| Other Fiber Types (Rayon, PEN) |

| Woven |

| Non-woven |

| Knitted |

| Automotive Interior Trim |

| Conveyor Belts |

| Transmission Belts |

| Fire Protective Apparel |

| Other Application (Industrial Filtration, etc.) |

| Automotive and Transportation |

| Mining and Material Handling |

| Oil and Gas |

| Construction |

| Food Processing |

| Energy (Wind and Solar) |

| Healthcare and Hygiene |

| Other End-User Industries (Agriculture, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Fiber Type | Fiberglass yarn | |

| Polyamide | ||

| Polyester | ||

| Aramid | ||

| Nylon | ||

| Other Fiber Types (Rayon, PEN) | ||

| By Fabric Construction | Woven | |

| Non-woven | ||

| Knitted | ||

| By Application | Automotive Interior Trim | |

| Conveyor Belts | ||

| Transmission Belts | ||

| Fire Protective Apparel | ||

| Other Application (Industrial Filtration, etc.) | ||

| By End-User Industry | Automotive and Transportation | |

| Mining and Material Handling | ||

| Oil and Gas | ||

| Construction | ||

| Food Processing | ||

| Energy (Wind and Solar) | ||

| Healthcare and Hygiene | ||

| Other End-User Industries (Agriculture, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for industrial fabrics be by 2031?

The industrial fabric market size stands at USD 157.72 billion in 2026, and it is projected to reach USD 183.38 billion by 2031 at a 3.06% CAGR.

Which fiber type is growing fastest?

Aramid registers the strongest 2026-2031 growth at 5.89% as safety and lightweighting standards tighten.

Why are cleanroom non-wovens a high-margin niche?

ISO 8 gigafactories specify non-wovens priced USD 18-25/m²-five-to-ten times spunbond rates-driving premium revenue in North America and Europe.

What share does Asia-Pacific hold today?

Asia-Pacific accounts for 41.14% of 2025 revenue and is on track for a 5.67% CAGR to 2031.

How are conveyor belts evolving?

Kevlar and self-healing chemistries are extending belt life 40-60%, reducing downtime, and shifting value from replacement to engineered solutions.

Page last updated on: