India Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

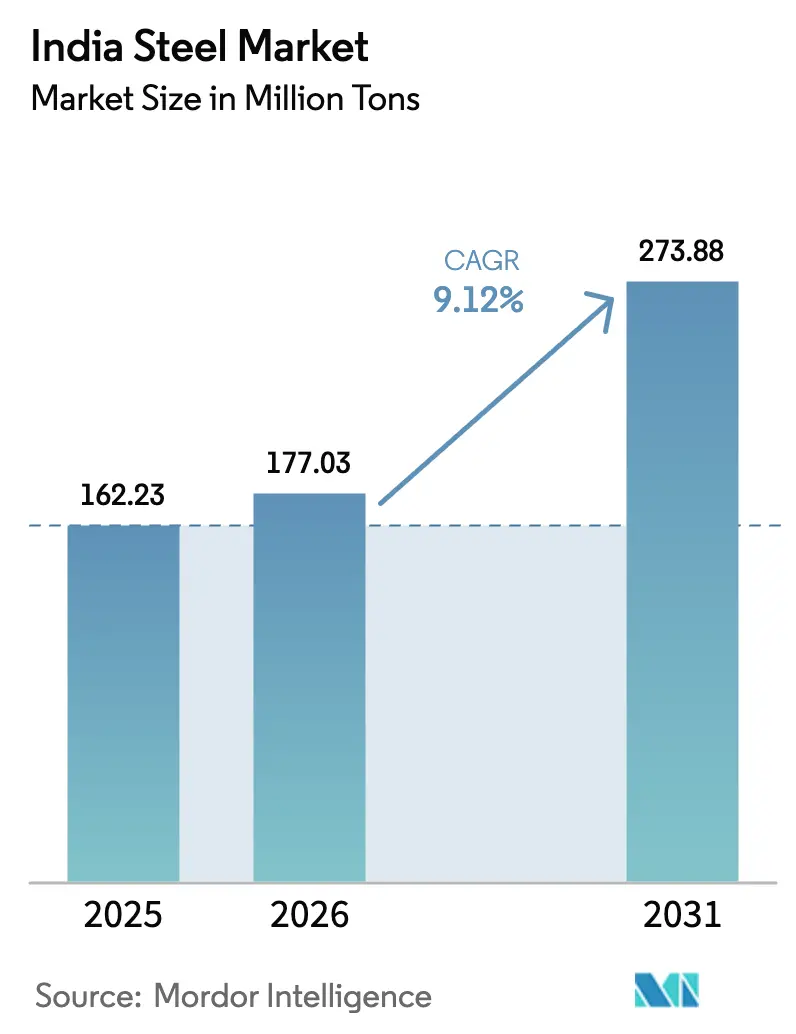

| Base Year Market Size (2025) | 162.23 Million tons |

| Market Volume (2026) | 177.03 Million tons |

| Market Volume (2031) | 273.88 Million tons |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

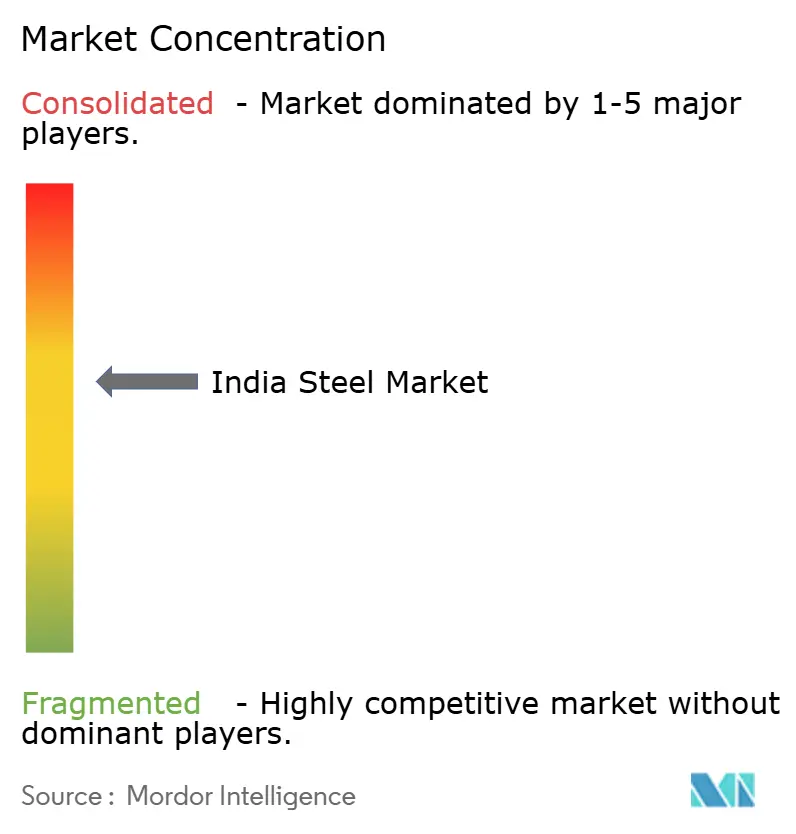

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

India Steel Market Analysis by ���ϲ�����

The India Steel Market size is expected to grow from 162.23 million tons in 2025 to 177.03 million tons in 2026 and is forecast to reach 273.88 million tons by 2031 at a 9.12% CAGR over 2026-2031. In 2025, India stood out as the sole top-10 producer to achieve a double-digit volume growth. In contrast, production in China, Japan, and the European Union either stagnated or declined. This sustained momentum can be attributed to three significant factors. Firstly, the Production Linked Incentive (PLI) scheme for specialty steel has catalyzed private commitments. However, by December 2025, less than half of the sanctioned projects had commenced, leading to a deferred-capacity wave that is expected to uphold pricing discipline until 2027. Secondly, integrated mills located in Odisha, Jharkhand, and Chhattisgarh have gained a competitive edge in landed costs. This advantage stems from securing long-term iron-ore leases under the revised Mines and Minerals Act. As a result, these mills, despite concerns over carbon intensity, managed to maintain a significant market share in 2025. Lastly, the National Infrastructure Pipeline's ambitious outlay has set a reliable demand baseline for structural sections and rebar. This is further bolstered by heightened demand for high-tensile products, driven by metro-rail initiatives in Tier-2 cities and the second phase of the Dedicated Freight Corridor.

Key Report Takeaways

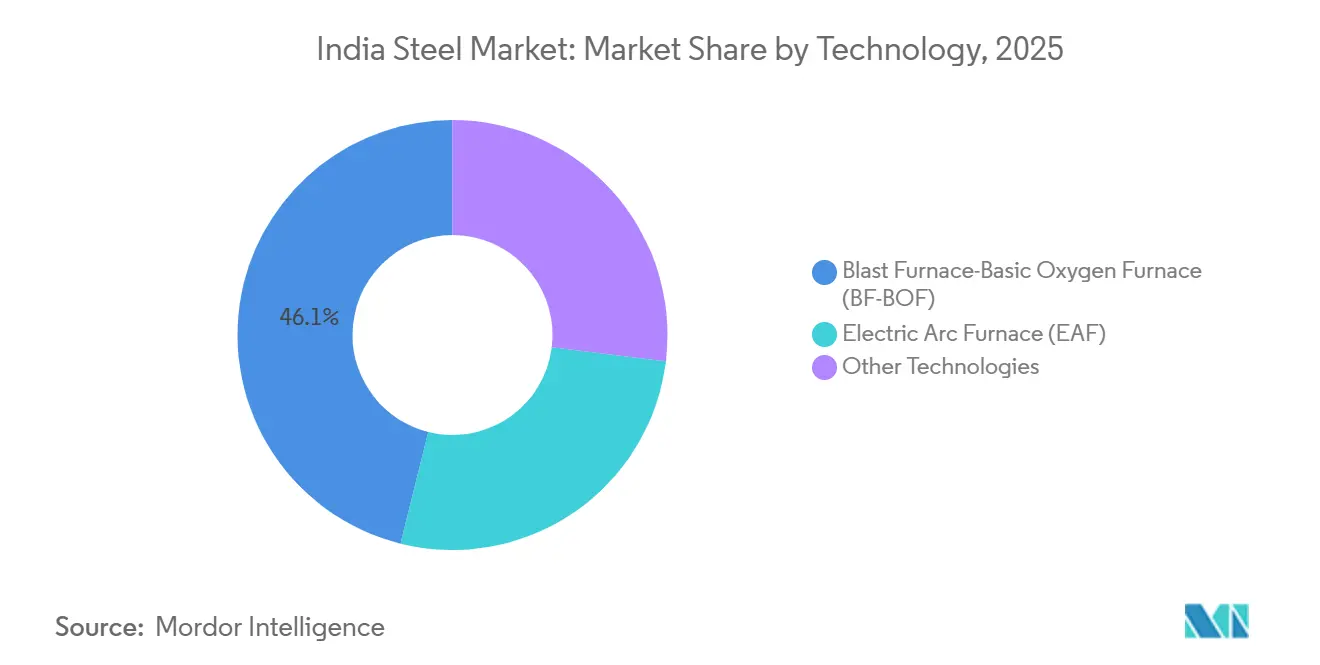

- By technology, Blast Furnace–Basic Oxygen Furnace routes held 46.12% of 2025 output and are forecast to grow at an 8.77% CAGR through 2031.

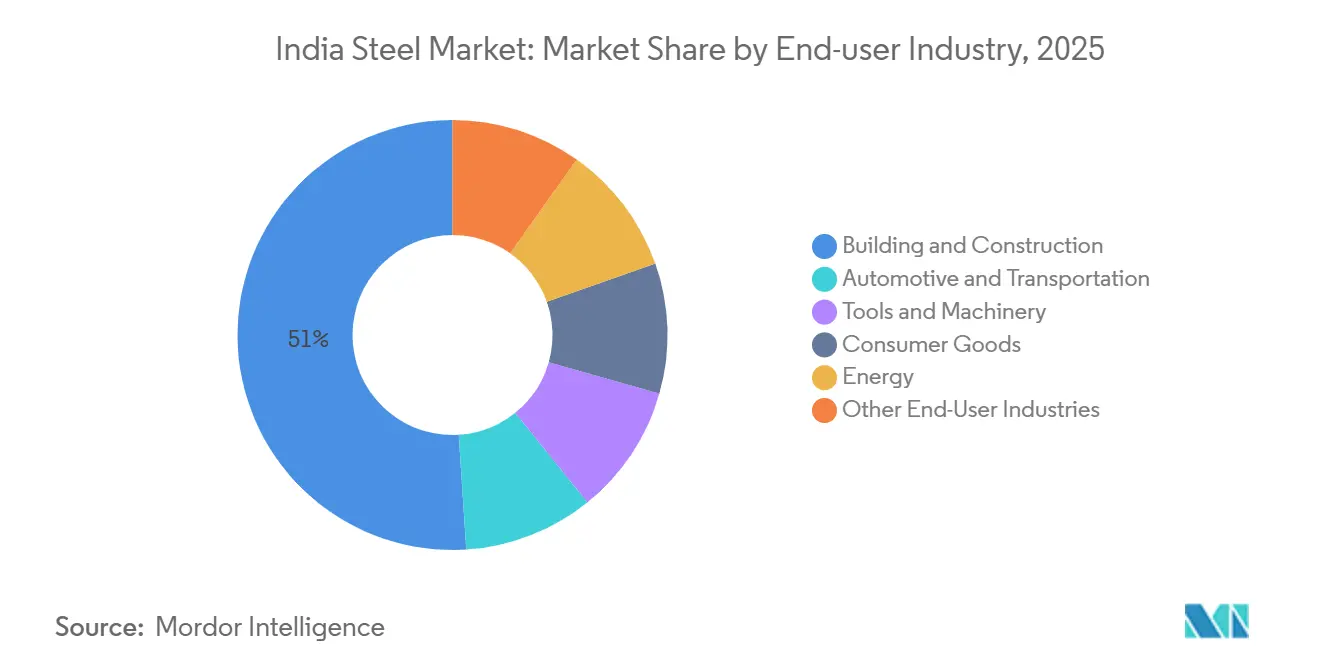

- By end-user, building and construction commanded 51.02% revenue share in 2025 and is projected to rise at a 9.84% CAGR, outpacing the India steel market average.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Steel Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PLI scheme catalyzing specialty-steel investment | +1.2% | Gujarat, Odisha, Karnataka | Medium term (2-4 years) |

| Domestic and foreign CAPEX surge | +1.8% | Odisha, Jharkhand, Chhattisgarh, Karnataka, Maharashtra | Long term (≥ 4 years) |

| Large infrastructure pipeline | +2.1% | National, early impact in Uttar Pradesh, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Auto-OEM shift to AHSS and EV grades | +1.0% | Gujarat, Maharashtra, Tamil Nadu, Karnataka | Short term (≤ 2 years) |

| Hydrogen-DRI pilots and scrap push | +0.7% | Odisha, Jharkhand, Gujarat | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Strong Policy Support Through the PLI Scheme for Specialty Steel

Despite three successive PLI tranches allocating significant funding for specialty capacity to be completed by 2027, only a portion had secured financial closure by December 2025. Early movers who commission coated, electrical, or alloy lines before mid-2027 can lock in an incentive for five years, translating to a substantial subsidy on production costs. The framework favors brownfield expansions, as existing integrated mills can leverage shared captive power and logistics, reducing lead times by up to 18 months. In a strategic move, automotive OEMs are collaborating with steelmakers to co-invest in domestic coating lines, a decision poised to shift a significant portion of annual demand from imports by 2028.

Surge in Domestic and Foreign CAPEX for Capacity Expansion

Between January 2024 and December 2025, JSW Steel and Tata Steel spearheaded a surge in announced additions. JSW Steel's ambitious program spans across Vijayanagar, Dolvi, and Odisha. Meanwhile, Tata Steel is investing in a Phase-II expansion at Kalinganagar. In FY25, foreign direct investment saw a significant leap. This uptick was largely driven by ArcelorMittal's increased stake in AM/NS India and Posco's strengthened technical collaboration with JSW. The mineral-rich eastern states enjoy a freight advantage when catering to northern demand centers. However, this advantage might diminish if the eastern segment of the Dedicated Freight Corridor implements a reduction in rail tariffs by 2027.

Large Infrastructure Pipeline Driving Long-Cycle Demand

The National Infrastructure Pipeline allocates significant funds through 2030, with highways, metro rail, and housing absorbing a major share. Bharatmala Phase I consumed a substantial amount of steel, and Phase II is poised to need higher annual steel requirements from 2027 as elevated corridors employ more steel per kilometer. The Pradhan Mantri Awas Yojana (Urban) 2.0 targets a large number of dwellings by 2029, implying incremental steel that must meet revised seismic codes mandating higher rebar density in high-risk zones[1]Bureau of Indian Standards, “IS:2062 Structural Steel Standards,” bis.gov.in .

Auto-OEM Pivot to High-Strength and EV-Grade Steels

In FY25, demand for steel in passenger vehicles increased significantly. As OEMs pursue the 2027 CAFE norms, Advanced High-Strength Steels (greater than or equal to 980 MPa) now constitute a notable portion of the mix. The domestic supply remains constrained. Despite Tata Steel launching an AHSS line and JSW introducing a facility in 2024, these additions fall short of bridging the import gap. In 2025, with EV production rising, the industry turned to battery tray steels. Currently, only Tata Steel and AM/NS India can supply these steels at scale.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Per-capita steel consumption still below global average | -0.4% | National, with acute gaps in rural and eastern regions | Long term (≥ 4 years) |

| Volatile raw-material and energy costs | -0.7% | National, with higher exposure for coastal integrated mills | Short term (≤ 2 years) |

| Slow domestic scrap-collection ecosystem | -0.5% | National, with infrastructure deficits in Uttar Pradesh, Bihar, Madhya Pradesh | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Per-Capita Steel Consumption Still Below the Global Average

In the first eight months of FY26, domestic consumption remained significantly below the global average and the levels typical of developed nations[2]Indian Steel Association, “Steel Industry Yearbook 2025,” indiansteel.in . To meet the government's target by FY31, consumption must grow annually, and real GDP needs to expand at a steady rate. Both of these thresholds are susceptible to downturns in the credit cycle. Adding to the challenge are regional imbalances: while Odisha, Jharkhand, and Chhattisgarh account for over half of the production, they only consume a small portion locally. This discrepancy forces mills to incur additional freight costs to deliver to customers in the western and southern regions.

Volatile Raw-Material and Energy Costs

In FY25, India imported coking coal at an average landed price that surged due to weather-related disruptions in Australia and logistical challenges in Mozambique, which tightened the supply. For integrated mills, every price hike in coal can shave off EBITDA margins unless these costs are passed on to customers. Following a price revision by Coal India, electricity tariffs for industrial consumers in Odisha and Jharkhand saw an uptick in FY25. This rise in tariffs diminished the savings from solar and wind installations, which require a hefty upfront investment.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Integrated Routes Anchor Volume Despite Carbon Intensity

Blast Furnace–Basic Oxygen Furnace lines produced 46.12% of 2025 output and are on track for 8.77% CAGR through 2031. Tata Steel’s Kalinganagar and JSW’s Vijayanagar plants, operating at high capacity, capitalize on captive ore and coal, achieving a cost advantage over rivals reliant on merchant sources. While Electric Arc Furnace capacity remains modest, it's slated for notable growth, buoyed by the Scrap Policy's boost of available feedstock by 2030. Though technologies like induction furnaces and nascent hydrogen-DRI pilots account for a smaller share of the tonnage, they grapple with challenges as Quality Control Orders phase out non-ISI-compliant steel from public projects.

Forecasts indicate the market for Electric Arc Furnace products in India will expand significantly by 2031. As construction codes increasingly emphasize tighter seismic standards, producers of stainless and micro-alloyed bars, who predominantly utilize scrap, stand to gain the most.

By Basic Form: Crude Steel Universality Masks Downstream Differentiation

In 2025, crude steel production hit significant levels and is expected to register a 7.73% CAGR through 2031. Yield optimization is bridging the divide between crude and finished volumes. An endless-strip line boasts higher yields, surpassing conventional mills. Meanwhile, a twin-roll caster has significantly reduced the melt-to-coil cycle. Odisha and Jharkhand exported semi-finished slabs to western processors, underscoring an inefficiency that may diminish with the launch of new hot-rolling lines in eastern clusters.

By Final Form: Finished Steel Drives End-User Engagement

In 2025, finished steel shipments in India increased, aligning with the market's projected 9.12% CAGR growth. While hot-rolled products commanded a significant market share, their growth lagged, partly due to the rising adoption of aluminum structures in light-industrial constructions. Benefiting from PLI incentives that introduced new capacity, cold-rolled and coated products saw robust growth. Meanwhile, driven by infrastructure projects like highways and metro construction, long products are set to grow steadily.

In 2025, cold-rolled and coated products accounted for a notable portion of the Indian steel market share, with projections suggesting an increase by 2031, highlighting a strategic shift towards automotive and appliance sectors.

By End-User Industry: Construction Dominance Meets Automotive Sophistication

Building and construction absorbed 51.02% of finished steel in 2025 and is pegged for a 9.84% CAGR. This sector is projected to grow steadily, buoyed by the steel-intensive Bharatmala Phase-II and the housing-driven PMAY (Urban) 2.0. The automotive and transportation sectors, which currently make up a significant portion of steel demand, are expected to grow as well. This growth comes even as the intensity of steel used in vehicles is anticipated to decline due to the adoption of Advanced High-Strength Steel (AHSS). Energy projects, particularly solar mounting structures and wind tower wire rods, are set to experience the most rapid growth. This surge aligns with the ambitious renewable capacity target set by the Ministry of New and Renewable Energy.

Geography Analysis

In 2025, Odisha, Jharkhand, and Chhattisgarh collectively produced crude steel, accounting for a significant portion of India's national output. This achievement was bolstered by the fact that these states hold a majority of the country's iron ore reserves. Odisha is set to boost its capacity further by 2028, thanks to new furnaces being commissioned by AM/NS India and JSW. Chhattisgarh is at the forefront of regional growth, driven by NMDC Steel's new facility and Jindal Steel's expansion. In 2025, Western India, anchored by automotive hubs in Pune and Ahmedabad, accounted for a notable share of the national demand. Southern states, while consuming a substantial amount, still found themselves importing coated products, a necessity due to their limited local galvanizing capacity. Meanwhile, demand centers in the north and east collectively utilized significant volumes but faced freight penalties when sourcing from eastern mills. However, with the eastern arm of the Dedicated Freight Corridor projected to come online by 2027, it's anticipated to reduce those freight costs. This development could reroute a considerable amount of annual flows inland, significantly reshaping the competitive landscape.

Competitive Landscape

The market is moderately consolidated. Integrated leaders are boosting their coated, electrical, and AHSS lines, achieving impressive EBITDA margins. Meanwhile, Electric Arc Furnace players are honing in on specialty long products, capitalizing on the upcoming scrap mandate for more affordable feedstock. Strategic technology partnerships are proving beneficial: JSW's collaboration focuses on electrical steels, while Tata's partnership centers on hydrogen-DRI, positioning these incumbents advantageously in the low-carbon, high-value market segments. Disruptors such as NMDC Steel, bolstered by their own ore and a newly established coastal terminal, are setting their sights on underpricing seasoned exporters in Southeast Asia. Such a downturn historically ignites price competition, often trimming margins—a challenge that tends to benefit mills with their own mines and integrated logistics.

India Steel Industry Leaders

Tata Steel

JSW Steel Limited

Steel Authority of India Limited (SAIL)

AM/NS India

Jindal Steel & Power Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: JSW Group announced a INR 1 lakh crore (USD 12 billion) investment to construct a steel plant in Gadchiroli, Maharashtra, with 25 million tonnes annual capacity.

- November 2024: ArcelorMittal Nippon Steel India announced an INR 1.5 lakh crore (~USD 18 billion) integrated plant at Anakapalle, Andhra Pradesh, with a 24 million ton capacity and 70,000 job creation.

India Steel Market Report Scope

Steel is an iron alloy with additional carbon to increase its strength and fracture resistance. It is utilized in structures, infrastructure, tools, ships, trains, cars, machinery, electrical appliances, weaponry, and rockets.

The India steel market is segmented by technology, basic form, final form, and end-user industry. By technology, the market is segmented into Blast Furnace-Basic Oxygen Furnace (BF-BOF), Electric Arc Furnace (EAF), and Other Technologies. By basic form, the market is segmented into Crude Steel. By final form, the market is segmented into Finished Steel. By end-user industry, the market is segmented into Automotive and Transportation, Building and Construction, Tools and Machinery, Consumer Goods, Energy, and Other End-User Industries. For each segment, market size and forecasts are based on volume (Tons).

| Blast Furnace-Basic Oxygen Furnace (BF-BOF) |

| Electric Arc Furnace (EAF) |

| Other Technologies |

| Crude Steel |

| Finished Steel |

| Automotive and Transportation |

| Building and Construction |

| Tools and Machinery |

| Consumer Goods |

| Energy |

| Other End-User Industries |

| By Technology | Blast Furnace-Basic Oxygen Furnace (BF-BOF) |

| Electric Arc Furnace (EAF) | |

| Other Technologies | |

| By Basic Form | Crude Steel |

| By Final Form | Finished Steel |

| By End-user Industry | Automotive and Transportation |

| Building and Construction | |

| Tools and Machinery | |

| Consumer Goods | |

| Energy | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the projected volume of the India steel market by 2031?

Demand is expected to reach 273.88 million tons by 2031, growing at a 9.12% CAGR, from 177.03 million tons in 2026.

Which segment will contribute the fastest growth in final form demand?

Finished steel products are forecast to expand at a 9.12% CAGR to 2031, outpacing other finished categories.

How will infrastructure spending influence steel consumption?

Bharatmala Phase-II and PMAY (Urban) 2.0 alone could create 30-plus million tons of incremental annual demand once fully mobilized after 2027.

What role does scrap play in India’s decarbonization roadmap?

The draft Scrap Policy aims to double domestic ferrous-scrap availability by 2030, lifting Electric Arc Furnace output and cutting carbon intensity.

Which region is set for the highest production growth?

Chhattisgarh is growing, helped by NMDC Steel’s Nagarnar plant and Jindal Steel’s Angul expansion.

Page last updated on: