Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

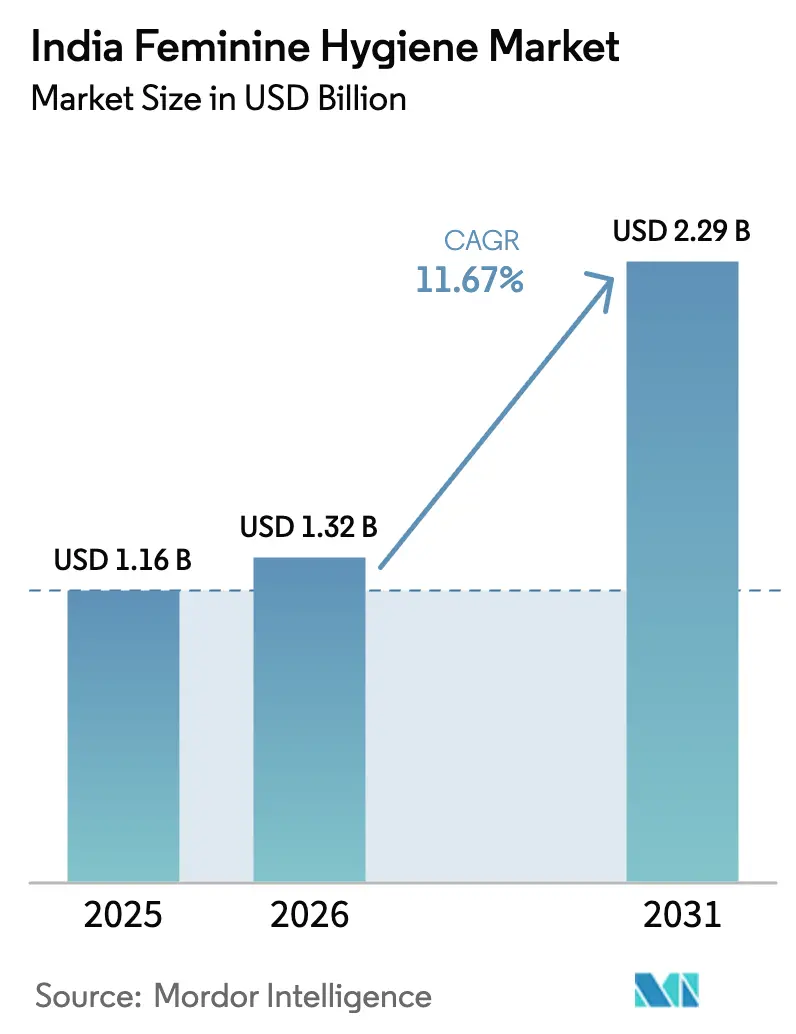

| Base Year Market Size (2025) | USD 1.16 Billion |

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 11.67% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

India Feminine Hygiene Market Analysis by ���ϲ�����

The India feminine hygiene products market was valued at USD 1.16 billion in 2025 and estimated to grow from USD 1.32 billion in 2026 to reach USD 2.29 billion by 2031, registering a compound annual growth rate (CAGR) of 11.67% during the forecast period (2026-2031). This growth is driven by several factors. Policy initiatives aimed at improving menstrual hygiene awareness and accessibility have played a significant role in expanding the market. Additionally, there is a growing consumer preference for organic and biodegradable materials, reflecting increased environmental consciousness and health awareness. Furthermore, the rapid digitization of distribution channels has enabled easier access to feminine hygiene products, bypassing traditional retail outlets and catering to a broader consumer base.

Key Report Takeaways

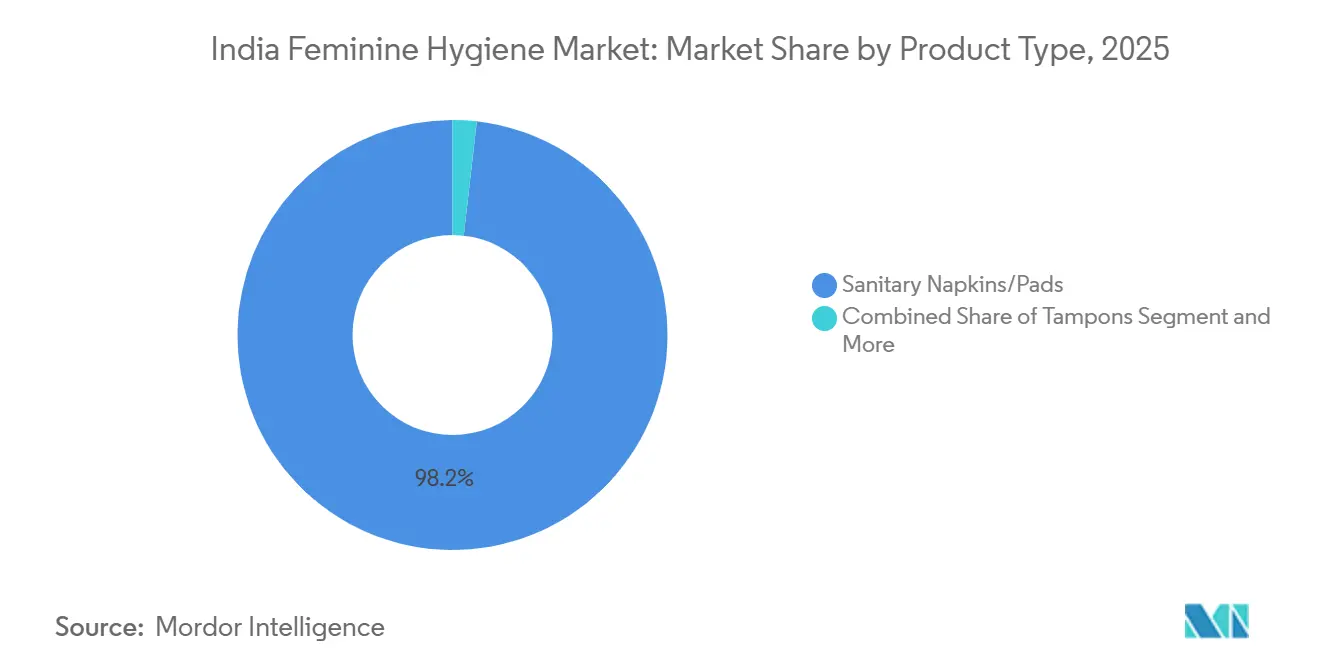

- By product type, sanitary napkins/pads held 98.21% of the India feminine hygiene products market share in 2025 and are expected to grow at the fastest CAGR of 11.57% through 2031.

- By product category, disposable products captured 91.21% of the market share in 2025; reusable options are projected to expand at a 12.07% CAGR over 2026-2031.

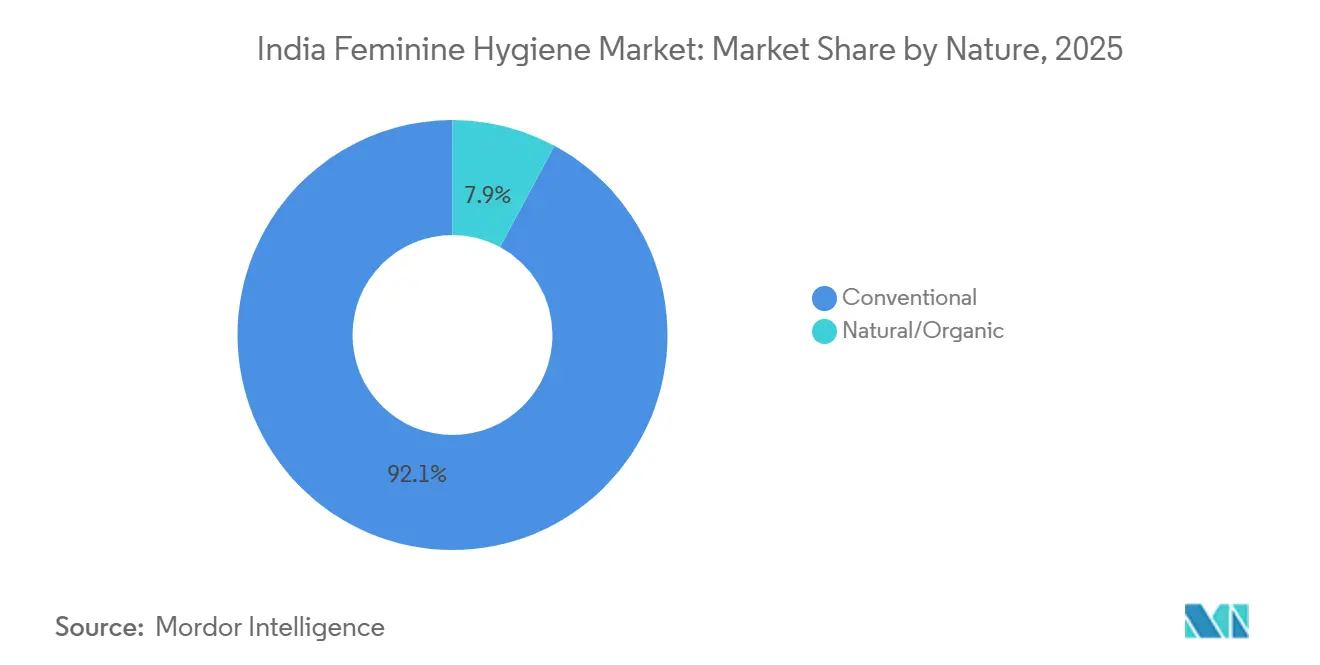

- By nature, conventional offerings accounted for 92.14% of 2025 revenue, whereas natural/organic formats are poised to grow at a 12.12% CAGR during the forecast period.

- By distribution channel, drug stores/pharmacies accounted for 37.31% of 2025 sales, yet online retail is expected to post an 11.85% CAGR through 2031.

- By region, North India contributed 38.21% of the 2025 value; East India is set to register the quickest 12.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Feminine Hygiene Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for organic, chemical-free, and hypoallergenic menstrual products | +2.5% | Urban centers across North, West, and South India, with early adoption in metros like Mumbai, Delhi, Bengaluru | Medium term (2-4 years) |

| Growing awareness around menstrual health, hygiene, and safe period practices | + 3.0% | National, with stronger momentum in South India (Tamil Nadu, Kerala) and urban pockets of North India | Long term (≥ 4 years) |

| Supportive government initiatives and menstrual equity programs improving product accessibility | +3.5% | Rural and semi-urban areas across all regions, particularly Uttar Pradesh, Bihar, Madhya Pradesh, and Odisha | Short term (≤ 2 years) |

| Increasing shift toward sustainable, biodegradable, and eco-friendly menstrual solutions | + 2.8% | Urban India with spillover to tier-2 cities in Maharashtra, Karnataka, and Gujarat | Medium term (2-4 years) |

| Positive cultural transformation supported by education and awareness campaigns | + 2.0% | National, with accelerated impact in states with active NGO presence and school-based MHM programs | Long term (≥ 4 years) |

| Expanding focus on women’s health and holistic wellness trends | + 1.5% | Urban and semi-urban India, particularly among working women in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising consumer preference for organic, chemical-free, and hypoallergenic menstrual products

Brands are increasingly adopting organic cotton and bamboo-fiber formulations in response to consumer concerns about rashes and irritation, which affect approximately 70% of menstruators. This shift reflects a growing willingness among consumers to pay premium prices for chemical-free alternatives. In May 2025, Kenvue introduced Stayfree Tampons with Dynamic Fit technology and a SilkTouch cover, aimed at urban millennials who value comfort and hypoallergenic materials. Saathi's biodegradable pads, made from banana and bamboo fibers, emphasize sustainability as accessible rather than exclusive. The product is BIS IS 5405:2019 certified, addressing safety concerns effectively. This segment expansion is compressing the dominance of synthetic materials, which historically offered lower unit costs but are now perceived as health liabilities. The shift is most pronounced in urban centers where disposable income and health literacy converge, creating a bifurcated market where incumbents must defend volume share in rural areas while investing in premium organic lines to protect margin in metros.

Growing awareness around menstrual health, hygiene, and safe period practices

The Union Health Ministry's approval of a national Menstrual Hygiene Policy for School-Going Girls in November 2024 institutionalizes awareness campaigns that previously relied on fragmented NGO efforts[1]Source: Ministry of Health and Family Welfare, “Menstrual Hygiene Policy for School-Going Girls,” pib.gov.in. Moreover, the Swasth Nari, Sashakt Parivar Abhiyaan conducted menstrual hygiene awareness sessions in Ladakh[2]Source: Ministry of Health and Family Welfare, “Swasth Nari Sashakt Parivar Abhiyaan Registers Massive Participation Across the Country,” pib.gov.in. Awareness and education are key drivers in the adoption of hygienic methods, playing a significant role in market penetration. However, their impact varies across regions, with some areas exhibiting higher adoption rates while others experience relatively low usage. This disparity underscores the need for awareness campaigns to be supplemented with affordability-focused initiatives to ensure that increased knowledge leads to actual purchasing behavior, especially in economically disadvantaged regions.

Supportive government initiatives and menstrual equity programs improving product accessibility

The Pradhan Mantri Bhartiya Janaushadhi Pariyojana achieved cumulative sales of 3.43 crore Suvidha pads at Rs. 1 per unit as of June 2020, effectively creating a parallel distribution network that bypasses traditional retail markups[3]Source: Ministry of Health and Family Welfare, “Sanitary Napkins available for Rs. 1/- per pad at Pradhan Mantri Bhartiya Janaushadhi Kendras,” pib.gov.in. These initiatives help narrow the rural-urban adoption gap by subsidizing costs, making hygienic products accessible to the poorest quintile, where period poverty affects over 75% of the population. Period poverty refers to the lack of access to sanitary products, menstrual hygiene education, and adequate sanitation facilities, which disproportionately impacts women in low-income groups. By offering Suvidha pads at a highly subsidized price, the program addresses affordability issues and promotes menstrual hygiene awareness. This development compels market incumbents to focus on quality and brand differentiation, as government programs set a price floor that reduces margins in the mass market segment.

Increasing shift toward sustainable, biodegradable, and eco-friendly menstrual solutions

India generates approximately 112,800 tonnes of sanitary waste annually from an estimated 12 billion pads, creating environmental pressure that regulators and consumers are beginning to address. The draft Solid Waste Management Rules proposed in 2024 mandate weekly collection of sanitary waste as a distinct stream and impose penalties for non-compliance, scheduled to take effect in October 2025. Biodegradable compostable materials are projected to grow at 14.42% CAGR through 2031, the fastest among material segments, as brands like Saathi claim 6-month degradation timelines and plastic-free packaging to appeal to environmentally conscious consumers. Reusable products, menstrual cups, cloth pads, and period underwear offer lifetime costs that are 9-19% of disposable alternatives, positioning sustainability as an economic rather than purely ethical choice for lower-income segments. Compliance with BIS IS 5405:2019 certification is emerging as a competitive threshold, as brands must demonstrate safety and biodegradability claims to avoid regulatory penalties and consumer backlash.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent social stigma and cultural taboos surrounding menstruation limiting adoption | -2.5% | National, with acute impact in rural areas and conservative pockets of North and Central India | Long term (≥ 4 years) |

| Limited awareness and inadequate education in rural and underserved regions | -2.0% | Rural India, particularly Uttar Pradesh, Bihar, Madhya Pradesh, Assam, and Chhattisgarh | Medium term (2-4 years) |

| Higher product costs coupled with strong price sensitivity among consumers | -1.8% | Rural and low-income urban households across all regions, with highest impact in poorest wealth quintiles | Short term (≤ 2 years) |

| Environmental and waste management concerns related to product disposal | -1.0% | Urban and semi-urban areas with inadequate waste management infrastructure | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Persistent social stigma and cultural taboos surrounding menstruation limiting adoption

Many menstruating women face multiple restrictions during their periods, such as being prohibited from entering temples or kitchens, and many also experience shame when discussing menstruation openly. Religious restrictions are widespread, and feelings of uncleanliness are common, creating psychological barriers that suppress demand even when products are affordable and accessible. These taboos influence purchasing behavior, as women often avoid in-store purchases due to embarrassment. This has contributed to the increasing preference for online retail channels that offer discreet home delivery. The strategic challenge is that awareness campaigns alone cannot dismantle deeply embedded cultural norms; brands must instead design distribution models that minimize social friction, such as subscription services and quick-commerce platforms that eliminate the need for face-to-face transactions.

Limited awareness and inadequate education in rural and underserved regions

Rural adolescent women are less likely to rely solely on hygienic menstrual methods compared to their urban counterparts, with many districts continuing to report low usage of modern menstrual products. State-level disparities are prominent, with some regions experiencing a high prevalence of period poverty, while others report significantly lower levels. Wealth and education play a critical role, as women from poorer households and those without schooling are substantially more likely to experience period poverty. This creates a cycle where low education limits awareness, which subsequently reduces demand, making it economically unviable for brands to invest in rural distribution infrastructure. Government initiatives partially address this issue by subsidizing unit costs; however, the last-mile challenge remains significant in districts where even Rs. 6 per pack is unaffordable for daily-wage households.

Segment Analysis

By Product Type: Pads Dominate, Tampons Emerge

Sanitary napkins/pads commanded 98.21% market share in 2025 and are projected to grow at 11.57% CAGR through 2031, reflecting entrenched consumer familiarity and the product format's compatibility with both urban and rural distribution networks. The overwhelming dominance of pads creates both inertia and opportunity. Incumbents benefit from established supply chains and consumer trust, but the format's association with bulk and disposal challenges opens space for disruptors offering thinner, biodegradable, or reusable alternatives. The emergence of the tampon category, although currently limited in size, provides an opportunity for international players to introduce internal protection formats that offer premium pricing and higher per-unit margins.

Kenvue's launch of Stayfree Tampons in May 2025 marks a strategic bet that urban millennials will adopt internal protection despite cultural hesitancy, leveraging Dynamic Fit technology and SilkTouch cover to differentiate on comfort. Tampons remain a niche segment, constrained by misconceptions about virginity and internal use, yet the format offers higher margin potential and appeals to working women seeking discretion and mobility. Panty liners serve a complementary role for light-flow days and daily freshness, while other product types, including menstrual cups and period underwear, are gaining traction among sustainability-focused consumers who prioritize reusability over convenience.

By Product Category: Disposables Retain Majority as Reusables Gain Visibility

Disposable products dominated the Indian feminine hygiene products market, accounting for 91.21% of total market share in 2025. This category includes items like sanitary pads, panty liners, tampons, and other single-use products. These products are widely preferred due to their convenience, affordability, and easy availability. The strong distribution networks in both urban and rural areas have made these products accessible to a large population. Additionally, government initiatives aimed at raising awareness about menstrual hygiene have played a significant role in boosting their adoption. Innovations such as ultra-thin pads, organic cotton options, and improved absorbency are further driving demand in this segment.

On the other hand, reusable feminine hygiene products are anticipated to grow at a CAGR of 12.07% during the forecast period of 2026–2031. This segment includes menstrual cups, reusable cloth pads, and period panties, which are becoming increasingly popular among environmentally conscious consumers. These products offer benefits such as long-term cost savings and a reduced environmental footprint, making them an attractive option. Awareness campaigns on social media and educational efforts by health organizations are helping to promote sustainable menstruation practices. These initiatives are particularly effective in encouraging younger and urban consumers to adopt reusable alternatives, contributing to the segment's growth.

By Nature: Conventional Retain Majority as Organic Gain Growth

Conventional feminine hygiene products led the India feminine hygiene products market, accounting for 92.14% of total revenue in 2025. This category includes widely used products such as sanitary pads, tampons, and panty liners made from synthetic absorbent materials. These products are popular due to their affordability, easy availability, and strong presence in retail stores across the country. Additionally, government initiatives promoting menstrual hygiene and extensive marketing campaigns by major brands have further boosted their adoption in both urban and rural areas. Their convenience and familiarity make them the preferred choice for most consumers.

On the other hand, natural and organic feminine hygiene products are expected to grow significantly, with a projected CAGR of 12.12% during the forecast period. This segment includes eco-friendly options like organic cotton pads, biodegradable tampons, and chemical-free menstrual care products. These alternatives are gaining popularity among consumers who are increasingly concerned about health, skin sensitivity, and environmental sustainability. The shift toward these products is driven by growing awareness of their benefits, such as reduced exposure to harmful chemicals and lower environmental impact. Furthermore, the rising availability of these products through online platforms and niche wellness brands is making them more accessible, particularly to urban and health-conscious consumers.

By Distribution Channel: Digital Commerce Broadens Private Purchasing

Drug stores/pharmacies captured 37.31% of the distribution share in 2025, serving as trusted intermediaries where consumers can seek advice and purchase discreetly, yet online retail stores are surging at 11.85% CAGR through 2031, propelled by quick-commerce platforms that compress delivery times to under 15 minutes in tier-1 cities. Quick-commerce platforms like Blinkit, Zepto, and Swiggy Instamart now account for a significant share of FMCG e-commerce sales for several companies, eliminating the social discomfort of in-store purchases and offering subscription models that ensure continuous supply.

Supermarkets/hypermarkets function as secondary distribution channels, offering bulk-purchase discounts that attract price-sensitive households. Other distribution channels cater to niche market segments. Pharmacies maintain structural advantages in rural areas where internet penetration and digital payment infrastructure are limited. However, their market share is declining in urban areas as e-commerce platforms expand through dark stores and last-mile logistics. The key shift is that online retail reduces traditional retail markups, compelling pharmacies to compete based on service quality and immediacy rather than price. Brands are now required to adopt dual distribution strategies, collaborating with pharmacies to capture rural demand while investing in digital marketing and quick-commerce fulfillment to protect urban market share from direct-to-consumer startups that bypass traditional intermediaries.

Geography Analysis

North India accounted for 38.21% of the market share in 2025, driven by factors such as population density and higher per-capita income in regions like Delhi NCR, Punjab, and Haryana. However, the region continues to face significant challenges in states such as Uttar Pradesh and Bihar, where period poverty remains prevalent, and many women in several districts lack access to hygienic menstrual products. The Pradhan Mantri Bhartiya Janaushadhi Pariyojana’s initiative to distribute Suvidha pads at highly subsidized rates through thousands of Janaushadhi Kendras is contributing to reducing the urban-rural disparity. Despite these efforts, the wealth quintile effect remains a critical issue, with women in the poorest quintile disproportionately affected by period poverty, which limits demand even when products are subsidized.

East India is projected to grow at 12.86% CAGR through 2031, the fastest among geographic segments, driven by Maharashtra's state-level Asmita scheme and Gujarat's emergence as a manufacturing hub that attracts ancillary investments in packaging and raw-material supply chains. Maharashtra's urban centers, Mumbai and Pune, exhibit high adoption rates and willingness to pay premium prices for organic and biodegradable products, while rural areas benefit from government schemes that subsidize unit costs. The region's growth trajectory reflects a virtuous cycle where manufacturing investments reduce logistics costs, which in turn compress retail prices and expand addressable market size. Quick-commerce platforms are particularly active in West India, with Blinkit, Zepto, and Swiggy Instamart establishing dark stores in Mumbai and Pune.

South India demonstrates the highest adoption rates, with Tamil Nadu leading in the use of hygienic methods. However, growth in the region is slower due to market saturation. The region's maturity presents strategic challenges for existing players, who must now focus on brand differentiation and product innovation rather than increasing penetration. Tamil Nadu's Free Sanitary Napkin Scheme, which distributes products through schools and public health centers, has effectively addressed the addressable market, leaving limited opportunities for volume growth. In response, brands are introducing premium organic and biodegradable product lines targeting environmentally conscious consumers in cities like Bengaluru, Chennai, and Hyderabad, where higher disposable incomes and greater health awareness support premium pricing. Future growth in the region is expected to rely on premiumization and category diversification, such as tampons, menstrual cups, and period underwear, rather than further penetration of the core sanitary napkin segment.

Competitive Landscape

The Indian feminine hygiene market is consolidated, yet the landscape is fragmenting as direct-to-consumer startups leverage e-commerce platforms to bypass traditional retail gatekeepers and capture price-sensitive and sustainability-conscious cohorts. Good Glamm Group's acquisition of Sirona Hygiene for Rs. 450 crore in October 2024 signals that incumbents view inorganic growth as a faster path to capturing niche segments. Sirona's PeeBuddy reached 3 million users and its menstrual cups served 4 million customers, demonstrating that focused product portfolios can achieve scale without the capital intensity of mass-market distribution.

White-space opportunities cluster around reusable products and biodegradable materials. Startups such as Saathi and Azah are addressing this market gap by utilizing agricultural waste, including banana fiber, bamboo, and corn fiber, which are more cost-effective compared to imported synthetic polymers. These companies are promoting sustainability as an accessible option rather than a premium choice. Quick-commerce platforms are emerging as kingmakers, offering instant delivery that eliminates the social discomfort of in-store purchases and subscription models that lock in recurring revenue.

Compliance with BIS IS 5405:2019 certification and the draft Solid Waste Management Rules scheduled for October 2025 will impose quality and environmental thresholds that favor incumbents with regulatory expertise but also create barriers for unorganized players who currently serve rural markets with uncertified products. Moreover, companies are adopting strategies such as localizing supply chains and reducing import dependence, which have become priorities due to fluctuating raw material costs and government initiatives aimed at lowering retail prices.

India Feminine Hygiene Industry Leaders

Procter & Gamble

Kimberly-Clark

Soothe Healthcare

Kenvue Inc.

Unicharm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stayfree has expanded its product portfolio by introducing Stayfree Tampons in partnership with O.B. This launch leverages O.B's global expertise in tampons alongside Stayfree's market presence to meet the evolving menstrual hygiene requirements of Indian women.

- February 2025: Unicharm Corporation announced the completion of its Ahmedabad Plant under Unicharm India Private Limited, its local subsidiary in India. The plant has been operational since February 2025. This facility will serve as the company's third production site in India, enhancing supply stability and enabling the delivery of products and services tailored to local requirements.

- December 2024: Stayfree has collaborated with GoFloRun to promote menstrual health. Through this partnership, Stayfree seeks to empower women and advance efforts to normalize conversations about menstruation.

- October 2024: Good Glamm Group acquired Sirona Hygiene for Rs. 450 crore in an all-cash deal, consolidating its position in the feminine hygiene and intimate care segments.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines India's feminine hygiene market as all disposable and reusable menstrual-care products, sanitary pads, tampons, menstrual cups, panty liners, as well as feminine wipes and intimate washes sold through retail and institutional channels to end consumers.

Scope Exclusions: Adult incontinence products, postpartum diapers, depilatories, and cosmetic intimate perfumes remain outside the model scope.

Segmentation Overview

- By Product Type

- Sanitary Pads/Napkins

- Tampons

- Menstrual Cups

- Panty Liners

- Feminine Wipes and Intimate Washes

- Others (External Intimate Care Products, etc.)

- By Product Category

- Disposable Products

- Reusable Products

- By Nature

- Conventional

- Natural/Organic

- By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacies/Drug Stores

- Online Retail Stores

- Other Distribution Channels

- By Region

- North India

- South India

- East India

- West India

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with product managers at leading pad and cup brands, gynecologists in tier-1 and tier-3 cities, rural health workers, and buyers at pharmacy chains. Their insights clarified adoption barriers, typical retail margins, and expected shifts toward biodegradable variants, ensuring that desk findings were grounded in lived market realities.

Desk Research

We started with publicly available statistics from the Ministry of Health & Family Welfare, National Family Health Survey-6, and the Reserve Bank of India's consumer price data to size the eligible female population, penetration, and average spend. Trade volumes from Volza, import duties published by the Central Board of Indirect Taxes, and state GST receipts helped benchmark formal and gray channel sales. Industry notes from the All India Sanitary Product Manufacturers Association, peer-reviewed articles on menstrual health, and company filings gathered via D&B Hoovers rounded the evidence base. These examples are illustrative, not exhaustive; many other trusted sources informed gap checks and trend validation.

Market-Sizing & Forecasting

A top-down population cohort model converts the menstruating female base into demand pools by applying usage frequency, product mix, and average selling price assumptions. Results are cross-checked with sampled supplier roll-ups and online channel checks to fine-tune totals. Key variables driving the model include female literacy rate, government subsidy scheme coverage, e-commerce share in hygiene, average pad ASP in INR, and shift toward reusable products. Multivariate regression on these indicators underpins the 2025-2030 forecast, while scenario analysis adjusts for currency volatility and subsidy rollouts. Bottom-up gaps, such as informal rural sales, are filled using calibrated uptake ratios drawn from primary fieldwork.

Data Validation & Update Cycle

Outputs pass three tiers of analyst review, variance screens against independent indicators, and follow-up calls where anomalies surface. We refresh every twelve months and trigger mid-cycle updates after material policy or taxation changes, so clients always receive an up-to-date baseline.

Why Mordor's India Feminine Hygiene Baseline Stands Reliable

Published estimates often differ because firms choose dissimilar product baskets, price anchors, and conversion rates.

Key gap drivers include exclusion of reusable items, uneven treatment of online direct-to-consumer volumes, and currency conversions frozen at older exchange rates, which our team updates quarterly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.56 B (2025) | ���ϲ����� | - |

| USD 959.6 M (2024) | Regional Consultancy A | Omits menstrual cups and wipes; conservative penetration assumption |

| USD 1.41 B (2024) | Global Consultancy B | Excludes online D2C sales; uses 2022 INR-USD rate |

These comparisons show that our disciplined scope selection, timely exchange rate updates, and dual-source validation deliver a balanced, transparent baseline managers can reference with confidence.

Key Questions Answered in the Report

What is the current size of the India feminine hygiene products market?

The market is worth USD 1.32 billion in 2026 and is forecast to reach USD 2.29 billion by 2031, growing at 11.67% annually.

Which product type dominates sales?

Sanitary napkins hold 98.21% of 2025 revenue and continue to expand, supported by continuous innovations in comfort and materials.

How fast are organic pads growing?

Organic products are advancing at a 12.12% CAGR, the fastest pace among the segment.

Which region is the most attractive for future growth?

East India is projected to post the highest regional CAGR of 12.86% through 2031, driven by cash-transfer schemes and a strong manufacturing base.

Page last updated on: