Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.75 Billion |

| Market Size (2026) | USD 0.82 Billion |

| Market Size (2031) | USD 0.94 Billion |

| Growth Rate (2026 - 2031) | 2.25% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

India Energy Drinks Market Analysis by ���ϲ�����

The India energy drinks market size is valued at USD 0.82 billion in 2026, growing from the 2025 value of USD 0.75 billion, and is forecast to climb to USD 0.94 billion by 2031, advancing at a 2.25% CAGR. The market's growth is driven by increasing consumer preference for on-the-go beverages, rising participation in esports, and the growing demand for premium products featuring zero-sugar and natural ingredients with clean-label claims. Despite a 40% GST burden compressing margins for mass-priced SKUs, leading players maintain their market share through extensive distribution networks, partnerships with quick-commerce platforms, and strategic sports sponsorships. Companies are expanding bottling operations into Tier 2 and Tier 3 cities, reducing logistics costs, and ensuring chilled product availability. Regulatory factors, such as Food Safety and Standards Authority of India caffeine limits and rPET (recycled polyethylene terephthalate) mandates, have increased compliance costs but also created entry barriers that favor established players with strong financial capabilities. The market is also witnessing a shift from sugar-centric energy drinks to a diverse portfolio of functional, sugar-free, and natural variants.

Key Report Takeaways

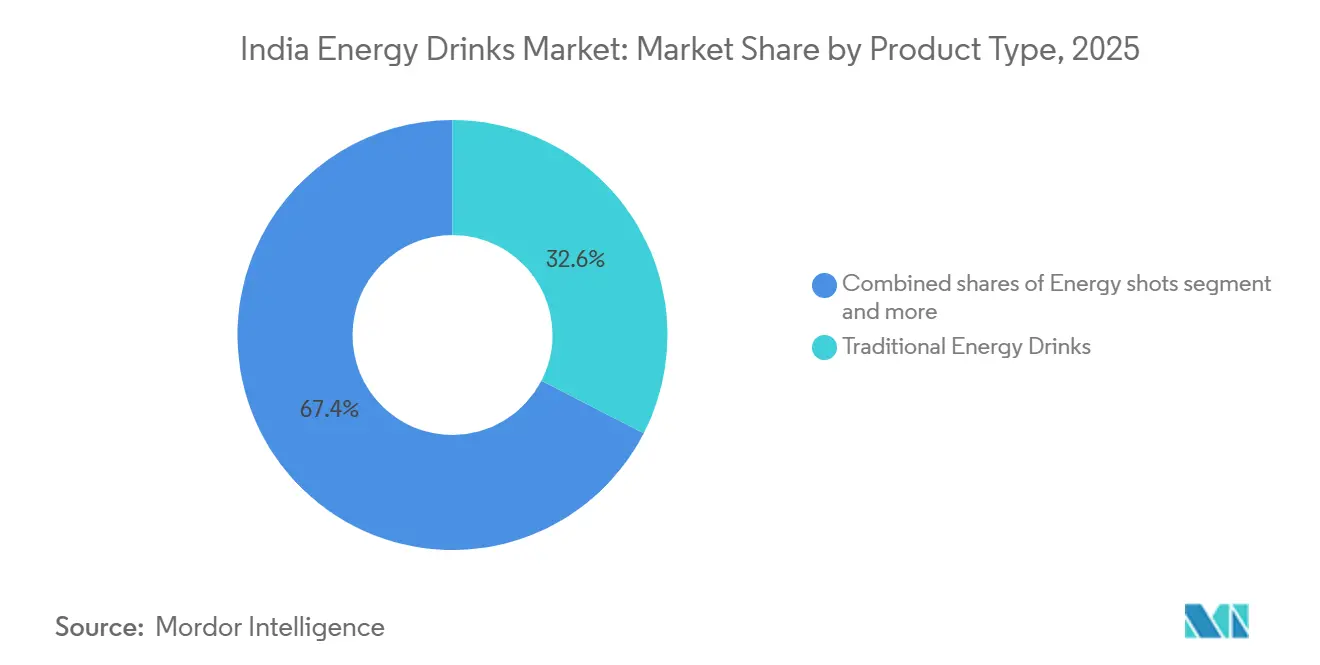

- By product type, traditional energy drinks led with 32.56% of India's energy drinks market share in 2025; natural/organic energy drinks are projected to grow at a 4.21% CAGR through 2031.

- By packaging, PET bottles captured 51.25% of the market share in 2025, while glass bottles represent the quickest-rising format at a 3.79% CAGR through 2031.

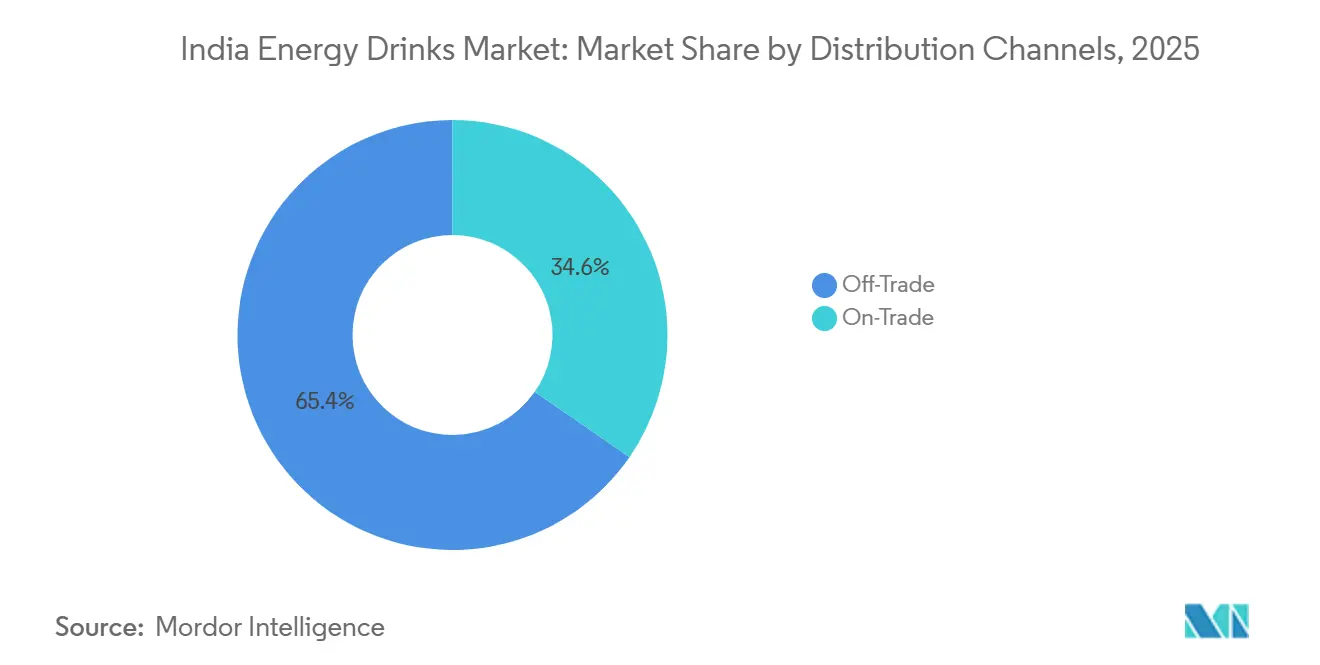

- By distribution channels, off-trade channels accounted for 65.38% of the Indian energy drinks market in 2025, and on-trade is expected to expand at a 4.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Energy Drinks Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising on-the-go workforce and demand for convenient energy options | +0.6% | Urban metros and Tier-1 cities; expanding to Tier-2 hubs | Medium term (2-4 years) |

| Expanding fitness and sports participation culture | +0.5% | Urban India; concentrated in metros and state capitals | Medium term (2-4 years) |

| Surge in e-sports and gaming boosting caffeine beverages | +0.3% | Pan-India with highest intensity in urban youth | Short term (≤ 2 years) |

| Cold-chain reach in Tier-2/3 cities enabling chilled RTD formats | +0.4% | Central and Eastern India Tier-2/3 cities; rural peri-urban corridors | Long term (≥ 4 years) |

| Shift to natural, sugar-free, and functional variants | +0.4% | Urban metros and affluent Tier-1 segments | Medium term (2-4 years) |

| Rapid urbanization and rising disposable incomes among working professionals | +0.5% | All-India with concentration in urban centers | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Understand The Key Trends Shaping This Market

Download Sample Report

Rising on-the-go workforce and demand for convenient energy options

India's gig economy and mobile workforce are significantly influencing beverage consumption patterns, positioning energy drinks as essential productivity tools rather than occasional leisure refreshments. According to the Ministry of Statistics and Programme Implementation, Urban monthly per capita consumption expenditure reached INR 6,996 in 2023-24, with beverages, refreshments, and processed foods accounting for a growing share of total urban household spending[1]Source: Ministry of Statistics and Programme Implementation, "Household Consumption Expenditure Survey: 2023-24", pib.gov.in. Quick-commerce platforms like Zepto, Blinkit, and Swiggy Instamart have further enabled impulse purchases during work hours, integrating energy drinks into daily routines rather than limiting them to occasional consumption. This shift highlights the importance of brands optimizing for single-serve, chilled formats and securing placement in modern trade and digital channels to capture a larger share of this on-the-go demand. Additionally, brands offering affordable single-serve chilled bottles at INR 20 are embedding the category into everyday consumption occasions, making energy drinks a staple for urban consumers.

Expanding fitness and sports participation culture

India has one of the largest youth populations in the world, which is driving significant changes in consumption patterns. The growing awareness of health and fitness among this demographic is fueling demand for functional beverages, including energy drinks. The fitness and sports industry in India is also expanding rapidly. In 2025, the Ministry of Youth Affairs and Sports approved 323 new sports infrastructure projects and 1,041 Khelo India Centres for athlete training and development[2]Source: Ministry of Youth Affairs and Sports, "India's Growing Focus on Youth and Sports", pib.gov.in. Gym memberships are on the rise, and boutique fitness studios are catering to affluent urban consumers who are willing to pay premium prices for specialized formulations. These include products enriched with electrolytes, amino acids, and natural caffeine sources. Energy drinks are increasingly being positioned as pre-workout or recovery beverages, available in gym vending machines, café counters, and sports nutrition stores. This creates a functional use case that differentiates them from carbonated beverages. Additionally, this fitness-linked consumption trend helps insulate energy drink brands from the health concerns associated with sugar-heavy soft drinks.

Rapid urbanization and rising disposable incomes among working professionals

India's urban-rural consumption gap narrowed to 70% in 2023-24, yet urban households still command a premium in monthly per capita expenditure, creating a concentrated purchasing base for premium beverages, whereas the bottom 5% of rural households saw monthly per-capita consumer expenditure rise 22% in 2023-24, as highlighted in the Household Consumption Expenditure Survey 2023-24. This indicates that affordability is expanding beyond urban strongholds. Beverages, refreshments, and processed food emerged as the largest contributors to household food expenditure in both rural and urban areas, signaling that packaged drinks have transitioned from discretionary to routine purchases. This shift suggests that the addressable market for affordable energy drinks is broadening, favoring brands that can deliver functional benefits at lower price points rather than premium INR 100+ formats. This trend indicates a burgeoning demand in semi-urban markets, a space already tapped by brands like PepsiCo's Sting and Coca-Cola's Thums Up Charged. Furthermore, the growing consumer awareness of health and wellness is driving demand for energy drinks with clean-label ingredients, creating an opportunity for brands to innovate and cater to this evolving preference.

Surge in e-sports and gaming boosting caffeine beverages

India has 1.002 billion internet users as of June 2025, making it one of the largest digital markets globally. The country also boasts over 400 gaming organizations and a digital gamer base exceeding 420 million. This aligns seamlessly with the energy drinks market, which primarily targets the 18-35 age demographic. E-sports tournaments, streamer collaborations, and in-game advertising have become integral marketing strategies for energy drink brands aiming to establish a strong presence within gaming culture. The increasing popularity of late-night gaming sessions and competitive online play has driven consistent demand for caffeinated beverages that enhance focus and combat fatigue. This positioning is distinct from the physical-performance narrative often used in fitness-related channels. Additionally, brands are capitalizing on influencer partnerships and user-generated content on platforms like Instagram to boost visibility among this tech-savvy audience. This demographic also shows a strong preference for digital commerce and quick-delivery platforms, further driving the growth of energy drink sales. The integration of energy drinks into gaming and digital lifestyles highlights the evolving consumer behavior in India, where convenience and functionality are becoming key purchase drivers.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over high caffeine, sugar, and artificial additives | -0.4% | Pan-India; amplified in urban educated segments with high health awareness | Short term (≤ 2 years) |

| Stringent regulations on labeling, caffeine limits, and advertising to youth | -0.3% | National; enforced by FSSAI with state-level variations in compliance rigor | Medium term (2-4 years) |

| Raw-material price spikes for botanicals and vitamins | -0.2% | National | Short term (≤ 2 years) |

| Rise of alternative functional beverages like kombucha or nootropics | -0.2% | Urban metros and affluent Tier-1 cities | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Health concerns over high caffeine, sugar, and artificial additives

The Indian energy drinks market is witnessing significant growth, driven by evolving consumer preferences and increasing awareness of health and wellness. FSSAI's nutraceutical regulations cap caffeine at 300 mg per day and 200 mg per single dose for adults, with mandatory warning labels required on packaging, forcing brands to balance efficacy with regulatory compliance. Growing health concerns over high caffeine, sugar, and artificial additives are significantly influencing consumer preferences. This trend has led to an increased demand for healthier alternatives, prompting brands to reformulate their products by incorporating natural caffeine sources such as green tea extract and guarana. Additionally, manufacturers are reducing sugar content, eliminating artificial additives, and focusing on clean-label and organic certifications to cater to the health-conscious demographic. Urban consumers, in particular, are driving this shift as they prioritize transparency and wellness in their purchasing decisions. To align with these evolving preferences, brands are repositioning their offerings from "energy boost" to "functional wellness," highlighting benefits such as vitamins, electrolytes, hydration, and cognitive support, rather than solely focusing on stimulation.

Stringent regulations on labeling, caffeine limits, and advertising to youth

The Food Safety and Standards Authority of India (FSSAI) enforces caffeine limits between 145 and 300 mg per liter for energy drinks and mandates prominent disclosure of caffeine content and health warnings on all packaging[3]Source: Food Safety and Standards Authority of India, "CHAPTER 2 FOOD PRODUCT STANDARDS 2.10", fssai.gov.in. These regulations create compliance costs and limit formulation flexibility for brands operating in the market. To address these challenges, many companies are reformulating their products to include natural caffeine sources, such as green tea extract or guarana, which align with consumer preferences for clean-label products. However, brands have to prominently disclose caffeine content to meet FSSAI requirements. Advertising restrictions targeting youth remain a regulatory gray area, with industry stakeholders anticipating tighter controls on broadcast and digital campaigns in the near future. For instance, Hector Beverages' Tzinga faced multiple recalls and reformulations due to objections from the FSSAI over ginseng content, highlighting the enforcement risks smaller brands face as they navigate India's evolving regulatory landscape.

Segment Analysis

By Product Type: Affordability Anchors Traditional Dominance

Traditional energy drinks commanded 32.56% of market share in 2025, driven by strong consumer familiarity and competitive pricing. Products like PepsiCo's Sting and Coca-Cola's Thums Up Charged, priced at INR 20 for a 250 ml pack, are significantly more affordable compared to Red Bull's INR 125 offering. This price advantage enables these brands to achieve widespread penetration, particularly through traditional grocery outlets and street stalls, making them accessible to a broader consumer base. The affordability factor, coupled with established brand recognition, continues to make energy drinks a preferred choice among consumers in both urban and rural markets.

Natural/organic energy drinks are expanding at a 4.21% CAGR through 2031, presenting a premiumization opportunity for brands that can effectively highlight clean-label credentials while maintaining affordability. The rising demand for sugar-free and low-calorie variants reflects a shift in consumer preferences toward functional benefits over indulgence. Additionally, energy shots, though a niche segment, are gaining popularity among on-the-go professionals seeking a concentrated caffeine boost in a compact format. Other energy drink categories, including hybrid formats such as coffee-energy blends and electrolyte-enhanced variants, are emerging as micro-segments. These products cater to specific use cases, such as pre-workout energy, post-exercise recovery, or cognitive focus, further diversifying the market landscape.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download Sample Report

By Packaging Type: Sustainability Mandates Reshape Material Choices

PET bottles accounted for 51.25% of the market share in 2025, driven by their affordability, portability, and compatibility with India's fragmented distribution infrastructure. However, glass bottles are expected to witness the fastest growth, with a projected CAGR of 3.79% through 2031, as sustainability concerns and premium positioning gain prominence. India's Ministry of Environment had mandated 30% recycled plastic content in rigid packaging in April 2025, with an annual increase of 10% to reach 60% by the fiscal year 2028-29. In response, companies like Indorama Ventures and Varun Beverages are collaborating to construct PET recycling facilities in Kathua and Khordha, aiming to achieve an annual recycled-PET capacity of 100,000 metric tons across all facilities.

Metal cans, while dominant in Western markets due to their recyclability and premium perception, face challenges in India due to higher unit costs and limited recycling infrastructure. Their adoption is primarily concentrated in urban modern trade and on-premise channels, where chilled consumption and brand visibility justify the price premium. Glass bottles, on the other hand, are gaining traction among premium and natural energy drink brands that aim to differentiate through sustainable packaging and enhanced shelf appeal. However, their higher weight and susceptibility to breakage increase logistics costs in a market where distribution efficiency is critical to profitability. Despite these challenges, the growing consumer preference for environmentally friendly packaging is expected to drive the adoption of glass bottles in niche segments.

By Distribution Channel: On-Trade Gains as Fitness and Foodservice Expand

Off-trade channels accounted for a 65.38% distribution share in 2025, reflecting the dominance of India's retail landscape, where grocery stores, convenience outlets, and street stalls play a significant role in fast-moving consumer goods distribution. Within the off-trade segment, supermarkets and hypermarkets offer enhanced brand visibility and chilled storage options, although their limited geographic reach restricts their overall impact. Conversely, convenience stores and street stalls drive high-volume sales due to their presence in high-footfall areas and their ability to cater to impulse purchases. However, their reliance on ambient-temperature storage limits the potential for premium product positioning. Online retail, which includes e-commerce and quick-commerce platforms, is emerging as a key distribution channel. It allows brands to overcome distribution challenges and directly target urban consumers, particularly professionals, through same-day delivery services.

On-trade venues such as cafes, bars, gyms, and restaurants are expected to grow at the fastest rate, with a projected CAGR of 4.48% through 2031. This growth is fueled by the expansion of the foodservice sector and the repositioning of energy drinks as functional beverages suited for fitness and social occasions. On-trade channels provide strategic benefits beyond just sales volume. Placement in gyms and fitness studios positions energy drinks as ideal pre-workout or recovery options, helping brands mitigate potential health-related concerns. Additionally, cafes and bars offer opportunities for mixology and premium pricing, enhancing the perception of energy drinks as lifestyle products. The evolving distribution landscape highlights the importance of tailoring strategies to leverage both off-trade and on-trade channels effectively, ensuring brands can meet diverse consumer needs while maximizing market penetration.

Get Detailed Market Forecasts at the Most Granular Levels

Download Sample Report

Geography Analysis

India's energy drinks market exhibits pronounced urban concentration, with metros and Tier-1 cities accounting for the majority of consumption due to higher disposable incomes, greater retail infrastructure, and stronger alignment with on-the-go lifestyles. Urban monthly per capita consumption expenditure reached INR 6,996 in 2023-24, a 70% increase over rural monthly per capita consumption expenditure of INR 4,122. Beverages, refreshments, and processed food captured 11.09% of urban household spending versus 9.84% in rural areas, indicating stronger per-household spending potential in cities. For instance, Hell Energy Drink's Black Cherry launch targeted Mumbai, Pune, Delhi NCR, Bengaluru, Hyderabad, and Chandigarh, metros and Tier-1 cities with established modern retail and quick-commerce infrastructure, reflecting the strategic prioritization of urban strongholds for new product introductions.

Tier-2 and Tier-3 cities represent the next growth frontier, yet cold-chain limitations and fragmented retail networks constrain market penetration. India's cold storage capacity reached 38.5 million tonnes in 2025, yet Central and Eastern India remain under-supplied. Varun Beverages' commissioning of greenfield facilities in Supa, Gorakhpur, and Khordha in 2024 extended cold-chain reach into previously underserved geographies, enabling chilled distribution of Sting and other PepsiCo brands in regional markets. Additionally, the rise of quick-commerce platforms in Tier-2 cities is gradually bridging the gap in accessibility, allowing brands to tap into semi-urban demand. Brands that can deliver functional benefits at INR 20-30 price points and secure distribution through traditional grocery and street stalls will capture this emerging rural and semi-urban demand.

Regional consumption patterns also reflect cultural and climatic variations, with Southern and Western states exhibiting higher per-capita beverage consumption due to warmer climates and greater urbanization. Meanwhile, Northern and Eastern states show lower penetration but faster growth rates as infrastructure improves. The addressable market for affordable energy drinks is broadening, favoring brands that can scale distribution beyond metros. The strategic imperative is to balance urban premiumization leveraging modern trade, on-premise, and e-commerce for higher margins with mass-market penetration in Tier-2/3 cities and peri-urban corridors through affordable formats and distribution channels. Furthermore, the increasing awareness of health and wellness trends across all regions is expected to drive demand for low-calorie and sugar-free energy drink variants, creating opportunities for product diversification.

Competitive Landscape

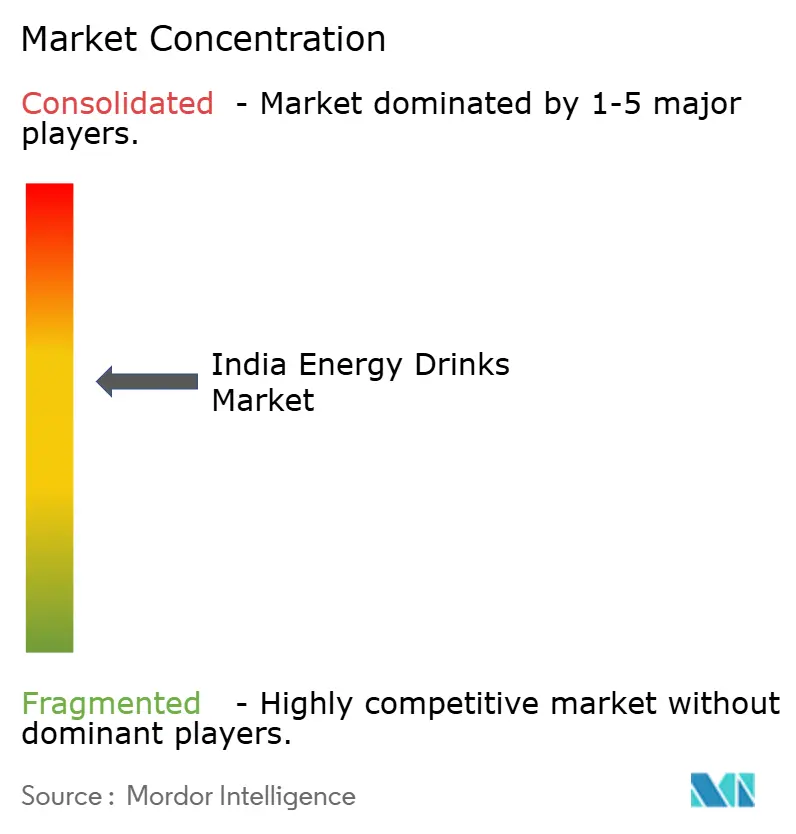

India energy drinks market is moderately consolidated, reflecting a landscape where energy drinks like PepsiCo's Sting disrupted price benchmarks and captured a major share of the market in earlier years. However, local challengers such as Tata Consumer's Say Never!, Bisleri's Urzza, and Hector Beverages' Tzinga are leveraging regional flavors, affordable pricing, and functional positioning to compete with key players. Varun Beverages, PepsiCo's largest franchisee, tripled its revenue between 2018-2023 to INR 16,042.6 crore. This highlights how bottler-led distribution infrastructure plays a critical role in determining market access.

Multinational players are now defending their market shares through flavor innovations, localized endorsements, and geographic expansion. For instance, Red Bull has introduced smaller pack sizes to cater to price-sensitive consumers, while Coca-Cola's Thums Up Charged has focused on leveraging its strong brand equity in India. Only 5 of India's 18 food-grade recycled-PET manufacturers hold FSSAI certification, creating a supply bottleneck that favors vertically integrated bottlers and presents an entry barrier for smaller brands. Emerging brands are adopting digital-first go-to-market strategies, leveraging quick-commerce platforms and influencer marketing to bypass distribution bottlenecks and target urban millennials and Gen Z consumers.

The GST on energy drinks compresses margins and discourages investment in innovation. However, it also protects incumbents by raising entry barriers for new players who lack the scale to absorb the tax burden. Despite these challenges, the market continues to grow, driven by increasing consumer awareness of functional beverages and a shift toward healthier lifestyles. Technology adoption remains nascent, with most brands relying on sales force automation and distributor management systems rather than advanced analytics or direct-to-consumer digital platforms. This presents an opportunity for tech-enabled challengers to gain market share through superior demand forecasting, targeted promotions, and enhanced consumer engagement strategies.

India Energy Drinks Industry Leaders

-

Anheuser-Busch InBev SA/NV

-

Monster Beverage Corporation

-

PepsiCo, Inc.

-

Red Bull GmbH

-

The Coca-Cola Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download Sample Report

Recent Industry Developments

- September 2025: 28 BLACK, a premium energy drink brand, launched its energy drinks in India. Initial flavors for India include best-seller Açai (fruity berry taste) and Gummibär, tailored to local preferences.

- September 2025: Hell Energy Drink, a rapidly expanding global brand from Hungary, has introduced its premium Black Cherry flavor in India, featuring an intense black cherry taste with the original energy formula enriched by multiple B-vitamins and no added preservatives.

- February 2025: Reliance Consumer Products Limited launched Spinner, a low-cost sports drink priced at INR 10 per bottle, co-created with cricketer Muttiah Muralitharan. Available in Lemon, Orange, and Nitro Blue flavors, Spinner secured visibility through partnerships with multiple IPL teams.

- September 2024: Indorama Ventures and Varun Beverages announced the construction of multiple PET recycling facilities in India, with two plants in Kathua (Jammu and Kashmir) and Khordha (Odisha). The joint venture targets 100,000 metric tons of annual recycled-PET capacity across all facilities to meet rising demand.

India Energy Drinks Market Report Scope

Energy drinks are non-alcoholic, functional beverages formulated with high concentrations of stimulants, primarily caffeine, along with ingredients like taurine, B vitamins, and guarana. It provides instant mental alertness and physical energy, sold in carbonated or non-carbonated ready-to-drink (RTD) cans, bottles, and shots. The India energy drinks market is segmented by product type, packaging, and distribution channel. Based on product type, the market is segmented into energy shots, natural/organic energy drinks, sugar-free/low-calorie energy drinks, Traditional energy drinks, and other energy drinks. By packaging, the market is segmented into PET bottles, glass bottles, metal cans, and others. By distribution channel, the market has been segmented into on-trade and off-trade channels. For each segment, the market sizing and forecasts have been done based on value (USD).

By Product Type

| Energy Shots |

| Natural/Organic Energy Drinks |

| Sugar-Free/Low-Calorie Energy Drinks |

| Traditional Energy Drinks |

| Other Energy Drinks |

By Packaging Type

| PET Bottles |

| Glass Bottles |

| Metal Can |

| Others |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarket/Hypermarket |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

| By Product Type | Energy Shots | |

| Natural/Organic Energy Drinks | ||

| Sugar-Free/Low-Calorie Energy Drinks | ||

| Traditional Energy Drinks | ||

| Other Energy Drinks | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Metal Can | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarket/Hypermarket | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| �䲹��é | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

���ϲ����� follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms

Get More Details On Research Methodology

Download Sample Report