Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

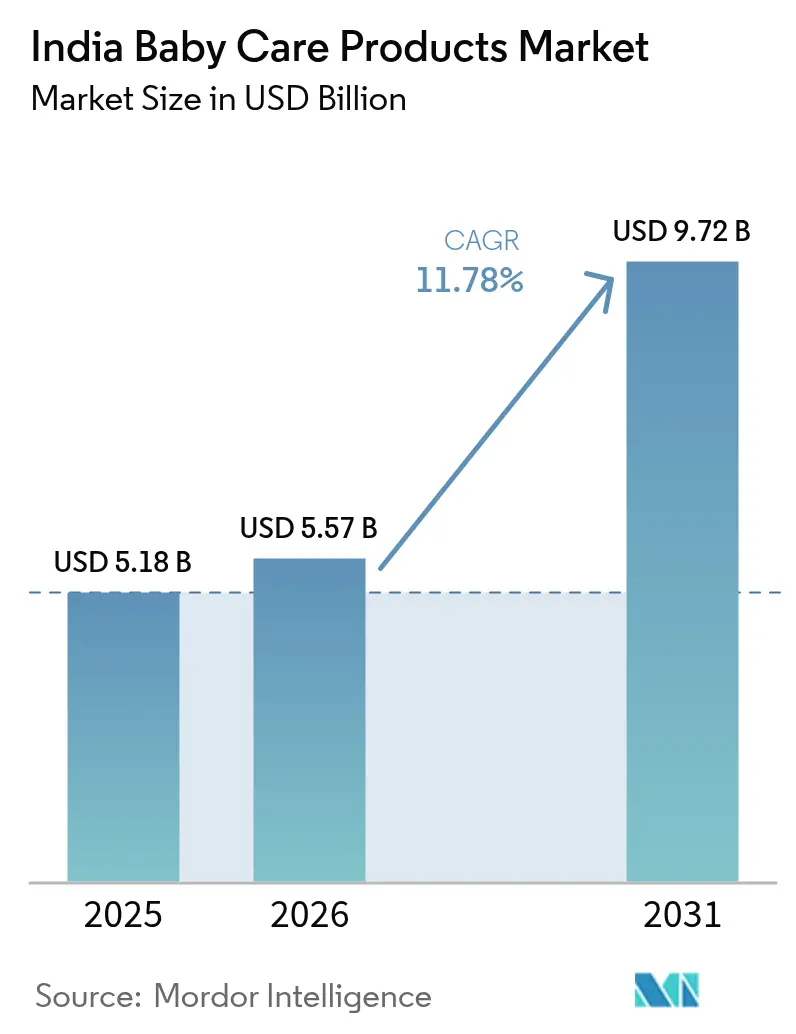

| Base Year Market Size (2025) | USD 5.18 Billion |

| Market Size (2026) | USD 5.57 Billion |

| Market Size (2031) | USD 9.72 Billion |

| Growth Rate (2026 - 2031) | 11.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

India Baby Care Products Market Analysis by ���ϲ�����

The India baby care products market size was valued at USD 5.18 billion in 2025, reached USD 5.57 billion in 2026, and is projected to grow to USD 9.72 billion by 2031, registering a compound annual growth rate (CAGR) of 11.78% during the forecast period of 2026-2031. This growth is primarily driven by rapid urbanization, a consistently high annual birth rate of approximately 26 million, and increasing disposable incomes. These factors are fueling demand for baby care products across metropolitan areas as well as tier-2 and tier-3 cities. Additionally, increasing digital penetration, the expansion of organized retail networks, and a growing preference for premium products are further contributing to market growth. The market is segmented by product type, with nutritional products and skincare items experiencing notable growth. By nature, organic products are gaining popularity and challenging the dominance of conventional offerings. In terms of age group, demand for infant-focused products is rising, although toddler-oriented products continue to hold a significant share. Distribution channels are also evolving, with e-commerce platforms playing a pivotal role in transforming consumer access to baby care products. The competitive landscape is moderately intense, with multinational corporations and domestic companies competing through pricing strategies and investments in innovation.

Key Report Takeaways

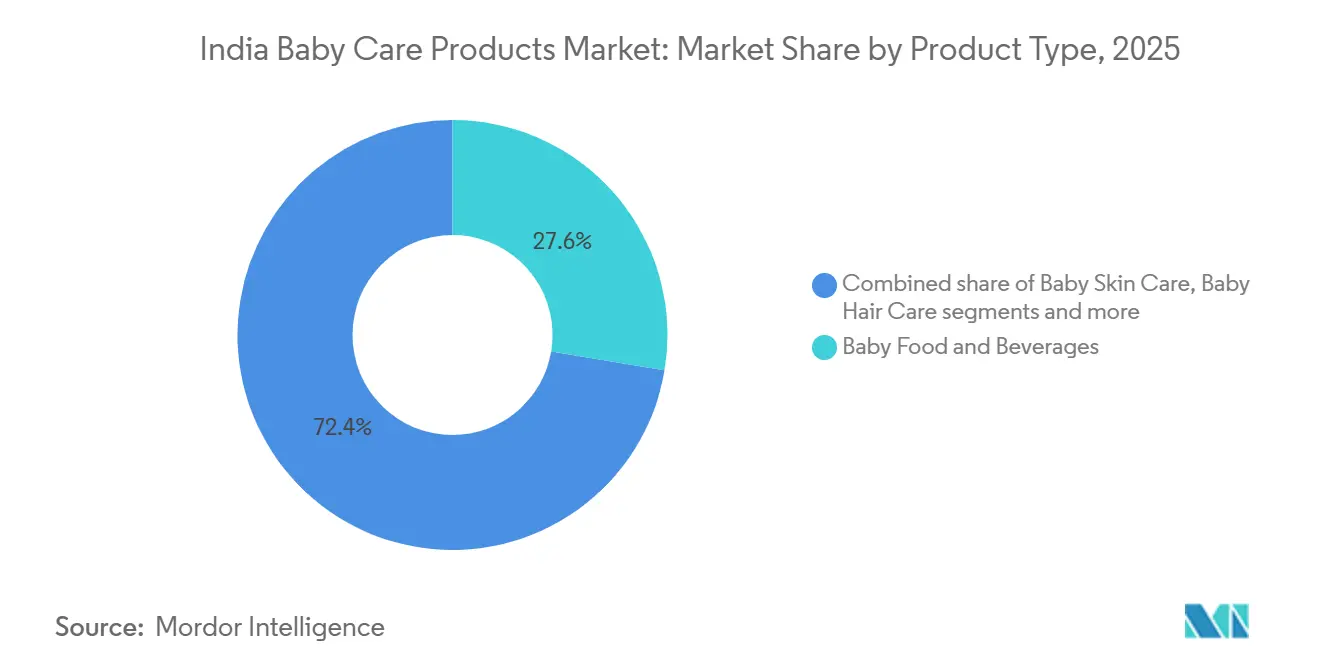

- By product type, baby food and beverages represented 27.62% of the India baby care products market share in 2025, while the baby skin care segment is anticipated to grow at a CAGR of 12.59% through 2031.

- By nature, synthetic/conventional products accounted for 77.08% of the India baby care products market size in 2025. In contrast, natural/organic products are expected to grow at a CAGR of 13.88% by 2031.

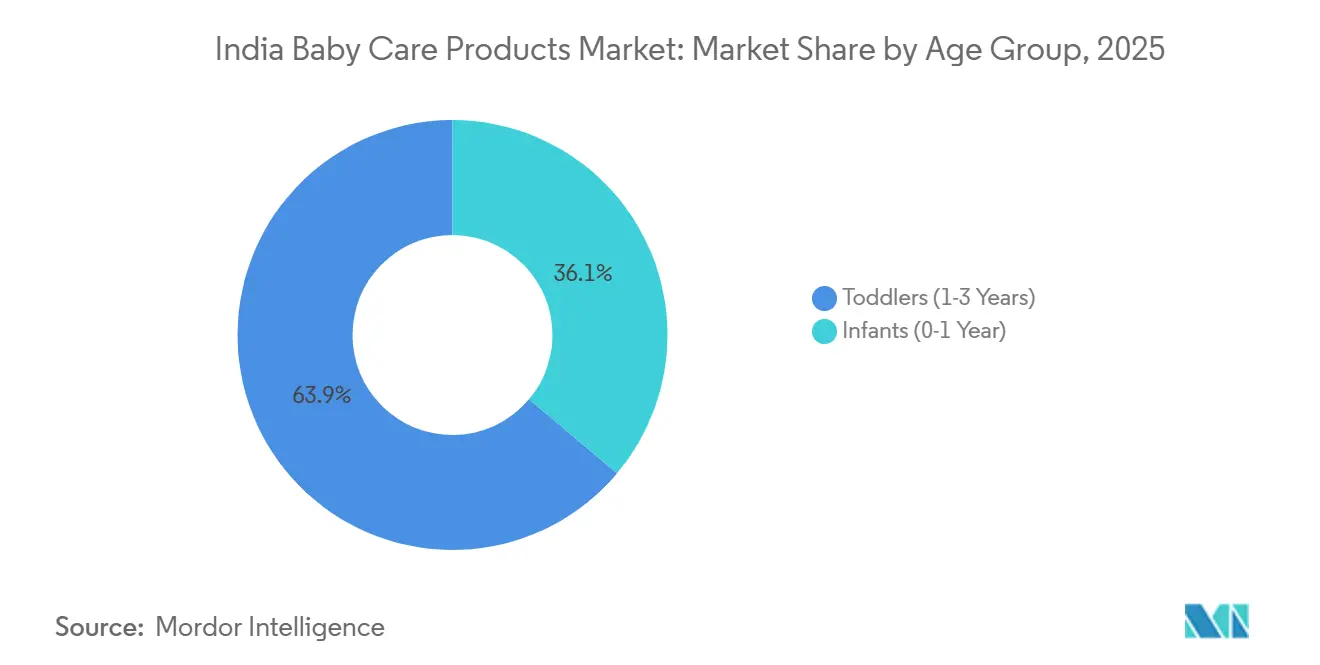

- By age group, toddlers (1-3 years) dominated with a 63.88% share of the India baby care products market size in 2025. Meanwhile, the infants (0-1 year) segment is projected to grow at a CAGR of 12.66% through 2031.

- By distribution channel, supermarkets/hypermarkets held a 36.37% revenue share in 2025, whereas online retail is expected to register the fastest CAGR of 12.57% by 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Baby Care Products Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing awareness of infant health and hygiene | +2.1% | National, with early gains in metro cities and tier-1 urban centers | Medium term (2-4 years) |

| Shift toward organic and chemical-free products | +1.8% | Urban India, expanding to tier-2 cities | Long term (≥ 4 years) |

| Innovations in product offerings | +1.6% | Localized adaptations for Indian climate and preferences | Short term (≤ 2 years) |

| Technological advancements in baby care products | +1.3% | Metro cities and affluent urban segments | Medium term (2-4 years) |

| Increasing awareness about product safety and certifications | +1.4% | National, driven by regulatory compliance requirements | Medium term (2-4 years) |

| Rising availability of international and premium brands | +1.2% | Tier-1 and tier-2 cities with growing retail infrastructure | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Growing awareness of infant health and hygiene

Awareness of infant health and hygiene is increasing rapidly in India, driven by heightened health consciousness following the pandemic and recommendations from pediatricians. Parents are prioritizing the purchase of baby care products that ensure safety and comfort for their children. This trend is particularly noticeable among urban families with dual incomes, where premium product offerings significantly influence purchasing decisions. According to the World Bank, approximately 25% of India’s population falls within the 0–14 age group as of 2024, ensuring a steady demand for baby care products [1]Source: World Bank, "Population Ages 0-14 (% of Total Population)", data.worldbank.org. Brands are introducing new products to differentiate themselves in the market. For instance, in January 2024, Pampers India launched its updated Pampers Premium Care diaper, marketed as India’s softest diaper, targeting parents seeking enhanced comfort for their infants.

Shift toward organic and chemical-free products

The demand for organic and chemical-free products is emerging as a significant trend in India’s baby care market, driven by rising household incomes and shifting consumer preferences toward safer and more natural options. According to the IMF, India’s GDP at purchasing power parity is projected to reach USD 17.65 trillion by 2025 [2]Source: International Monetary Fund, "GDP, Current Prices, Purchasing Power Parity; Billions of International Dollars", imf.org. This economic growth has encouraged parents to invest in premium baby care products that prioritize natural ingredients, gentle formulations, and overall child well-being. This trend is particularly evident among millennial parents, who actively prefer chemical-free and Ayurveda-inspired solutions, considering them healthier and safer for their children. Companies are addressing this demand with innovative product launches that blend traditional practices with scientific advancements. For instance, the Himalaya Baby Care Pure Cow Ghee range, introduced in 2024, is free from harsh chemicals and formulated to support the skin barrier and maintain the natural microbiome, making it suitable for sensitive skin and newborns. The preference for natural products also aligns with a broader premiumization trend, where parents are willing to pay a premium for quality, safety, and eco-friendly ingredients.

Increasing awareness about product safety and certifications

Awareness of product safety and certifications is increasingly influencing India’s baby care market, as parents prioritize transparency, reliability, and trust when selecting products for their children. Regulatory authorities have enhanced oversight to safeguard consumers. For example, the Food Safety and Standards (Labelling and Display) Amendment Regulations, 2022, implemented in 2023, require packaged products to prominently display key nutritional information, including sugar, salt, and fat content, in bold fonts, as mandated by the Food Safety and Standards Authority of India (FSSAI) [3]Source: Food Safety and Standards Authority of India, "Food Safety and Standards (Foods for Infant Nutrition) Regulations", fssai.gov. This regulation aims to provide consumers with clear and accessible information, enabling them to make informed decisions about the products they purchase. Consequently, parents are more inclined to choose brands offering certifications and QR-code authentication to verify product safety and quality. In response, companies are introducing safer, premium products to meet these demands. For instance, in June 2024, Lifelong Online entered the baby care market with a range of products, including wearable breast pumps, anti-slip baby bathers, baby seats, and strollers. These products reflect the growing emphasis on innovative, secure, and reliable solutions for infants, catering to the evolving preferences of parents who seek both functionality and assurance in the products they use for their children.

Technological advancements in baby care products

Technological advancements are reshaping India’s baby care products market, as companies adopt innovative solutions to enhance product safety, convenience, and reliability for parents. For instance, Kimberly-Clark has invested USD 15 million in its Pune technology center to develop smart diapers equipped with AI-enabled wetness alerts and temperature indicators, providing real-time monitoring while ensuring comfort for babies. Digital platforms are also utilizing advanced tools to improve the shopping experience. FirstCry, for example, uses predictive algorithms in its subscription model to automate delivery scheduling, catering to over 7.5 million users per month and simplifying the management of recurring needs for parents. Furthermore, augmented reality (AR) technology allows parents to visualize product fit and functionality before purchase, enabling more informed decision-making.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity and proliferation of counterfeit products | -1.8% | National, with acute impact in rural and semi-urban areas | Short term (≤ 2 years) |

| Complex multi-agency regulatory approvals for baby cosmetics | -0.9% | National, affecting all manufacturers and importers | Medium term (2-4 years) |

| Potential health concerns related to chemical residues | -1.2% | National, with heightened scrutiny in urban markets | Medium term (2-4 years) |

| Limited awareness in semi-urban/rural areas | -1.4% | Rural India and tier-3+ cities | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High price sensitivity and proliferation of counterfeit products

The Food Safety and Standards Authority of India (FSSAI) seized counterfeit and mislabeled food products valued at INR 1,000 crore (USD 120 million) in 2024 through over 12,000 inspections. This highlights the existence of a shadow economy driven by price-conscious consumers who are either unwilling or unable to pay premiums for authenticated brands. Counterfeit baby formula presents significant health risks due to inadequate nutrient profiles and potential contamination. However, enforcement efforts remain inconsistent, particularly in rural areas where organized retail has limited reach, and informal distribution networks are prevalent. E-commerce platforms also face difficulties in monitoring third-party sellers, as counterfeit listings occasionally appear despite marketplace policies requiring seller verification. The price gap between genuine and counterfeit products often exceeds 50%, creating strong economic incentives for illicit trade. This is especially evident in categories such as diapers and wipes, where brand differentiation is less distinct compared to products like infant formula or medicated skin care.

Potential health concerns related to chemical residues

The Food Safety and Standards Authority of India (FSSAI) has set contaminant limits of 0.01 mg/kg for lead and 0.05 μg/kg for aflatoxins in infant nutrition products, aligning with global best practices. However, enforcement is based on periodic sampling rather than continuous monitoring, which creates opportunities for non-compliant products to reach consumers. Isolated cases have revealed the presence of heavy metals such as arsenic and mercury, as well as pesticide residues in organic baby foods. These findings have led consumer advocacy groups to call for stricter testing protocols and public disclosure of test results. The Bureau of Indian Standards mandates testing for phthalates and parabens in baby cosmetics, substances associated with endocrine disruption in animal studies. However, the lack of mandatory third-party certification allows manufacturers to self-declare compliance. This practice undermines consumer trust, particularly when independent laboratory tests reveal inconsistencies. Additionally, the "clean label" movement, driven by siginifcant parent population seeking non-toxic formulations, highlights both perceived regulatory gaps and health concerns. This trend suggests that greater transparency and third-party validation could serve as competitive advantages for manufacturers.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Nutritional Leadership Meets Dermatological Upswing

In 2025, baby food and beverages accounted for a notable 27.62% share of India’s baby care products market, underscoring the growing emphasis on infant nutrition during the critical early years. This segment includes infant formula, cereals, juices, and fortified drinks, which are increasingly enriched with essential nutrients to support healthy growth and immunity. Urban parents show a strong preference for ready-to-use and clinically tested products that offer both convenience and safety. Domestic and international brands are responding by introducing age-specific formulations and user-friendly packaging to align with the evolving needs of modern consumers.

The baby skin care segment is the fastest-growing category in the market, with a projected CAGR of 12.59% through 2031. This growth is driven by rising awareness of infant skin sensitivity and the importance of product safety. Parents are increasingly opting for lotions, creams, oils, and gentle cleansers specifically formulated for delicate baby skin. Companies are adapting their products to suit India’s varied climates, ranging from humid coastal regions to dry inland areas, ensuring better protection and comfort. Hypoallergenic and dermatologically tested claims have become critical factors influencing purchasing decisions. Additionally, the use of natural and organic ingredients is gaining traction among parents who prioritize safety and gentle care for their children.

By Nature: Organic Momentum Challenges Conventional Scale

In 2025, synthetic/conventional products dominated the India baby care products market, accounting for 77.08% of total revenue. Their widespread popularity is attributed to affordability, easy availability, and strong brand recognition, particularly in rural and tier-3 cities. Robust distribution networks and competitive pricing make these products accessible to price-sensitive households. Additionally, aggressive marketing strategies and retailer incentives further strengthen their market position. Despite growing competition from organic alternatives, conventional products continue to attract consumers by offering consistent quality at lower costs.

In contrast, natural/organic formulations are experiencing rapid growth, with a projected CAGR of 13.88% through 2031, outpacing the overall market growth rate. Modern parents are increasingly prioritizing safety and health, opting for products made from plant-based or Ayurveda-inspired ingredients, even at higher price points. This segment includes baby lotions, oils, wipes, and creams, primarily targeting urban and affluent consumers. Certifications such as BIS organic labels play a crucial role in establishing credibility and ensuring product authenticity. As awareness of chemical-free and eco-friendly alternatives grows, natural and organic products are becoming significant drivers of innovation and premiumization in India’s baby care market.

By Age Group: Infant Upsurge Amid Toddler Dominance

In 2025, toddlers aged 1–3 years accounted for 63.88% of the total revenue in India’s baby care products market, making this segment the largest contributor. This dominance is attributed to the prolonged and consistent use of essential products such as diapers, cereals, and toiletries. Parents tend to invest more in toddler products due to their extended necessity. The segment performs particularly well in urban and semi-urban areas, where factors like convenience, brand recognition, and product familiarity significantly influence purchasing decisions. Furthermore, innovations in toddler-specific products, such as fortified foods and gentle skincare formulations, have strengthened this age group’s market leadership.

The infant segment (0–12 months) is projected to grow at a 12.66% CAGR through 2031, making it the fastest-growing category, surpassing the growth of the toddler segment. Urban parents are increasingly investing in premium infant products, including specialized diapers and dermatologically tested baby care solutions. Rising awareness of infant health and safety is driving demand for high-quality, chemical-free products. Additionally, technology-enabled offerings, such as smart baby monitors and organic formulations, are gaining traction. This trend highlights a growing focus on optimal care during the critical first year, positioning the infant segment as a key driver of future market growth.

By Distribution Channel: Digital Commerce Reconfigures Access

In 2025, supermarkets and hypermarkets accounted for the largest share of baby care product sales, representing 36.37% of the market. These outlets are particularly popular among urban shoppers due to their ability to offer a wide range of products, including diapers, baby food, wipes, and skincare, under one roof. Parents value these stores for their convenience, reliability, and frequent in-store promotions, which simplify shopping and reduce costs. The availability of well-known brands and attractive discounts further enhances their appeal, especially in tier-1 and tier-2 cities, solidifying supermarkets and hypermarkets as a vital distribution channel in the baby care industry.

Online retail is emerging as the fastest-growing distribution channel, with a projected CAGR of 12.57%, the highest among all channels. E-commerce platforms offer unmatched convenience, allowing parents to shop from home while accessing a diverse range of products, including premium and imported brands. Features such as personalized recommendations and easy payment options improve the online shopping experience. The increasing penetration of internet connectivity and smartphones across India is driving this trend, particularly in urban areas, positioning online retail as a significant driver of future growth in the baby care market.

Geography Analysis

Urban centers and Tier-1 cities contribute a disproportionately high share of market value in India’s baby care products sector, despite representing a smaller segment of the population. This trend is primarily driven by the increasing prevalence of dual-income families, who demonstrate a higher willingness to invest in premium, organic, and technology-enabled baby care solutions. Demand in these cities is projected to remain robust through 2031. Retailers are enhancing customer engagement by introducing experience-led store concepts, enabling parents to interact with smart baby devices and sustainable products before making a purchase. This approach aligns well with the preferences of digitally savvy and quality-conscious consumers.

Tier-2 and Tier-3 cities are emerging as the fastest-growing markets for baby care products, supported by a strong projected CAGR. Key factors driving this growth include the rapid expansion of organized retail formats and steadily rising household incomes. Companies such as FirstCry are accelerating their physical retail presence, with plans to open several hundred outlets in these cities by 2028 to meet the increasing demand for branded products. Additionally, brands are localizing product formulations to cater to regional needs, such as developing richer creams for colder northern climates or antifungal powders for humid coastal areas. These strategies are enabling brands to better address regional requirements and unlock growth potential in smaller urban centers.

Rural markets are experiencing slower growth, hindered by high price sensitivity and a continued reliance on traditional home-based care practices. However, awareness of commercial baby care products is gradually improving, supported by government health programs and grassroots education initiatives, including outreach efforts by local micro-influencers. Demand in rural areas is strongest for essential categories such as nutrition supplements and hygiene-related products. Companies like Dabur are leveraging their Ayurvedic heritage and extensive rural distribution networks to deepen market penetration. Meanwhile, multinational brands are collaborating with local self-help groups to build credibility and expand their presence in rural India.

Competitive Landscape

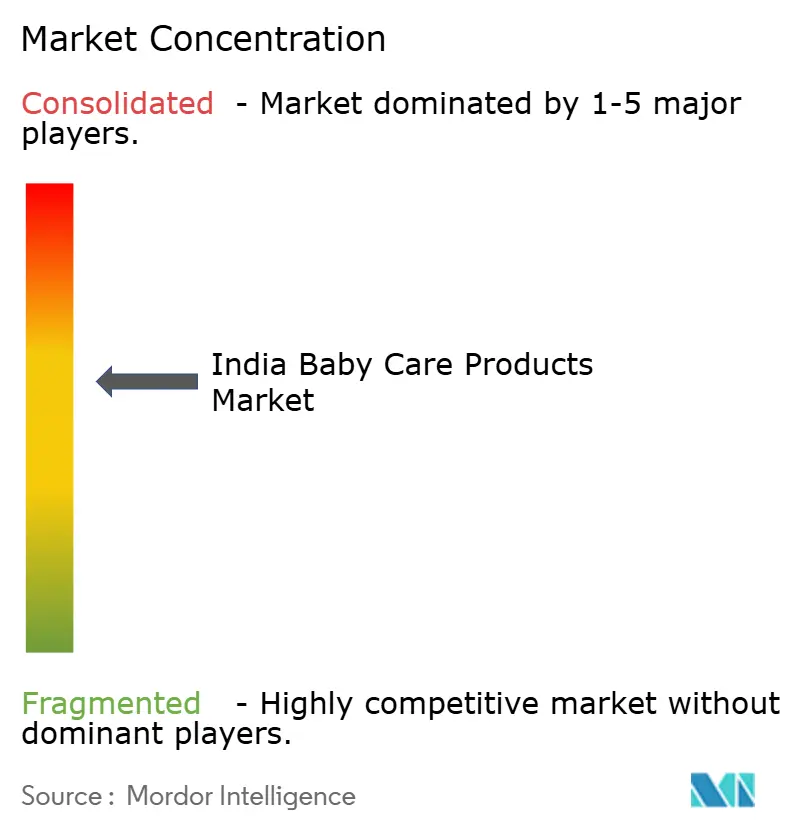

The Indian baby care products market is moderately consolidated, with competition arising between large multinational corporations and fast-growing domestic brands. International companies such as Nestlé, Unilever, and Procter & Gamble leverage their global research and development capabilities, established brand equity, and extensive supply networks to maintain their market positions. On the other hand, Indian companies such as Dabur, Patanjali, Honasa Consumer, and ITC leverage their deep understanding of regional consumer behavior, traditional preferences, and localized distribution networks to remain competitive. Across the market, brand strategies are shifting from aggressive pricing to credibility-driven growth, with a focus on product authenticity, safety certifications, and technology-based differentiation.

Mergers, acquisitions, and strategic collaborations are increasingly shaping the market as companies aim to expand their portfolios and enter specialized segments. For instance, ITC’s acquisition of Mother Sparsh in 2024 strengthened its position in the natural and toxin-free baby care segment. Similarly, Patanjali’s INR 11 billion investment in the home and personal care segment highlighted its ambition to compete with multinational brands in organized retail channels. Additionally, Doms Industries’ acquisition of a diaper manufacturing facility reflects a broader trend toward enhancing in-house manufacturing capabilities and achieving cost efficiencies. These developments underscore the growing importance of scale, vertical integration, and niche expertise in gaining a competitive edge.

Product innovation remains a key driver of growth, with companies allocating greater resources to research and accelerating go-to-market strategies. Notable examples include Kimberly-Clark’s introduction of AI-enabled smart diapers and Emami’s rapid launch of the Creme21 range to meet evolving consumer demands. To protect brand equity, companies are also adopting traceability and anti-counterfeiting measures to enhance consumer trust. Furthermore, omnichannel retail strategies are becoming increasingly critical, as modern parents seek consistent pricing, promotions, and brand experiences across both digital and physical platforms. Integrated engagement across these channels is emerging as a vital factor for success in the market.

India Baby Care Products Industry Leaders

-

Nestlé SA

-

Kenvue Inc.

-

Procter & Gamble Company

-

Unilever PLC

-

Danone SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: CuteStory, a newly launched baby-care brand, aims to provide safer, gentler, and more enjoyable baby care solutions for families. The brand focuses on gentle, reliable formulations that are dermatologically tested, free from harsh chemicals such as parabens and sulfates, and suitable for children from newborns up to 10 years old. It seeks to balance the gap between overly clinical and excessively decorative baby-care products.

- January 2025: Popees Baby Care has opened its 84th store in Kerala, emphasizing the provision of premium products and personalized services to its customers. This expansion underscores the brand's dedication to improving customer experience and reinforcing its presence in the region.

- January 2025: Panacea Biotec's wholly owned subsidiary, Panacea Biotec Pharma, introduced baby diapers and wipes under the brand name 'NikoMom'. This launch signified the company's entry into the baby care market.

- October 2024: Nestle India has announced plans to introduce 14 new variants of its Cerelac baby food line, excluding refined sugar. This initiative aims to address global concerns about added sugars in its current Cerelac products.

India Baby Care Products Market Report Scope

Baby care products can be defined as products intended to be utilized on infants or children.

India's baby care products market is segmented by type and distribution channel. By type, it is segmented into baby skin care, baby hair care, baby toiletries, and baby food and beverages. By distribution channel, the market studied is segmented into hypermarkets/supermarkets, pharmacies/drug stores, convenience stores, online retailing, and other distribution channels.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Baby Skin Care | |

| Baby Hair Care | |

| Baby Toiletries | Bath and Fragrances |

| Diapers and Wipes | |

| Baby Food and Beverages |

By Nature

| Organic/Natural |

| Conventional/Synthetic |

By Age Group

| Infants (0-1 Year) |

| Toddlers (1-3 Years) |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Baby Skin Care | |

| Baby Hair Care | ||

| Baby Toiletries | Bath and Fragrances | |

| Diapers and Wipes | ||

| Baby Food and Beverages | ||

| By Nature | Organic/Natural | |

| Conventional/Synthetic | ||

| By Age Group | Infants (0-1 Year) | |

| Toddlers (1-3 Years) | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies/Drug Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What is the current value of the India baby care products market?

The India baby care products market size is USD 5.57 billion in 2026.

How fast is the online channel growing for baby care in India?

Online retail sales are advancing at a 12.47% CAGR through 2031, the fastest among all channels.

Which product segment is expanding the quickest?

Baby skin care is the fastest-growing segment, projected at a 12.59% CAGR to 2031.

Why are organic/natural baby products gaining popularity in India?

Urban parents associate chemical-free formulations with safety, and BIS certification assures authenticity, driving a 13.88% CAGR for organic products.

Page last updated on: