Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

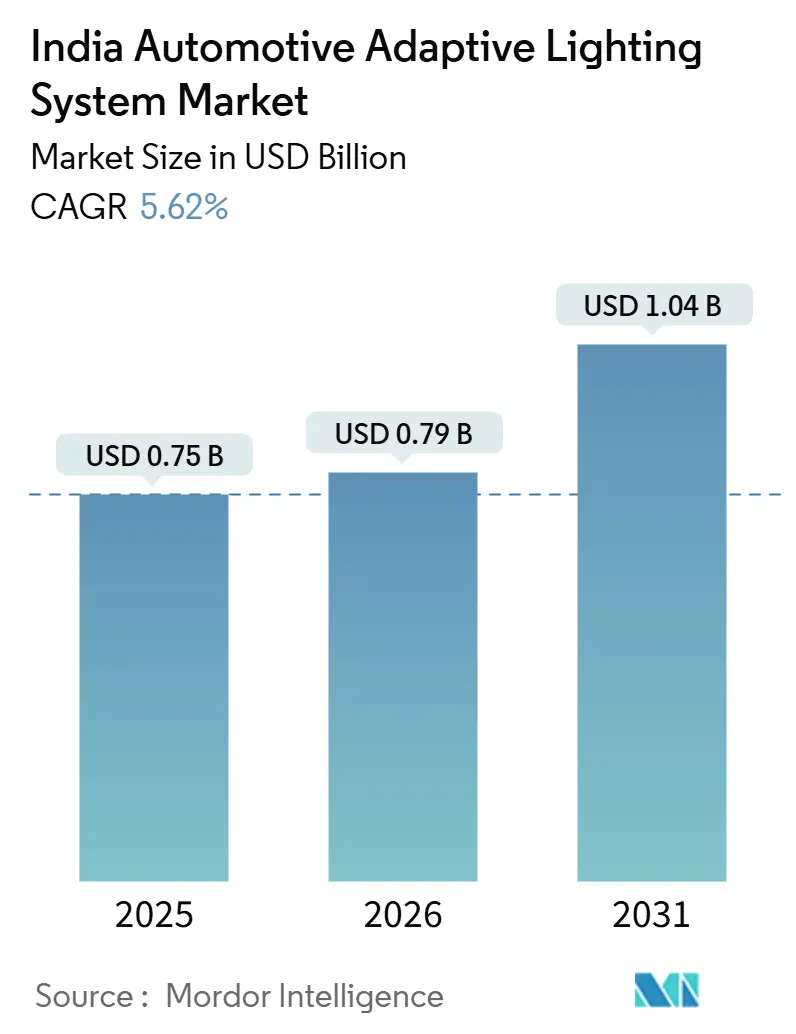

| Base Year Market Size (2025) | USD 0.75 Billion |

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2031) | USD 1.04 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

India Automotive Adaptive Lighting System Market Analysis by ���ϲ�����

The Indian automotive adaptive lighting system market size is expected to increase from USD 0.75 billion in 2025 to USD 0.79 billion in 2026, reaching USD 1.04 billion by 2031, growing at a CAGR of 5.62% over 2026-2031. Recent rule-making, notably the draft AIS-199 photometric standard, is nudging original equipment manufacturers (OEMs) to treat adaptive front lighting as a compliance feature rather than a luxury add-on. Meanwhile, persistent unit-cost pressures confine full-feature systems to premium and upper-mid trims, even as LED die-cost declines slowly narrow the affordability gap. Suppliers are localizing critical sensors and camera modules to qualify for production-linked incentives (PLI) and thereby shorten lead times and mitigate currency exposure. Growth prospects remain tied to OEM electrification roadmaps because energy-efficient lighting helps maximize real-world range, an attribute buyers value as charging infrastructure scales. Competitive intensity is moderate, with five global tier-1 suppliers leveraging established OEM relationships and in-house software stacks to defend share.

Key Report Takeaways

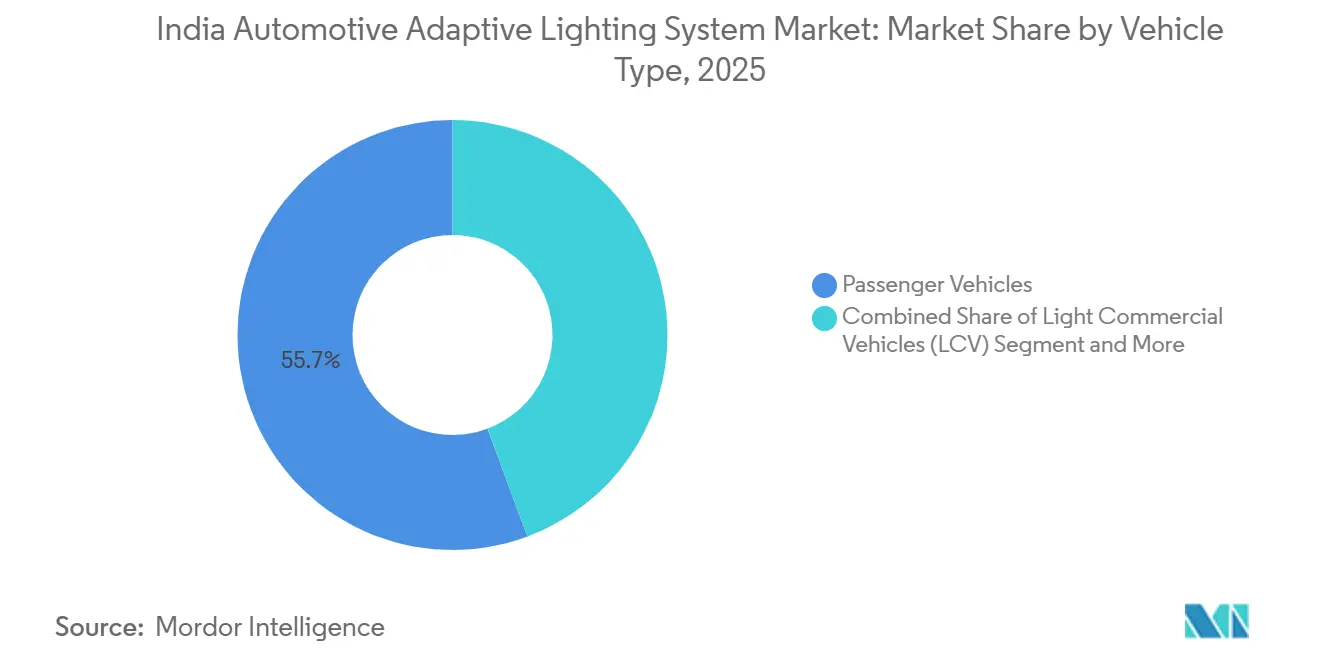

- By vehicle type, passenger vehicles led the India automotive adaptive lighting system market with 55.67% market share in 2025, and the segment is advancing at an 8.47% CAGR through 2031.

- By application, exterior lighting accounted for a 72.87% share of the India automotive adaptive lighting system market size in 2025 and is projected to expand at a 9.77% CAGR through 2031.

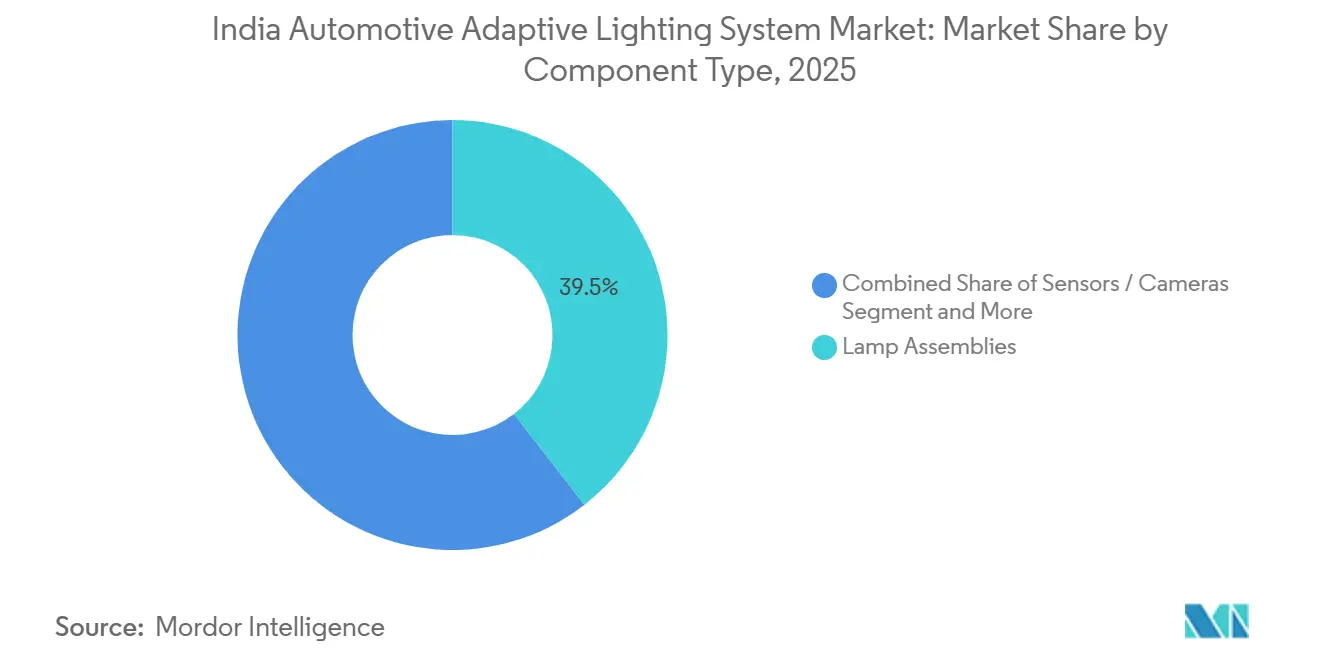

- By component type, lamp assemblies held 39.47% of the India automotive adaptive lighting system market share in 2025; sensors and cameras record the highest projected CAGR at 12.86% through 2031.

- By technology, LED modules commanded 82.99% of the India automotive adaptive lighting system market in 2025, whereas laser lighting is forecasted to grow at a 16.16% CAGR through 2031.

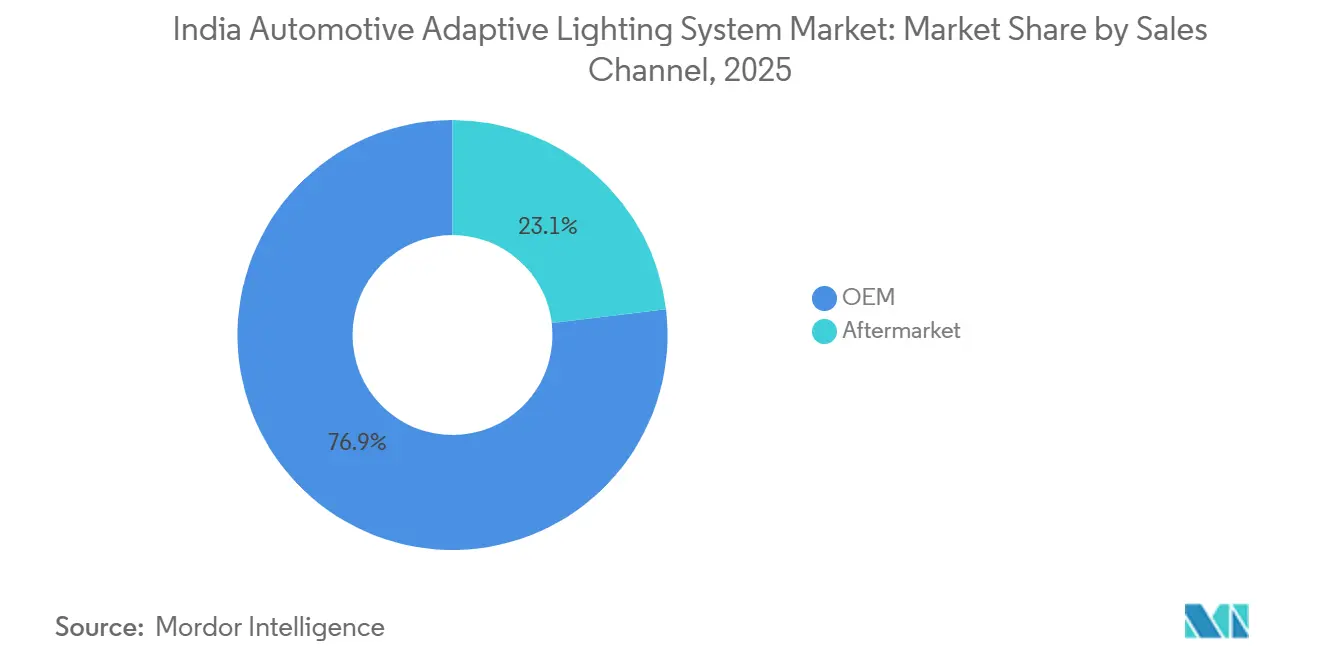

- By sales channel, OEMs captured 76.92% of the India automotive adaptive lighting system market share in 2025 and the aftermarket is rising at a 9.03% CAGR to 2031.

- By functionality, automatic high beam led with 41.45% share of the India automotive adaptive lighting system market size in 2025, but adaptive front lighting is climbing at an 11.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Automotive Adaptive Lighting System Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LED Cost Decline | +1.8% | Maharashtra, Tamil Nadu, Gujarat, Karnataka, Haryana | Medium term (2-4 years) |

| AIS-199 Regulation | +1.5% | Pan-India, with early compliance in Maharashtra, Tamil Nadu, Gujarat | Short term (≤ 2 years) |

| Demand for ADAS Bundle-Features | +1.2% | Delhi NCR, Pune, Chennai, Bangalore (OEM clusters) | Medium term (2-4 years) |

| Growing EV Penetration | +0.9% | Maharashtra, Karnataka, Delhi NCR, Gujarat | Long term (≥ 4 years) |

| Tier-1 Localization Incentives | +0.7% | Maharashtra, Tamil Nadu, Haryana, Gujarat | Medium term (2-4 years) |

| Micro-LED/Pixel ADB Integration | +0.5% | Karnataka, Tamil Nadu (R&D hubs), Maharashtra | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rapid LED Cost Declines Enabling Mid-Segment Adoption

ED headlamp prices have come down sharply as die-size optimization improves yield, allowing OEMs to equip cars with adaptive functions without breaching price ceilings. Indigenous prototypes validated by the Automotive Research Association of India prove that locally engineered LED adaptive modules can meet AIS-127 benchmarks at competitive costs. Added volumes from mid-segment trims improve scale economics for sensor and actuator suppliers. As price sensitivity remains a defining feature of India’s passenger-vehicle buyers, each incremental cost reduction unlocks a broader customer pool. Consequently, mid-segment electrified platforms increasingly specify automatic high-beam as standard.

AIS-199 Regulation Mandating AFS Photometric Standards (2024 Draft)

The 2024 draft standard consolidates illumination norms and references UN R-123, pushing carmakers to add glare-control logic, camera inputs, and adaptive optics to new platforms launched after 2026[1]"Adaptive Front Lighting System (AFLS)", The Automotive Research Association of India, araiindia.com. Tier-1 suppliers that already certify products for Europe can repurpose validated designs, easing homologation. Because the rule applies across vehicle classes, compliance pressure trickles into commercial-vehicle segments by the decade’s end. Export-oriented OEMs value this alignment because a single module can serve multiple regions, reducing engineering overhead. In the short term, AIS-199 effectively makes adaptive lighting mandatory for most new passenger models.

OEM Demand for ADAS Bundle-Features in Low-Budget Vehicles

Carmakers keen to differentiate mid-segment offerings now bundle lane-keep assist, adaptive cruise control, and adaptive lighting on shared sensor suites. Using a single forward-facing camera to power both ADAS and headlamp algorithms spreads component costs and shortens validation cycles. Demand is amplified by rising electric-vehicle penetration because energy-efficient LEDs dovetail with range-optimization goals. OEM interest in bundled safety suites, therefore, accelerates the trickle-down of adaptive lighting to price points once served only by static LED arrays.

Growing EV Penetration Raising Demand for Energy-Efficient Lighting

NITI Aayog targets 30% electric vehicle penetration by 2030, a trajectory that prioritizes low-wattage lighting to conserve battery charge[2]"Unlocking a $200 Billion Opportunity: Electric Vehicles in India", NITI Aayog, niti.gov.in. LEDs draw a fraction of the power of halogen systems, translating to marginal but meaningful range extensions that sway purchase decisions. Fleet operators managing e-buses and last-mile freight are increasingly focused on the total cost of ownership. Meanwhile, adaptive LEDs are proving their worth by extending service life and minimizing downtime. With the charging infrastructure growing at an uneven pace, technologies that enhance distance per charge are becoming strategically vital.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Unit-Cost | -1.5% | Pan-India, particularly in Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Semiconductor Supply-Chain Volatility | -0.8% | Maharashtra, Tamil Nadu, Gujarat (manufacturing hubs) | Short term (≤ 2 years) |

| Fragmented Aftermarket and Warranty-Void | -0.5% | Delhi NCR, Mumbai, Bangalore, Pune (aftermarket clusters) | Medium term (2-4 years) |

| Low Awareness Among Fleet Owners | -0.3% | Pan-India, particularly in LCV and MHCV segments | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Unit-Cost Limits Mass-Market Penetration

Full adaptive front-lighting assemblies cost well, forming a steep barrier for budget vehicles that dominate sales. Import dependence for sensor ASICs keeps bills of materials elevated, exposing OEMs to currency swings. Tier-1 suppliers are testing modular approaches that scale features with trim level, but fragmented volumes dilute cost savings. Until controller and camera prices drop through local fabrication, adaptive lighting remains a premium signifier rather than a mainstream safety norm.

Semiconductor Supply-Chain Volatility

Controller ICs and image sensors face allocation constraints, forcing OEMs to divert scarce chips toward powertrain or infotainment modules. Local fabrication projects will take years to reach automotive-grade yields, leaving the sector vulnerable to geopolitics and logistics shocks. Tier-1s hedge by dual-sourcing and redesigning boards for pin-compatible parts, but these efforts extend validation timelines and tie up engineering bandwidth.

Segment Analysis

By Vehicle Type: Passenger Cars Anchor Early Adoption

Passenger cars dominated the Indian automotive adaptive lighting system market share in 2025, holding 55.67% and growing at an 8.47% CAGR, largely because private buyers value the safety features and styling cues that adaptive headlamps offer. Regulatory deadlines tied to AIS-199 spur OEMs to launch compliant passenger platforms first, leaving trucks and buses on legacy setups. Electrified passenger cars further reinforce uptake, as low-wattage LEDs help extend driving range.

Supplier roadmaps, therefore, concentrate engineering resources on car-specific beam-shaping algorithms and compact sensor clusters. Commercial vehicles trail because fleet operators scrutinize return on investment more tightly. Nonetheless, rising night-haul logistics and stricter insurance norms may pull adaptive high beam into select LCV fleets sooner than heavy trucks. Over time, economies of scale achieved in the passenger domain are expected to lower cost barriers, enabling a gradual spill-over into goods carriers and intercity buses.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Exterior Systems Capture Spending

Exterior lighting accounts for the majority of the Indian automotive adaptive lighting system market because headlamps sit at the intersection of safety regulations and consumer visibility needs. In 2025, the category accounted for 72.87% of total value and is set to post the fastest expansion, clocking a 9.77% CAGR through 2031 as adaptive front lighting and dynamic bending modules move down-segment. Interior applications such as ambient cabin lighting grow from a lower base, anchored mostly in premium vehicles where personalization outweighs strict safety calculus. Suppliers, therefore, direct most engineering budgets into forward-lighting optics, sensors, and beam-forming software.

The exterior focus also reflects higher per-unit revenue, as complete headlamp assemblies integrate actuators, ECUs, and LEDs. Interior modules remain important for brand differentiation, yet they lack regulatory tailwinds, limiting their penetration. Over time, synchronized cabin-exterior light sequences may spur incremental demand once centralized body-domain controllers become common. For the forecast period, however, exterior headlamps remain the clear volume and value driver within adaptive lighting portfolios.

By Component Type: Sensors and Cameras Accelerate

Lamp assemblies still anchor bill-of-materials value, holding 39.47% share in 2025, but sensors and cameras are the fastest-growing elements, recording a 12.86% CAGR between 2026 and 2031. Their rapid trajectory reflects convergence with driver-assistance stacks, enabling a single forward imager to support lane-keeping, traffic-sign recognition, and beam-shaping algorithms. Controllers, actuators, and harnesses round out the architecture but expand more modestly because centralized vehicle computers absorb dedicated lighting ECUs. As image-sensor localization unlocks PLI incentives, suppliers co-locate camera lines with lamp plants to cut logistics overhead.

This migration of value toward intelligent sensing shifts competitive advantage toward firms that own perception software and silicon design. Lamp-housing specialists hedge by adding actuator and thermal-management capabilities, ensuring relevance even as LED die costs fall. Long term, pixelated micro-LED arrays could further tilt value toward software, but in the medium horizon, discrete cameras remain the pivotal differentiator. For now, robust growth in sensing hardware underpins the component landscape.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: LED Dominates, Laser Surges

LED modules account for 82.99% of the Indian automotive adaptive lighting system market, benefiting from energy efficiency, longevity, and fast modulation that align with AIS-199 photometric norms. Laser lighting, while nascent, is the fastest-advancing technology at a 16.16% CAGR to 2031, propelled by premium electric sedans that demand ultra-long-throw beams. Xenon and halogen options linger only on legacy platforms slated for phase-out once next-generation models launch post-2026. Supplier R&D, therefore, centers on LED thermal management and pixelated beam control, both of which are necessary for autonomous-ready illumination.

Laser’s steep growth trajectory stems from its potential to project high-definition patterns that support V2X communication and advanced driver cues. Thermal challenges and high unit costs currently confine it to luxury imports, but localized subsystem manufacture could lower barriers by decade-end. In the interim, incremental LED innovations, such as multi-pixel adaptive high beam, bridge the performance gap for mass-market vehicles. Accordingly, LEDs remain the workhorse, with laser positioned as an aspirational upgrade path.

By Sales Channel: OEM Installations Prevail

OEM channels accounted for 76.92% of the Indian automotive adaptive lighting system market share in 2025, reflecting factory-fit integration of sensors, ECUs, and calibrated optics. The aftermarket segment, however, is the fastest mover, growing at a 9.03% CAGR through 2031 as plug-and-play kits and standardized CAN interfaces reduce installation complexity. Warranty concerns and calibration demands still cap retrofit volumes, but falling component prices entice owners to upgrade older cars once factory cover lapses. Tier-1 suppliers experiment with certified accessory programs to capture this latent demand without cannibalizing OE contracts.

In urban clusters, independent workshops increasingly stock automatic high-beam kits that require minimal coding. Full adaptive front-lighting retrofits remain rare because they need dynamic steering and speed inputs, but modular software unlocks could change that landscape. OEM dominance, therefore, persists in the short term, yet a maturing aftermarket ecosystem promises supplemental growth, particularly for vehicles beyond their three-year maintenance window.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Functionality: Automatic High Beam Opens Doors

Automatic high beam retained the largest share of 41.45% in 2025, yet adaptive front lighting is the fastest-growing feature with an 11.86% CAGR through 2031. The laddered progression, from simple on-off toggling to fully dynamic beam shaping, lets OEMs calibrate cost versus benefit across trim levels. Dynamic bending and cornering lights occupy the middle ground, offering incremental safety improvements without full sensor fusion. As centralized domain controllers proliferate, feature upgrades become software-centric, allowing post-sale activation via over-the-air updates.

This functionality spectrum aligns with consumer willingness to pay: entry seekers accept basic glare mitigation, while premium buyers demand pixel-level beam precision. Suppliers craft modular architectures so the same hardware supports multiple tiers, unlocking scale economies. Over time, policy-driven safety scores may elevate adaptive front lighting to mainstream status, mirroring the trajectory of airbags and ABS in earlier decades.

Geography Analysis

Pune's dense cluster of OEM plants and engineering centers positions Maharashtra as the hub for India's automotive adaptive lighting system market. The close proximity of lamp manufacturers, sensor fabs, and vehicle assembly lines not only reduces logistics costs but also accelerates design iterations. While the national PLI program lays the groundwork, state-level incentives further entice global tier-1s to pursue brownfield expansions in the region.

Tamil Nadu follows closely, leveraging the “Automotive Corridor” that stretches from Chennai to Kancheepuram. Port access simplifies component import-export, suiting multinational suppliers that feed Southeast Asian plants. The region also boasts a skilled electronics workforce, which supports algorithm development and end-of-line calibration activities. Karnataka rounds out the southern triangle by providing software talent concentrated in Bangalore’s tech parks, a boon for perception-algorithm prototyping.

Gujarat and Haryana anchor northern and western nodes. Sanand’s vendor park serves Maruti Suzuki and Tata Motors, making it an attractive base for new sensor assembly lines. Haryana’s Manesar–Gurugram belt focuses on mid-priced passenger cars, a segment ripe for tiered adaptive lighting offerings. Collectively, these five states capture the lion’s share of current production, while Tier-2 cities await feeder-plant investments aimed at boosting local value addition beyond 50%

Competitive Landscape

Five global giants - Koito, Valeo, HELLA, Magneti Marelli, and Stanley - are at the forefront of the market, seamlessly integrating lamps, sensors, and beam-forming software into comprehensive modules. These companies leverage their deep expertise in platform-wide ECU harmonization and long-standing relationships with OEMs to maintain their dominance. Their ability to deliver turnkey solutions tailored to diverse automotive platforms further strengthens their market position. Additionally, their extensive R&D capabilities and global supply chain networks enable them to stay ahead of emerging technological trends. Moves like Valeo's significant expansion in India highlight the capital-intensive strategies essential for maintaining a competitive edge in this evolving market landscape.

Domestic challengers like Lumax, Uno Minda, and Varroc leverage cost competitiveness and PLI incentives to win localized programs. Joint ventures deliver technology transfer, as evidenced by the Tata AutoComp-Ichikoh tie-up that bundles optics expertise with domestic manufacturing heft. Yet gaps remain in high-resolution sensor design and pixel-level beam algorithms, areas where global incumbents still outpace local peers.

White-space segments include retrofits for the vast existing vehicle parc and adaptive systems tailored for two-wheelers, a category in which India is the world’s largest producer. Players that combine smart-sensor cost downs with rugged lamp housings tailored for motorcycles could unlock new volume pools. Intellectual-property barriers remain moderate, allowing fast followers with agile software teams to compete on differentiated value rather than hardware scale alone.

India Automotive Adaptive Lighting System Industry Leaders

-

HELLA KGaAHueck& Co.

-

Koito Manufacturing Co. Ltd

-

Valeo SA

-

Magneti Marelli SpA

-

Stanley Electric Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: Marelli and Motherson have launched a new automotive lighting manufacturing facility in Sanand, Gujarat. This marks an expansion of their joint venture, Marelli Motherson Lighting India (MMLI). The new facility will produce high-performance exterior lighting systems and debut several lighting technologies in India for the very first time.

- January 2026: Neolite ZKW Lightings Limited opened a new manufacturing facility for automotive lighting products in Pune, Maharashtra. The plant commenced operations in December 2025.

- April 2025: Valeo and Appotronics forged a strategic partnership to develop a next-generation front lighting system. These cutting-edge solutions aim to bolster adaptive lighting (ADB) functionalities in vehicles, thereby enhancing road safety and catering to drivers' growing preferences for comfortable lighting and entertainment features.

India Automotive Adaptive Lighting System Market Report Scope

The Indian Automotive Adaptive Lighting System market is segmented by vehicle type, application, component type, technology, sales channel, and functionality. By Vehicle Type, the market is segmented into Passenger, Light Commercial Vehicles, and Medium & Heavy-duty Commercial Vehicles. By Application, the market is segmented into Exterior Lighting and Interior Lighting. By Component Type, the market is segmented into Controllers, Sensors/Cameras, Lamp Assemblies, Actuators, and Others. By Technology, the market is segmented into LED, Xenon/HID, Halogen, and Laser Light. By Sales Channel, the market is segmented into OEM and Aftermarket. By Functionality, the market is segmented into Automatic High Beam, Dynamic Bending Lights, Cornering Lights, and Adaptive Front Lighting Systems. Market forecasts are provided in terms of Value (USD).

By Vehicle Type

| Passenger Vehicles |

| Light Commercial Vehicles (LCV) |

| Medium and Heavy Commercial Vehicles (MHCV) |

By Application

| Exterior Lighting |

| Interior Lighting |

By Component Type

| Controllers |

| Sensors / Cameras |

| Lamp Assemblies |

| Actuators |

| Others |

By Technology

| LED |

| Xenon / HID |

| Halogen |

| Laser Lighting |

By Sales Channel

| OEM |

| Aftermarket |

By Functionality

| Automatic High Beam |

| Dynamic Bending Light |

| Cornering Lights |

| Adaptive Front Lighting |

| By Vehicle Type | Passenger Vehicles |

| Light Commercial Vehicles (LCV) | |

| Medium and Heavy Commercial Vehicles (MHCV) | |

| By Application | Exterior Lighting |

| Interior Lighting | |

| By Component Type | Controllers |

| Sensors / Cameras | |

| Lamp Assemblies | |

| Actuators | |

| Others | |

| By Technology | LED |

| Xenon / HID | |

| Halogen | |

| Laser Lighting | |

| By Sales Channel | OEM |

| Aftermarket | |

| By Functionality | Automatic High Beam |

| Dynamic Bending Light | |

| Cornering Lights | |

| Adaptive Front Lighting |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is driving OEM interest in adaptive front-lighting for mid-segment cars?

Draft AIS-199 rules make glare control mandatory after 2026 and falling LED costs let carmakers add adaptive features without breaching price ceilings.

Which Indian states host most adaptive lighting production?

Maharashtra, Tamil Nadu, Gujarat, Karnataka and Haryana house the bulk of tier-1 plants and R&D centers.

Why do LED modules dominate over halogen and xenon in new Indian vehicles?

LEDs offer superior energy efficiency, faster beam modulation and easier compliance with photometric standards, all at improving cost points.

How does the PLI Auto Components Scheme influence supplier strategy?

It provides sales-linked incentives for 50% local value addition, prompting global and domestic firms to localize sensor and actuator lines.