Immunoglobulin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

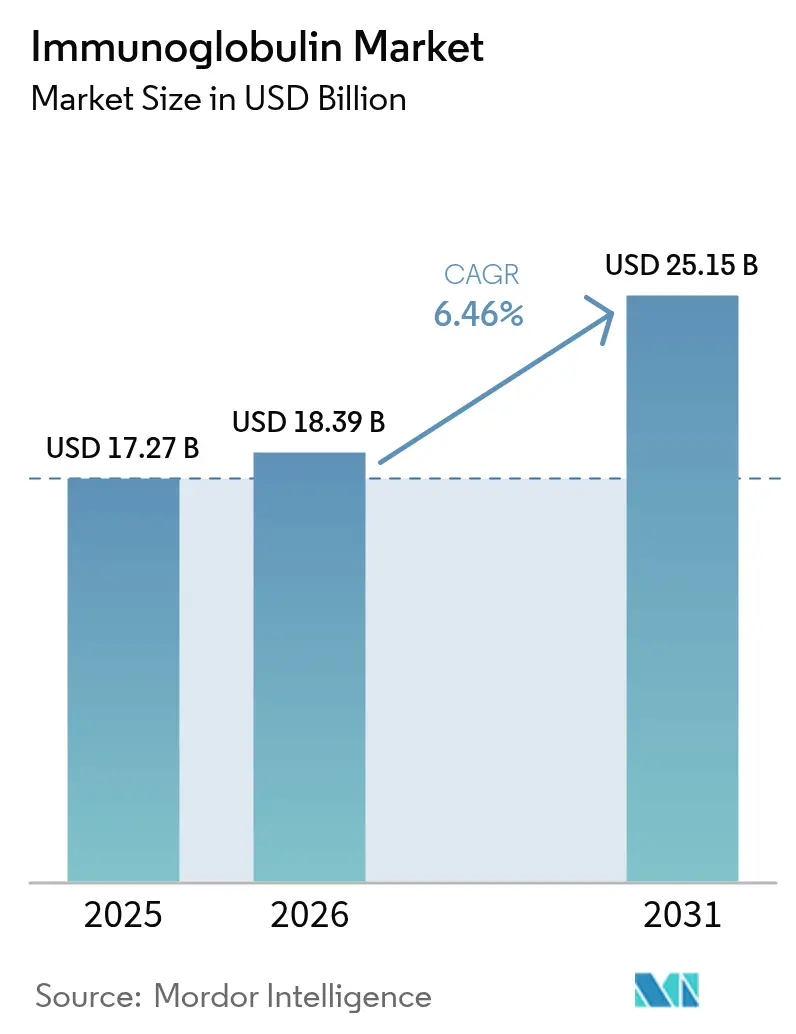

| Market Size (2026) | USD 18.39 Billion |

| Market Size (2031) | USD 25.15 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Immunoglobulin Market Analysis by ���ϲ�����

The Immunoglobulin Market size is projected to expand from USD 17.27 billion in 2025 and USD 18.39 billion in 2026 to USD 25.15 billion by 2031, registering a CAGR of 6.46% between 2026 to 2031.

Sustained demand stems from early genetic diagnosis of primary immunodeficiency, payer-backed migration to home-based treatment, and high-concentration subcutaneous formulations that shorten infusion time. Vertical integration of plasma collection protects supply yet raises capital intensity, while AI-enabled donor recruitment is lifting center utilization in North America and Europe. On the competitive front, Takeda, CSL Behring, and Grifols are expanding fractionation footprints ahead of anticipated neurology-driven volume spikes. Meanwhile, Fc-engineered monoclonal antibodies threaten intravenous immunoglobulin’s share in select autoimmune indications but remain cost-constrained niche options.

Key Report Takeaways

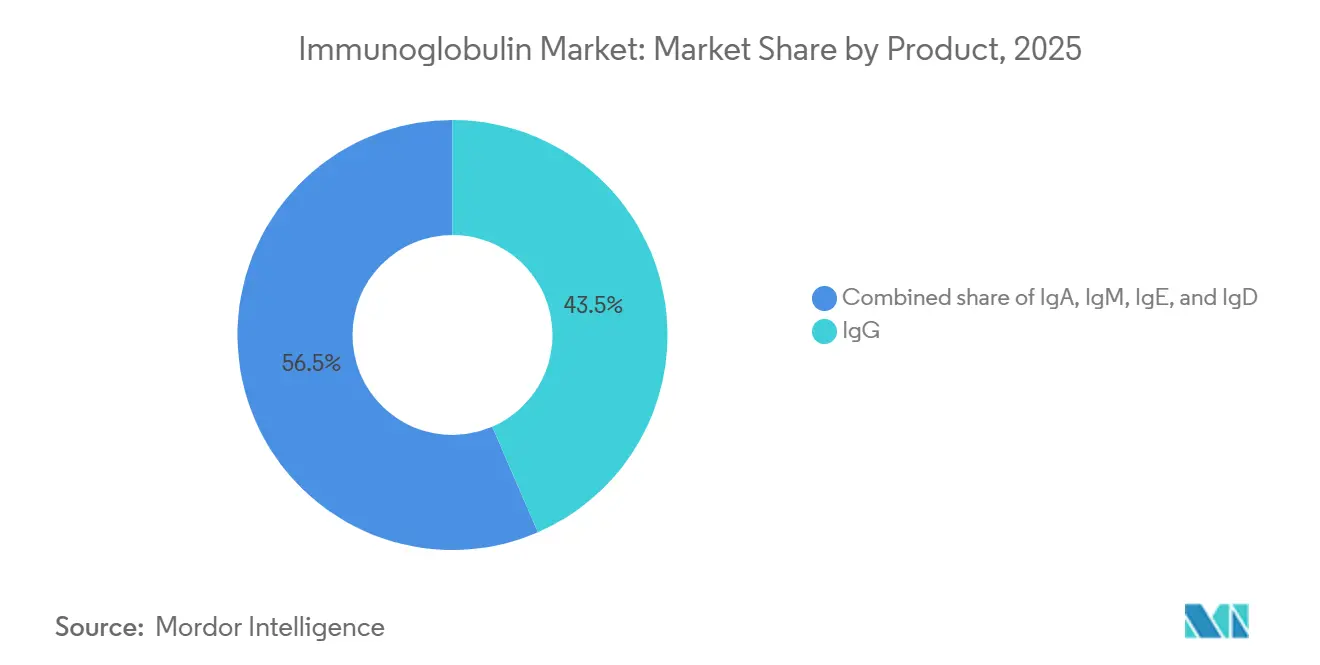

- By product category, IgG led with 43.55% of Immunoglobulin market share in 2025. IgE formulations are forecast to expand at a 9.85% CAGR through 2031.

- By mode of delivery, intravenous immunoglobulin accounted for 64.53% share in 2025. Subcutaneous immunoglobulin is advancing at a 10.75% CAGR to 2031.

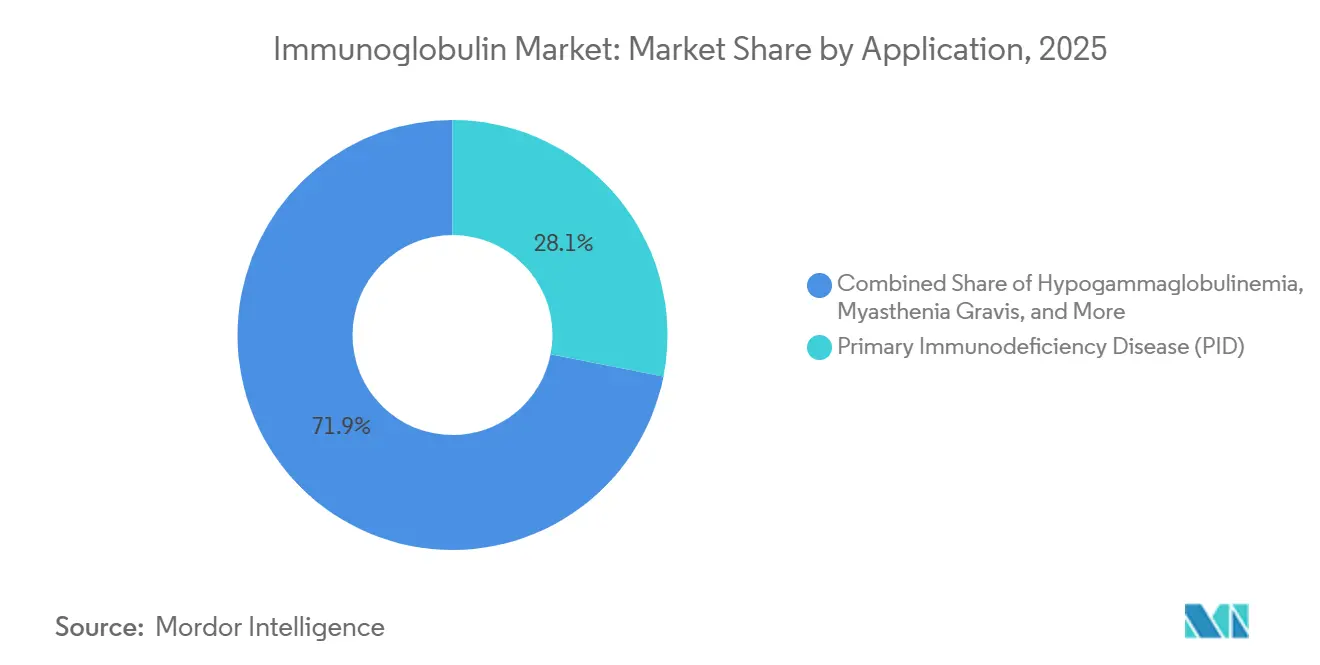

- By application, primary immunodeficiency disease captured 28.15% revenue share in 2025. Chronic inflammatory demyelinating polyneuropathy is the fastest-growing indication at a 10.82% CAGR to 2031.

- By distribution channel, hospital pharmacies held 64.52% share in 2025. Online and home-infusion providers are rising at a 9.12% CAGR over the forecast period.

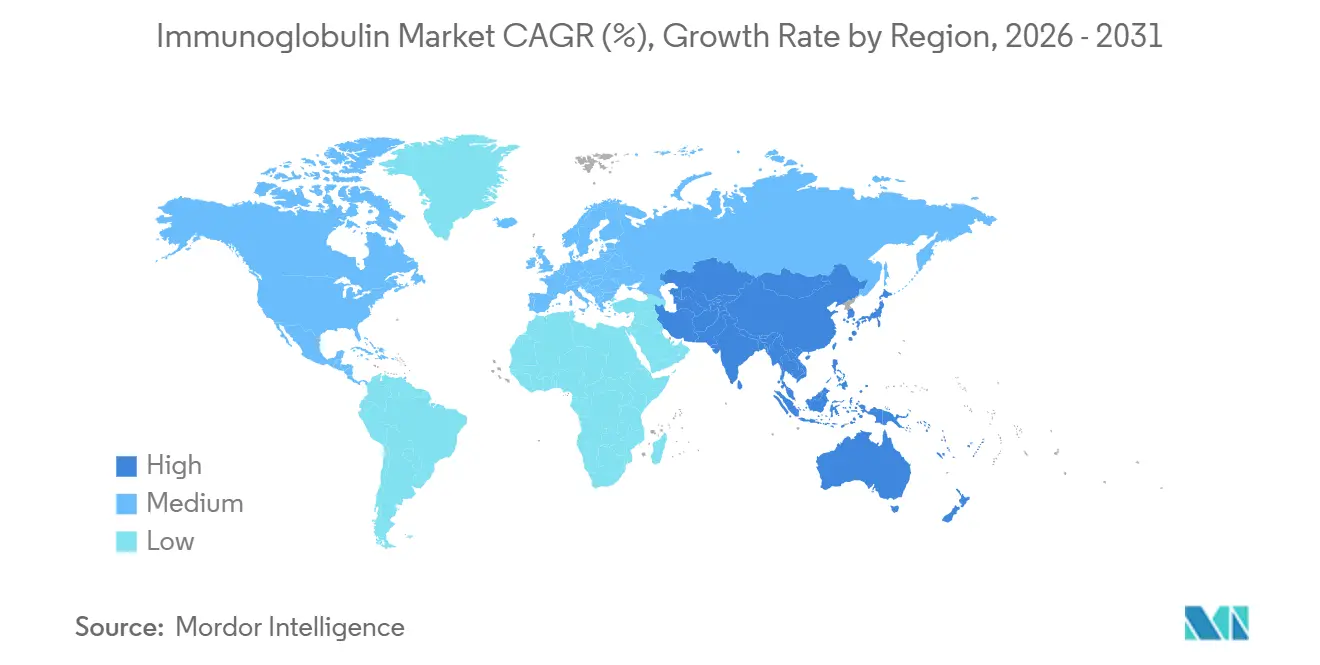

- By geography, North America led with 44.55% revenue share in 2025. Asia-Pacific is set to grow at a 7.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Immunoglobulin Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of primary immunodeficiency diseases | +1.2% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Growing IVIG use in neurology | +1.5% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Expansion of global plasma-fractionation capacity | +1.8% | China, Japan, spill-over to North America | Long term (≥ 4 years) |

| Favorable reimbursement and diagnostics uptake | +0.9% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| AI-driven plasma-supply optimization | +0.7% | Pilot centers in North America and Europe | Medium term (2-4 years) |

| On-body high-concentration SCIG devices | +1.1% | Japan, Germany, United States | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rising Prevalence of Primary Immunodeficiency Diseases

Newborn screening and next-generation sequencing are revealing 40% more primary immunodeficiency cases than earlier estimates, expanding the eligible patient pool for lifelong replacement therapy. Insurance mandates in the United States and Western Europe cut time-to-diagnosis from eight years to under 18 months, yet Asia-Pacific lags by up to seven years despite China’s pilot programs that may add 15,000-20,000 new diagnoses annually by 2029. Earlier detection lowers per-dose volumes but extends treatment duration, magnifying cumulative plasma demand. The resulting strain reinforces manufacturer investment in collection centers even as reimbursement shifts care out of hospitals. Sustaining this driver beyond 2028 will depend on ongoing declines in genetic testing costs and parallel reimbursement expansion.

Growing IVIG Use in Neurology (CIDP, GBS, MMN)

FDA guideline updates in early 2025 positioned IVIG ahead of corticosteroids for chronic inflammatory demyelinating polyneuropathy, Guillain-Barré syndrome, and multifocal motor neuropathy. Japan’s December 2024 approval of HYQVIA enabled monthly home dosing that bypasses intravenous access, accelerating neurologist uptake[1]Shohei Tanaka, “HYQVIA Gains CIDP Indication in Japan,” Takeda Pharmaceutical Company, takeda.com. Off-label adoption in stiff-person syndrome and autoimmune encephalitis is broadening demand, though high doses intensify plasma-supply competition and elevate annual therapy costs to USD 80,000-120,000. European payers now require head-to-head data versus rituximab, which could temper growth after 2028. Near-term, neurology adds 1.5 percentage points to the Immunoglobulin market CAGR.

Expansion of Global Plasma-Fractionation Capacity

Takeda’s USD 670 million Osaka expansion will deliver 1.2 million liters of new capacity by 2027, cutting Japan’s reliance on North American imports by 35%. Shanghai RAAS and Hualan Biological gained export-quality certifications, allowing them to pivot toward higher-margin IgG production for domestic demand. While Asia-Pacific plants operate below capacity today, commissioning and GMP validation require four to six years, delaying meaningful relief until after 2028. In the interim, allocation shortages remain likely if neurology uptake outpaces supply additions.

On-Body High-Concentration SCIG Devices for Home Therapy

Wearable pumps delivering 20% immunoglobulin solutions have trimmed infusion time below 60 minutes and eliminated hospital visits for many patients. Health-system savings of USD 25,000-35,000 per patient annually underpin payer incentives, yet upfront device costs of USD 3,000-5,000 slow adoption, especially among elderly users uncomfortable with self-injection. Regulatory guidance for combination products is still emerging, causing manufacturers to navigate country-specific approval pathways. Despite these hurdles, SCIG technology is poised to accelerate site-of-care migration and improve adherence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost and reimbursement gaps | -0.8% | Latin America, Middle East, rural Asia | Short term (≤ 2 years) |

| Stringent donor-screening regulations | -0.5% | Divergent FDA, EMA, PMDA frameworks | Long term (≥ 4 years) |

| Fc-engineered monoclonal antibody substitutes | -0.6% | North America, Europe | Medium term (2-4 years) |

| Carbon-intensity scrutiny of cold-chain logistics | -0.3% | Europe first, then North America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High Therapy Cost & Reimbursement Gaps

Annual immunoglobulin therapy costs range from USD 50,000 for maintenance immunodeficiency to USD 120,000 for high-dose neurology, leaving most patients in Latin America and parts of Asia without coverage[2]Laura Gómez, “Reimbursement Timelines in Argentina’s Sistema Único de Reembolsos,” Ministerio de Salud de la Nación, argentina.gob.ar. Argentina’s reimbursement queue stretches up to nine months, and Brazil rationed supply during 2024-2025 shortages. Because 70% of manufacturing expense arises before final fill-finish, price cuts are structurally difficult. Payers in developed markets now mandate home infusion to shave 30-40% off facility fees, but the underlying plasma cost persists, deterring new capacity investment.

Fc-Engineered Monoclonal Antibodies as Therapeutic Substitutes

Efgartigimod won FDA approval in 2024 for generalized myasthenia gravis and is in late-stage trials for other autoimmune indications. By accelerating pathogenic IgG clearance without plasma inputs, it removes supply constraints; yet its USD 150,000-180,000 price caps uptake to refractory cases. Substitution risk through 2031 is therefore limited to roughly one-fifth of addressable volume, but continued success of similar biologics could erode intravenous immunoglobulin’s foothold in neurologic care over the long term.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: IgG Anchors Revenue, IgE Gains Momentum

IgG held 43.55% of Immunoglobulin market share in 2025 on the strength of entrenched use across immunodeficiency and hematologic disorders. High-concentration IgG formulations such as Cuvitru reduce infusion time by half, boosting home-based adherence. IgE therapies, though nascent, are projected to outpace the broader Immunoglobulin market at a 9.85% CAGR on emerging eosinophilic applications. IgA and IgM remain niche but benefit from selective IgA deficiency cohorts that cannot tolerate standard products. Limited regulatory clarity for IgE endpoints tempers near-term launch certainty.

Manufacturers with advanced purification can command premium pricing for stable 20% products, yet hyaluronidase co-formulation adds USD 500-800 per dose, complicating payer negotiations. Regulatory lag for novel IgE and IgM programs may delay revenue until after 2029, but pipeline diversity positions the product mix for gradual broadening beyond IgG dominance.

By Mode of Delivery: SCIG Disrupts IVIG Hegemony

Intravenous immunoglobulin retained 64.53% revenue share in 2025 thanks to decades of clinician familiarity and hospital infusion infrastructure. Nevertheless, subcutaneous immunoglobulin is forecast to expand at 10.75% CAGR, reflecting payer push to lower facility costs and patient preference for at-home convenience. The Immunoglobulin market size linked to SCIG is poised to grow steadily as device interoperability standards mature.

Reimbursement misalignment slows transition: U.S. Medicare pays 20-30% less for subcutaneous products, and prior-authorization resets add bureaucracy. Patient self-training costs and real-time temperature monitoring further squeeze margins for specialty pharmacies. Despite these headwinds, weekly self-administration and lower adverse-event incidence support ongoing mode-shift momentum.

By Application: CIDP Outpaces Legacy Indications

Primary immunodeficiency retained 28.15% revenue share in 2025, but chronic inflammatory demyelinating polyneuropathy is steering the fastest growth at 10.82% CAGR. FDA guidance positioning IVIG as first-line therapy elevated neurological demand and widened dosing schedules. Myasthenia gravis faces competition from efgartigimod, pressuring IVIG growth in that subset.

Guillain-Barré and multifocal motor neuropathy create acute demand spikes that stretch plasma allocations. Hypogammaglobulinemia growth remains moderate yet stable. As neurology’s share rises, per-patient gram utilization lifts the Immunoglobulin market size disproportionately, straining fractionation capacity and distribution logistics.

By Distribution Channel: Home Infusion Captures Share

Hospital pharmacies commanded 64.52% of sales in 2025, but online and home-infusion providers are climbing at 9.12% CAGR. Payers realize 30-40% cost savings by shifting stable patients out of hospital suites, reinforcing SCIG adoption. Specialty pharmacies sit between channels, serving rural areas lacking logistics infrastructure.

Cold-chain delivery at 2-8 °C costs USD 150-300 per shipment and no-show waste erodes profitability. Tighter FDA temperature-excursion guidance will require IoT trackers, adding 10-15% to distribution costs. Nonetheless, embedded nurse support and digital adherence tools position home-infusion networks to capture incremental share as self-administration confidence grows.

Geography Analysis

North America remained the largest regional contributor with 44.55% revenue share in 2025 on unrivaled per-capita usage and over 900 licensed plasma centers. Growth is moderating to mid-single digits as donor saturation and payer pressure constrain expansion. Europe follows, where EMA’s 2024 pathogen-safety upgrade lengthened batch-release cycles by up to six weeks and lifted spot prices 15-20%[3]Isabella Rossi, “EMA Pathogen-Safety Regulations 2024,” European Medicines Agency, ema.europa.eu.

Asia-Pacific is the fastest-growing territory at 7.72% CAGR, propelled by China’s new export-quality certifications and Japan’s CIDP-focused HYQVIA launch. India’s Immunoglobulin market faces infrastructure and affordability gaps, limiting rural reach. Australia and South Korea track mature-market trends at 4-5% growth while expanding newborn screening.

South America and the Middle East trail amid funding constraints, though Gulf Cooperation Council countries are widening rare-disease budgets. Supply rationing in Brazil and Argentina underscores cost barriers and justifies manufacturers’ vertical-integration push. Africa’s demand is small but rising with concentrated initiatives in South Africa and Nigeria to address severe combined immunodeficiency.

Competitive Landscape

The Immunoglobulin market is moderately concentrated: the top five players—CSL Behring, Takeda, Grifols, Octapharma, and Baxter—account for a significant share of global revenue. Each operates extensive plasma-collection networks, with CSL’s fleet topping 300 centers worldwide. Takeda’s Osaka upgrade adds 1.2 million liters of capacity by 2027, while CSL’s Kankakee, Illinois, site will add 800,000 liters in 2025.

AI-based donor scheduling boosts utilization 12-18%, an edge incumbents are scaling quickly. Regional champions like Shanghai RAAS focus on domestic Asia-Pacific demand, insulated by limited cross-border plasma flows. Absence of biosimilar pathways preserves pricing but invites scrutiny from payers seeking alternatives; monoclonal antibodies such as efgartigimod offer the first credible non-plasma substitute albeit at premium cost.

Subcutaneous innovation is a competitive hotspot: HYQVIA’s Japanese label extension validated high-concentration home dosing, prompting rivals to accelerate similar programs. Smaller firms including ADMA Biologics pursue hyper-immune niches that command 2-3× revenue per liter but face scale constraints. Harmonized FDA-EMA-PMDA safety standards shorten global launch lag to under two years, favoring multiregional players equipped for simultaneous filings.

Immunoglobulin Industry Leaders

Baxter International Inc.

CSL Behring

Grifols S.A.

Takeda Pharmaceutical Co.

Octapharma AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Kedrion Biopharma secured FDA approval for QIVIGY 10% IVIG for adult primary humoral immunodeficiency.

- June 2025: The FDA cleared Takeda’s GAMMAGARD LIQUID ERC, the first low-IgA ready-to-use 10% IVIG for patients aged two and older with primary immunodeficiency.

Global Immunoglobulin Market Report Scope

As per the scope of the report, immunoglobulin, also known as an antibody, is a protein produced by plasma cells and other lymphocytes. It is a complex entity that exerts immunomodulatory effects on various components of the immune system. It is obtained from blood by fractionation and purified for therapeutic and non-therapeutic applications.

The immunoglobulin market is segmented by product into IgG, IgA, IgM, IgE, and IgD. By mode of delivery, the market is categorized into intravenous (IVIG), subcutaneous (SCIG), and intramuscular. Based on application, the market includes hypogammaglobulinemia, primary immunodeficiency disease (PID), chronic inflammatory demyelinating polyneuropathy (CIDP), myasthenia gravis, immune thrombocytopenia purpura (ITP), and other applications. By distribution channel, the market is divided into hospital pharmacies, specialty/retail pharmacies, and online & home-infusion providers. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the abovementioned segments.

| IgG |

| IgA |

| IgM |

| IgE |

| IgD |

| Intravenous (IVIG) |

| Subcutaneous (SCIG) |

| Intramuscular |

| Hypogammaglobulinemia |

| Primary Immunodeficiency Disease (PID) |

| Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) |

| Myasthenia Gravis |

| Immune Thrombocytopenia Purpura (ITP) |

| Other Applications |

| Hospital Pharmacies |

| Specialty / Retail Pharmacies |

| Online & Home-Infusion Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | IgG | |

| IgA | ||

| IgM | ||

| IgE | ||

| IgD | ||

| By Mode of Delivery | Intravenous (IVIG) | |

| Subcutaneous (SCIG) | ||

| Intramuscular | ||

| By Application | Hypogammaglobulinemia | |

| Primary Immunodeficiency Disease (PID) | ||

| Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) | ||

| Myasthenia Gravis | ||

| Immune Thrombocytopenia Purpura (ITP) | ||

| Other Applications | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty / Retail Pharmacies | ||

| Online & Home-Infusion Providers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Immunoglobulin market?

The Immunoglobulin market size reached USD 17.27 billion in 2025 and is on track for USD 18.39 billion in 2026.

How fast will global Immunoglobulin demand grow over the next five years?

Demand is projected to rise at a 6.46% CAGR from 2026 to 2031 as diagnostics broaden and home infusion gains traction.

Which product class leads sales?

IgG accounts for 43.55% of revenue, far ahead of other immunoglobulin isotypes.

Why is subcutaneous delivery gaining share?

High-concentration formulations and wearable pumps let patients self-administer at home, cutting facility costs by up to 40%.

Which region will post the fastest growth?

Asia-Pacific is forecast to expand at 7.72% CAGR thanks to China's new fractionation capacity and Japans neurology approvals.

Are monoclonal antibodies a real threat to IVIG?

Fc-engineered antibodies like efgartigimod can replace IVIG in select autoimmune diseases but currently cost 30-50% more, limiting near-term impact.

Page last updated on: