Hydrochloric Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

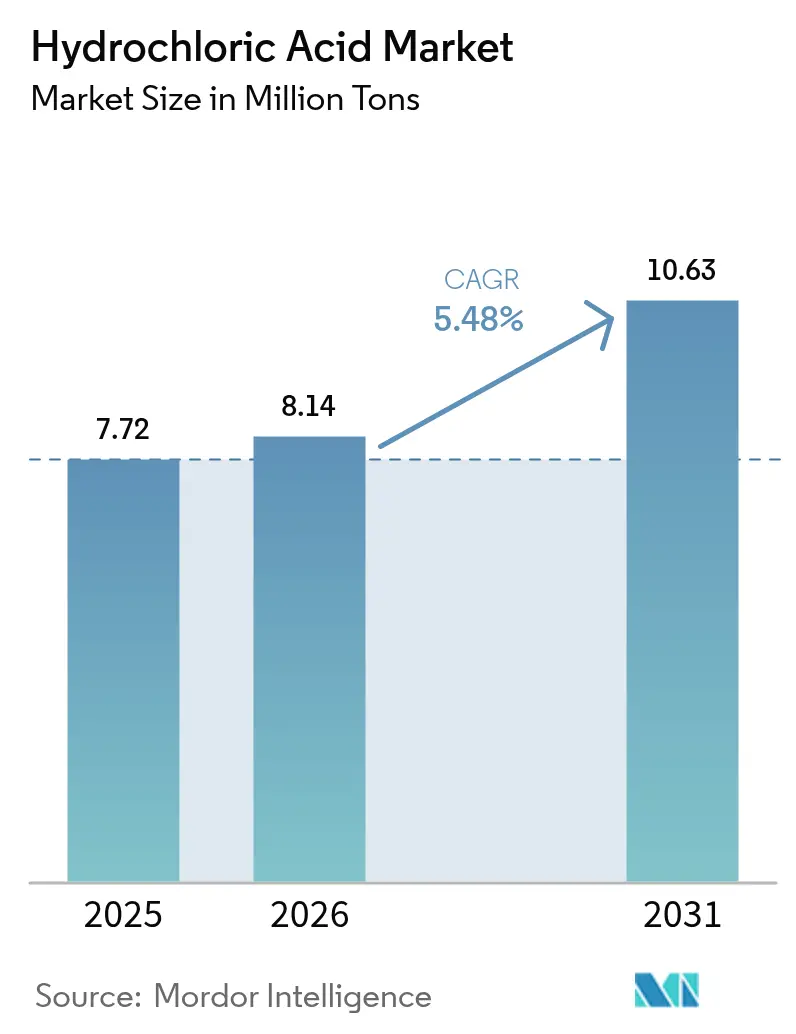

| Market Volume (2026) | 8.14 Million tons |

| Market Volume (2031) | 10.63 Million tons |

| Growth Rate (2026 - 2031) | 5.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Hydrochloric Acid Market Analysis by ���ϲ�����

The Hydrochloric Acid Market size is expected to grow from 7.72 million tons in 2025 to 8.14 million tons in 2026 and is forecast to reach 10.63 million tons by 2031 at a 5.48% CAGR over 2026-2031. A sustained rise in semiconductor fabrication, battery‐recycling hydrometallurgy, and shale‐gas acidizing anchors this expansion even as supply dynamics remain tied to caustic-soda demand cycles. Vertically integrated chlor-alkali producers continue to add capacity close to Gulf Coast petrochemical hubs and Asia-Pacific electronics clusters to minimize logistics costs and secure feedstock continuity. Merchant suppliers without captive chlorine outlets are more exposed to price swings because rising power tariffs and membrane cell retrofits raise the fixed cost base for stand-alone plants. Persistent investments in ultra-high-purity (UHP) grades serve fabs running sub-5 nm nodes where parts-per-trillion metal limits dictate multi-step distillation and ion-exchange polishing. Meanwhile, food-processing, water-treatment, and resin-regeneration applications sustain mid-grade demand, allowing producers to balance UHP volume with high-throughput industrial grades.

Key Report Takeaways

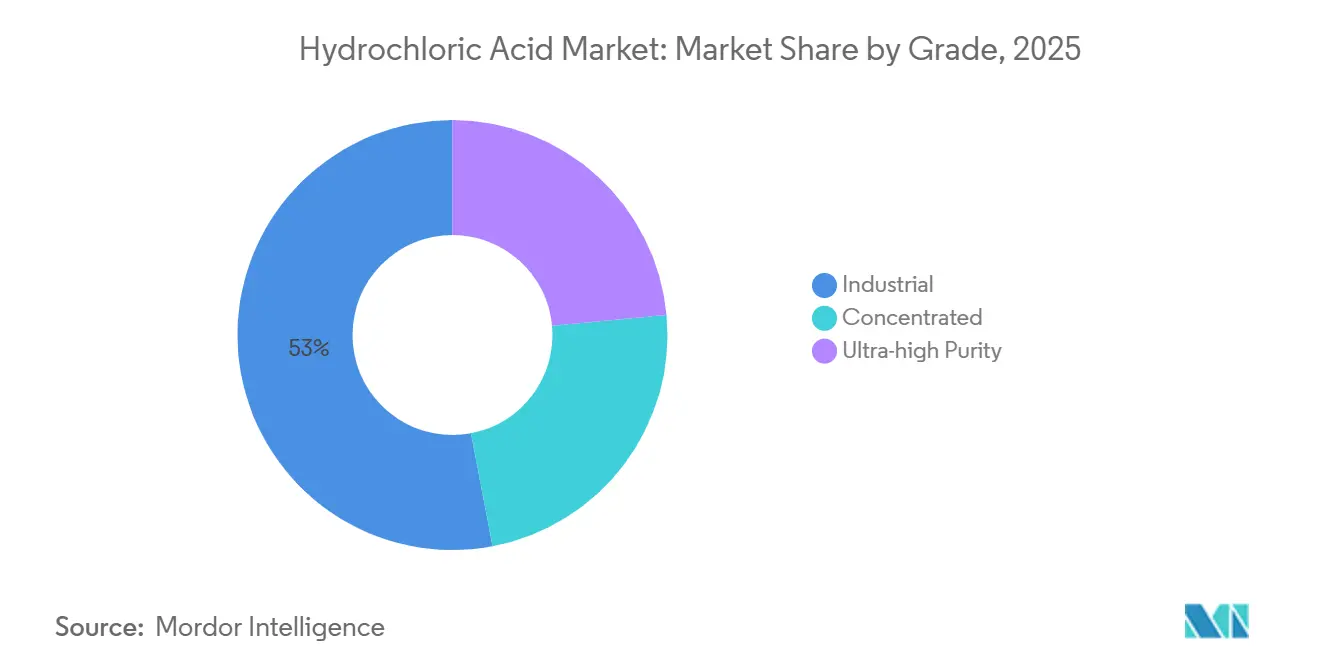

- By grade, industrial quality led with 52.98% revenue share in 2025; ultra-high-purity grades are projected to expand at a 5.88% CAGR through 2031.

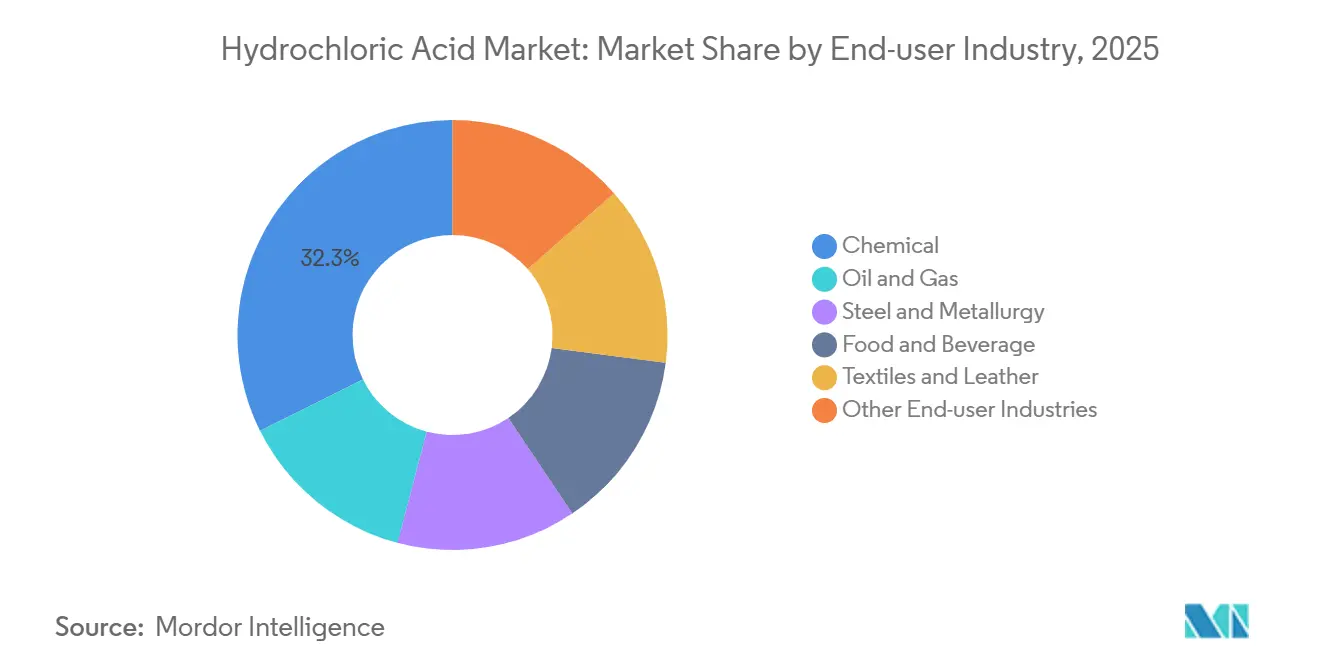

- By end-user industry, chemicals commanded 32.34% of the hydrochloric acid market share in 2025, while the same segment posts the fastest 6.12% CAGR to 2031.

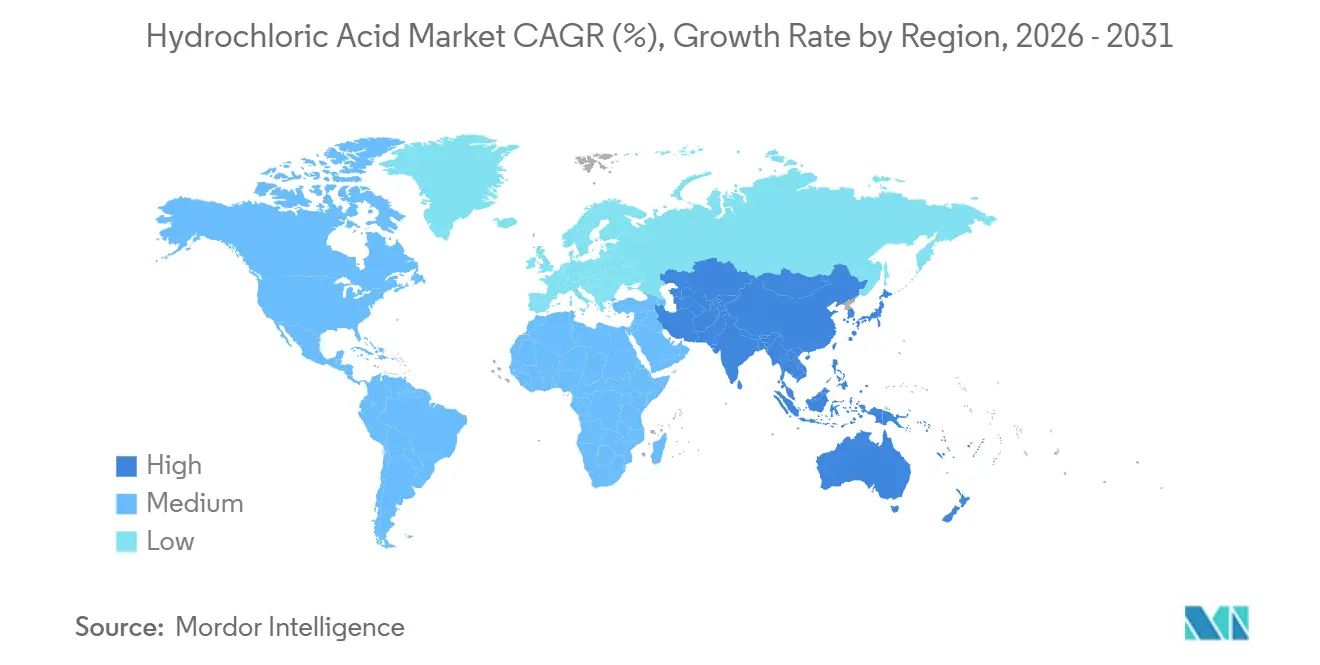

- By geography, Asia-Pacific accounted for 52.44% of volume in 2025; the region is expected to maintain a 5.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrochloric Acid Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil and gas well-stimulation demand surge | +1.2% | North America (Permian, Eagle Ford), Middle East (Saudi Arabia, UAE) | Medium term (2-4 years) |

| Water-treatment and food-processing hygiene needs | +0.8% | Global, with concentration in North America, Europe, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Semiconductor-grade HCl for advanced-node etching (≤5 nm) | +1.5% | Asia-Pacific (Taiwan, South Korea, China), North America (Arizona, Ohio) | Short term (≤ 2 years) |

| PFAS-removal resin regeneration requirements | +0.4% | North America and EU, early adoption in Scandinavia | Medium term (2-4 years) |

| Li-ion battery recycling leaching chemistry | +0.9% | Asia-Pacific core (China, South Korea), spill-over to North America, Europe | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Oil and Gas Well-Stimulation Demand Surge

Matrix and fracture acidizing of carbonate reservoirs still dominate industrial‐grade consumption. Permian operators maintain steady offtake for vertical zones while Middle Eastern producers intensify treatments across giant fields. Hybrid formulations blending HCl with surfactants extend reach in extended-reach horizontals, sustaining incremental volume despite a pivot to proppant-heavy slickwater fracs[1]American Petroleum Institute, “Technical Report on Acid Stimulation in Oil and Gas Wells,” API, api.org. Gulf Coast capacity additions place production near both shale basins and export jetties, preserving arbitrage to Saudi and UAE carbonate plays.

Water-Treatment and Food-Processing Hygiene Needs

Municipal utilities regenerate softening resins and correct pH with dilute hydrochloric acid under AWWA M20 guidelines, while FDA-compliant food-grade acid controls microbial growth in corn wet milling, gelatin hydrolysis, and beverage bottling[2]American Water Works Association, “Manual M20: Water Chlorination and Chloramination Practices,” AWWA, awwa.org. Upgrades to clean-in-place (CIP) lines in dairy and bottled-water facilities, spurred by post-pandemic needs, have driven up demand for solutions. These solutions effectively remove scale without the need for equipment dismantling.

Semiconductor-Grade HCl for Advanced-Node Etching (less than or equal to 5 nm)

SC-2 cleans for sub-5 nm wafers now relies on ultra-high-purity HCl. New fabs in Arizona, Ohio, and Taiwan set stringent standards, demanding metal limits at parts-per-trillion and particle counts under 10 per milliliter. This has led to long-term supply contracts with industry giants. Given that each 300 mm wafer requires ultra-high-purity HCl for multiple cleans, the demand is expected to increase significantly.

Li-Ion Battery Recycling Leaching Chemistry

Hydrometallurgical flowsheets recover lithium, cobalt, nickel, and manganese from black mass using HCl at 60-80 °C with hydrogen peroxide reductant. Commercial plants already process black mass annually, with EU battery regulations mandating recycled content in new cells by 2031.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chlor-alkali co-product price volatility | -0.9% | Global, acute in Europe due to energy costs | Short term (≤ 2 years) |

| Organic-acid substitution in pickling baths | -0.5% | Europe and North America, pilot projects in Asia-Pacific | Medium term (2-4 years) |

| Green-steel switch to hydrochloric-free pickling | -0.3% | Europe (Sweden, Germany), early North America adopters | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Chlor-Alkali Co-Product Price Volatility

In 2024, merchant chlorine prices increased significantly, while HCl prices trailed behind, squeezing margins for non-integrated distributors. Producers, facing swings in caustic demand, were compelled to either dump or neutralize surplus acid, a consequence of the stoichiometric link between chlorine, caustic soda, and HCl. In Europe, the cost exposure is heightened by energy-intensive membrane cells, leading to consolidation moves like Olin’s acquisition of INEOS assets to streamline output.

Organic-Acid Substitution in Pickling Baths

Citric and formic acids curb fumes and equipment corrosion yet require longer residence time and cost up to three times more per ton than hydrochloric acid. Trials in Belgium and Sweden remain pilot scale because closed-loop HCl regeneration recovers iron chloride for water treatment, offsetting reagent spend.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Ultra-High-Purity Captures Rapid Volume Premiums

Ultra-high-purity grades recorded a 5.88% CAGR over 2026-2031, outpacing other tiers as advanced fabs require ppb-level metal limits. The hydrochloric acid market for UHP products is forecasted to rise, bolstered by long-term contracts with fabs in Arizona, Ohio, and Taiwan. Industrial quality remained the volume leader with a 52.98% share in 2025, supplying steel pickling, shale-acidizing, and general synthesis. Membrane chlor-alkali retrofits and oxygen-depolarized cathodes enhance chlorine purity, boosting achievable UHP output yields.

As AI accelerators and automotive semiconductors surge, wafer starts are on the rise, propelling UHP growth within the larger hydrochloric acid market. The FDA's arsenic limit of less than or equal to 2 ppm bolsters mid-grade usage in food and pharmaceuticals, while concentrated (25-30%) solutions are reserved for specialized hydrolysis. With high premiums over industrial materials, niche suppliers like AGC are capitalizing.

By End-User Industry: Chemicals Accelerate on Battery Loop Closure

Chemicals commanded 32.34% of the 2025 volume and led 6.12% CAGR growth through 2031. This growth was bolstered by advancements in lithium-ion battery recycling, hydrometallurgy, and the demand for pharmaceutical intermediates. Hydromet leach lines have expanded their reach to China, Belgium, and the U.S., with each location utilizing hydrochloric acid for selective metal dissolution. The oil and gas sector maintained a consistent share, driven by carbonate acidizing, while the demand for steel pickling has plateaued, awaiting a broader acceptance of hydrogen-based direct-reduced iron.

The food and beverage sector enjoyed steady growth, fueled by corn wet-milling and gelatin processes. In the textiles and leather industry, hydrochloric acid was pivotal for pre-tanning and mercerization processes. However, the EPA's effluent limits mandated that discharges remain within a pH range of 6.0 to 9.0. Integrated chlor-alkali-VCM complexes are increasingly managing their chlorine balances in-house. This shift has reduced their reliance on merchant VCM intermediates but has simultaneously expanded their captive hydrochloric acid streams. With the EU's stringent battery regulations emphasizing recycled content, industry giants are ramping up their black-mass production capacity. This strategic move not only secures a multi-year demand for hydrochloric acid but also reinforces the overall growth trajectory of the hydrochloric acid market.

Geography Analysis

Asia-Pacific led with a 52.44% share in 2025 and a 5.82% CAGR to 2031 as China, Taiwan, and South Korea prioritized semiconductor self-sufficiency. Domestic suppliers have seamlessly integrated chlor-alkali plants with UHP purification trains, directly supplying fabs located in Tainan, Hsinchu, Pyeongtaek, and Xi’an. In Gujarat, India, leveraging port connectivity allows for the shipping of industrial-grade acid inland. This strategic move benefits textile and API hubs, slashing delivered costs compared to traditional truck imports. Meanwhile, ASEAN's expansion in Thailand and Vietnam has introduced membrane cells, which are now exporting surplus hydrochloric acid to electronics assemblers in Malaysia.

North America is reaping the rewards of shale-gas energy cost advantages, coupled with the initiation of significant fab projects. A notable development is Occidental’s membrane cell start-up in Ingleside, Texas, which has added a substantial amount of chlorine as a co-product. Furthermore, industry giants Intel in Ohio and TSMC in Arizona have secured timely off-take agreements with BASF and Merck KGaA, ensuring a consistent supply of UHP within just-in-time radii. Additionally, industrial-grade acid finds its application in upgrading bitumen at Canadian oil sands, ensuring a reliable outlet in Western Canada.

Europe grapples with soaring electricity costs, which surged during the 2022-2023 crisis. This spike has led to a reduction in membrane cell utilization. In a strategic move, Olin has integrated INEOS assets, streamlining operations and aligning output with the demands of its captive downstream. While green-steel pilots utilizing hydrogen DRI might diminish pickling volumes in the medium term, industrial-grade acid continues to play a pivotal role in closed-loop pickling lines, regenerating iron chloride for water treatment. In a nod to sustainability, Spain’s Vila-seca plant, powered by solar energy, has achieved ISCC Plus certification. This milestone hints at a potential resurgence of curtailed capacity, especially as power tariffs stabilize.

South America and the Middle-East, and Africa regions are still carving out their identities as emerging markets. In Brazil, the PVC chain is a significant consumer of industrial-grade HCl. Simultaneously, integrated chlor-alkali sites in Saudi Arabia are pivotal suppliers to the nation's polyurethane and epoxy clusters. Despite a limited capability in UHP, these regions predominantly deal in bulk grades. However, there's a silver lining: long-haul iso-tank exports occasionally fill supply voids for Gulf fabs.

Competitive Landscape

The hydrochloric acid market is moderately fragmented. Long-term supply agreements with fabs lock in minimum take-or-pay volumes, enhancing cash-flow visibility. Merchant distributors operating without integrated chlorine face squeezed margins when caustic cycles soften, as producers liquidate surplus acid into spot markets. Sustainability credentials, including ISCC Plus or renewable-power sourcing, increasingly influence tender awards in Europe and North America, nudging producers toward solar and wind power-purchase agreements.

Hydrochloric Acid Industry Leaders

Olin Corporation

Occidental Petroleum Corporation (OxyChem)

Westlake Corporation

BASF SE

Covestro AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Iraq established a major petrochemical plant and the new Basra industrial city in partnership with China. The facility, located at the General Company for Petrochemical Industries site, will produce 185 tons of hydrochloric acid using environmentally sustainable technology.

- January 2025: Jones-Hamilton Co. acquired Nexchlor LLC to strengthen its hydrochloric acid operations in North America. The acquisition enhanced the company's supply and logistics capabilities while bringing Jon Cupps as Division Manager of Chemicals and reinforcing its commitment to the American Chemistry Council's Responsible Care initiative.

Global Hydrochloric Acid Market Report Scope

Hydrochloric acid is a colorless solution. It is a strong inorganic acid with a distinctive pungent smell. Hydrochloric acid is a necessary laboratory reagent and industrial chemical. It is industrially prepared by dissolving hydrogen chloride in water.

The market is segmented by grade, end-user industry, and geography. By grade, the market is segmented into industrial, concentrated, and ultra-high purity. By end-user industry, the market is segmented into chemical, oil and gas, steel and metallurgy, food and beverage, textiles and leather, and other end-user industries. The report also covers the market sizes and forecasts in 16 countries. For each segment, the market sizing and forecasts were made based on volume (Tons).

| Industrial |

| Concentrated |

| Ultra-high Purity |

| Chemical |

| Oil and Gas |

| Steel and Metallurgy |

| Food and Beverage |

| Textiles and Leather |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Industrial | |

| Concentrated | ||

| Ultra-high Purity | ||

| By End-user Industry | Chemical | |

| Oil and Gas | ||

| Steel and Metallurgy | ||

| Food and Beverage | ||

| Textiles and Leather | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecasted volume growth for global hydrochloric acid between 2026 and 2031?

The hydrochloric acid market size is expected to rise from 8.14 million tons in 2026 to 10.63 million tons by 2031 at a 5.48% CAGR.

Which grade will contribute most to value growth over the next five years?

Ultra-high-purity hydrochloric acid will see the fastest 5.88% CAGR as sub-5 nm fabs demand ppb-level purity.

Why are integrated chlor-alkali producers advantaged in this market?

They control captive chlorine and caustic outlets, shielding margins from volatile spot prices that hurt stand-alone hydrochloric acid suppliers.

How is battery recycling influencing hydrochloric acid consumption?

Hydrometallurgical leaching uses 0.8-4 M HCl to recover metals, driving a 6.12% CAGR in the chemicals end-user segment.

Page last updated on: