Human Chorionic Gonadotropin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

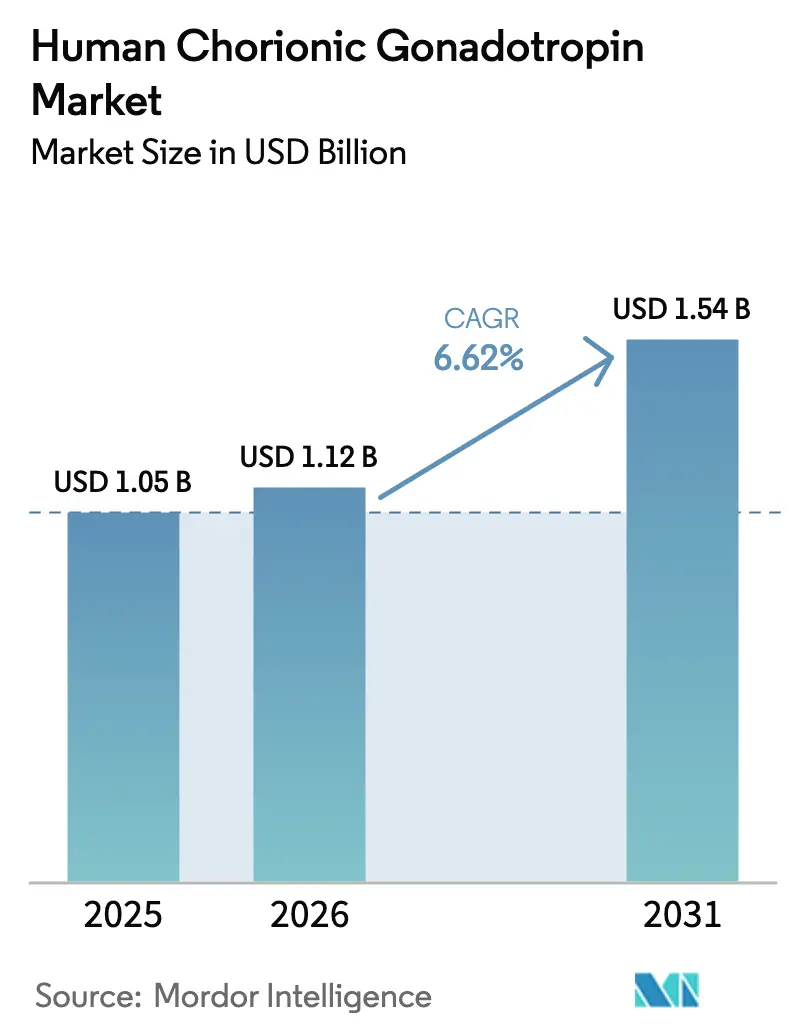

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.54 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Human Chorionic Gonadotropin Market Analysis by ���ϲ�����

The Human Chorionic Gonadotropin Market size was valued at USD 1.05 billion in 2025 and is estimated to grow from USD 1.12 billion in 2026 to reach USD 1.54 billion by 2031, at a CAGR of 6.62% during the forecast period (2026-2031).

Demographic shifts toward later parenthood, persistent growth in assisted reproductive technology (ART) cycles, and recombinant-DNA manufacturing gains are accelerating demand across fertility clinics, diagnostic laboratories, and emerging home-care settings. North America retains the leading revenue position, supported by well-insured ART users and established clinical protocols. At the same time, Asia-Pacific is delivering the fastest regional expansion, driven by clinic build-outs and medical tourism inflows. Within product classes, recombinant formulations continue to gain share by addressing purity and safety concerns surrounding urinary-derived products. At the same time, rising therapeutic adoption for male hypogonadism, broader application in point-of-care testing, and ongoing veterinary deployment broaden revenue channels for the hCG market.

Key Report Takeaways

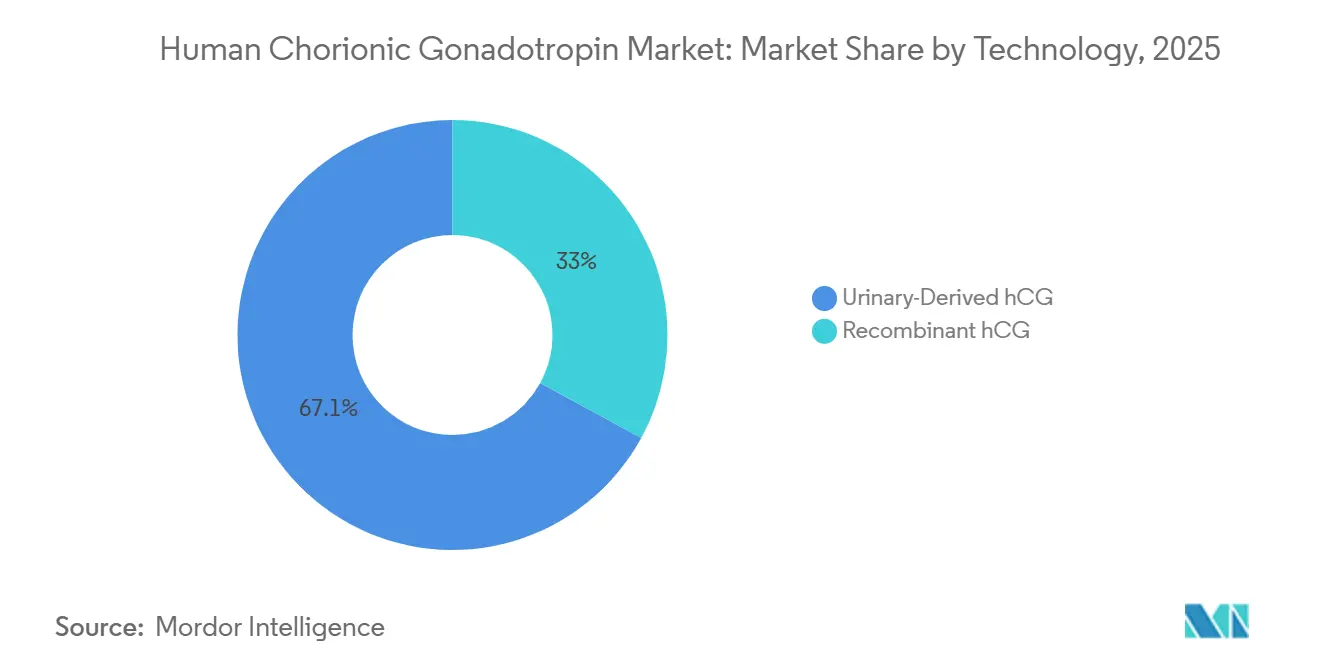

- By technology, urinary-derived products held 67.05% of the hCG market share in 2025, whereas recombinant formulations are projected to post the highest CAGR of 7.92% through 2031.

- By therapeutic area, female infertility accounted for 51.78% of the hCG market size in 2025, while male hypogonadism and azoospermia therapies are advancing at an 8.05% CAGR over 2026-2031.

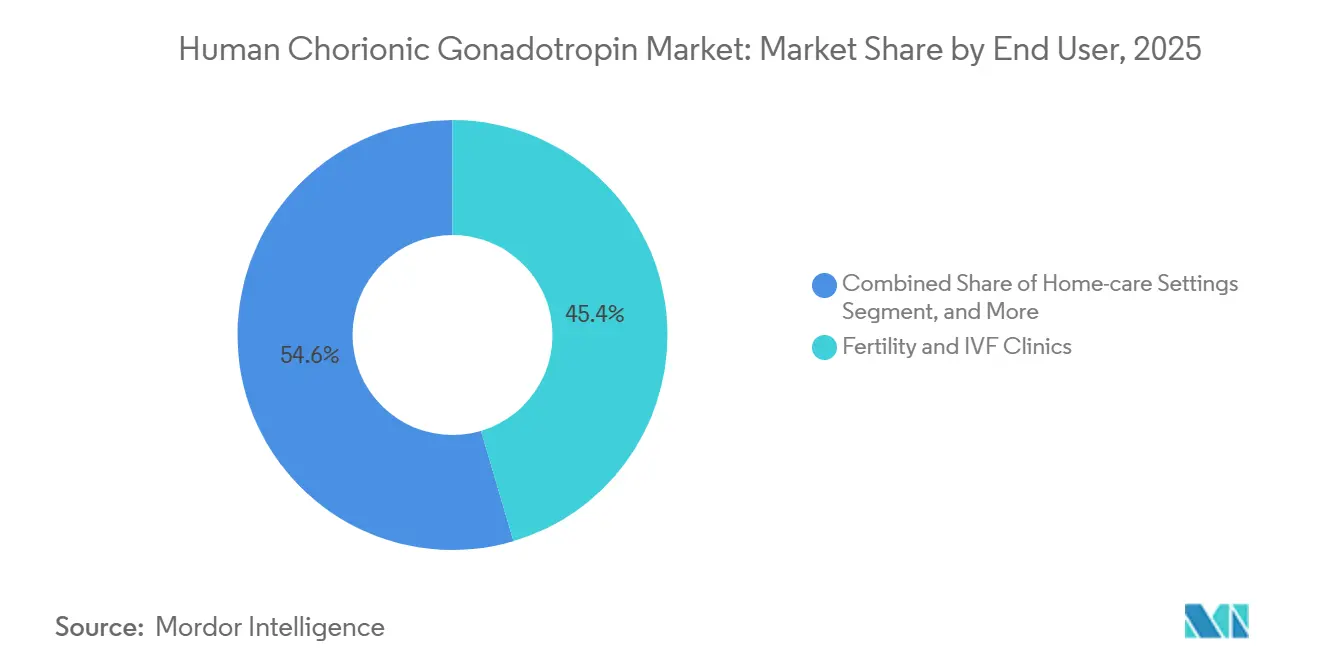

- By end user, fertility and IVF clinics accounted for 45.42% of revenue in 2025; home-care settings are on track to expand at an 8.31% CAGR thanks to rapid uptake of self-testing kits.

- By distribution channel, hospital pharmacies accounted for 46.35% of receipts in 2025, and online pharmacies are set to grow at an 8.22% CAGR through 2031 as cash-pay patients prioritize price transparency.

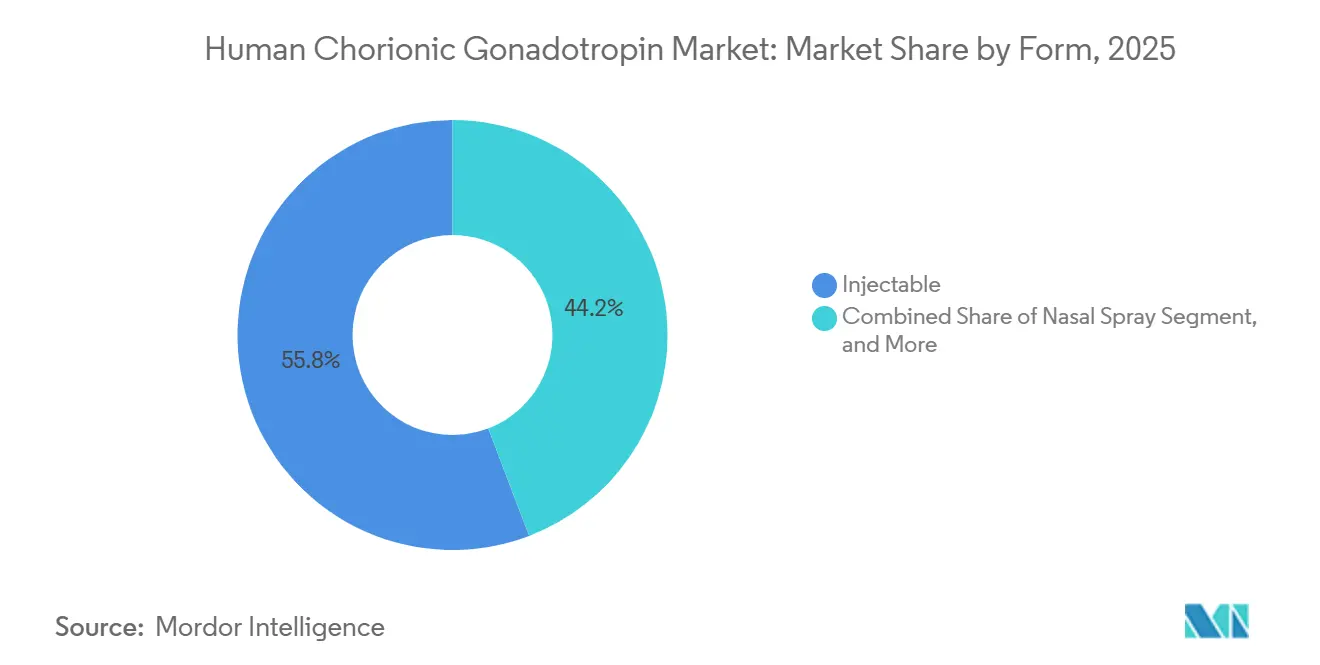

- By form, injectable preparations accounted for 55.8% of demand in 2025, while nasal-spray candidates are advancing at an 8.5% CAGR through 2031.

- By geography, North America led the hCG market with a 35.05% share in 2025, while Asia-Pacific is forecast to grow at an 8.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Human Chorionic Gonadotropin Market Trends and Insights

Driver Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising infertility prevalence & ART cycle volumes | +1.8% | Global with higher counts in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing incidence of male hypogonadism | +1.2% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Shift toward high-purity recombinant hCG | +1.5% | North America and Europe, expanding in Asia-Pacific | Long term (≥ 4 years) |

| Expansion of cross-border fertility tourism | +1.2% | Core hubs in India, Thailand, Malaysia, plus UAE and Mexico | Medium term (2-4 years) |

| Tele-fertility & home-based quantitative hCG testing | +0.9% | North America and Western Europe, early uptake in urban Asia-Pacific | Short term (≤ 2 years) |

| Emerging oncology biomarker applications of hCG | +0.9% | Asia-Pacific core, spill-over to Middle East & Africa | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rising Infertility Prevalence & ART Cycle Volumes

Infertility now affects roughly one in seven couples worldwide, with incidence climbing as average maternal age rises in developed economies. Each IVF cycle requires multiple injections of hCG to trigger final oocyte maturation and support the luteal phase, directly linking procedure growth to higher unit volumes in the hCG market. Asia-Pacific shows the sharpest gains: India is expected to shift from 250,000 IVF cycles in 2024 to 500,000-600,000 cycles by 2030, doubling hCG consumption in the process.[1]National Conference of State Legislatures, “State Infertility Coverage Mandates,” ncsl.org With ART outcomes improving and social acceptance broadening, fertility centers continue standardizing hCG-based protocols, reinforcing demand consistency. Delays in family planning and lifestyle-related subfertility are driving a global increase in assisted reproductive technology (ART) cycles. In the United States, ART cycles reached 413,776 in 2021, with preliminary figures indicating a rise to 415,953 in 2023, highlighting consistent demand for hCG trigger shots.[2]American Urological Association, “Testosterone Deficiency Guideline,” auanet.org In China, the introduction of the three-child policy has facilitated the licensing of 1,058 IVF centers by 2024, supporting approximately 1 million cycles annually.[3]National Health Commission of China, “Licensing of IVF Centers,” nhc.gov.cn Europe is experiencing similar growth, with 42 out of 49 countries implementing dedicated ART legislation to standardize reimbursement and quality benchmarks.

Shift Toward High-Purity Recombinant hCG

Regulatory agencies prioritizing biologics oversight value the consistency offered by recombinant formulations, which eliminate the batch variability inherent in urine-derived extractions. Pharmacokinetic studies demonstrate that recombinant hCG achieves peak serum concentration within 12-24 hours, mirroring urinary profiles. This predictability in dosing significantly reduces the risk of ovarian hyperstimulation syndrome (OHSS). Both the U.S. Food and Drug Administration and the European Medicines Agency have simplified biosimilar approval pathways, encouraging generic manufacturers to invest in cell-culture facilities. Producers are incorporating the molecule with subcutaneous auto-injectors, enabling easier self-dosing in tele-fertility programs. The transition from urine-collection networks to bioreactors reduces supply-chain volatility, attracting investments in recombinant capacity and driving long-term growth in the human chorionic gonadotropin market.

Expansion of Cross-Border Fertility Tourism

Significant cost differences are driving patients to affordable fertility hubs such as India, Thailand, the UAE, and Mexico, where a complete IVF cycle costs a fraction of U.S. prices. The implementation of clear accreditation rules under India’s Assisted Reproductive Technology (Regulation) Act 2021 has increased confidence among international couples. Dubai Healthcare City leverages tax-free pharmaceutical imports and multilingual staff to attract patients from the Gulf Cooperation Council, Africa, and South Asia. Clinics in these regions often include generic recombinant hCG in fixed-price packages, simplifying procurement for traveling patients. The growing influx of patients increases drug volumes, enabling regional biosimilar hCG producers to expand their market presence.

Tele-Fertility & Home-Based Quantitative hCG Testing

Digital health platforms enable clinicians to monitor ovarian stimulation remotely, reducing the need for in-person visits during the 10-14-day cycle. Patients receive electronic prescriptions, self-administer pre-filled hCG syringes at home, and upload quantitative test results via smartphone apps for physician review. The FDA's CLIA waivers for several point-of-care hCG devices validate their use outside laboratory settings, accelerating their adoption in home-care environments. Younger demographics that value convenience are willing to pay a premium for higher-purity recombinant options delivered directly to their homes. As a result, online pharmacies and tele-fertility platforms are emerging as key purchasing channels in the human chorionic gonadotropin market.

Restraint Impact Analysis

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Availability of GnRH-agonist ovulation triggers | -0.8% | Europe and North America, slowly diffusing to Asia-Pacific academic centers | Medium term (2-4 years) |

| High therapy cost & limited reimbursement | -1.1% | Global, most acute in North America and emerging markets without public coverage | Long term (≥ 4 years) |

| Regulatory warnings on off-label/weight-loss uses | -0.6% | Global, led by FDA and EMA jurisdictions | Medium term (2-4 years) |

| Raw-material supply risk for urine-derived hCG | -0.4% | North America & Europe, regulatory focus markets | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

GnRH-Agonist Triggers Gain Traction in IVF

Clinical trials demonstrate that GnRH-agonist triggers significantly reduce the incidence of moderate-to-severe OHSS by 85% among high-responder patients. In the 2024-2025 cycle year, the United Kingdom reported 67 severe OHSS cases, prompting National Health Service clinics to reevaluate their trigger protocols.[4]Human Fertilisation and Embryology Authority, “OHSS Incidence Report 2025,” hfea.gov.uk European guidelines now recommend agonist triggers, particularly for patients with polycystic ovary syndrome or elevated follicle counts, a segment that accounts for nearly 25% of IVF cycles in Western markets. While urinary and recombinant hCG remain essential for fresh-transfer strategies requiring extended luteal support, the increasing adoption of agonist substitutes is reducing hCG demand and slowing market growth.

High Therapy Cost & Limited Reimbursement

In the United States, an IVF cycle costs between USD 15,000 and 30,000, with each hCG dose adding an additional USD 50 to 250. However, only 21 states mandate partial fertility-treatment coverage. In emerging markets, cash-paying patients face similar financial challenges. For example, in India, an IVF cycle costs USD 3,000 to 5,000, which exceeds the median disposable income. Limited reimbursement options drive consumers toward lower-cost generic products and online pharmacies, compressing margins for branded manufacturers. While hospital-formulary rebates help maintain market share in insured markets, the overall burden of high out-of-pocket expenses continues to hinder the growth of the human chorionic gonadotropin market.

Segment Analysis

By Technology: Recombinant Platforms Gain Despite Urinary Dominance

The urinary-derived segment accounted for 67.05% of revenue in 2025, yet recombinant products are set to post the fastest 7.92% CAGR, signaling a structural pivot in the hCG market. Clinicians in North America and Europe now routinely favor recombinant vials for superior purity, an edge amplified by strict pharmacovigilance rules. As biosimilar versions enter Asia-Pacific, price gaps narrow and adoption widens. Manufacturers that master large-scale CHO-cell engineering and cost-efficient downstream purification will likely capture incremental share. Simultaneously, sustained need for affordable therapy in price-sensitive geographies preserves a sizeable, if gradually shrinking, urinary base. Collectively, technology differentiation drives robust competitive dynamics and underpins value migration across the hCG market.

Recombinant uptake also raises manufacturing-quality barriers. FDA warning letters to facilities with poor aseptic controls emphasize the regulatory premium on cGMP compliance, effectively shielding high-quality producers from commoditization risk. Capital-intensive bioprocessing and analytical validation expertise thus form durable moats for incumbents, shaping future consolidation trajectories within the hCG market.

By Therapeutic Area: Male Hypogonadism Emerges as Growth Engine

Female infertility retained 51.78% of the hCG market share in 2025, anchored in ovulation induction and luteal support regimens. Nonetheless, male hypogonadism-focused prescriptions are accelerating at an 8.05% CAGR, outpacing total market growth as endocrinologists pursue fertility-preserving options for younger men. Cryptorchidism remains a niche pediatric indication but provides a stable baseline demand. Home pregnancy and fertility test kits extend brand reach into consumer channels, reinforcing the hCG market’s decentralization trend. Meanwhile, oncology use cases, such as testicular cancer biomarker tracking, enrich diagnostic revenues. The breadth of the therapeutic spectrum underscores hCG’s pharmacologic versatility and supports a multi-segment go-to-market approach across the hCG industry.

By End User: Home-Care Settings Disrupt Traditional Channels

Fertility and IVF centers accounted for 45.42% of 2025 revenues, underscoring their role as anchor customers for therapeutic-grade injections. Hospitals closely follow high-risk protocols that require intensive monitoring. Yet home-care channels post an 8.31% CAGR, driven by digital pregnancy tests that deliver 99% accuracy and real-time results. Consumer preferences for discretion, speed, and cost-efficiency are driving diagnostics out of central labs, prompting manufacturers to redesign packaging, extend shelf life, and secure over-the-counter registrations. Diagnostic laboratories continue to supply quantitative β-hCG assays that refine clinical decision-making, while academic institutes expand their investigative use of novel formulations. End-user diversification therefore disperses risk and widens revenue pathways within the hCG market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Pharmacies Capture Cash-Pay Demand

In 2025, hospital pharmacies, leveraging formulary control and rebate agreements, captured 46.35% of distribution revenue. Their dominance remains strongest in regions with extensive insurance coverage. However, online pharmacies are projected to grow at an 8.22% CAGR through 2031, driven by cash-pay patients who prioritize transparent pricing. Generic recombinant products, often sold at 30-40% discounts compared to branded counterparts, are reaching a broader audience through international shipping.

While cross-border sourcing introduces regulatory complexities, it provides financial relief to patients facing high domestic prices. Additionally, this channel provides suppliers with valuable direct consumer feedback, driving packaging innovation. As a result, the human chorionic gonadotropin market is experiencing channel fragmentation, favoring agile and digitally proficient companies.

By Form: Nasal Spray Development Targets Adherence Gaps

In 2025, injectables dominated consumption with a 55.8% share, supported by their established clinical trust. However, concerns such as needle aversion and fatigue from chronic use are prompting pharmaceutical companies to explore intranasal delivery methods. Pipeline products are expected to grow at an 8.5% CAGR through 2031, with pharmacokinetic studies showing that nasal administration achieves peak serum levels within 30-60 minutes, indicating comparable bioavailability to traditional methods.

The regulatory landscape has matured, particularly following the approval of other intranasal biologics, providing manufacturers with a clear framework. If patient-reported adherence improves, nasal formats could capture a significant share of injectables, especially in the male hypogonadism segment, which requires prolonged therapy. This innovation cycle highlights the diverse delivery platforms shaping the future dynamics of the human chorionic gonadotropin market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America captured 35.05% of 2025 revenue, anchored by advanced IVF programs, partial insurance coverage in several U.S. states, and steady inflows of international patients seeking cost-moderate Mexican services. Strong professional-society guidelines standardize hCG dosing, ensuring predictable order volumes for suppliers. Canada’s publicly funded cycles add further base demand, and regulatory vigilance favors high-purity recombinant lines, fostering premium pricing latitude. Regional growth is steady rather than explosive, yet purchasing power keeps North America the single largest contributor to the global hCG market size.

Asia-Pacific is projected to log a 8.74% CAGR through 2031, the fastest worldwide, as economic development lifts disposable income and governments incentivize reproductive-health infrastructure. India alone opens more than 60 new fertility clinics each year, and its IVF cycles are set to more than double by decade-end. China’s relaxation of family-planning rules and healthcare reforms funnel new patient cohorts into ART pipelines, while Thailand and Malaysia sharpen medical-tourism value propositions. Cross-border traffic, attracted by sub-USD 3,000 IVF pricing in India, continues to broaden the regional customer base. Local fill-and-finish capacity additions by multinationals further reduce supply-chain risk, reinforcing Asia-Pacific’s status as growth engine of the hCG market.

Europe maintains a balanced position: generous public reimbursement in Germany, France, and portions of the United Kingdom ensures steady demand, while stringent EMA quality requirements tilt the mix toward recombinant products. Eastern Europe, led by Bulgaria and Czech Republic, leverages lower IVF package prices of roughly USD 12,000 for multiple cycles to lure inbound couples from Western Europe. Brexit-related customs complexities have been largely mitigated through regional distribution hubs, preserving supply continuity. Overall, Europe remains a mature yet opportunity-rich theater for suppliers able to meet exacting regulatory and pharmacovigilance standards.

Competitive Landscape

Multinational corporations such as Organon, Merck KGaA, and Ferring Pharmaceuticals dominate the branded recombinant and urinary portfolios of the human chorionic gonadotropin market, while Indian and Chinese manufacturers supply cost-effective generics. Organon, following its 2021 spinoff from Merck, has established itself as a women's health-focused company, marketing Pregnyl and Ovidrel, thereby protecting its revenue from fluctuations in raw-material costs. Meanwhile, Ferring's vertical integration into fertility clinic networks enables it to offer bundled medication packages, fostering customer retention.

Patent expirations are creating opportunities for biosimilar manufacturers like Bharat Serums, Cipla, and Lupin, which are expanding mammalian-cell facilities to produce hCG at costs 40-60% lower than branded North American products. Although regulatory requirements for comparative pharmacokinetics pose challenges, companies with biologics expertise and ISO-certified facilities are overcoming them. The competitive focus is shifting toward device innovation, with features such as auto-injector pens, lyophilized cold-chain-free powders, and smartphone-connected dosage trackers driving differentiation.

Opportunities extend beyond reproductive health into oncology, particularly in monitoring testicular cancer and gestational-trophoblastic disease, which require accurate beta-hCG tracking. Digital health companies are partnering with biosimilar manufacturers to integrate hCG dosing and testing into app-based fertility platforms, bypassing traditional hospital formularies. As direct-to-consumer logistics advance, the demand for pricing transparency and enhanced service convenience is expected to intensify competition, reshaping the market landscape.

Human Chorionic Gonadotropin Industry Leaders

Merck & Co. Inc.

Ferring BV

Fresenius Kabi AG

Sun Pharmaceutical Industries Ltd

Sanzyme Biologics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The U.S. Department of Justice announced convictions in Indiana and Florida related to the illegal sale of compounded human chorionic gonadotropin, underscoring heightened enforcement around controlled-substance distribution.

- February 2025: The FDA issued a warning letter to Aspen Pharmacare Holdings for cGMP violations at its South African site, pausing U.S. imports until remediation.

- October 2024: Mankind Pharma acquired Bharat Serums and Vaccines for USD 1.67 billion, expanding its fertility-drug portfolio that includes biosimilar hCG lines.

Global Human Chorionic Gonadotropin Market Report Scope

As per the scope of the report, the human chorionic gonadotropin hormone is a placental hormone secreted by syncytiotrophoblast cells during pregnancy. These hormones stimulate the corpus luteum to produce progesterone. The naturally extracted or recombinant human chorionic gonadotropin hormones are used in the treatment of infertility, male hypogonadism, and many other conditions.

The human chorionic gonadotropin market is segmented by product, application, distribution channel, form, and geography. By product, the market is segmented into naturally extracted and recombinant. By application, the market is segmented into male hypogonadism, female infertility treatment, oligospermia treatment, and other applications. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By form, the market is segmented into injectable, oral, and nasal spray. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Urinary-Derived hCG |

| Recombinant hCG |

| Female Infertility Treatment |

| Male Hypogonadism |

| Cryptorchidism |

| Pregnancy & Fertility Test Kits |

| Oncology & Other Indications |

| Fertility and IVF Clinics |

| Hospitals |

| Diagnostic Laboratories |

| Research Institutions |

| Home-care Settings |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Injectable |

| Oral |

| Nasal Spray |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Urinary-Derived hCG | |

| Recombinant hCG | ||

| By Therapeutic Area | Female Infertility Treatment | |

| Male Hypogonadism | ||

| Cryptorchidism | ||

| Pregnancy & Fertility Test Kits | ||

| Oncology & Other Indications | ||

| By End User | Fertility and IVF Clinics | |

| Hospitals | ||

| Diagnostic Laboratories | ||

| Research Institutions | ||

| Home-care Settings | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Form | Injectable | |

| Oral | ||

| Nasal Spray | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the global hCG market?

The hCG market size is USD 1.12 billion in 2026, with a forecast to reach USD 1.54 billion by 2031.

Which region is growing fastest for hCG products?

Asia-Pacific leads global growth with a projected 8.74% CAGR from 2026 to 2031.

Why are recombinant hCG products gaining popularity?

Recombinant lines offer higher purity, consistent bioactivity, and reduced contamination risk, prompting clinician preference in developed markets.

How is hCG used in male fertility treatment?

HCG stimulates endogenous testosterone and spermatogenesis, making it effective for hypogonadism and azoospermia without suppressing fertility.

What is driving home-care demand for hCG diagnostics?

Widespread availability of accurate, affordable pregnancy self-tests encourages consumers to shift away from laboratory-based assays.

Page last updated on: