HPV Testing And Pap Test Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.59 Billion |

| Market Size (2031) | USD 12.58 Billion |

| Growth Rate (2026 - 2031) | 10.63% CAGR |

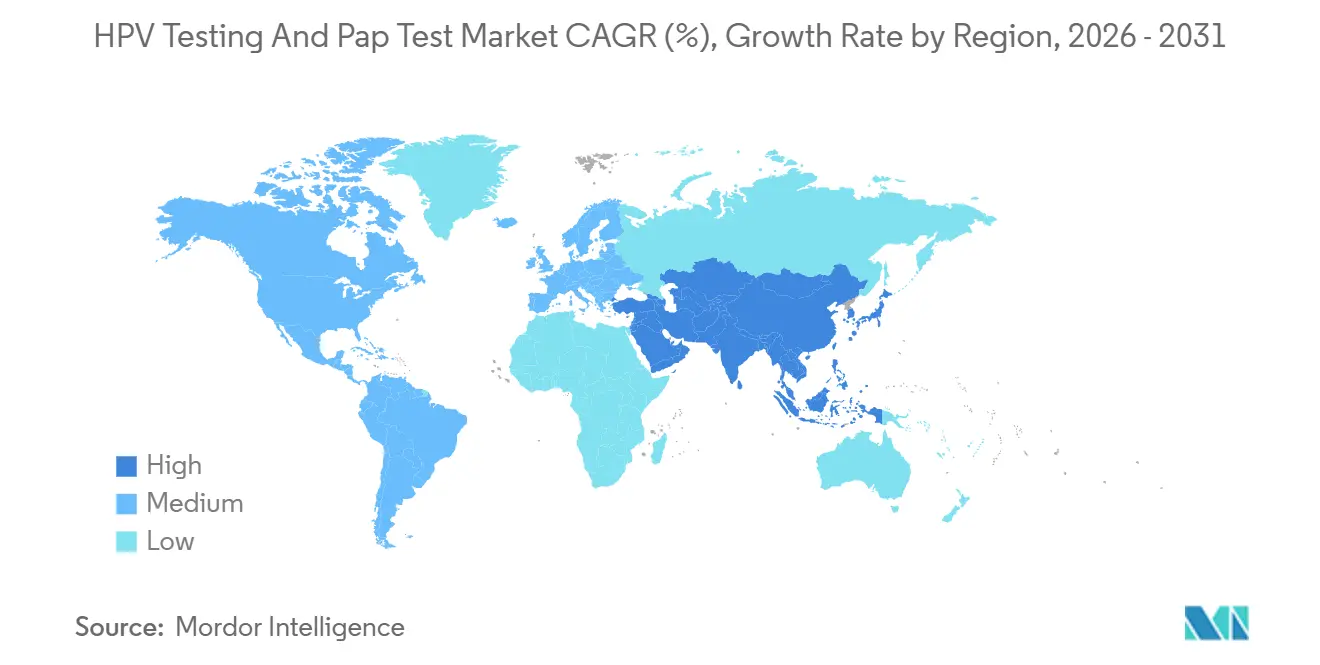

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

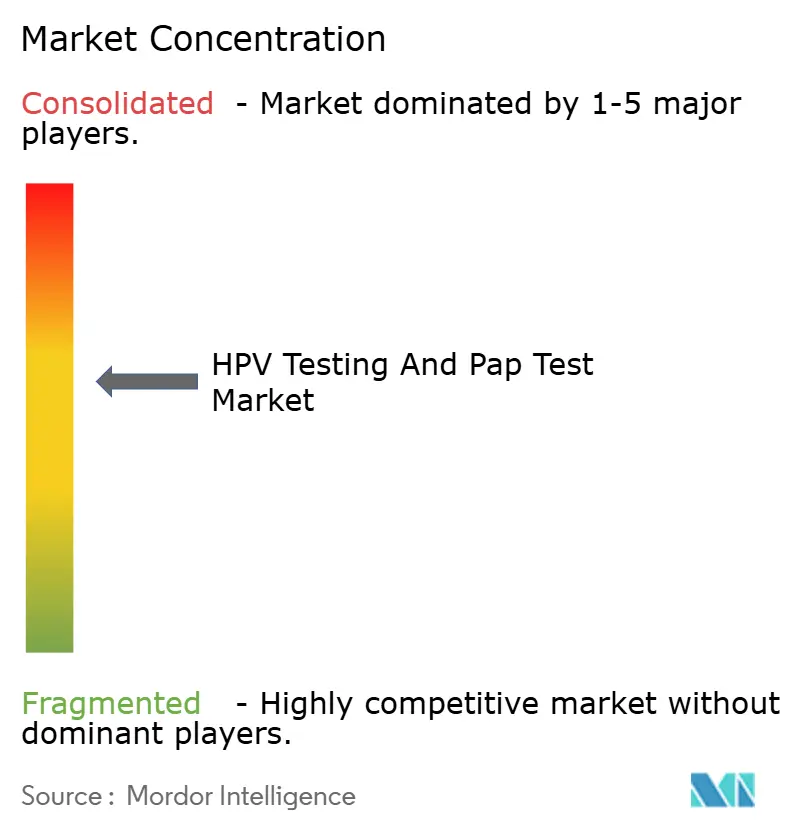

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

HPV Testing And Pap Test Market Analysis by ���ϲ�����

The HPV Testing And Pap Test Market size is expected to grow from USD 6.89 billion in 2025 to USD 7.59 billion in 2026 and is forecast to reach USD 12.58 billion by 2031 at 10.63% CAGR over 2026-2031.

Guideline revisions that elevate molecular assays to first-line screening, combined with government-funded rollouts in China and India, are steering laboratories away from cytology workflows and toward high-throughput PCR and next-generation sequencing platforms. Demand is also buoyed by self-sampling programs that increase participation among women who avoid in-clinic exams, while AI-assisted digital pathology helps narrow staffing gaps in cytology labs. Reagent supply constraints linger, yet capacity additions in India and the United States are trimming lead times, easing one of the most acute bottlenecks. Vendors are layering subscription-based software onto installed instruments, shifting revenue from one-off hardware sales to recurring digital fees. Collectively, these forces keep the HPV testing and pap test market on a double-digit growth trajectory even as HPV vaccination rates climb.

Key Report Takeaways

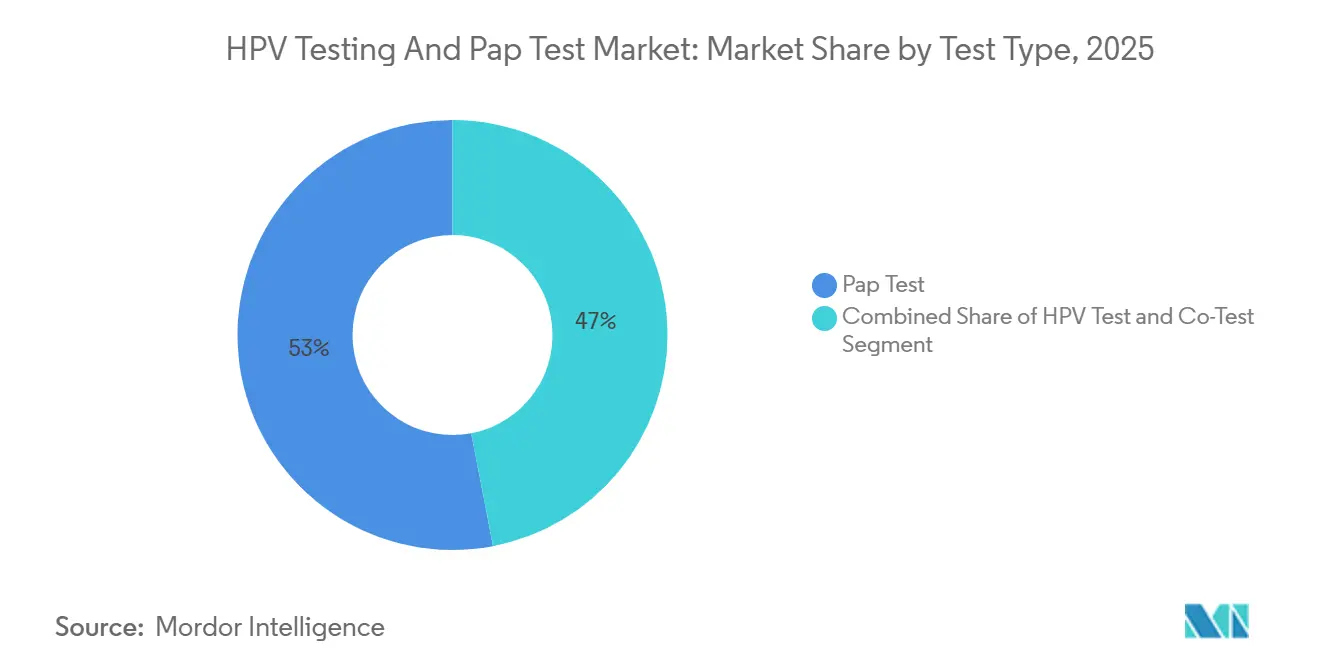

- By test type, Pap Tests led with 53.02% of HPV testing and pap test market share in 2025, while HPV Tests are advancing at an 11.26% CAGR through 2031.

- By product type, consumables and reagents captured 54.17% of the HPV testing and pap test market in 2025; software platforms are scaling fastest at a 12.35% CAGR through 2031.

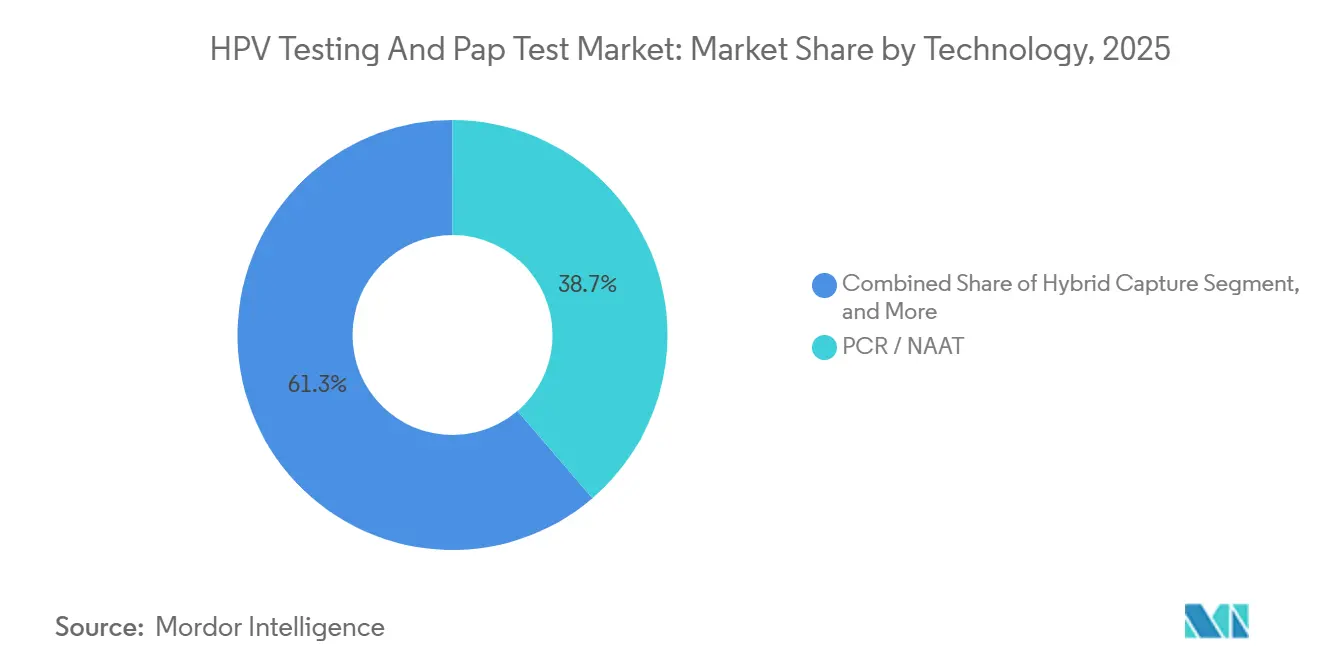

- By technology, PCR/NAAT accounted for 38.72% of 2025 revenue, whereas next-generation sequencing is set to expand at 13.04% CAGR, reshaping the premium tier.

- By application, cervical cancer screening accounted for 27.78% in 2025, while post-treatment follow-up is projected to grow at a 13.62% CAGR through 2031.

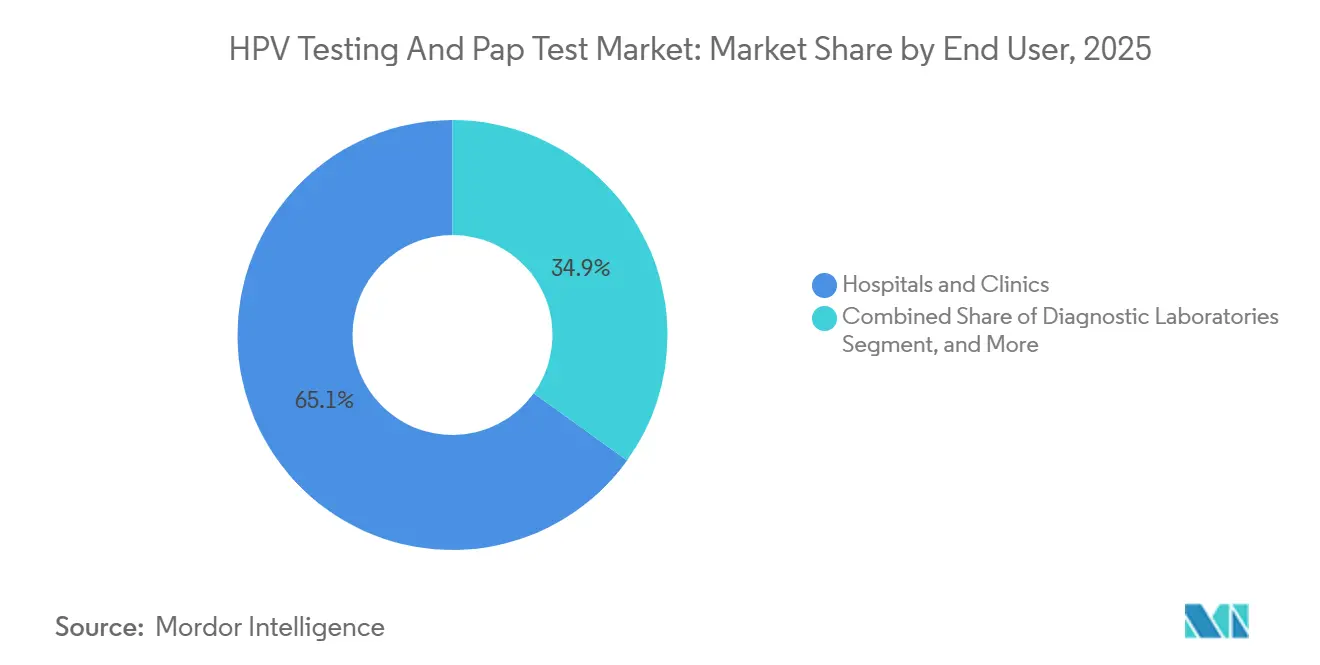

- By end user, hospitals and clinics accounted for 65.08% of demand in 2025; diagnostic laboratories are gaining ground at a 11.79% CAGR as payers consolidate testing volumes.

- By geography, North America accounted for 43.78% of revenue in 2025, while Asia-Pacific is the fastest-growing region at a 14.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global HPV Testing And Pap Test Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of HPV Infections and Cervical Cancer Burden | +2.8% | Global, with acute pressure in South Asia, Sub-Saharan Africa, and Latin America | Medium term (2–4 years) |

| Expanding Government-Funded Screening Programs and New Guidelines Favoring HPV Primary Testing | +3.1% | North America, Europe, China, India; spillover to Southeast Asia | Short term (≤2 years) |

| Technological Advancements in Molecular Diagnostics | +2.4% | Global, led by North America and Europe; rapid adoption in urban Asia-Pacific | Medium term (2–4 years) |

| Adoption of Self-Sampling / Home-Based HPV Kits Improving Screening Uptake | +1.7% | North America, Europe, Australia; pilot programs expanding in India, China, and Latin America | Short term (≤2 years) |

| AI-Enabled Cytology & Digital Pathology Alleviating Pathologist Shortages | +1.9% | North America, Western Europe, Australia; pilot programs in urban India and China | Long term (≥4 years) |

| Integration of HPV Screening into Women's Digital-Health Ecosystems & Bundled Care | +1.5% | North America, Western Europe; emerging adoption in urban Asia-Pacific markets | Medium term (2–4 years) |

| Source: ���ϲ����� | |||

Rising Prevalence of HPV Infections and Cervical Cancer Burden

Global cervical cancer incidence climbed 4.2% between 2020 and 2024, reversing earlier gains tied to Pap campaigns.[1]International Agency for Research on Cancer, “Global Cervical Cancer Incidence 2024,” iarc.who.int Screening gaps created during the pandemic left an estimated 35 million women untested, allowing lesions to progress unchecked. South Asia and Sub-Saharan Africa now carry 70% of mortality, pushing ministries to subsidize molecular HPV tests that deliver 90–95% sensitivity. Shifts in the genotype mix of non-vaccine types 31, 33, 45, 52, and 58 are now more common among women aged 30-39, spurring laboratories to adopt extended-genotyping assays that guide risk-stratified management. Regulators responded in 2024 by publishing draft guidance that formalizes genotyping reflex pathways, streamlines triage, and enhances test value.

Expanding Government-Funded Screening Programs and New Guidelines Favoring HPV Primary Testing

The 2024 USPSTF Grade A recommendation for HPV primary testing catalyzed immediate payer alignment, with major U.S. insurers raising reimbursement to USD 65-72 per assay. England finalized its nationwide switch to HPV-first screening, cutting cytology workload 40% and halving turnaround times. China earmarked RMB 12 billion (USD 1.65 billion) to screen 120 million rural women using domestic PCR kits, while India incorporated HPV testing into its Ayushman Bharat scheme, achieving 62% uptake in pilot states. These mandates compress replacement cycles for legacy microscopes, driving orders for automated molecular platforms and fueling the HPV testing and pap test market in the near term.

Technological Advancements in Molecular Diagnostics

Next-generation sequencing panels capable of genotyping 37 HPV strains, quantifying viral load, and flagging viral integration gained CE mark in 2025, commanding USD 150-200 per sample. Early adopters report an 18% drop in unnecessary colposcopies, offsetting premium pricing. mRNA-based assays targeting E6/E7 transcripts reduced false positives among women 25-29 by 22%, earning expanded FDA clearance and broadening the addressable base. Automation advances also cut labor per test by 35%, bringing molecular screening within budget for middle-income facilities and enlarging the HPV testing and pap test market footprint.

AI-Enabled Cytology & Digital Pathology Alleviating Pathologist Shortages

By 2024, the U.S. cytotechnologist deficit reached 28%, prolonging Pap turnaround times to 2 weeks in some regions. AI-assisted slide scanners now clear FDA hurdles, achieving 96% concordance with expert accuracy and processing slides 40% faster. Reference labs using these systems documented 30% higher daily throughput and 25% lower inter-observer variability. Europe moved quickly after IVDR benchmarks were published, with the Netherlands and Sweden digitizing 85% of cytology workflows by late 2025. Though reimbursement parity with manual reads constrains small-lab adoption, cloud-hosted pay-per-use models are widening access and sustaining growth in the HPV testing and pap test market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Molecular Tests in Low-Resource Settings | -1.6% | Sub-Saharan Africa, South Asia, rural Latin America | Medium term (2–4 years) |

| Variable Reimbursement & Complex Multi-Regional Regulatory Pathways | -1.3% | Global, with acute challenges in emerging markets; fragmented European systems | Short term (≤2 years) |

| Rising HPV Vaccination Coverage Reducing Long-Term Screening Volumes | -1.2% | High-income countries (North America, Western Europe, Australia); emerging impact in middle-income nations | Long term (≥4 years) |

| Supply-Chain Fragility for Specialized Reagents and Plastics Post-Pandemic | -0.9% | Global, with acute disruptions in Asia-Pacific manufacturing hubs and distribution to emerging markets | Short term (≤2 years) |

| Source: ���ϲ����� | |||

High Cost of Advanced Molecular Tests in Low-Resource Settings

PCR-based HPV tests cost USD 15–25 per sample in low- and middle-income countries, compared to USD 2–5 for visual inspection with acetic acid (VIA), the dominant screening method in Sub-Saharan Africa where per-capita health spending averages USD 50 annually.[2]World Health Organization, “Cost Barriers to HPV Screening in LMICs 2025,” who.int This price gap restricts molecular test adoption to urban tertiary hospitals and donor-funded pilot programs, leaving 80% of the at-risk population reliant on VIA, which has 50–60% sensitivity for high-grade lesions, compared with 90–95% for HPV DNA tests. Zambia's Ministry of Health piloted Cepheid's GeneXpert HPV assay in 2024 across 15 rural clinics, achieving 68% screening uptake, but suspended expansion after donor funding lapsed, citing unsustainable reagent costs of USD 18 per test. India's public health system negotiated HPV test prices down to USD 5–6 through bulk procurement, yet state budgets cover only 40% of eligible women, forcing rationing that prioritizes high-risk age groups (35–45) and excludes younger cohorts.

Rising HPV Vaccination Coverage Reducing Long-Term Screening Volumes

Global HPV vaccine coverage for girls aged 9–14 reached 48% in 2025, up from 32% in 2020, driven by GAVI's expansion in 50 low-income countries and school-based programs in high-income nations. Australia, which achieved 86% coverage by 2024, projects a 30% decline in cervical screening demand by 2035 as vaccinated cohorts age into the 25–65 screening window, per modeling by the Australian Institute of Health and Welfare.[3]Australian Institute of Health and Welfare, “Projected Screening Decline Post-Vaccination 2024,” aihw.gov.au The U.K.'s National Health Service reported a 22% drop in HPV prevalence among women aged 20–24 between 2020 and 2024, correlating with the 2008 introduction of the bivalent vaccine; screening volumes in this age group fell 18% as fewer women tested positive and required follow-up. The U.S. CDC's 2025 data showed 76% of adolescents received at least one HPV vaccine dose, with complete series coverage at 62%, levels that epidemiologists estimate will reduce cervical cancer incidence by 40% among vaccinated cohorts by 2040.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular HPV Assays Dethrone Legacy Cytology

HPV Tests are advancing at a 11.26% CAGR, eating into Pap Tests’ 53.02% share of the HPV testing and Pap test market recorded in 2025. The USPSTF guidance that elevates HPV primary screening triggered immediate coverage shifts, making standalone molecular assays the economical choice for laboratories processing 300-500 samples per shift.

Self-collection kits cleared in 2024 further accelerate adoption among women overdue for exams, boosting screening uptake by 28% in a large U.S. randomized study. Co-testing persists where malpractice concerns linger, though its 20% volume share is sliding as payers curtail dual-test reimbursement. In emerging markets, Pap Tests remain relevant for facilities lacking PCR capacity, yet falling instrument prices and reagent localization are steadily broadening access to HPV tests, expanding the HPV testing and Pap test market size at double-digit rates.

By Product Type: Software Platforms Capture Digital Upside

Recurring reagent sales delivered 54.17% of revenue in 2025, but software platforms are on course for a 12.35% CAGR as AI engines and cloud dashboards move cervical screening into integrated women’s health portals. Hologic’s Genius platform alone generated USD 180 million in license and subscription revenue in 2025, proof that digital layers now rival consumables in value capture.

Hospitals facing budget freezes increasingly favor software-as-a-service contracts over capital purchases, a pivot that locks clients into multi-year agreements and stabilizes vendor cash flows. Meanwhile, instruments and analyzers lengthen refresh cycles to 8-10 years, dampening hardware demand but broadening installed bases for future software attach. Services training, validation, and maintenance account for 10% of turnover and offer cross-sell opportunities for vendors seeking a holistic share of wallet in the HPV testing and pap test market.

By Technology: NGS Climbs the Value Chain

PCR/NAAT retained a 38.72% share in 2025, yet next-generation sequencing’s 13.04% CAGR signals a clear shift toward premium assays that detect 37 genotypes, viral load, and integration events in a single run. The HPV testing and pap test market tied to NGS remains modest today, but hospital consortia are piloting these panels for high-risk triage and clinical trials, citing an 18% reduction in unnecessary colposcopies.

Hybrid capture persists where budgets are tight, while mRNA tests fill a niche for women 25-29, delivering 22% fewer false-positives than DNA assays. Regulatory momentum favors diversification; a 2024 FDA draft explicitly welcomes NGS for primary screening, which should unlock broader reimbursement and cement the technology’s role as the market’s innovation frontier.

By Application: Surveillance Outpaces Primary Screening

Cervical cancer screening retained a 27.78% share in 2025, yet post-treatment follow-up’s 13.62% CAGR makes it the fastest-growing segment within the HPV testing and pap test market. Updated ASCCP guidelines recommend HPV testing at 6, 12, and 24 months post-excision, praising its 98% negative predictive value.

Hospitals bill USD 100-150 for surveillance panels versus USD 50-70 for routine screening, bolstering average selling prices. Clinical-trial demand spikes seasonally as therapeutic vaccines advance through late-stage studies. Vaginal cancer screening and opportunistic STI panels remain small but steady niches, offering incremental volumes without a meaningful effect on overall market share.

By End User: Central Laboratories Accelerate Consolidation

Hospitals and clinics account for 65.08% of current revenue, yet diagnostic laboratories are growing at a 11.79% CAGR, capturing volume through automation and payer-driven outsourcing. Quest Diagnostics’ reflex algorithm slashed turnaround to 48 hours while cutting labor by 30%, showcasing the scale economics driving consolidation.

LabCorp’s 2024 takeover of a regional cytology group added 1.8 million annual tests and trimmed redundant capacity, a template others are sure to copy. Direct-to-consumer portals, mobile vans, and public health labs collectively make up the balance, but their growth underscores the diversification of collection points and the broadening reach of the HPV testing and pap test market.

Geography Analysis

North America accounted for 43.78% of the HPV testing and Pap test market revenue in 2025. The USPSTF Grade A rating for HPV primary testing spurred reimbursement increases, yet vaccination progress and five-year screening intervals constrain absolute volume growth. Canada’s shift to HPV testing in its three largest provinces demonstrates provincial momentum, even as smaller regions weigh budget impacts. Mexico’s Seguro Popular program introduced HPV assays in 2024, but uneven lab capacity outside major metros slows uptake.

Asia-Pacific is expanding the fastest, with a 14.97% CAGR. China’s RMB 12 billion initiative to screen 120 million women using local PCR kits anchors volume, while India’s Ayushman Bharat integration lifted participation to 62% in pilot states. Japan resumed pro-vaccine policy in 2024 and lengthened intervals for vaccinated women, tempering near-term test counts but firming long-range demand through broader prevention. South Korea’s 2025 age-band expansion adds 4 million annual tests, even though reimbursement trails true cost.

England finalized its HPV-first rollout, Germany mandated tri-annual HPV screening for women ≥35, and France approved HPV primary testing though regional systems staggered implementation. Middle East & Africa and South America combined for 8% share; limited budgets and reagent stockouts inhibit scale, though donor-backed pilots in Brazil, South Africa, and Zambia validate demand when funding aligns. Overall, geographic variance hinges on policy maturity, payer generosity, and laboratory infrastructure, but Asia-Pacific’s momentum offsets plateauing North America, keeping the global HPV testing and pap test market on a solid growth arc.

Competitive Landscape

The HPV testing and pap test market displays moderate concentration. Roche, Hologic, and Qiagen collectively significant portion of revenue, leveraging vast reagent rental contracts and entrenched instrument fleets. Roche’s cobas platforms remain staples in hospital core labs, while Hologic’s Panther Fusion system wins share in decentralized clinics by bundling same-day HPV and STI results. Qiagen defends price-sensitive geographies with USD 12 assays, although PCR rivals are converging on similar cost points.

Competitive intensity sharpened in 2025 as BD acquired Cytognos, adding flow-cytometry HPV capability that complements its MAX PCR line. Illumina’s CE-marked NGS panel positioned it at the top of the risk-stratification niche, and Abbott’s Alinity m assay undercut European PCR pricing at EUR 20 per test. Domestic Chinese players Guangdong Hybribio and Sansure Biotech secure massive rural tenders by offering USD 5 tests, though global reach is constrained by a lack of FDA clearance.

White-space arenas include self-sampling, AI-enhanced triage, and ambient-stable reagents for low-resource zones. Cepheid’s GeneXpert vans in Zambia illustrated a mobility play, while Arbor Vita earned Breakthrough Device status for its USD 25 point-of-care test compatible with retail clinics. As reimbursement tightens, vendors pivot toward subscription software and post-treatment surveillance markets, aiming to protect margins and deepen stickiness across the expanding HPV testing and pap test market.

HPV Testing And Pap Test Industry Leaders

Arbor Vita Corporation

F. Hoffmann-La Roche Ltd

Seegene Inc.

Becton, Dickinson and Company

Qiagen NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Teal Health won FDA approval for the Teal Wand, the first at-home cervical cancer screening device, with 96% accuracy and 94% patient preference.

- March 2025: Ontario replaced Pap with HPV testing in its provincial program.

Global HPV Testing And Pap Test Market Report Scope

As per the scope of the report, the human papillomavirus (HPV) test is used to detect HPV, which can lead to the development of genital warts, abnormal cervical cells, or cervical cancer. A Pap smear, also called a Pap test or smear test, is a procedure doctors use to find cell changes or abnormal cells in the cervix. A Pap smear removes a microscopic sample of cells from the cervix to test for cancer and precancer. Pap tests are the most preferred tests to detect cervical cancer. These tests include microscopic observation of specimens.

The HPV testing and Pap test market is segmented by test type, product type, technology, application, end user, and geography. By test type, the market is segmented into HPV test, Pap test, and co-testing. By product type, the market is segmented by instruments and analyzers, consumables and reagents, software platforms, and services. The market is segmented by technology into PCR/NAAT, hybrid capture, mRNA-based assays, and next-generation sequencing. The market is segmented by application into cervical cancer screening, vaginal cancer screening, and other applications. By end user, the market is segmented into hospitals/clinics, diagnostic centers, and other end users. Geographically, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for the above segments.

| HPV Test |

| Pap Test |

| Co-test (HPV + Pap) |

| Instruments and Analyzers |

| Consumables and Reagents |

| Software Platforms |

| Services |

| PCR / NAAT |

| Hybrid Capture |

| mRNA-based Assays |

| Next-Generation Sequencing |

| Cervical Cancer Screening |

| Vaginal Cancer Screening |

| Post-treatment Follow-up |

| Clinical Trials & Epidemiology |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | HPV Test | |

| Pap Test | ||

| Co-test (HPV + Pap) | ||

| By Product Type | Instruments and Analyzers | |

| Consumables and Reagents | ||

| Software Platforms | ||

| Services | ||

| By Technology | PCR / NAAT | |

| Hybrid Capture | ||

| mRNA-based Assays | ||

| Next-Generation Sequencing | ||

| By Application | Cervical Cancer Screening | |

| Vaginal Cancer Screening | ||

| Post-treatment Follow-up | ||

| Clinical Trials & Epidemiology | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the HPV testing and pap test market by 2031?

The market is projected to reach USD 12.58 billion by 2031, reflecting a 10.63% CAGR from 2026.

Which test type is growing fastest?

Molecular HPV tests are advancing at 11.26% CAGR due to guideline changes that prioritize HPV primary screening.

Which region offers the highest growth potential?

Asia-Pacific is expanding at 14.97% CAGR, underpinned by large-scale public screening programs in China and India.

How are software platforms influencing industry revenues?

AI-driven software is growing at 12.35% CAGR, providing high-margin subscription income that complements reagent sales.

What impact will HPV vaccination have on future screening volumes?

Rising vaccination coverage may trim long-term demand, but extended genotyping and post-treatment surveillance keep testing essential through the 2030s.

Page last updated on: