High Energy Lasers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

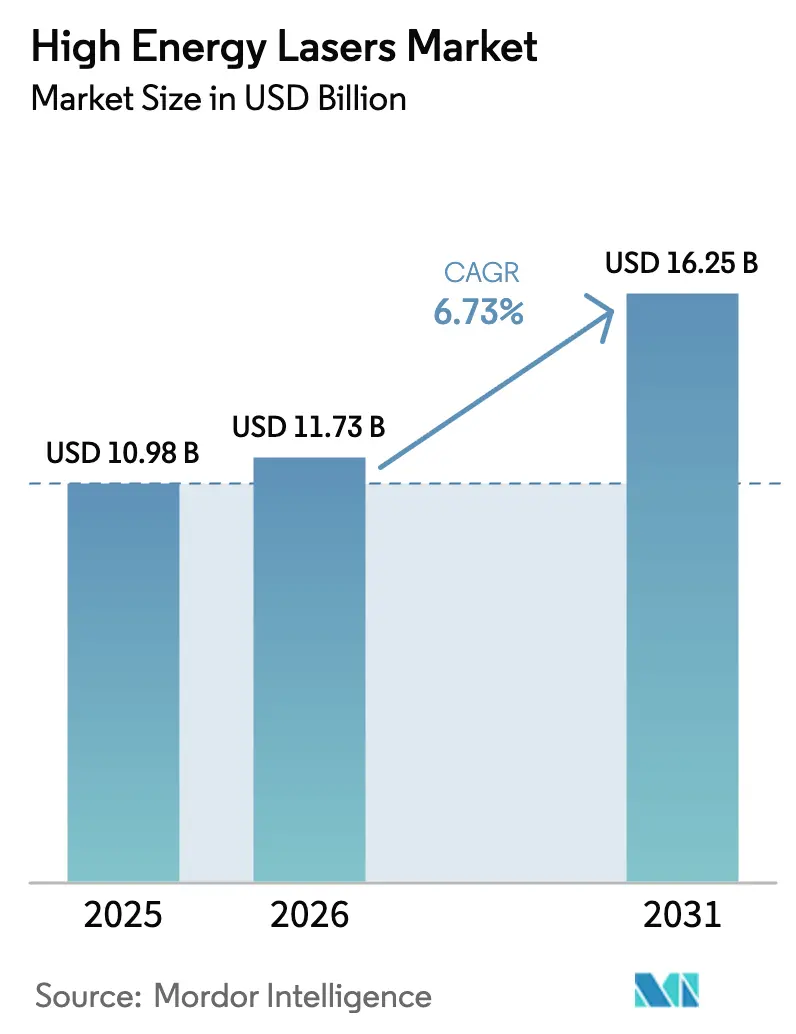

| Market Size (2026) | USD 11.73 Billion |

| Market Size (2031) | USD 16.25 Billion |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

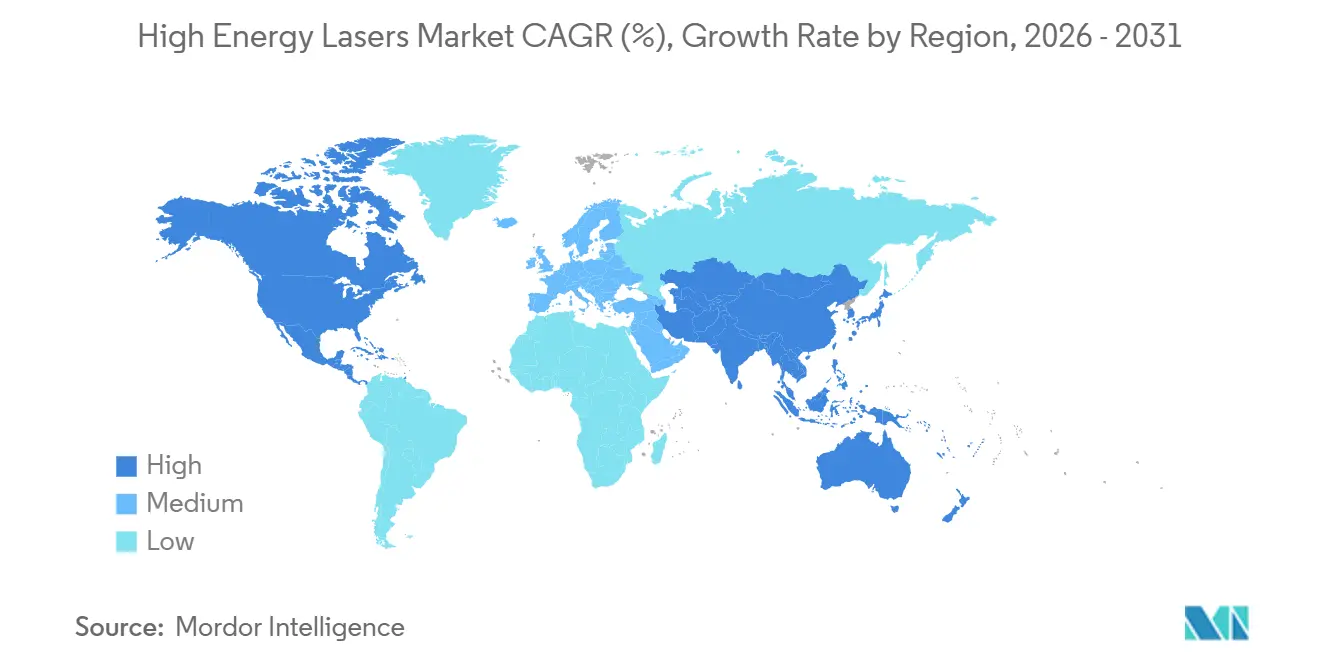

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

High Energy Lasers Market Analysis by ���ϲ�����

The High Energy Lasers Market size is expected to increase from USD 10.98 billion in 2025 to USD 11.73 billion in 2026 and reach USD 16.25 billion by 2031, growing at a CAGR of 6.73% over 2026-2031. Demand momentum is shifting from experimental trials toward routine field deployment as government customers emphasize cost-per-shot savings, power-scaling breakthroughs, and interoperability with AI-enabled command-and-control networks. Fiber architectures command attention because spectral beam combining raises output beyond 100 kW without proportional thermal penalties, while solid-state and gas designs cede share. Communications payloads on satellites, aircraft, and high-altitude platforms are accelerating adoption outside factory floors, opening fresh revenue for suppliers that historically served welding and cutting lines. Corporate strategies increasingly revolve around cross-border teaming, typified by Lockheed Martin and Rafael, because no single vendor controls all subsystems spanning diodes, beam control, power electronics, and fire-control software.

Key Report Takeaways

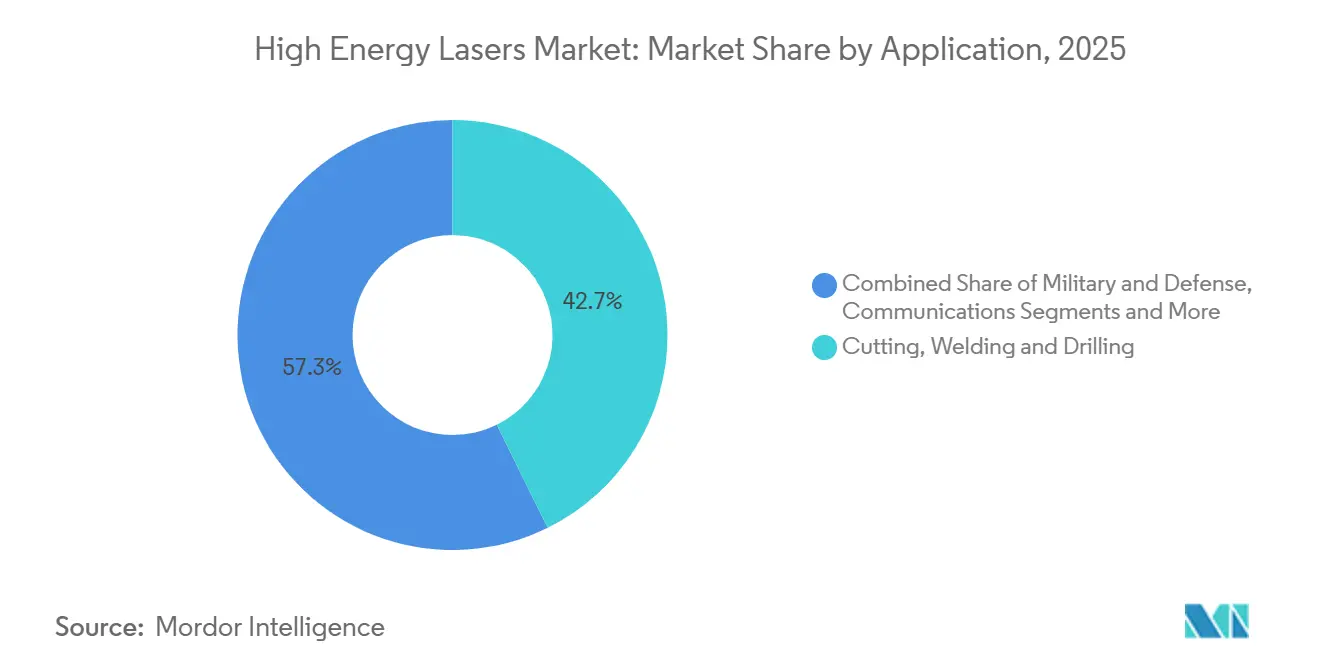

- By application, cutting, welding, and drilling led with 42.70% of High Energy Lasers Market share in 2025, while communications is the fastest growing segment at an 8.12% CAGR through 2031.

- By laser type, fiber lasers captured 55.71% share of the High Energy Lasers Market size in 2025 and are projected to expand at a 7.23% CAGR to 2031.

- By power output, systems above 100 kW are advancing at an 8.69% CAGR between 2026-2031, the quickest pace among all ranges.

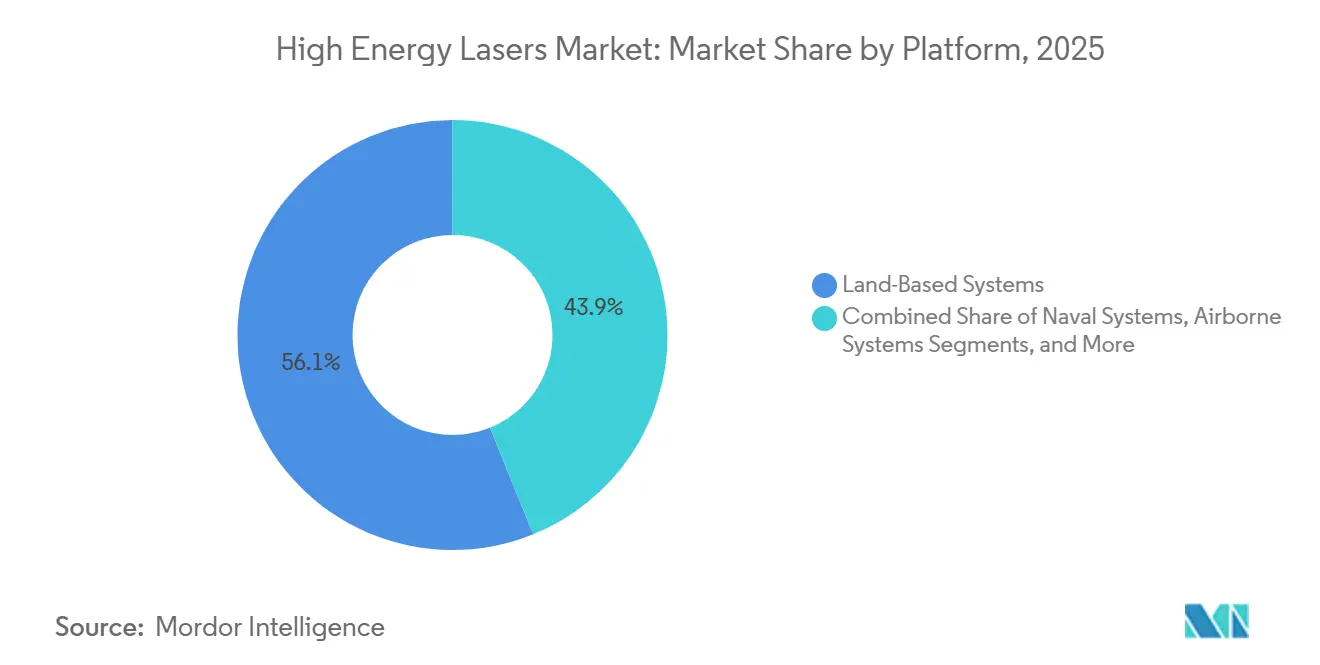

- By platform, land-based systems held 56.12% share in 2025, yet space-based platforms are rising at a 7.14% CAGR as satellite operators move to optical links.

- By end user, industrial manufacturing dominated with 52.74% share in 2025, whereas aerospace and defense is growing at a 6.89% CAGR on the back of counter-drone programs.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Energy Lasers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Directed-Energy Defense Budgets Among Major Powers | +1.8% | North America, Europe, Israel, India, South Korea | Medium term (2-4 years) |

| Demand for Cost-Per-Shot Reduction Versus Conventional Munitions | +1.5% | Middle-East littorals, Asia-Pacific naval corridors | Short term (≤ 2 years) |

| Rapid Advancements in Beam-Combining and Thermal Management Techniques | +1.2% | North America, Europe, advanced Asian manufacturing hubs | Long term (≥ 4 years) |

| Integration of AI-Enabled Targeting for Precision and Low-Collateral Damage | +0.9% | Early adoption in North America and Israel | Medium term (2-4 years) |

| Fiber Laser Efficiency and Scalability Driving Industrial Adoption | +0.7% | Global automotive, electronics, and machinery clusters | Short term (≤ 2 years) |

| Above-100 kW Power Scaling Unlocking New Military Missions | +0.6% | United States, Israel, China, India | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Escalating Directed-Energy Defense Budgets Among Major Powers

Defense ministries are reallocating procurement funds toward lasers because inexpensive drones and rockets saturate missile magazines. The United States appropriated USD 1.2 billion for Israel’s Iron Beam in April 2024, a figure that eclipses many interceptor line items.[1]Jon Harper, “US to Give Israel $1.2B for Iron Beam,” Defensescoop.comIndia is financing 30 kW and 300 kW prototypes for naval and border security, while South Korea placed a USD 132 million order for serial production of its 20 kW Block I system. These budgets position the High Energy Lasers Market for steady multi-year program funding rather than sporadic demonstrations.

Demand for Cost-Per-Shot Reduction Compared to Conventional Munitions

Lasers are revolutionizing military economics, significantly reducing costs from tens of thousands of dollars per missile to mere single-digit electricity expenses per shot. For example, each round of the Iron Dome system costs approximately USD 50,000, whereas interceptions carried out by the Iron Beam system are estimated to cost just about USD 2.[2]Clement Charpentreau, “What Is Israel's Iron Beam Laser Anti-Air System?,” Aerotime.aero Similarly, the UK's DragonFire laser weapon system demonstrates comparable single-digit cost efficiency. This dramatic reduction in operational expenses has garnered significant interest from Middle-Eastern nations, particularly due to their ongoing challenges with persistent drone swarms targeting critical infrastructure. The ability to deploy cost-effective and efficient laser systems offers a strategic advantage in addressing these threats. Additionally, the benefits of short supply chains and enhanced magazine depth make lasers an especially compelling option for naval ships. These vessels often operate in high-tempo engagement scenarios where the risk of ammunition depletion could compromise mission success, making the adoption of laser technology a critical consideration.

Rapid Advancements in Beam-Combining and Thermal Management Techniques

By stacking dozens of fiber outputs into a single coherent column, spectral beam combining enables suppliers to significantly exceed the 100 kW threshold without the risk of overheating. This advanced method has proven to be a game-changer in high-power laser systems. In 2024, Lockheed Martin successfully delivered a 300 kW-class prototype to the Pentagon, showcasing the potential of this innovative technique. Designers now benefit from enhanced integration flexibility, thanks to the incorporation of liquid cooling loops, compact heat exchangers, and additive-manufactured cold plates. These technological advancements not only improve thermal management but also reduce system footprints, making it feasible to mount these systems on tactical trucks and frigates, thereby expanding their operational versatility.

Integration of AI-Enabled Targeting for Precision and Low-Collateral Damage

In mere milliseconds, machine-learning algorithms classify, prioritize, and cue beams with remarkable efficiency. Lockheed Martin's Maneuver Short-Range Air Defense demonstrator effectively harnesses advanced computer vision technology to optimize dwell time across a fleet of drones, ensuring enhanced operational performance. Furthermore, AI's unparalleled precision in energy placement significantly mitigates fragmentation risks, which is especially crucial in densely populated urban areas. This capability aligns with the increasingly stringent rules-of-engagement standards, addressing critical safety and operational requirements.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal Blooming Limitations in High-Humidity or Dusty Environments | -1.1% | Tropical littorals, Middle-East deserts, South & Southeast Asia | Short term (≤ 2 years) |

| Stringent Export Control Regimes on Directed-Energy Technologies | -0.8% | Global, especially cross-border defense programs | Medium term (2-4 years) |

| Power Supply and Cooling Constraints on Mobile Platforms | -0.6% | Global naval and airborne integrators | Medium term (2-4 years) |

| Line-of-Sight and Weather Dependency Limiting Engagement Windows | -0.5% | Mountainous and high-latitude theaters | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Thermal Blooming Limitations in High-Humidity or Dusty Environments

Under high humidity conditions, atmospheric turbulence can significantly reduce beam intensity by as much as 40% at altitudes ranging between 5-8 km. This substantial reduction in beam intensity creates operational challenges, compelling operators to maintain backup interceptors to ensure system reliability and effectiveness. Although adaptive optics can help address this issue by compensating for the effects of turbulence, their implementation introduces additional weight and cost to the system. These added factors ultimately compromise the mobility and efficiency of the overall setup, posing further constraints for operators.

Stringent Export Control Regimes on Directed-Energy Technologies

Foreign sales face significant throttling due to the stringent regulations imposed by Category XII of the U.S. Munitions List and the Wassenaar Arrangement. These regulatory frameworks are designed to control the export of sensitive technologies, including high-energy laser systems, to ensure national security and prevent misuse. However, these restrictions result in extended lead times ranging from 12 to 24 months, thereby creating substantial delays in the supply chain and delivery timelines. Additionally, these measures contribute to the fragmentation of the addressable base within the High Energy Lasers Market, further complicating market dynamics, limiting the potential customer base, and hindering growth opportunities for manufacturers and suppliers operating in this space.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Communications Systems Gain Velocity

In 2025, cutting, welding and drilling held a dominant 42.70% share of the High Energy Lasers Market, driven by automakers and aerospace fabricators turning to fiber beams for precise alloy trimming. This segment's prominence highlights the critical role of high-energy lasers in achieving precision and efficiency in industrial applications. Meanwhile, communications platforms are on the rise, boasting an 8.12% CAGR. This growth underscores satellite operators' pursuit of terabit cross-links, allowing them to bypass congested radio frequencies and improve data transmission capabilities. Such a shift not only highlights the evolving landscape but also broadens revenue streams for suppliers, moving away from the traditional cyclical manufacturing reliance. The diversification of revenue pools is expected to provide stability and growth opportunities for market players in the long term.

The growing adoption of communications is bolstering the demand for components like narrow-linewidth emitters and indium phosphide modulators. These components are essential for enabling high-performance optical systems, which are increasingly critical in modern communication networks. Notably, Coherent ramped up its output of these critical components threefold in 2025 to meet the surging demand. Furthermore, military bandwidth requirements underscore this trend; optical terminals are now pivotal, transmitting reconnaissance data from low-Earth-orbit constellations to ground analysts in mere seconds. This capability significantly enhances the efficiency of military operations by compressing kill chains and enabling faster decision-making processes. The crossover between commercial and military applications further emphasizes the strategic importance of high-energy laser technologies in addressing diverse market needs.

By Laser Type: Fiber Architectures Extend Lead

Fiber lasers secured 55.71% High Energy Lasers Market share in 2025 and will expand at 7.23% CAGR through 2031 as electrical-to-optical conversion efficiencies above 40% outclass legacy gas and chemical units.[3]TRUMPF SE + Co. KG, “Annual Report 2024/25,” trumpf.comSpectral combining lets integrators stack modules without physics rewrites, trimming non-recurring engineering costs.

Free-electron and chemical alternatives linger in laboratory niches because of size and toxicity hurdles. Their limited field readiness keeps procurement officers centered on fiber pathways, reinforcing economies of scale that lower price per watt for industrial customers.

By Power Output: >100 kW Systems Unlock New Missions

As armies increasingly target 7 km intercept envelopes to effectively neutralize threats such as rockets, artillery, and cruise missiles, systems exceeding 100 kW are experiencing the fastest growth, with a remarkable CAGR of 8.69%. By 2031, the High Energy Lasers Market for this segment is projected to double in size, creating significant opportunities for integrators who excel in addressing challenges like thermal lensing mitigation. This growth highlights the strategic importance of high-power laser systems in modern defense applications.

Meanwhile, lower power bands, particularly in the 1-5 kW range, continue to dominate in terms of volume, primarily serving the needs of sheet-metal shops. However, Western sellers in this segment are increasingly facing margin pressures due to the rising competition from low-cost Asian imports. On the other hand, premium units exceeding 100 kW not only avoid the risks of commoditization but also offer additional value through service contracts, which include maintenance for chillers and optics refurbishment. These high-power systems represent a more sustainable and profitable segment for manufacturers and service providers in the market.

By Platform: Space-Based Installations Accelerate

In 2025, land-based systems captured 56.12% of the revenue, primarily due to their straightforward grid access, which simplifies the power supply process. These platforms benefit from established infrastructure, making them a dominant segment in the market. Meanwhile, space-based terminals, despite holding a smaller market share, are projected to grow at a notable 7.14% CAGR. This growth is largely driven by the increasing adoption of optical inter-satellite links by broadband constellations, which facilitate the global transmission of AI training data. The rising demand for high-speed data transfer and advancements in satellite technology further contribute to the expansion of this segment.

Naval combatants are emerging as the next frontier for laser technology applications. With features such as corrosion-resistant housings and 360-degree turrets, lasers are becoming an ideal solution for defending against drone swarms, which pose a significant threat in modern naval warfare. The ability of lasers to provide precise targeting and rapid response enhances their appeal in this domain. However, airborne adoption of laser systems continues to lag behind due to the challenges posed by 100 kW loads, which strain the capacity of existing generators. Despite these challenges, ongoing advancements in gallium-nitride power electronics are expected to address these limitations. By the end of the forecast period, these technological improvements could significantly close the gap, enabling broader adoption of laser systems in airborne platforms.

By End User: Defense Momentum Outpaces Industrial Cycles

In 2025, industrial manufacturing commanded a dominant 52.74% share of the High Energy Lasers Market. However, the aerospace and defense sector is poised for a more robust growth, boasting a projected CAGR of 6.89% through 2031. This surge is largely driven by fleet modernizations that are increasingly integrating lasers into counter-UAV systems. Meanwhile, research institutes are churning out groundbreaking intellectual property, which is swiftly transitioning to vendors. On another front, telecom carriers are experimenting with free-space optics for 5G backhaul, especially in areas where fiber build-outs are lagging.

The increasing adoption of high-energy lasers across various industries highlights their versatility and potential for innovation. In industrial manufacturing, these lasers are being utilized for precision cutting, welding, and material processing, driving efficiency and productivity. Similarly, the aerospace and defense sector is leveraging these technologies to enhance security and operational capabilities. As research institutes continue to develop advanced laser technologies, their commercialization is expected to further expand the market. Additionally, the exploration of free-space optics by telecom carriers underscores the growing demand for alternative solutions to address connectivity challenges in underserved regions.

Geography Analysis

High Energy Lasers Market in North America

In 2025, North America secured 40.01% of the High Energy Lasers Market revenue, bolstered by Pentagon initiatives like the Navy's HELIOS and the Army's Indirect Fire Protection Capability. The region's industrial adoption of high-energy lasers is particularly evident in the Midwest, where automotive body-in-white welding has become a focal point, and in the Southeast, where turbine machining activities are thriving. Meanwhile, Canadian strategists are exploring the establishment of Arctic laser sites to address the logistical challenges associated with resupplying interceptors across vast and remote distances.

Asia-Pacific, led by China's cost-effective fiber production and India's self-funded 30 kW and 300 kW weapons (backed by a USD 200 million investment), boasts the world's fastest growth at a 7.47% CAGR. The region's rapid expansion is further highlighted by South Korea's deployment of a 20 kW laser in 2024, which underscores the increasing technological capabilities within the area. Additionally, Japanese electronics firms are increasingly turning to lasers for automation purposes, a strategic move aimed at countering labor shortages while ensuring a steady and reliable base-load demand for high-energy laser systems.

Europe presents a mixed bag of trends. Germany's machine-tool exporters play a significant role in underpinning industrial sales, while the United Kingdom's DragonFire successfully completed sea trials in 2025, marking a notable achievement in the region's defense capabilities. However, Southern Europe's budget constraints and stringent export regulations have tempered the overall momentum of the high-energy lasers market in the region. In the Middle East, Israel's operationalization of the Iron Beam in 2025, along with Gulf states' increasing interest in acquiring similar advanced defense systems, signals a rapid acceleration in the adoption of high-energy laser technologies. Africa and South America remain in the nascent stages of market development; however, Brazil's burgeoning aerospace sector shows promise as a potential future hub for laser-driven additive manufacturing, which could significantly contribute to the region's industrial growth in the coming years.

Competitive Landscape

Top Companies in High Energy Lasers Market

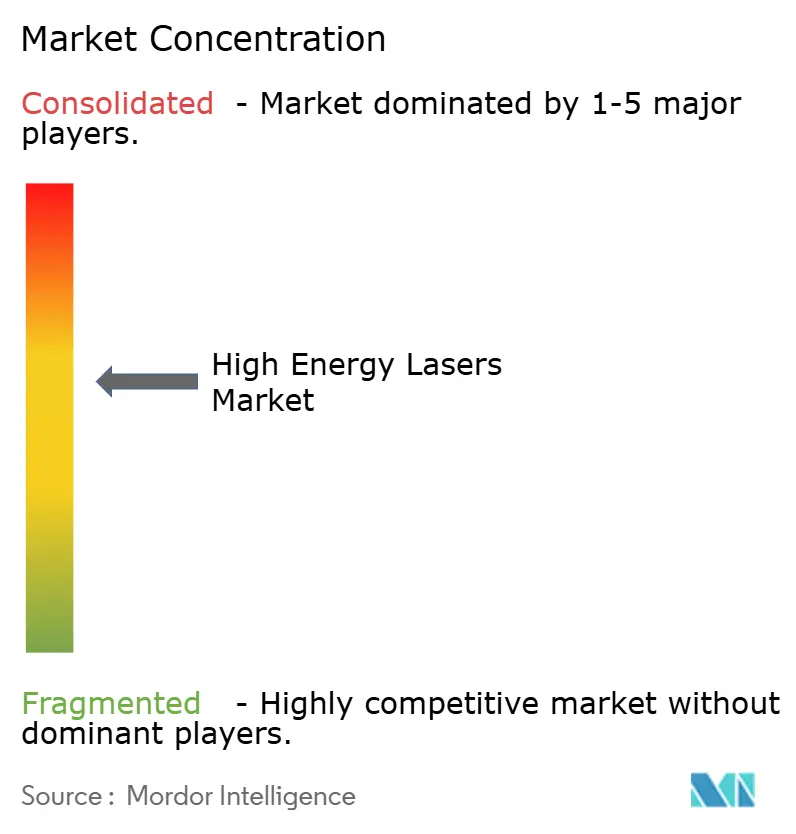

Moderate concentration characterizes the High Energy Lasers Market. The top five suppliers, Lockheed Martin, Raytheon, Northrop Grumman, TRUMPF, and IPG Photonics, command a combined share of about 65%. This significant concentration leads to a market score of 6, indicating a moderately consolidated market structure. Partnerships are increasingly prevalent, with primary players strategically sourcing beam modules from photonics specialists to enhance their technological capabilities. A notable example is Lockheed Martin’s collaboration with Rafael, aimed at co-producing 300 kW lasers for U.S. forces. This partnership underscores the growing synergy between U.S. system integrators and Israeli beam experts, reflecting a trend of cross-border cooperation to leverage specialized expertise.

Facing a slowdown in cutter sales, industrial vendors are pivoting towards defense applications to sustain growth and profitability. TRUMPF’s 2024 move to restrict military engagements to defensive applications, alongside a joint effort with Rohde & Schwarz to develop drone-defense systems, underscores this strategic shift. This realignment highlights the increasing focus on addressing emerging defense needs, such as counter-drone technologies, which are becoming critical in modern warfare. Meanwhile, IPG Photonics is transitioning to high-power diode platforms, which not only reduce size and cost but also enhance appeal for a broader range of applications. These include medical lithotripsy, where precision and efficiency are paramount, and naval interceptors, which demand robust and compact solutions for operational effectiveness.

Chinese players, Raycus and Han’s Laser, are capturing market share in the 1-10 kW segments by offering prices up to 30% lower than their Western counterparts. This aggressive pricing strategy enables them to compete effectively in cost-sensitive markets, particularly in regions where affordability is a key purchasing criterion. Export controls, particularly under ITAR and Wassenaar, limit U.S. and EU vendors from accessing markets in Asia and the Middle East. These restrictions create significant barriers for Western companies, occasionally nudging customers towards Chinese alternatives, which manage to bypass these constraints. As a result, Chinese manufacturers are steadily gaining traction in these regions, leveraging their ability to offer competitive pricing and navigate regulatory challenges more effectively.

High Energy Lasers Industry Leaders

IPG Photonics

TRUMPF Pvt. Ltd.

Coherent, Inc

nLight Inc.

BAE Systems plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Rafael delivered Israel’s first operational 100 kW Iron Beam laser shield to the Israel Defense Forces.

- December 2024: Coherent secured a preliminary USD 33 million CHIPS Act grant to expand indium phosphide wafer capacity in Texas.

- October 2024: Israel signed a USD 500 million production contract for Iron Beam components with Rafael and Elbit.

- October 2024: IPG Photonics agreed to acquire cleanLASER for USD 75 million to enter laser cleaning verticals.

Global High Energy Lasers Market Report Scope

High-energy lasers are used in numerous industries, with applications ranging across the defense, industrial, and medical sectors. Correctly, military lasers (lasers with a higher degree of photon output and coherence) such as gas, solid-state, and excimer lasers are used in core industries such as material processing and automotive.

The High Energy Lasers Market Report is Segmented by Application (Cutting, Welding and Drilling, and More), Laser Type (Gas, Chemical, Excimer, Solid State, and More), Power Output (Up to 10 kW, 11–50 kW, 51–100 kW, and Above 100 kW), Platform (Land, Naval, Airborne, and Space), End User (Defense, Industrial, Aerospace, Research, Telecom, and More), and Geography. Market Forecasts are Provided in Value (USD).

| Cutting, Welding and Drilling |

| Military and Defense |

| Communications |

| Other Applications |

| Gas Lasers |

| Chemical Lasers |

| Excimer Lasers |

| Solid State Lasers |

| Fiber Lasers |

| Free-Electron Lasers |

| Other Laser Types |

| Up to 10 kW |

| 11–50 kW |

| 51–100 kW |

| Above 100 kW |

| Land-Based Systems |

| Naval Systems |

| Airborne Systems |

| Space-Based Systems |

| Defense |

| Industrial Manufacturing |

| Aerospace and Aviation |

| Research Institutions |

| Telecommunications |

| Other End-Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Application | Cutting, Welding and Drilling | ||

| Military and Defense | |||

| Communications | |||

| Other Applications | |||

| By Laser Type | Gas Lasers | ||

| Chemical Lasers | |||

| Excimer Lasers | |||

| Solid State Lasers | |||

| Fiber Lasers | |||

| Free-Electron Lasers | |||

| Other Laser Types | |||

| By Power Output | Up to 10 kW | ||

| 11–50 kW | |||

| 51–100 kW | |||

| Above 100 kW | |||

| By Platform | Land-Based Systems | ||

| Naval Systems | |||

| Airborne Systems | |||

| Space-Based Systems | |||

| By End User | Defense | ||

| Industrial Manufacturing | |||

| Aerospace and Aviation | |||

| Research Institutions | |||

| Telecommunications | |||

| Other End-Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is global demand for high-energy laser weapons growing?

The High Energy Lasers Market is forecast to expand at a 6.73% CAGR from 2026-2031, driven by defense budgets and satellite communications rollouts.

Which laser architecture holds the largest revenue share?

Fiber lasers led with 55.71% of total revenue in 2025 due to high electrical efficiency and scalable beam combining.

Why are systems above 100 kW attracting attention?

Output over 100 kW enables interception of rockets and cruise missiles at ranges near 7 km, prompting an 8.69% CAGR for this power segment.

Which region is the fastest growing buyer of high-energy lasers?

Asia-Pacific is advancing at 7.47% CAGR as China and India invest in indigenous production and military deployment.

Page last updated on: