Herbal Fragrance Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.53 Billion |

| Market Size (2030) | USD 6.86 Billion |

| Growth Rate (2026 - 2031) | 8.65% CAGR |

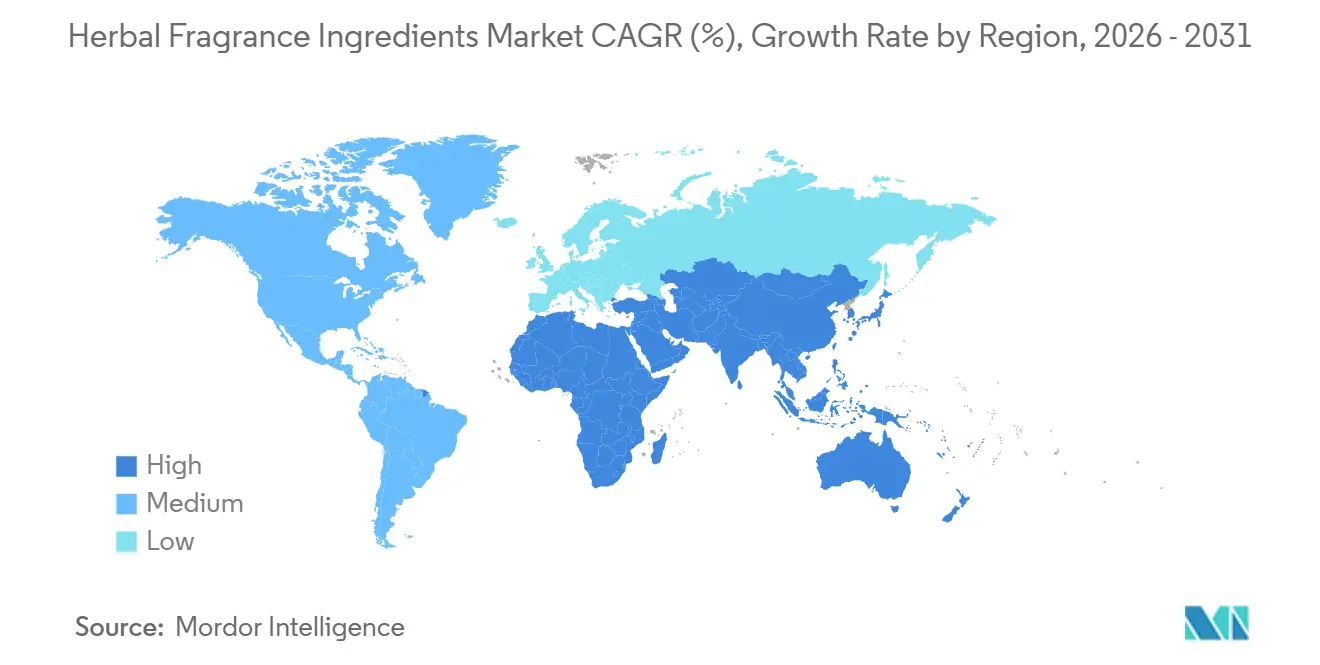

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Herbal Fragrance Ingredients Market Analysis by ���ϲ�����

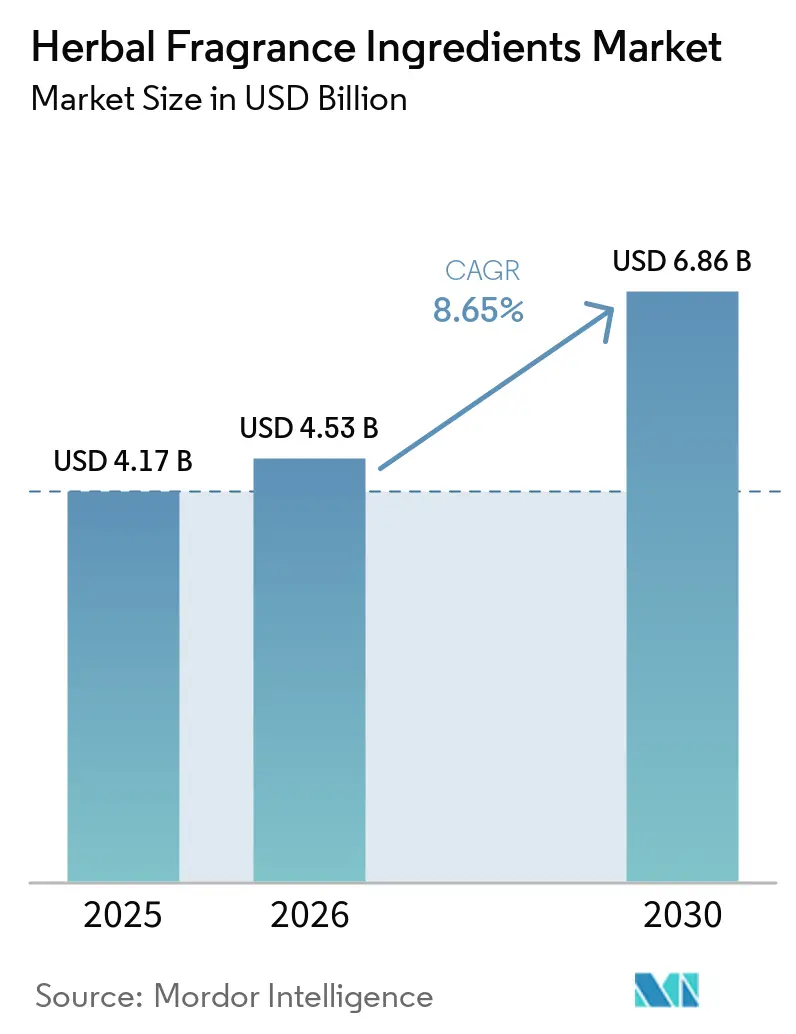

The herbal fragrance ingredients market size is expected to grow from USD 4.17 billion in 2025 to USD 4.53 billion in 2026 and is forecast to reach USD 6.86 billion by 2031 at 8.65% CAGR over 2026-2031. Consumers are increasingly prioritizing clean beauty and environmental values, driving significant growth in the demand for plant-based and natural fragrances. Companies are actively developing products infused with herbal ingredients such as lavender, rosemary, and chamomile, which are widely recognized for their therapeutic and mood-enhancing benefits. This trend is particularly evident in premium personal care products, niche perfumes, and spa aromatherapy offerings across global markets. Additionally, regulatory authorities are enforcing stricter limitations on synthetic chemicals, while climate-induced pressures on crop production are pushing brands to adopt plant-based alternatives. Companies are leveraging advancements in biotechnology to address raw material volatility and shorten production timelines, ensuring consistent and reliable yields for high-demand oils like vanilla, sandalwood, and citrus. In this competitive environment, brands with certified supply chains, robust safety documentation, and sustainable extraction methods are gaining a competitive edge.

Key Report Takeaways

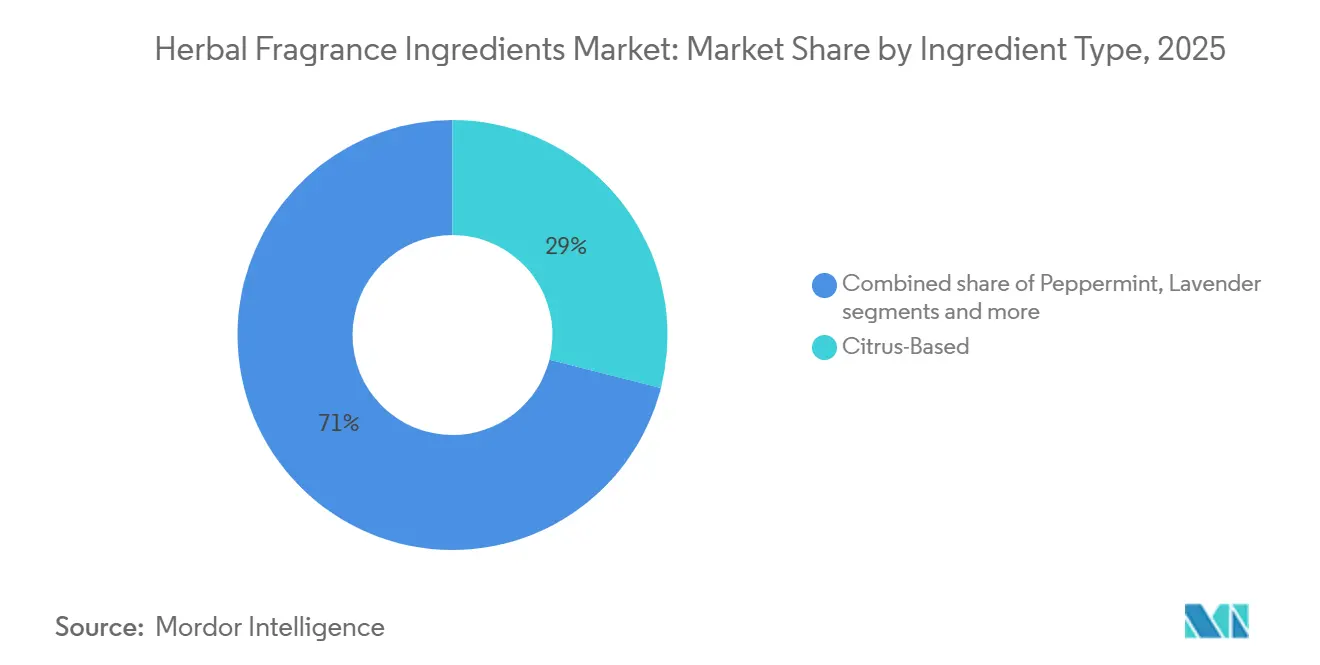

- By product type, citrus-based ingredients led with 28.96% of the herbal fragrance ingredients market share in 2025, whereas rosemary is projected to expand at a 9.12% CAGR through 2031.

- By form, liquid formats held 72.45% of the herbal fragrance ingredients market size in 2025, while powder variants represent the fastest trajectory at a 10.36% CAGR to 2031.

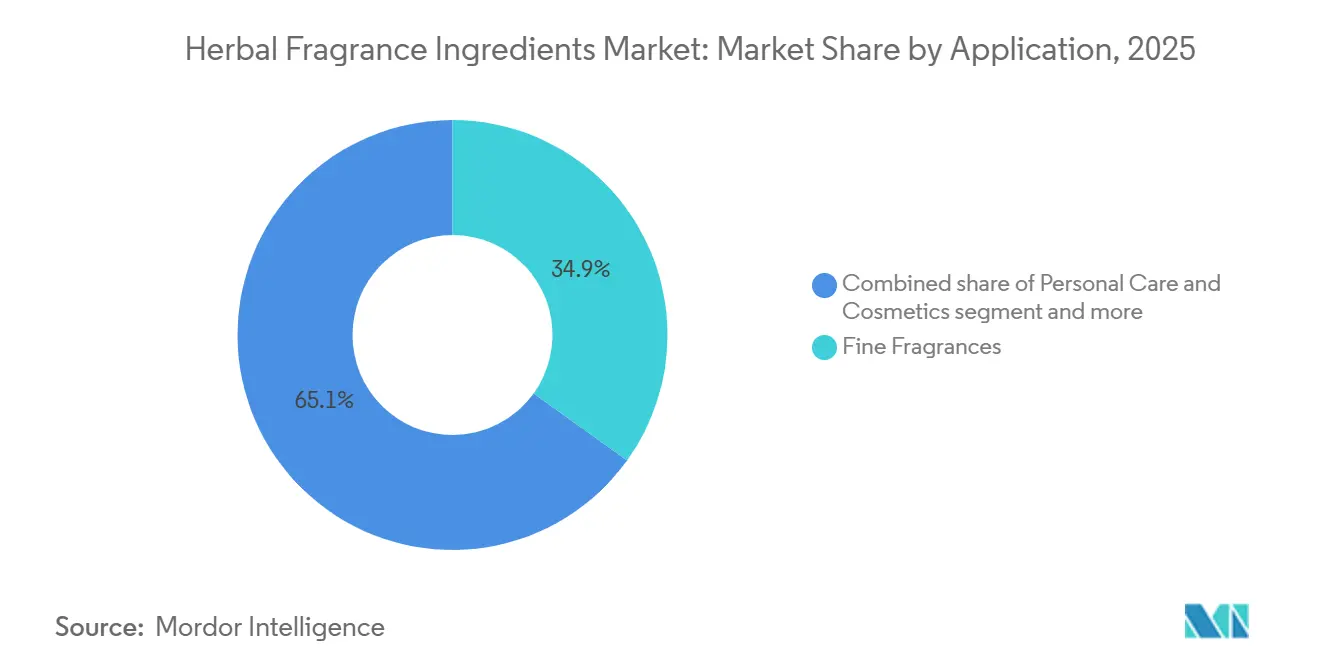

- By application, fine fragrances captured 34.93% of 2025 revenue, but aromatherapy and wellness is advancing at 9.47% CAGR through 2031.

- By geography, Europe commanded 33.76% 2025 revenue, yet Asia-Pacific is the fastest-growing region at 9.19% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Herbal Fragrance Ingredients Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for natural and plant-based fragrance ingredients | +2.2% | Global, with concentrated demand in North America, Western Europe, and urban Asia-Pacific | Medium to Long term (2-5 years) |

| Growing demand for clean-label and chemical-free personal care products | +1.9% | North America and EU, spillover to Australia, Japan, and urban China | Short to Medium term (1-3 years) |

| Increasing use of herbal fragrances in aromatherapy and wellness applications | +1.7% | Global, with early adoption in North America, EU, and premium segments in China and India | Medium term (2-4 years) |

| Expansion of natural cosmetics and organic beauty product launches | +1.5% | North America, EU, and Asia-Pacific urban centers, with regulatory support in France, Germany, and South Korea | Medium term (2-4 years) |

| Rising awareness regarding adverse effects of synthetic fragrances | +1.3% | Global, with regulatory acceleration in EU and North America | Long term (3-5 years) |

| Growing demand from premium and niche perfumery segments | +1.1% | North America, Western Europe, Middle East (Gulf states), and affluent Asia-Pacific markets (Japan, Singapore, Hong Kong) | Medium to Long term (2-5 years) |

| Source: ���ϲ����� | |||

Rising consumer preference for natural and plant-based fragrance ingredients

Rising consumer preference for natural and plant-based fragrance ingredients is a key driver of the herbal fragrance ingredients market, as buyers increasingly prioritize clean-label and toxin-free personal care products. Consumers are shifting away from synthetic fragrances and opting for botanical alternatives derived from herbs, flowers, and essential oils due to their perceived safety and wellness benefits. This trend is particularly strong in skincare, perfumes, and home fragrance applications where natural scent profiles are associated with authenticity and sustainability. According to the The Public Health and Safety Organization (NSF) March 2025 report, 74% of consumers consider organic ingredients important in personal care products, highlighting growing demand for clean formulations without harmful additives. The report also noted that 45% of respondents are willing to pay a premium for certified products with organic ingredients, reflecting strong perceived value[1]Source: Public Health and Safety Organization (NSF), "74% of Consumers Consider Organic Ingredients Important in Personal Care Products", nsf.org . This willingness to spend more encourages manufacturers to incorporate herbal fragrance components and emphasize certification claims. Additionally, brands are expanding portfolios with essential oil-based and plant-derived fragrance solutions to meet evolving consumer expectations.

Growing demand for clean-label and chemical-free personal care products

The increasing demand for clean-label and chemical-free personal care products is driving growth in the herbal fragrance ingredients market. Consumers are becoming more conscious of ingredient transparency and are actively seeking formulations free from synthetic fragrances, parabens, and harsh chemicals. This shift is encouraging manufacturers to utilize plant-derived fragrance ingredients sourced from herbs, flowers, and botanical extracts. Herbal fragrance components are perceived as safer and more compatible with sensitive skin, further supporting their adoption in skincare, haircare, and cosmetic products. According to research by CBI Ministry of Foreign Affairs, clean-label products are expected to account for over 70% of product portfolios in 2025 and 2026, rising from 52% in 2021[2] Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities", cbi.eu. This significant increase highlights the growing importance of natural and recognizable ingredients across personal care categories. As brands prioritize minimal ingredient lists and chemical-free claims, demand for herbal fragrance ingredients continues to expand.

Increasing use of herbal fragrances in aromatherapy and wellness applications

Increasing use of herbal fragrances in aromatherapy and wellness applications is a key driver of the herbal fragrance ingredients market. Consumers are increasingly adopting holistic health practices that focus on relaxation, stress relief, and mental well-being, boosting demand for natural fragrance solutions. Herbal ingredients such as lavender, rosemary, eucalyptus, and chamomile are widely used in essential oils, diffusers, massage oils, and spa products. These ingredients are valued for their calming, therapeutic, and mood-enhancing properties. The growth of wellness centers, yoga studios, and home aromatherapy practices is further accelerating market adoption. Additionally, rising consumer preference for natural and plant-based wellness products is encouraging manufacturers to expand herbal fragrance formulations. This trend is significantly strengthening the demand for herbal fragrance ingredients globally.

Rising awareness regarding adverse effects of synthetic fragrances

Rising awareness regarding the adverse effects of synthetic fragrances is significantly driving demand for herbal fragrance ingredients across personal care, cosmetics, and home care applications. Consumers are becoming more cautious about the potential health risks associated with synthetic fragrance compounds, including skin irritation, contact dermatitis, and respiratory sensitization. This growing concern is encouraging a shift toward natural, plant-based fragrance alternatives derived from herbs, flowers, and essential oils. Epidemiological studies linking synthetic fragrance compounds to contact dermatitis and respiratory sensitization have further intensified scrutiny of chemical-based formulations. This has also led to stricter regulatory actions, most notably the European Union’s decision to expand allergen disclosure requirements from 26 to 82 substances by July 2026. Such regulatory developments are pushing manufacturers to reformulate products with safer, herbal-based fragrance ingredients[3]Source: European Commission, "Cosmetic Legislation", commission.europa.eu .

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of natural herbal extracts compared to synthetic alternatives | -1.3% | Global, with acute pressure in price-sensitive markets (India, Southeast Asia, Latin America, and mass-market segments in developed economies) | Short to Medium term (1-3 years) |

| Limited availability and seasonal supply of botanical raw materials | -1.0% | Global, with critical bottlenecks in Mediterranean (lavender, rosemary), Southeast Asia (patchouli, vetiver), and Madagascar (vanilla) | Short to Medium term (1-3 years) |

| Shorter shelf life and stability challenges of herbal fragrances | -0.8% | Global, with heightened impact in tropical and subtropical regions (Southeast Asia, Latin America, Middle East, Africa) where heat accelerates degradation | Short term (1-2 years) |

| Variability in fragrance consistency due to natural ingredient sourcing | -0.6% | Global, affecting all markets but particularly challenging for multinational brands requiring batch-to-batch uniformity across geographies | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High cost of natural herbal extracts compared to synthetic alternatives

High cost of natural herbal extracts compared to synthetic alternatives is a key restraint affecting the herbal fragrance ingredients market. The extraction of botanical ingredients such as essential oils and herbal concentrates involves complex processes like steam distillation, solvent extraction, and cold pressing, which significantly increase production costs. Additionally, the yield of active fragrance compounds from natural sources is often low, further elevating overall pricing. Seasonal availability of raw materials and dependence on agricultural output also contribute to supply volatility and cost fluctuations. Compared to synthetic fragrance ingredients, herbal alternatives require higher sourcing, processing, and quality control expenses. This cost disparity limits their adoption, particularly in price-sensitive markets and mass-market personal care products. Manufacturers often face challenges in balancing cost efficiency with consumer demand for natural formulations. As a result, the higher cost structure of herbal extracts continues to restrain broader market penetration despite growing demand for natural ingredients.

Limited availability and seasonal supply of botanical raw materials

Limited availability and seasonal supply of botanical raw materials is a significant restraint in the herbal fragrance ingredients market. The production of herbal fragrance ingredients depends heavily on agricultural output, which is influenced by climatic conditions, soil quality, and harvesting cycles. Many key botanicals such as lavender, rosemary, jasmine, and citrus oils are available only during specific seasons, leading to inconsistent supply throughout the year. Weather fluctuations, droughts, and environmental changes can further disrupt raw material availability and impact production stability. This seasonal dependency often results in supply-demand imbalances and price volatility in the market. Additionally, the need for large cultivation areas and long growth cycles for certain herbs limits scalability. Manufacturers also face challenges in maintaining consistent quality and fragrance profiles due to variations in raw material sourcing.

Segment Analysis

By Product Type: Citrus Dominance Meets Rosemary's Functional Surge

Citrus-based ingredients accounted for 28.96% of the herbal fragrance ingredients market in 2025, making them the largest product type segment. Their dominance is primarily driven by widespread use in perfumes, personal care products, home care formulations, and aromatherapy applications. Citrus notes such as lemon, orange, bergamot, and grapefruit are highly preferred for their fresh, clean, and uplifting scent profiles. These ingredients are commonly incorporated into soaps, shampoos, deodorants, and air fresheners due to their refreshing and energizing fragrance characteristics. In addition, citrus-based ingredients are often associated with natural and clean-label positioning, which aligns with growing consumer preference for plant-derived fragrances. Their versatility in blending with floral, woody, and herbal notes further enhances their adoption across multiple fragrance formulations.

Rosemary is projected to register the fastest growth, expanding at a CAGR of 9.12% through 2031. The increasing popularity of herbal and aromatherapy-based fragrance solutions is driving demand for rosemary-derived ingredients. Rosemary offers a distinctive fresh, herbal, and slightly woody aroma, making it suitable for natural perfumes, essential oil blends, and wellness products. The ingredient is also gaining traction in personal care products such as shampoos, skincare formulations, and massage oils due to its perceived therapeutic benefits. Growing consumer interest in stress relief, relaxation, and holistic wellness is further accelerating adoption of rosemary-based fragrances. Additionally, the shift toward natural and plant-based ingredients is encouraging manufacturers to incorporate rosemary into clean-label product formulations.

By Form: Liquid Dominance Versus Powder Innovation

Liquid formats accounted for 72.45% of the herbal fragrance ingredients market in 2025, making them the dominant form segment. Their leading position is primarily attributed to ease of blending and compatibility with a wide range of end-use applications such as perfumes, personal care products, and home fragrances. Liquid herbal fragrance ingredients are commonly used in formulations including lotions, shampoos, soaps, and air fresheners due to their uniform dispersion and consistent scent delivery. Additionally, liquid forms allow manufacturers to adjust fragrance intensity and create customized blends more efficiently. The strong demand from the cosmetics and personal care industry further supports the widespread adoption of liquid formats. These ingredients also offer better solubility in oil- and alcohol-based formulations, which are widely used in fragrance development.

Powder variants are projected to register the fastest growth, expanding at a CAGR of 10.36% through 2031. The growth of this segment is driven by increasing demand for dry formulations in personal care, home care, and functional product applications. Powdered herbal fragrance ingredients are gaining traction in products such as dry shampoos, talcum powders, detergent powders, and incense-based applications. These formats offer advantages such as longer shelf life, improved stability, and reduced risk of spillage compared to liquid forms. Additionally, powders are easier to transport and store, making them attractive for bulk manufacturing and export-oriented supply chains. The rising popularity of waterless and concentrated formulations is also contributing to the adoption of powdered fragrance ingredients. Manufacturers are increasingly incorporating encapsulated fragrance powders to provide controlled scent release in various applications.

By Application: Aromatherapy Disrupts Fine Fragrance's Traditional Lead

Fine fragrances accounted for 34.93% of the herbal fragrance ingredients market revenue in 2025, making it the largest application segment. The dominance of this segment is driven by strong demand for natural and plant-based fragrance components in perfumes and colognes. Consumers are increasingly preferring herbal and botanical scent profiles that offer a fresh, authentic, and premium sensory experience. Ingredients derived from citrus, lavender, rosemary, and other botanicals are widely used in fine fragrance formulations. In addition, luxury and niche perfume brands are incorporating herbal fragrance ingredients to differentiate their offerings and align with clean-label trends. The growth of premium personal care products and artisanal perfumery is also supporting demand within this segment.

Aromatherapy and wellness represent the fastest-growing application segment, projected to expand at a CAGR of 9.47% through 2031. This growth is fueled by rising consumer focus on mental well-being, relaxation, and holistic health practices. Herbal fragrance ingredients are widely used in essential oils, diffusers, massage oils, and spa products designed to promote stress relief and emotional balance. The increasing popularity of home wellness routines and aromatherapy-based relaxation solutions is further driving adoption. Consumers are also seeking natural fragrance ingredients that provide therapeutic benefits alongside pleasant aromas. Additionally, the expansion of wellness centers, spas, and premium home fragrance products is supporting segment growth. Manufacturers are introducing new herbal blends targeting sleep support, mood enhancement, and mindfulness applications.

Geography Analysis

Europe accounted for 33.76% of the herbal fragrance ingredients market revenue in 2025, making it the largest regional segment. The region’s leadership is supported by a well-established fragrance and cosmetics industry, particularly in countries such as France, Germany, Italy, and the United Kingdom. Strong consumer preference for natural and botanical-based perfumes and personal care products is driving demand for herbal fragrance ingredients. Additionally, the presence of leading fragrance manufacturers and luxury perfume brands contributes to continuous innovation and product development. Regulatory emphasis on clean-label and sustainable ingredients further encourages the use of plant-derived fragrance components. The growing demand for organic personal care and premium fine fragrances also supports market growth in Europe.

Asia-Pacific is projected to register the fastest growth, expanding at a CAGR of 9.19% through 2031. Rapid urbanization, rising disposable incomes, and expanding middle-class populations are driving demand for personal care and fragrance products across the region. Countries such as China, India, Japan, and South Korea are witnessing increased consumption of herbal and natural fragrance formulations. Growing awareness of wellness, aromatherapy, and traditional botanical ingredients is further supporting market expansion. In addition, local manufacturers are incorporating regionally sourced herbs into perfumes, home fragrances, and personal care applications. The increasing popularity of clean-label cosmetics and natural beauty products is also contributing to strong growth.

North America represents a mature yet steadily growing market, supported by rising demand for clean-label and plant-based fragrance ingredients in cosmetics and home care products. Consumers in the United States and Canada are increasingly adopting aromatherapy, natural perfumes, and wellness-oriented fragrance solutions. South America is witnessing moderate growth, driven by increasing use of botanical ingredients in personal care and home fragrance products, particularly in Brazil and Argentina. Meanwhile, the Middle East and Africa region is gradually expanding due to rising demand for premium perfumes and traditional herbal fragrance oils.

Competitive Landscape

The herbal fragrance ingredients market exhibits moderate concentration, with a mix of large multinational fragrance manufacturers and specialized botanical ingredient suppliers competing for market share. Major players maintain strong positions through diversified product portfolios, global sourcing networks, and long-standing relationships with personal care and fragrance brands. At the same time, smaller regional companies focus on niche offerings such as organic essential oils, sustainably sourced botanicals, and customized herbal blends. This structure encourages innovation while allowing new entrants to compete through differentiated natural ingredients. Companies are increasingly emphasizing traceability, purity, and sustainable sourcing to strengthen their competitive positioning. Additionally, partnerships with cosmetic, home care, and aromatherapy brands are helping suppliers expand their customer base.

Leading companies are investing significantly in research and development to introduce innovative herbal fragrance ingredients with improved stability and performance. Product innovation is focused on natural extracts, essential oil blends, and encapsulated fragrance technologies that enhance longevity and controlled scent release. Manufacturers are also expanding their portfolios to include certified organic, vegan, and clean-label fragrance ingredients to align with evolving consumer preferences. Strategic product launches and collaborations with personal care and fine fragrance brands are commonly adopted to strengthen market presence. In addition, companies are enhancing production capabilities and improving extraction technologies to ensure consistent quality.

Mergers, acquisitions, and geographic expansion activities are further shaping the competitive landscape of the herbal fragrance ingredients market. Companies are acquiring smaller botanical extract producers to secure raw material supply and access proprietary extraction techniques. Expansion into fast-growing regions such as Asia-Pacific and the Middle East is also becoming a priority for market participants. Additionally, firms are focusing on sustainable sourcing partnerships with farmers to ensure long-term availability of herbal raw materials. Marketing strategies increasingly emphasize natural origin, therapeutic benefits, and eco-friendly production processes.

Herbal Fragrance Ingredients Industry Leaders

-

Symrise AG

-

Robertet Group

-

Givaudan SA

-

DSM-Firmenich AG

-

International Flavors & Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Symrise AG actively showcased its latest innovations at in-cosmetics Global 2026, focusing on longevity, inner beauty, and sustainability in cosmetic solutions. The company introduced Mindera® Euca, a 100% plant-based preservative derived from eucalyptus piperitone, specifically designed for rinse-off formulations to meet the growing demand for natural and sustainable ingredients.

- July 2025: Debut, a biotech firm, launched an innovative plant cell biotechnology platform that creates fragrance ingredients without relying on traditional cultivation methods. The company introduced this platform by producing an orris ingredient, derived directly from the root of the iris flower.

- October 2024: IFF, through its natural ingredients division LMR Naturals (LMR), unveiled three new fragrance ingredients. These include Ylanganate, a novel fragrance molecule, and oils extracted from Grapefruit and Persian Lime. Ylanganate not only boosts performance in perfumes and personal care products but also imparts natural traits to synthetic formulations.

- June 2024: IFF, through its natural ingredients division LMR Naturals (LMR), unveiled three new fragrance ingredients: Ylanganate, a novel fragrance molecule, and oils extracted from Grapefruit and Persian Lime. Ylanganate not only boosts performance in perfumes and personal care products but also imparts natural traits to synthetic formulations.

Global Herbal Fragrance Ingredients Market Report Scope

Herbal fragrance ingredients are naturally derived aromatic compounds extracted from herbs, plants, flowers, leaves, seeds, and roots, used to impart scent in perfumes, personal care products, home care items, and aromatherapy applications. The herbal fragrance ingredients market is segmented by product type, form, application and geography. Based on product type, the market is segmented into lavender, peppermint, rosemary, tea tree, citrus-based and others. Based on form, the market is segmented into liquid, powders and others. Based on application, the market is segmented into fine fragrances, personal care and cosmetics, household care, aromatherapy and wellness and food and beverages. By geography, the market is segmented into North America, Europe, Asia-Pacific, and South America and Middle East and Africa. For each segment, the market sizing and forecasts have been done in value terms (USD million).

| Lavender |

| Peppermint |

| Rosemary |

| Tea Tree |

| Citrus-Based (e.g., Orange, Lemon) |

| Others (e.g., Davana, Patchouli) |

| Liquid |

| Powder |

| Others |

| Fine Fragrances |

| Personal Care and Cosmetics |

| Household Care |

| Aromatherapy and Wellness |

| Food and Beverages |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Lavender | |

| Peppermint | ||

| Rosemary | ||

| Tea Tree | ||

| Citrus-Based (e.g., Orange, Lemon) | ||

| Others (e.g., Davana, Patchouli) | ||

| By Form | Liquid | |

| Powder | ||

| Others | ||

| By Application | Fine Fragrances | |

| Personal Care and Cosmetics | ||

| Household Care | ||

| Aromatherapy and Wellness | ||

| Food and Beverages | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which region is growing fastest in the herbal fragrance ingredients market?

Asia-Pacific shows the highest momentum with a projected 9.19% CAGR through 2031, driven by vertically integrated lavender, jasmine, and citrus supply chains.

What segment leads the herbal fragrance ingredients market size by application?

Fine fragrances retain the largest revenue at 34.93% for 2025, though aromatherapy is pacing faster growth.

How large is the herbal fragrance ingredients market size today?

The herbal fragrance ingredients market size is USD 4.53 billion in 2026 and forecast to reach USD 6.86 billion by 2031.

Which product type is expanding quickest?

Rosemary oil is set to record the fastest 9.12% CAGR, propelled by its antioxidant and antimicrobial duality.

Page last updated on: