Hemorrhoid Treatment Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

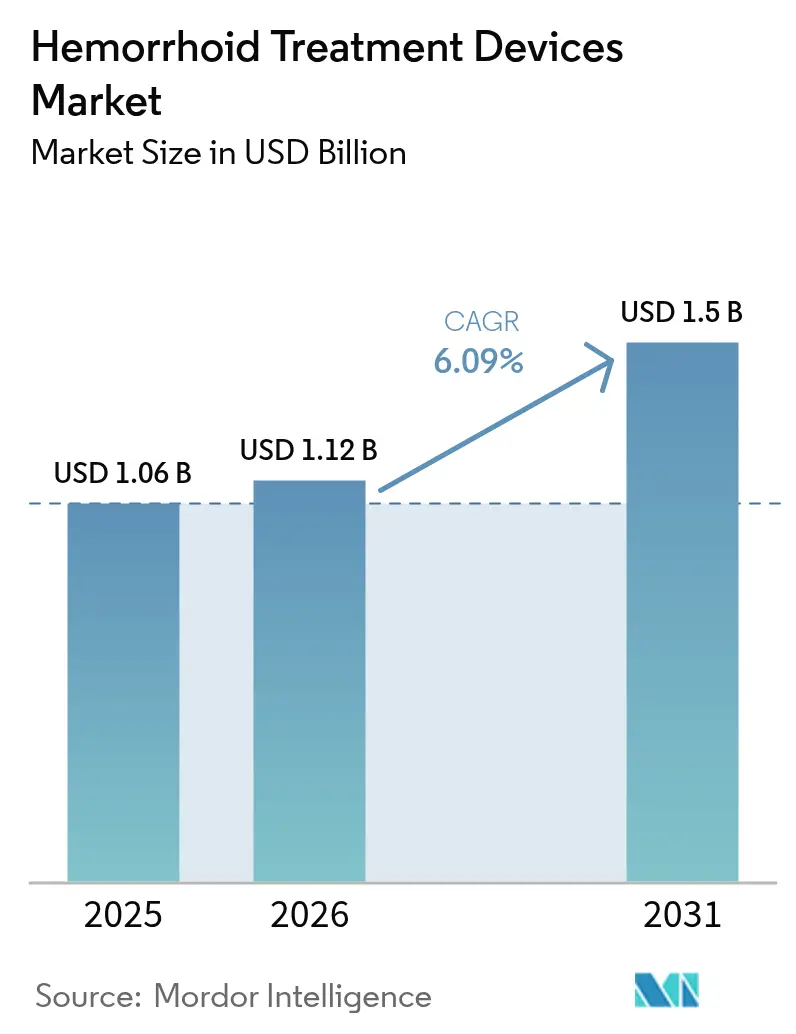

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.5 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

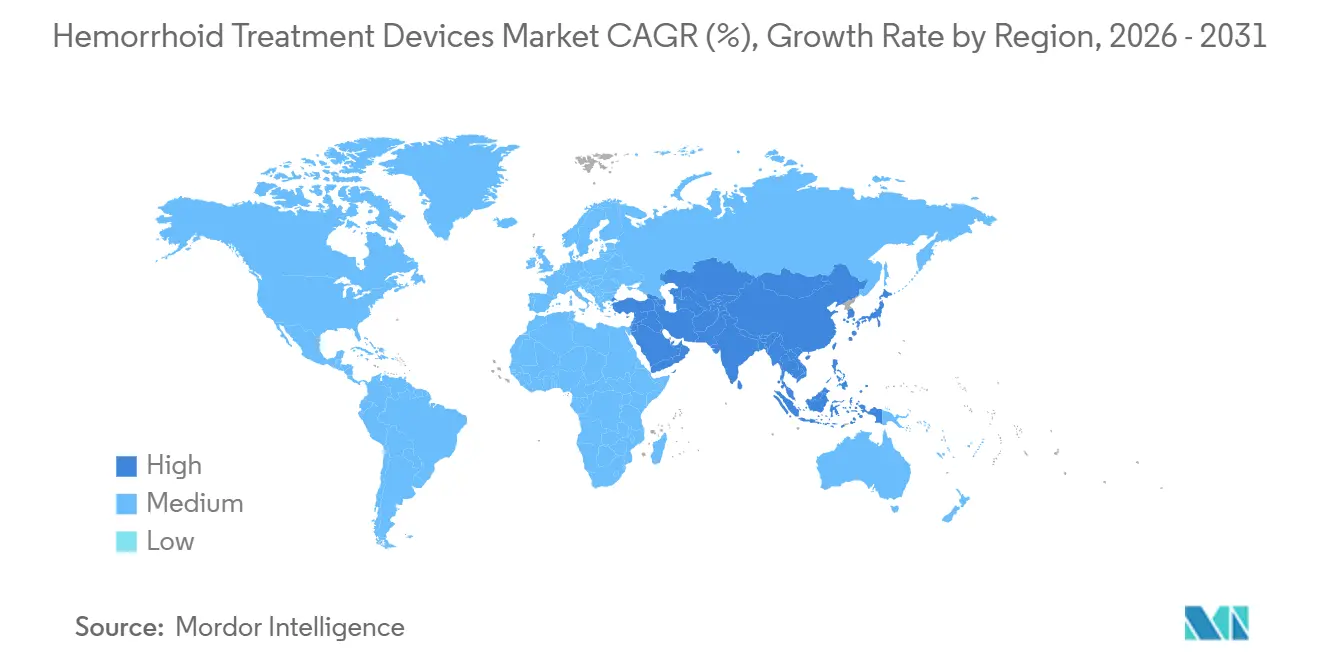

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Hemorrhoid Treatment Devices Market Analysis by ���ϲ�����

The Hemorrhoid Treatment Devices Market size is projected to expand from USD 1.06 billion in 2025 and USD 1.12 billion in 2026 to USD 1.5 billion by 2031, registering a CAGR of 6.09% between 2026 to 2031.

Demand is being pulled by an aging global population, sustained growth in outpatient colorectal procedures, and payer pressure to shift Grade II-IV hemorrhoid management from pharmacotherapy to device-based intervention.[1]National Institute of Diabetes and Digestive and Kidney Diseases, “Definition & Facts for Hemorrhoids,” NIDDK, niddk.nih.govAmbulatory surgery centers (ASCs) are capturing a rising share of these cases as Medicare and private insurers reimburse office-based ligation at attractive rates, while hospitals reserve operating rooms for complex colorectal surgery. Clinical studies reporting faster recovery and lower pain after laser hemorrhoidoplasty are accelerating the switch toward energy-based platforms, and infection-control concerns are fueling single-use device uptake.[2]J. Muthusamy et al., “Endoscope Reprocessing Failures and Infection Risk,” JAMA Network, jamanetwork.com With half of adults over 50 still managed medically, a sizable latent pool remains for device conversion, especially in Asia-Pacific where screening programs are scaling.

Key Report Takeaways

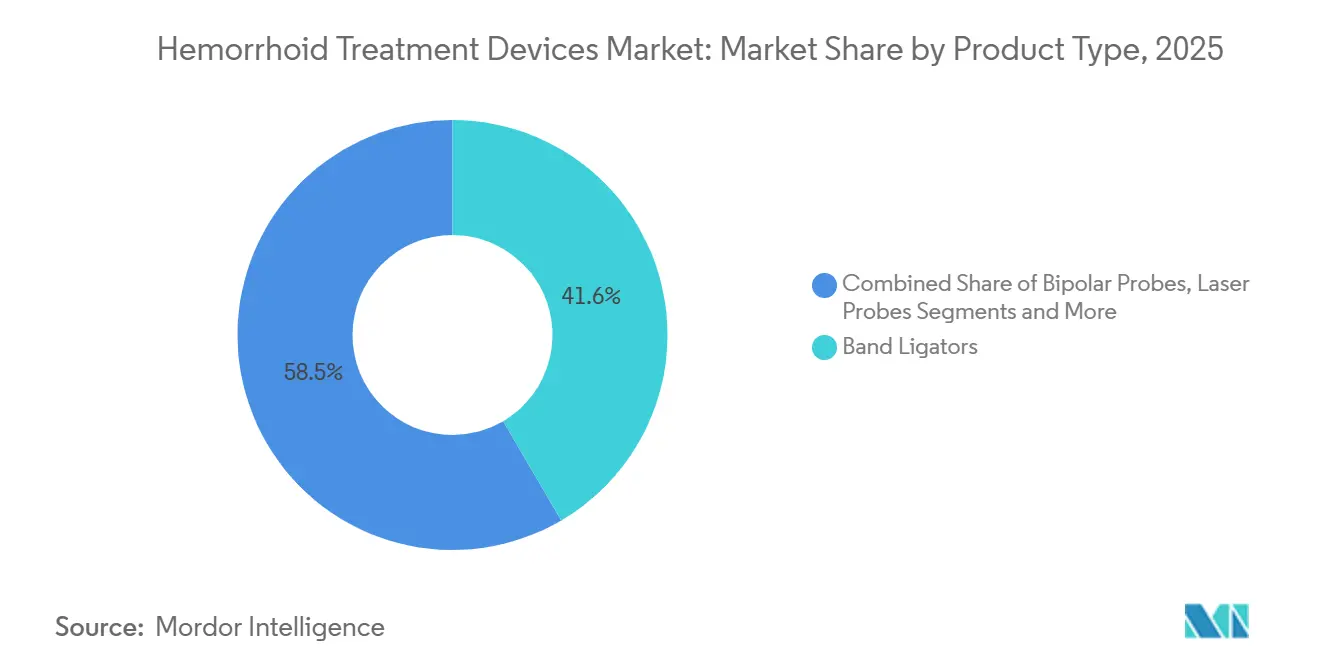

- By product type, band ligators led with 41.55% of the hemorrhoid treatment devices market share in 2025, while laser probes are forecast to expand at a 9.01% CAGR through 2031.

- By technology platform, mechanical systems commanded 53.74% share of the hemorrhoid treatment devices market size in 2025, and energy-based devices are projected to grow at 8.92% CAGR to 2031.

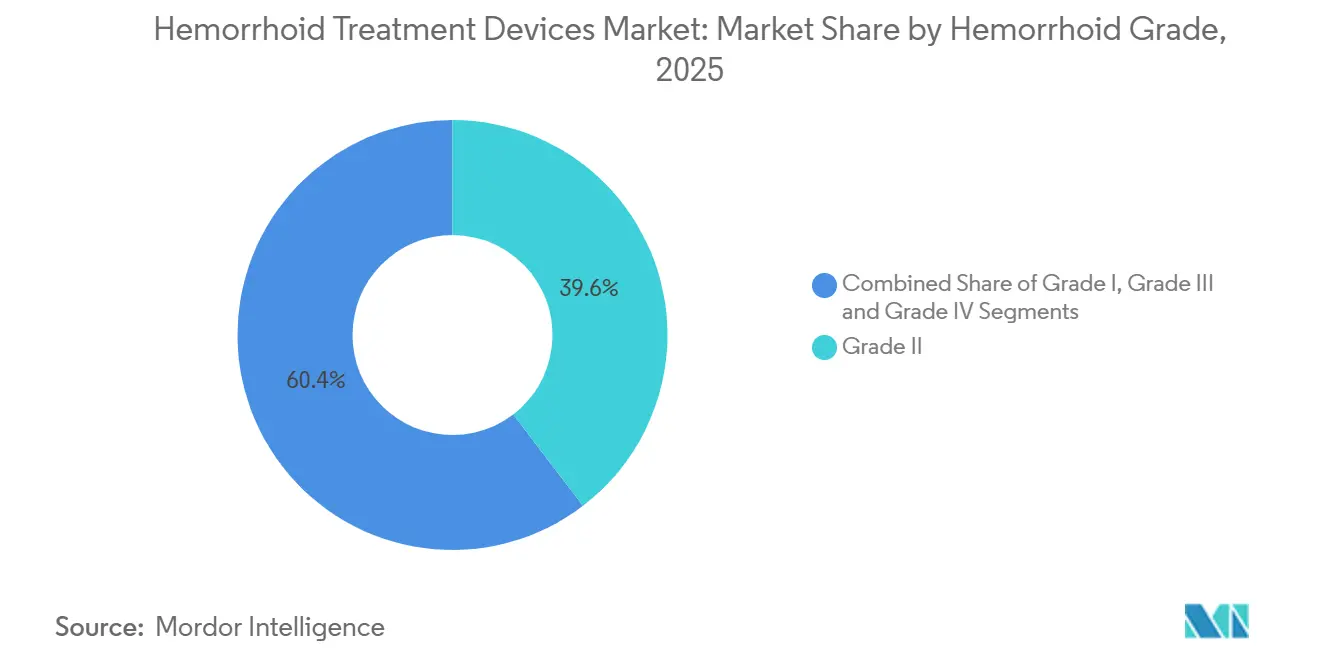

- By hemorrhoid grade, Grade II cases accounted for 39.62% of procedures in 2025; Grade IV treatments are set to rise at an 8.01% CAGR over the same horizon.

- By procedure, rubber band ligation held 37.76% share of the hemorrhoid treatment devices market size in 2025, while laser therapy is advancing at a 9.14% CAGR to 2031.

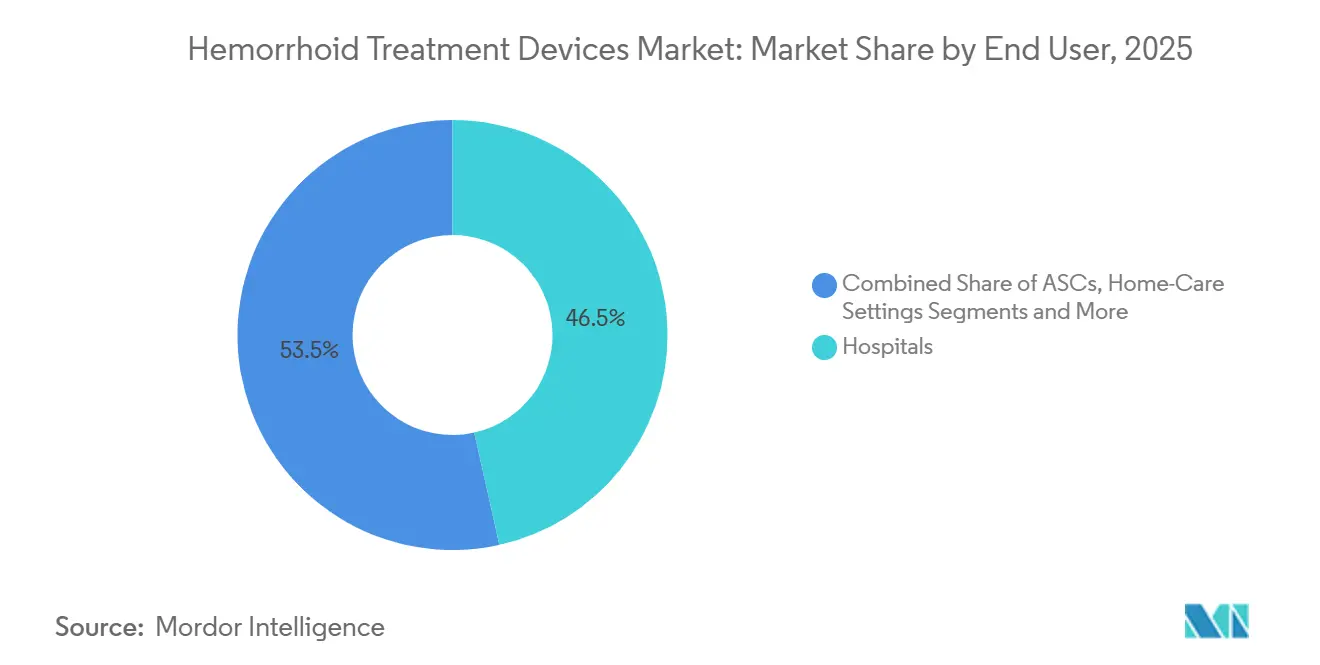

- By end user, hospitals captured 46.51% of 2025 revenue, yet ASCs are forecast to post the fastest growth at 8.33% CAGR through 2031.

- By geography, North America dominated with a 33.43% revenue share in 2025; Asia-Pacific is projected to register the quickest regional climb at an 8.43% CAGR.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hemorrhoid Treatment Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of hemorrhoidal disease | +1.6% | Global | Long term (≥ 4 years) |

| Growing adoption of minimally invasive outpatient procedures | +1.3% | North America, Asia-Pacific, selective EU | Medium term (2-4 years) |

| Technological advances in ligation and energy devices | +1.0% | Global, earliest in US/EU | Medium term (2-4 years) |

| Expanding healthcare infrastructure in emerging economies | +0.9% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Tele-endoscopy and remote guidance | +0.6% | Rural Asia, Africa, remote Australia | Medium term (2-4 years) |

| Infection-control push toward single-use ligators | +0.5% | US, EU, Japan | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rising Prevalence of Hemorrhoidal Disease

Up to 50% of adults older than 50 experience symptomatic hemorrhoids, and growing life expectancy is pushing absolute case numbers higher. China alone is bracing for 1.4 million annual colorectal cancer cases by 2040; national screening rollouts mean more incidental hemorrhoid diagnoses that move quickly to procedural care.[3] J. Zheng et al., “Colorectal Cancer Projections in China,” The Lancet Oncology, thelancet.com Similar screening acceleration is visible in India, Japan, and South Korea. The clinical community now favors earlier device intervention for Grades II-III to prevent progression, anchoring a long-term tailwind for the hemorrhoid treatment devices market.

Growing Adoption of Minimally Invasive Outpatient Procedures

Payers continue to steer patients away from inpatient excisional surgery toward office or ASC-based ligation. Medicare reimburses rubber band ligation (CPT 46221) at USD 158.85 per facility case in 2026, a level that supports high-volume practice economics. Vizient forecasts a 19% jump in total U.S. outpatient surgery between 2024 and 2034, with gastrointestinal work leading the rise. The convenience of 15-minute visits and same-day discharge aligns with patient preference, accelerating device throughput and revenue.

Technological Advances in Ligation and Energy Devices

Single-use bipolar probes, infrared coagulators, and reloadable clips continue to roll out with superior ergonomics and faster hemostasis. Olympus’ 2025 Retentia HemoClip and EZ Clip launches blended reusable and disposable strategies to accommodate divergent hospital budgets. Peer-reviewed trials report postoperative pain scores 30-40% lower with laser hemorrhoidoplasty than with conventional excision, supporting premium pricing and higher adoption of energy-based devices.

Expanding Healthcare Infrastructure in Emerging Economies

India’s pledge to lift public health spending to 2.5% of GDP by 2025 is translating into new endoscopy suites and subsidized colorectal screening. Similar budgets are visible in Indonesia, Vietnam, and Saudi Arabia. As middle-income hospitals secure financing, they are procuring mid-tier mechanical ligators first, then layering on energy platforms as procedure volumes climb. This gradual technology laddering broadens the total addressable base of the hemorrhoid treatment devices market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of stapling and laser systems | –1.2% | Global, highest in low- and middle-income | Long term (≥ 4 years) |

| Stringent FDA / CE regulatory pathways | –0.7% | United States, European Union, Japan | Medium term (2-4 years) |

| Competition from topical pharmacotherapy | –0.6% | Global | Short term (≤ 2 years) |

| Shortage of colorectal specialists | –0.5% | Africa, South Asia, rural Latin America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Cost of Stapling and Laser Systems

Capital outlays above USD 50,000 for a single laser console discourage adoption in resource-constrained hospitals despite clinical benefits. Deferred purchases are common in sub-Saharan Africa and lower-tier Chinese cities where budget committees favor mechanical ligators that cost one-tenth as much. Financing programs and leasing models are emerging, yet payback timelines stretch beyond five years for many facilities, slowing energy platform penetration.

Stringent FDA/CE Regulatory Pathways

Energy-based devices often require De Novo or pre-market approval, adding years and millions in test costs. Signum Surgical’s BioHealx cleared the FDA’s De Novo route only in mid-2024 after multiple clinical rounds, illustrating the hurdle for smaller innovators. While necessary for patient safety, these steps delay market entry and compress patent-protected sales windows.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Band Ligator Leadership, Laser Momentum

Band ligators owned 41.55% of 2025 revenue, underpinning the mechanical core of the hemorrhoid treatment devices market. High throughput, CPT-linked reimbursement, and a five-minute room turnaround keep demand brisk in physician offices and ASCs. The segment also benefits from infection-control upgrades as manufacturers roll out single-use variants. Laser probes, however, are set for a 9.01% CAGR, driven by compelling randomized evidence of superior pain relief and quicker return to work. Hospitals looking to differentiate colorectal programs are acquiring laser consoles, and private insurers in Germany and Japan now reimburse laser hemorrhoidoplasty, further lifting penetration.

By Technology Platform: Mechanical Base, Energy Upswing

Mechanical systems generated 53.74% of the hemorrhoid treatment devices market size in 2025 thanks to band ligator ubiquity and their minimal learning curve. Budget-sensitive public hospitals in Latin America and Africa still prioritize these platforms. Energy-based devices are catching up at an 8.92% CAGR, led by bipolar and infrared coagulators that eliminate costly endoscope reprocessing. ASCs in the U.S. often bundle a disposable probe into the procedure fee, easing capital constraints and smoothing the upgrade path for surgeons.

By Hemorrhoid Grade: II Dominant, IV Accelerating

Grade II treatments represented 39.62% of global volume in 2025, reflecting payers’ and clinicians’ preference for early outpatient management. The hemorrhoid treatment devices market share in Grade IV remains smaller but is expanding at an 8.01% CAGR as tertiary centers adopt Doppler-guided artery ligation and stapled hemorrhoidopexy for complex prolapse. Improved anesthesia protocols and faster discharge policies now allow many Grade IV cases to be scheduled in ASCs instead of inpatient ORs, broadening device demand.

By Procedure: Rubber Band First, Laser Fastest

Rubber band ligation dominated with 37.76% of 2025 procedures, and its cost advantage guarantees continued leadership. That said, laser therapy is rising on a 9.14% trajectory. Surgeons appreciate the bloodless field and reduced postoperative edema, and patients favor the short recovery window. Doppler-guided artery ligation and stapled hemorrhoidopexy fill more specialized niches, typically reserved for recurrent or circumferential prolapse.

By End User: Hospital Core, ASC Growth Track

Hospitals held 46.51% of 2025 spending, anchored by complex Grade III-IV caseloads and in-house anesthesia teams. Still, the hemorrhoid treatment devices market size captured by ASCs is climbing quickly at 8.33% CAGR as payers shift authorizations toward same-day settings. Physician offices remain the workhorse for single-ligator visits, especially in North America, while home-care use of disposable anoscopes is embryonic but gathering interest from tele-health startups.

Geography Analysis

North America generated 33.43% of 2025 revenue, underpinned by 6,300 Medicare-certified ASCs and clear procedural reimbursement. FDA device-intensive policies continue to influence purchasing, and infection-control rules make single-use ligators standard in many U.S. hospitals. Canada shows similar patterns, though provincial budgets extend capital cycles by one to two years longer than U.S. averages.

Asia-Pacific is the fastest-growing arena at 8.43% CAGR through 2031. China is scaling colorectal screening, and provincial insurance now covers laser hemorrhoidoplasty in several pilot provinces. India’s private hospital chains are opening dedicated day-surgery wings, equipping them with bipolar and infrared platforms to differentiate from public facilities. Southeast Asian markets such as Indonesia are piggybacking on endoscopy infrastructure funded for gastric cancer programs, creating incremental device demand.

Europe represents a mature but technology-hungry region. Germany and France reimburse energy-based procedures at higher tariffs than mechanical ligation, encouraging steady console refresh cycles every five to seven years. The United Kingdom is channeling National Health Service capital toward infection-risk reduction, pushing single-use devices to the fore. In Southern Europe, lingering budget limits lengthen adoption timelines, though EU-wide infection directives are narrowing the gap.

The Middle East & Africa and South America together account for a modest share but are important long-run contributors. Gulf Cooperation Council hospitals have moved rapidly into Doppler-guided and laser techniques to attract medical tourists, while Brazil and Colombia are expanding public coverage of outpatient ligation. Persistent shortages of colorectal surgeons and capital constraints temper growth, yet tele-endoscopy pilots and private specialty clinics are beginning to unlock latent demand.

Competitive Landscape

Market rivalry is moderate, characterized by a handful of diversified surgical conglomerates and several focused innovators. Boston Scientific, Medtronic, Johnson & Johnson’s Ethicon, and Olympus collectively control most band ligator and stapler placements, leveraging broad distribution and bundled service contracts. Olympus pursued a dual-track device policy in 2025, rolling out the reusable EZ Clip for cost-sensitive buyers and the single-use Retentia HemoClip for infection-conscious centers.

Niche challengers are carving footholds. THD S.p.A. continues to build share with its Doppler-guided ligator platform, especially in Italian and U.K. NHS hospitals. Signum Surgical received FDA De Novo clearance in 2024 for its BioHealx radiofrequency device targeting the submucosal plexus, bringing a tissue-sparing alternative to the U.S. market. Merit Medical’s USD 120 million purchase of Biolife broadened its hemostatic sealant range, enabling procedural kits that bundle ligators with bleeding-control products.

Strategy themes include disposable product launches to meet infection-control mandates, cross-selling of hemostatic agents alongside ligators, and geographic expansion via local distributors in Asia-Pacific. Patent filings show a pivot toward hybrid mechanical-energy devices, while venture investors are funding start-ups focused on low-cost single-use consoles for emerging markets.

Hemorrhoid Treatment Devices Industry Leaders

Boston Scientific Corporation

Medtronic Plc

Cook Medical

Integra LifeSciences Corporation

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Al Buraimi Hospital, Oman, installed a surgical laser platform for hemorrhoid and anal fistula treatment, reinforcing the Ministry of Health’s specialization agenda.

- May 2025: Apollo Spectra Hospital, India, began daycare radiofrequency ablation (Rafaelo) for hemorrhoids under local anesthesia.

- March 2025: Olympus introduced the Retentia HemoClip single-use hemostasis clip for outpatient GI cases in the United States and European Union.

Global Hemorrhoid Treatment Devices Market Report Scope

Hemorrhoid treatment devices are medical tools designed to non-surgically treat or manage symptomatic hemorrhoids in the anal canal, offering a minimally invasive alternative to surgery.

The Hemorrhoid Treatment Devices Market Report is segmented by Product Type, Technology Platform, Hemorrhoid Grade, Procedure, End User, and Geography. By Product Type, the market is segmented into Band Ligators, Infrared Coagulators, Proctoscopes & Anoscopes, Bipolar Probes, Doppler-Guided Ligators, Cryotherapy Devices, Laser Probes, Stapling Devices, and Other Emerging Devices. By Technology Platform, the market is segmented into Energy-based Devices, Mechanical Devices, and Hybrid/Combination Devices. By Hemorrhoid Grade, the market is segmented into Grade I, Grade II, Grade III, and Grade IV. By Procedure, the market is segmented into Rubber Band Ligation, Sclerotherapy, Infrared Coagulation, Laser Therapy, Doppler-Guided Artery Ligation, Stapled Hemorrhoidopexy, Conventional Hemorrhoidectomy, and Other Procedures. By End User, the market is segmented into Hospitals, Clinics & Physician Offices, Ambulatory Surgery Centers, Home-Care Settings, and Others. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Band Ligators |

| Infrared Coagulators |

| Proctoscopes & Anoscopes |

| Bipolar Probes |

| Doppler-Guided Ligators |

| Cryotherapy Devices |

| Laser Probes |

| Stapling Devices |

| Other Emerging Devices |

| Energy-based Devices |

| Mechanical Devices |

| Hybrid/ Combination Devices |

| Grade I |

| Grade II |

| Grade III |

| Grade IV |

| Rubber Band Ligation |

| Sclerotherapy |

| Infrared Coagulation |

| Laser Therapy |

| Doppler-Guided Artery Ligation (DG-HAL) |

| Stapled Hemorrhoidopexy |

| Conventional Hemorrhoidectomy |

| Other Procedures |

| Hospitals |

| Clinics & Physician Offices |

| Ambulatory Surgery Centers |

| Home-Care Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Band Ligators | |

| Infrared Coagulators | ||

| Proctoscopes & Anoscopes | ||

| Bipolar Probes | ||

| Doppler-Guided Ligators | ||

| Cryotherapy Devices | ||

| Laser Probes | ||

| Stapling Devices | ||

| Other Emerging Devices | ||

| By Technology Platform | Energy-based Devices | |

| Mechanical Devices | ||

| Hybrid/ Combination Devices | ||

| By Hemorrhoid Grade | Grade I | |

| Grade II | ||

| Grade III | ||

| Grade IV | ||

| By Procedure | Rubber Band Ligation | |

| Sclerotherapy | ||

| Infrared Coagulation | ||

| Laser Therapy | ||

| Doppler-Guided Artery Ligation (DG-HAL) | ||

| Stapled Hemorrhoidopexy | ||

| Conventional Hemorrhoidectomy | ||

| Other Procedures | ||

| By End User | Hospitals | |

| Clinics & Physician Offices | ||

| Ambulatory Surgery Centers | ||

| Home-Care Settings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the hemorrhoid treatment devices market?

The market stood at USD 1.12 billion in 2026 and is projected to reach USD 1.50 billion by 2031.

Which product type leads global sales?

Band ligators led with 41.55% revenue share in 2025 due to their cost-effectiveness and clear reimbursement pathway.

Which region is growing the fastest?

Asia-Pacific is forecast to expand at an 8.43% CAGR through 2031, driven by investments in colorectal screening and endoscopy capacity.

How quickly are ambulatory surgery centers adopting hemorrhoid devices?

ASC revenue is predicted to rise at 8.33% CAGR, fueled by payer incentives for same-day, minimally invasive procedures.

What technological trend is reshaping device choice?

Single-use, infection-control-focused ligators and energy probes are gaining traction as hospitals seek to cut reprocessing risk and labor cost.

Which companies are at the forefront of innovation?

Olympus, THD S.p.A., and Signum Surgical are actively launching single-use or radiofrequency devices that target shorter recovery and improved safety.

Page last updated on: