Heavy Gauge And Thin Gauge Thermoformed Plastics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

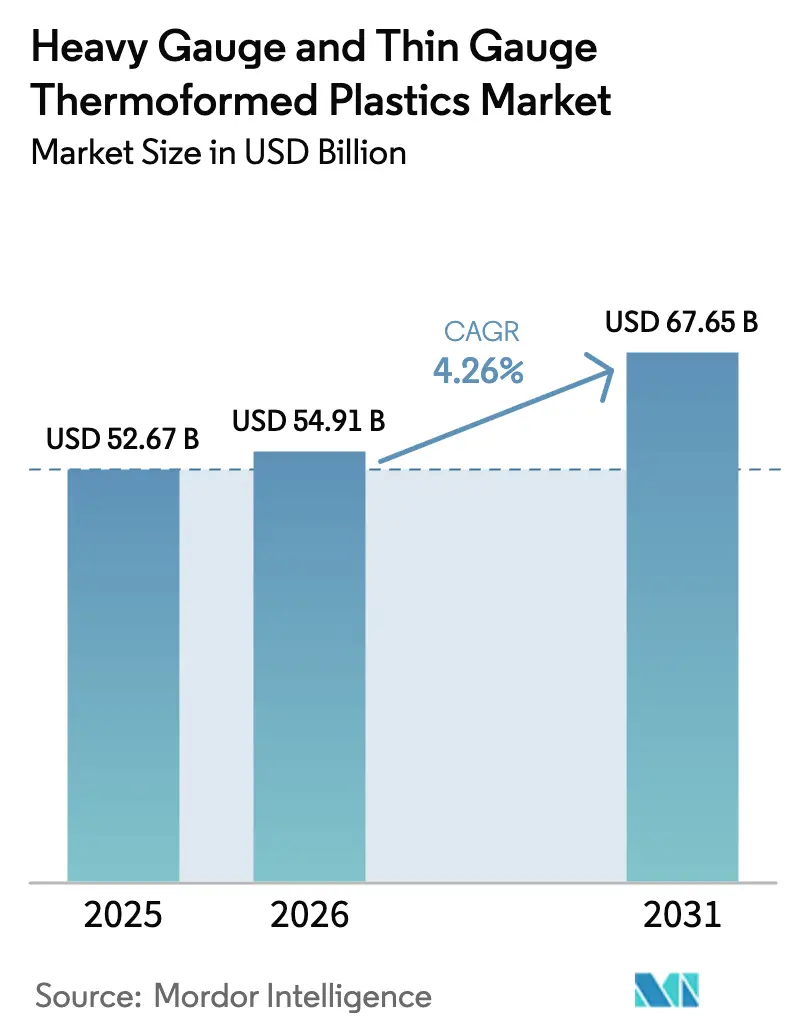

| Market Size (2026) | USD 54.91 Billion |

| Market Size (2031) | USD 67.65 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Heavy Gauge And Thin Gauge Thermoformed Plastics Market Analysis by ���ϲ�����

The Heavy Gauge and Thin Gauge Thermoformed Plastics Market size is expected to increase from USD 52.67 billion in 2025 to USD 54.91 billion in 2026 and reach USD 67.65 billion by 2031, growing at a CAGR of 4.26% over 2026-2031. Converters are responding to ongoing food safety regulations, an expanding pharmaceutical cold chain, and incentives for a circular economy. They are redesigning resin blends, investing in rPET decontamination, and incorporating digital in-mold labeling. In the Asia-Pacific, intensified national recycled-content mandates are driving up sheet demand. Meanwhile, North American producers are grappling with the costs of phasing out PFAS and the risks of substituting molded fiber. The industry is witnessing a trend toward scale efficiency and integrated recycling, highlighted by Novolex's USD 6.7 billion acquisition of Pactiv Evergreen. Heavy-gauge growth is bolstered by lightweighting initiatives in electric vehicles and industrial robots. Furthermore, the adoption of depolymerized rPET film in pharmaceutical blisters underscores the validation of recycled content in regulated environments.

Key Report Takeaways

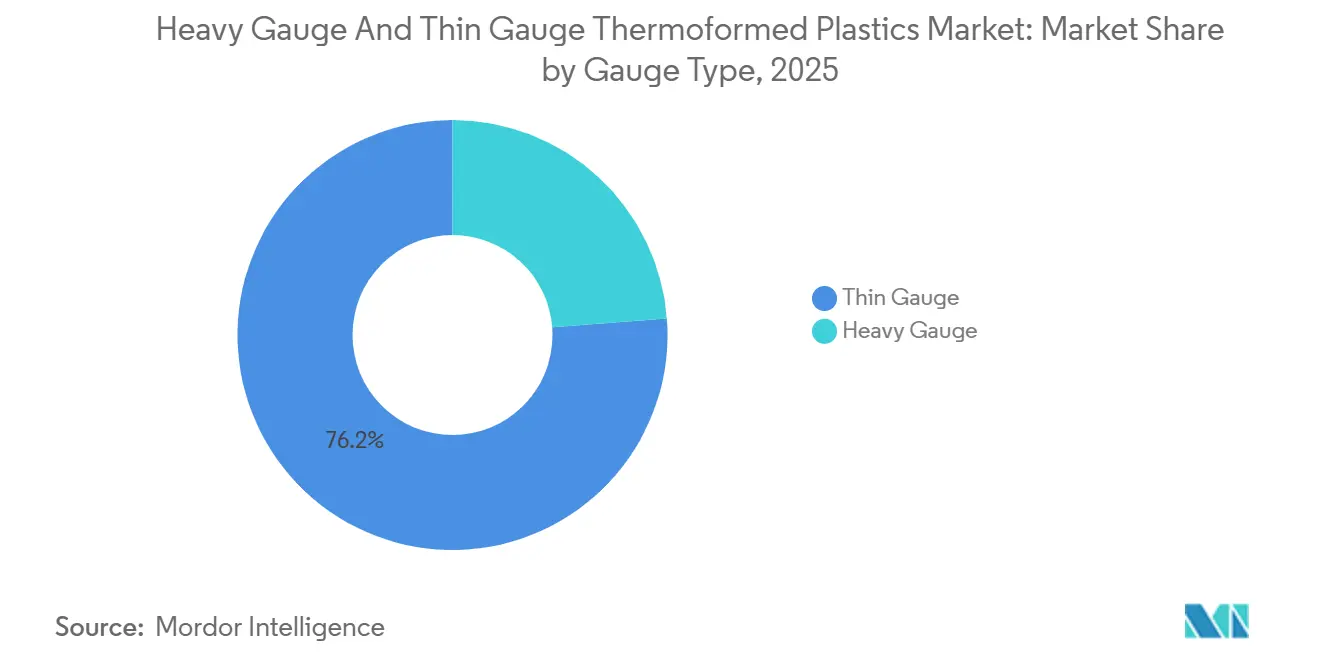

- By gauge type, thin-gauge formats secured 76.22% of the Heavy Gauge and Thin Gauge Thermoformed Plastics market share in 2025 and are forecast to expand at a 4.33% CAGR between 2026-2031.

- By end-use industry, food and beverage packaging held 62.22% revenue share in 2025 and faces rising compostable-fiber competition. Medical and pharmaceutical packaging is projected to grow at the fastest 4.77% CAGR through 2031 as blister compliance and biologics cold-chain demand rise.

- By geography, Asia-Pacific accounted for 44.45% of the Heavy Gauge and Thin Gauge Thermoformed Plastics market size in 2025 and is projected to record the highest projected growth at 4.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Heavy Gauge And Thin Gauge Thermoformed Plastics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand spike from fresh and frozen food packaging | +1.20% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Expanding pharma-grade blister and tray usage | +0.90% | North America, Europe, India | Medium term (2-4 years) |

| Closed-loop rPET thermoforming initiatives | +0.80% | Europe, California, India | Medium term (2-4 years) |

| Autonomous mobile-robot enclosures | +0.40% | North America, Europe, China | Long term (≥ 4 years) |

| Digital in-mold-labeling adoption | +0.50% | Europe, North America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Demand Spike from Fresh and Frozen Food Packaging

Global retailers are adopting modified-atmosphere trays and microwave-ready CPET containers to reduce food waste and take advantage of extended producer responsibility (EPR) fee reductions. Crystalline PET and polypropylene multicompartment designs endure repeated freeze-thaw cycles, enabling brand diversification without reducing shelf life. In Europe, tray-to-tray recycling is gaining traction after Perstorp’s Akestra co-extrusion polyester, which features post-consumer content and heat resistance, received an endorsement[1]Perstorp, “Akestra™ Delivers Circular High-Heat PET,” perstorp.com . The United Kingdom introduced EPR rules in 2024, permitting fee offsets for verified closed-loop collections. This has spurred investments, including Cirrec’s ambitious expansion to process billions of trays annually. Meanwhile, North America faces a tight supply, as only a limited amount of PET thermoforms were recycled domestically in 2023, increasing competition for food-grade rPET flake.

Expanding Pharma-Grade Blister and Tray Usage

As regulators tighten limits on extractables and leachables, the demand for recyclable high-barrier films is increasing. In 2024, Amcor established automated Class 7 capacity in Wisconsin, integrating ISO 13485-compliant thermoforms and die-cut lids within a single facility. TekniPlex, in collaboration with Alpek, utilized depolymerization to introduce a blister film that ensures compliance with both European and U.S. Pharmacopeias while maintaining recyclability in polyester streams. Under EU PPWR regulations, only A or B recyclability grades will be accepted after 2038, driving converters toward mono-PET structures.

Closed-Loop rPET Thermoforming Initiatives

In Europe and California, extended producer responsibility (EPR) fee modulation and mandates for recycled content are incentivizing converters to adopt vertical recycling. Placon's EcoStar facility processes bottles daily, transforming them into sheets with recycled content. The BACHMANN Group from Switzerland has invested in an in-house rPET film extrusion, achieving decontamination efficiency to comply with PPWR food-contact regulations. California's SB 54 law is pushing for upgrades in material recovery facilities (MRFs) and setting targets for thermoform-only bale collections, with the goal of boosting the state's current thermoform recycling rate.

Autonomous Mobile-Robot Housings Require Large Thermoformed Enclosures

Warehouses and factories are increasingly adopting heavy-gauge ABS and PC housings. These housings, featuring integrated mounting bosses and cable channels, are available in single-piece enclosures, significantly reducing assembly time. CW Thomas highlights the economic viability of vacuum-forming parts up to ten feet for production runs. Wilbert Plastic Services, recognized with an SPE Gold Award for its pressure-formed MRI covers, underscores the material's reliability for use in electromedical and robotics enclosures. Hanwha Azdel's lightweight reinforced thermoplastic substrates achieve a reduction in mass and offer enhanced flexural strength, thereby broadening design possibilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Molded-fiber tray substitution risk | -0.60% | North America, Europe | Short term (≤ 2 years) |

| Tightening PFAS barrier-coating regulations on food trays | -0.40% | North America, Europe, export-oriented Asia-Pacific | Medium term (2-4 years) |

| Shortage of high-clarity rPET flake for recycled-content laws | -0.50% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Molded-Fiber Tray Substitution Risk

In 2024, Dart Container partnered with PulPac, introducing dry-molded-fiber lines to the United States. These lines operate significantly faster than traditional pulp equipment, with the goal of replacing low-barrier thermoforms in takeaway services. Iggesund's Inverform, a solid-bleached-board substrate, boasts formability and compatibility with paper recycling, making it more appealing for chilled ready meals. However, fiber alternatives face challenges. They struggle with grease and moisture resistance and encounter limited industrial composting infrastructure, primarily confined to select regions in the United States and the European Union. This restricts their potential in high-barrier markets such as meat and seafood.

Tightening PFAS Barrier-Coating Regulations on Food Trays

In 2025, the FDA retracted several notifications for PFAS grease-proofers, effectively banning their use in the United States. Meanwhile, the European Union's PPWR draft guidance has set a cap on targeted PFAS, with enforcement slated for August 2026, compelling converters to seek and validate alternative coatings. ECHA's revised proposal, while offering limited exceptions, introduces a five-year sunset period, amplifying transition costs[2]Food Packaging Forum, “ECHA Updates PFAS Restriction Proposal,” foodpackagingforum.org . Converters reliant on fluorinated processing aids now face the challenge of either retrofitting or certifying new chemistries, significantly increasing their compliance expenses.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gauge Type: Thin Gauge Dominates Single-Use Foodservice

Thin-gauge captured 76.22% of the Heavy Gauge and Thin Gauge Thermoformed Plastics market share in 2025 and is expected to grow at a 4.33% CAGR during the forecast period of 2026-2031. Foodservice clamshells, deli lids, and crystallized polyethylene terephthalate (CPET) ready-meal trays dominate in volume consumption, while medical blisters offer higher margins. Converters aim to achieve 100% recyclable or renewable sales by 2030, driving the adoption of recycled polyethylene terephthalate (rPET) and mono-material polypropylene substrates.

Heavy-gauge sheets, ranging from 0.060 to 0.500 inches, are used in automotive, white-goods, and industrial housings. These applications benefit from the cost-effectiveness of vacuum forming for large parts and mid-volume production. For example, Röchling’s convertible roof beam reduced weight in a Mercedes-Benz program and decreased the part count significantly. Additionally, specialized acrylonitrile butadiene styrene/polycarbonate (ABS/PC) blends with in-mold paint films reduce the need for downstream finishing labor. However, when annual volumes exceed 100,000 units, the economics of injection-molding tooling become more favorable, limiting the addressable share for heavy-gauge applications.

By End-Use Industry: Food Packaging Leads, Pharma Grows Fastest

Food and beverage packaging retained 62.22% of the heavy gauge and thin gauge thermoformed plastics market revenues in 2025, driven by increasing e-grocery demand and extended-shelf-life formats. However, the segment faces margin pressures due to the growing adoption of compostable fibers and the high costs of rPET flakes.

Meanwhile, the medical and pharmaceutical sector is projected to register the highest CAGR of 4.77% during the forecast period (2026-2031), supported by rising biologics cold-chain logistics volumes and regulatory preferences for unit-dose adherence packs. Highlighting the industry's evolution, TekniPlex has introduced rPET blister film, demonstrating the compatibility of recycled content with stringent barrier requirements. Additionally, investments in cleanroom facilities and the attainment of ISO 13485 certification are enabling premium pricing. While sectors such as automotive, electronics, and industrial equipment utilize heavy-gauge panels for weight reduction, these remain secondary in terms of market value.

Geography Analysis

Asia-Pacific contributed 44.45% of global revenues in 2025 and is set to post a 4.46% CAGR during the forecast period of 2026-2031, driven by rising disposable income, stringent food-safety codes, and escalating pharmaceutical output. In a move to meet its recycled-content law, India inaugurated a PET recycling facility in Egypt to satisfy domestic tray demand. China's enhanced cold-chain standards, coupled with the rise of e-commerce meal kits, are fueling a surge in thin-gauge consumption. Meanwhile, the ASEAN region is attracting foreign direct investment (FDI) in contract processing.

North America, supported by established foodservice networks, remains the second-largest player. Novolex is strategically integrating on a large scale, focusing on closed-loop rPET sourcing and PFAS-free coatings to maintain its market share. California's SB 54 is accelerating thermoform bale separation. However, with a recycling rate that lags behind Europe, North America is drawing increased attention from policymakers.

Europe faces stringent regulations. By 2030, PPWR mandates recycled content in contact-sensitive PET, with recyclability standards set for 2035. Investments in decontamination processes, exemplified by BACHMANN's line in Switzerland, are ensuring compliance. While tray collections exceed significant annual volumes, only a fraction is recycled, largely due to challenges with multilayer formats. Meanwhile, South America and the Middle-East and Africa are emerging as regions with potential, as urban retail and pharmaceutical fill-finish capacities expand.

Competitive Landscape

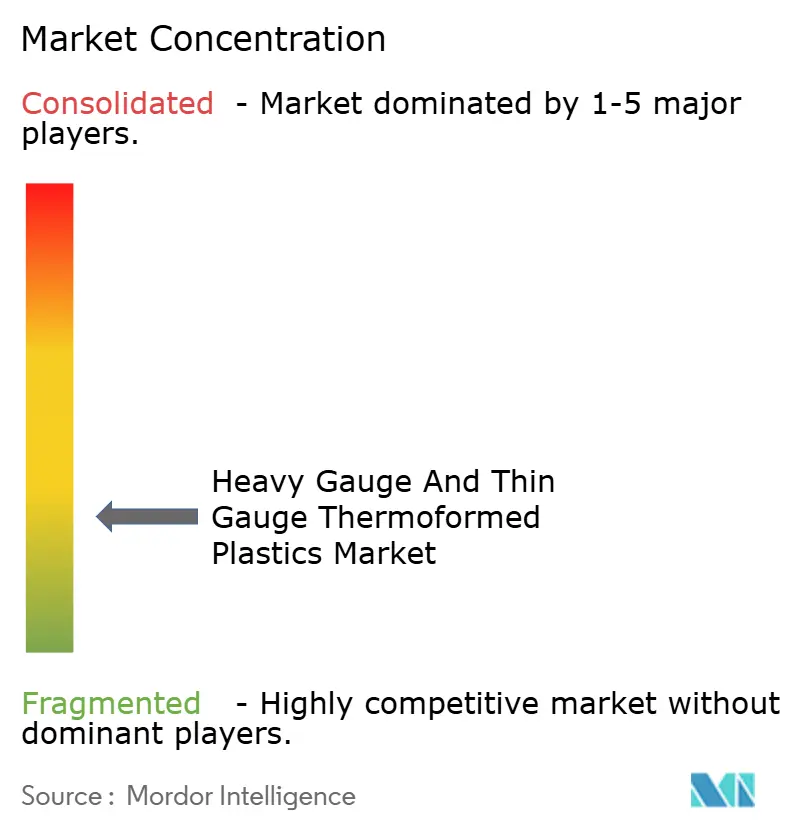

The Heavy Gauge and Thin Gauge Thermoformed Plastics market is fragmented. While global giants such as Amcor, Novolex, and Sonoco boast extensive portfolios, their collective revenue share indicates ample room for regional players. In a significant move, Novolex acquired Pactiv Evergreen, bringing together numerous brands and SKUs and capitalizing on synergies in rPET flake procurement and digital printing. Meanwhile, Sonoco divested its thermoformed operations, channeling its focus toward paper and metal and achieving a notable reduction in net debt.

Today's value-chain dynamics hinge on three pivotal levers: in-house sheet extrusion tied to recycling capabilities, ISO-class cleanrooms that command medical premiums, and expertise in PFAS-free barriers. Leveraging depolymerization, TekniPlex offers rPET blister film compliant with pharmacopeia standards, securing an early-mover edge. Winpak introduced its mono-polyolefin ReFresh ReForm films, which are pre-qualified for How2Recycle drop-off, ensuring a foothold in CPG pilot lines. Heavy-gauge industry leaders, Röchling and Hanwha Azdel, are utilizing hybrid molding and LWRT composites to reduce EV component weight, aligning with OEM sustainability goals.

As molded-fiber entrants intensify competitive pressures, converters are responding with advanced barrier science, rapid tooling changes, and tailored SKU customization. Major operators are capitalizing on EPR-fee arbitrage by advocating for circular feedstock. Meanwhile, specialty converters are reaping rewards in niche markets such as pharmaceuticals, electronics, and autonomous robotics, where regulatory challenges and design complexities limit substitute options.

Heavy Gauge And Thin Gauge Thermoformed Plastics Industry Leaders

Amcor plc

Dart Container Corporation

Greiner AG

Novolex

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Novolex completed the USD 6.70 billion acquisition of Pactiv Evergreen. This acquisition enhances Novolex's geographical presence and reinforces its position in the heavy gauge and thin gauge thermoformed plastics markets.

- April 2025: Sonoco Products Company has completed the sale of its Thermoformed and Flexibles Packaging business ("TFP") to TOPPAN Holdings Inc. for approximately USD 1.8 billion.

Global Heavy Gauge And Thin Gauge Thermoformed Plastics Market Report Scope

Thermoformed plastics are manufactured by heating plastic sheets until they become pliable and then shaping them over a mold to create specific products. In the thermoforming process, plastics are classified as thin gauge or heavy gauge, primarily based on the sheet thickness and the type of product produced. Heavy gauge thermoforming utilizes thicker sheets, typically between 0.125 and 0.500 inches, to manufacture durable and robust components. This process is commonly applied to industrial and commercial products requiring long-term durability. In contrast, thin gauge thermoforming uses sheets less than 0.060 inches thick, making it suitable for high-volume production of lightweight parts.

The Heavy Gauge And Thin Gauge Thermoformed Plastics Market is segmented by gauge type, end-use industry, and geography. By gauge type, the market is segmented into heavy gauge and thin gauge. By end-use industry, the market is segmented into automotive and transportation, food and beverage packaging, medical and pharmaceutical, electrical and electronics, industrial equipment, consumer goods, and others. The report also covers the market size and forecasts for heavy gauge and thin gauge thermoformed plastics in 20 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Heavy Gauge |

| Thin Gauge |

| Automotive and Transportation |

| Food and Beverage Packaging |

| Medical and Pharmaceutical |

| Electrical and Electronics |

| Industrial Equipment |

| Consumer Goods |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| Italy | |

| United Kingdom | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Gauge Type | Heavy Gauge | |

| Thin Gauge | ||

| By End-Use Industry | Automotive and Transportation | |

| Food and Beverage Packaging | ||

| Medical and Pharmaceutical | ||

| Electrical and Electronics | ||

| Industrial Equipment | ||

| Consumer Goods | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| United Kingdom | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will Asia-Pacific demand become by 2031?

The Heavy Gauge and Thin Gauge Thermoformed Plastics market size stands at USD 54.91 billion in 2026, and it is projected to reach USD 67.65 billion by 2031 at a 4.26% CAGR.

What triggers the fastest segment growth?

Medical and pharmaceutical packaging rises at a 4.77% CAGR as biologics and compliance blister packs proliferate across regulated markets.

Which regulation most affects recycled content targets?

EU Packaging and Packaging Waste Regulation (EU 2025/40) mandates 30% recycled content in contact-sensitive PET packaging by 2030.

Why are heavy-gauge parts favored in electric vehicles?

Vacuum-formed panels cut component weight, Röchling’s roof beam removed 700g, supporting range and assembly simplification.

How are converters mitigating PFAS bans?

Companies validate alternative barrier chemistries, invest in decontamination, and phase in PFAS-free coatings ahead of August 2026 EU limits.

What recycling bottleneck curbs thin-gauge growth in North America?

Only 14% of PET thermoforms enter domestic recycling streams, limiting food-grade rPET flake supply despite growing mandates.

Page last updated on: