Healthcare Enterprise Resource Planning (ERP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

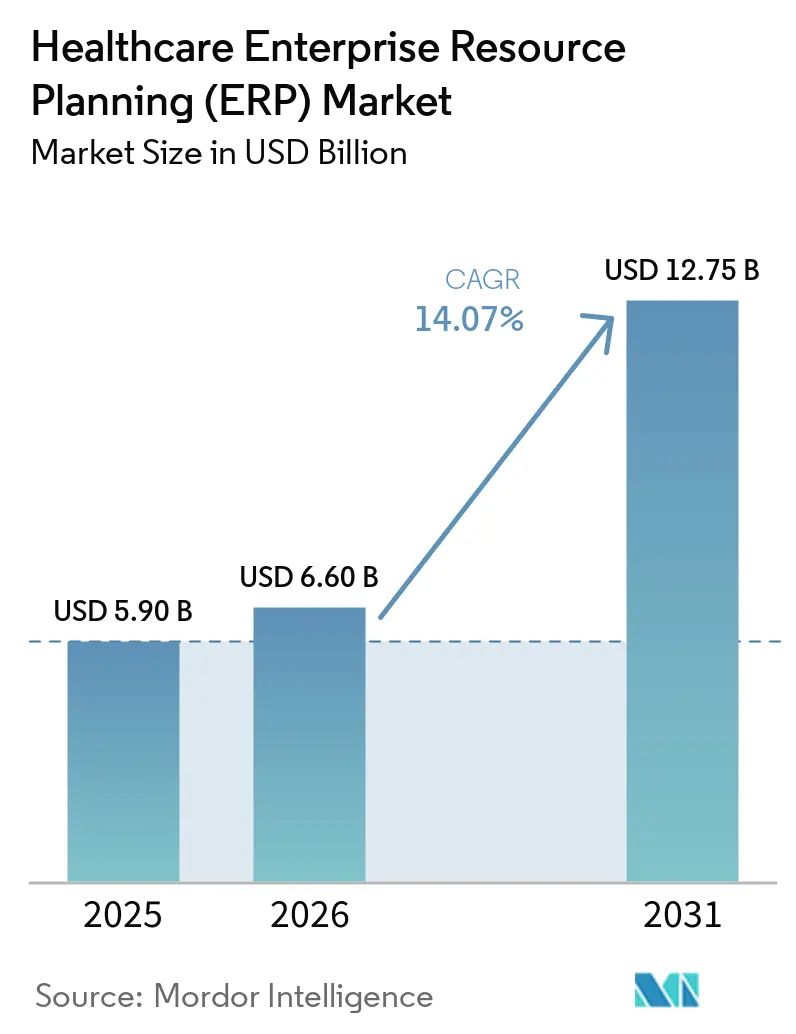

| Market Size (2026) | USD 6.60 Billion |

| Market Size (2031) | USD 12.75 Billion |

| Growth Rate (2026 - 2031) | 14.07% CAGR |

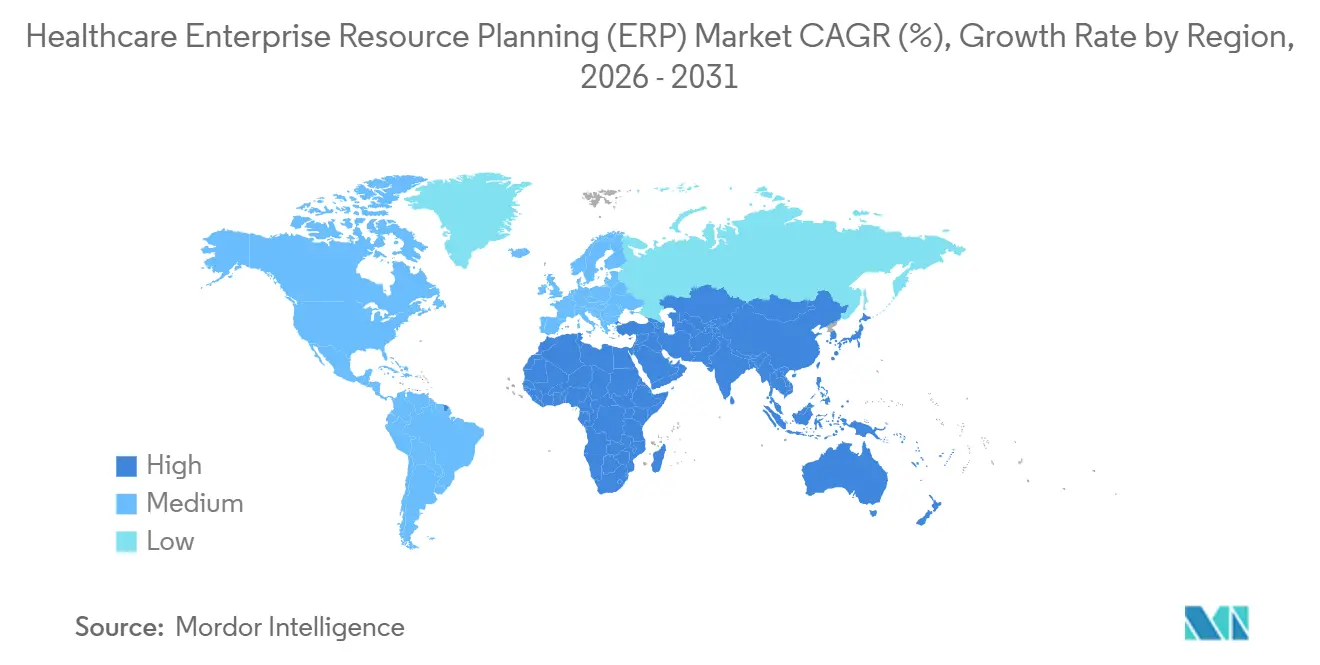

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

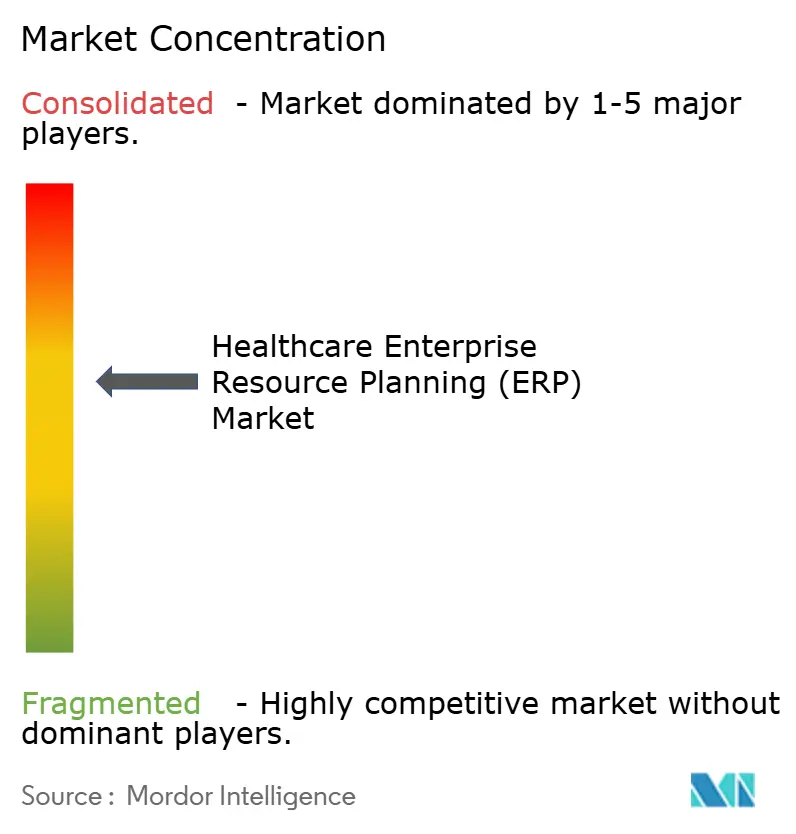

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Healthcare Enterprise Resource Planning (ERP) Market Analysis by ���ϲ�����

The healthcare ERP market size is projected to expand from USD 5.90 billion in 2025 and USD 6.60 billion in 2026 to USD 12.75 billion by 2031, registering a CAGR of 14.07% between 2026 and 2031. Disparate point solutions are giving way to unified platforms that combine artificial intelligence, real-time costing engines, and regulator-mandated interoperability. Cloud-based deployments accounted for nearly half of spending in 2025, yet hybrid architectures are growing even faster as hospitals keep sensitive clinical data on-premises while shifting finance, supply chain, and human resources workloads to public cloud infrastructure. Software still accounts for most revenue, though professional services are expanding briskly as workforce shortages push health systems to outsource data migration, HL7-to-FHIR integration, and change management. Finance and accounting remain the largest functional category, but serialization mandates and rising procurement costs are propelling double-digit gains in supply chain modules. Regionally, North America holds the lion’s share, while Asia-Pacific is the fastest growing corridor as large-scale national digitization programs roll out.

Key Report Takeaways

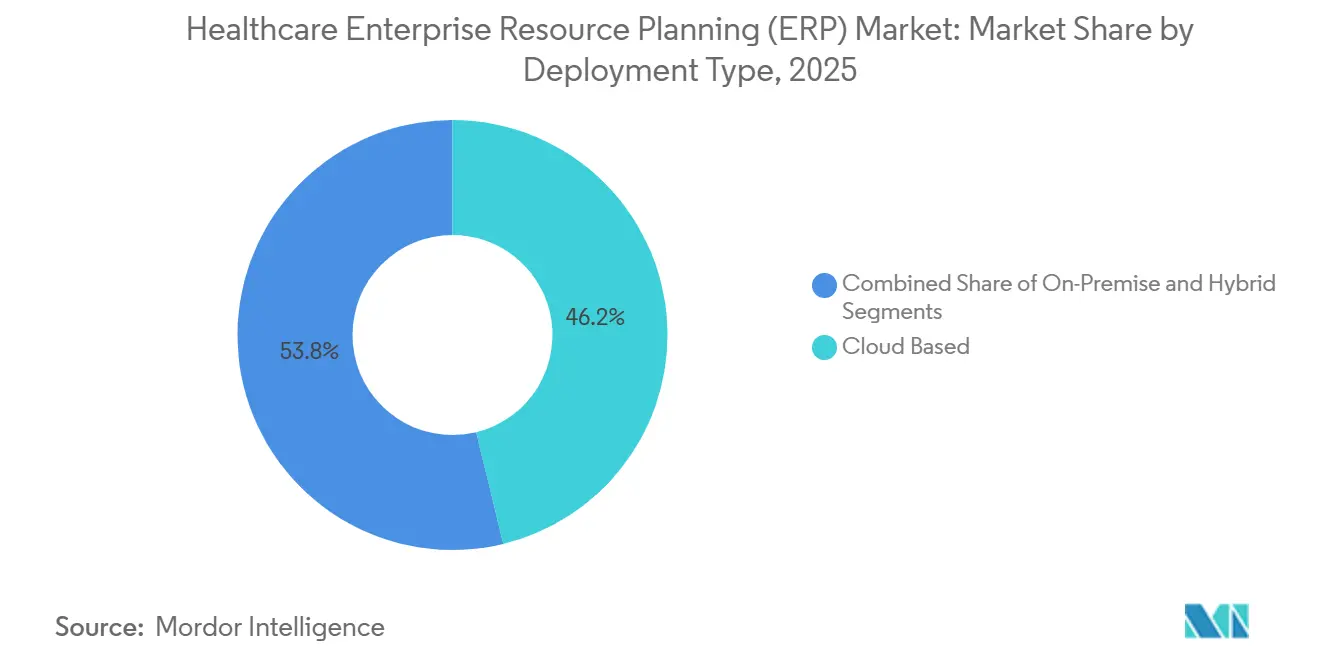

- By deployment model, cloud deployments led with 46.20% of the healthcare ERP market share in 2025, while hybrid architectures are forecast to grow at a 17.60% CAGR through 2031.

- By component, software licenses captured 61.00% of the healthcare ERP market in 2025, whereas services are projected to expand at a 15.40% CAGR from 2026 to 2031.

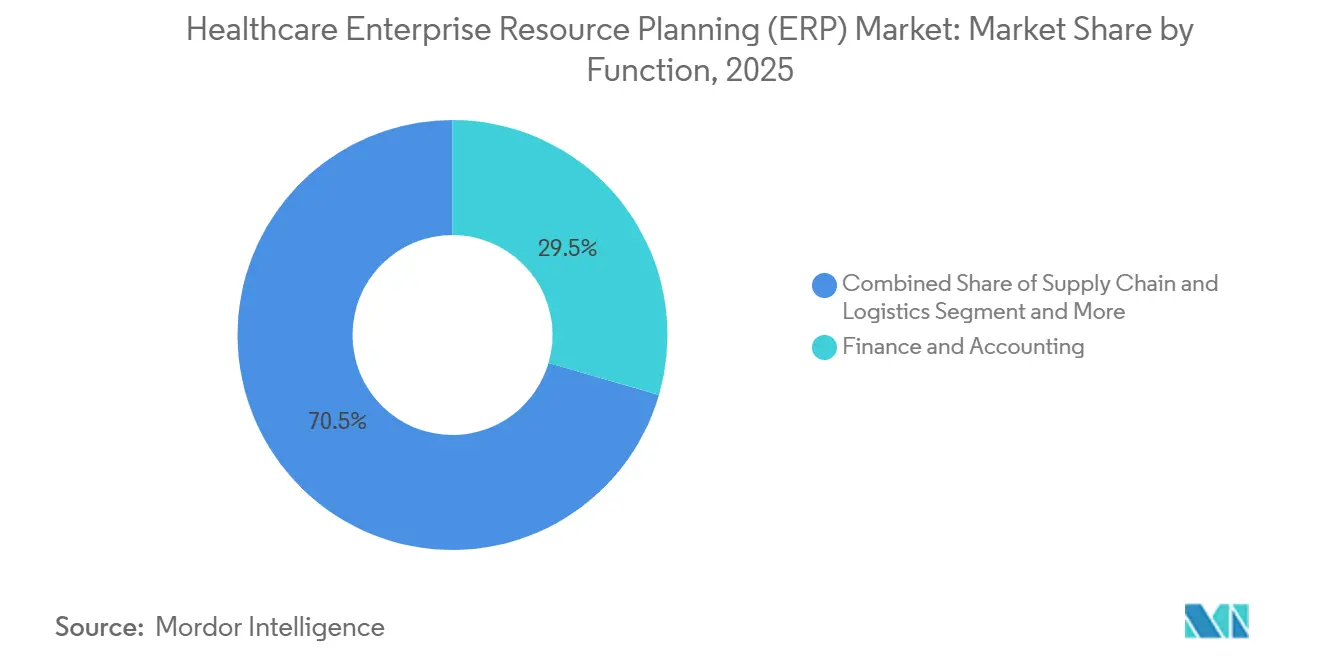

- By function, finance and accounting held 29.50% of the healthcare ERP market share in 2025; supply chain and logistics modules are advancing at a 14.90% CAGR to 2031.

- By end user, hospitals accounted for 38.00% of the healthcare ERP market in 2025, but pharmaceutical and biotechnology companies are the fastest movers, growing at a 16.20% CAGR through 2031.

- By geography, North America dominated with 41.70% revenue share in 2025, while Asia-Pacific posts the highest regional CAGR at 16.80% through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Enterprise Resource Planning (ERP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of AI Driven Analytics into ERP Suites | +3.2% | Global, early use in North America and Europe | Medium term (2-4 years) |

| Rising Demand for Real Time Patient Costing Visibility | +2.8% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Migration Toward Value Based Reimbursement Models | +2.5% | North America core, pilots in Europe and Australia | Medium term (2-4 years) |

| Post Pandemic Acceleration of Cloud First Hospital IT Strategies | +2.3% | Global | Short term (≤ 2 years) |

| Government Mandates for Interoperable Financial Reporting | +2.0% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Emergence of Industry Specific Low Code ERP Platforms | +1.5% | Global, rapid in mid-market hospitals | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Integration Of AI Driven Analytics Into ERP Suites

Artificial intelligence is shifting from descriptive dashboards to autonomous decisions that adjust staffing, inventory, and surgical scheduling in real time. Oracle embedded generative AI across its Fusion Cloud suite in 2024, allowing finance teams to converse with the ledger and automate journal entries.[1]Oracle Corporation, “Oracle Fusion Cloud Customer Stories,” oracle.com Infor CloudSuite Healthcare deployed machine learning to forecast implant demand using surgeon preference cards, reducing waste across multiple U.S. hospitals.[2]Infor, “AI in Healthcare Supply Chains,” infor.com Community Health Systems documented an 18% drop in claim denials six months after activating AI-powered revenue-cycle modules, translating into USD 47 million in recovered reimbursements chs.net. The ability to close monthly books in under five days is becoming a competitive necessity, especially where labor costs are highest. Vendors are racing to differentiate on AI capabilities rather than core transaction processing, magnifying the driver’s 3.2-point boost to the overall CAGR.

Rising Demand For Real Time Patient Costing Visibility

Bundled payments and prospective payment systems require granular cost attribution at the patient and procedure level. Traditional overnight batch costing is inadequate, so real-time engines now capture supply usage, labor stamps, and pharmacy dispenses as they occur, flagging margin leakage within hours. A 400-bed U.S. hospital piloting CostFlex cut per-case variance by 22% and enabled lower cost implant substitutions without harming outcomes. Infinx reported 14% faster prior-authorization turnaround, where finance and clinical data interfaced instantly. As CMS ties 30% of hospital reimbursement to cost-efficiency metrics by 2027, demand for real-time insight is spreading from North America to Asia-Pacific. The driver adds 2.8 percentage points to the CAGR.

Migration Toward Value Based Reimbursement Models

Fee-for-service is receding as alternative payment models proliferate. Over 40% of U.S. Medicare spend now funnels through MIPS and APM frameworks that penalize poor cost and quality reporting.[3]Centers for Medicare and Medicaid Services, “Quality Payment Program Overview,” cms.gov NextGen Healthcare clients using tightly integrated ERP and EHR platforms scored 27% higher under the Quality Payment Program, demonstrating the financial upside of interoperability. Population health modules within ERP suites stratify risk, enabling care teams to intervene early; a 2024 JAMIA study found a 19% drop in emergency visits when diabetic patients were proactively flagged. Europe is piloting bundled payments in orthopedics, extending this driver’s influence across the Atlantic. The trend contributes 2.5 points to CAGR.

Post Pandemic Acceleration Of Cloud First Hospital IT Strategies

COVID-19 exposed the brittleness of on-premise data centers during lockdowns. Hospitals now favor SaaS platforms that auto-patch, scale elastically, and offload disaster recovery. Monash Health replaced eight legacy systems with Oracle Fusion Cloud, lowering five-year total cost by 34% and eliminating a 12-person infrastructure team. Saudi provider Alrajhi Medicine is running Oracle Health Foundation EHR alongside Fusion Cloud ERP in a hybrid setup that handles 3,000 concurrent users without local servers. SAP will end mainstream support for ECC 6.0 in 2027, further nudging laggards onto cloud editions. The cloud-first pivot boosts CAGR by 2.3 points worldwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Licensing and Implementation Costs | -2.1% | Global, acute in rural and critical-access hospitals | Short term (≤ 2 years) |

| Data Security Concerns Around Multi Tenant Cloud Deployments | -1.6% | North America and Europe, heightened post-breach | Medium term (2-4 years) |

| Shortage of Healthcare IT Staff Skilled in ERP Migration | -1.2% | Global, severe in North America and Europe | Long term (≥ 4 years) |

| Integration Complexities With Legacy Clinical Systems | -1.0% | Global, acute in hospitals with aging EHRs | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High Upfront Licensing And Implementation Costs

Enterprise projects often exceed budgets by 30-50% as scope expands and data migration missteps surface. University Hospitals in Ohio said its USD 400 million Epic build needed another USD 80 million in consulting and hardware, while Trinity Health’s USD 800 million rollout forced other IT projects into limbo.[4]University Hospitals, “2024 Financial Statements,” uhhospitals.org Source: Reuters, “TriZetto Breach Costs Rise,” reuters.com Mid-size hospitals budgeting USD 5-10 million often see hidden interface costs push totals to near USD 20 million. Rural facilities with thin margins postpone modern ERP altogether, prolonging spreadsheet-driven processes that elevate compliance risk. Inflation-driven consulting rates keep pressure high, shaving 2.1 points from CAGR worldwide.

Data Security Concerns Around Multi Tenant Cloud Deployments

Lateral attack surfaces in shared-tenant clouds intensify scrutiny of encryption, access controls, and residency guarantees. Precipio Diagnostics and Insightin Health each suffered breaches in 2025, while the 2024 TriZetto incident cost the vendor USD 120 million in remediation. Healthcare breaches have risen 93% over three years, with average ransomware demands hitting USD 1.4 million. HIPAA’s USD 1.5 million-per-category fines and Europe’s GDPR penalties further chill buying cycles. Hospitals now require third-party audits and contractual breach clauses, adding costs and lengthening sales cycles, trimming 1.6 points from CAGR.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Balance Control And Innovation

Hybrid cloud installations are advancing at a 17.60% CAGR through 2031. Although cloud captured 46.20% of the healthcare ERP market share in 2025, chief information officers still keep electronic health records and certain analytics on-premise for latency and sovereignty reasons. Hybrid lets finance and supply chain migrate first, easing capex while meeting regional data-localization rules. On-premise footprints shrink but persist inside academic medical centers, housing decade-old middleware investments. Monash Health’s split deployment cut total cost by 34% in five years, while Saudi Arabia’s Alrajhi Medicine supports thousands of users in a similar setup. The model’s growth underscores how the healthcare ERP market rewards deployment agility amid tightening privacy mandates.

A second tailwind is vendor policy. SAP sunsets ECC mainstream maintenance in 2027, and Oracle’s latest license terms favor cloud renewals. Hospitals unable to fully exit data centers are selecting containerized middleware to bridge on-premise clinical engines with cloud-resident administrative modules. The healthcare ERP market size for hybrid deployments will therefore widen its lead among large systems and cross-border groups where customs, shipping, and multi-currency accounting add complexity.

By Component: Services Surge Amid Implementation Complexity

Software still accounted for 61.00% of revenue in 2025, but services are expanding at 15.40% each year, as a few hospitals retain staff to map clinical workflows into ERP templates. The healthcare ERP market, including consulting, integration, and managed services, will exceed USD 5 billion by 2031. Nordic Consulting and Pivot Point are packaging fixed-fee migrations that promise go-lives in under 12 months. Shortages of qualified staff, average ERP vacancy sits at 89 days, keep driving outsourcing demand.

Low-code platforms reduce but do not eliminate configuration work; mapping cost centers, catalog items, and grant codes into pre-built objects still requires domain expertise. Pharmaceutical firms face additional validation complexity under 21 CFR Part 11, swelling documentation and test-script workloads. As subscription licensing compresses software margins, vendors themselves are ramping up implementation arms, ensuring the healthcare ERP market continues to shift its revenue mix toward services.

By Function: Supply Chain Modules Capture Serialization Mandates

Finance and accounting held 29.50% healthcare ERP market share in 2025, yet supply chain modules are now the fastest-growing niche. United States DSCSA and Europe’s Falsified Medicines Directive mandate unit-level traceability by 2027, pressing hospitals and manufacturers alike to integrate scanning, RFID, and temperature logs directly into ERP workflows. GHX pilots showed 22% lower inventory carrying costs after predictive replenishment, and AI-guided implant selection is saving systems millions. The healthcare ERP market size linked to supply chain is projected to grow at a 14.90% CAGR as providers chase 2-3-point margin gains.

Beyond drugs and devices, consumables such as lab reagents and PPE now feed real-time dashboards that compare contract prices against catalog spend. As value-based care magnifies the cost of waste, boards are reallocating budgets from standalone materials management systems to unified ERP modules that align purchasing with clinical demand.

By End User: Pharmaceutical Companies Drive Compliance Spend

Hospitals accounted for 38.00% of spending in 2025, yet pharmaceutical and biotech firms will deliver the steepest gains, with a 16.20% CAGR to 2031. Serialization, electronic batch-records, and cold-chain integrity raise the stakes; SAP S/4HANA already powers 95% of big pharma finance and production, and newer entrants like RxERP layer FEFO warehouse logic on top. The healthcare ERP market size attached to pharmaceutical users benefits from continual line extensions, global recall coordination, and stringent FDA audit trails.

Clinics and ambulatory surgical centers, meanwhile, pick lightweight SaaS suites that start under USD 1 million, bundling claims, scheduling, and materials tracking. Medical device makers and payers round out demand, integrating regulatory submissions and actuarial models, respectively. Combined, these groups ensure the healthcare ERP market maintains diversified demand across its forecast horizon.

Geography Analysis

North America commanded 41.70% of revenue in 2025. ONC’s HTI-1 Final Rule extended information-blocking definitions to financial data, compelling the use of certified FHIR APIs for billing and claims exchange. U.S. hospitals alone invest USD 90-100 billion in IT annually, while Canada pilots province-wide ERP rollouts to harmonize fiscal reporting. Mexican private hospitals are embracing ERPs to attract medical tourists and secure international accreditations.

Asia-Pacific is expanding at 16.80% CAGR. China’s National Health Commission targets 95% digitization of tertiary hospitals by 2030, pushing ERP and EHR bundles into 30,000 facilities. Japan’s My Number insurance card, launched in 2024, requires back-office integration for real-time copay adjudication, and India’s Ayushman Bharat Digital Mission gives 600 million citizens unified IDs, spiking transaction volumes that only cloud ERPs can handle. Australia’s My Health Record ties financial and clinical data together as part of its national digital health strategy.

Europe held roughly one-quarter of sales, led by Germany, the United Kingdom, and France. GDPR’s stiff fines force vendors to guarantee regional data residency. Germany’s mandatory ePA aligns clinical and fiscal datasets, and the U.K. NHS Federated Data Platform unifies metrics across more than 200 trusts. The implementation of the European Health Data Space from 2025 introduces cross-border billing data requirements. South America grows off a smaller base, with Brazil upgrading private chains and Argentina modernizing public hospitals. The Middle East enjoys double-digit CAGR, exemplified by Saudi Arabia’s SAR 100 billion (USD 26.63 billion) Vision 2030 investment and the United Arab Emirates’ Smart Dubai Health program, all catalysts for the healthcare ERP market.

���ϲ����� provides coverage of the healthcare erp market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The healthcare ERP market remains moderately concentrated. SAP, Oracle, Microsoft, and Workday together hold a mid-revenue share. SAP dominates pharmaceutical manufacturing with its S/4HANA suite, which embeds serialization and 21 CFR Part 11 validation. Oracle’s 2024 absorption of Cerner forged an end-to-end EHR-ERP stack but added integration burdens that slow cross-selling. Microsoft leverages Azure and Dynamics 365 to bundle ERP, CRM, and collaboration at a lower cost, courting hospitals already standardized on Microsoft 365. Workday excels in human capital management, securing academic medical centers that prize unified payroll and credentialing.

Vendor strategies converge on platform breadth, AI infusions, and low-code configurability that trims go-lives under 12 months, a critical edge as 83% of providers struggle to hire ERP talent. Infor CloudSuite Healthcare and Epicor address the mid-market hospital market with surgery scheduling, implant tracking, and regulatory presets. NetSuite and Acumatica target ambulatory clinics with bundles priced 30-40% below incumbents, while low-code newcomers enable on-the-fly workflow tweaks that reduce dependence on programmers.

White-space opportunities cluster in specialty practices, post-acute care, and cross-border provider groups. Security-first buyers gravitate to single-tenant or sovereign-cloud offerings, encouraging hyperscalers to spin up regional health clouds. As incumbents pivot to subscription models and tuck-in acquisitions, the healthcare ERP market welcomes fresh entrants intent on niche verticals and AI-driven automation of revenue-cycle, supply chain, and workforce planning.

Healthcare Enterprise Resource Planning (ERP) Industry Leaders

SAP SE

Oracle Corporation

Infor, Inc.

Microsoft Corporation

Epicor Software Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Oracle expanded Oracle Health Foundation EHR and Fusion Cloud ERP at Alrajhi Medicine, supporting 3,000 concurrent users across Saudi facilities.

- January 2026: Microsoft released AI-powered financial planning modules in Dynamics 365 for healthcare, cutting budget cycle times by 25%.

- November 2025: SAP finished migrating 15 pharmaceutical firms to S/4HANA Cloud with serialization features for DSCSA compliance.

- October 2025: Workday partnered with Epic to link financial and HCM data with EHR workflows at academic medical centers.

Global Healthcare Enterprise Resource Planning (ERP) Market Report Scope

The Healthcare ERP market encompasses specialized enterprise software solutions and associated services that manage, integrate, and optimize administrative, financial, and operational processes across healthcare organizations and related entities. Healthcare ERP systems are purpose-built platforms that centralize core functions such as finance, supply chain management, human resources, customer relationship management (CRM), and inventory management into a unified system. These solutions are tailored to address the unique requirements of the healthcare sector, including regulatory compliance, patient-centric operations, complex supply chains, and operational efficiency across clinical and non-clinical functions.

The Healthcare ERP Report is Segmented by Deployment Model (Cloud Based, On Premise, and Hybrid), Component (Software, and Services), Function (Finance and Accounting, Supply Chain and Logistics, and more), End User (Hospitals, Clinics and Ambulatory Surgical Centers, Pharmaceutical and Biotechnology Companies, and more), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Cloud Based |

| On Premise |

| Hybrid |

| Software |

| Services |

| Finance and Accounting |

| Supply Chain and Logistics |

| Human Resources |

| Customer Relationship Management |

| Inventory and Material Management |

| Other Functions |

| Hospitals |

| Clinics and Ambulatory Surgical Centers |

| Pharmaceutical and Biotechnology Companies |

| Medical Device Manufacturers |

| Health Insurance Providers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Model | Cloud Based | |

| On Premise | ||

| Hybrid | ||

| By Component | Software | |

| Services | ||

| By Function | Finance and Accounting | |

| Supply Chain and Logistics | ||

| Human Resources | ||

| Customer Relationship Management | ||

| Inventory and Material Management | ||

| Other Functions | ||

| By End User | Hospitals | |

| Clinics and Ambulatory Surgical Centers | ||

| Pharmaceutical and Biotechnology Companies | ||

| Medical Device Manufacturers | ||

| Health Insurance Providers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will global spending on healthcare ERP become by 2031?

The healthcare ERP market size is forecast to reach USD 12.75 billion by 2031, expanding at a 14.07% CAGR from 2026.

Which deployment model is growing the fastest?

Hybrid cloud deployments are advancing at a 17.60% CAGR through 2031 as providers balance data-control with cloud scalability.

Why are pharmaceutical manufacturers investing heavily in ERP?

Serialization mandates, electronic batch-record validation, and cold-chain tracking under 21 CFR Part 11 are driving a 16.20% CAGR for pharma ERP adoption.

What is the main restraint on ERP rollouts in rural hospitals?

High upfront licensing and consulting costs, often topping USD 15 million for mid-size projects, still deter many rural facilities.

How are AI capabilities changing ERP benefits?

Embedded AI now automates journal entries, predicts implant demand, reduces claim denials, and cuts month-end close times by half, improving both cost and speed.

Which region is expected to post the highest growth rate?

Asia-Pacific leads with a 16.80% CAGR as China, Japan, India, and Australia accelerate national healthcare digitization programs.

Page last updated on: