Health Economics And Outcomes Research (HEOR) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 3.68 Billion |

| Growth Rate (2026 - 2031) | 13.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Health Economics And Outcomes Research (HEOR) Services Market Analysis by ���ϲ�����

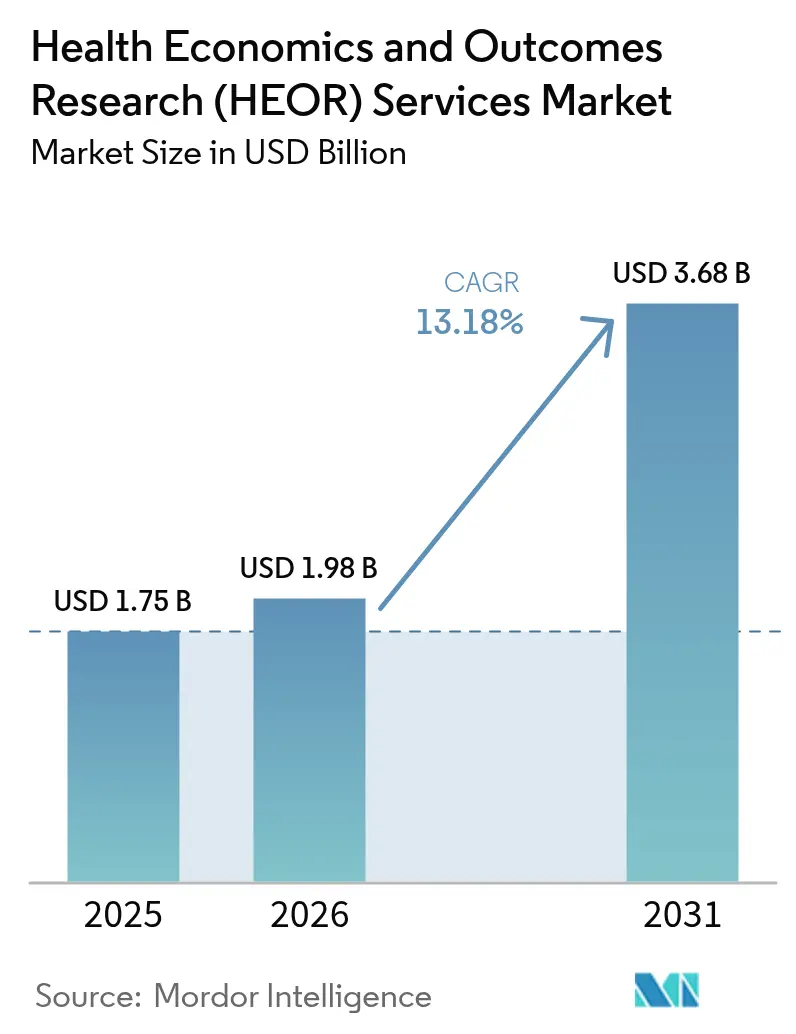

The Health Economics And Outcomes Research Services market size is expected to grow from USD 1.75 billion in 2025 to USD 1.98 billion in 2026 and is forecast to reach USD 3.68 billion by 2031 at 13.18% CAGR over 2026-2031.

Heightening reimbursement scrutiny, the shift to value-based payment models, and widening health technology assessment (HTA) mandates are fueling demand for faster, more defensible evidence packages. Generative AI cuts literature-review cycle times by 60%, reshaping project economics and enabling early payer engagement. Multinational pharmaceutical pipelines, especially in obesity, oncology, and gene therapy, generate sustained needs for sophisticated cost-effectiveness modeling. Service providers deploy large language models on federated real-world data (RWD) networks to unlock multi-jurisdiction evidence without breaching privacy guardrails. Providers that combine therapeutic depth with AI-enabled workflow automation are widening their competitive moat as clients consolidate vendor panels to generate integrated clinical-to-economic evidence.

Key Report Takeaways

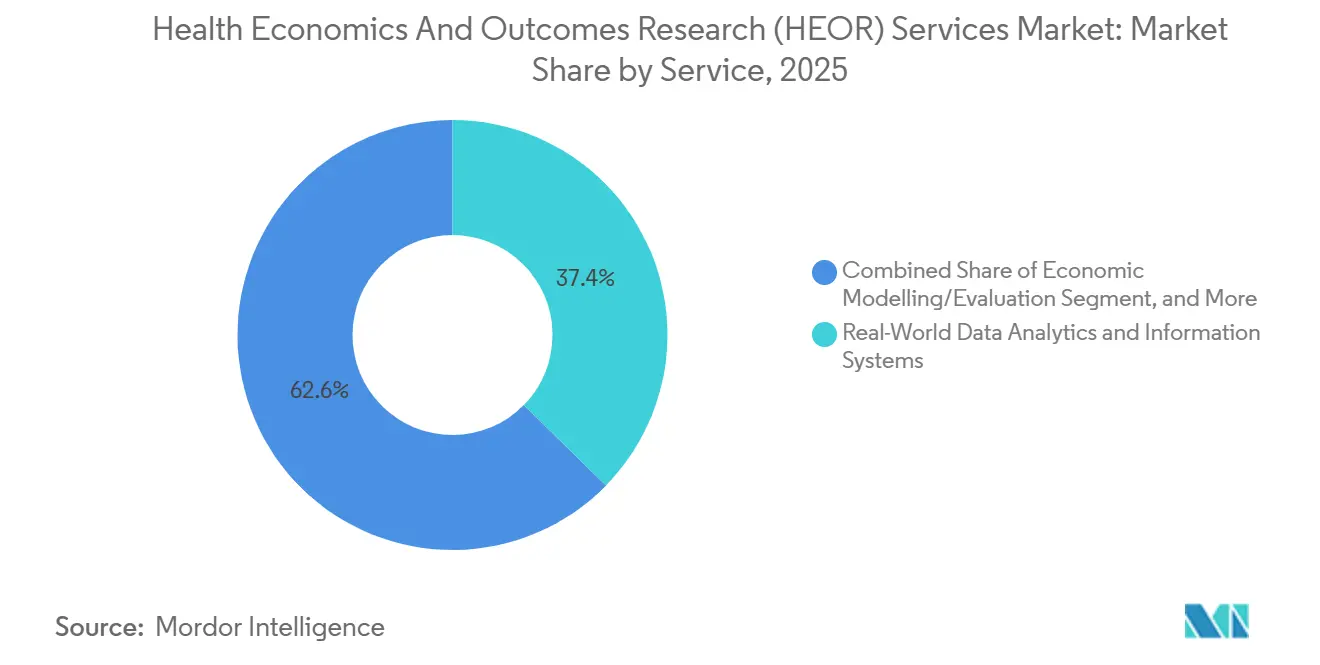

- By service, real-world data analytics & information systems led with 37.35% revenue share in 2025; market access & reimbursement is projected to expand at a 16.82% CAGR to 2031.

- By service provider, consultancies held 47.86% of the health economics and outcomes research services market share in 2025, while contract research organizations recorded the highest projected CAGR at 15.05% through 2031.

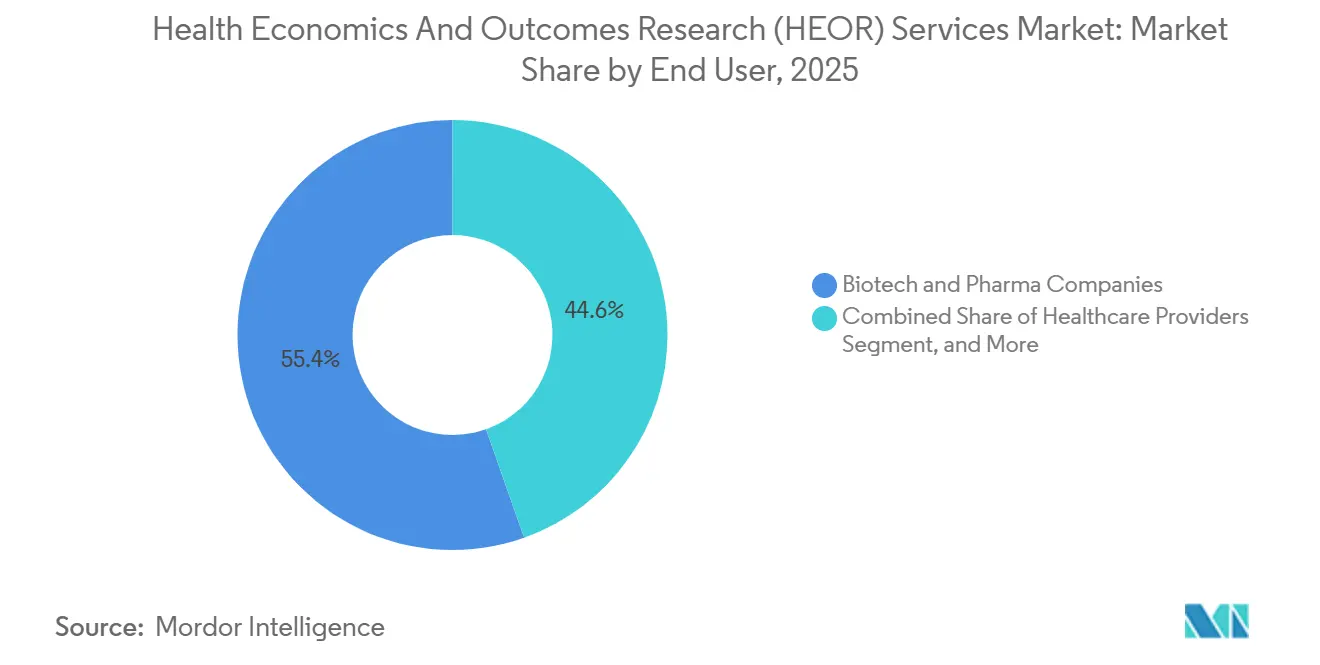

- By end user, biotech & pharma companies accounted for 55.42% of the health economics and outcomes research services market in 2025, and healthcare providers are advancing at a 14.46% CAGR through 2031.

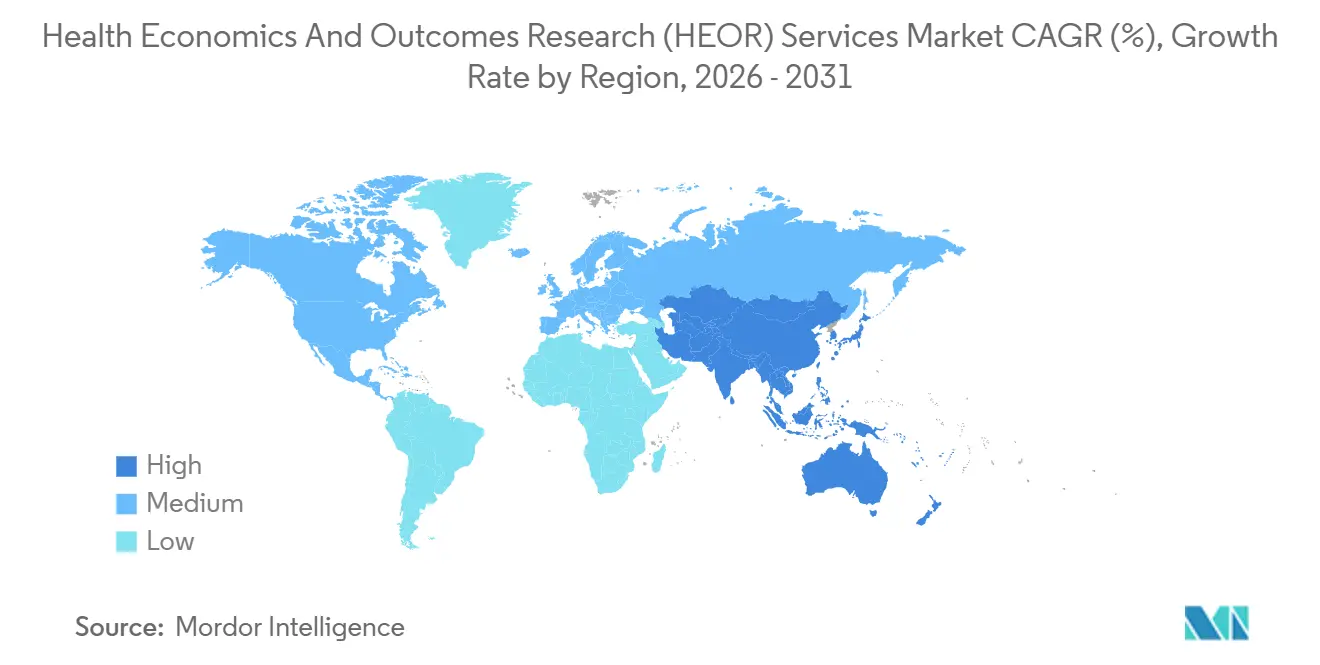

- By geography, North America captured a 45.95% share in 2025; Asia Pacific is forecast to rise at a 17.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Health Economics And Outcomes Research (HEOR) Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing demand for real-world evidence for reimbursement | +3.2% | Global; strongest in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Expansion of HTA & value-based care frameworks | +2.8% | Europe, Asia-Pacific, North America | Long term (≥4 years) |

| Surge in novel drug launches & clinical trials | +2.5% | Oncology and rare-disease hubs worldwide | Short term (≤2 years) |

| Generative-AI-enabled rapid evidence synthesis | +1.9% | North America, Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Federated multi-jurisdiction RWD networks | +1.4% | Europe, North America, nascent in Asia-Pacific | Long term (≥4 years) |

| Vendor consolidation toward integrated HEOR-clinical platforms | +1.1% | Global | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Growing Demand for Real-World Evidence for Reimbursement

Payers increasingly require real-world effectiveness data to justify premium pricing and coverage terms. The FDA’s 2024 guidance endorsing electronic health record and claims data for regulatory decision-making firmly positions RWD as a primary evidence stream.[1]U.S. Food and Drug Administration, “Use of Real-World Evidence to Support Regulatory Decision-Making,” fda.gov The Centers for Medicare & Medicaid Services expanded outcomes-based contract structures to 40% more therapeutic areas than in 2023, raising the stakes for manufacturers that lack mature RWE programs. Europe’s HTA Regulation adds a second compliance layer by obliging multinational dossiers to include comparative effectiveness data across 27 member states. Collectively, these mandates shift budgets toward analytics platforms capable of transforming dispersed claims, registry, and device telemetry data into payer-ready economic narratives. Premium pricing commanded by specialized RWE boutiques highlights the urgency with which sponsors are closing evidence gaps ahead of post-launch price negotiations.

Expansion of HTA / Value-Based Care Frameworks

Global HTA bodies now evaluate therapies using broader societal value criteria, extending beyond traditional cost-per-QALY thresholds. The EU Joint Clinical Assessment, in effect since January 2025, establishes a harmonized evidence dossier for oncology and ATMPs while allowing member states to maintain price autonomy.[2]RTI Health Solutions, “EU Joint Clinical Assessment: Implications for Evidence Generation,” rti.org Japan, South Korea, and China are strengthening HTA review depth, integrating budget impact and patient-reported outcomes. The French National Authority for Health’s 2025-2030 roadmap prioritizes AI screening tools to vet manufacturer submissions, signaling a digital transformation within the assessors themselves.[3]French National Authority for Health, “2025-2030 Strategic Plan,” has-sante.fr In the United States, hospital systems enrolled in alternative payment models must demonstrate procedure-level cost-effectiveness, accelerating provider-led outcomes research purchases. Heightened methodological expectations push sponsors toward specialist consultants with credentialed pharmacoeconomists and multi-country data rights.

Surge in Novel Drug Launches & Clinical Trials

Clarivate’s 2025 “Drugs to Watch” lists 11 assets forecast to exceed USD 1 billion annual sales within two years of launch, spanning obesity, oncology, and gene therapy. Each modality poses unique modeling challenges; one-time gene therapies require lifetime horizon projections, while GLP-1 obesity drugs demand budget impact detail across public and private payer pools. Concurrently, decentralized and hybrid trials produce volumetric wearable and app data demanding advanced cleaning and linkage methods. ICON’s tokenization platform processes 10 billion annual patient transactions, feeding this data into economic models that assess therapy durability beyond short-run trial endpoints. Rising pipeline complexity, therefore, amplifies the demand for HEOR specialists who are conversant in both advanced analytics and disease-area nuances.

Generative-AI-Enabled Rapid Evidence Synthesis

Large language models are moving from proof-of-concept to production within HEOR workflows. ISPOR’s 2024 evaluation found that systematic reviews were 60% faster without a loss in quality. IQVIA’s AI Assistant ingests 530 million deidentified patient records, automatically scopes research questions, and drafts GRADE-compliant evidence summaries for human validation. Firms embed retrieval-augmented generation to detect safety signals across live claims feeds, creating near-real-time economic models that anticipate payer renegotiations. Regulators direct developers to maintain algorithm transparency and human oversight, codified in the FDA’s 2024 AI pharmacovigilance draft guidance. These compliance guardrails favor incumbents with robust validation infrastructure, widening the competitive gap against tech-lite boutiques.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Scarcity of skilled HEOR specialists | −1.8% | Global; acute in North America, Europe | Short term (≤2 years) |

| Privacy restrictions limiting RWD access | −1.3% | Europe (GDPR), North America (HIPAA) | Medium term (2-4 years) |

| Payer skepticism over AI model transparency | −0.9% | Europe, North America | Medium term (2-4 years) |

| Cloud-compute inflation is raising modeling costs | −0.7% | Global | Short term (≤2 years) |

| Source: ���ϲ����� | |||

Scarcity of Skilled HEOR Specialists

Industry surveys forecast a 35% global shortfall in qualified health economists by 2030 as demand outstrips academic pipeline output. Axtria alone plans to hire 1,000 data scientists in India to shore up modeling capacity. Wage premiums climb and project lead times lengthen, squeezing service-provider margins even as top-line demand accelerates. Specialized fields such as cell-therapy modeling suffer most because standard pharmacoeconomic curricula lag behind therapeutic innovation, forcing firms to retrain clinical statisticians on value-assessment frameworks.

Privacy Restrictions Limiting RWD Access

GDPR has curtailed cross-border patient-level data flows by 40% since 2024, compelling country-specific analyses and raising project duplication costs. HIPAA and a patchwork of US state privacy laws further constrain data linkages between payers, providers, and researchers. New national-security directives on genomic data transfers tighten controls in China and the United States. Smaller biotech companies, lacking dedicated privacy counsel, face prohibitive compliance burdens and may defer launch in markets where evidence demands outweigh internal capacity. Fragmented datasets reduce the statistical power of cost-effectiveness analyses, risking negative reimbursement decisions.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Real-World Data Dominates, Market Access Accelerates

Real-World Data Analytics & Information Systems accounted for 37.35% of revenue in 2025, reflecting sponsors’ need for defensible economic evaluations grounded in routine-care evidence. Consultancies and CROs invest in scalable cloud architectures that query claims, registries, and wearables data in near real time, shortening evidence cycles and reducing manual abstraction labor. The segment benefits from regulators’ explicit endorsement of RWD, with FDA guidance accelerating purchase decisions among late-stage biotech developers. Competitive pressure spurs innovation: IQVIA rebadged its HTA Accelerator as Market Access Insights in 2024, bundling dossier automation with budget impact simulation. Looking ahead, automated platform adoption, regional data-access partnerships, and the integration of payer adjudication feeds will keep the segment expanding faster than the overall health economics and outcomes research services market, as sponsors double down on post-launch real-world performance monitoring.

Market Access & Reimbursement is the fastest-growing service line with a 16.82% CAGR through 2031. Rising HTA rigor and divergent sub-national payer rules require continuous benefit re-assessment, especially for one-time therapies whose value unfolds over decades. Vendors are embedding policy trackers and scenario engines that flag threshold breaches for list-price renegotiations, helping clients pre-empt formulary delisting risks.

By Service Provider: Consultancies Lead, CROs Gain Ground

Consultancies retained 47.86% of % health economics and outcomes research services market share in 2025, thanks to entrenched C-suite relationships and strategy pedigree. Yet CROs expand at 15.05% CAGR on the back of integrated development offerings that bundle evidence planning with protocol design and site operations. The model promises seamless data flow from trial to launch, lowering handover risk and reducing vendor count. ICON’s Real World Intelligence suite, built on tokenized patient IDs, illustrates the convergence; it converts clinical database snapshots directly into payer-ready economic evidence.

Syneos Health similarly scales longitudinal data assets to inform portfolio strategy, price-volume negotiations, and real-time safety analytics. Boutique HEOR firms respond by specializing in high-uncertainty modalities, for example, cell and gene therapy annuity modeling, where agility trumps scale. M&A activity is set to intensify as platforms seek to fill gaps in therapeutic depth or secure regional data entitlements.

By End-User: Pharma Dominates, Providers Emerge

Biotech & Pharma Companies represent 55.42% of end-user demand in 2025, reflecting the sector's primary responsibility for generating health economic evidence to support regulatory submissions and reimbursement negotiations. However, healthcare providers exhibit the strongest growth trajectory, with a 14.46% CAGR through 2031, signaling the market's evolution toward provider-led outcomes research as value-based care adoption accelerates across global healthcare systems. This shift reflects providers' increasing need to demonstrate treatment effectiveness and cost-efficiency to payers, particularly as bundled payment models expand beyond traditional fee-for-service arrangements.

Government & HTA Agencies maintain steady demand for specialized assessment capabilities, with the EU's Joint Clinical Assessment implementation creating new evidence requirements across 27 member states. The Canadian Drug Agency's establishment in 2024, following CADTH's transition, exemplifies how government bodies are strengthening their HTA capabilities to manage pharmaceutical spending more effectively. Other End Users, including medical device manufacturers and digital health companies, represent emerging growth opportunities as these sectors face increasing pressure to demonstrate clinical and economic value. The end-user diversification suggests market maturation, where HEOR services are becoming essential across the broader healthcare ecosystem rather than remaining concentrated within pharmaceutical companies.

Geography Analysis

North America captured 45.95% revenue in 2025, underpinned by sophisticated reimbursement schemes that demand robust economic evidence. The FDA’s RWD framework validation propels analytic spending and cements the United States as the reference market for methodological standards. Canada’s transformation of CADTH into the Canadian Drug Agency strengthens national HTA capacity and is expected to widen economic scrutiny of specialty drugs. Shortfalls in data-science talent and wage inflation could temper regional growth; nonetheless, mid-term expansion remains resilient because pipeline intensity translates directly into HEOR workload.

Asia Pacific posts the fastest CAGR of 17.93% through 2031, driven by rising clinical-trial volume, drug-pricing reforms, and digital-health infrastructure upgrades. Japan’s 2025 drug-price adjustments tie reimbursement to real-world utilization, spurring pharmaceutical companies to adopt proactive budget-impact tracking. China’s NMPA alignment with ICH guidelines increases global dossier commonality, yet provincial tendering rules still require province-level evidence cuts. India’s RWD network pilots provide cost-effective data sources for multinationals seeking broader ethnic representation. Service providers are localizing staff and forging data-licensing ventures with hospital consortia to comply with data localization statutes.

Europe maintains a substantial share owing to the newly operational Joint Clinical Assessment, which standardizes the clinical-effectiveness components of submissions across 27 member states. While dossier unification reduces duplication, national payers retain price-setting autonomy, compelling sponsors to run country-specific budget-impact analyses. The French National Authority for Health’s AI evaluation program sets a precedent for algorithm-assisted appraisal, potentially accelerating the review of AI-ready dossiers. Middle East & Africa and South America display mixed trajectories. Saudi Arabia operationalized managed entry agreements, pulling in HEOR expertise to structure risk-sharing deals. Brazil’s judiciary overrules negative HTA recommendations in most patient litigation cases, inserting uncertainty that forces extensive scenario modeling. Vendors that master heterogeneous evidence rules position themselves for outsized wins as payer systems mature.

Competitive Landscape

The health economics and outcomes research services market shows moderate concentration, with technology scale acting as a primary moat. IQVIA, ICON, and Syneos Health occupy leadership positions through end-to-end capabilities, large patient-level databases, and deep regulatory affairs consulting. IQVIA’s AI Assistant, launched in October 2024, automates evidence-synthesis tasks and integrates conversational analytics with its longitudinal data warehouse. ICON acquires niche modeling teams to deepen gene-therapy economics expertise, while Syneos Health invests in cloud-native simulation engines for rapid scenario testing.

Mid-tier players such as Axtria compete on analytics accelerators but face pressure to recruit talent, prompting aggressive outreach to academic programs and offshore hubs. Specialist boutiques differentiate through therapeutic focus; Analysis Group leverages oncology trial liaison networks to deliver payer-preferred indirect-comparison studies. Emerging entrants exploit decentralized-trial datasets and digital ROI measurement for medical-device clients, seeding future consolidation targets. Algorithmic transparency mandates and data-sovereignty laws create compliance overhead that may tilt the share toward incumbent firms with established governance frameworks.

Health Economics And Outcomes Research (HEOR) Services Industry Leaders

Axtria, Inc.

Syneos Health

McKesson Corporation

Optum (UnitedHealth Group)

Pharmalex GmBH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Red Nucleus agreed to acquire Bridge Medical Consulting to strengthen its AI-enabled systematic-review and integrated-evidence planning capabilities.

- October 2025: HealthVerity and Claritas Rx launched a partnership to link privacy-compliant real-world data with patient-journey analytics, boosting evidence generation across the product lifecycle.

- July 2025: LCP Health Analytics partnered with COTA to develop cross-border oncology RWD methodologies for multinational HTA submissions.

- May 2025: Cytel and Nested Knowledge integrated AI automation into the LiveSLR® platform, creating a living evidence environment for HEOR and HTA.

- February 2025: France’s HAS released a 202has 5-2030 strategy that prioritizes AI adoption in evidence evaluation, foreshadowing methodological updates for EU HTA bodies.

Global Health Economics And Outcomes Research (HEOR) Services Market Report Scope

As per the scope of the report, health economics and outcomes research (HEOR) services guide healthcare providers to examine and select from multiple treatment options. The HEOR services establish and measure the link between treatment and actual outcomes. Therefore, enables evidence-based guidance for improving care. The health economics and outcomes research (HEOR) services market is segmented by service, providers, end user, and geography. By service, the market is segmented into economic modelling/evaluation, real-world data analysis and information systems, clinical outcomes, and market access solutions and reimbursement, among others. By service provider, the market is segmented into consultancy and contract research organizations (CROs). By end users, the market is segmented into biotech/pharma companies, healthcare providers, government organizations, and healthcare payers. By geography, the market is segmented as North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers the value (in USD) for the above segments.

| Economic Modelling / Evaluation |

| Real-World Data Analytics & Information Systems |

| Clinical Outcomes Research |

| Market Access & Reimbursement |

| Other Services |

| Consultancies |

| Contract Research Organisations (CROs) |

| Biotech & Pharma Companies |

| Healthcare Providers |

| Government & HTA Agencies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa |

| By Service | Economic Modelling / Evaluation | |

| Real-World Data Analytics & Information Systems | ||

| Clinical Outcomes Research | ||

| Market Access & Reimbursement | ||

| Other Services | ||

| By Service Provider | Consultancies | |

| Contract Research Organisations (CROs) | ||

| By End-User | Biotech & Pharma Companies | |

| Healthcare Providers | ||

| Government & HTA Agencies | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How big is the health economics and outcomes research services market in 2026?

The market is valued at USD 1.98 billion in 2026 and is projected to grow rapidly through 2031.

What is the forecast CAGR for HEOR services through 2031?

Global revenue is expected to rise at a 13.18% CAGR during 2026-2031.

Which service line within HEOR generates the most revenue today?

Real-World Data Analytics & Information Systems leads, accounting for 37.35% of 2025 revenue.

Which region is growing fastest for HEOR outsourcing?

Asia Pacific is forecast to expand at an 17.93% CAGR to 2031 due to maturing HTA frameworks and rising clinical-trial activity.

What technological shift is most affecting evidence-generation timelines?

Generative AI cuts systematic-review cycle times by 60%, enabling quicker payer submissions and market access decisions.

Page last updated on: