Green Building Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

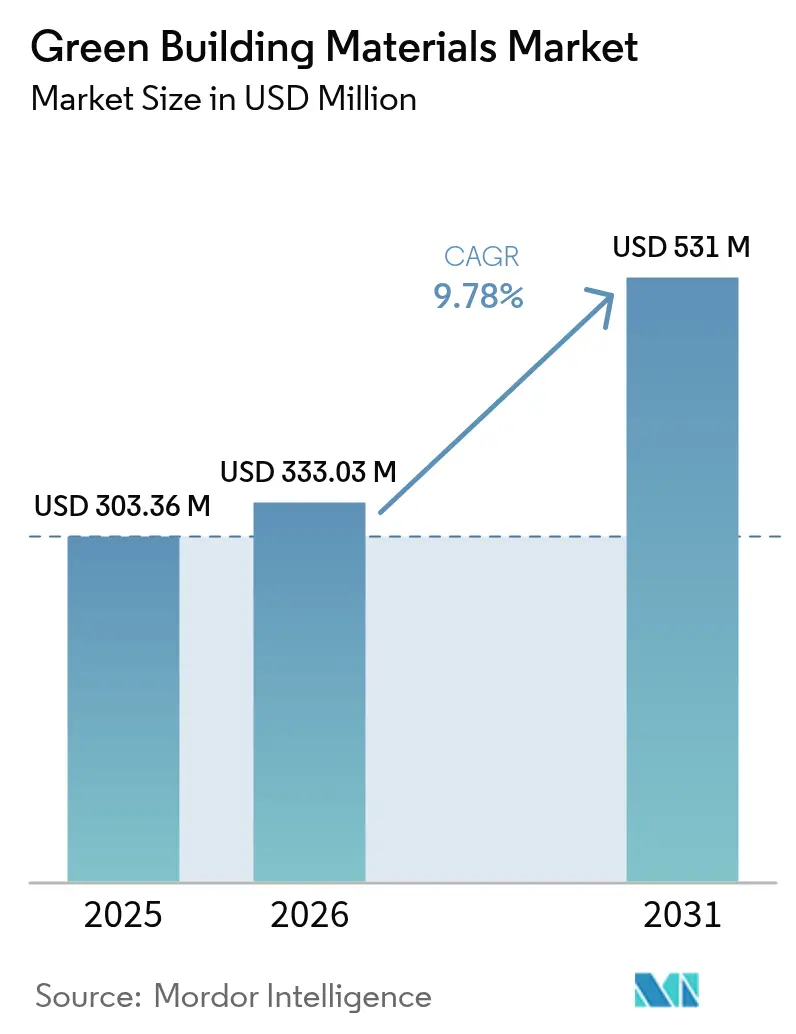

| Market Size (2026) | USD 333.03 Million |

| Market Size (2031) | USD 531 Million |

| Growth Rate (2026 - 2031) | 9.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Green Building Materials Market Analysis by ���ϲ�����

The Green Building Materials Market size is projected to be USD 303.36 million in 2025, USD 333.03 million in 2026, and reach USD 531 million by 2031, growing at a CAGR of 9.78% from 2026 to 2031. As federal procurement rules tighten and European digital-passport mandates emerge, the uptake of verified low-carbon products is accelerating, especially with the advent of corporate net-zero contracts. This expansion broadens the pool of projects specifying these products. In the United States, suppliers boasting environmental product declarations now enjoy preferred access to institutional construction spending. Meanwhile, the Asia-Pacific region, with China and India tying urban-development subsidies to national green-building codes, is poised to become the next growth hub. Material innovation is shifting toward cellulose insulation, calcined-clay cement, and mass-timber framing, driven by code amendments favoring vapor-permeable and bio-based assemblies. However, producers grapple with chief operational risks stemming from feedstock constraints on coal ash and agricultural residue. To navigate these challenges, many are either securing long-term supply contracts or vertically integrating into biomass streams.

Key Report Takeaways

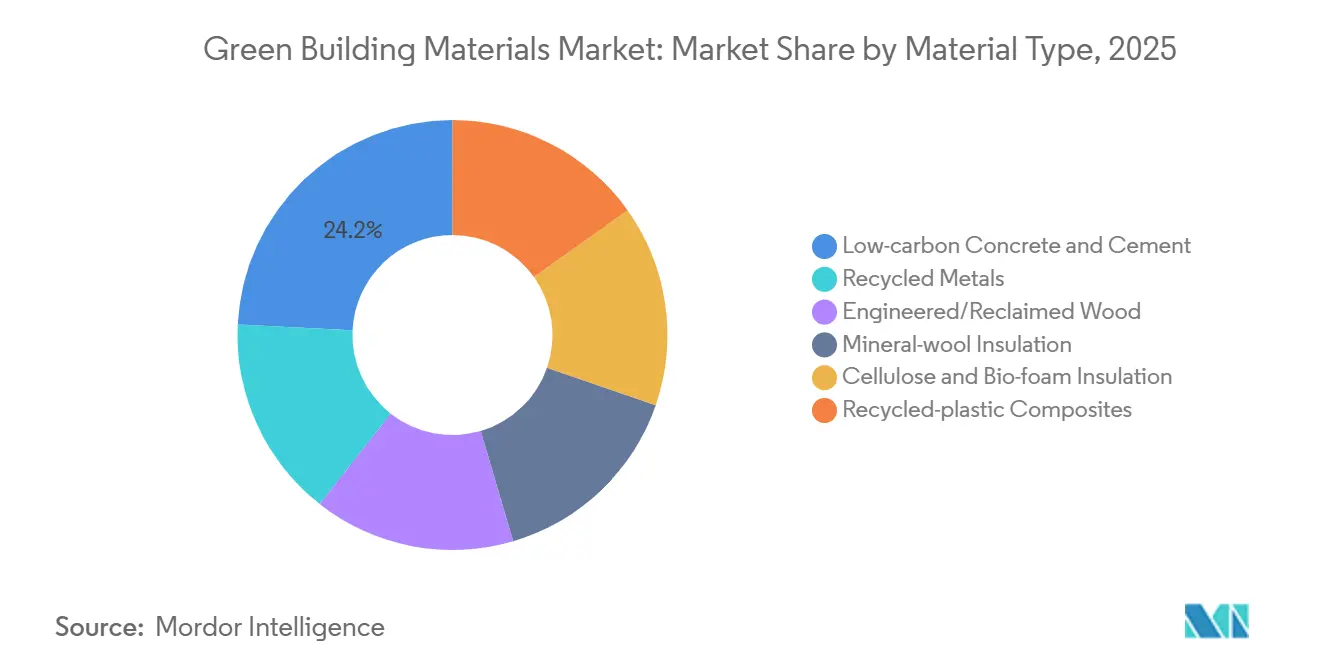

- By material type, low-carbon concrete and cement led with 24.23% revenue share in 2025; cellulose and bio-foam insulation are advancing at a 10.45% CAGR through 2031.

- By application, framing accounted for 23.22% of the Green building materials market share in 2025, while insulation is forecast to expand at a 10.11% CAGR through 2031.

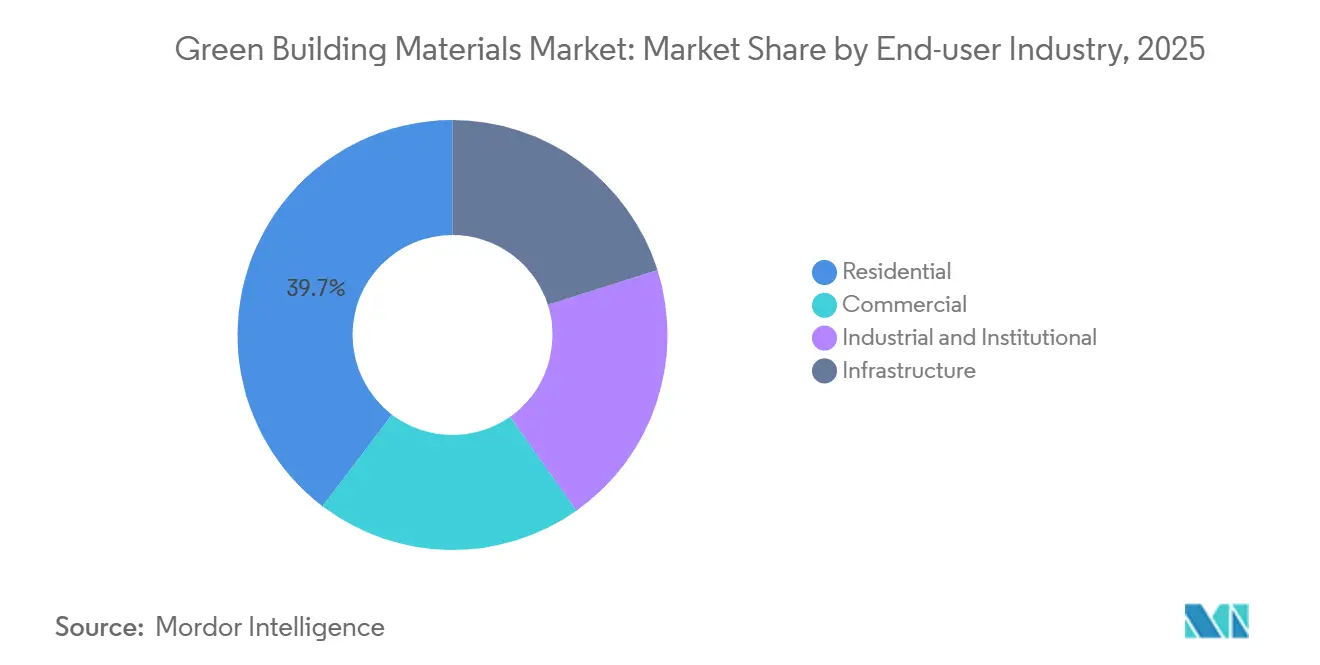

- By end-user, residential construction captured 39.67% of 2025 demand, whereas commercial projects are projected to grow at a 9.88% CAGR to 2031 as tenant specifications penalize high-carbon finishes.

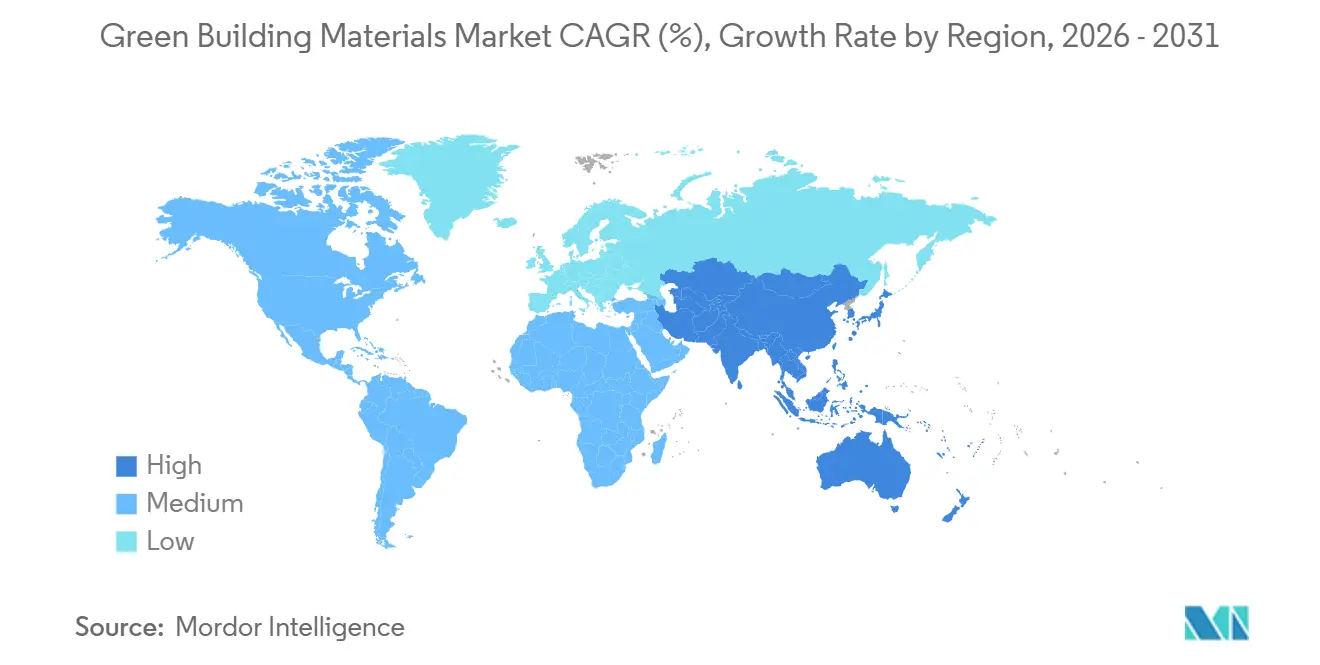

- By geography, North America dominated with 40.67% of 2025 revenue, yet Asia-Pacific is poised to register a 10.99% CAGR through 2031 as China targets 50% certified green urban construction.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Green Building Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives and Certification Schemes | +2.10% | Global, with peak intensity in North America and EU | Medium term (2-4 years) |

| Corporate Net-Zero and Embodied-Carbon Procurement Targets | +1.80% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Retrofit Wave for Ageing Building Stock | +2.30% | EU core, North America urban centers, spill-over to APAC | Long term (≥ 4 years) |

| Digital Material Passports Monetizing End-of-Life Value | +1.40% | EU mandatory, early pilots in Singapore and Canada | Medium term (2-4 years) |

| EU-2028 Mandatory Urban-Mining Quotas for Demolition Waste | +1.20% | EU-27, with demonstration projects in Netherlands and France | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Government Incentives And Certification Schemes

Federal agencies and European regulators are reshaping specifications to prioritize verified low-carbon products. The U.S. General Services Administration is directing substantial funding into low-embodied-carbon materials through 2030, effectively sidelining suppliers lacking environmental product declarations from federal bidding[1]U.S. General Services Administration, “GSA Announces New Actions to Advance Low-Embodied Carbon Construction Materials,” GSA.gov . In the European Union, the updated Energy Performance of Buildings Directive mandates whole-life-carbon assessments in permits by 2028, amplifying the call for transparent supply chains. India's ECBC+ code has integrated embodied carbon into its compliance benchmarks, paving the way for preferential bank financing for certified projects. Collectively, these regulations are bolstering the green building materials market by mitigating the perceived technological risks of emerging materials and establishing a solid demand base.

Corporate Net-Zero And Embodied-Carbon Procurement Targets

Technology and e-commerce giants are embedding carbon intensity caps directly into their contracts. Microsoft, for instance, limits the concrete used in its data centers to a specific carbon intensity. This move pushes ready-mix plants to either adopt mineralization additives or switch to alternative binders. Similarly, Amazon has set the same threshold for its construction pipeline, which encompasses significant annual construction. Moreover, standardized toolkits from the Carbon Leadership Forum are shifting the liability for any overruns onto general contractors. This shift is not just a financial maneuver - it is a strategic push, accelerating the adoption of low-carbon practices across private projects. Collectively, these initiatives are bolstering the Green Building Materials Market by weaving carbon ceilings into mainstream commercial contracts.

Retrofit Wave For Ageing Building Stock

Most emissions in the building sector stem from existing assets. The EU's Renovation Wave initiative, targeting deep retrofits by 2030, is boosting the demand for bio-based insulation and recycled cladding. In the United States, New York City's Local Law 97 and Washington State's performance standards impose escalating fines on buildings that surpass carbon caps, driving upgrades to building envelopes. Furthermore, Section 179D of the United States tax code offers incentives for reducing embodied carbon, which is steering retrofit designs towards the use of salvaged wood and recycled metals. These measures are redirecting the green building materials market's focus towards retrofitting, a domain that has traditionally emphasized operational-energy strategies.

Digital Material Passports Monetizing End-Of-Life Value

Effective January 2026, all construction products sold within the EU must include a QR-coded passport that specifies their composition and recyclability. According to EU pilot projects, verified data allows demolition contractors to resell reclaimed steel, aluminum, and timber at premiums of up to 30%. Similarly, Singapore is testing comparable passports for precast concrete, aiming to reduce landfill disposal by 25% by 2030. By converting waste into a tradable asset, these passports expand the secondary materials pool and strengthen circular revenue streams, thereby driving growth in the green building materials market beyond initial-use sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certification and Performance Complexity Across Regions | -1.30% | Global, with acute friction in cross-border projects spanning EU, North America, and APAC | Short term (≤ 2 years) |

| Bio-Based Feedstock Supply Crunch Post-2027 | -1.70% | North America and EU, with spill-over to APAC bio-insulation markets | Medium term (2-4 years) |

| Scarcity of Low-Carbon SCMs (Fly-Ash/Slag) after Coal Phase-Out | -1.90% | Global, with peak impact in North America and India | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Certification And Performance Complexity Across Regions

Developers working across various jurisdictions frequently face challenges due to the contrasting standards set by LEED, BREEAM, and local regulations. A recent study highlighted that pursuing both LEED and BREEAM certifications simultaneously can significantly prolong the design phase and increase documentation expenses. While LEED v5 emphasizes comprehensive carbon assessments from inception to disposal, BREEAM focuses on energy consumption, requiring concurrent product evaluations. Many smaller suppliers hesitate to invest in the high costs associated with regional compliant product declarations. This hesitation not only limits their export options but also slows the overall growth of the green building materials market.

Bio-Based Feedstock Supply Crunch Post-2027

As agricultural and forestry residues dwindle, products such as cellulose insulation, hemp fiber, and engineered wood are feeling the squeeze. U.S. softwood output has seen a notable decline over the years, with tariffs further complicating imports from Canada. Once a go-to for insulation mills, wheat straw is now being redirected to biofuel refineries, thanks to the Renewable Fuel Standard's absorption rate. In Europe, varying THC limits on hemp cultivation are hampering interstate trade. Without expanding acreage and processing capabilities, growers risk bottlenecks that could stifle the growth of the Green Building Materials Market, particularly its thriving retrofit segments.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Concrete Dominates While Bio-Insulation Surges

Low-carbon concrete and cement commanded 24.23% of 2025 revenue, highlighting the crucial importance of clinker-replacement strategies in the green building materials market. Carbon-mineralization systems, now active in over 2,000 batch plants, are not only reducing embodied carbon per cubic meter but also boosting margins through enhanced compressive strength. The Green building materials market size tied to cellulose and bio-foam insulation is projected to expand at a 10.45% CAGR, the fastest within the mix, after building codes embraced vapor-permeable envelopes that lower mold risk.

Engineered wood, particularly cross-laminated timber, is capitalizing on recent approvals for 18-story constructions and a significant capacity boost in North America. Although recycled metals can be recycled indefinitely, they still account for a notable share of the carbon emissions linked to primary steel production, mainly due to the energy demands of melting furnaces. While mineral-wool insulation faces stiff competition from bio-based alternatives, life-cycle assessments reveal a substantial carbon footprint tied to mineral wool's high-temperature manufacturing process. In 2024, Trex announced a significant revenue increase for its composite decking crafted from recycled plastics, but its broader acceptance in structures is hindered by difficulties in achieving fire-rating standards.

By Application: Retrofit-Driven Insulation Gains Momentum

Insulation is expected to grow at a 10.11% CAGR through 2031, driven by New York City's Local Law 97 and other regulations aimed at limiting operational and embodied emissions. This growth is projected to add billions to the green building materials market, particularly for bio-insulation products. Framing accounted for 23.22% of 2025 revenue in the application mix, supported by the dominance of concrete and steel. However, mass timber is gradually gaining traction, especially in flagship high-rise projects that are altering risk perceptions.

Roofing demand is increasing as California's cool-roof codes align with Toronto's green-roof incentives, promoting reflective and vegetated assemblies. In wildfire-prone areas, exterior siding is shifting towards ignition-resistant composites. Meanwhile, WELL certification is driving interior finishes toward low-VOC and recycled materials. Foundations and pavements, under a USD 1 billion U.S. highway program, are exploring recycled aggregates and geopolymer binders, further expanding the Green building materials market for next-generation concrete.

By End-User Industry: Commercial Contracts Encode Carbon Ceilings

Commercial developments are projected to grow at a CAGR of 9.88% during the forecast period 2026-2031. This growth is primarily driven by Fortune 500 companies embedding carbon caps into tenant-improvement specifications, particularly for data centers that consume significant amounts of concrete annually. In 2025, residential work constituted 39.67% of the demand. However, cost sensitivity and the voluntary nature of code status have slowed the adoption of premium materials. This limitation is particularly evident in the green building materials market for single-family homes.

Industrial and institutional facilities, which often rely on public financing, are increasingly seeking LEED or BREEAM certification. This trend is boosting demand for third-party-verified low-carbon systems. Although infrastructure projects represent a smaller segment, they are experimenting with low-carbon pavements and bridge decks, supported by federal demonstration grants. This experimentation indicates a potential growth avenue for the green building materials market within civil works.

Geography Analysis

North America generated 40.67% of 2025 revenue, supported by the Inflation Reduction Act's expanded tax incentives and the GSA's establishment of a low-carbon procurement floor. In Canada, Infrastructure Canada funding is now tied to embodied-carbon audits, promoting the use of mass timber in schools and transit hubs. Meanwhile, Mexico's nearshoring surge has led U.S. developers to enforce LEED standards on new border logistics hubs, channeling more investments into the green building materials market.

Asia-Pacific is forecast to advance at a 10.99% CAGR during the 2026-2031 period. China’s 14th Five-Year Plan calls for 50% of new urban construction to meet national green standards by 2025[2]China State Council, “14th Five-Year Plan,” gov.cn. In India, the expansion of ECBC+ to encompass embodied carbon is unlocking concessional lending for certified projects, boosting demand even in provinces beyond Tier-1 metros. Japan's commitment is evident as it offers substantial subsidies for low-carbon aggregates until 2030, a move that lured CRH to acquire Eco Material in 2025.

Europe is preparing for growth, with plans for mandatory digital passports in 2026 and an ambitious goal to retrofit millions of buildings by 2030. Germany is taking strides by capping embodied carbon for housing, thereby promoting the use of recycled aggregates. The United Kingdom is pushing for a significant reduction in operational carbon for new homes, targeting a substantial decrease under the 2025 Future Homes Standard. In South America, Brazil stands out with numerous LEED projects gaining traction. However, the regional green building materials market faces challenges due to high import costs for certified materials. Meanwhile, the Middle-East is integrating cool roofs and recycled concrete into its giga-projects, aligning with the ambitious Vision 2030 targets.

Competitive Landscape

The green building materials industry is moderately fragmented, with leading suppliers holding a significant revenue share. This fragmentation is due to varying regional codes and feedstock patterns, limiting widespread dominance. Holcim, for example, gained attention with its acquisition of Xella and a controlling stake in Huaxin Cement. Such acquisitions reflect a growing trend where industry leaders acquire low-carbon capacities to avoid the lengthy process of building new green plants. This strategy strengthens their asset portfolios and ensures compliance with carbon mandates. Similarly, Sika's acquisition of MBCC added carbon-mineralization admixtures to its portfolio, enhancing its competitiveness in data centers and infrastructure projects with strict carbon benchmarks.

Opportunities remain in niches like cellulose insulation and digital passports. Saint-Gobain partnered with TimberHP to secure bio-fiber supplies and address potential feedstock shortages. CRH's acquisition of Eco Material integrated the company into Japan's secondary-aggregate market, driven by passport mandates. CarbonCure has highlighted the profitability of technology royalties, building a network of licensed installations and enabling faster scaling compared to traditional plant ownership.

Patent applications for geopolymer cement have risen, with many recent approvals going to companies in China and India. Emerging players like Plantd and Fiber Global are attracting venture capital for carbon-negative boards and blockchain-based traceability solutions. Competition is intense in the low-carbon concrete segment, where suppliers aim for better carbon metrics and cost-efficient delivery. This rivalry has pressured margins, benefiting firms with quick access to clinker alternatives and valuable mineralization patents.

Green Building Materials Industry Leaders

Kingspan Group

Holcim Ltd

Owens Corning

Saint-Gobain

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Coromandel International Ltd. formed a joint venture through its wholly-owned subsidiary Coromandel Chemicals Limited with Sakarni Plaster to manufacture and market phosphogypsum-based green building materials.

- April 2025: Kingspan Group announced plans to establish a EUR 280 million manufacturing campus in Ukraine for building technology. The facility will create more than 700 jobs and manufacture insulation and green building materials to support reconstruction initiatives.

Global Green Building Materials Market Report Scope

Green building materials are defined as materials that are non-toxic, environment-friendly, and sustainable, leading to improved occupancy health, lowered energy cost, and reduced energy consumption. The operating costs of green buildings are lower than that of regular buildings, with 63% lower water usage and 53% lower electricity usage.

The green building materials market is segmented by material type, application, end-user industry, and geography. By material type, the market is segmented into low-carbon concrete and cement, recycled metals, engineered/reclaimed wood, mineral-wool insulation, cellulose and bio-foam insulation, and recycled-plastic composites. By application, the market is segmented into framing, insulation, roofing, exterior siding, interior finishing, and other applications. By end-user industry, the market is segmented into residential, commercial, industrial and institutional, and infrastructure. The report also covers the market size and forecasts for the green building materials in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Low-carbon Concrete and Cement |

| Recycled Metals |

| Engineered/Reclaimed Wood |

| Mineral-wool Insulation |

| Cellulose and Bio-foam Insulation |

| Recycled-plastic Composites |

| Framing |

| Insulation |

| Roofing |

| Exterior Siding |

| Interior Finishing |

| Other Applications |

| Residential |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Low-carbon Concrete and Cement | |

| Recycled Metals | ||

| Engineered/Reclaimed Wood | ||

| Mineral-wool Insulation | ||

| Cellulose and Bio-foam Insulation | ||

| Recycled-plastic Composites | ||

| By Application | Framing | |

| Insulation | ||

| Roofing | ||

| Exterior Siding | ||

| Interior Finishing | ||

| Other Applications | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial and Institutional | ||

| Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What growth rate is projected for the green building materials market up to 2031?

The green building materials market size stands at USD 333.03 million in 2026, and it is projected to reach USD 531.00 billion by 2031 at a 9.78% CAGR.

Which material holds the largest 2025 share in green construction?

Low-carbon concrete and cement led with a 24.23% revenue share in 2025.

Why is Asia-Pacific considered the fastest-growing region?

China’s mandate for 50% green certification of new urban buildings and India’s embodied-carbon code updates accelerate regional demand, driving a 10.99% CAGR forecast.

What policy in the United States boosts demand for low-carbon materials?

The U.S. General Services Administration committed USD 2.15 billion to procure low-embodied-carbon materials for all large federal projects through 2030.

Which application is set to grow quickest through 2031?

Insulation, driven by retrofit mandates, is projected to rise at a 10.11% CAGR.

Page last updated on: