Weaving Machinery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.86 Billion |

| Market Size (2031) | USD 8.78 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

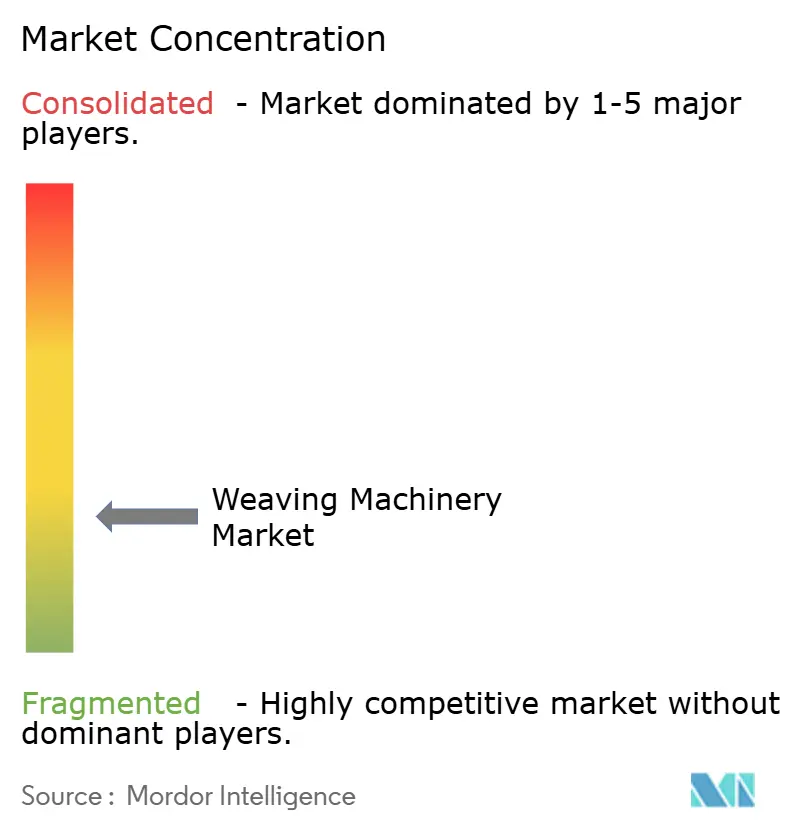

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Weaving Machinery Market Analysis by ���ϲ�����

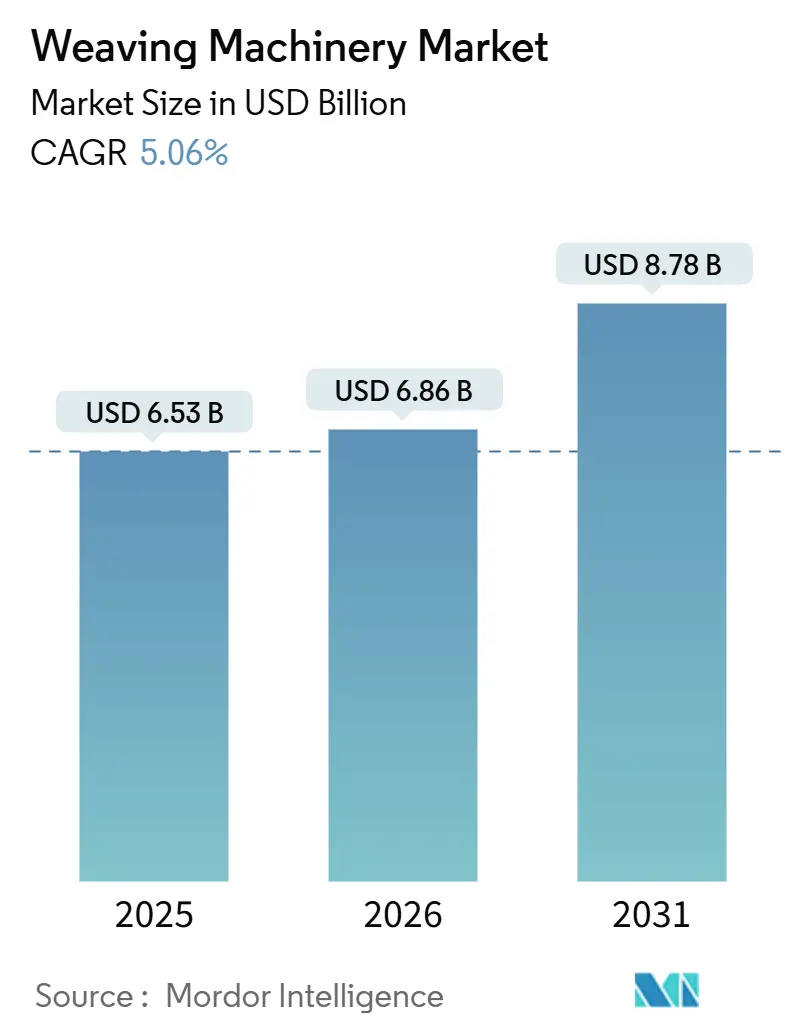

The Weaving Machinery Market size is expected to grow from USD 6.53 billion in 2025 to USD 6.86 billion in 2026 and is forecast to reach USD 8.78 billion by 2031 at 5.06% CAGR over 2026-2031.

This upward curve reflects an accelerating migration from shuttle to high-speed shuttleless looms, wider use of AI-driven predictive-maintenance platforms, and policy-led reshoring programs across the United States and European Union. Growing electric-vehicle production is stimulating demand for battery-separator fabrics and lightweight carbon-fiber preforms, which in turn lifts orders for specialized looms that can handle brittle technical yarns. At the same time, garment exporters in India, Vietnam, and Bangladesh are modernizing capacity under government incentive schemes that lower effective capital cost and reward energy-efficient equipment. Moderate raw-material volatility and tightening credit markets temper momentum but have not derailed long-term investment in advanced weaving assets.

Key Report Takeaways

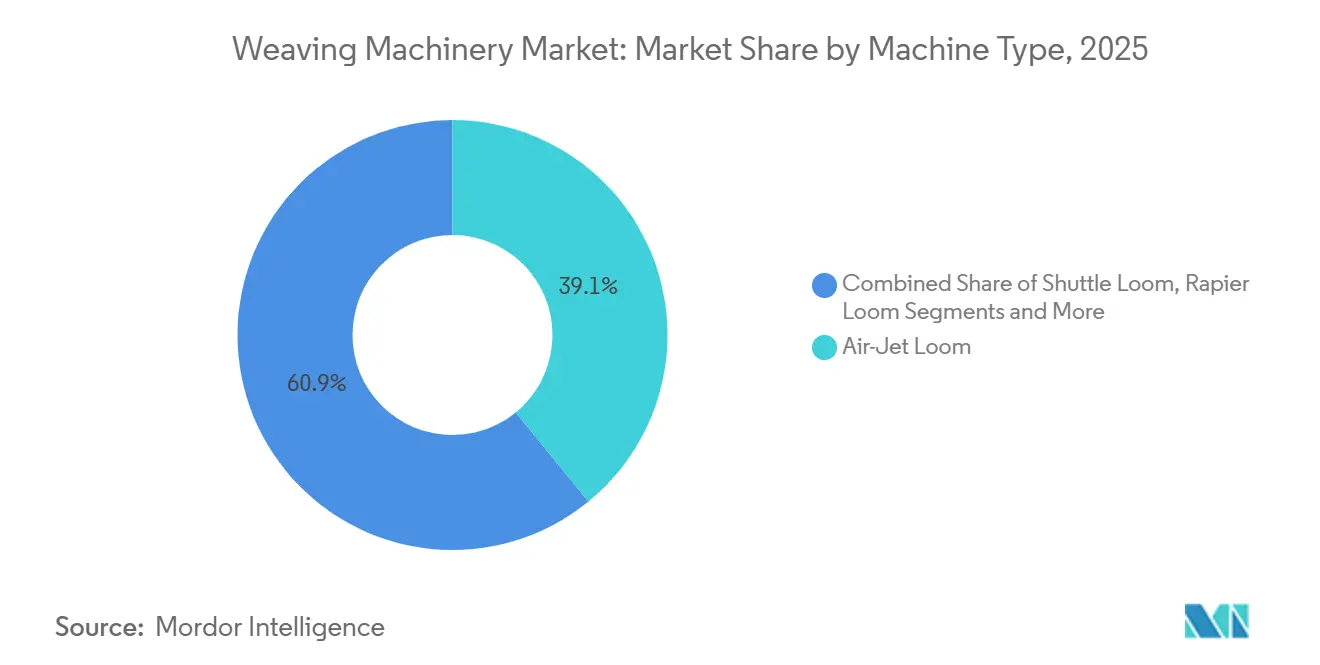

- By machine type, air-jet looms led with 39.11% of the weaving machinery market share in 2025, while water-jet models are forecast to expand at a 6.74% CAGR through 2031.

- By geography, Asia-Pacific captured 52.49% revenue in 2025 and is advancing at a 5.86% CAGR to 2031.

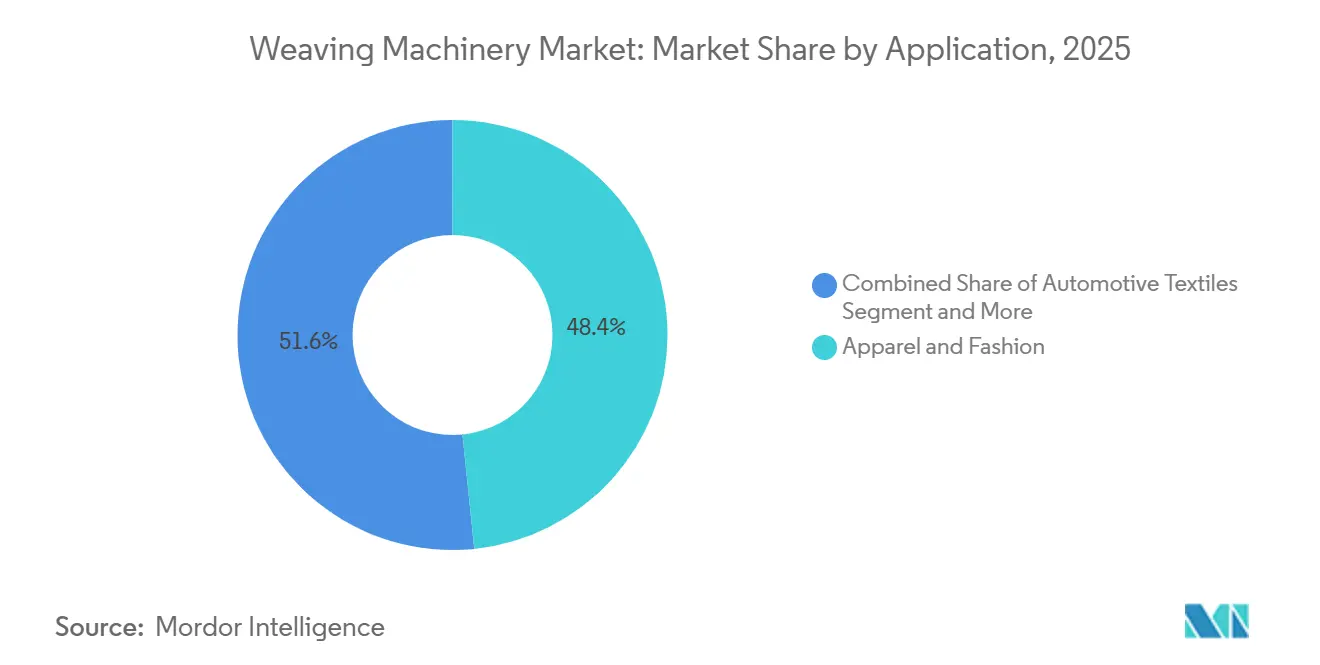

- By application, apparel retained 48.39% of 2025 demand, whereas industrial and technical textiles are climbing at an 8.14% CAGR to 2031.

- By shedding system, cam mechanisms accounted for 43.71% of 2025 sales, yet electronic Jacquard units are projected to rise at a 6.05% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Weaving Machinery Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for advanced technical textiles for EV battery thermal-management and lightweighting | +1.1% | Global, with concentration in North America, EU, and China automotive hubs | Medium to long term (2–4+ years) |

| Expanding apparel consumption across India and ASEAN as middle-class incomes rise | +1.0% | Asia-Pacific core (India, Vietnam, Indonesia, Bangladesh) | Medium to long term (2–4+ years) |

| Accelerated adoption of AI-enabled, Industry 4.0 looms with predictive-maintenance analytics | +0.8% | Global, early adoption in EU, North America, and large Asian mills | Short to medium term (≤ 3 years) |

| Reshoring of textile production to the US and EU, supported by IRA tax credits and EU CBAM incentives | +0.7% | North America and EU, with spill-over to Mexico and Eastern Europe | Medium term (2–4 years) |

| Loom retrofits to handle colored post-consumer recycled fibers ahead of mandatory 2030 targets | +0.6% | EU primarily, with global spill-over as brands adopt circular sourcing | Medium to long term (2–4+ years) |

| Rapid uptake of 3D woven carbon-fiber preforms for hypersonic and aerospace platforms | +0.5% | North America and EU, with emerging demand in the Asia-Pacific defense sectors | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Surging Demand for Advanced Technical Textiles for EV Battery Thermal-Management and Lightweighting

Electric-vehicle platforms require woven separators, thermal shields, and carbon-fiber reinforcements that tolerate high temperatures and deliver weight savings. Hexcel’s HiTape unidirectional carbon fabrics enable automated dry-preform lay-up with 58-60% fiber volume content suitable for aerospace and now automotive battery casings. Research at TU Dresden’s Institute of Textile Machinery using a Dornier P1 rapier loom produced multilayer carbon fabrics up to 4,500 g/m², underscoring the need for looms with precise tension control. Demand for such machinery is translating into premium margins for suppliers capable of handling brittle filaments without breakage. Loom builders are integrating modular shedding and adaptive warp-let off systems to serve this niche. The steady rise in EV penetration thus feeds directly into the global weaving machinery market.

Expanding Apparel Consumption Across India and ASEAN as Middle-Class Incomes Rise

India’s textile sector reached USD 194 billion in fiscal 2025-26, helped by Production Linked Incentive subsidies covering up to 10% of weaving-machinery capex. Vietnam exported USD 44-48.8 billion worth of garments in 2025, with the weaving subsector growth averaging 6.1%, but soaring electricity costs now 8-14% of the conversion cost are steering mills toward energy-efficient looms.[1]Asian Productivity Organization, “Energy Efficiency in Vietnam’s Textile Sector,” apo-tokyo.orgASEAN as a bloc shipped USD 34.9 billion in textiles during 2025, and buyers on the Source ASEAN platform now demand compliance-ready, digitally connected machinery. Rising disposable incomes, therefore, sustain fabric demand and loom installations across the region, bolstering the weaving machinery market.

Accelerated Adoption of AI-Enabled Industry 4.0 Looms with Predictive-Maintenance Analytics

Textile mills are shifting from break-fix maintenance to sensor-driven predict-and-prevent models. A peer-reviewed study at Crescent Textile Mills recorded a 26.7% jump in daily output and a 37.5% cut in downtime after deploying machine-learning algorithms on Picanol OmniPlus-i looms. Picanol’s PicConnect suite, launched at ITMA Asia 2025, centralizes tooling, diagnostics, and energy dashboards, while its EcoBoost module trims power use by up to 1.5 kW per loom. Comparable cloud platforms retrofitted to legacy lines in Asia have achieved mean absolute errors below 0.14 on key quality parameters, proving viability without full capital replacement. These productivity gains and cost savings are propelling AI adoption throughout the weaving machinery market.

Reshoring of Textile Production to US and EU, Supported by IRA Tax Credits and EU CBAM Incentives

Washington’s Americas Act earmarks USD 75 million a year for five years to support domestic and near-shore textile capacity, supplemented by USD 3 billion in grants and USD 10 billion in loans for circularity projects.[2]CFDA, “Americas Act and FABRIC Act Legislative Summaries,” cfda.com In Europe, the Carbon Border Adjustment Mechanism and revised Waste Framework Directive make local sourcing more attractive by internalizing the environmental costs of imports. Itema’s February 2026 purchase of Palmetto Loom Reed reflects a strategy to supply looms closer to rising U.S. demand. Such policy shifts are nudging orders back toward domestic vendors, providing a tangible uplift to the weaving machinery market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising capex requirements for high-speed rapier and air-jet looms amid tighter global credit markets | -0.6% | Global, acute in emerging markets and SME-dominated clusters | Short to medium term (≤ 3 years) |

| Persistent volatility in polyester and polypropylene filament prices driven by petro-feedstock shifts | -0.4% | Global, with the highest exposure in the Asia-Pacific polyester hubs | Short term (≤ 2 years) |

| Chronic water-stress regulations curbing new water-jet loom installations in North India and China | -0.4% | Asia primarily (North India, China), with regulatory spill-over to Southeast Asia | Medium term (2–4 years) |

| Cybersecurity and IP-theft risks associated with cloud-connected, AI-driven quality-control cameras | -0.3% | Global, with heightened concern in North America, the EU, and China | Short to medium term (≤ 3 years) |

| Source: ���ϲ����� | |||

Rising Capex Requirements for High-Speed Rapier and Air-Jet Looms Amid Tighter Global Credit Markets

Advanced shuttleless looms can cost several hundred thousand U.S. dollars, a burden for small and medium-sized mills that dominate South Asian clusters. India’s Bank of Baroda now requires a 25% equity margin on new machinery loans, pushing some applicants to defer upgrades.[3]Bank of Baroda, “Financing Scheme for Textile Units,” bankofbaroda.in In the United Kingdom, Sellers Textile Engineers needed a USD 1.25 million facility backed by an 80% government guarantee to finance carpet-finishing equipment. With global interest rates elevated, similar stories are unfolding in Turkey and Indonesia. The squeeze limits near-term replacement cycles and clips potential expansion of the weaving machinery market.

Persistent Volatility in Polyester and Polypropylene Filament Prices Driven by Petro-Feedstock Shifts

Crude oil swings flow directly into PTA, MEG, and propylene costs, destabilizing synthetic yarn pricing and mill margins. CCFGroup reported Chinese polyester capacity rising from 86.34 million t/y in January 2025 to 90.74 million t/y by December, yet downstream demand lagged, compressing processing spreads. Turkey’s textile sector lost 380,000 jobs over three years as inflation and raw-material spikes drove 4,500 plant closures by 2025. Mills, faced with volatile input costs, often postpone capex, dulling the immediate growth outlook for the weaving machinery market.

Segment Analysis

By Machine Type: Water-Jet Looms Gain Share in Synthetic-Fiber Hubs

Air-Jet Loom units held 39.11% of the weaving machinery market size in 2025, reflecting their dominance in high-volume polyester and nylon apparel output. Air-jet models remain premium, yet water-jet demand is forecast to outpace at a 6.74% CAGR between 2026 and 2031 as Chinese and Indian mills retrofit lines to meet strict water-reuse mandates. A national study across 343 Chinese prefectures identified textile finishing as one of the heaviest industrial water consumers and highlighted 18.9 km³ of potential savings if recirculation technologies are fully adopted. Complying factories increasingly pair closed-loop dyeing with modern water-jet looms that curb consumption and ease effluent treatment costs, underscoring sustainability’s role in shaping the weaving machinery market.

Rapier machines keep a firm foothold in heavy-duty fabrics and complex color patterns. Picanol’s Ultimax rapier, installed at Auro Textiles in March 2024, clocks over 800 wefts/min and integrates sensors for predictive diagnostics. Shuttle machines survive in artisanal niches, whereas projectile and circular looms serve wide-width and seamless tubes. India’s Technology Upgradation Fund Scheme offsets 10% of weaving-machinery spend, trimming payback periods. These varied performance and cost profiles collectively broaden the customer base, enlarging the global weaving machinery market.

Note: Segment shares of all individual segments available upon report purchase

By Shedding/Patterning: Jacquard’s Digital Leap Drives Premium Segment

Cam shedding systems captured 43.71% of 2025 revenue, owing to their cost edge in plain-weave and staple home-textile runs. Nonetheless, electronic Jacquard units are set to expand at a 6.05% CAGR through 2031, energizing the weaving machinery market. Picanol’s Supermax rapier configured with a 12-harness Jacquard for saree production exemplifies the flexibility demanded by fashion brands racing from concept to shelf. Dornier’s P2 platform, praised for modularity, lets mills upgrade shedding modules without scrapping frames, lengthening asset life.

Regulation is another catalyst. The EU’s Ecodesign rule will require Digital Product Passports by 2030, prompting mills to weave RFID-compatible patterns directly into cloth for traceability.[4]European Commission, “Ecodesign for Sustainable Products Regulation,” europa.eu The Netherlands now targets 50% sustainable material use by 2030, pushing designers toward recycled fibers that perform unpredictably on rigid cams. Electronic Jacquards can vary the shed geometry on the fly, mitigating yarn breakage and enhancing circularity compliance. Cost-sensitive mills may still opt for dobby or cam systems, but premium demand is steering growth within the weaving machinery market toward digitized Jacquard.

By Application: Industrial and Technical Textiles Outpace Apparel

Apparel commanded 48.39% of 2025 revenue, yet industrial and technical textiles are projected to climb at an 8.14% CAGR from 2026 to 2031, making them the fastest mover inside the weaving machinery market size. Aerospace OEMs increasingly substitute aluminum with woven carbon preforms; Hexcel’s HiTape delivers comparable compression-after-impact properties while slashing cure times. Automotive plants adopt similar fabrics for battery housings and body panels, while water-purification firms require precision filtration cloths now regulated under tightening quality codes in Europe and China.

To serve these customers, loom builders add open-reed units, multiple warp let-offs, and climate-controlled enclosures. TU Dresden’s carbon-fabric trials prove multilayer constructs up to 4,500 g/m² are feasible at production scale. Tsudakoma’s ZAX001neo Plus, launched under its 2024-26 plan, blends air-jet speed with gentle yarn handling, targeting synthetic composites for aircraft tanks. As regulators push Extended Producer Responsibility and microplastic limits, mills pivot toward on-demand, high-value technical runs, fuelling a structural mix shift in the weaving machinery market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific retained 52.49% revenue in 2025, and its weaving machinery market is forecast to grow at a 5.86% CAGR through 2031. Vietnam alone exported up to USD 48.8 billion of apparel in 2025, but its energy bill doubled over 2016-2020, prompting mills to install energy-efficient looms and rooftop solar arrays to curb electricity that now averages 8-14% of cost. India’s USD 194 billion textile universe enjoys 10% capital subsidies that lower effective loom pricing, while 73 PLI-approved firms prepare for man-made-fiber expansion. Bangladesh secured more than USD 150 million in fresh Chinese investment for composite yarn and garment lines, reinforcing its buyer appeal.

North America and Europe are experiencing a policy-led resurgence. The United States channels USD 75 million annually into reshoring grants and extends 15% credits for circular-textile projects, leading Itema to buy Palmetto Loom Reed in February 2026. Brussels, meanwhile, enforces Extended Producer Responsibility and prepares a Carbon Border Adjustment that internalizes the emissions cost of imports, nudging manufacturers to relocate near EU customers. Studies show an intra-EU supply shift could trim carbon footprints by up to 4.4 million t for electric-motor-related textiles.

Elsewhere, Turkey’s weaving capacity contracted after 4,500 factory closures in 2025 and a 5.1% drop in EU orders, illustrating how macro volatility can erode regional share. Latin America, the Middle East, and Africa hold smaller bases but leverage cotton output and trade agreements to lure investment; Brazil and Egypt supply long-staple cotton, while Ethiopia markets low-cost labor within duty-free access to the EU and U.S. These dynamics collectively reinforce the primacy of Asia-Pacific while spreading pockets of growth across the global weaving machinery market.

Competitive Landscape

Competition in the weaving machinery market is moderate. European and Japanese OEMs such as Picanol, Itema, Dornier, Toyota Industries, Tsudakoma, Stäubli, and Van de Wiele continue to dominate premium rapier, air-jet, and Jacquard niches by bundling high-speed hardware with digital ecosystems. Picanol surpassed the 400,000-unit mark in 2025 and now supplies roughly 2,600 mills worldwide, leveraging its EcoBoost energy module to cut per-loom consumption by up to 1.5 kW. Dornier complements hardware with myDoX, an online parts and service portal that shortens downtime and enables data benchmarking across plants.

Chinese makers such as Jingwei, Erfangji, and Zhejiang Tongda fill price-sensitive slots, especially shuttle and entry-level shuttleless machines in South and Southeast Asia. Aggressive local after-sales teams and government-supported financing anchor their competitiveness. Yet, to win premium orders, they increasingly add edge-AI modules and compliance features. Retrofit specialists are emerging too, offering sensor kits that bring predictive maintenance to legacy fleets, slicing life-cycle cost for SME mills, and broadening the customer base of the weaving machinery market.

Strategic M&A is reshaping supply chains. Itema’s February 2026 acquisition of Palmetto Loom Reed establishes a U.S. production outpost, mirroring reshoring incentives under the Americas Act. Toyota Industries, despite lowered FY 2026 profit guidance due to engine-certification settlements, retains heft through cross-segment synergies and a USD 26.7 billion revenue scale. Overall, the top five players account for roughly 60-65% of premium shuttleless sales, placing the market concentration score at 6.

Weaving Machinery Industry Leaders

Picanol

Itema S.p.A.

Toyota Industries

Dornier GmbH

Tsudakoma Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Itema America acquired Palmetto Loom Reed to boost U.S. manufacturing and service, aligning with USD 75 million in annual reshoring grants.

- February 2026: Tianford Bangladesh Textile invested USD 19.59 million to build a 7 million-piece garment plant in Uttara EPZ, employing 3,254 staff.

- October 2025: Picanol launched the OmniPlus-i Connect air-jet loom featuring EcoBoost, AirStream, and PicConnect at ITMA Asia + CITME.

- October 2025: The EU’s revised Waste Framework Directive took effect, mandating Extended Producer Responsibility for textiles.

Global Weaving Machinery Market Report Scope

Weaving machine is a device mainly used for weaving fabrics and tapestry. The basic function of a weaving machine is for holding the warp threads under tension for enabling the interweaving of weft threads. Weaving machine can be used for various types of weaves such as plain Weave, satin weave, twill weave, etc. The Global Spinning Machinery market is segmented by Machine Type (Shuttle Weaving Machine, Circular Weaving Machine, Others), by Weaving Type (Plain Weave, Satin Weaving, Twill Weaving, Others), by Application (Clothing, Upholstery Fabric, Automotive Textiles, Sportswear, Others) and by Geography (North America (United States, Mexico and Canada), Asia-Pacific (China, Japan, India, Bangladesh, Turkey, South Korea, Australia, Indonesia and Rest of Asia), Europe (Germany, France, United Kingdom, Italy, Spain, Russia and Rest of Europe), Middle East & Africa (Egypt, South Africa, Saudi Arabia and Rest of Middle East & Africa) and South America (Brazil, Argentina, Rest of South America)). The report offers market size and forecasts for Global Spinning Machinery market in value (USD billion) for all above segments.

| Shuttle Loom |

| Rapier Loom |

| Air-Jet Loom |

| Water-Jet Loom |

| Projectile Loom |

| Others (Circular Loom, Narrow-fabric looms, Auxiliaries) |

| Cam (tappet) |

| Dobby (mechanical, electronic) |

| Jacquard (electronic; stitch density/number of hooks) |

| Apparel & Fashion |

| Home Textiles & Upholstery |

| Automotive Textiles |

| Industrial, Technical & Filtration Textiles |

| Others (labesl, tapes, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Machine Type | Shuttle Loom | |

| Rapier Loom | ||

| Air-Jet Loom | ||

| Water-Jet Loom | ||

| Projectile Loom | ||

| Others (Circular Loom, Narrow-fabric looms, Auxiliaries) | ||

| By Shedding / Patterning | Cam (tappet) | |

| Dobby (mechanical, electronic) | ||

| Jacquard (electronic; stitch density/number of hooks) | ||

| By Application | Apparel & Fashion | |

| Home Textiles & Upholstery | ||

| Automotive Textiles | ||

| Industrial, Technical & Filtration Textiles | ||

| Others (labesl, tapes, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is global demand for shuttleless looms growing?

Shuttleless equipment sales in the weaving machinery market are increasing at a 5.06% CAGR between 2026 and 2031, fueled by higher speed, lower energy use, and rising technical-textile demand.

Which region leads loom installations today?

Asia-Pacific holds 52.49% of 2025 revenue and remains the fastest-growing geography at a 5.86% CAGR through 2031, driven by Vietnam, India, and Bangladesh.

What segment is expanding the quickest by application?

Industrial and technical fabrics are projected to climb at an 8.14% CAGR to 2031 as EV, aerospace, and filtration sectors scale up.

How will new EU regulations affect loom purchasing?

Mandatory Extended Producer Responsibility and Digital Product Passports push mills toward looms that can weave recycled fibers and embed traceability, encouraging investment in electronic Jacquard and AI-enabled models.

Are financing constraints slowing modernization?

Yes, high-speed rapier and air-jet looms require sizeable capex, and tighter credit markets add a -0.6% drag on the weaving machinery market CAGR, especially in SME-heavy clusters.

Which companies dominate the high-end segment?

Picanol, Itema, Dornier, Toyota Industries, and Tsudakoma collectively control roughly 60-65% of premium shuttleless sales, reflecting a market concentration score of 6.

Page last updated on: