Market Overview

| Study Period | 2021 - 2031 |

|---|---|

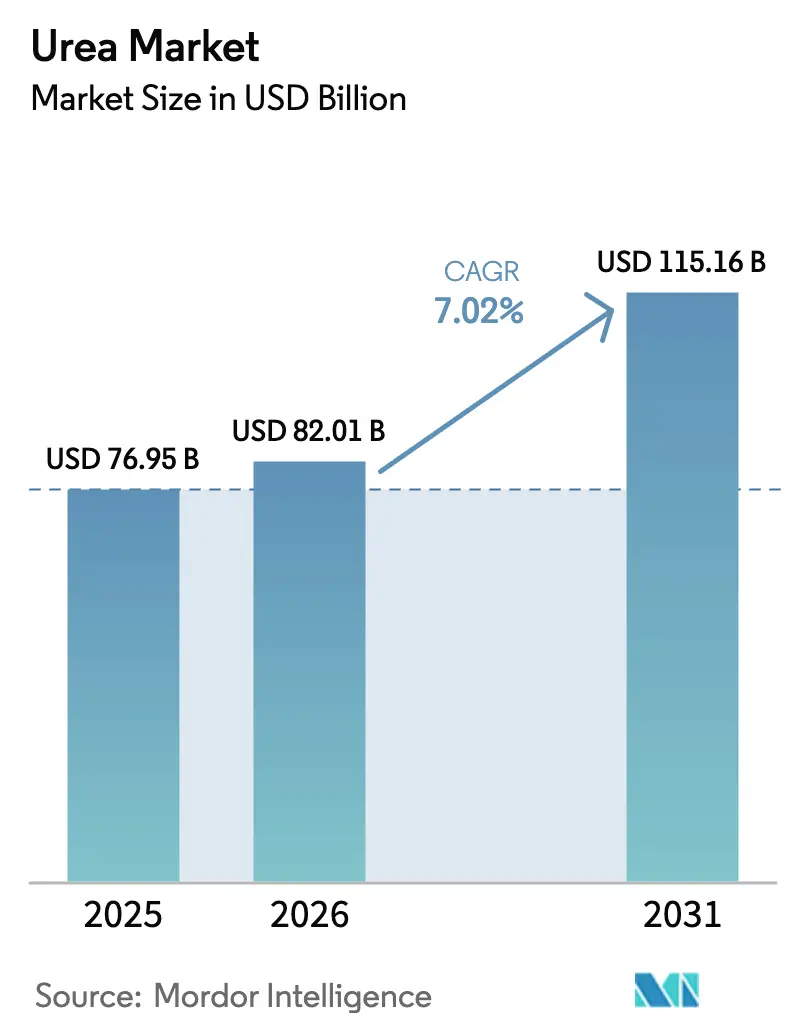

| Market Size (2026) | USD 82.01 Billion |

| Market Size (2031) | USD 115.16 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Urea Market Analysis by ���ϲ�����

The urea market size was valued at USD 76.95 billion in 2025 and estimated to grow from USD 82.01 billion in 2026 to reach USD 115.16 billion by 2031, at a CAGR of 7.02% during the forecast period (2026-2031). Demand is rising as population growth lifts cereal consumption, particularly in South Asia and Sub-Saharan Africa, where irrigation projects are widening nutrient application gaps. Low-cost natural gas in the Middle East and North America keeps production economics favorable compared with competing nitrogen sources, sustaining the price advantage that anchors global trade flows. Green ammonia projects that feed directly into urea synthesis are scaling up, positioning low-carbon product lines to secure premiums under emerging carbon-border rules in the European Union and North America. Import-focused regions are adopting port-side modular plants that convert shipped ammonia into urea near the point of use, cutting inland freight costs and improving supply flexibility. Precision-farming tools in developed economies are boosting granular urea demand because uniform particles improve variable-rate placement accuracy, a trend that commands premium margins in North America and Western Europe.

Key Report Takeaways

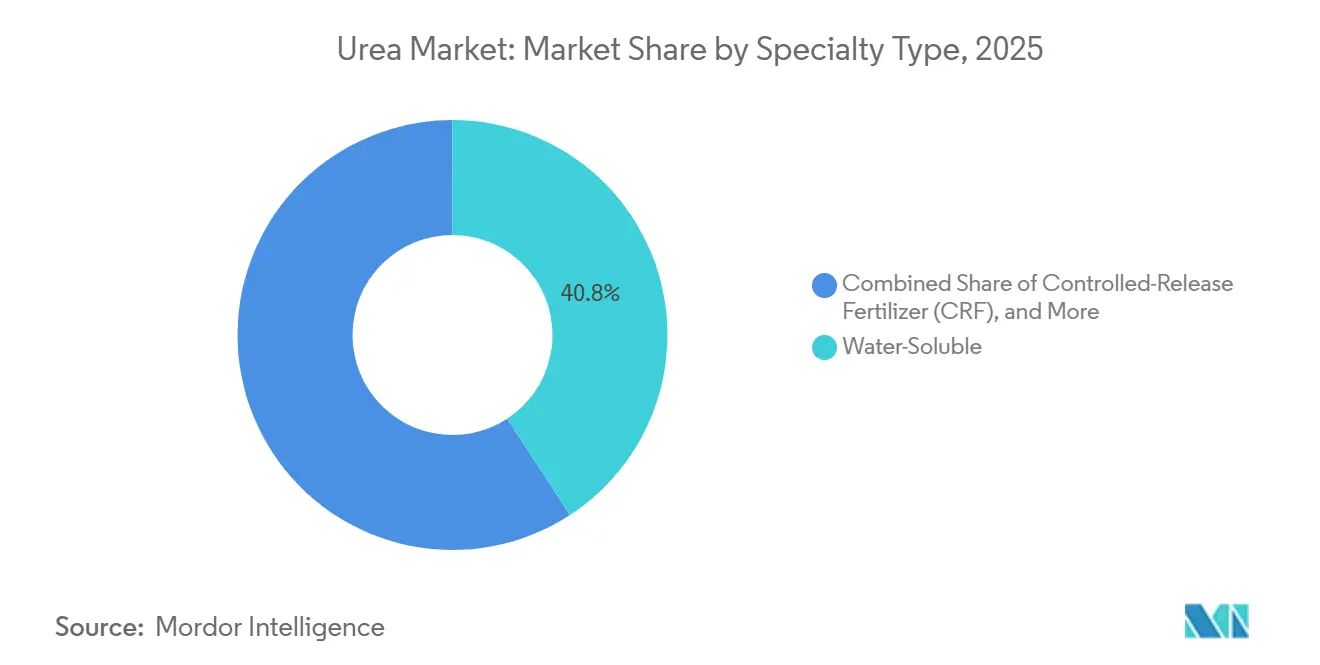

- By specialty type, water-soluble products led with 40.8% of the urea market share in 2025, while controlled-release fertilizers are advancing at a 7.6% CAGR through 2031.

- By form, conventional material accounted for 93.2% of the urea market size in 2025, whereas the specialty segment is projected to grow at a 7.0% CAGR over 2026-2031.

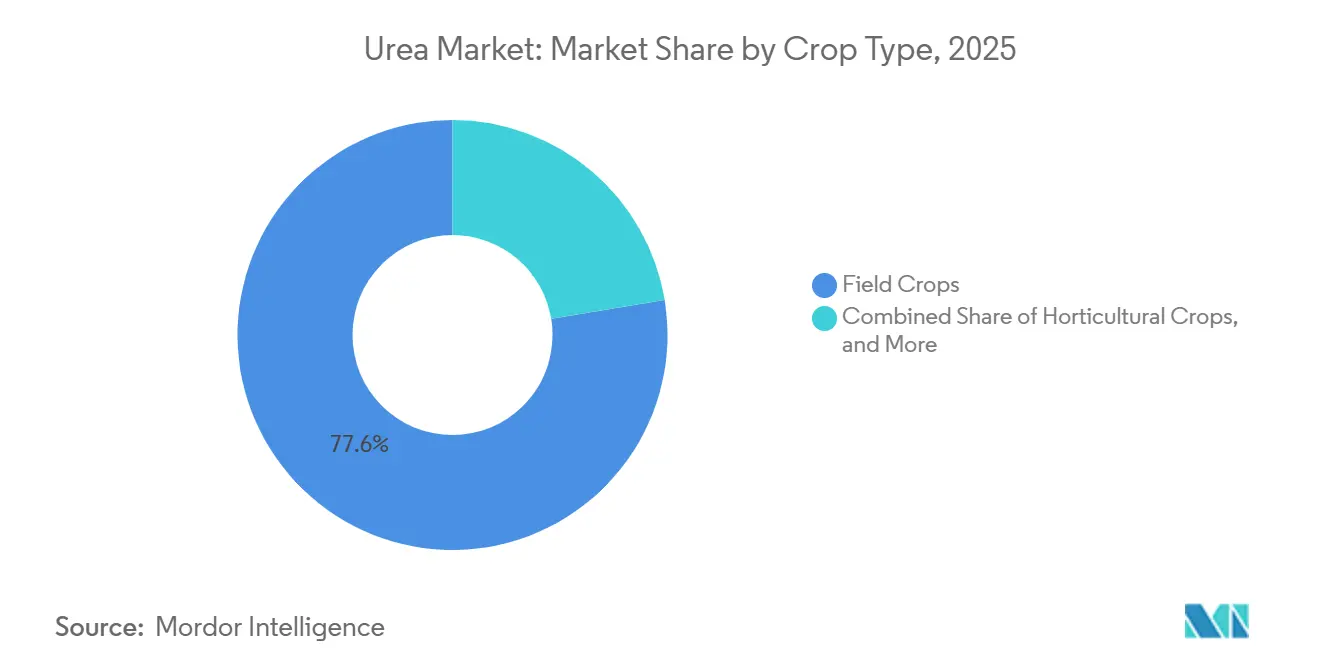

- By crop type, field crops accounted for 77.6% of 2025 revenue, yet horticultural crops are forecast to post an 8.9% CAGR through 2031.

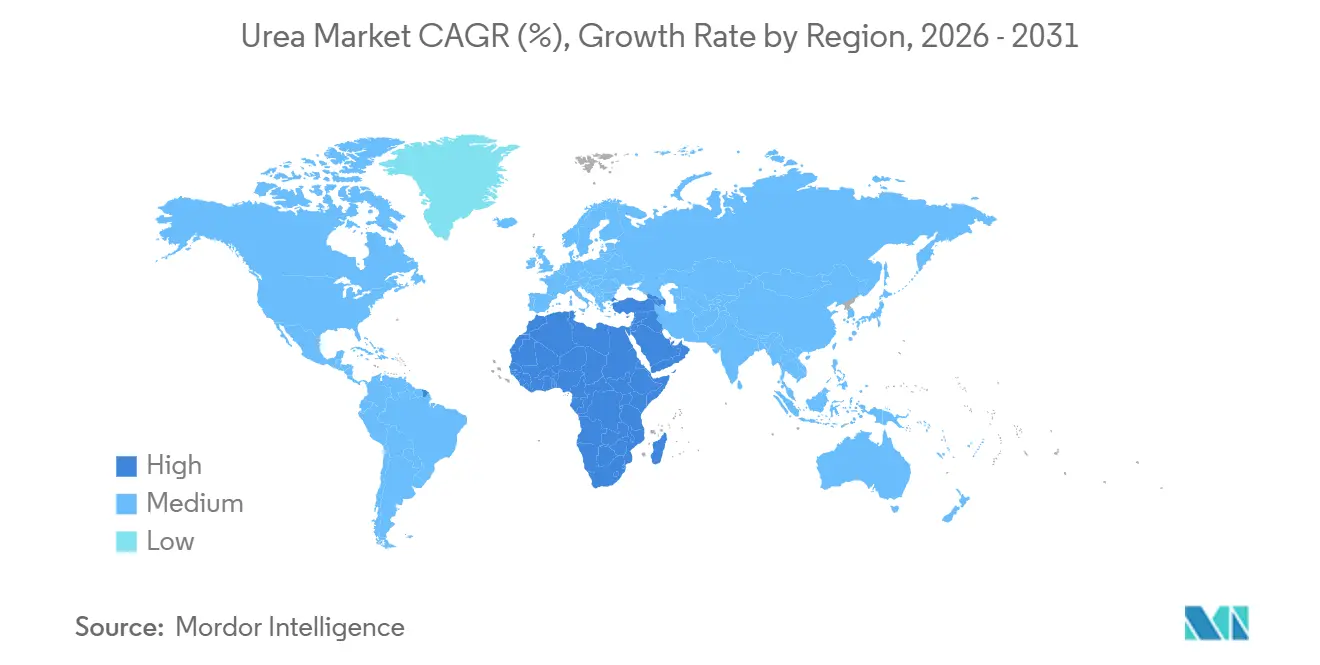

- By geography, Asia-Pacific held 45.1% of global value in 2025, and Africa is projected to expand at a 9.5% CAGR, the fastest among all regions.

- Market concentration remains low, with the top five suppliers, Yara International ASA, CF Industries Holdings, Inc., OCI N.V., SABIC Agri-Nutrients Company, and Nutrien Ltd., holding a limited share of the market.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Urea Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying cereal crop cultivation | +1.4% | Asia-Pacific core, Sub-Saharan Africa, and South America | Medium term (2-4 years) |

| Cost advantage of urea versus other nitrogen fertilizers | +1.3% | Global with strongest effect in South Asia and Middle East | Short term (≤2 years) |

| Fertilizer demand growth from population and dietary shifts | +1.0% | Global concentrated in Africa and South Asia | Long term (≥4 years) |

| Granular urea adoption in precision farming | +0.7% | North America, Western Europe, and Australia | Medium term (2-4 years) |

| Renewable-hydrogen-based green urea capacity additions | +0.6% | Europe and Middle East with pilot projects in Asia-Pacific | Long term (≥4 years) |

| Port-side modular urea plants lowering logistics costs | +0.4% | Import-dependent regions including Africa, Southeast Asia, and South America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Understand The Key Trends Shaping This Market

Download Sample Report

Intensifying Cereal Crop Cultivation

Global wheat, rice, and maize area climbed to 718 million hectares in 2025, up 2.1% from 2024, with South Asia and Sub-Saharan Africa accounting for the majority of the new hectares[1]Source: Food and Agriculture Organization, “World Food and Agriculture Statistical Yearbook 2025,” FAO, fao.org. Irrigation programs in India added 3.2 million hectares in 2025, raising average nitrogen application from 110 to 135 kilograms per hectare in newly irrigated districts. China’s pivot to high-protein wheat lifted urea use by 1.4 million metric tons on the North China Plain in the 2025 winter season. Urea’s 46% nitrogen content remains cheaper per nutrient unit than ammonium sulfate in these regions, reinforcing volume growth. Should irrigation funding falter, demand could retreat quickly, so policy monitoring is essential for distributors.

Cost Advantage of Urea Versus Other Nitrogen Fertilizers

In 2025, natural gas prices for producers in the Middle East and North America remained below USD 4 per million British thermal units, while European contracts averaged USD 11, significantly widening the delivered-cost gap. This disparity in natural gas prices has had a notable impact on production costs and regional competitiveness. Gulf exporters shipped prilled material at USD 280 per metric ton free on board, which was USD 90 lower than European ammonium nitrate on an equal-nitrogen basis, highlighting the cost advantage for Gulf producers[2]Source: World Bank, “Commodity Markets Outlook 2025,” World Bank, worldbank.org. In the United States, CF Industries Holdings, Inc. reduced cash costs at its Donaldsonville facility following catalyst optimization in 2025, showcasing the benefits of operational efficiency improvements. A sustained increase in gas prices could compress margins, potentially leading to reduced application rates and impacting overall market dynamics. Currently, the price spread continues to favor urea imports, even as landed prices remain competitive, further influencing global trade flows and purchasing decisions.

Granular Urea Adoption in Precision Farming

In 2025, variable-rate technology was used on 68% of Midwestern corn and soybean acres, up from 54% two years prior[3]Source: United States Department of Agriculture, “Precision Agriculture and Nitrogen Management 2025,” USDA, usda.gov. This growth highlights the growing adoption of precision agriculture practices to optimize input use and improve yields. Granular urea accounted for the majority of solid nitrogen sales within these systems, as its free-flowing particles prevent segregation in pneumatic applicators, ensuring uniform application. Field trials conducted by Deere & Company demonstrated that its ExactApply sprayer reduced waste when used with granular grades, showcasing the potential for cost savings and environmental benefits. Although the product is priced premium, it enhances placement accuracy across application zones ranging from 80 to 180 kilograms per hectare, contributing to better crop performance. While premium adoption remains limited in price-sensitive regions, facilities with granulation capacity achieve higher margins in North America and Western Europe, driven by the demand for advanced agricultural inputs.

Renewable-Hydrogen-Based Green Urea Capacity Additions

Green ammonia capacity reached 4.1 million metric tons in 2025, and projects totaling 6.8 million metric tons are scheduled before 2028[4]Source: International Renewable Energy Agency, “Green Hydrogen and Ammonia Production 2025,” IRENA, irena.org . Yara International ASA’s 75,000 metric tons facility in Norway achieved the first commercial batch of carbon-neutral urea under European Union certification in early 2025. OCI N.V. is investing USD 500 million in Texas to produce 1.1 million metric tons of green ammonia by 2027, with 60% earmarked for urea, targeting a USD 40 to USD 60 premium from California and European buyers. These initiatives gain ground as carbon border fees loom, though subsidy shifts remain a threat. Nonetheless, low-carbon supply is set to reshape procurement strategies in regulated markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural gas price volatility raising production costs | -1.2% | Global with greatest stress in Europe and import-dependent Asia | Short term (≤2 years) |

| Tightening runoff and greenhouse gas regulations on nitrogen use | -0.9% | North America and European Union with new rules emerging in Australia | Medium term (2-4 years) |

| Substitution threat from ammonium nitrate and nitrogenous fertilizers | -0.7% | Europe, North America, and selected South American markets | Medium term (2-4 years) |

| Geopolitical trade-route disruptions | -0.6% | Global with sharp impacts in Africa, South America, and Southeast Asia | Short term (≤2 years) |

| Source: ���ϲ����� | |||

Natural Gas Price Volatility Raising Production Costs

Natural gas accounts for a significant share of urea cash costs in gas-intensive regions. European facilities ceased production in early 2025 due to high hub prices, underscoring the impact of energy costs on production economics. In the United States, Henry Hub averages are forecast at USD 3.80 per million British thermal units in 2026, with potential fluctuations that could result in a 160% spread, complicating budget planning and introducing significant uncertainty for producers. According to CF Industries Holdings, Inc., an increase in natural gas prices adds to its cost curve, underscoring the critical impact of energy prices on profitability. As a result, margin visibility depends on fuel contracts or on integrating renewable gas, both of which require substantial capital investments that many mid-tier companies may lack, potentially limiting their competitiveness in the market.

Geopolitical Trade-Route Disruptions

Sanctions on Russian and Belarusian fertilizers have redirected 12 million metric tons since 2024, compelling Brazil to procure additional volumes from the Middle East and China at a freight premium. This shift has significantly impacted global trade flows, increasing dependency on alternative suppliers and raising transportation costs. Security concerns in the Red Sea caused delays of up to 15 days for shipments from the Arabian Gulf to East Africa in 2025, further straining supply chains. Producers situated along alternative routes redirected supplies to capitalize on spot premiums, emphasizing the advantages of diversified portfolios while leaving import-dependent nations vulnerable to abrupt shortages. These developments underscore the critical need for resilient supply chain strategies to mitigate risks associated with geopolitical and logistical disruptions.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Specialty Type: Water-Soluble Leads While Controlled-Release Accelerates

Water-soluble formulations accounted for 40.8% of the urea market share in 2025. This growth was supported by the adoption of fertigation systems, which reduce leaching losses in arid regions such as the Middle East and Mediterranean Europe. These formulations dissolve rapidly and integrate with drip irrigation systems, enabling higher yields in greenhouse tomatoes. Additionally, their compatibility with precision agriculture techniques has further driven their adoption, enabling efficient nutrient management and improved crop productivity.

Polymeric coatings are narrowing the cost gap, leading to an anticipated annual growth rate of 7.6% for controlled-release grades through 2031, as coating costs decrease. Controlled-release grades are projected to become the fastest-growing segment. Their extended nutrient release aligns with the uptake patterns of perennial crops like citrus and coffee, reducing field passes and labor costs. Furthermore, these grades contribute to enhanced environmental sustainability by minimizing nutrient runoff and improving nitrogen use efficiency. In regulated markets with stricter nitrogen limits, these products offer compliance at a lower total cost, thereby enhancing their position in the urea market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download Sample Report

By Form: Conventional Dominates but Specialty Gains Momentum

Conventional materials are projected to account for 93.2% of the urea market size in 2025, driven by the continued preference for cost-effective solutions in bulk cereal applications. Subsidy programs in India set lower retail prices, reinforcing farmers' reliance on the most affordable nutrient options. The dominance of conventional materials is further supported by their widespread availability and established distribution networks, which cater to the high demand in developing agricultural economies.

Specialty forms are projected to grow the fastest, with a forecast CAGR of 7.0%. Polymer-coated and liquid urea products can reduce per-hectare application rates, which helps justify their premium cost in high-value applications such as fruits, vegetables, and turf. These products are anticipated to gain a larger share of the urea market in developed economies, where environmental compliance is increasingly tied to financial penalties. Additionally, the rising awareness of sustainable farming practices and the need to minimize nutrient runoff are driving the adoption of specialty forms, particularly in regions with stringent environmental regulations.

By Crop Type: Field Crops Anchor Volume, Horticultural Crops Drives Growth

Field crops represented 77.6% of the urea market share in 2025, driven by government efforts to achieve self-sufficiency in key crops such as wheat, rice, and maize. These crops are essential staples in many countries, and ensuring their availability is a priority for food security. India's Direct Benefit Transfer (DBT) initiatives, such as Pradhan Mantri Kisan Samman Nidhi (PM-KISAN), play a vital role in providing financial stability to farmers by directly transferring funds to Aadhaar-linked bank accounts, helping manage price volatility. These programs, combined with insurance schemes like Pradhan Mantri Fasal Bima Yojana (PMFBY), credit access, and mechanization support, contribute to stable production and income support.

Horticultural crop cultivation is growing at the fastest rate, with an 8.9% CAGR. In Saudi Arabia, hydroponic vegetable farming, and in China, greenhouse complexes, use nitrogen in water-soluble forms. This high application intensity significantly boosts revenue contributions despite smaller land areas. The adoption of advanced cultivation techniques in these regions underscores the growing focus on efficient resource use and higher yields. Additionally, premium turf and ornamental users in North America pay considerably higher prices than agricultural users, which supports strong profit margins and reflects their willingness to invest in quality inputs for superior results.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download Sample Report

Geography Analysis

Asia-Pacific is the largest geography, holding 45.1% of the urea market share in 2025, driven by India's demand and China's production and export capacity. India maintained stable retail prices despite fluctuations in import parity, ensuring consistent application rates, though this increased fiscal exposure during periods of price volatility. The region's dominance is further supported by government policies that promote agricultural productivity and by the presence of key market players. In 2025, China reduced exports as domestic industrial demand recovered, tightening global supply. Additionally, the growing population and rising food demand in the Asia-Pacific region are projected to sustain the region's significant share in the urea market.

Africa is the fastest-rising region, with a projected 9.5% CAGR to 2031, driven by irrigation schemes and subsidy reform. Nigeria’s Presidential Fertiliser Initiative retailed urea at USD 180 per metric ton, against a procurement cost of USD 350, unlocking 1.5 million metric tons of smallholder uptake in 2025. Ethiopia raised application rates after voucher expansion, pushing national consumption in 2025.

North America and Europe represent significant markets for urea. The United States has benefited from stable gas prices and the adoption of precision systems, while Canada has utilized urea for crops such as canola and wheat. In Europe, consumption declined due to elevated energy costs, leading to production shutdowns and stricter Nitrates Directive caps reducing application rates. This has resulted in increased reliance on imports, particularly from North Africa.

Get Analysis on Important Geographic Markets

Download Sample Report

Competitive Landscape

Market concentration remains low, with the top five suppliers, Yara International ASA, CF Industries Holdings, Inc., OCI N.V., SABIC Agri-Nutrients Company, and Nutrien Ltd., holding a limited share of the market. Yara International ASA, CF Industries Holdings, Inc., and OCI N.V. operate fully integrated ammonia-urea complexes that enable them to switch between products as spreads change, thereby cushioning margin shocks. Indian cooperatives, notably Indian Farmers Fertiliser Cooperative Limited (IFFCO) and Krishak Bharati Cooperative Limited (KRIBHCO), sell most of their output under long-term government contracts that guarantee stable cash flow even during price downturns.

Middle Eastern companies, including SABIC Agri-Nutrients and Qatar Fertiliser Company (QAFCO), benefit from lower natural gas prices, which have reduced production costs following recent catalyst upgrades. Strategic investments are being directed toward the back-integration of green ammonia.

Technology adoption among mid-tier players is progressing rapidly. Indian Farmers Fertiliser Cooperative Limited (IFFCO) sold 26.5 million bottles of Nano Urea Plus in 2025, replacing conventional nutrients, highlighting its potential to significantly impact volume metrics. Emerging companies like Fertiberia are integrating renewable energy into ammonia production units to supply premium-priced, low-carbon products to Europe and North Africa, underscoring the growing importance of carbon intensity alongside price and logistics as key differentiators.

Urea Industry Leaders

CF Industries Holdings, Inc.

Nutrien Ltd.

OCI N.V.

SABIC Agri-Nutrients Company

Yara International ASA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download Sample Report

Recent Industry Developments

- December 2025: Uralchem Group has signed a Memorandum of Understanding (MoU) with Indian public sector undertakings Rashtriya Chemicals and Fertilizers (RCF), National Fertilizers Limited (NFL), and Indian Potash Limited (IPL) to develop a urea joint venture plant in Russia with a production capacity of 1.8–2 million metric tons. The project aims to ensure long-term fertilizer supplies for India and will be financed by Indian companies, utilizing ammonia sourced from Togliattiazot JSC.

- December 2025: Italian engineering firm Saipem has been awarded two significant contracts by Dangote Fertilizer to provide technology and engineering services for six high-capacity urea units. These units include four in Nigeria and two in Ethiopia, each with a capacity of 4,235 metric tons per day (MTPD). The plants will utilize Snamprogetti's patented urea technology, significantly enhancing Africa's overall urea production capacity.

- December 2025: Adecoagro has finalized the acquisition of Profertil S.A., the largest and most cost-efficient producer of granular urea in South America. The transaction, valued at approximately USD 1.1 billion, establishes Adecoagro as the controlling shareholder with a 90% ownership stake.

- October 2025: United Capital Fertilizer (UCF) has launched a USD 641 million urea manufacturing plant in Chilanga, Zambia. This facility represents a significant step in Zambia’s plan to double its fertilizer production and establish itself as a regional agricultural hub. The plant aims to reduce Zambia’s dependence on imports. In 2024, the country imported approximately 800,000 metric tons of fertilizer, with urea comprising 36% of the total volume.

Global Urea Market Report Scope

Urea fertilizer is a high-concentration, nitrogen-rich organic compound, chemically known as carbamide, with the formula CO(NH2)2. It is the most widely used solid nitrogenous fertilizer globally. The Urea Market Report is Segmented by Speciality Type (Controlled-Release Fertilizer (CRF), Slow-Release Fertilizer (SRF), and More), by Crop Type (Field Crops, Horticultural Crops, and More), by Form (Conventional and Speciality), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Speciality Type

| Controlled-Release Fertilizer (CRF) | Polymer Coated |

| Polymer-Sulfur Coated | |

| Others | |

| Liquid Fertilizer | |

| Slow-Release Fertilizer (SRF) | |

| Water Soluble |

By Crop Type

| Field Crops |

| Horticultural Crops |

| Turf and Ornamental |

By Form

| Conventional |

| Speciality |

By Geography

| North America | Canada |

| Mexico | |

| United States | |

| Rest of North America | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Ukraine | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | Australia |

| Bangladesh | |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Pakistan | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Middle East | Turkey |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | Nigeria |

| South Africa | |

| Rest of Africa |

| By Speciality Type | Controlled-Release Fertilizer (CRF) | Polymer Coated |

| Polymer-Sulfur Coated | ||

| Others | ||

| Liquid Fertilizer | ||

| Slow-Release Fertilizer (SRF) | ||

| Water Soluble | ||

| By Crop Type | Field Crops | |

| Horticultural Crops | ||

| Turf and Ornamental | ||

| By Form | Conventional | |

| Speciality | ||

| By Geography | North America | Canada |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Ukraine | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | Australia | |

| Bangladesh | ||

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Pakistan | ||

| Philippines | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| South Africa | ||

| Rest of Africa | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Urea: Conventional Fertilizer, Controlled-release Urea Fertilizers, and Slow-Release Urea Fertilizer

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

���ϲ����� follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download Sample Report