Market Overview

| Study Period | 2020 - 2031 |

|---|---|

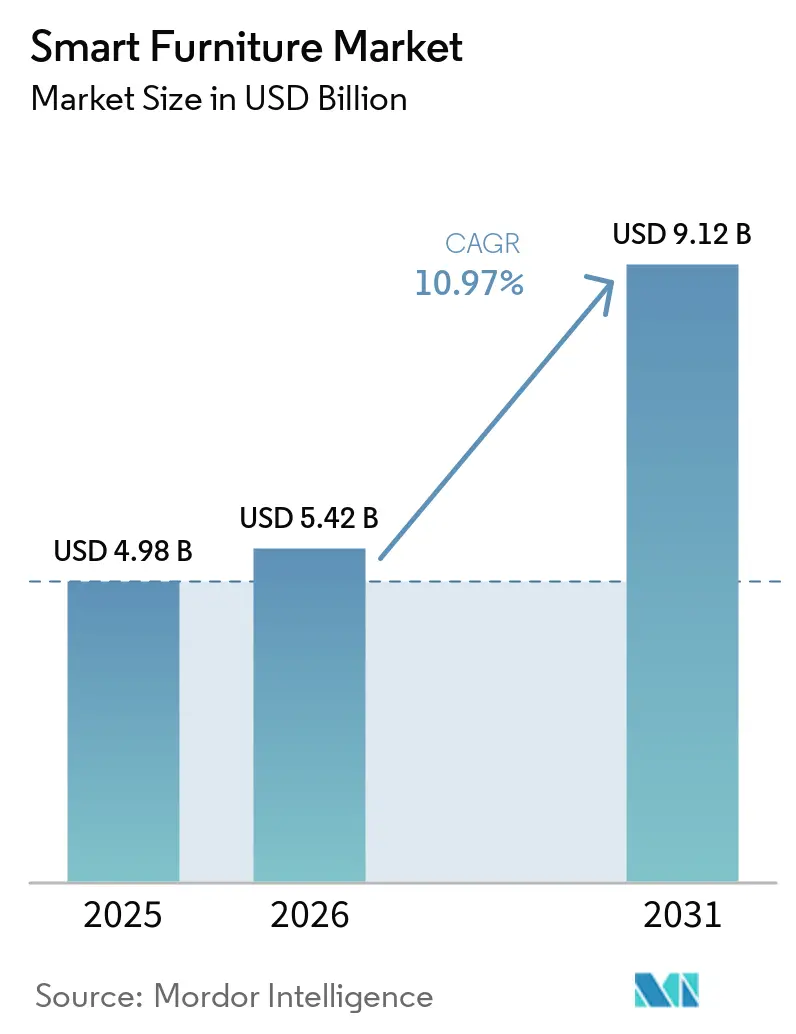

| Market Size (2026) | USD 5.42 Billion |

| Market Size (2031) | USD 9.12 Billion |

| Growth Rate (2026 - 2031) | 10.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Smart Furniture Market Analysis by ���ϲ�����

The global smart furniture market size is projected to expand from USD 4.98 billion in 2025 and USD 5.42 billion in 2026 to USD 9.12 billion by 2031, registering a CAGR of 10.97% between 2026 to 2031. This expansion signals a shift from passive fixtures to connected furnishings that blend sensors, actuators, and wireless modules into daily living and work environments, increasing utility and personalization. Standardized interoperability is reducing setup friction and enabling users to manage furnishings alongside lighting and climate through mainstream smart home controllers. The momentum around connected sleep systems and ergonomic desks is turning health and wellness features into core purchase drivers rather than optional add-ons. Supply chains and design toolchains are aligning across residential, office, and clinical environments, which supports scale and accelerates time-to-market for feature-rich products.

Key Report Takeaways

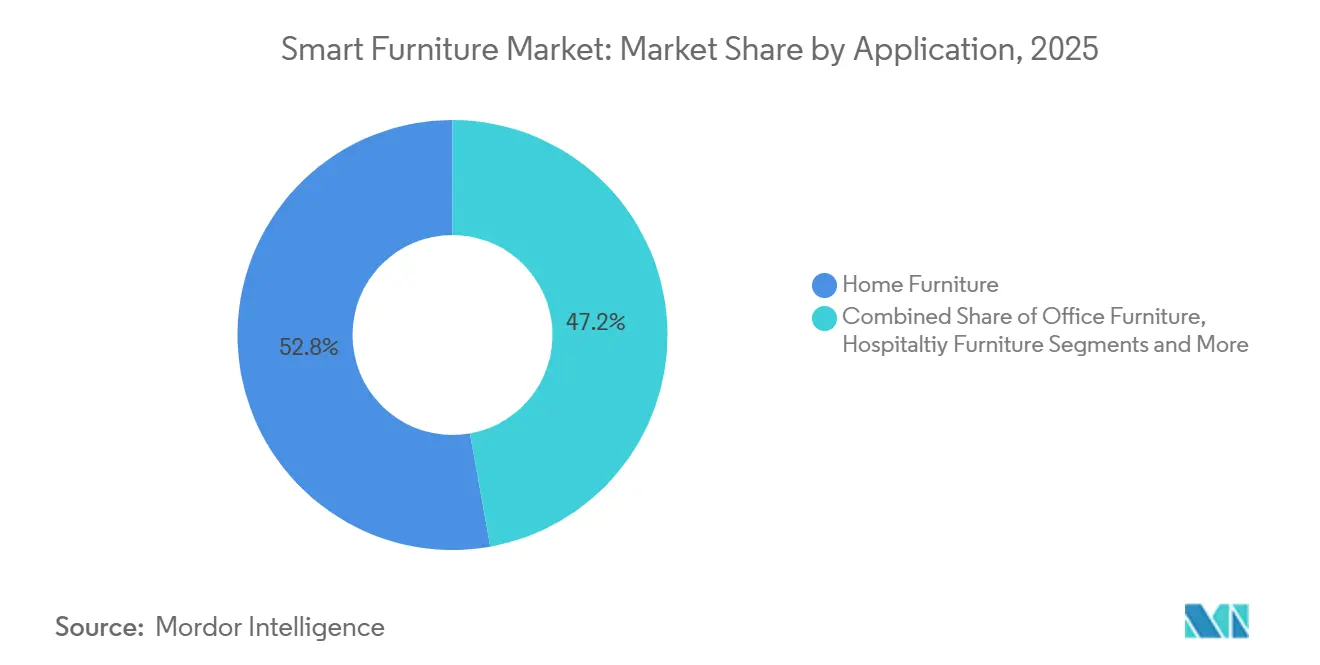

- By application, home furniture led with 52.80% of the global smart furniture market share in 2025, while healthcare is projected to expand at a 13.20% CAGR through 2031.

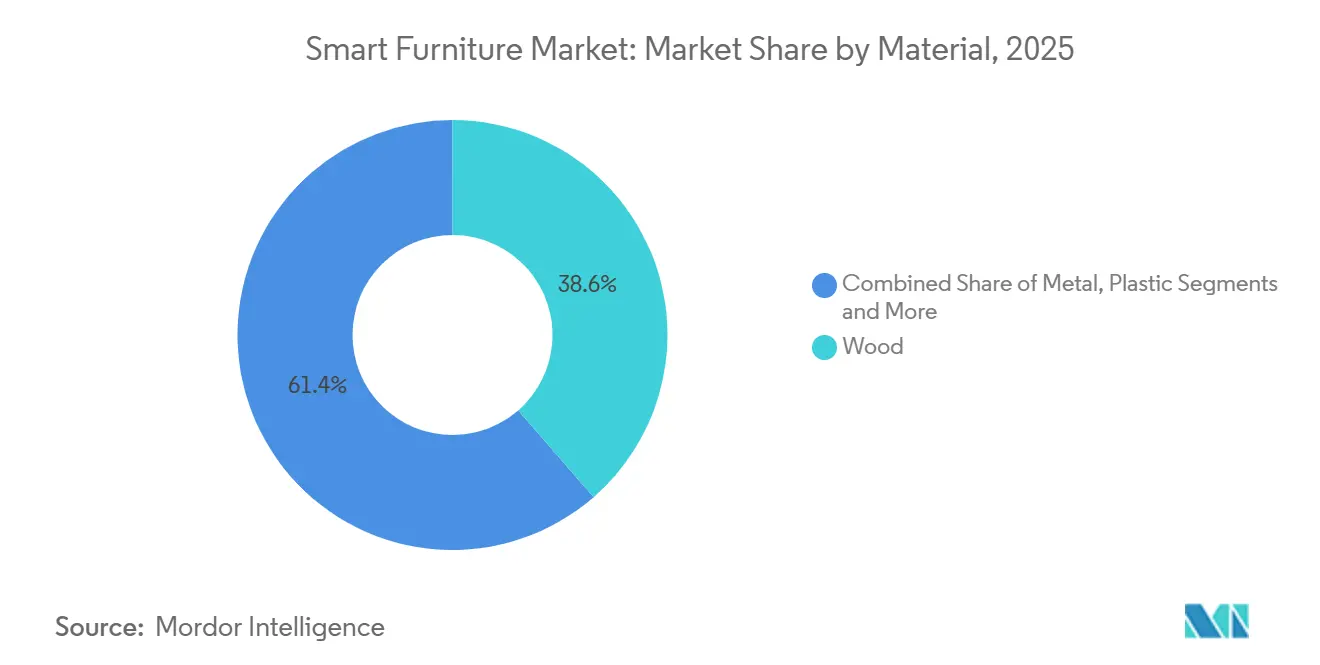

- By material, wood accounted for 38.60% of the global smart furniture market share in 2025, and plastic & polymer are forecast to grow at a 12.10% CAGR to 2031.

- By distribution channel, B2C/retail dominated with 64.40% of the global smart furniture market share in 2025, while B2B/project is expected to post a 12.75% CAGR through 2031.

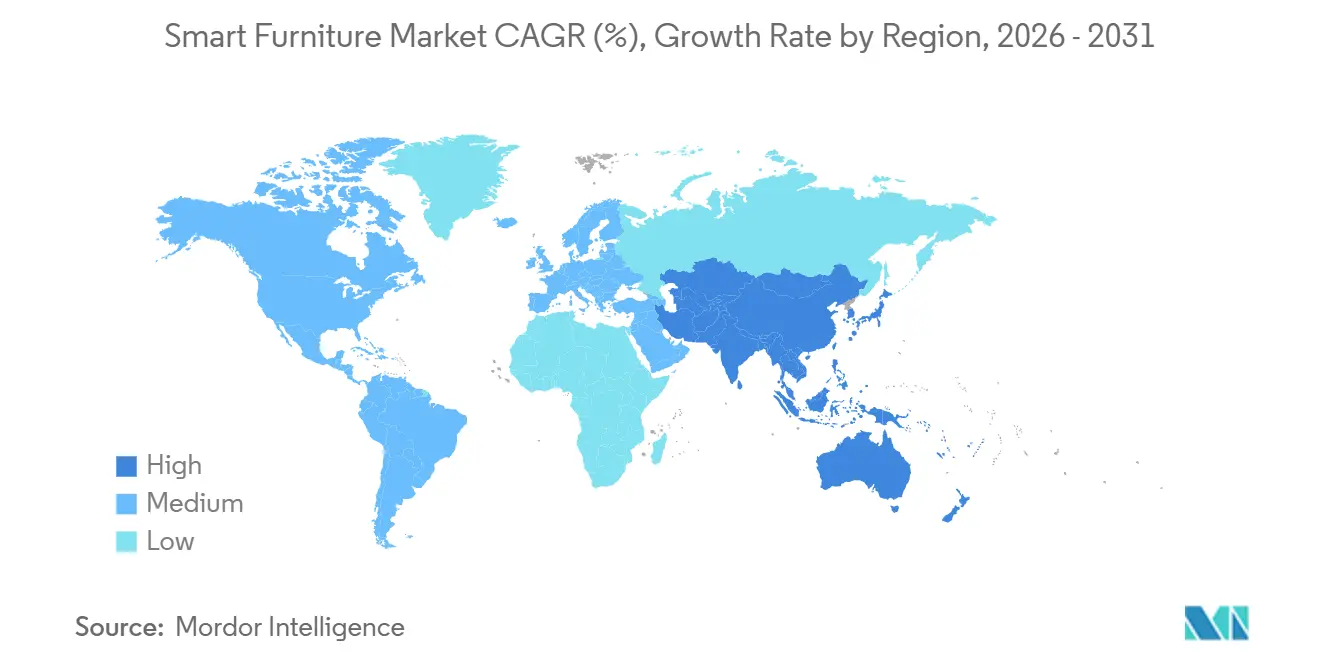

- By geography, North America held 34.90% of the global smart furniture market share in 2025, and Asia-Pacific is set to expand at a 12.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart Home and IoT Ecosystem Integration Across Furnishings | +2.8% | Global, with early gains in North America and Western Europe, rising adoption in urban APAC | Medium term (2-4 years) |

| Hybrid Work And Ergonomic Wellness Drive Sensorized Desks | +1.9% | North America and the EU core, expanding to APAC, strongest in corporate tech hubs. | Short term (≤ 2 years) |

| Sleep-Health Technologies and Connected Adjustable Bases Boost Smart Beds | +2.1% | Global, premium skew in North America and fast-growing adoption in APAC | Medium term (2-4 years) |

| Interoperability Standards Reduce Integration Friction | +1.5% | Global, the strongest infrastructure in North America and the EU | Short term (≤ 2 years) |

| Sensorized Workplace Storage and Asset Management Scale with Hybrid Offices | +0.9% | Urban centers in North America and the EU, early adoption in corporate and co-working | Medium term (2-4 years) |

| Connected Clinical Workstations and Smart Hospital Beds Normalize Smart Furnishings | +1.8% | Global, North America leads, and APAC accelerates | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Smart Home and IoT Ecosystem Integration Across Furnishings

Interoperability advances are turning the smart furniture market from a set of proprietary pilots into cohesive systems managed through common controllers. The Matter standard, developed by the Connectivity Standards Alliance with contributions from leading platforms, enables furnishings to join IP-based smart home networks that span brands, reducing onboarding friction and long-term lock-in. Recent launches show how this standard reaches mass-market audiences, as IKEA introduced a broad lineup of Matter-compatible products that work with Amazon Alexa, Google Home, Apple Home, and Samsung SmartThings. This path lowers the technical burden for users who want furnishings to coordinate with lighting and climate and do so without brand-specific bridges in many cases. As more products adopt this common language, the smart furniture market benefits from easier setup and more predictable performance across different home and office environments[1]IKEA, “The New Smart Home from IKEA: Matter Compatible,” IKEA Global Newsroom, ikea.com. The retail rollouts of interoperable accessories and controllers from IKEA reinforce confidence that furniture-embedded electronics can join wider ecosystems with fewer steps and fewer support issues over their lifecycle.

Hybrid Work and Ergonomic Wellness Drive Sensorized Desks

Workplace experience priorities are reshaping the smart furniture market as employers invest in desks and seating that track usage and promote healthier postures. Steelcase has highlighted how sensorized and connected workstations integrate with workplace management platforms to guide space allocation and ergonomic practices, which support policy shifts that accompany hybrid schedules. This integration enables facility teams to monitor occupancy patterns and intervene with targeted improvements, while giving employees a more supportive desk experience with fewer manual adjustments. Adjacent infrastructure, such as smart lockers, reinforces these outcomes by automating device handoffs and pickups, reducing wait times, and cutting routine support interactions for IT teams. Vendors such as LocknCharge and Ricoh report gains in ticket reduction and time-to-issue improvements when companies deploy smart locker systems, further aligning digital tools with physical asset flows in shared spaces[2]Steelcase, “5 Ways Your Office Will Change by 2026,” Steelcase Research, steelcase.com. This pattern, coupled with innovation from manufacturers of purpose-built smart workstations, strengthens the value case for connected office furniture across regions with high rates of hybrid work adoption.

Sleep-Health Technologies and Connected Adjustable Bases Boost Smart Beds

Sleep remains a prominent use case, and it continues to define how consumers perceive the smart furniture market at home. Eight Sleep’s Pod 5 showcases dual-zone climate control and automated temperature programs that adjust to the sleeper through onboard sensing and software-driven profiles, which position beds as active wellness tools rather than static fixtures. Sleep Number emphasizes temperature regulation, snore response, and longitudinal tracking through its SleepIQ platform, and it bundles connected features without a subscription, which encourages sustained engagement across the installed base. Tempur-Pedic’s ActiveBreeze pairs adjustable bases with climate and coaching features to expand premium choices for buyers who want sleep improvements integrated into the bed frame and mattress. These launches validate a shift toward embedded sensing, edge analytics, and actuator control in bedroom furniture, and they set the stage for broader hospitality and senior-care deployments that value consistency, hygiene, and remote-friendly interfaces.

Interoperability Standards Reduce Integration Friction

Standards-driven progress is central to expanding the total addressable market for smart furniture because it reduces integration risk for buyers and lowers support costs for sellers. Matter’s IP-first architecture supports Wi-Fi and Thread, with Bluetooth Low Energy used during commissioning, thereby avoiding the complexity of multiple proprietary hubs for day-to-day control. Multi-admin control lets the same device appear in multiple ecosystems, a feature that protects households and businesses from lock-in and service discontinuities over time. As furniture connects via controllers that also manage lighting and HVAC, interoperable devices contribute to broader energy and comfort routines, boosting utility while keeping setup consistent. Retailers and manufacturers that deliver certified controllers and bridges, such as IKEA with Dirigera, give users a path to unify legacy and new devices, which preserves past investments as they upgrade. This consistency is a foundation for growth because it assures buyers that connected furnishings will continue to work as platform ecosystems evolve[3]Connectivity Standards Alliance, “Matter,” Connectivity Standards Alliance, csa-iot.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost and Total Cost of Ownership | -3.2% | Price sensitivity is higher in emerging economies, moderate impact in developed markets | Short term (≤ 2 years) |

| Data Privacy and Cybersecurity Concerns in Connected Furniture | -1.7% | Higher impact in the EU and North America with strong regulatory scrutiny | Medium term (2-4 years) |

| Fragmented Ecosystems and Vendor Lock-In Hinder Seamless Experiences | -1.1% | Global, especially relevant for retrofit projects | Medium term (2-4 years) |

| Compliance And Safety Certification Overhead Slows Time-To-Market | -0.8% | Global, with stricter enforcement in North America and the EU | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Upfront Cost and Total Cost of Ownership

Acquisition price and lifecycle costs can delay upgrades to connected furnishings, especially for budget-constrained buyers and value-focused procurement teams. Many smart products pair hardware with embedded electronics and software, which introduces ongoing maintenance, updates, and occasional replacements. To address this, vendors are increasingly offering leasing, managed services, and modular designs that enable selective upgrades instead of full replacement cycles. In offices, complementary investments like smart lockers help reduce indirect costs by improving device turnaround and after-hours access, offsetting productivity losses and supporting overhead that typically inflate the total cost of ownership. As financing and service models mature, pay-as-you-go options and bundling across asset classes may reduce barriers to adoption in the smart furniture market, particularly for multi-site enterprises and institutions that need predictable budgeting for refreshes.

Data Privacy and Cybersecurity Concerns in Connected Furniture

Concerns around monitoring, data sharing, and device hardening can slow purchasing decisions, especially in regions with stringent privacy rules. Standards that codify security baselines help manage these risks by promoting device authentication, encrypted communications, and secure update pathways across ecosystems. The push toward on-device analytics is also gaining ground, since processing data locally minimizes cloud exposure while still enabling adaptive features that users value in bedrooms, offices, and clinics. Vendors that apply privacy-by-design, offer opt-in controls, and publish clear retention policies will see stronger acceptance from buyers who prioritize governance. As more certified controllers, bridges, and end devices enter the channel, consistent implementation of security frameworks should lift confidence and support broader deployments in the smart furniture market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Home Furniture Dominates, Healthcare Furniture Accelerates with Clinical Integration

Home furniture captured 52.80% of the smart furniture market share in 2025, supported by strong demand for connected beds, voice-instrumented side tables, and living room pieces that integrate charging and ambient control. The category now benefits from mainstream ecosystems and controllers, making it easier for consumers to add furnishings without changing other devices in the home. Connected sleep systems illustrate this pull, as brands deliver dual-zone climate and snore-response features embedded directly into bed platforms that work through familiar apps. The residential base also benefits from a growing set of interoperable accessories and hubs that operate as the backbone for lighting, climate, and furniture controls. As households move from first devices to coordinated routines, the smart furniture market becomes a natural extension of smart home expectations.

Healthcare is the fastest-growing application with a projected 13.20% CAGR through 2031, propelled by connected beds and clinical workstations that support monitoring, positioning, and data exchange with hospital systems. Vendors are adding real-time sensing and ergonomic assistance into beds and seating that must meet exacting standards for safety, hygiene, and reliability. As clinical teams scale remote oversight and fall prevention workflows, these features are moving from premium to standard in new facilities and retrofits. Privacy and compliance requirements also drive edge analytics, where data is processed on the device to limit transmission of sensitive information while enabling responsive adjustments. The smart furniture market in healthcare settings is poised to grow as institutions standardize on connected equipment that aligns with digital clinical pathways.

By Material: Wood Retains Premium Appeal, Plastic & Polymer Surge with Bio-Based Innovations

Wood remained the top material with a 38.60% share in 2025 and continues to anchor premium lines where natural aesthetics and durability are priorities. Manufacturers are embedding wireless charging, sensors, and cable routing into wooden frames and surfaces without sacrificing design, which sustains appeal among residential and executive office buyers. Interoperable controllers and accessories released by major retailers can be paired seamlessly with wooden pieces, which helps users avoid visible clutter from adapters and external hubs. Advances in computer-controlled machining have improved fit and finish for complex cutouts that house electronics and ventilation, supporting reliability while preserving the visual look. As sustainability standards evolve, certified wood sourcing and low-emission finishes are becoming core purchasing criteria alongside connectivity.

Plastic and polymer components are the fastest-growing material category with a projected 12.10% CAGR through 2031, driven by lightweight designs and molded geometries that simplify integration of sensors and charging coils. These materials enable single-piece shells with wire channels and reinforcement zones, reducing assembly steps and facilitating recycling at the end of life. Hybrid constructions that combine wood veneers over polymer cores are also gaining ground, offering the warmth of wood with moisture resistance and weight savings. Metal remains in structural frames and shielding layers for desks and hospital beds, though hybrid approaches are reducing total metal mass by using it where strength and interference control are essential. As circular-economy policies expand, material selection and documentation will further shape procurement, which raises the profile of polymer blends with known origins and clear recycling or refurbishing pathways in the smart furniture market.

By Distribution Channel: B2B/Project Outpaces Retail with Subscription-Based Procurement

B2C/Retail held 64.40% share in 2025, reflecting consumer comfort with in-store trials, guided demos, and home delivery for complex connected furnishings. Retailers that stock interoperable devices create accessible pathways for buyers to assemble coherent ecosystems around lighting, climate, and furniture control. Big-box and specialty stores are extending their assortments with controllers, bridges, and accessories that simplify furniture onboarding, and they are pairing these assortments with staff who can explain how devices work together. Direct-to-consumer brands are using online configurators and app previews to reduce purchase anxiety for higher-priced smart beds and desks, thereby supporting conversions without in-person trials. As home ecosystems become more cohesive, repeat purchases in the same environment help scale the installed base of connected furnishings in the smart furniture market.

B2B/project, with an expected 12.75% CAGR through 2031, is accelerating on the back of hybrid work, facility optimization, and managed workplace services. Enterprises are bundling desks, seating, and smart lockers to improve ergonomics and streamline asset logistics across shared neighborhoods, which reduces downtime and support tickets. Integration with ticketing and identity platforms enables secure, after-hours device pickups and returns, keeping employees productive without manual coordination. The smart furniture market size for B2B deployments is set to expand as organizations convert capex into service-driven models and align furnishing refresh cycles with broader IT and real estate strategies. Vendor programs that combine hardware, software, and analytics for utilization benchmarking are increasingly central to procurement decisions in large accounts.

Geography Analysis

North America led the smart furniture market with a 34.90% share in 2025, underpinned by high connected-home penetration, employer wellness programs, and widespread access to controllers that unify lighting, climate, and furnishings. Adoption has been strengthened by strong retail and direct channels that explain connected features in plain terms and demonstrate them in-store or online. Workplace strategies that emphasize better ergonomics are accelerating installations of sensorized desks and lockers that reduce help desk loads and improve equipment turnaround times. In the home, bed platforms that layer temperature control, snore response, and sleep tracking are now offered by several brands, broadening the shopper base and increasing repeat purchases. As standards-based ecosystems scale, household and corporate buyers in North America are more willing to expand deployments across rooms and sites because the control experience now feels consistent[4]Sleep Number, “Smart Beds with SleepIQ Technology,” Sleep Number, sleepnumber.com.

Asia-Pacific is the fastest-growing region, with a projected 12.95% CAGR through 2031, supported by dense urbanization, active innovation hubs, and strong manufacturing ecosystems. Compact households and co-working footprints encourage multifunctional furniture with embedded power, lighting, and sensing, reducing clutter and setup steps. Regional vendors are advancing workstation designs with integrated docking, wireless charging, and cloud profiles that adapt desk settings for hot-desking and shared spaces. As mass-market retail expands assortments of interoperable accessories, consumers in major cities are finding it easier to add connected furnishings to existing smart home setups. The smart furniture market in Asia-Pacific is set to grow in line with rising comfort with connected devices and the steady adoption of standardized products in mainstream retail.

Europe maintains a steady trajectory as sustainability and product safety frameworks shape material choices, lifecycle planning, and cybersecurity requirements for connected devices. Buyers favor durable constructions and certified materials for home and office settings, and they are adopting furnishings that can be repaired, upgraded, or remanufactured to extend useful life. Corporate customers are elevating governance requirements in RFPs, pushing vendors to document data flows, update practices, and obtain security certifications for connected components. Southern Europe, the Middle East, and South America are building momentum from a smaller base as retail networks expand and as buyers seek space-saving solutions that incorporate power and ambient control. As global brands and regional specialists broaden their sales footprints, shoppers in these markets gain more options across price tiers, which supports entry-level to premium growth in the smart furniture market.

Competitive Landscape

The smart furniture market remains fragmented, with the top five players accounting for an estimated 29.37% combined share in 2024, leaving room for specialists, platform suppliers, and service-led entrants to scale. This structure rewards ecosystem compatibility and service capabilities because buyers want options that can grow from single rooms to entire homes or buildings without vendor lock-in. Platform partners that provide actuators, controllers, and modular sensor kits are expanding their influence by enabling many brands to add smart features without building their own electronics stacks from scratch. As supply chains converge across residential, office, and clinical products, firms that master shared modules and software updates can lower development costs and speed feature rollouts. This dynamic supports faster category expansion and a rising baseline for connected features even in mid-priced ranges of the smart furniture market.

Brands are also differentiating through monetization and engagement approaches that complement their hardware portfolios. In sleep, Eight Sleep emphasizes software-driven experiences with automated temperature and position adjustments, while Sleep Number highlights integrated sensing with no subscription to sustain trust and engagement across large installed bases. In premium segments, Tempur-Pedic is combining adjustable bases with climate features and coaching to address comfort and recovery use cases that resonate with wellness-centric buyers. In offices, Steelcase and other workplace leaders are connecting desks and seating to analytics platforms, which enables targeted ergonomic interventions and better space allocation. These moves show how recurring software value and data-backed interventions are becoming central to competitive positioning in the smart furniture market.

Ecosystem partners in storage and device logistics are reinforcing the case for connected furnishings inside enterprises and institutions. Vecos-powered implementations, distributed through channel partners, demonstrate how networked lockers enable dynamic assignments, visibility into usage, and reduced idle inventory across large sites. LocknCharge customers report sharp reductions in ticket volume and faster device swap times after deploying smart lockers, thereby shortening disruption windows for employees and students. Ricoh documents similar outcomes with enterprise-scale locker deployments that align asset access with identity systems and ticketing platforms. These practical gains link workplace IoT investments to daily productivity and support quantifiable returns, thereby strengthening vendor narratives and procurement justification across the smart furniture market.

Smart Furniture Industry Leaders

Ashley Furniture Industries, Inc.

HNI Corporation

Sleep Number Corporation

Desktronic

IKEA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: IKEA expanded its Matter-compatible smart home portfolio to 21 products, including sensors, lights, and controls that integrate directly with Amazon Alexa, Google Home, Apple HomeKit, and Samsung SmartThings without requiring proprietary hubs. This strategic push positions IKEA as a mass-market leader in interoperable smart furnishings, leveraging its global retail footprint to normalize Matter-ready accessories and controllers.

- May 2025: Eight Sleep launched the Pod 5 smart bed featuring dual-zone water cooling, automated temperature and elevation adjustments based on biometric data, and snore response via head elevation. The product underscores the ongoing shift to embedded sensing and actuator control as core purchase criteria in connected beds.

- June 2025: Sleep Number presented research findings at the SLEEP 2025 conference highlighting the role of temperature programs in improving sleep quality for women experiencing menopause-related symptoms. The findings reinforce the wellness value of intelligent temperature and position control within bed platforms.

Global Smart Furniture Market Report Scope

Smart furniture is a furniture with integrated technology such as sensors and intelligent systems to provide enhanced functionality, for example, coffee tables with wireless charging. A complete analysis of the global smart furniture market, which includes an assessment of the emerging market trends by segments, significant changes in the market dynamics and market overview, is covered in the report. The Global Smart Furniture Market is Segmented By Product (Smart Desks, Smart Tables, Smart Chairs, Other Smart Furniture), By End User (Residential, Commercial), By Distribution Channel (Home Centers, Specialty Stores, Online, Other Distribution Channels), By Geography (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa).

By Application

| Home Furniture | Smart Chairs |

| Smart Beds | |

| Smart Sofas | |

| Smart Tables | |

| Smart Wardrobes | |

| Office Furniture | Smart Chairs |

| Smart Desks & Tables | |

| Smart Storage Cabinets | |

| Smart Soft Seating | |

| Hospitality Furniture | |

| Educational Furniture | |

| Healthcare Furniture | |

| Other Applications |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Retail Channels | |

| B2B / Project |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Application | Home Furniture | Smart Chairs |

| Smart Beds | ||

| Smart Sofas | ||

| Smart Tables | ||

| Smart Wardrobes | ||

| Office Furniture | Smart Chairs | |

| Smart Desks & Tables | ||

| Smart Storage Cabinets | ||

| Smart Soft Seating | ||

| Hospitality Furniture | ||

| Educational Furniture | ||

| Healthcare Furniture | ||

| Other Applications | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Retail Channels | ||

| B2B / Project | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the smart furniture market?

The category stands at USD 5.42 billion in 2026 and is forecast to reach USD 9.12 billion by 2031 at a 10.97% CAGR, reflecting strong momentum across residential, office, and clinical use cases.

Which application leads global demand today?

Home furniture leads with a 52.80% share in 2025, driven by connected beds, side tables, and living room solutions that integrate charging and ambient controls within standardized ecosystems.

Where is the fastest growth expected geographically?

Asia-Pacific is projected to grow at 12.95% through 2031, supported by compact living, innovative workstation designs, and expanding assortments of interoperable accessories in mainstream retail.

What technologies are defining the next wave of connected furnishings?

Interoperability through Matter, Thread-ready controllers and bridges, edge analytics for privacy, and actuator-driven features in beds and desks are becoming standard, enabling coordinated routines across devices.

Which distribution channels are shaping adoption patterns?

B2C/Retail dominates with a 64.40% share for in-store demos and home delivery, while B2B/Project is the fastest-growing channel as enterprises bundle desks, seating, and smart lockers for hybrid work.

How are privacy and security concerns being addressed?

Certified interoperability frameworks define security baselines, while vendors increasingly use on-device analytics and clear opt-ins to reduce risk and build confidence among household and enterprise buyers.

Page last updated on: