Rice Snacks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

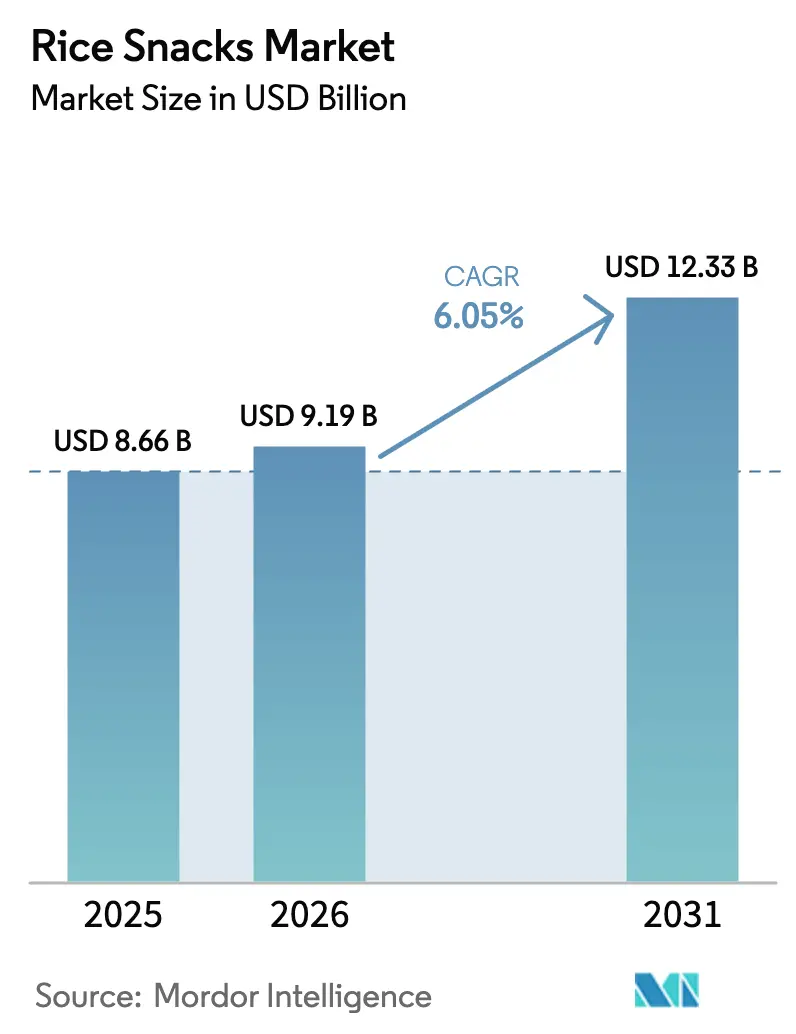

| Market Size (2026) | USD 9.19 Billion |

| Market Size (2031) | USD 12.33 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

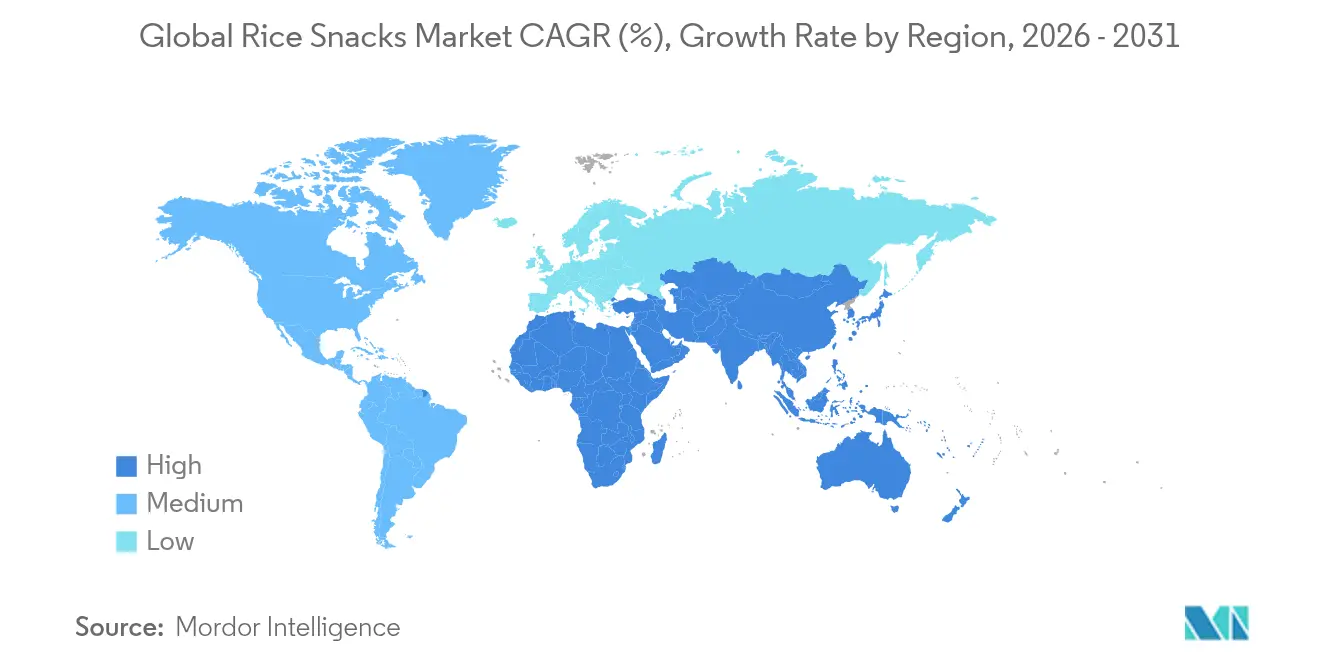

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Rice Snacks Market Analysis by ���ϲ�����

The rice snacks market size is projected to expand from USD 8.66 billion in 2025 and USD 9.19 billion in 2026 to USD 12.33 billion by 2031, registering a CAGR of 6.05% between 2026 and 2031. As health consciousness rises and front-of-pack labeling rules tighten, consumers are increasingly prioritizing portion control and ingredient transparency. Mainstream SKUs are seeing a boost in perceived nutritional value as clean-label reformulations swap out refined rice flour for whole-grain or rice-bran ingredients. Meanwhile, premiumization tactics, like the introduction of umami-rich seasonings, are expanding price ranges without stifling demand. In the Asia-Pacific region, deep-rooted rice-cracker traditions maintain the area's dominance. However, North America is swiftly catching up, with supermarkets allocating more shelf space to "better-for-you" salty snacks. On the supply front, fluctuations in rice prices, driven by climate factors, are pushing publicly listed manufacturers to adopt vertically integrated sourcing strategies and hedging programs, especially as they navigate quarterly margin evaluations. Additionally, manufacturers are investing in research and development to develop innovative product offerings that align with evolving consumer preferences.

Key Report Takeaways

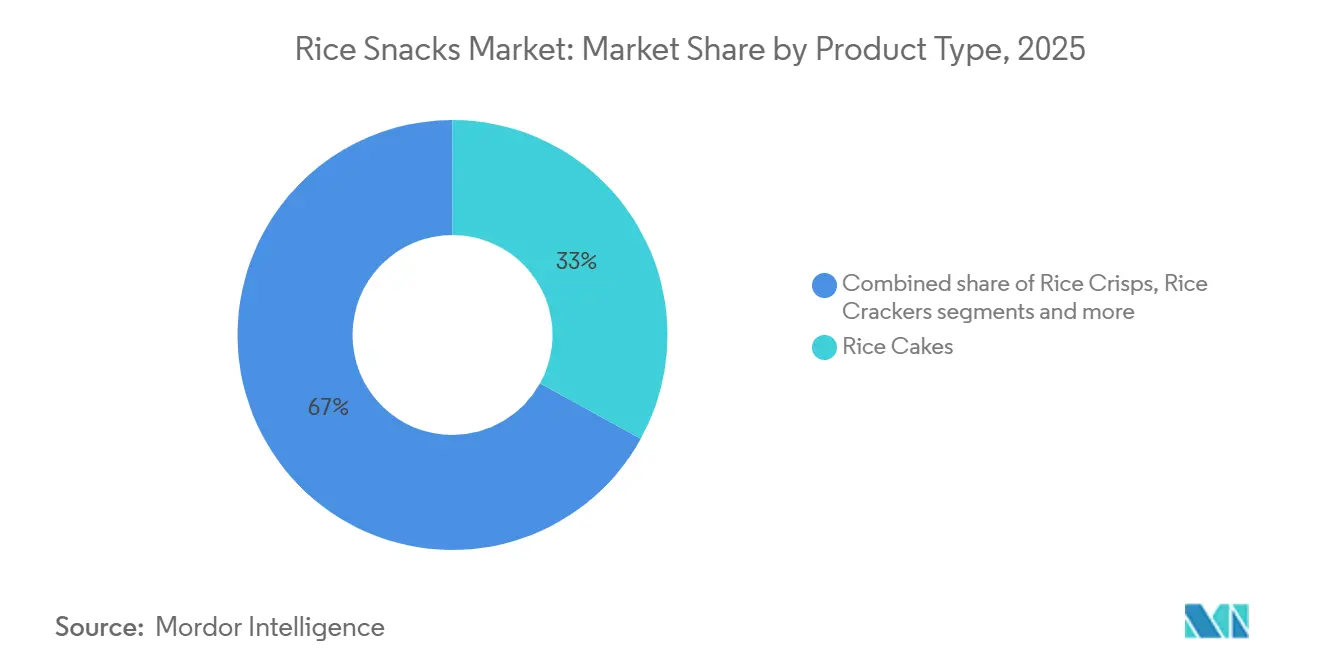

- By product type, rice cakes secured 33.02% of 2025 global revenue, while rice crackers are forecast to expand at an 8.23% CAGR through 2031.

- By flavor, salty variants controlled 47.58% of the 2025 share; spicy profiles are advancing at a 6.52% CAGR to 2031.

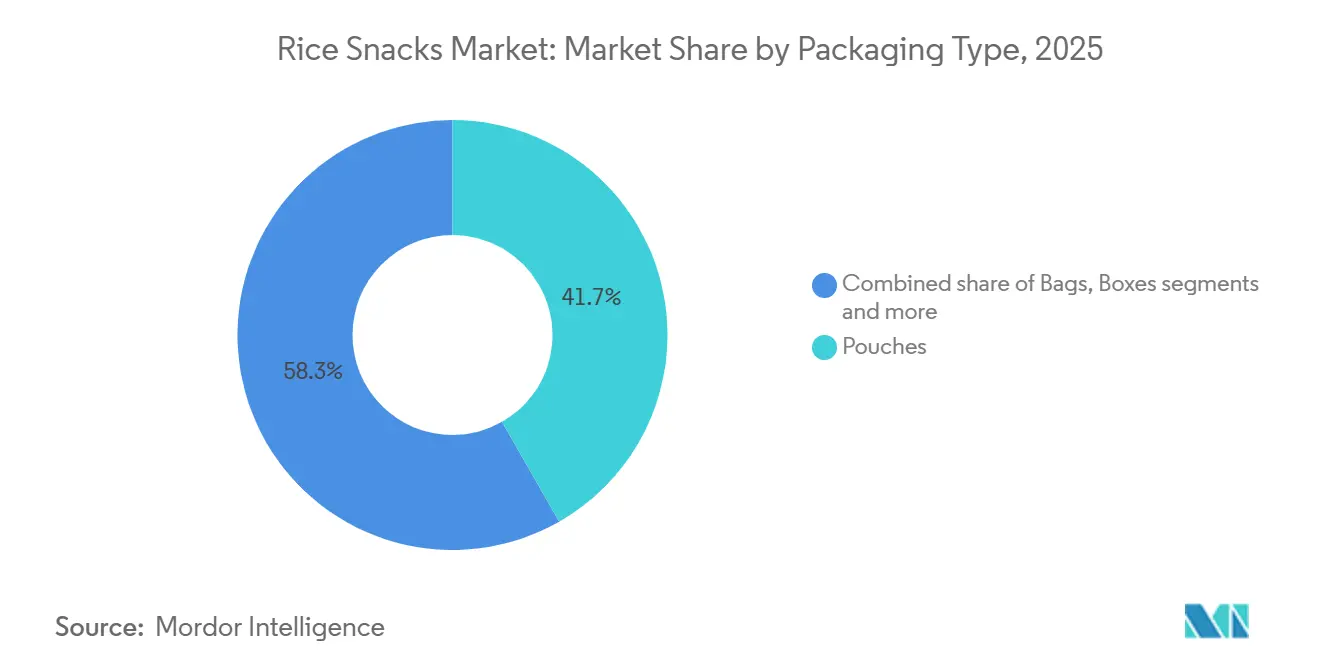

- By packaging, pouches commanded 41.58% of 2025 sales and are rising at a 7.05% CAGR through 2031.

- By distribution, supermarkets and hypermarkets represented 52.48% of 2025 turnover, whereas online retail is accelerating at a 9.11% CAGR through 2031.

- By geography, Asia-Pacific contributed 46.22% of 2025 revenue, but North America is projected to log a 7.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rice Snacks Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health awareness and demand for healthier snacks | +1.2% | Global, peak in North America and Western Europe | Medium term (2-4 years) |

| Convenience and on-the-go snacking | +0.9% | Global, urban Asia-Pacific and North America | Short term (≤ 2 years) |

| Innovation in flavours and formats | +1.0% | Global, earliest in Asia-Pacific and North America | Medium term (2-4 years) |

| Eco-friendly packaging mandates and circular-economy pilots | +0.6% | Europe and North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Increasing investment in marketing and promotional activities | +0.7% | Global, digitally mature markets | Short term (≤ 2 years) |

| Rice-bran valorisation opens premium functional niches | +0.5% | North America and Europe, emerging urban Asia-Pacific | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Health awareness and demand for healthier snacks

In 2024, the FDA updated its definition of "healthy," permitting whole-grain rice snacks with minimal added sugar to make health claims. This shift has prompted major brands to urgently reformulate their products. As consumers increasingly turn to GLP-1 drugs, there's a noticeable shift towards lower-calorie, nutrient-rich products that not only prevent nausea but also ensure a feeling of fullness. Retailers are becoming stricter about third-party certifications, elevating the importance of clean-label status from a unique selling point to a standard requirement. Brands that delay obtaining these certifications face the risk of being removed from premium channels, which are crucial for maintaining category profit margins. As a result, growth in the premium tier is now influencing mainstream offerings, broadening the market for healthier rice snacks. This trend underscores the growing consumer preference for transparency and health-focused innovations in the food industry.

Convenience and on-the-go snacking

In 2024, the International Food Information Council (IFIC) reported that 73% of U.S respondents snacked at least once daily[1]Source: International Food Information Council (IFIC), "2024 IFIC Food and Health Survey", ific.org. As hybrid work patterns disrupt traditional eating schedules, there's a growing preference for single-serve snacks. These snacks, ideal for desk consumption, minimize mess and don't require refrigeration. Rice-based items have emerged as a solution, as their low water activity not only extends shelf life but also ensures a satisfying crunch and quiet bite. The rise of convenience-store formats in countries like Indonesia, India, and Brazil has bolstered grab-and-go sales. Additionally, novel resealable pouches are enhancing freshness across multiple snacking moments, curbing household waste, and elevating perceived value. Consequently, urban centers in developing regions are witnessing a shift in impulse-driven sales from traditional potato chips to portable rice snacks. This trend highlights the growing demand for convenient, portable, and sustainable snacking options.

Innovation in flavours and formats

In 2024, Kameda Seika reported a notable 12% rise in export revenue, a trend driven by manufacturers blending traditional soy and seaweed with modern seasonings like truffle and smoked paprika. By optimizing extrusion parameters, hybrid bases such as rice-quinoa crackers effectively bridge perceived protein gaps while maintaining a light puffiness. Mini rice-cake clusters, now tailored for yogurt or salad, are transforming rice snacks from mere indulgences to integral meal components. These successful SKUs, adhering to a 150-calorie portion norm, resonate with the "guilt-free" trend popular among millennials. The sensory novelty of specialty seasonings justifies their premium pricing, allowing manufacturers to achieve higher price points. Additionally, the increasing focus on health-conscious eating habits is further boosting the demand for innovative rice snack products.

Eco-friendly packaging mandates and circular-economy pilots

By 2030, all packaging in the EU must be recyclable or reusable, prompting a shift from multi-layer laminates to mono-material polyethylene films[2]Source: European Commision, "Packaging Waste Regulation," environment.ec.europa.eu . In 2024, PepsiCo invested USD 75 million to retrofit Quaker rice-cake lines, positioning itself for cost advantages as regulations tighten. Yet, while mono-films are a step forward, they permit more oxygen ingress, potentially shortening shelf life. This challenge necessitates the adoption of natural oxygen scavengers, inflating research and development costs. In select Chinese provinces, deposit-return pilots saw a 30% consumer participation rate, especially when paired with loyalty incentives, highlighting their feasibility even in fragmented retail environments. Brands that highlight verifiable life-cycle-assessment reductions are gaining traction, appealing to eco-conscious shoppers willing to pay a premium in the rice snacks market. Companies that fail to adapt to these regulatory and consumer shifts risk losing market share to more agile competitors.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High competition from alternative protein and granola snacks | -0.8% | Global, especially North America and Europe | Short term (≤ 2 years) |

| Volatile rice prices linked to climate-related supply shocks | -0.5% | Global, sharper in import-dependent regions | Medium term (2-4 years) |

| Stricter HFSS front-of-pack labels in OECD markets | -0.4% | OECD countries, led by UK and EU | Medium term (2-4 years) |

| Limited shelf-life for clean-label products without additives | -0.3% | Global, most acute in humid tropics | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High competition from alternative protein and granola snacks

Protein bars, consistently offering 15–20 g of protein, have outshone unfortified rice snacks, securing prime shelf visibility. Meanwhile, keto-friendly granola clusters are capturing market share from carb-conscious consumers, casting rice in a high-glycemic light. In a bid to regain functional significance, rice-cracker brands are toying with almond-butter toppings and chia inclusions. However, they grapple with capital expenditure challenges in co-manufacturing. The shelves in North America and Europe are fiercely competitive, leading to tighter promotional schedules and heightened trade-spend inflation. Lacking distinct functional differentiation, products in the rice snacks market risk commoditization, especially among the younger fitness demographic. As consumer preferences continue to evolve, innovation remains critical for brands to maintain relevance in this competitive landscape.

Volatile rice prices linked to climate-related supply shocks

Despite a record global supply, the USDA highlighted that regional droughts and floods in 2025 led to 25% swings in spot prices[3]Source: United States Department of Agriculture (USDA), "Grains, Feeds and Fodders," fas.usda.gov . In the EU and MENA, processors reliant on imports faced unexpected cost surges, particularly where contracts didn't include escalation clauses, thereby squeezing their gross margins. While diversifying sourcing origins and forming long-term alliances with farmers can buffer against such shocks, they also tie up working capital, making it challenging for smaller firms. Anticipating more frequent El Niño episodes, many multinationals are gravitating towards partial backward integration. This uneven ability to hedge risks is driving consolidation, shifting power dynamics in favor of established players in the rice snacks market.

Segment Analysis

By Product Type: Rice Crackers Lead Innovation Velocity

In 2025, rice cakes commanded a dominant 33.02% share of the rice snacks market revenue, particularly thriving in North America's health-centric aisles. Their strong shelf presence is bolstered by whole-grain certifications. These cakes, a go-to for calorie-conscious consumers, have introduced multigrain and bran-enriched variants. These not only double the protein content but also maintain servings at around 90 calories, countering the allure of indulgent alternatives. Yet, their perceived uniformity poses a challenge, limiting their trade-up potential and leaving them susceptible to competitors with bolder flavors. Despite facing incremental shelf space erosion from a surge of cracker SKUs in Asian specialty outlets, rice cakes firmly anchor wellness and diet channels. Meanwhile, emerging extruded puff formats in the "others" category hint at a potential breakfast disruption, especially if fortified options can deliver a superior mouthfeel.

Forecasted to grow at an 8.23% CAGR through 2031, rice crackers are set to outpace rice cakes. Their thin, crunchy texture lends itself well to intense seasonings, enabling swift adaptation to culinary trends. This adaptability allows them to command a 30% price premium over plain variants. With this flavor depth, rice crackers are poised to eclipse rice cakes in premium grocery channels by 2029, as taste innovation takes precedence over calorie control. On the other hand, rice crisps, which combine puff lightness with crunch, face challenges due to their vague positioning, hindering sales momentum. The competitive landscape has shifted focus from commodity costs to textural research and development, underscoring the importance of innovation for market leadership.

Note: Segment shares of all individual segments available upon report purchase

By Flavor: Spicy Variants Capture Millennial Palates

In 2025, salty variants captured 47.58% of the rice snacks market, solidifying their status as pantry staples in many households. Their broad appeal is rooted in familiarity, yet they grapple with stagnant sales growth, especially under scrutiny from health-conscious consumers advocating for sodium reduction. Sweet variants, while secondary, play a pivotal role in appealing to children and seniors, ensuring a balanced portfolio that shields against demographic shifts. Regional flavors, such as seaweed and kimchi, carve out strong geographic niches, infusing cultural authenticity and enhancing export potential. This diverse foundation positions salty variants as the steadfast anchor amidst changing taste trends. Manufacturers are increasingly exploring sodium-reduction technologies to address health concerns while maintaining flavor integrity.

Spicy rice snacks are on a rapid ascent, forecasting a 6.52% CAGR through 2031. The benefits of capsaicin, particularly its satiety effects, resonate with today's weight-management focus, allowing brands to market them as health-centric rather than just spicy. Convenience stores in U.S. college towns are leading the charge in adoption, and innovative flavor encapsulation techniques are extending shelf life by 3–4 weeks by moderating capsaicin reactions. Brands are adeptly adjusting spice levels to cater to diverse palates, all while navigating stricter sodium regulations. Nutritional claims spotlighting metabolic advantages further validate their premium pricing. As a result, flavor research and development has transitioned into a pivotal, data-driven strength, fueling the spicy segment's growth.

By Packaging Type: Pouches Dominate Sustainability Narratives

In the rice snacks market, pouches maintain market leadership with a 41.74% share in 2025. This market position is attributed to increasing consumer demand for packaging solutions that offer convenience, portability, and resealable functionality while maintaining product integrity. The structural advantages of pouches, including their minimal weight, storage efficiency, and product preservation capabilities, position them as the optimal choice for contemporary consumption patterns. Technological advancements in flexible packaging manufacturing have facilitated the integration of environmentally sustainable materials, addressing ecological considerations. Furthermore, the design characteristics of pouches facilitate effective brand communication and product presentation in retail environments.

Bags retain a substantial market presence due to their economic efficiency and established distribution infrastructure. The reduced production costs associated with bag packaging enable manufacturers to implement competitive pricing strategies, particularly appealing to price-conscious market segments. The configuration of bags facilitates optimal retail space utilization, rendering them suitable for large-scale retail operations. Boxes occupy the premium market segment, specifically catering to specialized rice snack products and multiple-serving configurations. Their structural integrity accommodates substantial product volumes and assortment variations, positioning them effectively for gift presentations and premium retail distribution channels. The format of boxes enhances product presentation parameters, fulfilling consumer requirements for bulk purchasing options and specialized product selections.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Retail Disrupts Traditional Slotting Economics

In 2025, supermarkets and hypermarkets, leveraging their scale and bulk-volume leadership, dominated the rice snacks distribution landscape, seizing 52.48% of the total market share. They fortified their position with click-and-collect options, effectively countering basket fragmentation. Meanwhile, convenience outlets within this network capitalized on immediate access and premium single-serve displays, bolstering brand visibility. The "others" category, encompassing vending, foodservice, and corporate pantries, serves as a captive outlet but emphasizes the need for precise portioning and pricing to enhance uptake. Even as growth slows, these traditional channels ensure consistent household penetration, standing firm against the encroachment of digital alternatives. Their well-established infrastructure continues to bolster core volume, even in the face of margin erosion from e-commerce.

Online retail stores are emerging as the fastest-growing segment, boasting a 9.11% CAGR. Their growth is driven by a wider assortment of products, the convenience of home delivery, and direct-to-consumer models that avoid slotting fees, allowing for nimble flavor testing. These DTC strategies not only facilitate agile flavor testing but also amass first-party data, leveraging it for algorithmic promotions and tailored offers, which in turn elevate conversion rates by 12–15%. To counterbalance high last-mile delivery costs, bundled subscriptions at five-pack levels have been introduced, ensuring profitability even for single-bag orders. In response, brick-and-mortar establishments are rolling out omnichannel loyalty programs and retail media networks, trading digital visibility for a more efficient advertising spend. This evolution is reshaping the rice snacks market, placing emphasis on data expertise and the speed of fulfillment.

Geography Analysis

In 2025, the Asia-Pacific region commanded a dominant 46.22% share of the revenue pie, buoyed by Japan's deep-rooted senbei tradition, the burgeoning middle class in China's suburbs, and the expansion of organized retail in India. To counter a plateauing domestic snack expenditure, Japanese giants Kameda Seika and Calbee are turning their gaze outward, tapping into the urban millennial market across Southeast Asia. Meanwhile, China's Want Want is capitalizing on its distribution strength, introducing premium seaweed and mala flavors to tier-2 cities, and enjoying a surge with double-digit unit growth. In India, despite a fragmented market, heightened health consciousness and the rise of e-commerce are paving the way for premium rice-cake segments, commanding prices 20% above traditional namkeen. Countries like Indonesia, Thailand, and Vietnam are becoming hotspots for global players, keen on establishing local production to combat humidity-related shelf-life challenges.

North America, while smaller in size, is on track to achieve the fastest growth rate globally, with a projected CAGR of 7.43%. This surge is largely attributed to the FDA's clear nutrition labeling, which not only simplifies product reformulation but also bolsters retailer trust. The U.S. stands at the forefront of this growth, with supermarkets strategically placing rice crackers alongside gluten-free items, tapping into the celiac and keto consumer base. In Canada, a diverse culinary landscape is fueling the popularity of kimchi and sriracha products. Simultaneously, Mexico's economic progress is ushering rice-cake snacks into mainstream grocery outlets. In a strategic move, PepsiCo is channeling its 2026 investment in Kazakhstan to ensure a steady, cost-effective supply stream to U.S. coastal ports, safeguarding against potential trade tensions in East Asia. As a result, North America's trend towards premiumization is expanding the appeal of rice snacks, reaching audiences beyond traditional health-focused consumers.

Europe experiences a more tempered growth, shaped by regulations like HFSS and evolving packaging laws. Leading the charge in volume are Germany, France, and the UK, capitalizing on their dense retail networks to prioritize compliant and recyclable products. Southern European nations, rooted in a snacking culture centered around nuts and olives, are slower to embrace these changes. However, health-conscious consumers are increasingly gravitating towards rice crackers, especially those touting gluten-free benefits. In Eastern Europe, countries like Poland are emerging as potential hotspots, driven by a surge in modern retail and growing disposable incomes. While import restrictions in Turkey and Russia pose challenges, the burgeoning e-commerce landscape offers a glimmer of hope for bridging these access hurdles. On a broader scale, Europe's stringent standards are not just reshaping its own market but are also setting global benchmarks, influencing rice snack formulations worldwide.

Competitive Landscape

The rice snacks market showcases a moderate fragmentation with a balanced mix of global giants and nimble regional players. Companies like PepsiCo, General Mills, and Nestlé leverage their scale in procurement, research and development, and distribution. This breadth allows them to navigate commodity price fluctuations. Meanwhile, regional leaders such as Kameda Seika, Want Want, and Calbee dominate their home markets. They do this through localized flavors, robust distribution networks, and branding that resonates culturally. There's a clear strategic split: while multinationals, like PepsiCo, enhance their demand forecasting accuracy by 18% in 2024 using AI, local firms capitalize on unique textures and festival-themed editions to boost seasonal sales.

Digital changes are challenging traditional gatekeeping. Direct-to-consumer brands, like Lundberg Family Farms, are harnessing rice-bran health claims and compelling narratives to attract early adopters. However, many of these brands grapple with unit economics, prompting them to forge partnerships with co-packers or license their intellectual property to more established entities. The trend of mergers and acquisitions is on the rise, with global firms often taking minority stakes to foster innovation. A case in point is General Mills’ 2025 investment in a California rice-bran startup, signaling a potential full buyout in the future.

Sustainability is becoming a key differentiator. Companies aligning their packaging with EU's circular economy targets are gaining faster shelf space and consumer trust than those lagging behind. As market capabilities evolve, the reallocation of market share will depend on expertise in data-driven personalization, cohesive supply chains, and innovative cycles that adhere to regulations. Additionally, brands that integrate sustainable practices across their value chains are likely to see long-term cost efficiencies. This shift is expected to influence consumer loyalty and drive competitive advantages in the forecast period.

Rice Snacks Industry Leaders

-

PepsiCo Inc.

-

General Mills Inc.

-

Element Snacks Inc.

-

Nestlé S.A. (Osem)

-

Hunter Foods LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: SnackPure has rolled out new chip flavors, featuring brown rice chips. These products prioritize both taste and nutrition, delivering flavorful options devoid of artificial additives.

- July 2025: Ibis Rice has launched bean and rice cakes, delivering a protein and fiber boost in a handy snack. These treats come in two flavors: plain and kelp sea salt.

- March 2025: Kellanova launched Rice Krispies Treats Bliss, offering two enticing flavors: Chocolate Sea Salt Pretzel and Caramel Sea Salt Pretzel. Shoppers can find the product packaged in convenient six-count boxes.

- February 2024: Richy launched the Jinju rice cracker brand, debuting three new flavors: grilled pepper beef with sun-dried tomatoes, milk nuggets, and sweet honey Ganjang.

Global Rice Snacks Market Report Scope

A rice snack is a small portion of food eaten between meals. Rice snack is made with whole grain rice. Rice Snacks are being packaged snack foods or other processed foods, among other shapes and sizes. The Rice Snacks Market is segmented by type into rice cakes, rice crisps, rice crackers, and other types. By distribution channel into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, market sizing and forecasts have been done on the basis of value (USD million) and volume(Tons).

| Rice Cakes |

| Rice Crisps |

| Rice Crackers |

| Others |

| Salty |

| Sweet |

| Spicy |

| Others |

| Pouches |

| Bags |

| Boxes |

| Others |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Rice Cakes | |

| Rice Crisps | ||

| Rice Crackers | ||

| Others | ||

| By Flavor | Salty | |

| Sweet | ||

| Spicy | ||

| Others | ||

| By Packaging Type | Pouches | |

| Bags | ||

| Boxes | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the rice snacks market in 2026?

The rice snacks market size is USD 9.19 billion in 2026, with a 6.05% CAGR outlook to 2031.

Which product type leads sales?

Rice cakes generated the highest 2025 revenue share at 33.02%, benefiting from diet-friendly positioning.

What region is growing fastest?

North America posts the highest regional CAGR at 7.43% due to gluten-free adoption and e-commerce reach.

Why are flexible pouches so popular?

Pouches deliver reseal ability, lower material usage, and recyclable options that meet retailer sustainability mandates.