Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 102.44 Billion |

| Market Size (2031) | USD 253.94 Billion |

| Growth Rate (2026 - 2031) | 19.91% CAGR |

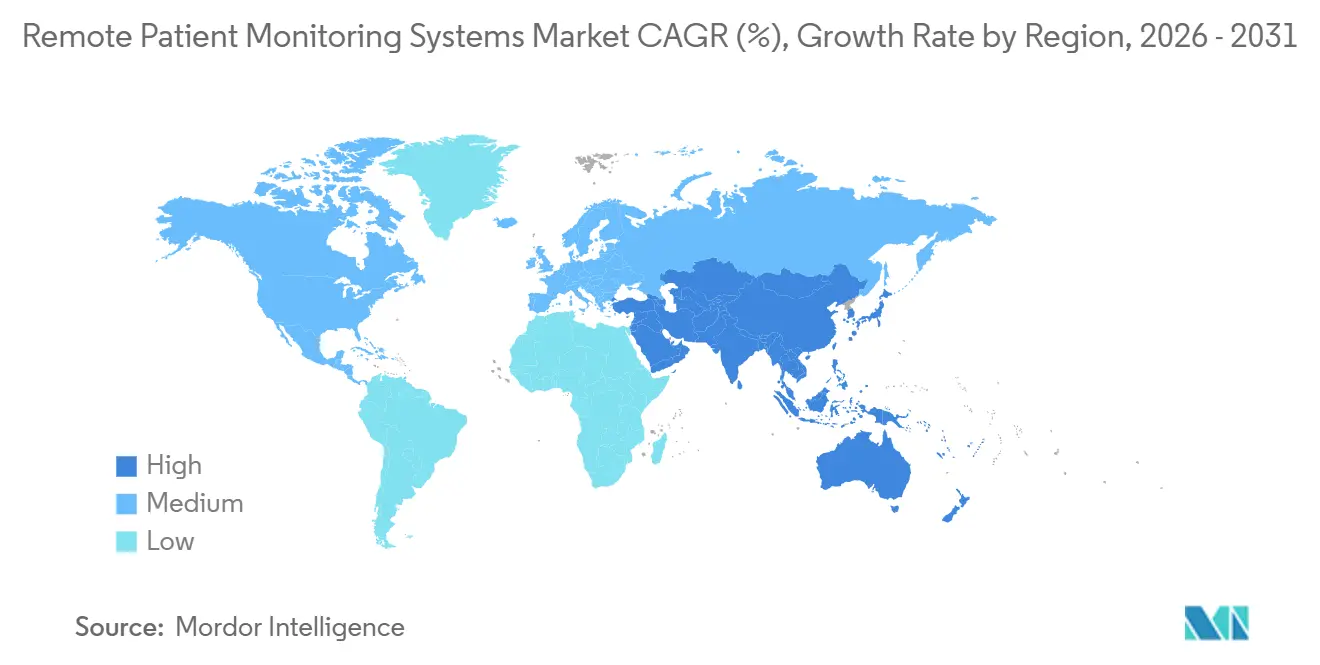

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

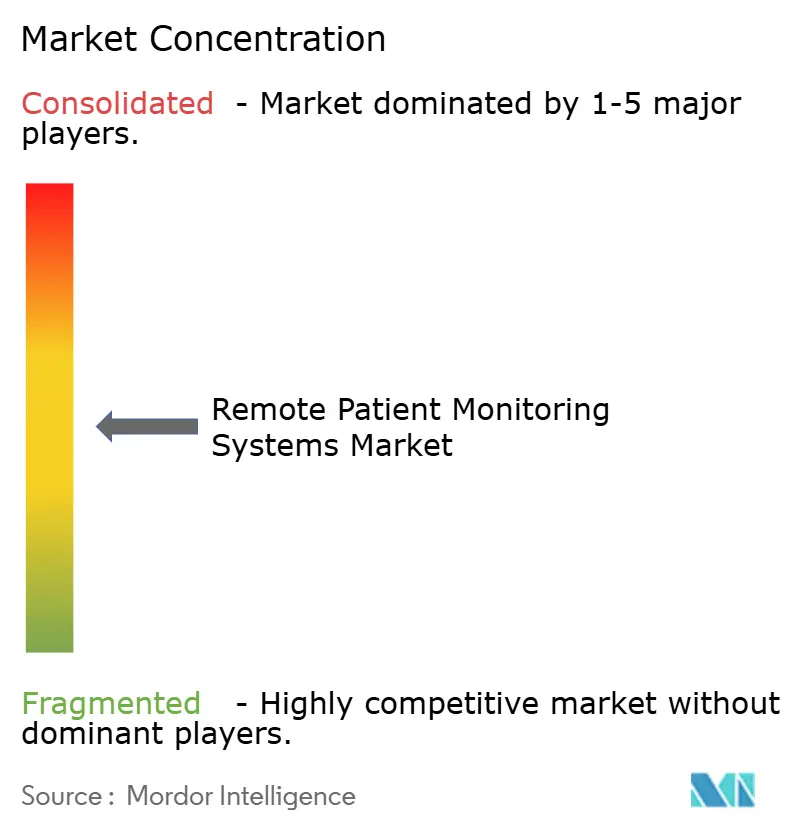

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Remote Patient Monitoring Systems Market Analysis by ���ϲ�����

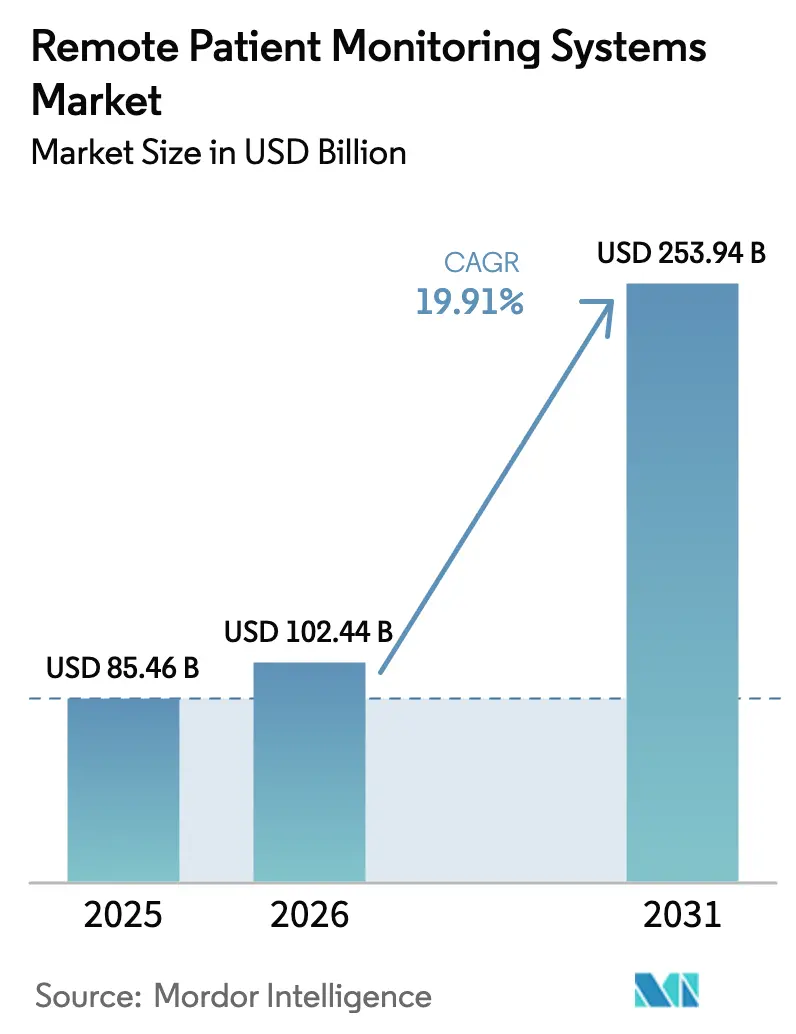

The Remote Patient Monitoring Systems Market size is expected to increase from USD 85.46 billion in 2025 to USD 102.44 billion in 2026 and reach USD 253.94 billion by 2031, growing at a CAGR of 19.91% over 2026-2031.

Growing reimbursement coverage, sensor miniaturization, and value-based care incentives are propelling device adoption in both acute and chronic-care pathways. Providers now deploy predictive algorithms that flag early decompensation, cutting readmission penalties and freeing scarce inpatient capacity. Consumer-electronics companies are entering with lower-priced, FDA-cleared wearables that blend lifestyle and clinical features, broadening the addressable user base. Simultaneously, private 5G networks are shrinking transmission latency, enabling near-instantaneous arrhythmia alerts in intensive-care telemetry. Cybersecurity threats and data-localization rules temper momentum but have not derailed capital flows into home-based surveillance platforms.

Key Report Takeaways

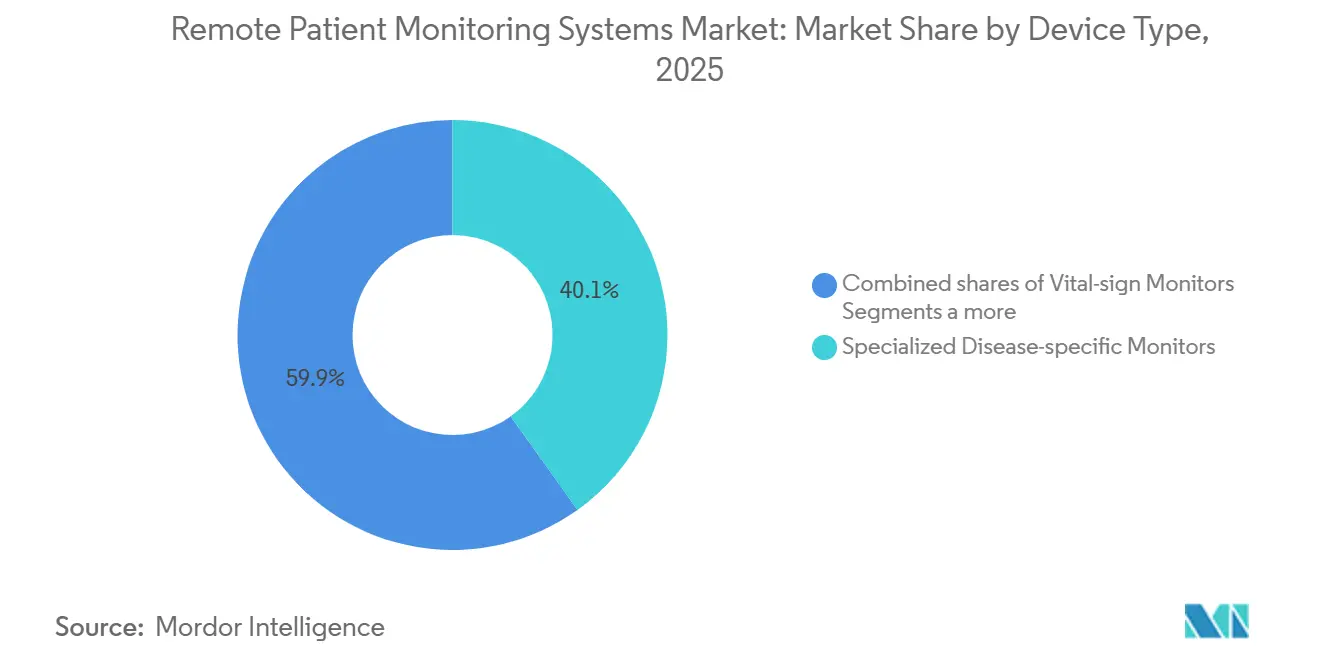

- By device type, specialized disease-specific monitors held 40.12% of the remote patient monitoring system market share in 2025, while wearable sensor patches are advancing at a 20.11% CAGR through 2031.

- By application, cardiovascular diseases led with 30.11% of 2025 revenue; diabetes management is projected to expand at a 20.45% CAGR to 2031.

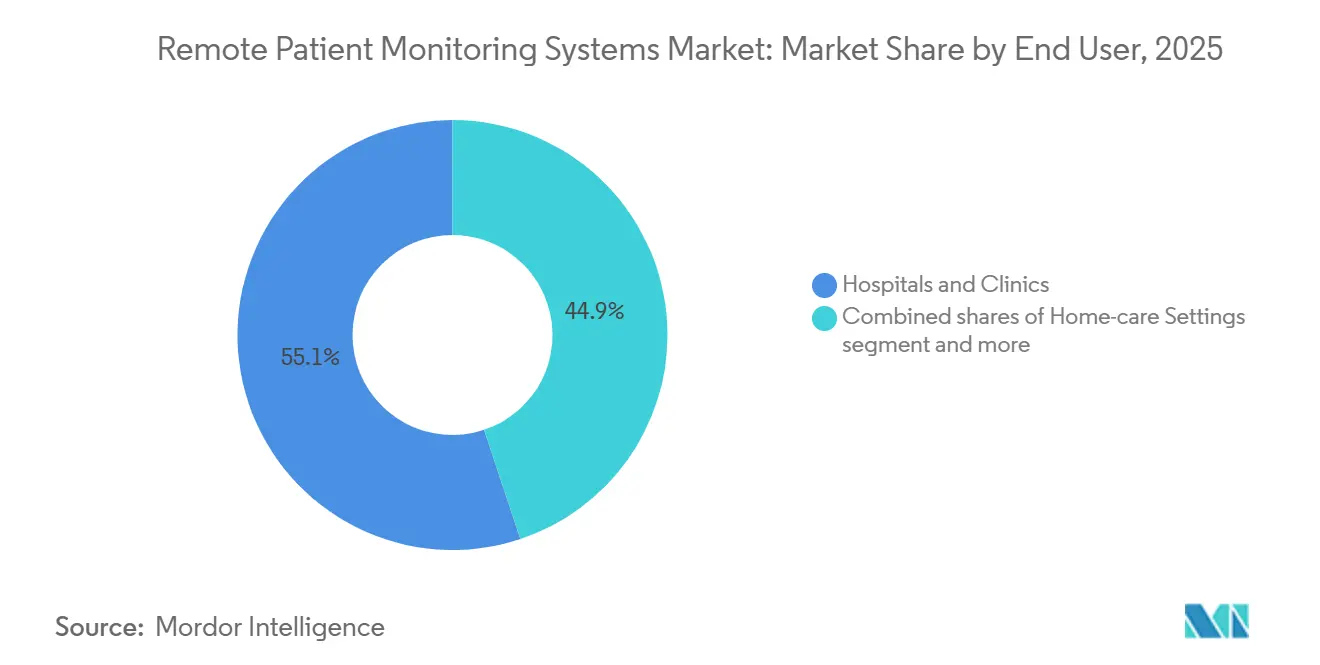

- By end user, hospitals and clinics captured 55.12% share of the remote patient monitoring system market size in 2025, yet home-care settings are rising at a 22.12% CAGR through 2031.

- By geography, North America accounted for 41.22% of revenue in 2025, whereas Asia-Pacific is forecast to grow at 21.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Remote Patient Monitoring Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic-Disease Burden Escalation | +3.2% | Global, peak in North America and Europe | Long term (≥ 4 years) |

| Geriatric Population and Home-Care Shift | +4.1% | Japan, Germany, United States | Medium term (2-4 years) |

| AI-Based Digital Biomarkers | +2.8% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Private 5G Hospital Campuses | +1.5% | North America, select EU and APAC hospitals | Short term (≤ 2 years) |

| Favorable Reimbursement Expansion | +3.6% | Primarily North America, emerging in Europe | Short term (≤ 2 years) |

| Post-COVID Telehealth Normalization | +2.9% | Global, sustained in North America and Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Chronic-Disease Burden Escalation

Cardiovascular disease and diabetes now claim over 18 million lives per year, costing high-income economies USD 1.2 trillion annually [1]World Health Organization, “Global Health Estimates 2025,” who.int. Remote patient monitoring platforms convert episodic check-ups into continuous oversight, catching deterioration before a critical event. A 2024 Lancet Digital Health study showed a 33% drop in heart-failure admissions and USD 8,200 savings per patient when implantable pulmonary sensors were used. The Centers for Disease Control confirmed in 2025 that 60% of U.S. adults live with at least one chronic condition, up nine points in five years. Payers are therefore tying reimbursement to outcome metrics, rewarding providers that deploy remote surveillance to prevent emergency episodes. As a result, the Remote patient monitoring system market is tightly coupled to chronic-disease prevalence trends.

Geriatric Population and Home-Care Shift

The world already counts 761 million people aged 65+ and will reach 1.6 billion by 2050. Long-term-care facilities operate at 94% occupancy in the United States, leaving scant surge capacity. Medicare’s Hospital-at-Home waiver, extended to December 2026, enables acute-level treatment in residences, provided continuous telemetry meets Joint Commission standards. JAMA Network Open documented a 19% decline in 30-day readmissions and 24% episode-cost savings using home-based RPM kits. This demographic and policy convergence accelerates migration of care from wards to living rooms, further lifting the Remote patient monitoring system market.

AI-Based Digital Biomarkers Enabling Predictive RPM

In 2025 the FDA granted Breakthrough Device designation to 12 AI-powered RPM algorithms that predict sepsis or arrhythmia hours before clinical symptom onset. Abbott’s BinaxNOW CardioSense flags atrial fibrillation with 94% sensitivity by fusing ECG with neural-network analytics. Philips’ HealthSuite now ingests feeds from 4.2 million devices, auto-stratifying patients into risk quintiles in the cloud. Edge processors embedded in patches execute inference locally, ensuring sub-second notification without relying on cloud round-trips. These innovations strengthen payer confidence and accelerate recurring-revenue models within the Remote patient monitoring system market.

Private 5G Hospital Campuses Reducing Latency

Cleveland Clinic achieved sub-10 millisecond latency for ICU telemetry after switching to a private 5G network in 2025. Wi-Fi jitters previously delayed arrhythmia alerts by up to 150 milliseconds. The FCC’s CBRS auction made mid-band spectrum affordable for 80 U.S. hospitals by mid-2025. Mayo Clinic reported a 22% improvement in code-blue response times using 5G-enabled remote ICUs. Performance gains reduce clinical risk, validating the network investments that underpin the Remote patient monitoring system market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Cybersecurity Concerns | -2.3% | Global, acute in North America and EU | Medium term (2-4 years) |

| Interoperability and Integration Costs | -1.9% | Global, most severe in fragmented U.S. EHR landscape | Long term (≥ 4 years) |

| Tariff and Data-Localization Cost Inflation | -1.2% | APAC, MEA, South America | Short term (≤ 2 years) |

| Device Fatigue and Patient Adherence | -1.6% | Global, higher among younger demographics | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Data-Privacy and Cybersecurity Concerns

Ransomware events affecting U.S. providers jumped 45% year on year, with 725 incidents logged in 2025 [2]HHS Office for Civil Rights, “Breach Portal,” hhs.gov. Change Healthcare’s 2024 breach exposed data for 100 million individuals, underscoring systemic vulnerabilities. The EU imposed a EUR 1.2 billion fine on a multinational EHR vendor in 2025 for inadequate encryption. To regain trust, vendors must fund multifactor authentication and zero-trust architectures, adding 18–22% to per-device costs. Regulatory friction slows deployments and dents growth for the Remote patient monitoring system market.

Interoperability and Integration Costs

Only 38% of U.S. hospitals achieved seamless HL7 FHIR flows between RPM platforms and EHRs in 2025. Integration projects exceed USD 500,000 per system, straining mid-tier provider budgets. HIMSS surveys rank data exchange as the top barrier to RPM adoption for 62% of IT leaders. Fragmented schemas force clinicians to toggle screens, undermining workflow efficiency and tempering the expansion of the Remote patient monitoring system market.

Segment Analysis

By Device Type: Wearable Patches Reshape Monitoring Paradigm

Specialized disease-specific monitors held a 40.12% remote patient monitoring system market share in 2025 [3]VitalConnect, “Investor Presentation 2025,” vitalconnect.com. Wearable patches are on track for a 20.11% CAGR, driven by 14-day skin-safe adhesives and Bluetooth Low Energy radios that eliminate bulky transmitters. Abbott’s Lingo integrates continuous glucose, lactate, and ketone sensing in a 2 mm patch, avoiding finger-stick calibrations. Multi-parameter monitors cover vital signs for post-surgical home recovery, whereas vital-sign bedside units face margin compression as care migrates home. Implantables like Medtronic’s LINQ II capture long-term arrhythmia data with a 4.5-year battery, securing high reimbursement for cryptogenic-stroke cases.

Consumer familiarity with fitness trackers lowers adoption hurdles for patches. Patients prefer disposable devices that avoid sterilization overheads. Journal of Clinical Monitoring and Computing found ambulatory patches offer comparable accuracy to bedside monitors at one-third the capital cost. Specialized monitors maintain supremacy in epilepsy or advanced cardiology, yet commoditization looms as patches add multi-modal sensors. Multi-parameter devices serve transitional-care scenarios, strengthened by Medicare’s Hospital-at-Home waiver. This product-mix evolution anchors sustained revenue diversification inside the Remote patient monitoring system market.

By Application: Diabetes Algorithms Outpace Cardiac Incumbents

Cardiovascular monitoring generated 30.11% of 2025 revenue, but diabetes management is projected for a 20.45% CAGR through 2031. Dexcom’s G7 achieved an 8.1% mean absolute relative difference, shipping 3.2 million sensors in Q4 2025 alone. Respiratory platforms such as ResMed’s AirView served 8.5 million sleep-apnea users in 2025. Oncology RPM monitors chemotherapy side effects, while sleep and mental-health apps employ passive smartphone sensors. Weight-management tools blur consumer and clinical lines; Apple Watch generated over 400,000 AFib notifications in 2025, though only 12% sought follow-up care.

Cardiology enjoys mature reimbursement via CPT 93264, whereas diabetes coverage only broadened in 2024, explaining its faster trajectory. COPD inhaler sensors still lack billing codes, curbing uptake. Oncology and mental-health segments await clearer fee schedules. Yet as predictive algorithms mature, payer recognition is likely expanding the Remote patient monitoring system market size for newer clinical domains.

By End User: Home Settings Capture Institutional Runoff

Hospitals and clinics controlled 55.12% of the remote patient monitoring system market size in 2025, leveraging telemetry in step-down units and accountable-care cohorts. Home-care settings are climbing at 22.12% CAGR, buoyed by the Hospital-at-Home waiver and commercial payer savings of 24% per episode recorded by Humana. Ambulatory centers serve rehabilitation and skilled-nursing populations that need oversight without full admission. The Joint Commission now mandates 15-minute escalations for critical alerts, a bar that 24/7 command centers meet through nurse staffing.

An AARP survey shows 87% of U.S. seniors prefer aging in place if safety nets exist. Hospitals respond with “hospital-without-walls” programs that ship RPM kits within 24 hours of discharge. Ambulatory clinics rely on RPM to protect capitated payments by pre-empting emergency visits. Long-term-care centers extend limited nursing ratios via remote vitals oversight. Collectively, these shifts cement home and community sites as the fastest-growing node of the Remote patient monitoring system market.

Geography Analysis

North America captured 41.22% of 2025 revenue, propelled by Medicare’s expanded codes and the VA commitment to universal RPM by 2027. Twelve million Medicare beneficiaries were enrolled by December 2025, up from 4.8 million two years earlier. Canada earmarked CAD 200 million (USD 148 million) for rural virtual care, including RPM, while Mexico piloted diabetes and hypertension monitoring across 80,000 patients.

Asia-Pacific is forecast to grow at 21.78% CAGR through 2031. China reimburses RPM for hypertension, diabetes, and COPD under its Healthy China 2030 blueprint. India’s Ayushman Bharat Digital Mission connected 200 million citizens to cloud health records by late 2025. Japan allows RPM chronic-care management without clinic visits; South Korea pilots post-stroke surveillance in Seoul and Busan. Australia added telehealth item numbers for RPM in 2024, though reimbursement sits 30% below in-person rates.

Europe held a significant share in 2025. Germany reimburses certified digital health applications, approving over 40 RPM tools by mid-2025. The UK allocated GBP 250 million for remote heart-failure and COPD monitoring. France cleared 12 devices under its connected-medical-device pathway, though integration with the national EHR lags. GCC states such as the UAE launched a 10,000-patient diabetes pilot in 2025, indicating early traction. Infrastructure gaps and limited reimbursement restrain broader MEA and South American adoption, but multi-lateral development loans targeting digital health could unlock latent demand, bolstering the Remote patient monitoring system market over the long term.

Competitive Landscape

The field is moderately fragmented: the top five vendors hold a significant share, while more than 200 competitors address niches from AI analytics to mental-health monitoring. Incumbents enjoy integrated ecosystems covering sensors, gateways, and cloud dashboards, creating switching costs. Yet consumer brands like Apple, with 100 million AFib-enabled watches, now dwarf traditional cardiac-monitor installed bases. Patent filings reflect the arms race; Medtronic filed 47 RPM patents in 2025 versus 23 for startup VitalConnect.

Strategic activity centers on vertical integration and geographic reach. Abbott bought Cardiovascular Systems for USD 890 million in January 2025 to add peripheral-artery disease monitoring. Philips invested USD 420 million in expanding HealthSuite cloud to Singapore and São Paulo, satisfying data-residency mandates. Teladoc and Omron bundle blood-pressure cuffs with virtual primary care, capturing hypertensive users hesitant to visit clinics.

Smaller entrants differentiate via regulatory speed. Biobeat offers cuffless blood-pressure patches cleared for both hospital and ambulatory use, while Current Health supplies hospital-at-home kits through Best Buy. Success increasingly hinges on HL7 FHIR and Continua certifications, now baseline requirements in hospital RFPs. Overall, technology convergence and reimbursement expansion sustain a dynamic Remote patient monitoring system market despite cybersecurity and interoperability headwinds.

Remote Patient Monitoring Systems Industry Leaders

Abbott Laboratories

Medtronic PLC

GE Healthcare

Boston Scientific Corporation

Omron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Biolinq won FDA De Novo clearance for its Shine multi-analyte sensor patch.

- May 2025: Aevice Health announced that its flagship medical device, the AeviceMD, has received U.S. Food and Drug Administration (FDA) 510(k) clearance for use in pediatric patients aged 3 years and above.

- April 2025: Dexcom received FDA approval for a 15-day G7 sensor, extending wear time for users.

Global Remote Patient Monitoring Systems Market Report Scope

As per the scope of the report, Remote Patient Monitoring (RPM) is a transformative healthcare delivery model that utilizes digital technology and Internet of Things (IoT)-enabled devices to collect and transmit medical data from patients in one location to healthcare providers in another.

The remote patient monitoring system market is segmented by device type, application, end user, and geography. By device type, it is segmented into vital-sign monitors, specialized disease-specific monitors, multi-parameter monitors, wearable sensor patches, and implantable sensors. By application, the market is segmented into cardiovascular diseases, diabetes management, respiratory (COPD/asthma), oncology support, sleep & mental-health monitoring, and weight management & fitness. By End users, the market is segmented into hospitals, cardiac centers & clinics, home-care settings, ambulatory surgical centers, and others.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

By Device Type

| Vital-sign Monitors |

| Specialized Disease-specific Monitors |

| Multi-parameter Monitors |

| Wearable Sensor Patches |

| Implantable Sensors |

By Application

| Cardiovascular Diseases |

| Diabetes Management |

| Respiratory (COPD / Asthma) |

| Oncology Support |

| Sleep & Mental-health Monitoring |

| Weight Management & Fitness |

By End-User

| Hospitals & Clinics |

| Home-care Settings |

| Ambulatory Surgical centers |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Vital-sign Monitors | |

| Specialized Disease-specific Monitors | ||

| Multi-parameter Monitors | ||

| Wearable Sensor Patches | ||

| Implantable Sensors | ||

| By Application | Cardiovascular Diseases | |

| Diabetes Management | ||

| Respiratory (COPD / Asthma) | ||

| Oncology Support | ||

| Sleep & Mental-health Monitoring | ||

| Weight Management & Fitness | ||

| By End-User | Hospitals & Clinics | |

| Home-care Settings | ||

| Ambulatory Surgical centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the remote patient monitoring system market today?

The remote patient monitoring system market size stands at USD 102.44 billion in 2026, on track to reach USD 253.94 billion by 2031.

Which segment is expanding fastest within remote patient monitoring?

Wearable sensor patches are the fastest-growing device type, advancing at a 20.11% CAGR through 2031 as users favor lightweight, skin-friendly formats.

Why is diabetes monitoring expected to outpace cardiac applications?

Continuous glucose monitors now carry predictive alerts and full Medicare coverage, fueling a 20.45% CAGR that edges out cardiovascular growth paths.

What factors limit wider adoption of remote monitoring?

Cybersecurity breaches, high EHR-integration costs, and patient device fatigue each subtract multiple percentage points from forecast CAGR

Which regions present the strongest future growth opportunities?

Asia-Pacific leads with a projected 21.78% CAGR through 2031 thanks to new reimbursement in China and large-scale digital-health missions in India.

Page last updated on: