Lab Automation Software Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

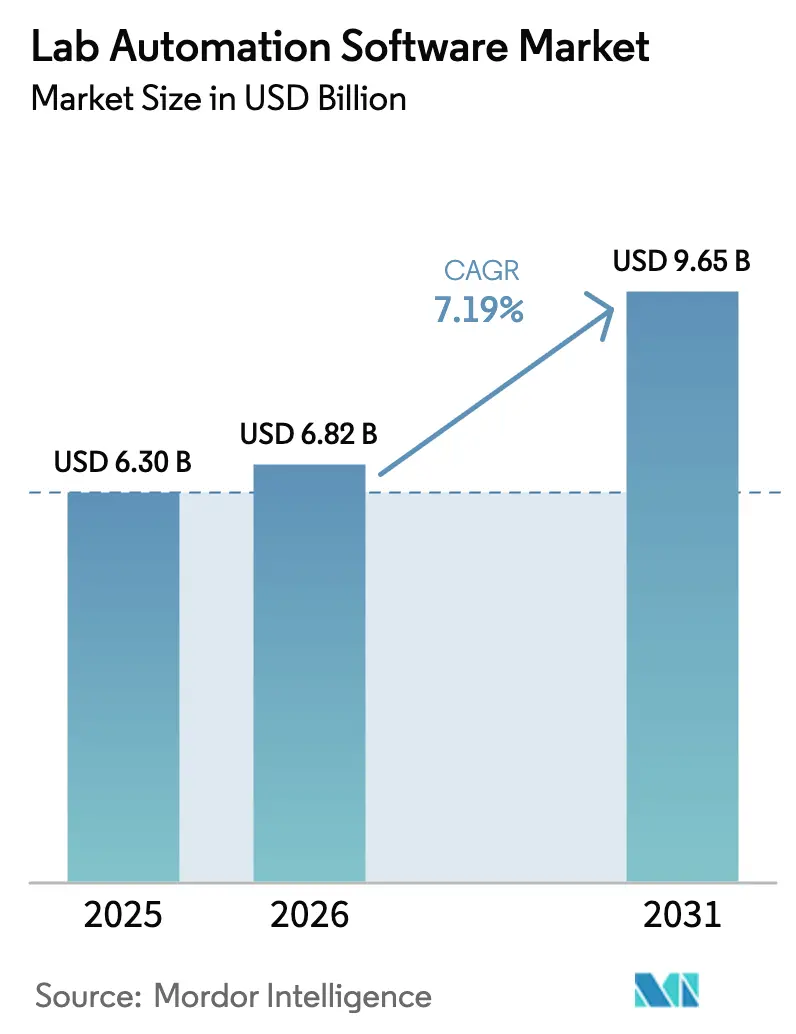

| Market Size (2026) | USD 6.82 Billion |

| Market Size (2031) | USD 9.65 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

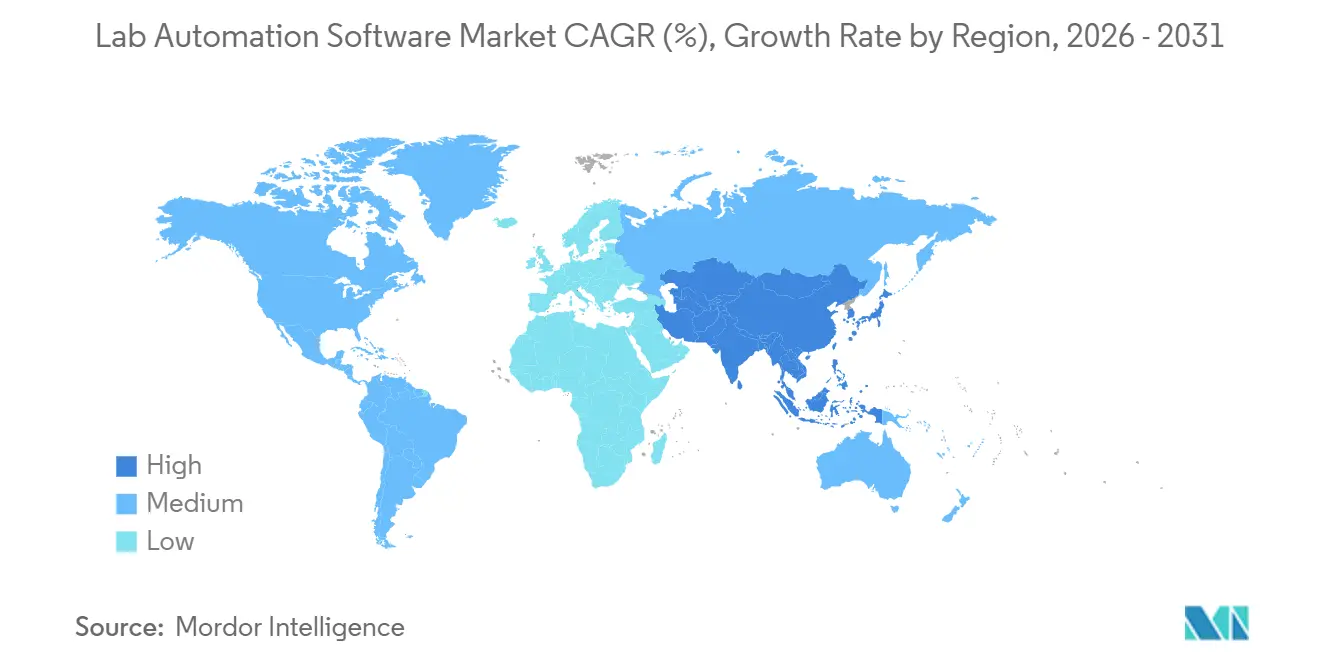

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

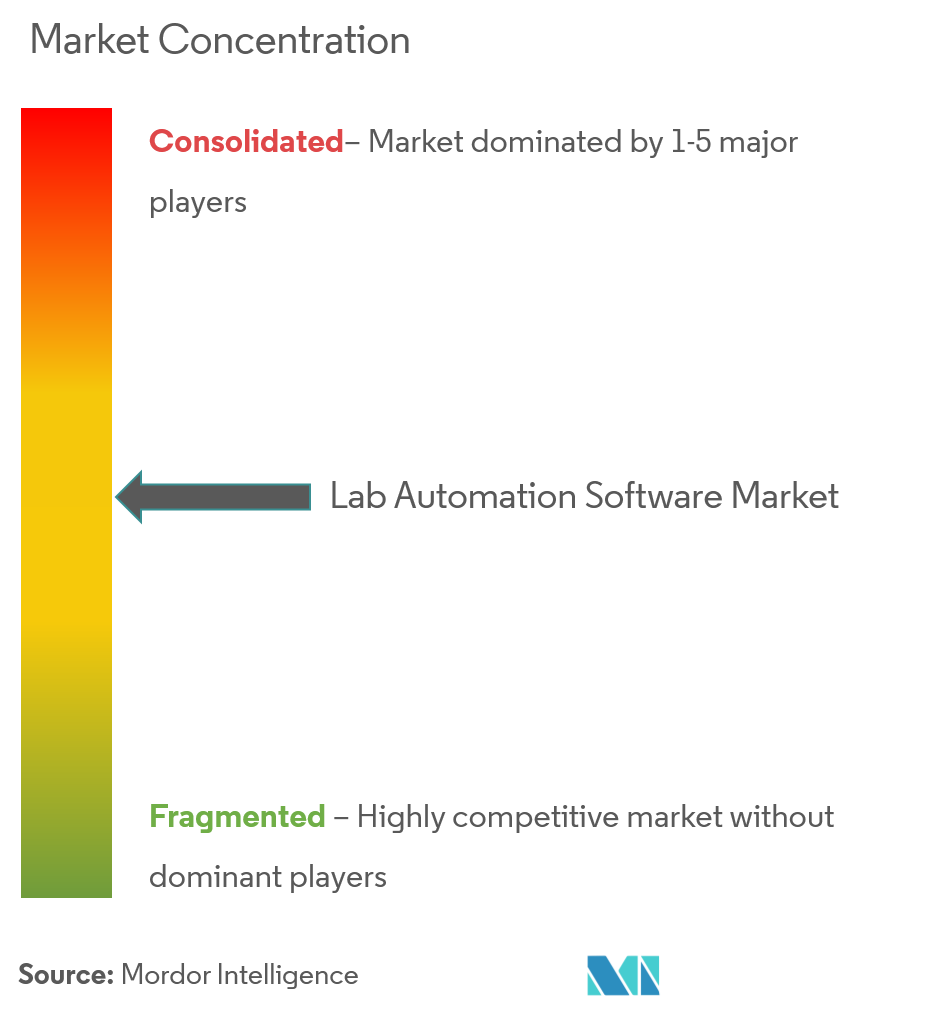

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Lab Automation Software Market Analysis by ���ϲ�����

The Lab Automation Software Market size is projected to be USD 6.30 billion in 2025, USD 6.82 billion in 2026, and reach USD 9.65 billion by 2031, growing at a CAGR of 7.19% from 2026 to 2031. Advancing artificial-intelligence scheduling, cloud-native Laboratory Information Management Systems (LIMS), and stricter electronic-record mandates are shortening research timelines and lowering compliance risk across pharmaceutical, biotechnology, and diagnostic laboratories. Incumbents are embedding generative AI into execution systems to automate sample routing and calibration, while 21 CFR Part 11 rules continue to accelerate the phase-out of paper documentation.[1]U.S. Food and Drug Administration, “21 CFR Part 11 Draft Guidance,” fda.gov Cloud deployments already exceed half of installed LIMS instances, and subscription pricing is convincing contract research organizations (CROs) to modernize multi-site data workflows. Market opportunity also widens as Asia-Pacific CROs attract Western sponsors seeking lower trial costs, and multi-omics integrations demand software capable of orchestrating petabyte-scale datasets.

Key Report Takeaways

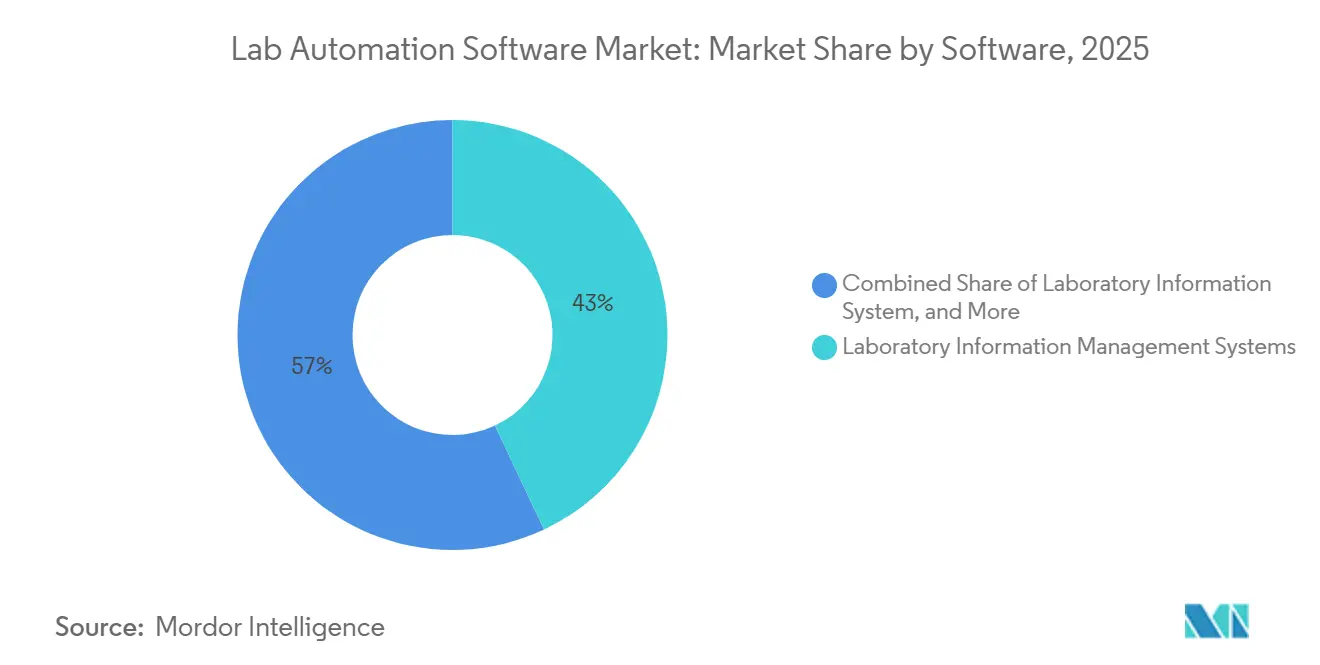

- By software, Laboratory Information Management Systems held 43.00% revenue in 2025 and are forecast to grow at a 13.40% CAGR through 2031.

- By deployment, cloud-based models represented 51.20% of revenue in 2025 and are projected to expand at a 15.20% CAGR through 2031.

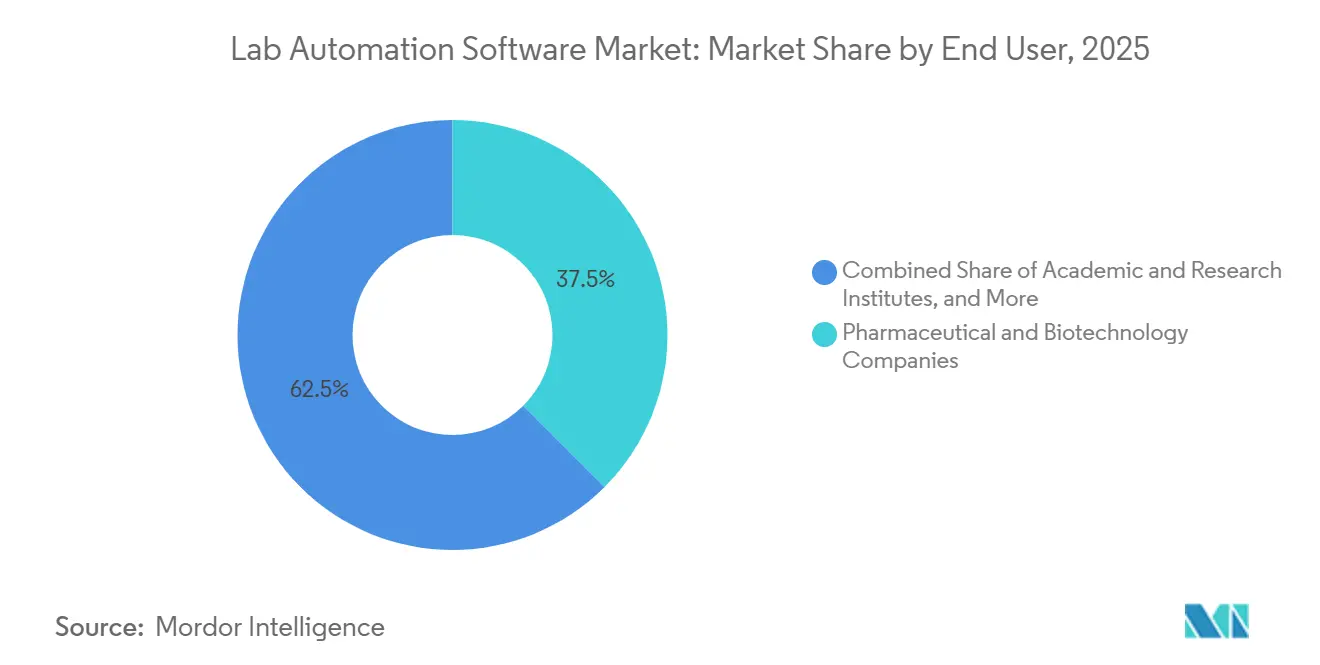

- By end user, CROs are expected to record the fastest 11.80% CAGR to 2031, whereas pharmaceutical and biotechnology companies retained 37.50% share in 2025.

- By application, drug discovery led with 41.80% revenue in 2025, while genomics is poised for the highest 14.90% CAGR through 2031.

- By region, North America commanded 34.00% of 2025 revenue, and Asia-Pacific is anticipated to post a 12.60% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lab Automation Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated AI-Driven Workflow Optimization | +2.1% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Rising Adoption of Cloud-Native LIMS Platforms | +1.8% | Global, led by North America and the Asia-Pacific | Short term (≤ 2 years) |

| Pharma Outsourcing Surge in Emerging Markets | +1.3% | Asia-Pacific core, spillover to the Middle East and Africa | Long term (≥ 4 years) |

| Convergence of Multi-omics and Automation | +1.0% | North America and Europe, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Regulatory Push for Data Integrity (21 CFR Part 11) | +0.6% | North America and Europe | Short term (≤ 2 years) |

| ESG-Linked Funding for Green Laboratories | +0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Accelerated AI-Driven Workflow Optimization

Generative AI now schedules instrument runs, predicts reagent depletion, and flags anomalous peaks before human review, cutting repetitive tasks and improving first-pass yield. Thermo Fisher Scientific integrated large language models across its Unity Lab Services platform in January 2026, allowing researchers to issue natural-language queries and receive protocol recommendations in seconds. Early adopters report protocol-development cycles shrinking by 60% during 2025 beta programs. Ginkgo Bioworks scaled autonomous foundries that iterate strain designs without manual intervention, showing the model’s viability beyond pharmaceuticals. Mid-term benefit peaks once labs validate AI-generated methods under ISO 17025 and CLIA, though definitive regulatory guidance remains forthcoming.

Rising Adoption of Cloud-Native LIMS Platforms

Separating compute from storage lets labs scale resources during heavy sequencing runs and idle them during lulls. A December 2025 TetraScience survey found 68% of biopharma quality-control labs planning at least one cloud migration by end-2026, citing disaster recovery and remote access as top drivers. Kubernetes-orchestrated microservices, introduced in LabVantage LIMS v8.7, enable automated failovers with sub-second queries across multi-terabyte datasets. CROs with global footprints see immediate ROI, as ICON plc reduced cross-site data reconciliation by 40% after deploying cloud-based sample tracking. Sovereign data laws in China and Russia still compel hybrid topologies, creating nuanced architecture decisions.

Pharma Outsourcing Surge in Emerging Markets

Multinational sponsors are shifting preclinical toxicology and early-phase trials to Asia-Pacific to gain budget flexibility and accelerate patient recruitment. WuXi AppTec’s laboratory-services revenue grew 22% year-over-year in 2025 on this trend. India attracted USD 1.8 billion in foreign direct investment during 2025 for GMP-compliant automation laboratories, catalyzed by tax incentives for pharma infrastructure. Charles River Laboratories opened an additional 15,000 square-foot automated facility in Shanghai in August 2025, integrating real-time sponsor portals to shorten decision cycles. Long-term growth stems from large graduate-scientist pools and expanding ICH alignment, lowering validation friction for Western sponsors.

Convergence of Multi-omics and Automation

Genome, proteome, metabolome, and transcriptome data volumes have outgrown manual data-management approaches. Illumina’s NovaSeq X Plus, upgraded in January 2026, outputs up to 16 terabases per run, necessitating automated compression and annotation pipelines. Element Biosciences’ AVITI sequencer links directly to Benchling’s R&D cloud, delivering real-time variant calls and trimming bioinformatics backlog. Oxford Nanopore’s PromethION 2 Solo adds edge base-calling modules, trimming cloud-egress fees, and accelerating infectious-disease surveillance. Labs that automate multi-omics data flows can cut turnaround from weeks to days, a decisive gain for precision-oncology programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Domain-Savvy Automation Engineers | -0.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Data-Security Concerns in Public Cloud Deployments | -0.6% | Global, heightened in Europe and North America | Medium term (2-4 years) |

| High Validation Costs for Regulated Labs | -0.4% | North America and Europe | Medium term (2-4 years) |

| Legacy System Incompatibility with Modern APIs | -0.3% | Global, concentrated in established markets | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Shortage of Domain-Savvy Automation Engineers

BioSpace reported 73% of U.S. biopharma firms unable to fill automation-engineer roles within 120 days during 2025, extending project timelines.[2]BioSpace, “Automation Engineer Talent Report 2025,” biospace.com Skills must span assay protocols, API design, and regulatory statutes such as GAMP 5, creating rare hybrid profiles. Tecan Group launched an internal academy to cross-train technicians in Python scripting and robotic-arm programming. Universities offer limited laboratory-informatics coursework, forcing companies to fund six-to-twelve-month upskilling, slowing near-term software rollouts.

Data-Security Concerns in Public Cloud Deployments

A February 2025 ransomware attack encrypted a European diagnostics network’s patient results and demanded USD 2 million, spotlighting public-cloud vulnerabilities. The HHS updated HIPAA guidance in August 2025, classifying cloud providers as business associates that must sign audit agreements.[3]U.S. Department of Health and Human Services, “HIPAA Cloud Guidance 2025,” hhs.gov Export-control rules such as ITAR and Wassenaar further limit cross-border data storage. Labs increasingly request SOC 2 Type II attestations and penetration tests, extending procurement cycles by up to six months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software: Integrated Ecosystems Redefine Value

Laboratory Information Management Systems accounted for 43.00% of 2025 revenue, anchoring the lab automation software market with validated batch-release workflows in regulated pharma quality-control environments. Cloud-native variants are forecast to expand at a 13.40% CAGR, propelled by CRO demand for elastic capacity and pay-per-sample economics. Electronic lab notebooks and scientific data management systems are converging into unified subscription bundles, as Thermo Fisher’s AI-enriched Unity platform bundles LIMS, ELN, and middleware for one fee. Chromatography data systems remain entrenched, but Waters embedded core CDS functions directly into Arc HPLC firmware to lower standalone license costs. Integrated platforms from ABB and Mettler Toledo link benchtop robotics to enterprise analytics, signaling a shift toward holistic orchestration. These developments create a competitive gradient where established vendors rely on regulatory pedigrees while API-first entrants court cost-sensitive labs. The lab automation software market size for integrated platforms is expected to expand steadily, given their double-digit CAGR and growing preference among multi-omics programs.

Legacy LIS environments in diagnostics are gradually merging with LIMS as molecular pathology blurs research and clinical domains; Roche’s cobas pro automates sample flow from accessioning to report, exemplifying this overlap. Benchling’s ELN advanced version-control features attracted cross-functional discovery teams, especially where fine-grained audit trails are vital. Dotmatics’ machine-learning classifiers auto-tag unstructured datasets, improving knowledge capture in large pharmas. ISO 17025 and CLIA validation continues to favor incumbents with long audit histories, yet pre-validated connectors from startups are eroding traditional switching costs.

By Deployment Model: Cloud Adoption Reshapes Budgets

Cloud deployments held 51.20% revenue in 2025 and are projected to climb at a 15.20% CAGR, marking the fastest shift inside the lab automation software market. Subscription models convert hardware outlays to operational expense, and lab teams rely on built-in redundancy instead of on-premise server rooms. Kubernetes-ready releases such as LabVantage v8.7 illustrate container portability across AWS, Azure, or private data centers. Hybrid topologies, which replicate metadata to the cloud while retaining raw instrument files locally, appeal to jurisdictions enforcing strict data-residency rules. However, data-egress fees emerge as hidden costs; Oxford Nanopore mitigates these by performing edge base calling. The lab automation software market share for on-premise deployments remains sticky in defense and agrochemical labs bound by export-control mandates, yet overall momentum favors cloud incremental migrations.

Rapid cloud validation is another catalyst. Providers now supply pre-qualified instances with 21 CFR Part 11 controls, cutting validation from months to weeks. Nevertheless, the 2025 ransomware breach in Europe forced many labs to require SOC 2 Type II reports and third-party penetration audits before contract signature, elongating sales cycles. Over the forecast period, workload portability and unit-based pricing will tilt even cautious enterprises toward cloud-heavy hybrids.

By End User: CROs Accelerate Adoption Curve

CROs represent the fastest-growing cohort, projected to grow at a 11.80% CAGR through 2031 as big pharma sponsors externalize more discovery and clinical tasks. ICON plc shaved 40% off cross-site reconciliation times with cloud sample tracking, securing more competitive bids. WuXi AppTec’s 22% revenue jump in 2025 underscores the pull of Asia-Pacific capacity. Pharmaceutical and biotechnology companies still account for 37.50% of revenue in 2025, leveraging enterprise LIMS to meet cGMP lot-release obligations. The lab automation software market size for academic institutes grows modestly, constrained by grant cycles, but open-source frameworks like LabKey help bridge budget gaps.

Clinical diagnostics labs automate high-throughput PCR and molecular assays, with BD’s Kiestra middleware linking microbiology data to hospital systems in real time. Smaller food-safety and environmental labs value localized support and ISO 17025 compliance, creating white space for regional vendors. Validation resource scarcity keeps many mid-tier CROs in mixed environments, creating integration consulting opportunities for system integrators.

By Field of Application: Genomics Leads Growth Curve

Drug discovery still dominates revenue at 41.80% in 2025, powered by ultra-high-throughput screens and machine-learning optimization of compound libraries. Yet genomics workflows are forecast to grow at a 14.90% CAGR, the fastest across use cases, as precision oncology and national population genetics initiatives scale. Illumina’s NovaSeq X Plus upgrade positions labs for large-cohort sequencing, while Element Biosciences and Oxford Nanopore address latency and cost barriers for real-time analysis. Proteomics gains momentum from Danaher’s USD 5.7 billion Abcam acquisition, pairing antibody discovery with liquid-handling robotics to deliver integrated protein analytics.

Clinical diagnostics emerges as the third-largest application, automating EGFR and KRAS mutation testing via Roche’s cobas pro system to hasten treatment decisions. Metabolomics and lipidomics remain niche but are increasingly embedded into multi-omics panels aimed at elucidating drug mechanisms. Bio-Rad’s QX ONE droplet digital PCR automates vector copy-number assays crucial for cell and gene therapy manufacturers. ISO 20387 biobank compliance and CLIA requirements continue to favor vendors offering validated instrument connectors.

Geography Analysis

North America held 34.00% of market revenue in 2025, supported by dense biopharma clusters in Boston, San Francisco, and Raleigh. The FDA’s 2025 21 CFR Part 11 update clarified cloud-signature expectations, prompting many legacy LIMS migrations to AWS and Azure. Canada’s National Research Council awarded CAD 50 million (USD 37 million) in grants to help small laboratories automate cleantech and ag-genomics workflows, expanding addressable demand.[4]National Research Council Canada, “Laboratory Automation Grants 2025,” nrc.canada.ca Mexico’s contract-manufacturing hubs have adopted cloud-based LIMS to meet FDA export audit requirements, though rural connectivity gaps still necessitate hybrid installations.

Asia-Pacific is forecast to post a 12.60% CAGR during 2026-2031, the fastest worldwide. China’s National Medical Products Administration certified domestic LIMS vendors with Mandarin interfaces, easing validation for local labs. India’s USD 1.8 billion in FDI inflows into biopharma automation in 2025 reflects policy incentives and a large STEM talent pool. South Korea earmarked KRW 120 billion (USD 90 million) to digitize public health labs, while Japan is pushing clinical automation to manage an aging population. Australia’s draft software-as-medical-device guidance in 2025 opens regulatory pathways for cloud LIMS in diagnostics.

Europe’s outlook is tied to the EU Clinical Trials Regulation, which mandates electronic source-data capture; Germany’s Annex 11 update in 2024 further clarified cloud validation standards, unlocking migrations among Bavarian manufacturers. The United Kingdom now runs a divergent post-Brexit regime, forcing dual-compliant systems among pan-European labs. France allocated EUR 40 million (USD 45 million) to academic automation grants, and Spain’s Catalonia region issued tax credits for AI-enabled bioprocessing. In the Middle East, Saudi Vision 2030 earmarked SAR 2 billion (USD 533 million) for genomics labs that must support Arabic-language LIMS reporting. Africa remains early stage; South Africa’s National Health Laboratory Service piloted cloud chromatography data systems to centralize HIV testing across provinces.

Competitive Landscape

The lab automation software market exhibits moderate concentration: the top five vendors account for roughly 40-45% of global revenue, with no single firm exceeding a 15% share. Instrument makers are vertically integrating into software to capture recurring revenue, as seen in Danaher’s USD 5.7 billion Abcam buyout that merges proteomics data with automated liquid handlers. Thermo Fisher’s January 2026 NVIDIA partnership illustrates a pivot toward algorithmic differentiation over pure hardware. Vendors like Agilent, Siemens Healthineers, and Roche embed informatics in multi-modal instruments, locking customers into proprietary ecosystems.

API-first disruptors Benchling and Dotmatics gain traction in mid-tier CROs and academic labs that view enterprise suites as over-engineered. Open-source foundations such as OpenBIS underlie managed-service offerings that undercut incumbents on price but still monetize through premium support. Regulatory compliance remains a formidable moat; packages with documented change-control records and 21 CFR Part 11 validation scripts shorten audit prep. Yet cloud providers’ pre-qualified environments are diluting this advantage by trimming validation to six weeks.

Patent filings underscore AI’s strategic priority. Thermo Fisher secured 12 U.S. patents in 2024-2025 covering machine-learning models that predict maintenance schedules, improving uptime. Standards groups like the Allotrope Foundation promote vendor-neutral formats to facilitate data portability, potentially commoditizing instrument middleware. Competitive intensity is likely to rise as ESG-linked lab funding in Europe rewards vendors offering energy-efficient orchestration features.

Lab Automation Software Industry Leaders

Thermo Fisher Scientific

Danaher Corporation

Hudson Robotics

Becton Dickinson

Synchron Lab Automation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Thermo Fisher Scientific began a multi-year collaboration with NVIDIA to embed generative AI into Unity Lab Services, enabling natural-language queries and real-time workflow optimization.

- January 2026: Illumina upgraded NovaSeq X Plus chemistry to 16 terabases per run, intensifying demand for automated data pipelines.

- December 2025: Danaher Corporation completed the USD 5.7 billion acquisition of Abcam, integrating antibody discovery with Beckman Coulter robotics.

- October 2025: Agilent Technologies acquired BioTek Instruments for USD 1.165 billion, adding automated microplate readers and imaging systems.

- September 2025: TetraScience survey showed 68% of biopharma QC labs plan at least one LIMS cloud migration by end-2026.

Global Lab Automation Software Market Report Scope

Lab automation software automatically detects any faults or defects and notifies the concerned person to take action. Moreover, it helps in maintaining schedules and lab routines, which can be accessed through the software present for various platforms. Some laboratories have established an integrated end-to-end robotics system that requires software to operate and track maintenance.

The Lab Automation Software Market Report is Segmented by Software (LIMS, LIS, CDS, ELN, SDMS, Integrated Platforms), Deployment Model (On-Premise, Cloud-Based, Hybrid), End User (Pharma and Biotech, CROs, Clinical Diagnostics, Academic Institutes, Others), Field of Application (Drug Discovery, Genomics, Proteomics, Clinical Diagnostics, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Laboratory Information Management System (LIMS) |

| Laboratory Information System (LIS) |

| Chromatography Data System (CDS) |

| Electronic Lab Notebook (ELN) |

| Scientific Data Management System (SDMS) |

| Integrated Automation Platforms |

| On-Premise |

| Cloud-Based |

| Hybrid |

| Pharmaceutical and Biotechnology Companies |

| Contract Research Organizations |

| Clinical Diagnostics Laboratories |

| Academic and Research Institutes |

| Other End Users |

| Drug Discovery |

| Genomics |

| Proteomics |

| Clinical Diagnostics |

| Other Field of Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Software | Laboratory Information Management System (LIMS) | |

| Laboratory Information System (LIS) | ||

| Chromatography Data System (CDS) | ||

| Electronic Lab Notebook (ELN) | ||

| Scientific Data Management System (SDMS) | ||

| Integrated Automation Platforms | ||

| By Deployment Model | On-Premise | |

| Cloud-Based | ||

| Hybrid | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Contract Research Organizations | ||

| Clinical Diagnostics Laboratories | ||

| Academic and Research Institutes | ||

| Other End Users | ||

| By Field of Application | Drug Discovery | |

| Genomics | ||

| Proteomics | ||

| Clinical Diagnostics | ||

| Other Field of Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast growth rate for the lab automation software market to 2031?

The market is projected to grow at a 7.19% CAGR, rising from USD 6.82 billion in 2026 to USD 9.65 billion by 2031.

Which region is expected to expand the fastest through 2031?

Asia-Pacific is expected to expand the fastest through 2031.

Why are CROs adopting automation software more quickly than pharmaceutical sponsors?

CROs pursue automation to shorten study timelines, win more outsourcing contracts, and harmonize data across multi-site labs, resulting in an estimated 11.80% CAGR for this user group.

How is AI affecting purchasing decisions for laboratory software?

Generative AI features that automate scheduling, protocol design, and anomaly detection are becoming key differentiators, leading many buyers to choose platforms with embedded machine-learning capabilities.

What major security concern influences cloud-based LIMS adoption?

High-profile ransomware attacks and evolving HIPAA obligations push laboratories to demand SOC 2 reports, hybrid architectures, and third-party penetration tests before moving sensitive data to public clouds.

Page last updated on: