Gluten Free Prepared Foods Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

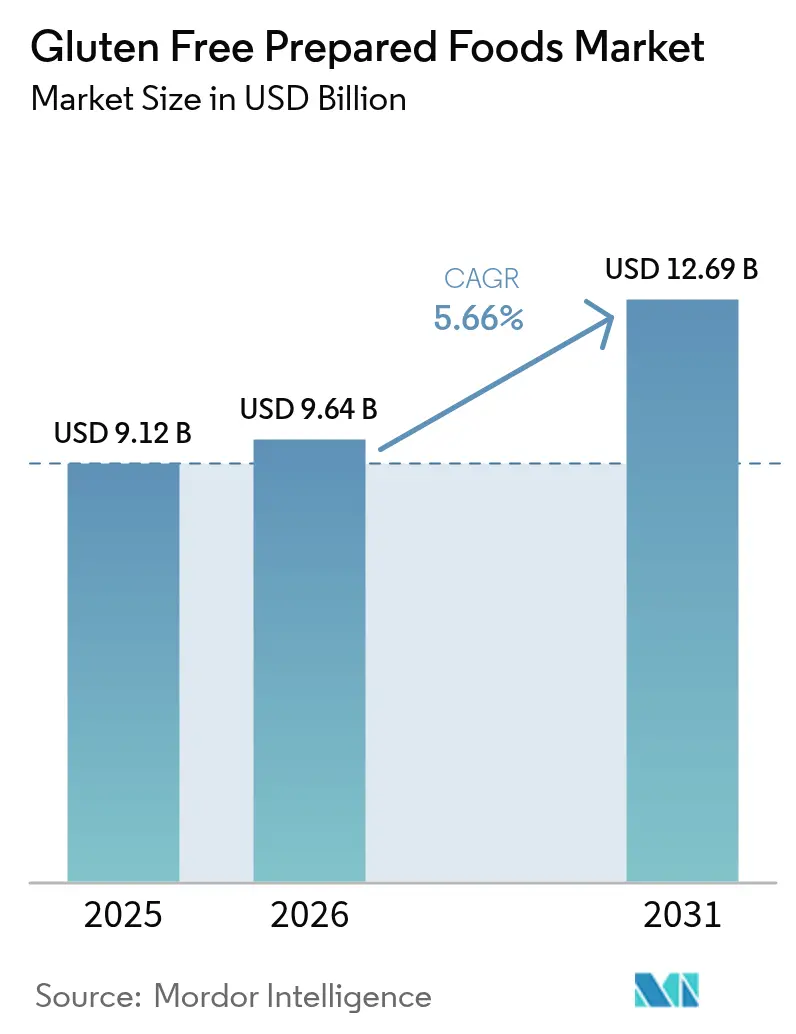

| Market Size (2026) | USD 9.64 Billion |

| Market Size (2031) | USD 12.69 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Gluten Free Prepared Foods Market Analysis by ���ϲ�����

The gluten-free prepared foods market size is steadily expanding, growing from USD 9.12 billion in 2025 to USD 9.64 billion in 2026, and is projected to reach USD 12.69 billion by 2031, with a CAGR of 5.66% during 2026-2031. This growth is primarily driven by the rising diagnosis of gluten-related disorders and increased medical awareness regarding dietary management, which has established a consistent consumer base reliant on certified gluten-free products for daily nutrition. Additionally, the growing demand for convenience foods catering to specific dietary restrictions is a significant factor contributing to market growth. Advances in formulation science and food processing technologies have enhanced the taste, texture, and shelf stability of gluten-free products, reducing the quality gap with traditional foods and fostering repeat purchases.

Key Report Takeaways

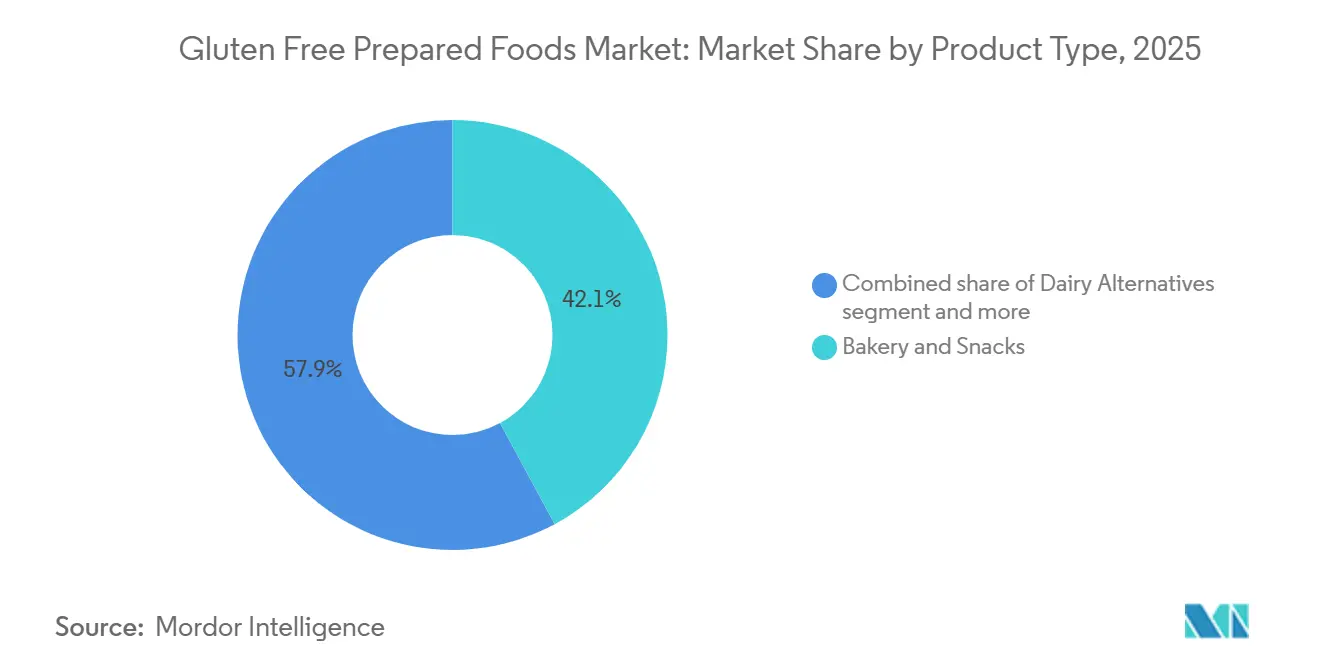

- By product type, Bakery and Snacks led with 42.12% of the gluten-free food market share in 2025, while Ready Meals are forecast to expand at a 6.71% CAGR through 2031.

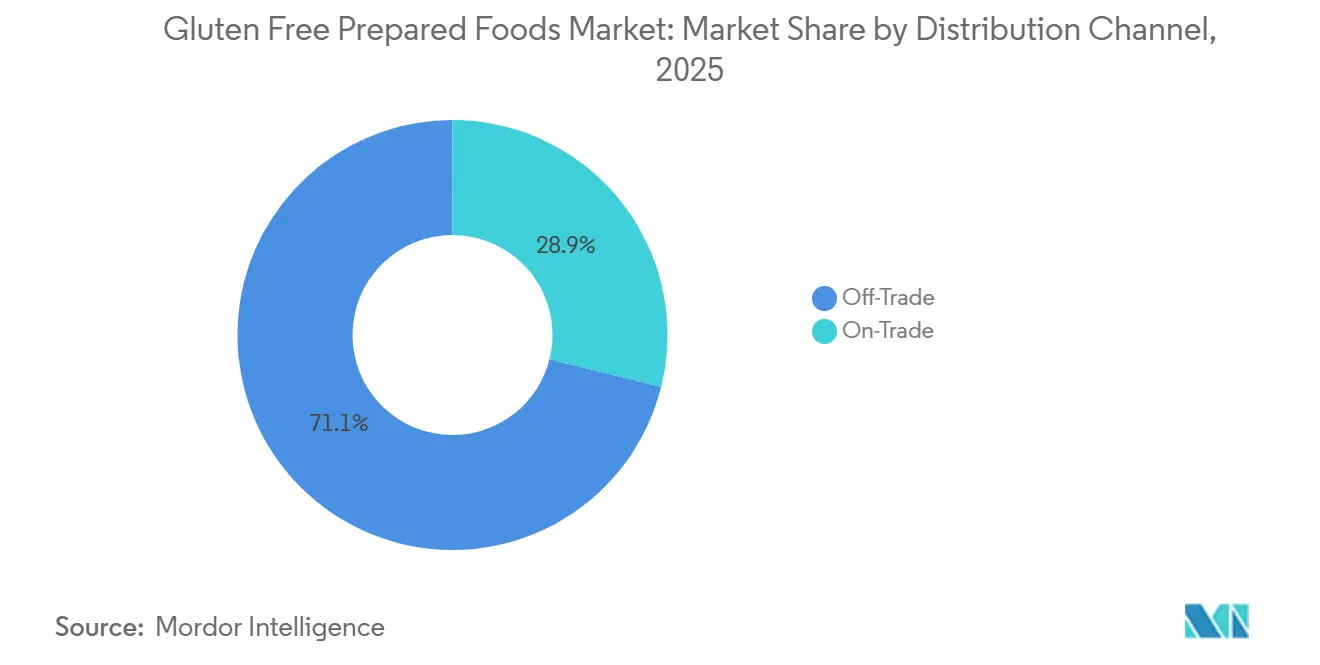

- By distribution channel, Off-Trade held 71.12% of the gluten-free food market size in 2025, whereas On-Trade is advancing at a 5.75% CAGR through 2031.

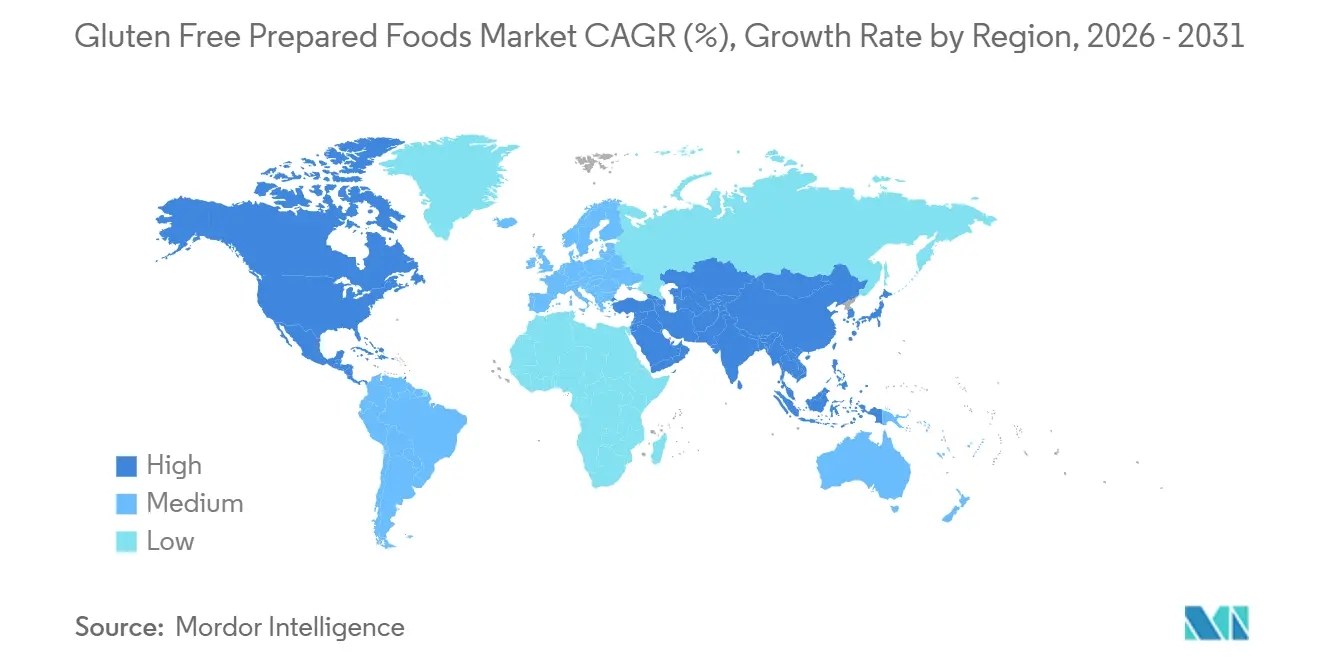

- By geography, North America accounted for 38.18% of 2025 revenue, while Asia-Pacific is projected to grow at a 6.58% CAGR between 2026 and 2031

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gluten Free Prepared Foods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of celiac disease | +0.8% | Global, with acute impact in North America and Europe | Long term (≥ 4 years) |

| Health and wellness lifestyle adoption | +1.2% | Global, led by North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Demand for convenient ready-to-eat meals | +1.0% | North America and Europe core, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Product innovation and improved taste and texture | +0.9% | Global, with Research and Development (R&D) concentration in North America and Europe | Short term (≤ 2 years) |

| Technological advancements in gluten-free food processing | +0.7% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Expansion of clean-label and allergen-free trends | +0.6% | North America and Europe, spillover to Asia-Pacific premium segments | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising prevalence of celiac disease

The rising prevalence and diagnosis of celiac disease are key drivers of the global gluten-free prepared foods market. Individuals diagnosed with this condition must strictly and permanently avoid gluten to prevent intestinal damage and long-term health complications. Unlike lifestyle-based dietary choices, this necessity creates a consistent and non-substitutable demand for certified gluten-free prepared foods, as patients rely on safe, clearly labeled products for daily dietary management. For example, according to Beyond Celiac, approximately 1 in 133 Americans has celiac disease, representing a significant consumer base requiring gluten-free products as a medical necessity [1]Source: Beyond Celiac, "Celiac Disease: Fast Facts", beyondceliac.com. This sustained demand supports continuous market growth, as gluten-free prepared foods are essential for maintaining health and preventing complications, thereby driving the expansion of the global gluten-free prepared foods market.

Health and wellness lifestyle adoption

The increasing adoption of health- and wellness-focused eating habits is driving the market, as consumers increasingly associate gluten-free diets with digestive comfort, clean eating, and preventive health management. A notable segment of consumers now purchases gluten-free foods without a diagnosed medical condition, incorporating them into broader lifestyle choices such as clean-label eating, weight management, and gut-health awareness. This trend extends the market beyond consumers with medical restrictions, fostering higher product trials, repeat purchases, and deeper category penetration across everyday packaged meals and snacks. For instance, according to IfD Allensbach, approximately 2.23 million people in Germany purchased gluten-free products in 2025, compared to 2.16 million in 2024, reflecting a growing voluntary adoption rather than solely medical consumption [2]Source: IfD Allensbach, "Number of people in Germany who bought gluten-free products ", ifd-allensbach.de. This lifestyle-driven demand plays a significant role in market growth, as gluten-free prepared foods transition from a specialized dietary need to a mainstream health and wellness category.

Demand for convenient ready-to-eat meals

The growing demand for convenience foods is driven by consumers seeking meal solutions that require minimal preparation while adhering to strict dietary restrictions. Individuals following gluten-free diets often encounter challenges in home cooking, such as scrutinizing ingredient lists, avoiding hidden gluten sources, and preventing cross-contact during preparation. Ready-to-eat and heat-and-serve gluten-free meals address these issues by providing safe, pre-formulated products with verified labeling. These options enable consumers to save time while maintaining dietary compliance. This convenience is particularly significant for working professionals, students, and households looking for quick meal solutions without compromising health requirements. In response, manufacturers are expanding their product portfolios to include frozen and shelf-stable options, supported by advanced preservation technologies, clear allergen labeling, and dedicated gluten-free production practices.

Product innovation and improved taste and texture

Continuous product innovation and improvements in sensory quality are key factors driving the global gluten-free prepared foods market. Earlier gluten-free products were often criticized for being dry, dense, or crumbly due to the absence of gluten’s natural binding and elasticity. To address this, food manufacturers are utilizing alternative flours such as rice, sorghum, and pulse-based ingredients, along with specialized processing techniques, to better replicate the structure, softness, and mouthfeel of conventional products. Advances in formulation science, including optimized fat systems, starch blends, and moisture-retention technologies, have significantly reduced the quality gap between gluten-free and traditional foods. This has enhanced consumer satisfaction and encouraged repeat purchases. For example, in January 2026, Tate’s Bake Shop expanded its gluten-free cookie line by introducing products made with rice flour, butter, and chocolate. These cookies are also nut-free, produced in a dedicated gluten-free facility, and certified by the Gluten-Free Food Program.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher product prices than conventional foods | -0.9% | Global, most acute in price-sensitive Asia-Pacific and South America | Short term (≤ 2 years) |

| Taste and texture limitations | -0.6% | Global, with higher impact in foodservice/on-trade applications | Medium term (2-4 years) |

| Risk of cross-contamination during processing | -0.4% | Global, particularly in shared-facility environments | Long term (≥ 4 years) |

| Strict regulatory labeling requirements | -0.3% | North America and Europe, with emerging impact in Asia-Pacific | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Higher product prices than conventional foods

Higher pricing compared to conventional foods remains a significant restraint on the gluten-free prepared foods market. Gluten-free products necessitate specialized raw materials, including rice flour, sorghum, millet, quinoa, and pulse-based ingredients, which require careful processing and handling to avoid contamination. Additionally, manufacturers often utilize dedicated production lines, enforce stringent cleaning protocols, and conduct regular gluten testing to comply with certification standards. These additional manufacturing and quality assurance measures increase production complexity and drive up overall product costs. Consequently, gluten-free prepared foods generally have a noticeable price premium, deterring frequent purchases, especially among consumers without a medical necessity for a gluten-free diet. The higher cost also limits impulse buying and reduces product trial among new consumers, slowing mainstream adoption.

Taste and texture limitations

Taste and texture challenges continue to act as significant restraints in the global gluten-free prepared foods market. Gluten serves an essential functional role in conventional foods by providing elasticity, structure, and moisture retention. In its absence, many products face difficulties in achieving comparable softness, chewiness, and volume, often resulting in crumbly, dry, or dense textures. Despite advancements in formulation techniques, some consumers still perceive gluten-free baked and prepared foods as less satisfying than their traditional counterparts. This perception can hinder repeat purchases and long-term brand loyalty. Manufacturers have sought to address these issues by incorporating starch blends, gums, and protein additives. However, these alternatives do not always fully replicate the sensory qualities of wheat-based products and may sometimes alter flavor profiles. Consequently, first-time consumers may try gluten-free prepared foods but often return to conventional options unless they have specific dietary restrictions.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready Meals Drive Innovation Beyond Traditional Bakery

The bakery and snacks segment, which accounted for 42.12% of global gluten-free prepared foods revenue in 2025, is a primary driver of the market. This is due to the essential role of gluten replacement in this category, where its absence is most noticeable. Conventional baked goods rely heavily on wheat flour for structure, elasticity, and volume. Consequently, consumers adopting gluten-free diets actively seek suitable alternatives, generating consistent and recurring demand. Manufacturers have addressed this demand by advancing formulations using rice flour, sorghum, millet, corn, buckwheat, and pulse-based ingredients. These are combined with hydrocolloids and plant proteins to replicate gluten functionality, significantly enhancing softness, shelf stability, and overall palatability compared to earlier products.

The ready meals segment, projected to grow at a 6.71% CAGR through 2031, is one of the fastest-growing areas in the gluten-free prepared foods market. This growth is fueled by increasing consumer demand for complete meal solutions that adhere to strict dietary restrictions without requiring home preparation. Individuals following gluten-free diets often face challenges in preparing safe meals due to the risk of accidental gluten exposure during ingredient handling and cooking. Professionally manufactured, clearly labeled ready meals provide a trusted alternative. To meet this demand, food manufacturers are investing in dedicated gluten-free production lines, certified facilities, and rigorous testing protocols. These measures ensure product safety and reliability, strengthening consumer confidence and encouraging repeat purchases.

By Distribution Channel: On-Trade Acceleration Signals Foodservice Transformation

The off-trade distribution channel accounted for 71.12% of gluten-free prepared foods sales in 2025. This channel drives the market as consumers managing gluten-related dietary restrictions prefer controlled and transparent purchasing environments. Retail outlets, including supermarkets, hypermarkets, health food stores, pharmacies, and online grocery platforms, provide detailed ingredient lists, allergen declarations, and certified gluten-free labeling. These features enable buyers to confidently evaluate products and avoid accidental gluten exposure. Additionally, shelf merchandising in dedicated free-from or health aisles enhances product visibility, simplifies comparisons, and encourages brand switching and trials of new products.

The on-trade distribution channel is projected to grow at a 5.75% CAGR through 2031, gaining significance in the gluten-free prepared foods market. Foodservice operators are increasingly offering diet-specific menu options to cater to consumers with medically necessary or lifestyle-driven dietary restrictions. Restaurants, cafés, quick-service chains, and institutional catering providers are expanding gluten-free menus and implementing standardized preparation procedures, such as separate cooking surfaces, dedicated utensils, and ingredient verification protocols, to minimize cross-contact risks and build consumer trust. This segment's growth is further supported by the global expansion of the foodservice industry. For instance, the United States Department of Agriculture (USDA) reported foodservice outlet sales reaching USD 1.52 trillion in 2024, reflecting rising menu diversification and greater accommodation of special dietary needs [3]Source: United States Department of Agriculture (USDA), "Food Service Industry", usda.gov.

Geography Analysis

In 2025, North America accounted for 38.18% of global gluten-free prepared foods sales, making it the leading regional market. This dominance is attributed to strong clinical awareness and well-established dietary management practices. The region has a high diagnosis rate of gluten-related disorders, supported by healthcare professionals, dietitians, and patient advocacy groups, which promotes long-term adherence to gluten-free diets. Clear labeling standards, extensive third-party certification programs, and high retailer participation enable consumers to easily identify compliant products, boosting purchasing confidence and repeat consumption. Additionally, manufacturers in the region frequently launch new formulations with improved taste, fortified nutrition profiles, and clean-label positioning. Retailers further support the market by dedicating specific free-from sections, enhancing product visibility, and encouraging trials.

Asia-Pacific is the fastest-growing region, expanding at an annual growth rate of 6.58%. Awareness of digestive health and food intolerance is rapidly improving among urban populations. Factors such as increasing diagnoses of wheat sensitivity, changing dietary habits, and greater exposure to global health trends are driving consumers to explore specialized diets. The region benefits from the traditional consumption of naturally gluten-free grains like rice and millet, simplifying product formulation for manufacturers and ensuring cultural acceptance among consumers. Local producers are introducing regionally adapted gluten-free prepared meals and snacks, while the expansion of modern retail and e-commerce platforms is improving accessibility and consumer education.

Europe's gluten-free prepared foods market is strongly influenced by its structured regulatory environment and certification frameworks, which enhance consumer trust. Strict gluten-free labeling thresholds and standardized allergen disclosure rules encourage manufacturers to maintain compliance and consistent quality. In the United Kingdom, certification programs supported by national health guidance significantly contribute to market adoption. For instance, Coeliac UK, whose accreditation is recognized by the National Health Service, reports that over 3,000 food venues in the country are gluten-free accredited. South America is experiencing a gradual adoption of gluten-free prepared foods as awareness of food intolerances and digestive health increases, particularly in urban centers. In the Middle East, demand is primarily driven by growing dietary awareness, expanding modern retail infrastructure, and the rising importance of certified specialty foods.

Competitive Landscape

The gluten-free prepared foods market is moderately fragmented, featuring both specialized free-from manufacturers and large diversified packaged-food companies. Gluten-free specialists emphasize certification, formulation expertise, and building brand trust, while multinational food corporations utilize large-scale manufacturing, procurement capabilities, and global distribution networks to expand their market presence. Key players in the market include Dr. Schär AG, General Mills, Inc., The Hain Celestial Group, Inc., The Kraft Heinz Company, and Conagra Brands, Inc. Competition in the market is shaped by a dual structure: specialists focus on medical credibility and product authenticity, while large food manufacturers compete on pricing, shelf presence, and product variety across multiple prepared food categories.

A significant strategic development in the industry is the shift by multinational conglomerates to integrate gluten-free formulations into mainstream product portfolios. Rather than treating gluten-free as a niche health segment, companies are reformulating existing products and launching gluten-free variants under established core brands. This strategy helps retain brand loyalty among consumers with dietary restrictions while attracting health-conscious shoppers. Retailers are also contributing to this trend by expanding private-label gluten-free prepared food offerings, intensifying competition for both premium specialist brands and branded packaged-food manufacturers. Consequently, differentiation is evolving beyond basic free-from labeling to include factors such as taste, nutritional fortification, clean-label ingredients, and broader dietary compatibility, including plant-based and allergen-friendly options.

Technology plays a critical role in driving competitiveness within the gluten-free prepared foods market. Manufacturers are investing in advanced ingredient systems, enzyme technologies, and hydrocolloid blends to replicate gluten’s elasticity and structure, enhancing texture and shelf stability in prepared foods. Dedicated production lines, cross-contamination control systems, and analytical gluten testing capabilities are essential for maintaining certification standards and consumer trust. Additionally, packaging innovations, such as modified-atmosphere and frozen preservation technologies, are enabling longer shelf life and improved product quality during distribution.

Gluten Free Prepared Foods Industry Leaders

-

Dr. Schär AG

-

General Mills, Inc.

-

The Hain Celestial Group Inc.

-

The Kraft Heinz Company

-

Conagra Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Wow! Momo has launched an innovative gluten-free range of momos made with quinoa and chickpeas. This newly introduced product line will be available in 11 major metro cities across India, catering to the growing demand for healthier food options.

- April 2025: Crave launched its first gluten-free and vegan pink wafer biscuits, named Pink Cheetah Wafers, in the United Kingdom. The product features pink wafers filled with vanilla cream.

- March 2025: Douglicious, a cookie dough brand, has expanded its vegan and gluten-free Soft Baked Gourmet Cookie range with four new varieties. The new offerings include Double Chocolate Chip, Salted Caramel, Chocolate Chip, and Banana Good Granola.

- October 2024: Goodles has launched a gluten-free pasta line, which contains 8 grams of protein and 3 grams of fiber per serving. The products are made from corn, brown rice, chickpeas, and other plant-based ingredients.

Global Gluten Free Prepared Foods Market Report Scope

A prepared food that doesn't have a gluten-containing ingredient. Based on product type, the market is segmented into baked goods, dairy products, confectionery products, sauces, dressings, and seasonings, and other product types. Based on the distribution channel, the market is segmented into on-trade and off-trade. The off-trade segment is further segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Also, the study provides an analysis of the gluten-free prepared food market in the emerging and established markets across the world, including North America, Europe, Asia-Pacific, South America, and Middle-East, and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Bakery and Snacks | Biscuits |

| Cookies | |

| Cakes | |

| Others | |

| Dairy Alternatives | |

| Confectionery | |

| Sauces, Dressings and Seasonings | |

| Ready Meals | |

| Soups and Broths | |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Bakery and Snacks | Biscuits |

| Cookies | ||

| Cakes | ||

| Others | ||

| Dairy Alternatives | ||

| Confectionery | ||

| Sauces, Dressings and Seasonings | ||

| Ready Meals | ||

| Soups and Broths | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the gluten-free food market be by 2031?

It is projected to reach USD 12.69 billion by 2031, growing at a 5.66% CAGR from 2026-2031.

Which product category is expanding fastest?

Ready Meals lead growth, advancing at a 6.71% CAGR thanks to processing advances that improve texture and shelf life.

What share does Off-Trade hold today?

NOff-Trade commands 71.12% of 2025 sales, supported by supermarket aisles and accelerating online subscriptions.

Which region offers the highest growth upside?

Asia-Pacific is forecast to grow 6.58% annually as urban China and India combine rising incomes with greater diagnostic awareness.

Page last updated on: