Genetically Modified Seeds Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

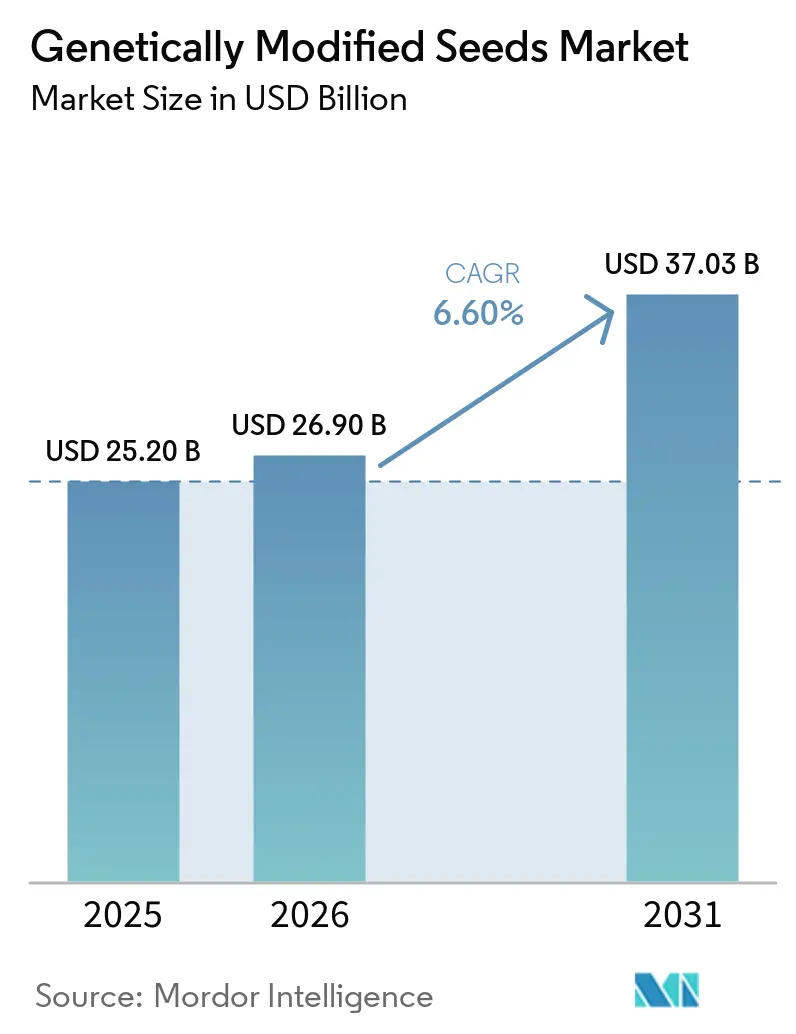

| Market Size (2026) | USD 26.90 Billion |

| Market Size (2031) | USD 37.03 Billion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Genetically Modified Seeds Market Analysis by ���ϲ�����

The genetically modified seeds market size is projected to increase from USD 25.2 billion in 2025 to USD 26.9 billion in 2026 and reach USD 37.03 billion by 2031, growing at a CAGR of 6.6% over 2026-2031. The genetically modified seeds market remains supported by a built-in seed replacement cycle in major row crops, as farmers buy new seed every planting season, which keeps demand more stable than for many other farm inputs. Feed demand, biodiesel growth, and the need for higher field performance are keeping growers focused on seeds that combine stronger yield stability with trait protection across multiple agronomic risks. The genetically modified seeds market is also becoming more concentrated around companies that control both germplasm and trait licensing, raising the cost of entry for smaller developers and making partnerships more important for commercial scale. At the same time, resistance pressure, uneven regulatory timelines, and competition from identity-preserved conventional acreage are forcing the genetically modified seed market to refresh older trait packages more quickly than before.

Key Report Takeaways

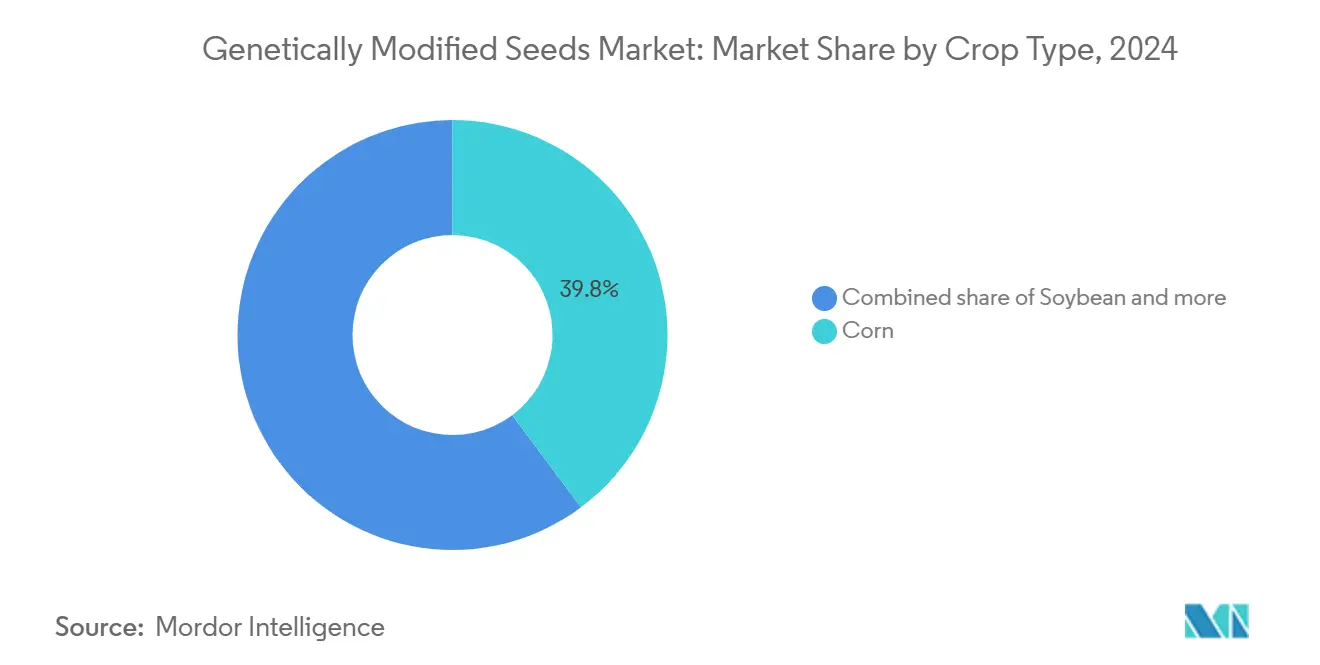

- By crop type, corn accounted for 39.8% of the genetically modified seeds market in 2025, whereas genetically modified cotton is projected to grow at a CAGR of 9.8% during the forecast period.

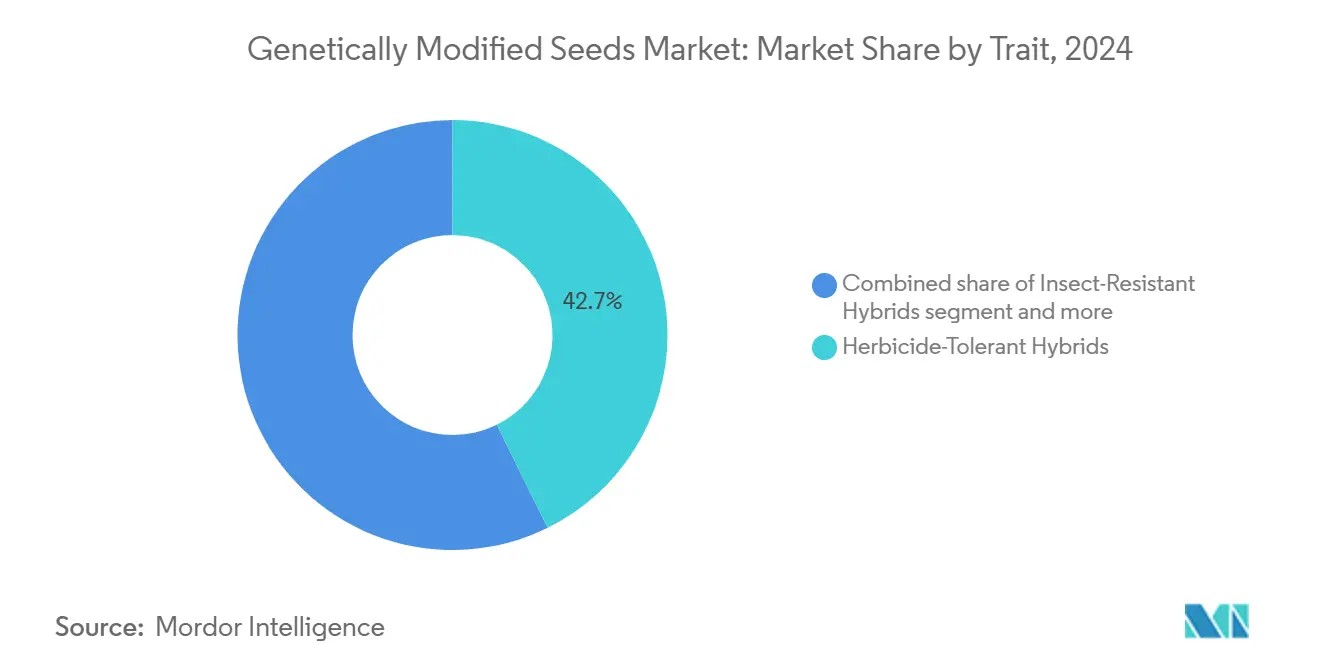

- By trait, herbicide-tolerant hybrids led with a 42.7% share of the genetically modified seeds market size in 2025, while stacked-trait is advancing at a 10.9% CAGR through 2031.

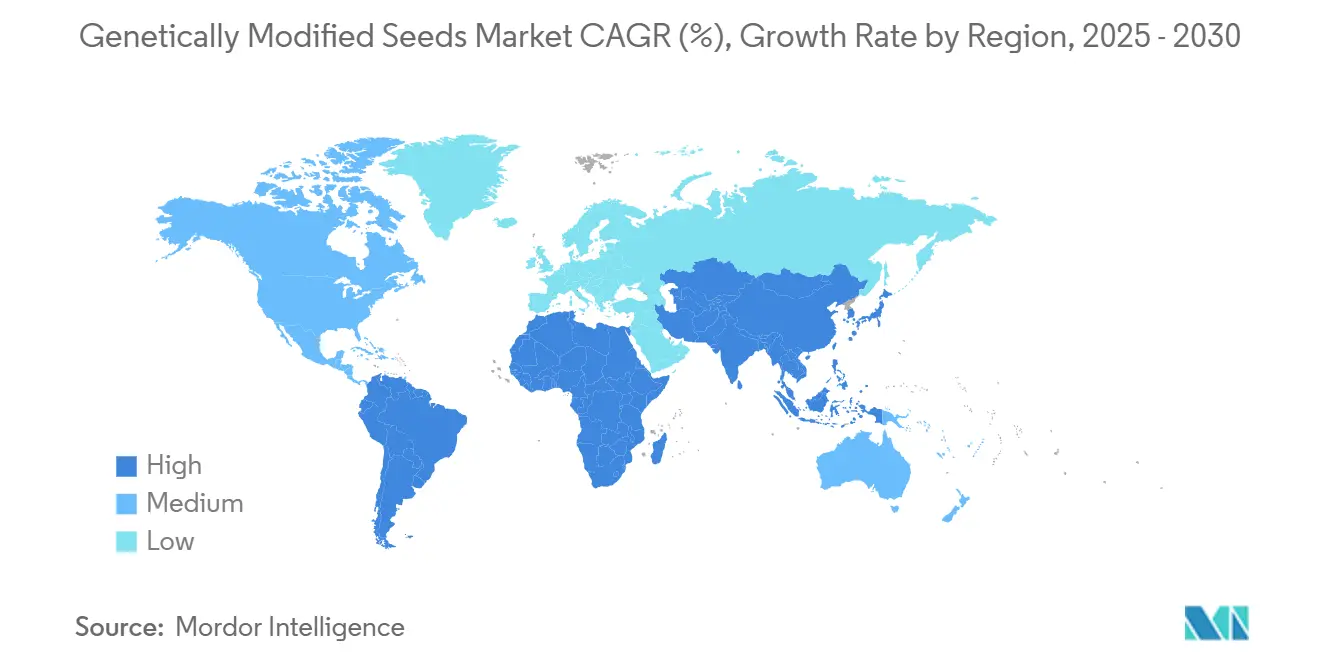

- By region, North America held 39.2% of the genetically modified seeds market share in 2025, whereas Asia-Pacific is projected to expand at an 8.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Genetically Modified Seeds Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stacked-trait corn and soybean acreage expansion | +1.5% | North America and South America, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Gene-editing rule liberalization for seed commercialization | +1.2% | Global, with early gains in North America, China, and United Kingdom | Long term (≥ 4 years) |

| Drought and heat tolerance approvals in staple crops | +1.0% | Asia-Pacific core, South America, and Africa | Long term (≥ 4 years) |

| Biofuel and feed demand reinforcing Genetically Modified seed replacement cycles | +0.9% | North America and South America | Short term (≤ 2 years) |

| Carbon-program economics favoring low-till trait packages | +0.5% | North America and Europe | Medium term (2-4 years) |

| Biological seed treatments improving early trait payback | +0.4% | Global, with early gains in North America | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Stacked-Trait Corn and Soybean Acreage Expansion

The genetically modified seeds market is seeing greater value from stacked-trait adoption, as growers now prefer a single seed purchase that covers multiple agronomic risks. In 2025, 84% of United States corn acres and 87% of United States upland cotton acres were planted with stacked herbicide-tolerance and insect-resistance varieties, which shows how limited the runway has become for single-trait offers in mature systems[1]Source: Laura Dodson, “Adoption of Genetically Engineered Crops in the United States – Recent Trends in GE Adoption,” USDA Economic Research Service, ers.usda.gov. This matters because each added mode of action extends product differentiation and supports higher trait value for developers who can keep refreshing performance. The genetically modified seeds market, therefore, benefits not only from more hectares but also from a rising number of commercial trait layers embedded in each hectare.

Gene-Editing Rule Liberalization for Seed Commercialization

The genetically modified seeds market is benefiting from a regulatory framework that is becoming more workable for selected gene-edited traits, especially when product reviews focus on plant risk and food safety outcomes rather than the breeding method alone. The Environmental Protection Agency also issued a tolerance exemption for the SpCas9 protein in citrus in December 2025, indicating that edited or engineered crop tools are moving through narrower, more product-specific reviews in selected use cases[2]Source: “SpCas9 Protein; Exemption From the Requirement of a Tolerance,” Environmental Protection Agency, regulations.gov. Commercial behavior is already adjusting, because seed companies are signing platform access and research evaluation agreements earlier in the development cycle to secure optionality in future traits. The genetically modified seeds market is likely to see more challengers enter focused trait niches when regulatory timelines become more predictable and platform access becomes easier to license.

Biofuel and Feed Demand Reinforcing Genetically Modified Seed Replacement Cycles

The genetically modified seeds market is also supported by biofuel and feed demand, as both uses reward stable yields, dependable crop quality, and measurable field performance across repeated planting cycles. The Environmental Protection Agency's proposal for 2026 and 2027 Renewable Volume Obligations raised biomass-based diesel targets sharply above 2024 levels, and the United States Department of Agriculture's Economic Research Service estimated that this would require 5 million additional metric tons of crushed soybeans per year, which is close to 4% of current United States production. Brazil’s soybean crushing is projected to reach a record level in 2025/26, supported by biodiesel demand and domestic crush growth. In the United States, the Kansas City Fed noted that biofuel policy is likely to keep raising future corn and soybean demand, reinforcing the case for high-performing seed systems across the feedstock supply chain[3]Source: Francisco Scott and Ayesha Cooray, “Biofuel Policies Are Likely to Drive Future Demand for U.S. Corn and Soybeans,” Federal Reserve Bank of Kansas City, kansascityfed.org. That keeps the genetically modified seeds market tied to recurring demand from processors and fuel-linked buyers rather than to a single season of crop prices.

Drought and Heat Tolerance Approvals in Staple Crops

The genetically modified seeds market is widening its long-term opportunity as climate-stress traits move closer to broader commercial use in staple crops and in crops that historically had fewer biotechnology options. China approved its first gene-edited rice variety for cultivation in December 2024 and issued 5 new gene-edited biosafety certificates that month for soybean, corn, and wheat, indicating that climate- and performance-related traits are advancing across multiple crop pipelines simultaneously. The Corteva, Inc. and Pairwise partnership, formed in 2024, also targets climate resilience and yield improvement across corn, soy, wheat, canola, and other row crops, signaling where development budgets are being allocated for the next cycle of product launches. This matters because drought- and heat-tolerant traits can open demand in regions where growers still see biotechnology as a tool for risk control rather than solely for weed or insect management. The genetically modified seeds market should therefore gain from a broader crop set and from a more diversified agronomic value story over time.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent and breeders' rights litigation over stacked traits | -0.8% | North America and Europe | Medium term (2-4 years) |

| Herbicide-resistant weeds eroding legacy trait premiums | -0.6% | North America, South America, and Australia | Short term (≤ 2 years) |

| Asynchronous labeling and gene-editing classification rules | -0.5% | Global, particularly Europe, China, and emerging markets | Long term (≥ 4 years) |

| Non-Genetically Modified Organism and organic premiums diverting food-grade acreage | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Herbicide-Resistant Weeds Eroding Legacy Trait Premiums

The genetically modified seeds market faces a direct commercial drag when resistant weeds reduce the field value of older herbicide-tolerance systems that still account for the largest installed trait base. Corteva Agriscience reported that herbicide-resistant Palmer amaranth had been confirmed in 34 United States states by 2025, with resistance spanning several key herbicide groups used in major weed-control programs. This pattern forces growers to add more chemistry, more field passes, or newer stacks, which cuts into the simple premium that legacy single-trait packages once captured. The Environmental Protection Agency’s 2025 dicamba proposal also introduced tighter application conditions, indicating that the herbicide system around these traits is becoming more constrained rather than less. The genetically modified seed market can still grow under these conditions, but companies must refresh trait packages more quickly to keep the performance gap wide enough for farmers to pay for upgrades.

Patent and Breeders' Rights Litigation Over Stacked Traits

The genetically modified seeds market also slows when new stacked products require access to several patent families, breeding rights, and elite germplasm pools before a commercial launch can move forward. The concentration of trait ownership among Bayer AG, Corteva, Inc., Syngenta Group Co. Ltd., and BASF SE means that licensing terms are often as important as biology in deciding whether a new product can scale across major crop systems. Corteva, Inc. said in May 2026 that Vylor, Inc. launches with more than 4,000 germplasm patents and 2,000 biotechnology patents, which illustrates how large the intellectual property estates have become in this field. When a new stack depends on several protected layers, mid-tier developers face longer negotiations, higher royalty burdens, and more legal exposure than integrated leaders with broader patent coverage. That is why the genetically modified seeds market continues to favor companies that can pair strong breeding assets with internal trait ownership and cross-licensing leverage.

Segment Analysis

By Crop Type: Corn and Soybean Anchor Volumes as Cotton Accelerates

Corn held 39.8% of the genetically modified seeds market share in 2025, and this part of the genetically modified seeds market size stayed central because feed demand, ethanol use, and recurring seasonal seed purchases keep replacement activity high across large planted areas. In the United States, more than 92% of corn acres were planted with herbicide-tolerant, genetically engineered varieties in 2025, and 87% carried insect-resistant traits, demonstrating how deeply biotechnology is embedded in the crop’s production system. Soybean remained the second-largest crop block, supported by record global crush demand and by policy support for biodiesel feedstocks in both the United States and Brazil.

Cotton is the fastest-growing crop type in the genetically modified seeds market and is projected to grow at 9.8% through 2031, supported by continued adoption in large Asian-producing countries and by the addition of herbicide-tolerance layers on top of established insect-resistance packages. In China, genetically modified cotton already covered close to 95% of planted cotton area in 2025, leaving room for value growth through better trait combinations rather than first-time adoption. Smaller crop categories such as citrus, specialty vegetables, and other niche crops remain commercially modest, but regulatory developments in these areas show that the genetically modified seed market is not limited to the largest row crops.

By Trait: Herbicide Tolerance Leads While Stacked Traits Drive Future Value

Herbicide tolerance accounted for 42.7% of the genetically modified seed market in 2025 and remained the largest trait class because it is already integrated across the broadest germplasm base in corn, soybean, and cotton. That position reflects years of alignment between seed genetics and field weed-control systems, even though resistance pressure is now making the older value proposition less secure. The Environmental Protection Agency’s 2025 dicamba proposal showed that regulators still support use in dicamba-tolerant cotton and soybean systems, while also tightening operating conditions for those products. For the genetically modified seeds industry, that means the biggest trait category remains commercially necessary, but it also needs more stewardship and more frequent upgrades than before. Disease resistance and quality traits remain smaller in scale, yet they are becoming more relevant as developers seek value beyond simple weed control.

Stacked traits are the fastest-growing trait category in the genetically modified seeds market and are forecast to expand at 10.9% through 2031, as growers increasingly seek combined protection against insects, weeds, and abiotic stress in a single seed purchase. Syngenta Group Co., Ltd. said its Durastak platform for spring 2026 planting includes a triple Bt protein stack for corn rootworm, demonstrating how companies are responding to resistance pressure by adding more independent modes of action to a single commercial product. The United States Department of Agriculture Animal and Plant Health Inspection Service's 2025 petition review changes may further reduce timeline burdens for selected trait classes, which is helpful for products that combine several performance claims in one seed. As a result, the genetically modified seeds market is shifting from simple single-function traits toward more layered, defensible technology packages.

Geography Analysis

North America held 39.2% of the genetically modified seed market share in 2025, maintaining its position as the largest regional market, as adoption is already near saturation in the most important field crops. In 2025, genetically engineered varieties were used on 96% of soybean acres, 92% of corn acres, and 93% of upland cotton acres in the United States. This demonstrates the limited potential for first-time adoption and highlights that growth now primarily depends on premium trait turnover. As a result, the region's growth relies more on deeper stack penetration, variety refreshes, and closer integration with crop protection systems than on increased planted area. Canada adds a separate source of demand through canola development, and BASF SE’s 2026 investment in Saskatchewan points to continued breeding intensity for improved hybrid performance.

Asia-Pacific is the fastest-growing regional segment in the genetically modified seeds market, and its market size is projected to grow at 8.7% through 2031. China is the main growth engine, as the country expanded the area of genetically modified corn and soybeans sharply and issued a third round of seed production licenses to 42 companies in November 2025. The same report showed that biosafety certificates were issued for new crop varieties in late 2024 and early 2025, which confirms that commercialization is moving from the trial phase into scaled deployment for selected crops. India supports the regional profile through the depth of its cottonseed business, while Japan and Australia contribute through controlled research and field activity. The Asia-Pacific genetically modified seeds market is therefore expanding through a mix of state-led adoption, local licensing, and a broader crop pipeline than the region had a few years ago.

South America remains a major contributor to the genetically modified seeds market size because biofuel demand, export crop scale, and farmer acceptance keep genetically modified corn and soybean systems commercially strong. Europe still has a limited planting base, so its role in the genetically modified seeds market is shaped more by regulatory debate and import demand than by broad domestic cultivation. Africa remain smaller in current volume, but they represent a broader long-term opportunity as more countries explore approvals for staple crops and climate-resilience traits.

Competitive Landscape

The genetically modified seeds market remains moderately concentrated at the trait development and licensing level in 2025, with Bayer AG, Corteva, Inc., Syngenta Group Co. Ltd., Groupe Limagrain Holding SA, and BASF SE setting much of the competitive pace through patent control, breeding depth, and established channel access. The structure of the Genetically Modified (GM) seeds market imposes high entry barriers, as potential competitors must integrate elite germplasm, regulatory expertise, and access to cross-licensed traits to compete effectively at scale. Bayer AG's March 2025 petition to the United States Department of Agriculture Animal and Plant Health Inspection Service for MON 95275 maize highlights the ongoing efforts by leading companies to enhance biological protection for core crops. This filing focused on a rootworm resistance stack combining Bt proteins with RNA interference, emphasizing a strategy to safeguard trait value through multiple modes of action. Such product architectures enable large companies to defend pricing and extend commercial exclusivity in mature acreage within the genetically modified seeds market.

Corteva, Inc. is reshaping the competitive landscape through structural adjustments rather than solely relying on product launches. In May 2026, the company announced that its seed and genetics spinoff would operate as Vylor, Inc., launching with over 4,000 germplasm patents and 2,000 biotechnology patents. This move establishes a pure-play seed genetics company with a focused capital allocation strategy, potentially influencing pricing and partnership dynamics across the genetically modified seeds market. Similarly, Syngenta Group Co., Ltd. demonstrated another competitive approach in March 2026 by securing a research evaluation license from KOMO Biosciences for site-specific DNA insertion in maize. This highlights the trend of large incumbents leveraging external platform technologies to accelerate development while conserving internal R&D resources for scalable trait platforms.

A second tier of competitors remains active, primarily in regional niches rather than global trait dominance. Companies such as JK Agri Genetics Limited, Nuziveedu Seeds Limited, Rasi Seeds Private Limited, and Yuan Longping High-Tech Agriculture Co., Ltd. leverage locally adapted germplasm and established domestic seed distribution networks. Additionally, BASF SE's expansion in canola breeding in Canada and Bayer AG's camelina alliance with bp illustrate how leading players are diversifying their crop and end-market exposure beyond traditional corn and soybean platforms. As a result, while the genetically modified seeds market remains concentrated, competition continues to evolve through investments in new crops, platform partnerships, and regional specialization.

Genetically Modified Seeds Industry Leaders

Bayer AG

BASF SE

Groupe Limagrain Holding SA

Syngenta Group Co., Ltd.

Corteva, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bayer AG and bp formed a long-term strategic alliance to jointly scale camelina, marketed as NewGold, as an intermediate oilseed crop for renewable diesel and sustainable aviation fuel production in North America. The alliance positions Bayer AG at the intersection of low-carbon fuel supply chains and its genetically modified seed portfolio.

- May 2026: Corteva, Inc. named its advanced seed and genetics spinoff Vylor, Inc., with a target fourth-quarter 2026 separation. Vylor launches with more than 4,000 germplasm patents and 2,000 biotechnology patents, including a pipeline in hybrid wheat, multi-disease resistance corn, next-generation biofuel traits, and gene editing.

- March 2026: BASF SE committed CAD 27 million (USD 19.4 million), to expand its Canola Breeding Center of Innovation in Saskatoon, Saskatchewan, through end-2027, integrating advanced automation and precision-controlled growth systems to accelerate genomic selection and shorten InVigor hybrid canola development cycles.

Global Genetically Modified Seeds Market Report Scope

Genetically modified seeds are engineered in laboratories by inserting specific genes into a plant's DNA. This alteration confers desirable traits such as pest resistance, drought tolerance, or increased nutritional value.

The genetically modified seeds market report is segmented by crop type (corn, soybean, cotton, canola and rapeseed, alfalfa, sugar beet, potato, and others), trait (herbicide tolerance, insect resistance, stacked traits, disease resistance, drought tolerance, and quality traits), and geography (North America, South America, Europe, Asia-Pacific, and Africa). The market forecasts are provided in value (USD) and volume (metric tons).

| Corn |

| Soybean |

| Cotton |

| Canola and Rapeseed |

| Alfalfa |

| Sugar Beet |

| Potato |

| Eggplant |

| Papaya |

| Squash |

| Apple |

| Sugarcane |

| Herbicide Tolerance | |

| Insect Resistance | |

| Stacked Traits | Herbicide Tolerance and Insect Resistance |

| Herbicide Tolerance, Insect Resistance, and Abiotic Stress | |

| Other Multi-Trait Combinations | |

| Disease Resistance | |

| Drought and Heat Tolerance | |

| Quality and Output Traits |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Spain |

| Portugal | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Crop Type | Corn | |

| Soybean | ||

| Cotton | ||

| Canola and Rapeseed | ||

| Alfalfa | ||

| Sugar Beet | ||

| Potato | ||

| Eggplant | ||

| Papaya | ||

| Squash | ||

| Apple | ||

| Sugarcane | ||

| By Trait | Herbicide Tolerance | |

| Insect Resistance | ||

| Stacked Traits | Herbicide Tolerance and Insect Resistance | |

| Herbicide Tolerance, Insect Resistance, and Abiotic Stress | ||

| Other Multi-Trait Combinations | ||

| Disease Resistance | ||

| Drought and Heat Tolerance | ||

| Quality and Output Traits | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Spain | |

| Portugal | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the Genetically Modified seeds market?

The Genetically Modified seeds market stands at USD 26.9 billion in 2026 and is forecast to reach USD 37.03 billion by 2031 at a 6.6% CAGR.

Which crop category leads revenue generation?

Corn is the largest crop type with 39.8% share in 2025, supported by steady use in feed and fuel-linked value chains.

Which trait category is expanding the fastest?

Stacked traits are the fastest-growing trait segment and are projected to expand at 10.9% through 2031 because growers want multi-layer protection in one seed purchase.

Why does North America remain the largest regional block?

North America leads because genetically modified seed adoption is already very high in the United States across soybean, corn, and cotton, which supports repeat purchases and premium trait upgrades.

Why is Asia-Pacific growing faster than other regions?

Asia-Pacific is growing the fastest at 8.7% through 2031, led by China's commercialization push, new biosafety approvals, and broader seed production licensing.

What is the main risk to legacy trait portfolios?

Herbicide-resistant weeds remain the main near-term risk because they reduce the value of older herbicide-tolerance systems and force companies to launch refreshed stacks more quickly.

Page last updated on: