Electronic Medical Records Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

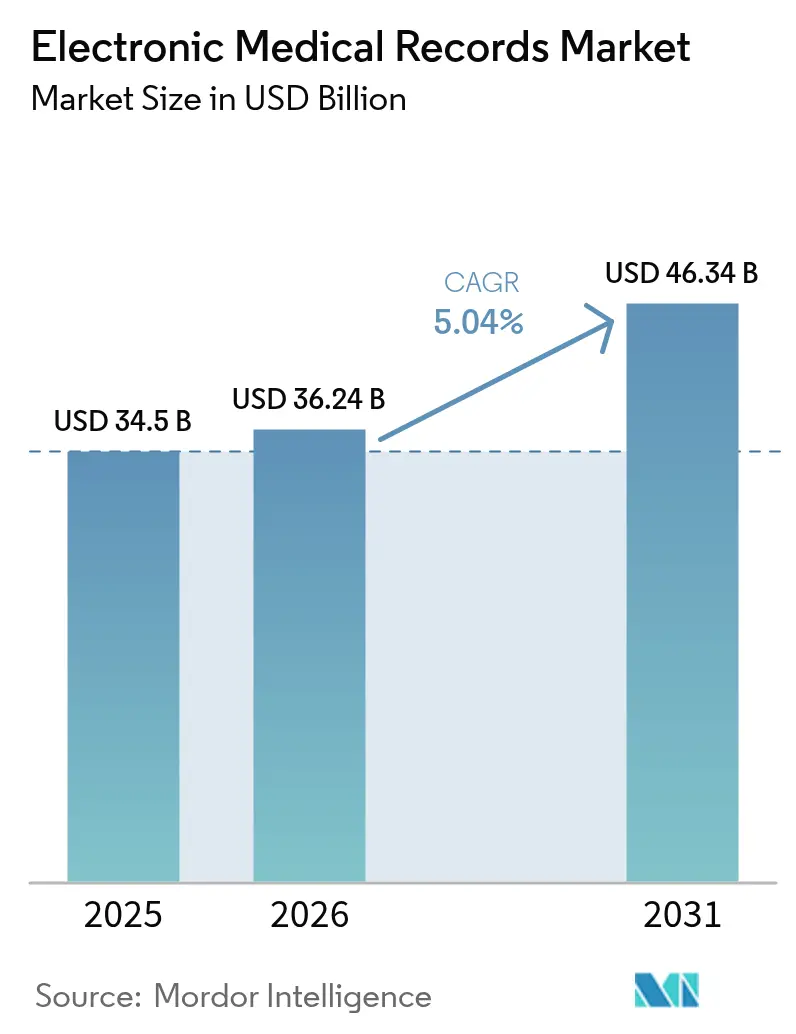

| Market Size (2026) | USD 36.24 Billion |

| Market Size (2031) | USD 46.34 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

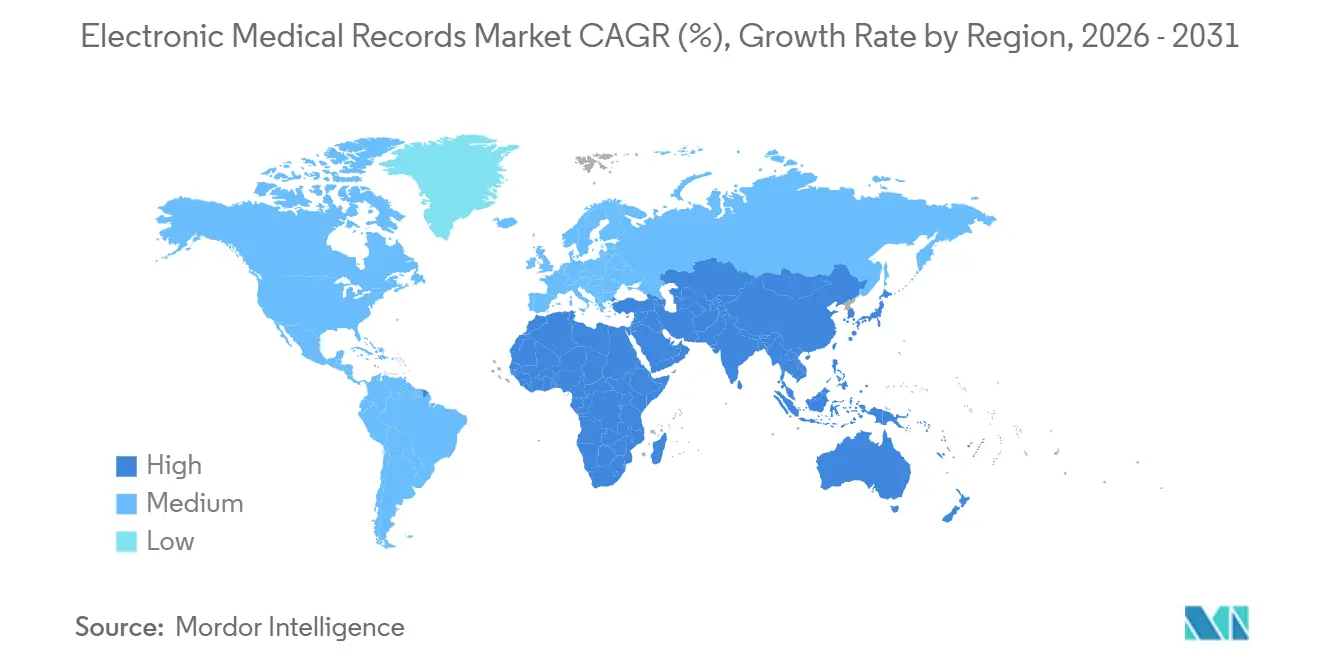

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

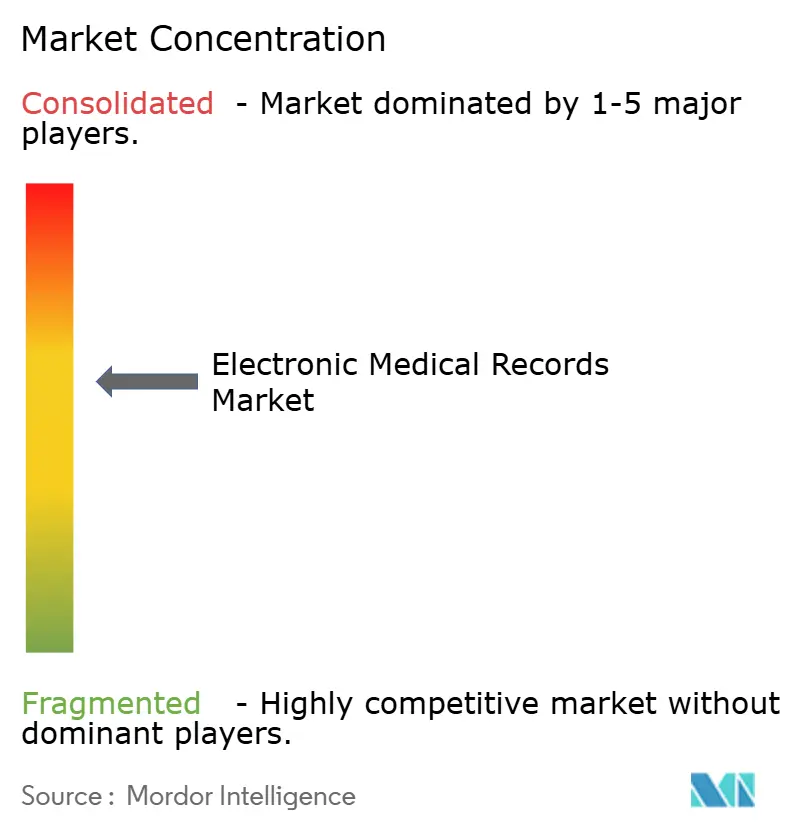

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Electronic Medical Records Market Analysis by ���ϲ�����

The Electronic Medical Records Market size was valued at USD 34.5 billion in 2025 and is estimated to grow from USD 36.24 billion in 2026 to reach USD 46.34 billion by 2031, at a CAGR of 5.04% during the forecast period (2026-2031).

Persistent digitization mandates, the growing preference for cloud-native deployments, and embedded artificial-intelligence workflow tools continue to drive growth in the electronic medical records market. Vendor competition is intensifying as software suppliers pivot from perpetual licenses to subscription bundles that integrate billing, scheduling, and patient engagement into a single interface. The shift unlocks recurring revenue streams for suppliers but raises switching costs for providers, who must retrain staff and migrate historical data. Technology differentiation is increasingly anchored in open, vendor-neutral FHIR APIs that let hospitals add niche telehealth or analytics modules without rewriting core code.

Key Report Takeaways

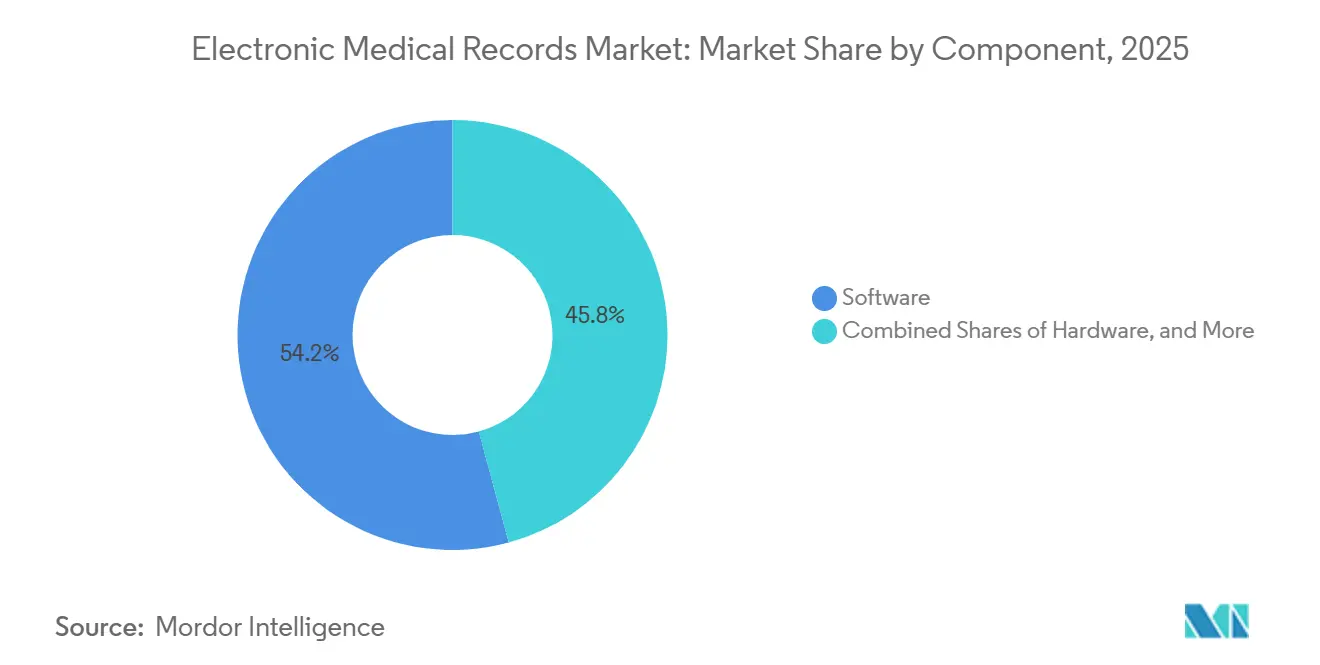

- By component, software captured 54.22% of the electronic medical records market share in 2025, while services are advancing at a 6.22% CAGR through 2031.

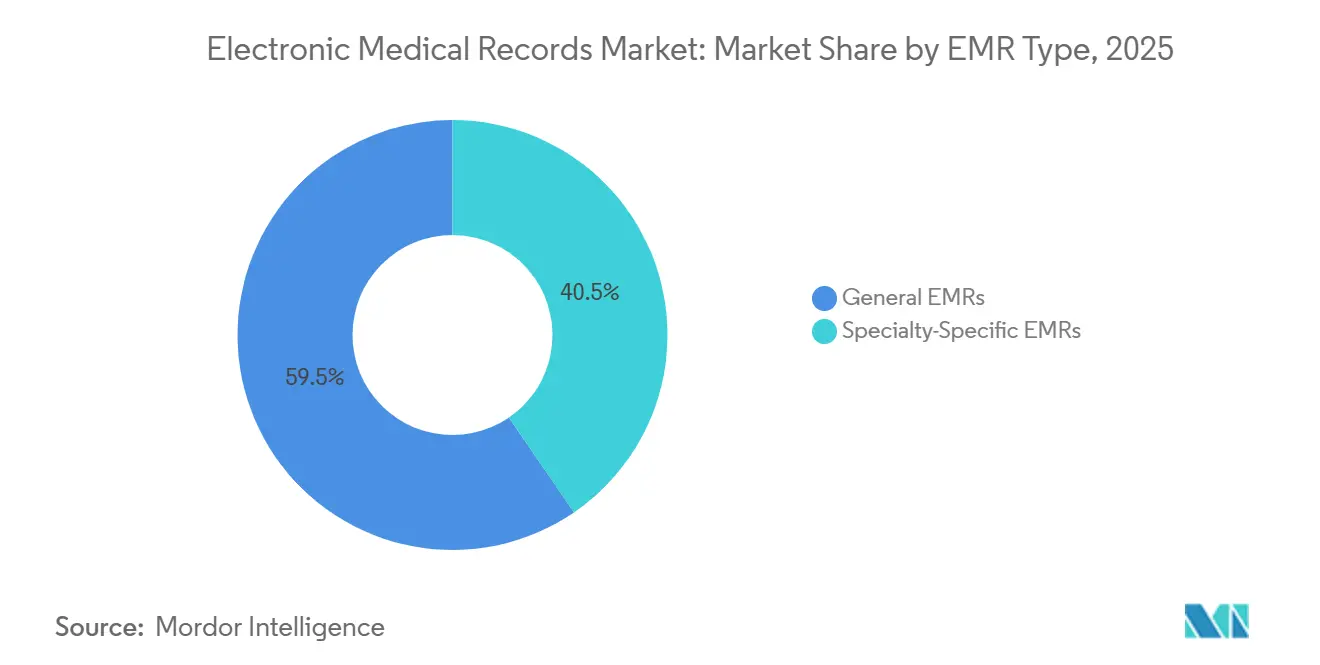

- By EMR type, general platforms led with 59.55% revenue share in 2025; specialty systems are forecast to expand at a 6.49% CAGR to 2031.

- By delivery mode, cloud solutions accounted for 55.90% of the electronic medical records market size in 2025 and are expanding at a 5.67% CAGR through 2031.

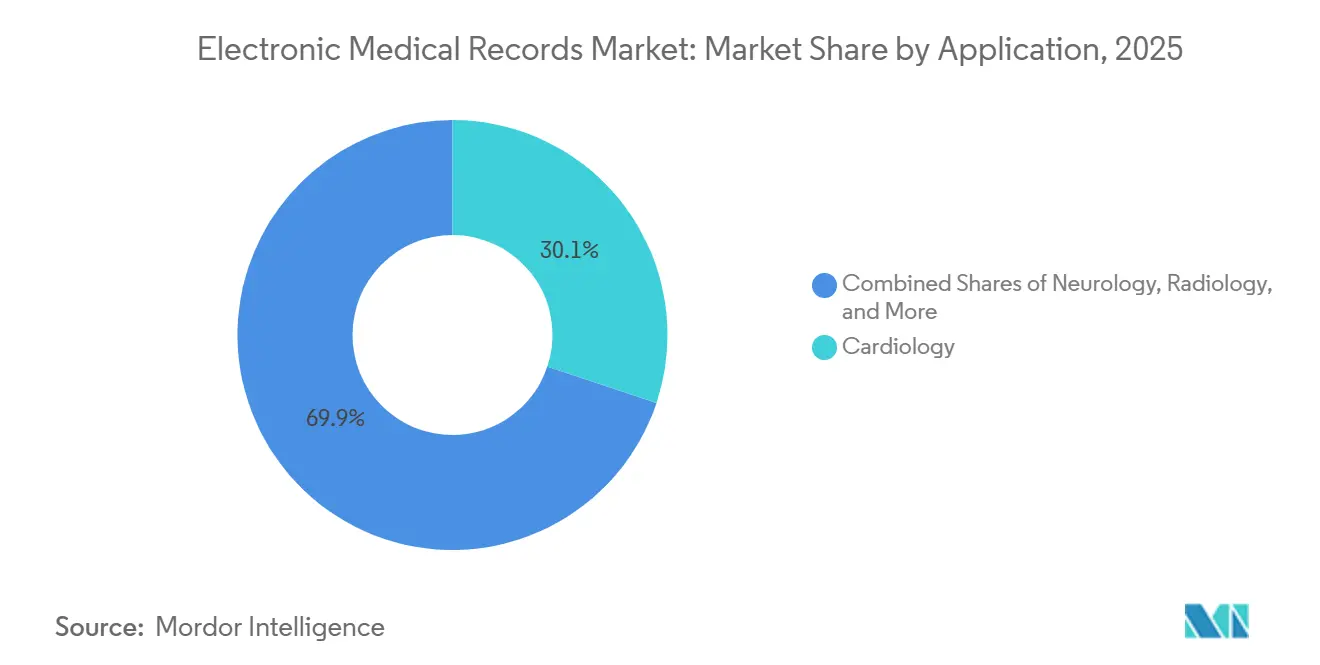

- By application, cardiology accounted for 30.12% of revenue share in 2025, whereas neurology is projected to grow at a 5.98% CAGR over 2026-2031.

- By end user, hospital installations accounted for 59.05% of 2025 deployments; ambulatory and physician clinics are growing at a 6.09% CAGR through 2031.

- By geography, North America dominated with a 43.30% share in 2025, whereas Asia-Pacific is on track for a 6.99% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electronic Medical Records Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory financial incentives sustaining digitization | +0.8% | North America, Europe, APAC core | Medium term (2-4 years) |

| AI-powered clinical decision support embedded in EMRs | +1.1% | Global, with early adoption in North America & EU | Long term (≥ 4 years) |

| Migration from client-server to cloud-native platforms | +0.9% | Global, accelerated in APAC & Latin America | Short term (≤ 2 years) |

| Value-based care contracts demanding longitudinal data | +0.7% | North America, expanding to EU | Medium term (2-4 years) |

| Vendor-neutral FHIR APIs unlocking third-party ecosystems | +0.6% | Global, led by North America & EU | Long term (≥ 4 years) |

| Edge-computing EMR Lite stacks for field & home care | +0.5% | APAC, MEA, rural North America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Regulatory Financial Incentives Sustaining Digitization

Governments keep tying reimbursements to the adoption and interoperability of electronic medical records. The U.S. Promoting Interoperability program now pegs 9% of Medicare physician payments to EMR-enabled quality reporting.[1]Centers for Medicare & Medicaid Services, “Promoting Interoperability Program,” cms.gov In March 2025, the European Union earmarked EUR 1.2 billion (USD 1.3 billion) to co-fund national EMR infrastructure, contingent on cross-border patient data exchange under the European Health Data Space regulation.[2]European Commission, “Digital Europe Programme,” ec.europa.eu India’s Ayushman Bharat Digital Mission mandates EMR use in public facilities by 2027, accelerating vendor deployments across 700 district hospitals.[3]National Health Commission of the People’s Republic of China, “Hospital EMR Level 5 Targets,” nhc.gov.cn These schemes converge on HL7-FHIR compliance, nudging laggards to retire proprietary interfaces.

AI-Powered Clinical Decision Support Embedded in EMRs

Large vendors are folding artificial-intelligence models into core software rather than selling them as bolt-ons. Epic’s Cosmos engine applies predictive analytics on 300 million de-identified charts, trimming rare-disease diagnostic delays by 18% at early-adopter academic centers. Oracle Health’s Clinical Digital Assistant converts ambient voice into structured notes, reclaiming 2.3 physician hours per day during 2025 pilots. Smaller suppliers lacking in-house data-science teams must license algorithms, lifting cost bases and fueling consolidation across the electronic medical records market.

Migration From Client-Server to Cloud-Native Platforms

Providers continue redirecting capital budgets toward cloud subscriptions. Amazon Web Services’ HealthLake ingests HL7-FHIR feeds from major EMRs and frees hospitals from maintaining separate data warehouses. Microsoft’s Mission Critical support program delivers proactive resiliency assessments for health system workloads, reducing downtime and smoothing Electronic Medical Records market migrations. Latency-sensitive emergency departments hedge with hybrid setups that cache allergy lists locally to guarantee sub-second retrieval.

Value-Based Care Contracts Demanding Longitudinal Data

Shared-savings and bundled-payment models reward coordinated documentation. Accountable Care Organizations covered 13 million Medicare lives in 2025 and require electronic quality reporting on readmissions, medication adherence, and chronic-disease control. Humana disclosed lower diabetes-related hospitalizations among providers using population-health EMR modules, proving the financial upside of longitudinal records. Clinics without data analysts are gravitating toward cloud systems that ship with prebuilt dashboards.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cyber-security liability & soaring insurance premiums | -0.9% | Global, acute in North America | Short term (≤ 2 years) |

| Physician burnout tied to poor user-interface design | -0.7% | North America, EU | Medium term (2-4 years) |

| Capital constraints at small & mid-size providers | -0.5% | Global, severe in rural APAC & MEA | Short term (≤ 2 years) |

| Data-governance complexity in multi-vendor estates | -0.4% | North America, EU | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Cyber-Security Liability & Soaring Insurance Premiums

Healthcare remains the most-targeted industry for ransomware, logging 1,710 security incidents in 2025 alone. Breached records expose providers to regulatory fines, class-action litigation, and rising cyber-insurance premiums that now eclipse USD 8 million annually for large systems. A high-profile breach at a major cloud vendor in early 2025 intensified scrutiny of supply-chain risk, prompting boards to demand independent penetration testing and round-the-clock monitoring. Rural hospitals are especially vulnerable, with 60% reporting at least one cyber incident in the past 3 years, often while still running outdated record-keeping software. These pressures slow procurement cycles, lengthen due diligence, and marginally dampen overall growth in the electronic medical records market.

Physician Burnout Tied to Poor User-Interface Design

Usability shortcomings fuel clinician frustration. Peer-reviewed research shows that each 1-point rise in EMR usability scores cuts burnout odds by 2% among U.S. nurses. The American Medical Association lists streamlined data entry, intuitive task flows, and modular configuration among top fixes, yet only a minority of products meet all criteria. Market demand for AI transcription tools that eliminate manual note-taking has spawned dozens of startups, but accuracy gaps and integration complexity have delayed wide deployment. Until the interface redesign catches up with clinical expectations, adoption enthusiasm in specific physician segments remains muted, acting as a second-order drag on the expansion of the electronic medical records market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Software Growth

Services revenue is advancing at 6.22% through 2031 as hospitals divert budgets toward interoperability engineering, workflow redesign, and cybersecurity. Consulting line items climbed during cloud transitions that require historical data cleansing and staff retraining. Software retains a 54.22% Electronic Medical Records market share in 2025, thanks to enterprise agreements at large systems and per-encounter subscriptions at small clinics. Hardware spend continues to taper because cloud hosting displaces server refresh cycles. The 21st Century Cures Act’s information-blocking rules are channeling new demand into API and FHIR testing services. Health systems that rushed rollouts during the pandemic report success rates below 40%, prompting fresh spending on workflow redesign, data conversion, and user training. Consultancy teams conversant with both HL7 standards and bedside routines command premium rates, underpinning the services boom. Meanwhile, lower hardware demand accompanies the shift to browser-based clients, trimming on-premise server budgets but not eliminating niche device opportunities such as medical-grade tablets.

Service expansion also mirrors new reimbursement realities. Value-based payment contracts penalize readmissions and adverse events, so providers hire engineers to tune clinical decision-support rules and continuously audit data quality. This post-go-live optimization translates into sticky annuity revenue for integrators and fuels the services slice of the electronic medical records market. Several leading hospital chains now embed outcome-based incentives in their vendor agreements, further entrenching the expertise of external partners.

By EMR Type: Specialty-Specific Solutions Gaining Momentum

General EMRs held 59.55% of the electronic medical records market share in 2025, mainly because multi-specialty hospitals seek a single source of truth for enterprise reporting. These systems bundle inpatient, outpatient, and billing workflows, simplifying audit trails. Yet orthopedics, oncology, and fertility clinics increasingly view monolithic designs as burdensome, stoking a 6.49% CAGR in niche solutions built around specialty templates. Vendors catering to subspecialties embed disease-specific order sets and integrate diagnostic devices natively, reducing the number of clicks for clinicians.

Adoption momentum is strongest in ambulatory networks where one dominant specialty drives revenue. Neurology groups deploying seizure-tracking dashboards and tele-EEG streaming inside lightweight specialty EMRs report 15% faster documentation and higher patient satisfaction. To stay competitive, enterprise vendors have begun releasing modular micro-apps that slot specialty features into the core database, blurring lines between categories and preserving data continuity across service lines. This hybrid approach is expected to recalibrate the size of the electronic medical records market over the next five years.

By Mode of Delivery: Cloud Dominates New Deployments

Cloud-hosted installations accounted for 55.90% of the electronic medical records market in 2025 and will grow at a 5.67% CAGR through 2031. Providers cite predictable subscription billing, automatic upgrades, and built-in disaster recovery as compelling advantages. Notably, the electronic medical records market size for cloud systems is expanding fastest among mid-tier health systems that lack the capital reserves to maintain large server rooms. United States government agencies also favor managed hosting; the Department of Veterans Affairs renewed its multi-year cloud contract in 2025 to accelerate modernization across 171 facilities.

On-premise footprints are receding but will persist where local control is mandated, such as defense hospitals or jurisdictions with data-sovereignty laws. In these settings, private-cloud appliances replicate the elastic expansion of hyperscale providers behind the hospital firewall. Transition roadmaps emphasize incremental data migration to minimize downtime. The coexistence of deployment models keeps integration firms busy harmonizing interfaces, further supporting service revenue growth in the electronic medical records market.

By Application: Neurology Emerges as Growth Leader

Cardiology retains the lion’s share, accounting for 30.12% of the electronic medical records market share in 2025, thanks to ubiquitous ECG, cath-lab, and cardiac imaging workflows. AI-assisted lesion detection and risk-stratification tools layered onto cardiology EMRs help explain enduring demand. In contrast, neurology registers the fastest expansion, with a 5.98% CAGR through 2031. Precision-medicine protocols for multiple sclerosis and Parkinson’s disease need longitudinal data sets combining imaging, genomics, and wearable telemetry, functions well-suited to EMR architectures.

Academic centers report early success using EMR-embedded algorithms to predict seizure likelihood, enabling timely medication titration. Oncology, radiology, and emergency-medicine deployments likewise push vendors to refine AI triage features that surface critical results faster. Collectively, these high-complexity specialties raise the bar for sophistication in the electronic medical records market, influencing product roadmaps across all suppliers.

By End-User: Ambulatory Care Centers Drive Growth

Hospitals accounted for 59.05% of the electronic medical records market share in 2025, reflecting enterprise-scale commitments and comprehensive care needs. However, ambulatory networks and physician groups are closing the gap; their segment will post a 6.09% CAGR through 2031 as payers steer procedures to lower-cost outpatient settings. Monthly per-provider cloud subscriptions that fit smaller budgets have lowered barriers, letting independent specialists upgrade legacy software. Diagnostic and imaging centers adopt EMRs that connect scheduling, picture archiving, and results letters, improving throughput without extra clerical staff.

Value-based reimbursement further incentivizes ambulatory clinics to document care comprehensively; missing data can jeopardize shared-savings bonuses. As a result, ambulatory growth is a pivotal contributor to the overall expansion of the electronic medical records market. Vendors courting this tier emphasize rapid implementation, mobile interfaces, and curated specialty templates, differentiating their offerings from hospital-centric rivals.

Geography Analysis

North America accounted for 43.30% of the electronic medical records market revenue in 2025. Federal stimulus programs after the HITECH Act led to near-universal hospital adoption, leaving current growth focused on system replacement and optimization. Interoperability certification deadlines keep spending buoyant, but the region’s 4.25% CAGR to 2031 trails all others. Provider M&A activity consolidates purchasing decisions, strengthening the bargaining power of top vendors and accelerating platform standardization.

Asia-Pacific, by contrast, will compound at 6.99% CAGR, the fastest worldwide. Health ministries in China, India, and Japan subsidize cloud pilots that leapfrog client-server generations, helping rural facilities connect to specialists via telehealth. Mobile-first designs proliferate, aligning with clinicians’ smartphone habits. The associated demand for data centers and cybersecurity services feeds local IT ecosystems, reinforcing the self-sustaining cycle that underpins the electronic medical records market in the region.

Europe shows a steady 4.82% CAGR as the EHDS initiative harmonizes record architectures across member states, balancing innovation with stringent GDPR safeguards. National programs in Germany and the Nordics that reimburse AI-supported diagnostics provide incremental tailwinds. Latin America grows 6.36% CAGR, led by Brazil’s national digital-health plan and Argentina’s private-sector oncology networks. The Middle East & Africa follow closely, with Gulf Cooperation Council hospitals adopting United States vendor platforms under joint-venture arrangements.

Competitive Landscape

The electronic medical records market tilts toward moderate concentration. Epic amplified its footprint by winning several multi-hospital selections in 2025, while Oracle Health preserved 21.7% share through federal contracts and a renewed VA option period. MEDITECH and Altera Digital Health round out the top tier. Collectively, the five largest suppliers control around 60% of global installations, leaving room for agile entrants in subspecialty niches.

Competitive attention centers on application-programming-interface maturity. Epic’s early compliance with USCDI v3 and its open-exchange framework strengthen network effects, enticing third-party app developers. Oracle counters with deeper AI integration, leveraging in-house large-language models to automate scheduling and consent documentation. MEDITECH’s cloud-native Expanse platform targets community hospitals needing lower total cost of ownership, whereas newcomer modular designs from Oystehr and Canvas Medical stress developer friendliness.

Strategic partnerships blossom: in February 2025, 8x8 integrated its contact-center suite with Epic, Oracle, and MEDITECH to streamline patient engagement workflows. Exalt Health adopted WellSky’s rehabilitation-oriented EMR in May 2025 to unify clinical and financial data across expanding multi-state operations. Regional governments also influence vendor trajectories; Tasmania’s USD 306 million “Bluegum” project awarded to Epic underscores the growing role of public tenders in shaping share dynamics. Overall, product road maps converge on AI, specialty depth, and secure interoperability differentiators likely to guide market share shifts through the decade.

Electronic Medical Records Industry Leaders

Athenahealth Inc.

eClinicalWorks

Epic Systems Corporation

MEDITECH

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ireland’s Health Service Executive received cabinet approval to shortlist suppliers for a national electronic health record program, launching the procurement phase.

- January 2026: Oracle Health pledged USD 1.2 billion to expand cloud-EMR data centers across Europe and APAC, adding capacity for 500 hospitals and bolstering data-residency compliance.

- September 2025: Athenahealth upgraded its AI-native athenaOne platform to automate routine tasks and deliver personalized insights ahead of its November 2025 Thrive customer event.

- August 2025: Oracle released an ambulatory EHR on Oracle Cloud Infrastructure with voice commands that let clinicians call up lab or medication data hands-free.

- May 2025: Epic Systems secured the contract for Tasmania’s statewide EMR rollout, the second phase of a USD 306 million digital-health program.

Global Electronic Medical Records Market Report Scope

Within the scope of the report, an electronic medical record (EMR) is a computerized version of a paper record that securely stores information and is accessible to authorized users/practitioners. It is an electronic version of a patient's medical history that is maintained. It includes all data related to the patient's care under a particular doctor, such as demographics, progress notes, problems, medications, vital signs, past medical history, immunizations, laboratory data, and radiology reports.

The electronic medical records market is segmented by component: hardware, software, and services. By end user, the market is segmented into hospital-based EMR, physician-based EMR, specialty clinics, diagnostics and imaging centers, and other end users. By EMR type, the market is segmented into general EMRs and specialty-specific EMRs. By delivery mode, the market is segmented into cloud-based and on-premises models. By application, the market is segmented into cardiology, neurology, radiology, oncology, and other applications. By type, the market is segmented into traditional EMRs, speech-enabled EMRs, interoperable EMRs, and other types. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East, Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in (USD million) for the above segments.

| Hardware |

| Software |

| Services |

| General EMRs |

| Specialty-Specific EMRs |

| Cloud-based |

| On-premise |

| Cardiology |

| Neurology |

| Radiology |

| Oncology |

| Emergency & Trauma |

| Obstetrics & Gynecology |

| Other Applications |

| Hospital-based EMR |

| Physician / Ambulatory Care Centers |

| Specialty Clinics |

| Diagnostic & Imaging Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By EMR Type | General EMRs | |

| Specialty-Specific EMRs | ||

| By Mode of Delivery | Cloud-based | |

| On-premise | ||

| By Application | Cardiology | |

| Neurology | ||

| Radiology | ||

| Oncology | ||

| Emergency & Trauma | ||

| Obstetrics & Gynecology | ||

| Other Applications | ||

| By End-User | Hospital-based EMR | |

| Physician / Ambulatory Care Centers | ||

| Specialty Clinics | ||

| Diagnostic & Imaging Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the Electronic Medical Records market expected to grow through 2031?

It is forecast to expand at a 5.04% CAGR from 2026 to 2031, rising from USD 36.24 billion in 2026 to USD 46.34 billion.

Which component of EMR spending is growing the quickest?

Services, including implementation, interoperability, and cybersecurity support, are advancing at a 6.22% CAGR as providers favor ongoing assistance over one-time licenses.

Why are cloud-based EMRs gaining share?

Cloud platforms avoid capital outlays, offer automatic updates, and synchronize data across multi-site systems, lifting their Electronic Medical Records market share to 55.90% in 2025.

What is driving specialty-specific EMR adoption?

Oncology, cardiology, and neurology clinicians want pre-configured templates and AI tools that shorten documentation, pushing specialty systems to a 6.49% CAGR.

Which region will post the fastest EMR growth?

Asia-Pacific leads with a 6.99% CAGR as China, India, and Japan roll out national interoperability mandates and digital-health subsidies.

How are cyber-security risks affecting EMR investments?

Soaring ransomware losses and higher insurance premiums add cost pressure, prompting hospitals to invest in stronger security controls before expanding EMR functionality.

Page last updated on: