Egg White Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 331.90 Million |

| Market Size (2031) | USD 429.47 Million |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

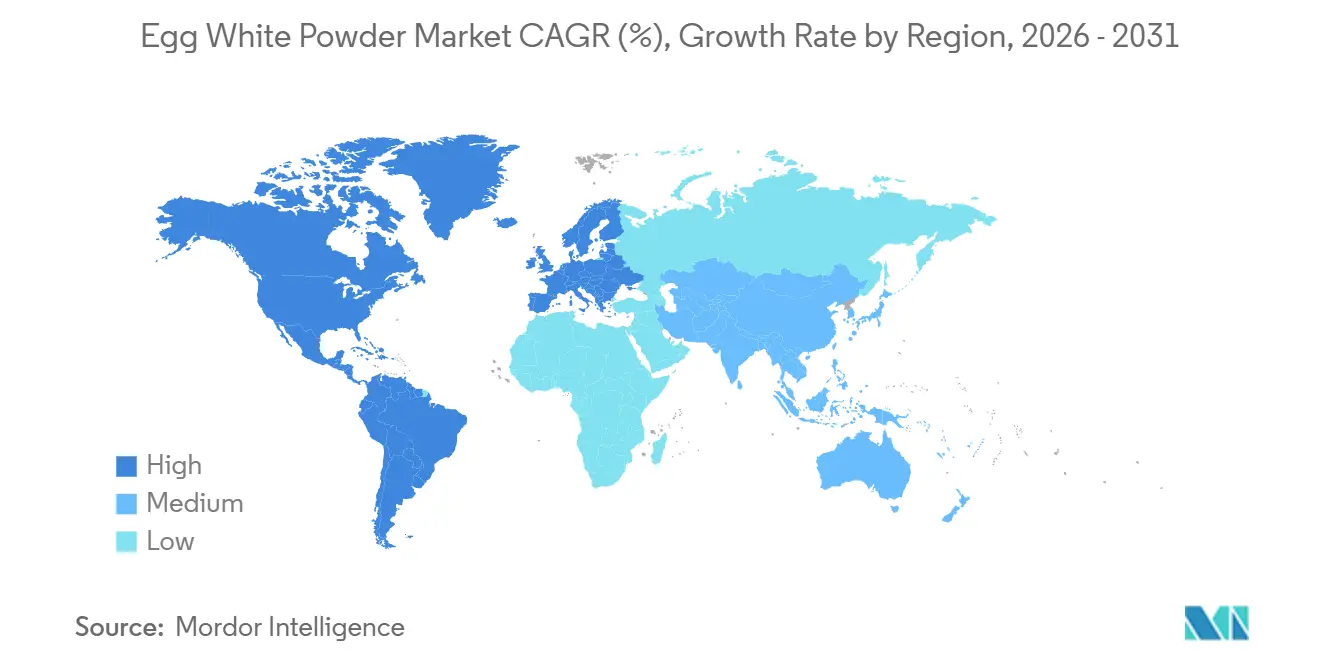

| Fastest Growing Market | South America |

| Largest Market | Europe |

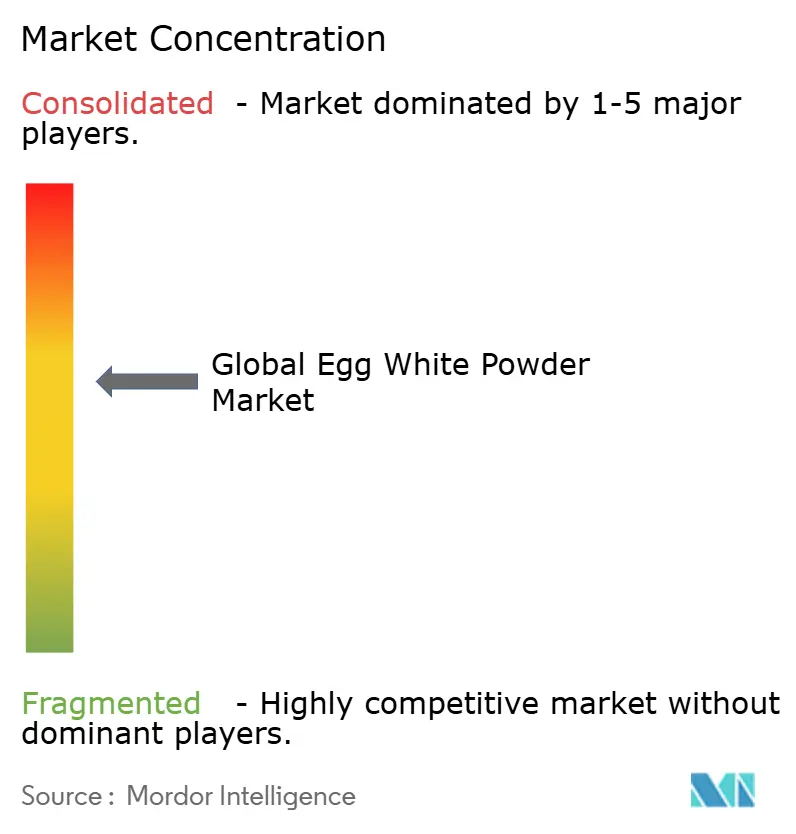

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Egg White Powder Market Analysis by ���ϲ�����

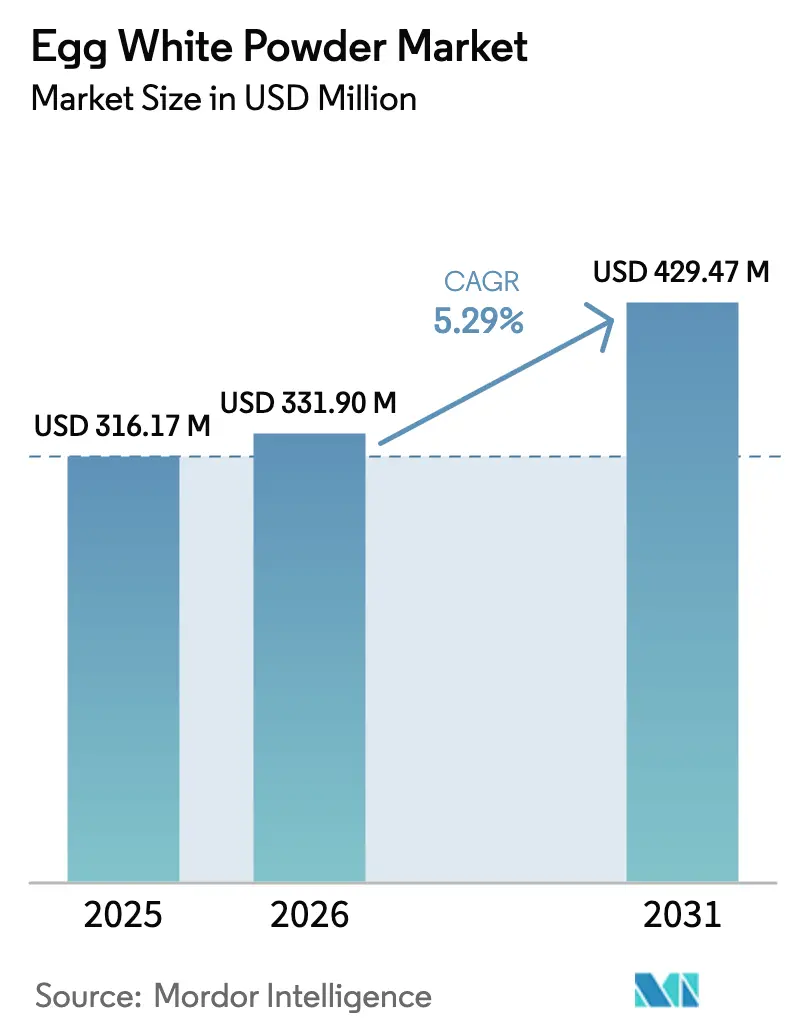

The egg white powder market size is expected to grow from USD 316.17 million in 2025 to USD 331.90 million in 2026 and is forecast to reach USD 429.27 million by 2031 at a 5.29% CAGR over 2026-2031. Rapid gains reflect the ingredient’s unique foaming, emulsifying, and gelation abilities that remain difficult for alternative proteins to replicate, even as precision-fermented ovalbumin products enter specialty channels. Food processors value the powder’s functionality across broad temperature and pH ranges, sustaining demand despite price volatility triggered by recurring avian-influenza outbreaks. Supply-chain consolidation accelerated in 2024-2025 as leading producers acquired mid-sized farms to secure shell-egg inputs, a strategy that both strengthens procurement and concentrates bio-security risk. Momentum in high-protein diets, expanding sports-nutrition formats, and stricter “healthy” labeling rules introduced by the United States Food and Drug Administration in February 2025 further reinforce purchasing appetite for a recognizable, single-ingredient protein source[1]Source: US Food and Drug Administration, "FDA Finalizes Updated “Healthy” Nutrient Content Claim", www.fda.gov.

Key Report Takeaways

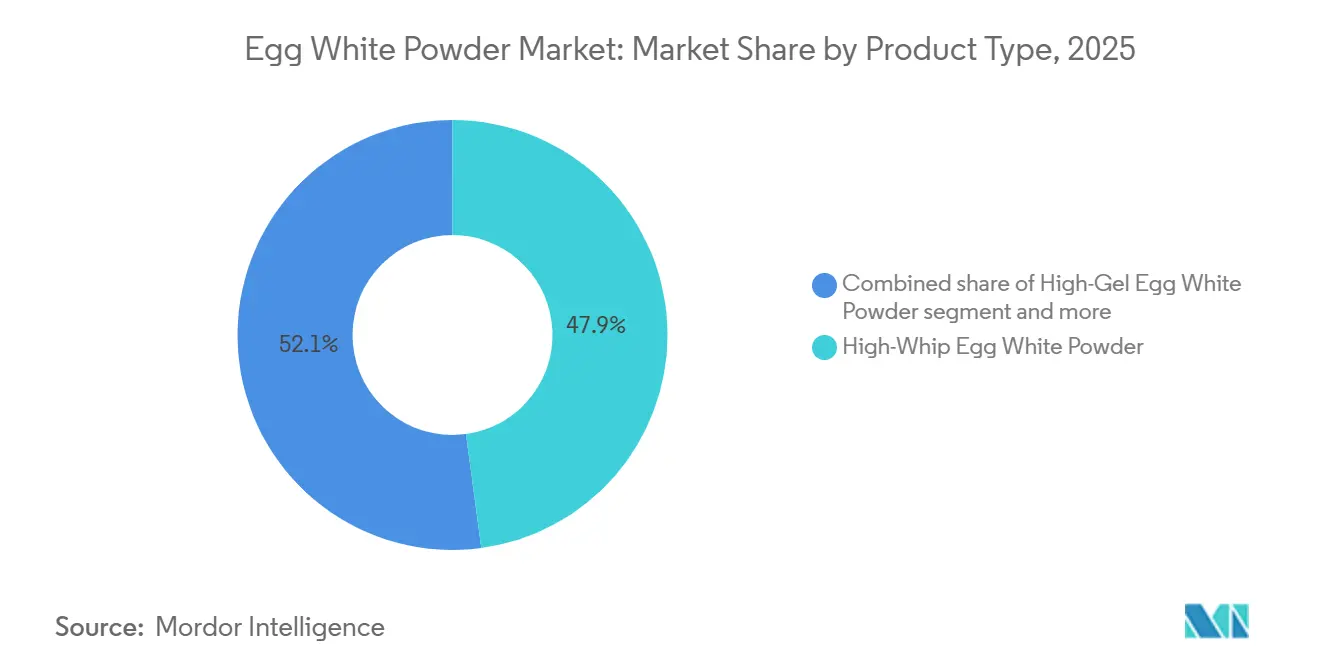

- By product type, high-whip powder commanded 47.86% of the egg white powder market share in 2025, while high-gel variants are projected to advance at a 6.07% CAGR between 2026-2031.

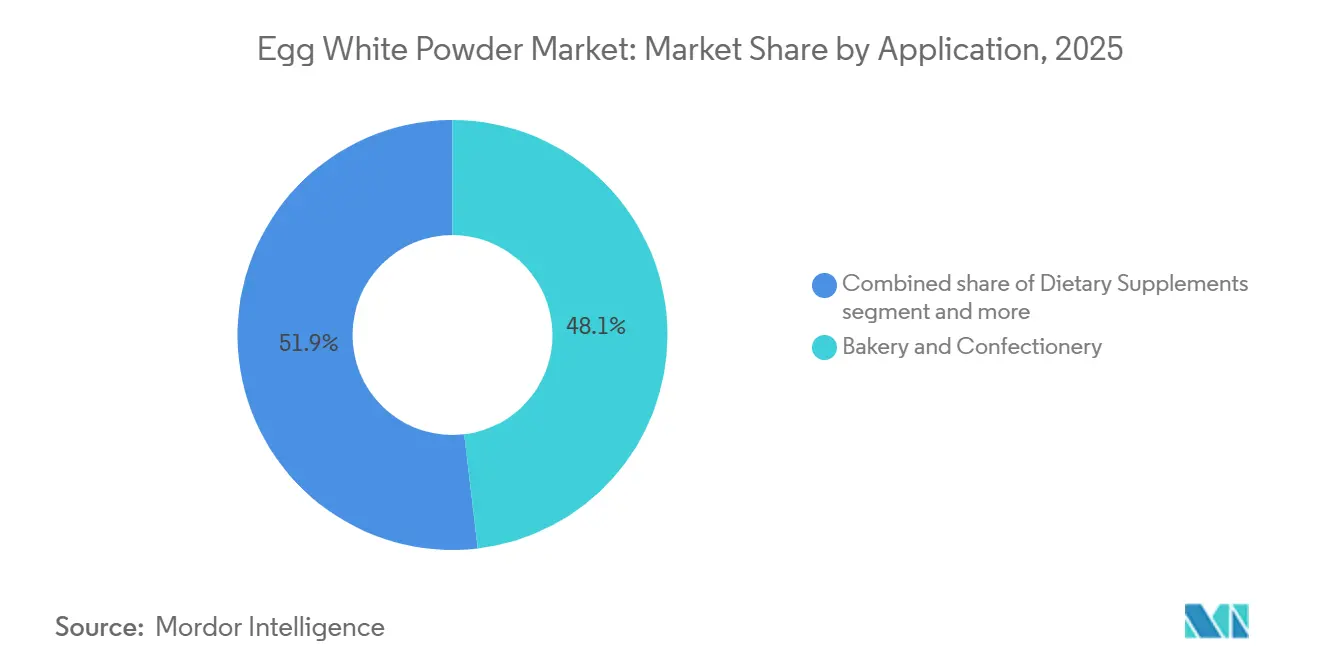

- By application, bakery and confectionery led with 48.12% of 2025 revenue; dietary supplements are expected to expand at a 7.21% CAGR through 2031.

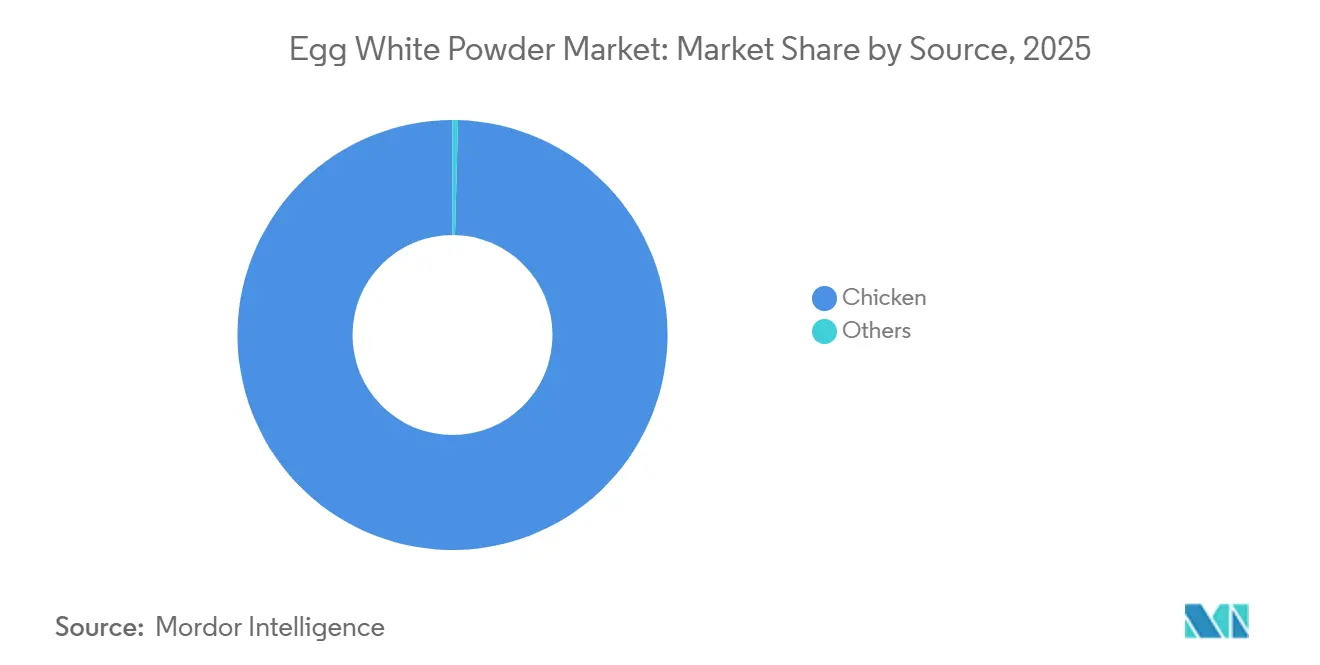

- By source, chicken-derived powder held a 99.56% share of the egg white powder market size in 2025, and exhibited a 5.30% CAGR to 2031.

- By geography, Europe dominated with 32.25% of 2025 revenue, while South America is forecast to post a 6.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Egg White Powder Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Protein-Rich Diet Trends | +1.8% | Global, with the strongest impact in North America and Europe | Medium term (2-4 years) |

| Functional Properties in Food Processing | +1.5% | Global, particularly Asia-Pacific food manufacturing hubs | Long term (≥ 4 years) |

| Increasing Demand for Clean-Label Ingredients | +1.2% | North America and Europe, expanding to Asia-Pacific urban markets | Medium term (2-4 years) |

| Expansion of Dietary Supplements and Sports Nutrition | +1.0% | Global, with early gains in North America, Europe, Australia | Short term (≤ 2 years) |

| Technological Advancements in Processing | +0.8% | Global, concentrated in developed manufacturing regions | Long term (≥ 4 years) |

| Growing Bakery and Confectionery Industry | +0.9% | Asia-Pacific core, spill-over to the Middle East and Africa, and Latin America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Growth in Protein-Rich Diet Trends

Consumer protein intake patterns shifted dramatically, with average U.S. consumption reaching 97 grams daily for males and 69 grams for females, maintaining animal protein's 64% share of total intake, according to the the Agricultural Research Service (ARS), a research agency of the U.S. Department of Agriculture (USDA). This stability contradicts predictions of plant protein dominance, as egg white powder's complete amino acid profile and 1.0 protein digestibility score position it advantageously against incomplete plant alternatives. The trend toward high-protein diets creates sustained demand across demographics, with egg white powder serving as a neutral-tasting, highly soluble protein source that integrates seamlessly into beverages and processed foods. European consumption patterns show similar resilience, with protein intake correlating positively with GDP per capita, suggesting continued growth in developed markets Wiley Online Library. Rising health consciousness drives consumers toward recognizable protein sources, favoring egg white powder over synthetic alternatives in premium product formulations.

Functional Properties in Food Processing

Egg white powder's irreplaceable functional characteristics drive sustained industrial demand despite price volatility and supply constraints. Recent research demonstrates that citric acid treatment can enhance foaming capacity by increasing protein hydrophobicity and free sulfhydryl content, enabling applications in 3D food printing and customized texture development. The protein's unique combination of gelation, emulsification, and foaming properties cannot be fully replicated by single plant proteins, requiring complex blends that often compromise cost-effectiveness. Food processors increasingly rely on egg white powder's consistent functionality across temperature ranges and pH conditions, particularly in large-scale manufacturing where batch-to-batch variation must be minimized. Advanced spray-drying techniques now preserve more native protein structure, maintaining functional properties while extending shelf life beyond traditional limitations.

Increasing Demand for Clean-Label Ingredients

Clean-label requirements intensified following FDA's February 2025 implementation of updated "healthy" food definitions, which favor recognizable ingredients like egg white powder over synthetic alternatives Federal Register. Consumer trust in recognizable ingredients accelerates the shift away from synthetic additives, while regulatory bodies raise quality benchmarks that favor suppliers able to certify sustainability and traceability. For instance, according to the International Food Information Council, in 2023, approximately 29% of respondents in the United States mentioned that they buy food and beverages on a regular basis because they are labeled as “clean ingredients”. Egg white powder's single-ingredient profile appeals to manufacturers seeking clean-label compliance without sacrificing functionality, particularly as regulatory scrutiny increases on artificial additives and processing aids. The ingredient's natural origin and minimal processing requirements align with consumer preferences for "real food" ingredients, creating competitive advantages over chemically modified protein isolates. Brazilian regulations on emerging ingredients for clean-label products emphasize proper labeling and traceability, standards that established egg white powder suppliers can meet more easily than novel protein developers.

Expansion of Dietary Supplements and Sports Nutrition

The sports nutrition sector's growth accelerates egg white powder adoption as formulators seek complete protein sources with rapid absorption characteristics. Precision fermentation alternatives like EVERY's egg white protein demonstrate the market's willingness to pay premiums for egg protein functionality, even from non-animal sources. Dietary supplement manufacturers increasingly specify egg white powder for its neutral taste profile and high solubility, enabling clear protein beverages that compete with whey-based products. The ingredient's naturally occurring lysozyme content provides additional antimicrobial benefits, extending product shelf life without synthetic preservatives. Regulatory approval processes favor established ingredients like egg white powder over novel proteins requiring extensive safety documentation, accelerating time-to-market for new supplement formulations. Moreover, supporting this trend, data from the government and associations highlight the rising demand for dietary supplements and sports nutrition. For instance, the Council for Responsible Nutrition’s October 2024 Consumer Survey revealed that 74% of U.S. adults turn to dietary supplements. Similarly, according to the Office for National Statistics (UK), in 2023, the sales volume of protein concentrates increased to approximately 96 thousand tons[2]Source: Office for National Statistics (UK), "UK manufacturers' sales by product", www.ons.gov.uk.

Restrains Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Alternative Proteins | -1.4% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Price Volatility of Raw Materials | -1.1% | Global, most severe in North America | Short term (≤ 2 years) |

| Shelf-Life Limitations | -0.6% | Global, particularly in tropical and humid regions | Long term (≥ 4 years) |

| Possible Off-Flavors or Odors | -0.4% | Global, concentrated in premium product segments | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Competition from Alternative Proteins

Plant-based protein alternatives intensify competitive pressure, with companies like Fudi Protein developing RuBisCo-based egg white replacements that promise identical functional properties at potentially lower environmental costs. Precision fermentation technologies enable the production of bioidentical ovalbumin without animal agriculture, with Onego Bio's Bioalbumen achieving over 90% protein content and complete amino acid profiles. Pulse protein concentrates demonstrate effectiveness as egg replacers in specific applications, with soy concentrate showing particular promise in pancake formulations Springer. In line with this, an increased production of respective alternative ingredients is further posing a threat to the market's growth. According to the Japan Plant Factory Association, in 2024, the domestic production volume of powdered concentration of soy proteins in Japan amounted to 183 tons, increased from 97 tons in the previous year[3]Source: Japan Plant Factory Association, "Plant protein production, shipping and in-house use", www.protein.or.jp. However, cost parity remains elusive for most alternatives, and functional performance gaps persist in demanding applications like high-volume commercial baking. The competitive threat intensifies as venture capital funding flows toward alternative protein startups, potentially accelerating technological breakthroughs that could disrupt egg white powder's market position.

Price Volatility of Raw Materials

Highly pathogenic avian influenza created unprecedented price volatility, with wholesale egg prices reaching USD 5.91 per dozen and the USDA forecasting an additional 20.3% increase in 2025. The loss of birds demonstrates the industry's vulnerability to disease outbreaks, with concentrated production facilities amplifying supply disruptions. U.S. egg production declined 1-4% year-over-year in 2024, while demand remained stable, creating sustained upward price pressure that affects powder production economics, according to the United States Department of Agriculture National Agricultural Statistics Service. Price volatility complicates long-term supply contracts and forces food manufacturers to consider alternative ingredients, potentially eroding egg white powder's market share in price-sensitive applications. The concentration of egg production among fewer, larger operations increases systemic risk, as single facility outbreaks can significantly impact regional supply chains.

Segment Analysis

By Product Type: High-Whip Dominance Faces Gel Innovation

High-whip egg white powder commands 47.86% market share in 2025, reflecting its critical role in bakery and confectionery applications where foaming properties remain irreplaceable. The segment's dominance stems from industrial baking requirements for consistent leavening and structure formation, applications where plant-based alternatives consistently underperform in commercial-scale production. High-gel egg white powder demonstrates the strongest growth potential at 6.07% CAGR through 2031, driven by expanding meat processing applications and clean-label binding solutions that replace synthetic additives.

Recent innovations in citric acid treatment enhance high-whip powder's foaming characteristics, enabling new applications in 3D food printing and customized texture development that extend beyond traditional bakery uses. High-gel variants benefit from technological advances in spray-drying conditions, with optimal inlet temperatures and flow rates improving gel strength and water-holding capacity crucial for meat processing applications. The functional property divide between high-whip and high-gel variants creates distinct market segments with limited substitutability, supporting pricing power for specialized applications.

By Application: Dietary Supplements Segment Disrupts Bakery Leadership

The escalating demand for egg white powder (EWP) within the bakery and confectionery sectors, accounting for 48.12% of 2025 revenue, stems from its superior functionality over liquid or plant-based alternatives. EWP offers concentrated ovalbumen, a protein essential for structural aeration and stable foaming in high-ratio cakes and meringues. This trend is supported by safety standards from bodies like the USDA and EFSA, advocating pasteurized powders to eliminate Salmonella risks. For instance, Eurovo Group’s 2024 launch of "Extra-Whip" EWP targets high-humidity commercial bakeries. Additionally, the International Egg Commission (IEC) notes EWP reduces storage and transport costs by up to 75%, prompting Rose Acre Farms' 2024 acquisition of spray-drying facilities to focus on the stable B2B bakery channel.

The dietary supplements segment is projected to grow at a 7.21% CAGR through 2031, driven by the "Clean Label" movement and egg protein's superior biological value. With a PDCAAS of 1.0, egg white protein is a "gold standard" for lactose-intolerant athletes and health-conscious consumers. Supporting this, Egglife Foods in 2025 expanded its patented egg-white technology into the dry-mix category for high-protein, zero-carb home baking. Technological advancements like Sanovo Technology Group’s 2026 "Low-Energy Pasteurization" aim to improve protein retention by 15%, targeting the 2026–2031 supplement growth window.

By Source: Chicken Supremacy Driven by Innovation

The dominance of chicken-derived powder, expected to hold a 99.56% market share in 2025, stems from the global poultry industry's established infrastructure and the biological standard set by Gallus gallus domesticus eggs. According to the International Egg Commission (IEC), chicken eggs are the only source capable of meeting the industrial scale required for global food processing, as alternative avian sources (like duck or quail) lack the protein consistency and cost-efficiency needed for B2B applications. This dominance is further supported by USDA grading and pasteurization protocols tailored to chicken eggs, creating a regulatory "moat" for manufacturers. A key example is Cal-Maine Foods’ 2025 expansion of egg processing facilities after acquiring ISE America assets, aimed at boosting chicken-derived powder output to meet the projected 5.30% CAGR through 2031.

Growth in this segment is also driven by the "functional gold standard" of chicken egg whites, rich in ovalbumin, which provides superior gelling and binding properties for the meat and bakery industries. While lab-grown or plant-based egg alternatives have emerged, the American Egg Board highlights chicken-derived EWP as the most bioavailable and "clean-label" protein, with a PDCAAS of 1.0. To leverage this, Eurovo Group in 2024 launched an "Extra-Whip" chicken egg white powder using proprietary pasteurization for enhanced stability in extreme climates. Additionally, the industry is shifting toward specialized chicken powders; for instance, Moba Group’s 2025 acquisition of a functionalized powder startup enabled tailored whipping speeds, reinforcing chicken sources' dominance over niche avian alternatives.

Geography Analysis

Europe’s 32.25% revenue share in 2025 stems from its advanced food processing infrastructure and stringent "Clean Label" regulations. The European Food Safety Authority (EFSA) enforces strict standards on animal welfare and food traceability, driving manufacturers toward high-quality, pasteurized egg white powder (EWP). The European Union’s "Farm to Fork" strategy further supports this shift by promoting sustainable, shelf-stable ingredients to reduce food waste. Eurovo Group’s 2024 launch of "Extra-Whip" chicken EWP in Italy highlights the region’s focus on meeting precise aeration needs in the high-end confectionery sector. Additionally, strategic acquisitions, such as Moba Group’s 2025 purchase of a functionalized powder startup, enable European producers to offer tailored "designer" powders, reinforcing their market leadership.

South America is projected to grow at a 6.86% CAGR through 2031, transitioning from raw commodity exports to high-value ingredient processing. Brazil and Argentina are expanding drying capacities to leverage their poultry sectors, as noted by ALA (Asociación Latinoamericana de Avicultura). Cal-Maine Foods' 2025 partnerships in South America secure a "counter-seasonal" egg supply, ensuring year-round EWP availability. European technology, such as Sanovo Technology Group’s 2026 "Low-Energy Pasteurization" lines in Brazil, boosts protein integrity and export potential. Combined with lower production costs, South American firms are targeting the dietary supplement market, which values egg protein’s PDCAAS 1.0 rating.

Regional divergence is shaped by supply chain strategies. Europe focuses on premiumization, while South America scales for volume and reliability. A notable example is the 2024 partnership between Iscon Balaji Foods (Hungritos) and South American processors to source cost-effective EWP for global appetizer coatings, ensuring product crispiness despite fluctuating European egg prices. Granja Tres Arroyos’ 2024 acquisition of spray-drying facilities signals South America’s move toward industrializing its egg supply chain. By 2026, as South American facilities align with USDA and EFSA standards, the region is set to challenge established players, sustaining its growth trajectory through the decade.

Competitive Landscape

The global egg white powder market remains moderately fragmented. Major players in the market include Royal Van Beek Group, Wulms Egg Group, Agroholding Avangard, Ovobrand S.A., and Rembrandt Foods. The leadership of Royal Van Beek and Wulms Egg Group is supported by strong export-oriented operations, vertically integrated sourcing, and a focus on high-quality spray-dried egg white powders tailored for bakery, sports nutrition, and confectionery applications. Between 2024 and 2026, leading European processors have prioritized capacity modernization, automation upgrades, and expansion of pasteurization and drying facilities to enhance output efficiency and meet growing demand from protein-fortified food manufacturers.

Strategically, major players are increasingly differentiating through product innovation and functional customization. Rembrandt Foods and Ovobrand S.A., for instance, have emphasized high-gelling, high-foaming, and heat-stable egg white powder variants designed for clean-label bakery and high-protein beverage applications. From 2024 onward, companies have expanded into specialty segments such as instantized egg white powders for sports nutrition and ready-to-mix formulations for industrial customers. Agroholding Avangard has leveraged its integrated poultry operations to strengthen cost competitiveness, while also investing in export partnerships across Asia and the Middle East to diversify geographic revenue streams. Sustainability initiatives, including cage-free sourcing, carbon footprint reduction programs, and traceability certifications, have also become central competitive levers, particularly in European and North American markets.

Given that over half of the market is controlled by smaller regional players, competitive intensity remains high, with consolidation opportunities emerging. From 2024 to 2026, the industry has seen strategic collaborations between egg processors and food ingredient distributors to improve supply chain resilience and expand private-label offerings. Larger players are exploring acquisitions of smaller drying facilities to enhance regional presence and reduce logistics costs. Additionally, partnerships with sports nutrition brands and functional food manufacturers are strengthening demand visibility for high-protein applications. Overall, the competitive landscape is evolving toward scale efficiencies, specialty functionality, and sustainability-driven positioning, as leading companies seek to protect margins amid raw material price volatility and shifting consumer preferences toward high-protein, clean-label products.

Egg White Powder Industry Leaders

-

Royal Van Beek Group

-

Wulms Egg Group

-

Agroholding Avangard

-

Ovobrand S.A.

-

Rembrandt Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bouwhuis-Enthoven launched a tailored suite of customizable egg white powder solutions for industrial and bakery applications. The new products focused on delivering specific functional benefits—such as tailored whipping and gelling properties—adapted to unique customer formulations.

- January 2025: Judee’s Gluten Free updated and relaunched their classic dried egg white powder in a new resealable, stand-up pouch format. Made with 100% dried egg whites and no additives, the relaunch highlighted freshness, gluten-free production facilities, and improved storage. The packaging update targets increased shelf-life demands and retail convenience for home bakers and foodservice.

- October 2024: SKM Egg Products launched a premium, pasteurized egg white powder line formulated specifically for health and fitness supplement markets. These new products emphasize protein purity, excellent flavor neutrality, and improved safety due to advanced pasteurization methods. They cater to athletes and health-conscious consumers seeking high-quality, functional protein ingredients for shakes and supplements.

- June 2024: Pulviver SPRL introduced a range of instant egg white powders with enhanced solubility and superior foam stability, targeted at the industrial bakery and dessert sectors. The innovation is credited to advances in spray-drying and freeze-drying, resulting in clean-label powders that reconstitute rapidly in water with exceptional functional performance. These powders were asserted to significantly improve efficiency for industrial users and help to extend the shelf life of processed products.

Global Egg White Powder Market Report Scope

| High-Whip Egg White Powder |

| High-Gel Egg White Powder |

| Standard Egg White Powder |

| Bakery and Confectionery |

| Dietary Supplements |

| Meat and processed foods |

| Sauces, Dressings, and Spreads |

| Dairy and Frozen Desserts |

| Other Applications |

| Chicken |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | High-Whip Egg White Powder | |

| High-Gel Egg White Powder | ||

| Standard Egg White Powder | ||

| By Application | Bakery and Confectionery | |

| Dietary Supplements | ||

| Meat and processed foods | ||

| Sauces, Dressings, and Spreads | ||

| Dairy and Frozen Desserts | ||

| Other Applications | ||

| By Source | Chicken | |

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the egg white powder market in 2026?

The egg white powder market size is expected to grow from USD 316.17 million in 2025 to USD 331.90 million in 2026 and is forecast to reach USD 429.27 million by 2031 at a 5.29% CAGR over 2026-2031.

What is driving growth in South America?

Rapid expansion of food-processing capacity and rising protein consumption push South America growth to a 6.86% CAGR through 2031.

Which product type leads sales?

High-whip powder holds 47.86% of global revenue owing to its irreplaceable foaming performance in bakery and confectionery.

How are companies managing supply risk?

Leading producers are acquiring upstream farms and installing advanced pasteurization to secure raw eggs and maintain quality during outbreaks.

What role do clean-label trends play?

Tighter labeling rules favor egg white powder because it is a single, recognizable ingredient that meets updated “healthy” criteria.

Are plant proteins a major threat?

Alternative proteins are improving, but cost parity and exact functional matching remain challenges, limiting market displacement through 2030.

Page last updated on: