Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.48 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

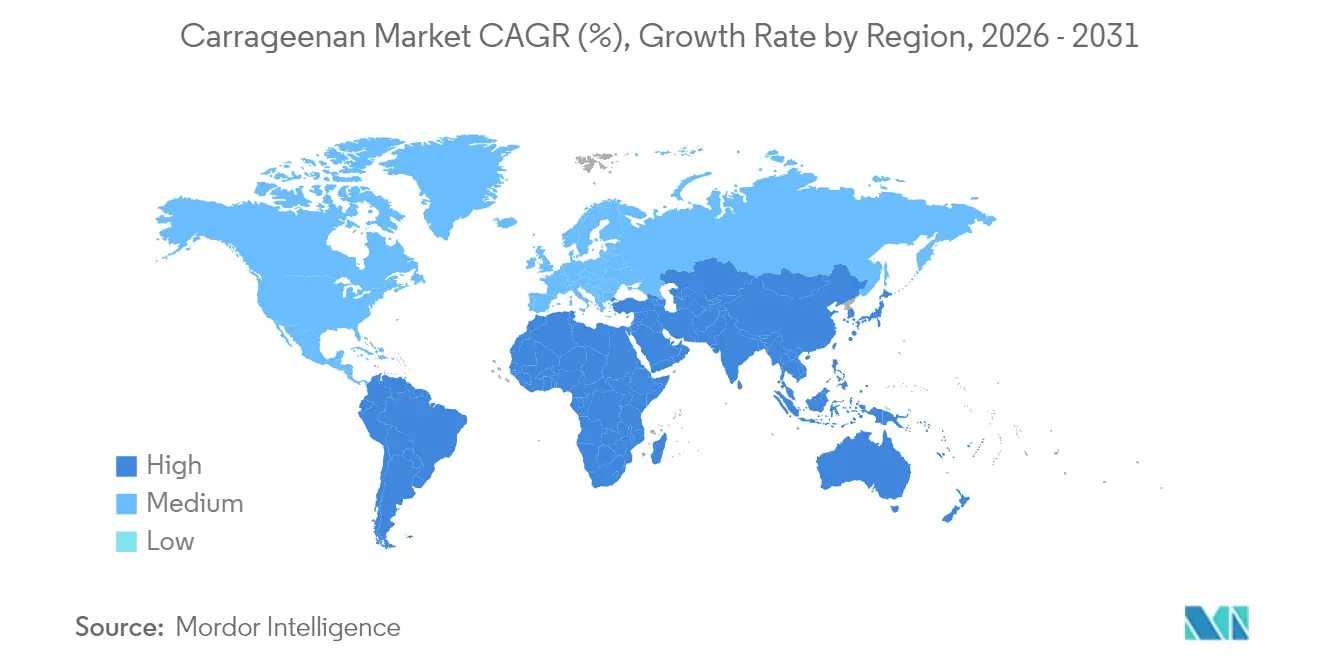

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Carrageenan Market Analysis by ���ϲ�����

The Carrageenan market size is expected to increase from USD 1.06 billion in 2025 to USD 1.12 billion in 2026 and reach USD 1.48 billion by 2031, growing at a CAGR of 5.73% over 2026-2031. Demand for natural hydrocolloids in clean-label foods, pharmaceutical excipients, and personal-care formulas is outpacing supply additions, tightening the Carrageenan market even as semi-refined grades expand capacity in China and Indonesia. Consolidation among Western suppliers is reshaping bargaining power after Tate & Lyle absorbed CP Kelco and Roquette bought IFF’s Pharma Solutions, integrating pectin, alginate, and carrageenan portfolios and giving multinationals leverage in high-purity niches. Raw-seaweed price volatility, triggered by climate-related harvest shocks in Southeast Asia, continues to squeeze processor margins, making direct farmer partnerships and traceability systems central to risk management. Meanwhile, the European Commission’s draft limits on infant-food carrageenan are raising compliance costs, but they also create technical barriers that favor vertically integrated processors with GMP-certified facilities.

Key Report Takeaways

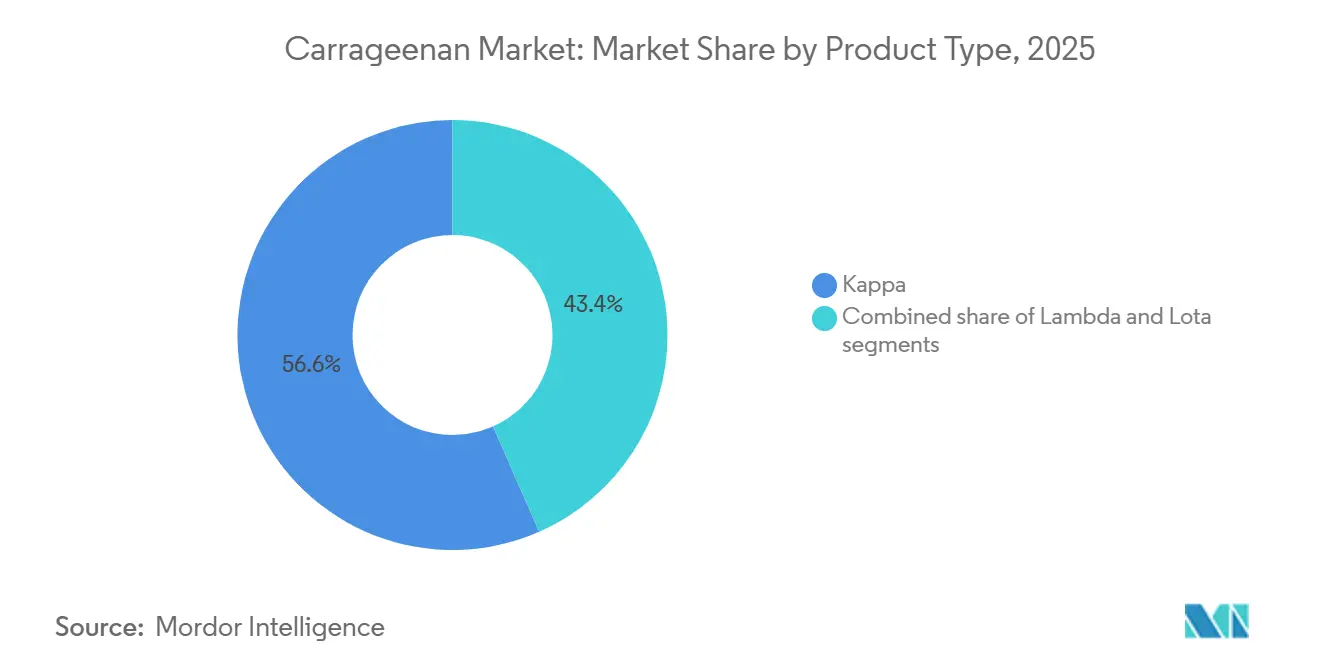

- By type, kappa held 56.62% of the Carrageenan market size in 2025; lambda is advancing at a 6.50% CAGR to 2031.

- By processing grade, semi-refined captured 35.74% of the Carrageenan market share in 2025, whereas refined grades are forecast to grow at a 6.71% CAGR to 2031.

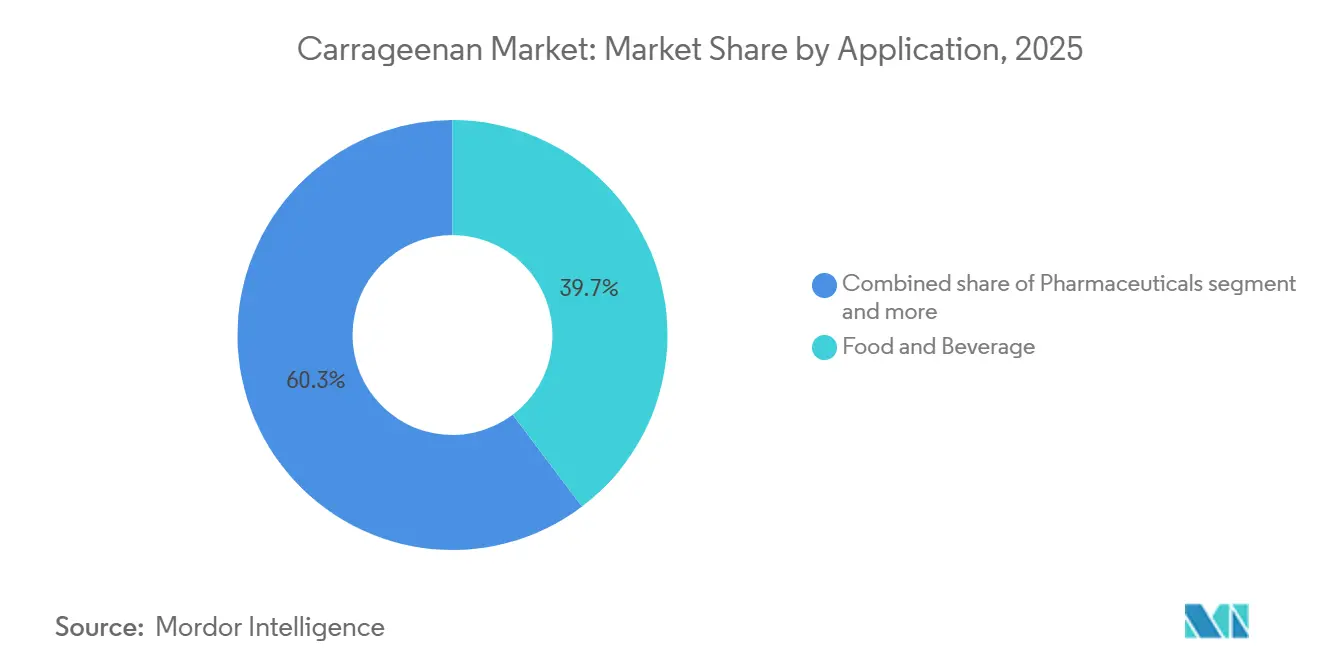

- By application, food and beverage led with 39.71% revenue share in 2025; personal care and cosmetics are the fastest-growing end-use at 6.42% CAGR to 2031.

- By geography, Europe commanded 33.43% of the Carrageenan market share in 2025, while Asia-Pacific is projected to expand at a 6.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carrageenan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean label moment fueling demand for natural thickener in processed food industry | +1.5% | Global, with strongest influence in North America and Europe | Medium term (2-4 years) |

| Expanding dairy alternatives sector driving usage of kappa and Iota type carrageenan | +1.2% | North America, Europe, Urban Asia-Pacific | Medium term (2-4 years) |

| Widespread use as a fat replacer in low-calorie food | +0.9% | Global, with emphasis on developed markets | Medium term (2-4 years) |

| Shelf-life extension and stabilizing | +0.7% | Global, with higher impact in regions with developing cold chain infrastructure | Short term (≤ 2 years) |

| Increasing demand in gluten-free and allergen-free products | +0.6% | North America, Europe, Australia | Medium term (2-4 years) |

| Preference for seaweed-based ingredients in natural formulation | +0.5% | Global, with stronger presence in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Clean label moment fueling demand for natural thickener in processed food industry

Globally, the clean label movement is reshaping how ingredients are chosen, with significant insights provided by CBI, the Ministry of Foreign Affairs. Their research highlights this ongoing transformation, forecasting that the share of clean-label products in portfolios will jump from 52% in 2021 to over 70% by 2025 and 2026 [1]CBI Ministry of Foreign Affairs, "Which trends offer opportunities or pose a threat on the European natural food additives market?", cbi.eu. This uptick is driven by consumers' heightened scrutiny of product ingredients, spurring a demand for clean-label ingredients that are natural, minimally processed, and free from artificial additives. Seaweed-derived ingredients are now increasingly supplanting synthetic stabilizers and thickeners in processed foods, as manufacturers cater to the consumer preference for recognizable, plant-based components. The clean label moment's influence stretches beyond mere ingredient choices, reshaping entire supply chains. For instance, Cargill has rolled out traceability programs for its carrageenan sources. Additionally, a noteworthy ripple effect is the rise of hybrid clean-label solutions, blending carrageenan with other natural ingredients to replicate functionalities once exclusive to synthetic additives.

Expanding dairy alternatives sector driving usage of kappa and Iota type carrageenan

The explosive growth of the dairy alternatives market is creating unprecedented demand for carrageenan, particularly kappa and iota types, which provide crucial stability and mouthfeel in plant-based milks and yogurts. Lambda carrageenan is particularly effective in plant-based milks, creating a texture remarkably similar to dairy through its interaction with plant proteins, while preventing separation and ensuring consistent quality throughout shelf life. The technical challenge of replicating dairy's complex sensory attributes has positioned carrageenan as an essential ingredient, with manufacturers developing specialized grades specifically optimized for alternative dairy applications. Interestingly, the functionality of carrageenan in plant-based products often exceeds its performance in traditional dairy, creating a competitive advantage for alternative products in terms of texture stability and shelf life. This functional superiority is driving innovation in specialized carrageenan blends designed to address the unique challenges of specific plant protein sources, from soy and almond to emerging options like pea and oat.

Widespread use as a fat replacer in low-calorie food

The increasing use of carrageenan as a fat replacer in low-calorie foods is a significant driver of the carrageenan market. Governments and health organizations worldwide are promoting the consumption of low-calorie and low-fat foods to combat rising obesity rates and related health issues. For instance, the World Health Organization (WHO) has consistently emphasized the need for reducing calorie intake to address global health concerns. Additionally, regulatory bodies such as the US Food and Drug Administration (FDA) have approved carrageenan as a safe food additive, further encouraging its adoption in the food industry. The National Institute of Health also supports the use of carrageenan due to its functional properties, including its ability to replace emulsifying salts without compromising texture or taste [2]National Institute of Health, "Carrageenan as a functional additive in the production of cheese and cheese-like products", ncbi.nlm.nih.gov. These factors collectively drive the demand for carrageenan in the production of low-calorie food products.

Shelf-life extension and stabilizing properties driving adoption

Carrageenan's multifunctional properties as a stabilizer, thickener, and gelling agent are revolutionizing food preservation strategies, with recent studies demonstrating its ability to extend shelf life by up to 8 days in certain applications. Beyond simply preventing physical separation in emulsions, carrageenan creates protective barriers that inhibit moisture migration and microbial growth, addressing multiple deterioration mechanisms simultaneously. When incorporated into edible films and coatings, carrageenan demonstrates significant antimicrobial and antioxidant properties, effectively protecting foods from spoilage while maintaining quality parameters. The integration of carrageenan with nanoparticles like SiO2 and ZnO has shown remarkable enhancement of water vapor barrier properties and antimicrobial activity, creating next-generation packaging solutions that actively extend product freshness. This multifunctional approach to shelf-life extension is particularly valuable in high-moisture foods where conventional preservatives face limitations, positioning carrageenan as a critical tool in reducing food waste while meeting clean label requirements

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent product quality across processing grade | -0.9% | Global, with higher impact in regions sourcing from multiple suppliers | Medium term (2-4 years) |

| Low awareness in emerging economies | -0.6% | Africa, South America, Southeast Asia | Medium term (2-4 years) |

| Concern over sustainability and marine ecosystem impact | -0.5% | Global, with particular emphasis on coastal producing regions | Long term (≥ 4 years) |

| High cost associated with the purified grade | -0.4% | Global, with greater impact in price-sensitive markets | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Inconsistent product quality across processing grades

In the carrageenan market, inconsistent product quality across different processing grades acts as a significant market restraint. Variations in quality can arise due to differences in raw material sourcing, processing techniques, and adherence to quality standards. These inconsistencies can impact the performance of carrageenan in various applications, such as food, pharmaceuticals, and cosmetics, leading to challenges for manufacturers and end-users. For instance, in the food industry, variations in carrageenan quality can affect the texture, stability, and shelf life of products, which can result in customer dissatisfaction and potential financial losses for manufacturers. Similarly, in the pharmaceutical sector, inconsistent quality can compromise the efficacy and safety of products, posing risks to consumer health and regulatory compliance. Furthermore, the cosmetics industry, which relies on carrageenan for its thickening and stabilizing properties, may face issues with product consistency and performance due to quality variations. Ensuring uniform quality across all grades is critical for maintaining customer trust, meeting regulatory requirements, and achieving operational efficiency. However, achieving this remains a persistent challenge for the industry, as it requires significant investments in quality control measures, advanced processing technologies, and robust supply chain management.

Low awareness in emerging economies limiting market expansion

Despite carrageenan's versatility and functional benefits, limited awareness in emerging economies creates significant market penetration barriers, particularly in regions that could benefit most from its shelf-life extension properties. The knowledge gap extends beyond consumers to food manufacturers in these regions, who often lack technical understanding of carrageenan's applications and optimal usage parameters, resulting in suboptimal implementation or complete avoidance of this ingredient. This awareness deficit is exacerbated by fragmented distribution networks in many emerging markets, creating accessibility challenges that further restrict carrageenan adoption. Educational initiatives by industry leaders are beginning to address this restraint, with companies like CP Kelco and Cargill implementing technical training programs for food manufacturers in Southeast Asia and Africa. According to the Food and Agriculture Organization (FAO)The establishment of regional application laboratories in emerging markets represents a strategic approach to overcoming awareness limitations, providing local manufacturers with hands-on experience and technical support that can accelerate carrageenan adoption [3]The Food and Agriculture Organization (FAO), "Social and economic dimensions of carrageenan seaweed farming", fao.org.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Kappa Dominates While Lambda Accelerates

In 2025, Kappa carrageenan emerged as the leading segment, capturing 56.62% of the market revenue. This dominance is attributed to its strong, brittle gel-forming properties, which are critical for achieving the desired texture in a wide range of applications, including dairy desserts, processed meats, and confectionery products. Kappa carrageenan's ability to interact with casein in the presence of potassium ions enhances its functionality, particularly in stabilizing chocolate milk and preventing syneresis in puddings. These properties make it an indispensable ingredient for manufacturers aiming to improve product quality and shelf stability in these categories.

On the other hand, Lambda carrageenan is gaining traction in the market, with a CAGR of 6.50% through 2031. This growth is primarily driven by its unique cold-soluble functionality, which eliminates the need for a cooking step, making it highly suitable for ready-to-drink beverages. The convenience offered by Lambda carrageenan aligns with the growing consumer preference for time-saving and easy-to-use products, further boosting its adoption. Additionally, its ability to provide viscosity and mouthfeel without requiring heat processing has positioned it as a preferred choice for manufacturers looking to streamline production processes while maintaining product quality. As the demand for innovative and functional ingredients continues to rise, both Kappa and Lambda carrageenan are expected to play pivotal roles in shaping the future of the global carrageenan market.

By Processing Grade: Semi-Refined Leads While Refined Grows Fastest

In 2025, semi-refined carrageenan accounted for 35.74% of the global carrageenan market, primarily driven by its widespread use in the meat processing industry. Meat processors prefer semi-refined carrageenan due to its high cellulose content, which significantly enhances water-binding capacity, improving the texture and shelf life of processed meat products. This segment continues to dominate the market due to its cost-effectiveness and functional benefits in various food applications. Semi-refined carrageenan is also extensively used in other food products, such as dairy and bakery items, where its gelling, thickening, and stabilizing properties are highly valued. Its ability to improve the viscosity and consistency of food products makes it a preferred choice for manufacturers aiming to enhance product quality while optimizing production costs.

While semi-refined carrageenan maintains its leadership, refined grades are projected to experience robust growth, with a forecasted CAGR of 6.71% through 2031. This growth is attributed to increasing demand from the pharmaceutical, nutraceutical, and high-end dairy sectors, which require carrageenan with stricter microbial and heavy-metal specifications to meet regulatory and quality standards. Refined carrageenan is gaining traction in these industries due to its superior purity and functionality, making it suitable for applications such as drug formulations, dietary supplements, and premium dairy products like yogurts and desserts.

By Application: Food and Beverage Dominates While Personal Care Rises

In 2025, the food and beverage sector dominated the global carrageenan market, holding a significant 39.71% share. This dominance was primarily attributed to the extensive use of carrageenan in dairy and meat products, where its strong water-binding properties and ability to extend shelf life are critical. Carrageenan is widely utilized in the food industry for its functional benefits, such as preventing ice crystal formation in ice cream, which ensures a smoother texture, enhancing the aeration of whipped cream for improved consistency, and stabilizing particulate beverages to maintain uniformity and quality over time. These applications underscore its importance in meeting consumer demands for high-quality and long-lasting food products.

Meanwhile, the personal care sector, although representing a smaller portion of the global carrageenan market, is experiencing notable growth. This segment is advancing at a robust CAGR of 6.42%, driven by the increasing preference for vegan, sulfate-free, and texture-rich formulations. Carrageenan is gaining traction among formulators for its ability to create innovative products such as jelly cleansers and solid shower gels, which cater to evolving consumer preferences for sustainable and effective personal care solutions. The growing focus on environmentally friendly and cruelty-free products further supports the expansion of carrageenan applications in this sector, positioning it as a key ingredient in the development of modern personal care formulations.

Geography Analysis

In 2025, Europe commands a 33.43% share of the global carrageenan market, propelled by stringent clean-label regulations and advanced food-processing industries that appreciate carrageenan's natural origins and versatile functions. Europe's leadership is especially evident in dairy and meat sectors, where carrageenan plays a pivotal role as a stabilizer and texturizer in premium offerings. Germany, the UK, and France stand out as the top European markets, with Germany playing a dominant role in the region's carrageenan imports. European buyers show a marked preference for refined carrageenan grades that adhere to stringent quality and purity benchmarks, allowing suppliers to command premium prices.

Asia-Pacific is set to outpace others with a projected 6.52% CAGR from 2026-2031, driven by swift industrialization, a burgeoning food processing sector, and a growing consumer awareness of functional ingredients. China stands tall as both a leading producer and consumer, with its processing capabilities shaping global supply trends. Meanwhile, Indonesia and the Philippines emerge as pivotal raw material suppliers, together dominating global seaweed production for carrageenan extraction. Urban centers in China, Japan, and India are witnessing a surge in demand for convenience foods and dairy alternatives, further propelling the region's growth.

North America, while mature, is experiencing steady growth, with the U.S. at the forefront, thanks to its expansive food processing industry and a shift towards natural ingredients. Demand is particularly high for specialized carrageenan grades, especially in the burgeoning plant-based food arena. Mexico is carving out its niche, with a rising trend of carrageenan use in traditional dairy and processed meats. The clean label trend has reshaped North American offerings, with a spotlight on carrageenan's natural seaweed roots. Innovations abound, from using carrageenan for fat reduction in meats to its role as a stabilizer in plant-based drinks.

Competitive Landscape

Multinational giants and regional specialists dominate the global carrageenan market, resulting in a moderate concentration. Major players in the market include ACCEL Carrageenan Corporation, Cargill, TBK Manufacturing Corporation, Ingredion, and Marcel Trading Corporation. Leading players are increasingly turning to vertical integration, forging direct ties with seaweed farmers. This strategy not only ensures a steady raw material supply but also champions sustainability, responding to rising environmental concerns. For instance, Cargill has invested in initiatives to support seaweed farming communities while securing high-quality raw materials. Similarly, CP Kelco has partnered with local seaweed farmers to enhance supply chain efficiency and promote sustainable practices.

The spotlight of innovation shines on crafting specialized carrageenan grades, especially for the booming plant-based food sector. Here, manufacturers are tailoring solutions to meet the distinct challenges posed by alternative proteins. For example, DuPont (now part of IFF) has developed carrageenan solutions specifically designed for plant-based dairy alternatives, addressing texture and stability issues. Additionally, Marcel Carrageenan has introduced customized carrageenan blends for meat substitutes, catering to the growing demand for vegan and vegetarian products. Shemberg Marketing Corporation has also diversified its carrageenan offerings to cater to the pharmaceutical and personal care industries, where carrageenan is used as a stabilizer and thickening agent.

Strategic partnerships and acquisitions are shaping the competitive landscape further. For instance, Cargill’s acquisition of FMC’s carrageenan business has bolstered its position in the market, enabling it to offer a broader range of products. Meanwhile, Gelymar has strengthened its presence in the European market by introducing innovative carrageenan solutions tailored for bakery and confectionery applications. Partnerships between regional players and multinational companies are helping to bridge gaps in supply chains and enhance market penetration. These strategies are expected to drive growth and intensify competition during the forecast period.

Carrageenan Industry Leaders

-

TBK Manufacturing Corporation

-

Ingredion Incorporated

-

Cargill, Incorporated

-

Marcel Trading Corporation

-

Ingredion

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cargill launched Satiagel VPC614 kappa carrageenan, specifically formulated for personal-care emulsions, targeting the growing demand for marine-derived ingredients in skincare and oral-care products. The product offers film-forming, moisturizing, and thickening properties and is marketed as a natural, sustainable alternative to synthetic polymers, aligning with clean-beauty trends in Europe and North America.

- June 2024: Tate & Lyle acquired CP Kelco for USD 1.8 billion, closing the transaction in Q4 2024. The acquisition combines Tate & Lyle's sweetener and texturant portfolios with CP Kelco's hydrocolloid expertise (carrageenan, pectin, xanthan), creating a global ingredient platform with enhanced research and development capabilities and geographic reach. The deal is expected to drive cross-selling opportunities and accelerate innovation in plant-based and clean-label food applications.

- March 2024: Roquette agreed to acquire IFF's Pharma Solutions business for USD 2.85 billion, with the transaction expected to close in H1 2025. The acquisition includes carrageenan-based pharmaceutical excipients and positions Roquette as a leading supplier of plant-derived and seaweed-derived ingredients for drug-delivery systems, controlled-release tablets, and mucoadhesive formulations.

Global Carrageenan Market Report Scope

Carrageenan is a main ingredient that comes from red seaweed and is used a lot in the food industry. It is used for its gelling, thickening, and stabilizing properties. It has wide applications in both dairy and meat products. There are three categories for the global carrageenan market: type, application, and geography. Based on type, the market is segmented into kappa, lota, and lambda. Based on application, the market is segmented into the food industry, pharmaceutical industry, cosmetics industry, and other applications. Based on geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

Type

| Kappa |

| Lota |

| Lambda |

Processing Grade

| Refined |

| Semi-Refined |

| Alcohol Precipetation |

Application

| Food and Beverage | Dairy and Desserts |

| Meat and Poultry Products | |

| Sauces and Dressings | |

| Bakery and Confectionery | |

| Beverage | |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Others |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| Type | Kappa | |

| Lota | ||

| Lambda | ||

| Processing Grade | Refined | |

| Semi-Refined | ||

| Alcohol Precipetation | ||

| Application | Food and Beverage | Dairy and Desserts |

| Meat and Poultry Products | ||

| Sauces and Dressings | ||

| Bakery and Confectionery | ||

| Beverage | ||

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Carrageenan market by 2031?

The Carrageenan market is forecast to reach USD 1.48 billion by 2031.

Which region is expected to grow fastest through 2031?

Asia-Pacific is projected to post the strongest 6.52% CAGR, powered by rising middle-class food demand and new Indonesian capacity.

Why are refined grades growing faster than semi-refined?

Pharmaceutical and premium food clients require higher purity, pushing refined carrageenan toward a 6.71% CAGR versus slower semi-refined growth.

How will European regulation affect suppliers?

Draft EU limits on infant-food carrageenan tighten specifications, raising compliance costs and favoring vertically integrated processors with traceable supply chains.

Page last updated on: