Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.46 Billion |

| Market Size (2031) | USD 5.18 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

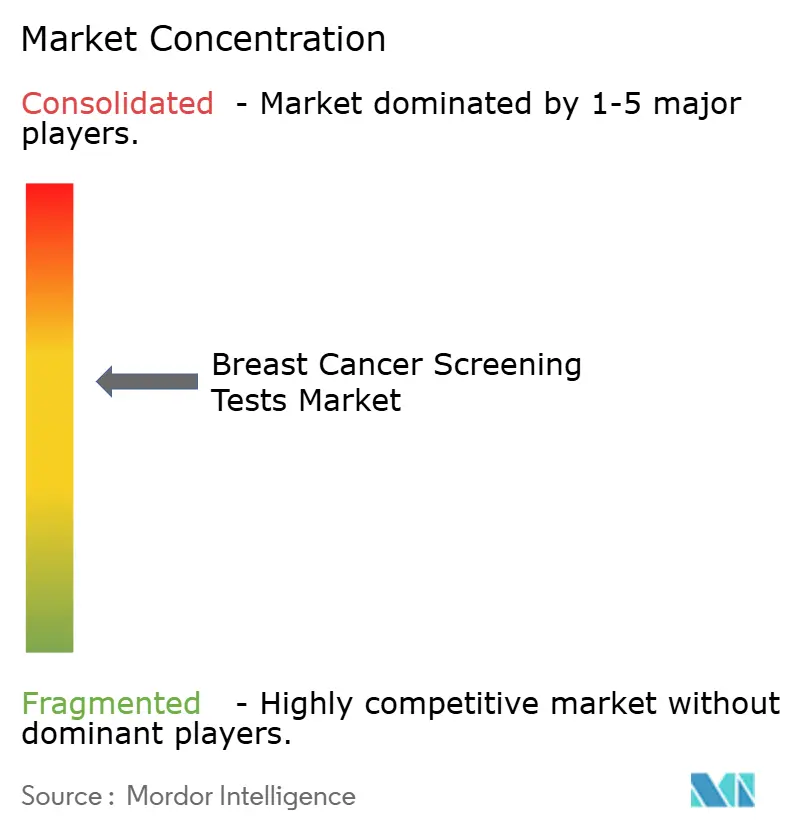

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Breast Cancer Screening Tests Market Analysis by ���ϲ�����

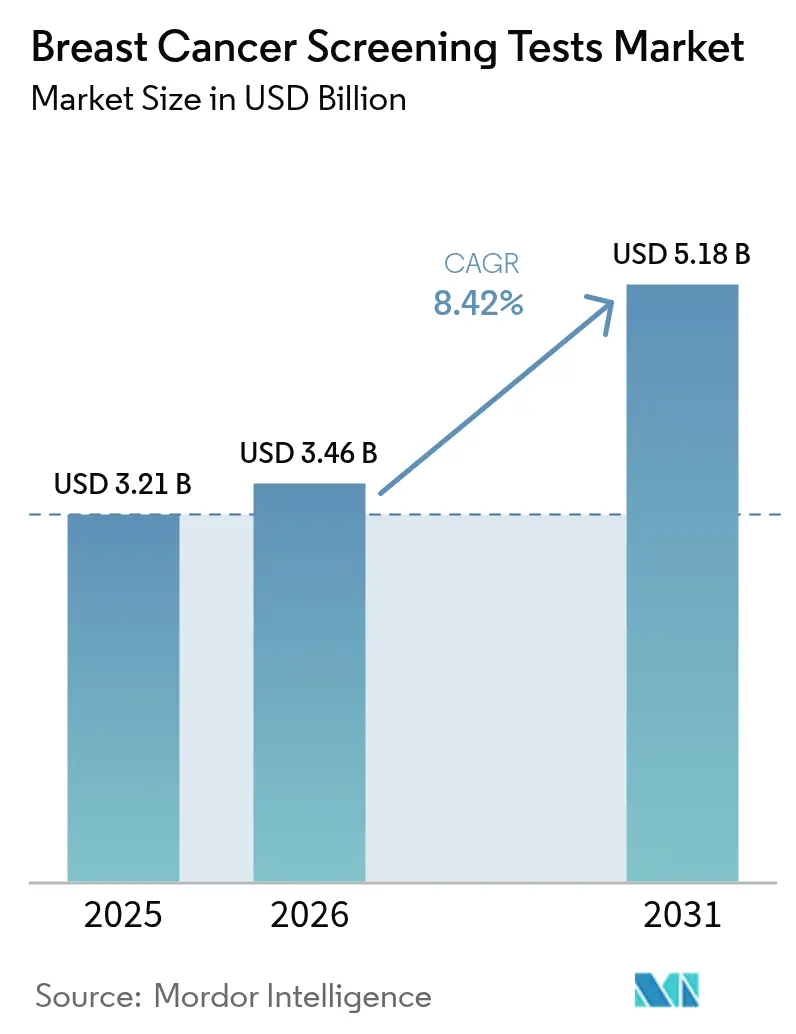

The Breast Cancer Screening Tests Market size is projected to be USD 3.21 billion in 2025, USD 3.46 billion in 2026, and reach USD 5.18 billion by 2031, growing at a CAGR of 8.42% from 2026 to 2031.

Expanded age-eligibility rules, faster artificial-intelligence triage, and approvals for blood-based biomarkers are widening the addressable population and boosting per-site throughput. National programs now cover women as young as 40, adding more than 20 million U.S. lives and tens of millions in Asia and Europe. Simultaneously, software that pre-reads images trims radiologist time by 30-40%, unlocking cost savings that providers redirect toward hardware upgrades. Liquid-biopsy platforms promise stage-I detection without radiation, a value proposition that is attracting both regulators and payers. Together, these levers are shifting the revenue mix from purely imaging toward a blended, multi-modal ecosystem anchored in precision risk assessment.

Key Report Takeaways

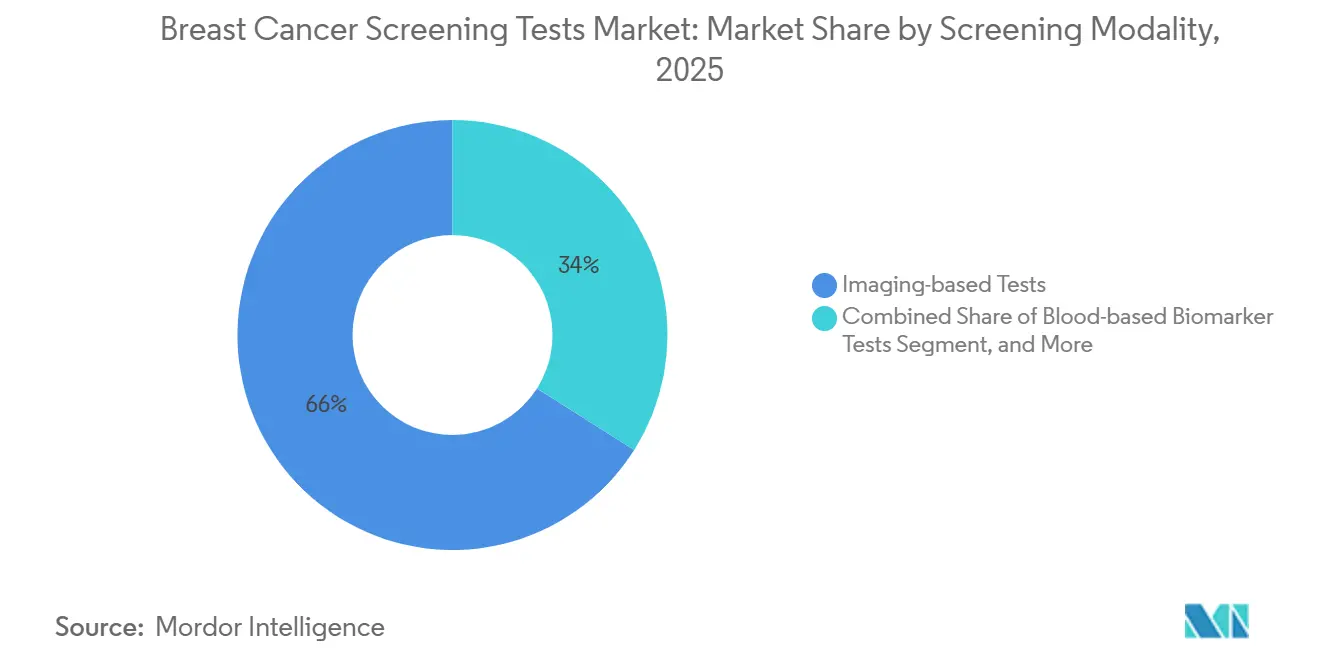

- By screening modality, imaging-based tests led with 66.02% of the breast cancer screening tests market share in 2025, and blood-based biomarker tests are projected to expand at a 9.06% CAGR to 2031.

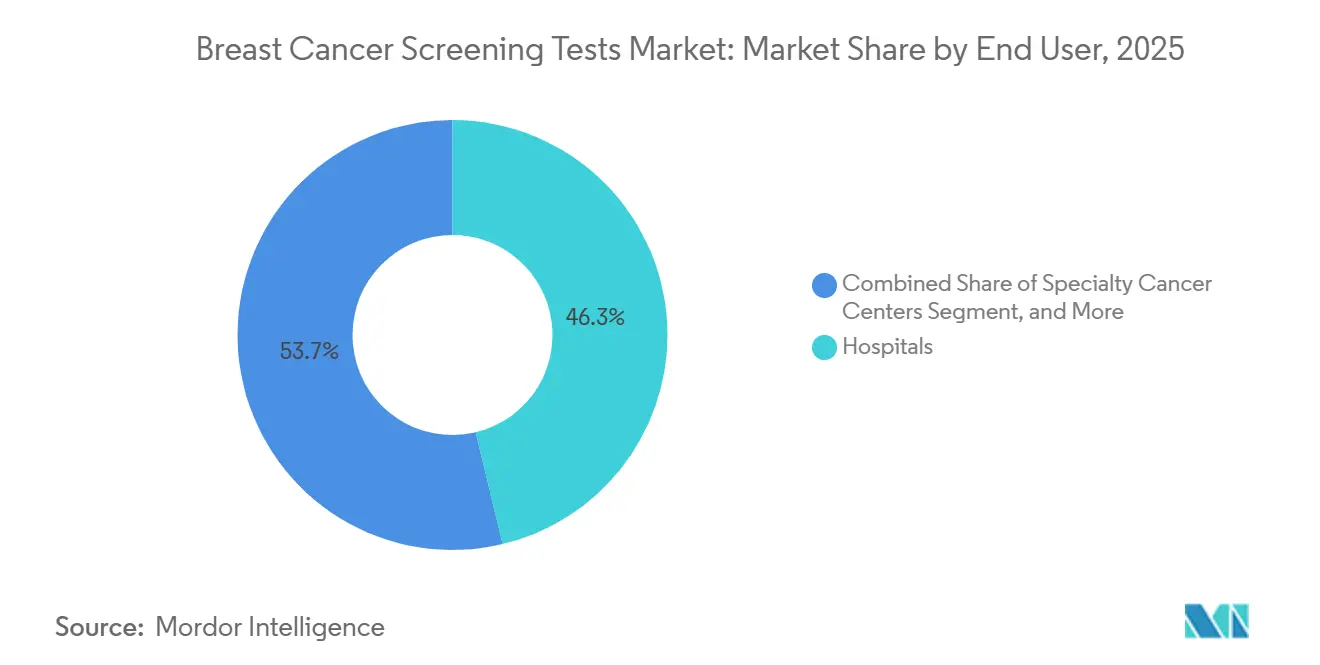

- By end user, hospitals accounted for 46.27% of the breast cancer screening market in 2025, and specialty cancer centers are advancing at a 11.63% CAGR through 2031.

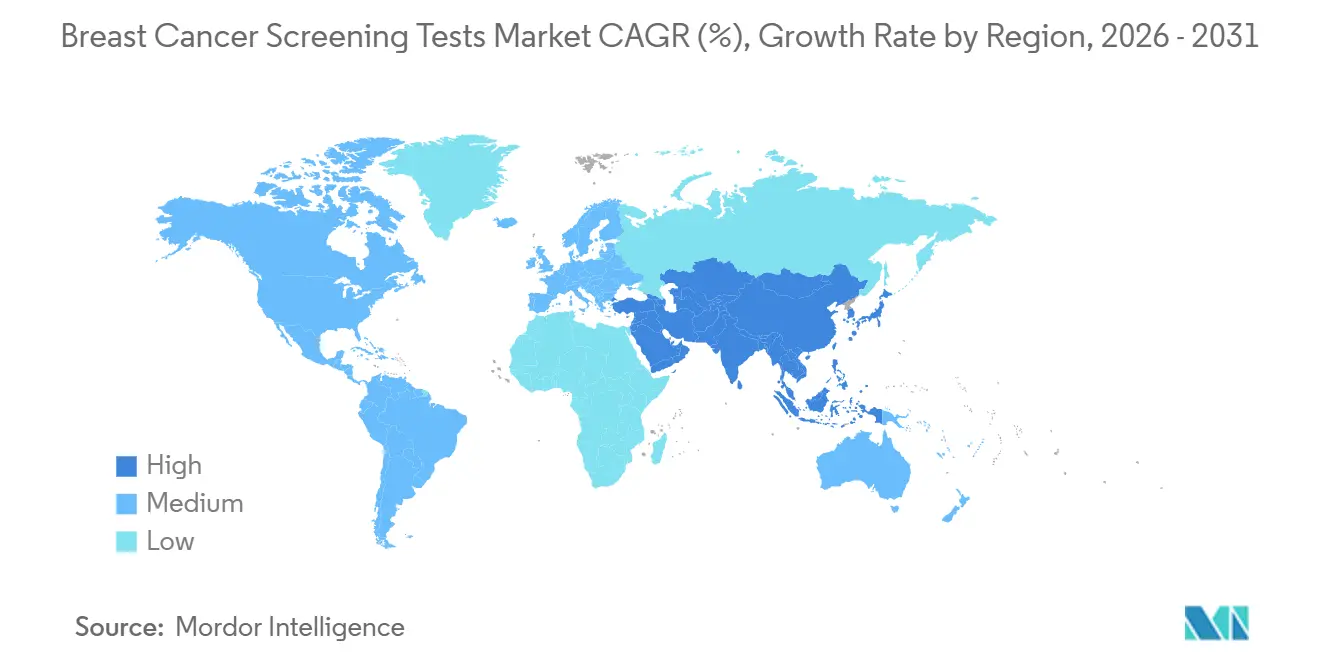

- By geography, North America accounted for 41.08% of revenue in 2025, and Asia-Pacific is pacing at a 10.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breast Cancer Screening Tests Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Breast Cancer | +1.8% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Favorable Government Screening Recommendations | +1.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Technological Advances in 3-D Mammography | +1.2% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Intensifying Public-Private Awareness Campaigns | +0.9% | Global, focus on India, Brazil, South Africa | Short term (≤ 2 years) |

| AI Triage Tools Lowering Image-Reading Cost | +1.4% | North America & Europe first, then Asia-Pacific | Medium term (2-4 years) |

| Employer-Funded Mobile Screening | +0.7% | India, Indonesia, Latin America, Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Prevalence of Breast Cancer

Global incidence climbed to 2.3 million cases in 2024 and is projected to reach 2.9 million by 2030, a trajectory driven by aging demographics, urban lifestyle shifts, and broader diagnostic reach.[1]World Health Organization, “Breast Cancer Screening Guidelines and Programs,” who.int The United States logged 310,000 new diagnoses in 2025, while China reported 420,000, underscoring the dual pressure of scale and urbanization. Disease onset before 50 now accounts for 12% of Western cases, prompting guideline bodies to lower the screening start age from 50 to 40 years. This policy change alone expands the breast cancer screening tests market by an estimated 25 million women. Mortality is falling by 1.3% annually in high-income regions thanks to earlier detection, yet stagnates in low-resource countries, where coverage remains below 20%, highlighting the opportunity for mobile and point-of-care modalities.

Favorable Government Screening Recommendations

The 2024 U.S. shift to age-40 biennial mammography lowers mortality 19% in women 40-49, pushing volume through the reimbursement pipeline. The U.K. added women 47-73, funding GBP 120 million for mobile vans and training. Japan mandated annual ultrasound for dense breast tissue, affecting 40% of its cohort, and swelling equipment demand. China is subsidizing 70% of rural exam costs for 50 million women, pairing subsidies with AI triage in county hospitals. Compliance frameworks such as the FDA’s MQSA align volume with strict quality metrics.

Technological Advances In 3-D Mammography

Digital Breast Tomosynthesis adoption reached 68% of U.S. facilities in 2025 after reimbursement parity eliminated the price gap with 2-D units.[2]Radiological Society of North America, “Digital Breast Tomosynthesis: Clinical Outcomes and Adoption Trends,” rsna.org Systems that synthesize 2-D views from raw DBT data cut exam time by a third and raise detection by 1-2 cancers per 1,000 screens. Photon-counting detectors reduce radiation 30% while preserving resolution, easing patient concerns. The upshot: sites report 10-12% higher satisfaction scores and 8% fewer malpractice claims, reinforcing the need for refresh cycles.

Intensifying Public-Private Awareness Campaigns

Retail-clinic coalitions delivered 120,000 free mammograms to underserved U.S. women in 2024, finding 480 early cancers.[3]American Cancer Society, “Screen to Save Initiative,” cancer.org In 2025, India’s 200 mobile vans screened 300,000 women, 70% of whom were at stages I-II. Brazil’s Pink October lifted national uptake by 18% with BRL 150 million in corporate sponsorships. Programs that merge education with on-site access convert intent into exams at three times the rate of message-only drives, guiding future outreach design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiation-Exposure Concerns Among Patients | −0.6% | Global, most acute in North America & Europe | Short term (≤ 2 years) |

| High Cost of Advanced Imaging Equipment | −1.1% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| False Positives Leading to Overdiagnosis | −0.8% | North America & Europe | Medium term (2-4 years) |

| Regulatory Uncertainty for Liquid-Biopsy Tests | −0.5% | U.S. and EU | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Radiation-Exposure Concerns Among Patients

Modern mammography delivers 0.4 milligrays per view, yet 22-28% of surveyed women still cite radiation fear, often conflating CT doses with screening levels. Density notifications, while clinically useful, inadvertently raise anxiety and push some women toward costlier MRI. Vendor countermeasures include photon-counting detectors and contrast-enhanced techniques that can reduce dose by up to 40%.

High Cost of Advanced Imaging Equipment

Premium DBT plus AI can cost USD 500,000 upfront and another USD 60,000 per year in service, far beyond the means of systems operating on USD 200 per capita budgets. Africa has fewer than 200 functional mammography units across 48 countries. Pay-per-scan leasing at USD 15 an exam and certified refurbished units at 50-60% discounts are easing barriers, but cannot close the gap alone.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Screening Modality: Blood-Based Biomarkers Gain Momentum

Imaging-based Tests retained 66.02% of the revenue in 2025, yet the breast cancer screening tests market for Blood-based Biomarker Tests is expanding the fastest at a 9.06% CAGR through 2031. Mammography generated 1.2 billion exams, with Digital Breast Tomosynthesis overtaking 2-D in the United States and nearing parity in Europe. Handheld ultrasound devices added 15 million Asia-Pacific screens, while fast MRI protocols halved scan time and reduced costs to USD 600, pushing the modality beyond high-risk cohorts. Guardant’s Shield and Exact Sciences’ CancerSEEK multi-cancer assays, priced around USD 995, now compete with MRI for high-risk women, securing payer pilots that could widen use once mortality endpoints mature. Multi-analyte panels integrating proteins, microRNAs, and ctDNA are lining up behind early adopters, though regulatory clarity will ultimately dictate uptake.

By End User: Specialty Centers Capture High-Acuity Volume

Hospitals contributed 46.27% of 2025 sales, but Specialty Cancer Centers are pacing 11.63% CAGR, outstripping hospital growth. The breast cancer screening tests market for networked diagnostics centers is growing as Radiology Partners and others consolidate 45 U.S. clinics, leveraging common AI platforms to increase throughput. Retail chains performed 8 million mammograms at cash prices of USD 99-149, reaching uninsured patients. Specialty centers differentiate by integrating imaging, liquid biopsy, and polygenic risk into a single visit; Memorial Sloan Kettering’s program cut overdiagnosis by 22% and missed cancers 8% in a 50,000-person cohort. Bundled payments of USD 8,000 per screening-to-treatment episode, versus USD 12,000 under fee-for-service, cement their value-based edge.

Geography Analysis

North America generated 41.08% revenue in 2025, backed by Medicare’s USD 150-200 reimbursement per exam and a 2024 guideline shift that added 20 million eligible women. Three large states require dense-breast ultrasound coverage without cost-sharing, pushing supplemental volume. Canada invested CAD 180 million (USD 133 million) in DBT upgrades, boosting penetration from 22% to 38% in one year. Mexico’s mobile-unit rollout achieved 50% higher early-detection rates than fixed-site screening. Persistent radiologist shortages of 2,000 by 2028 are keeping AI triage and cross-border teleradiology in demand.

Asia-Pacific is the fastest-growing region, with a 10.27% CAGR to 2031. China’s Healthy China 2030 allocates CNY 50 billion (USD 7 billion) for screening expansion to 70% urban coverage. India’s Ayushman Bharat added screening at 5,000 health centers, targeting 30 million women by 202. Japan, already at 50% participation, deploys combined mammography-ultrasound for dense tissue, while South Korea’s program pilots AI in 200 municipal clinics. Radiologist density varies sharply from 0.8 per 100,000 in India to 8 in Japan, necessitating task shifting and cloud AI solutions.

Centralized invitation systems and free-of-charge protocols keep participation near 75%. Germany now reimburses MRI for women with ≥20% lifetime risk, lifting MRI screens by 18%. The U.K. cleared a COVID backlog after AI cut read times by a quarter. France’s dense-breast notification pilot raised diagnostic yield by 12% but also false positives by 8%, prompting protocol review. Spain began integrating liquid biopsy for BRCA carriers, detecting 15% more interval cancers. Elsewhere, donor-funded mobile programs seed infrastructure in Nigeria, Kenya, South Africa, Brazil, and Argentina, but still face out-of-pocket hurdles for 40-50% of target populations.

Competitive Landscape

Top-five imaging vendors Hologic, GE HealthCare, Siemens Healthineers, Fujifilm, and Philips capture a significant share of equipment revenue, maintaining their positions through service contracts, trade-ins, and rapid software refreshes. The breast cancer screening tests market remains fragmented in liquid biopsy and AI, with more than 20 contenders vying for analytical accuracy and payer coverage. Delphinus Medical Technologies focuses on dense-breast ultrasound niches, while iCAD and Kheiron lead stand-alone AI for interpretation. Lunit and Volpara use software-as-a-service to circumvent capex barriers, each with more than 2,500 installations. Patent filings for AI triage grew 40% in 2024-2025, signaling intensifying R&D activity. Consolidation is quickening: GE HealthCare bought MIM Software to pair PET analytics with mammography, and Siemens Healthineers tapped Varian to link screening data to therapy planning. Regulatory complexity favors incumbents with dedicated quality teams, yet the rapid uptake of cloud AI shows pathways remain open for agile newcomers.

Breast Cancer Screening Tests Industry Leaders

Siemens Healthineers

Hologic Inc.

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

FUJIFILM Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Hologic’s AI mammography flagged one-third of cancers initially missed in a study of 7,500 exams.

- December 2025: Astrin Biosciences launched Certitude, an AI + proteomics blood test for early detection, effective even in dense breast tissue.

- November 2025: IAEA donated an advanced mammography unit to expand screening access in the Amazon.

- October 2025: Prerna introduced CANTEL, a microRNA-based blood test for breast cancer screening.

Global Breast Cancer Screening Tests Market Report Scope

As per the scope, breast cancer screening is carried out to detect cancer early and ensure timely treatment for the patients. Different types of breast cancer depend on the type of cancer cell that becomes cancerous. Breast cancer can affect different parts of the breast, such as the ducts and the lobes. The Breast Cancer, Screening Test Market, is Segmented by Test (Genomic Tests and Imaging Tests) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

By Screening Modality

| Imaging-based Tests | Mammography |

| Digital Breast Tomosynthesis | |

| Ultrasound | |

| Magnetic Resonance Imaging | |

| PET & Molecular Imaging | |

| Blood-based Biomarker Tests | Liquid Biopsy (ctDNA) |

| Multi-analyte Protein Panels | |

| microRNA Panels | |

| Genetic & Genomic Tests | BRCA 1/2 Mutation Tests |

| Multi-gene Panels | |

| Polygenic Risk Scores | |

| Wearable & AI-enabled Screening | Smart-bra Sensors |

| Hand-held AI Ultrasound |

By End User

| Hospitals |

| Specialty Cancer Centers |

| Diagnostic Imaging Centers |

| Ambulatory Care Centers |

| Other End Users |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Screening Modality | Imaging-based Tests | Mammography |

| Digital Breast Tomosynthesis | ||

| Ultrasound | ||

| Magnetic Resonance Imaging | ||

| PET & Molecular Imaging | ||

| Blood-based Biomarker Tests | Liquid Biopsy (ctDNA) | |

| Multi-analyte Protein Panels | ||

| microRNA Panels | ||

| Genetic & Genomic Tests | BRCA 1/2 Mutation Tests | |

| Multi-gene Panels | ||

| Polygenic Risk Scores | ||

| Wearable & AI-enabled Screening | Smart-bra Sensors | |

| Hand-held AI Ultrasound | ||

| By End User | Hospitals | |

| Specialty Cancer Centers | ||

| Diagnostic Imaging Centers | ||

| Ambulatory Care Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the breast cancer screening tests market expected to grow to 2031?

It is forecast to expand at 8.42% CAGR between 2026 and 2031, moving from USD 3.46 billion in 2026 to USD 5.18 billion by 2031.

Which screening modality is expanding the quickest?

Blood-based biomarker tests are pacing at a 9.06% CAGR through 2031 as liquid-biopsy platforms gain validation and reimbursement.

What share of 2025 revenue came from imaging-based tests?

Imaging-based tests commanded 66.02% of 2025 revenue, underscoring mammography’s ongoing dominance.

Which region delivers the highest growth rate?

Asia-Pacific leads with a projected 10.27% CAGR, propelled by large-scale subsidy programs in China and India.

Why are specialty cancer centers outpacing hospitals?

Bundled payments and integrated multi-omics workflows let specialty centers deliver coordinated care at lower episode costs, fueling an 11.63% CAGR to 2031.

Page last updated on: