Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

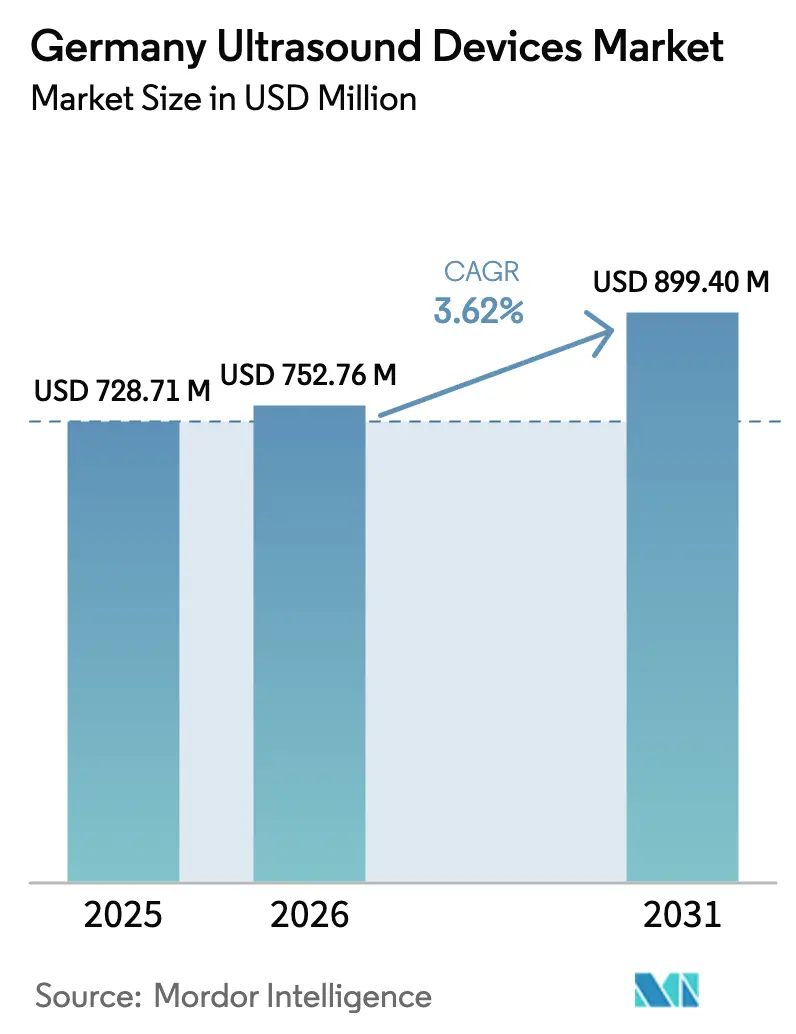

| Base Year Market Size (2025) | USD 728.71 Million |

| Market Size (2026) | USD 752.76 Million |

| Market Size (2031) | USD 899.40 Million |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Germany Ultrasound Devices Market Analysis by ���ϲ�����

The Germany Ultrasound Devices Market size is expected to increase from USD 728.71 million in 2025 to USD 752.76 million in 2026 and reach USD 899.40 million by 2031, growing at a CAGR of 3.62% over 2026-2031.

Demand remains resilient because an aging population drives imaging volumes, while 2024 hospital-reform legislation steers a portion of routine diagnostics away from tertiary centers toward outpatient clinics equipped with compact platforms. Portable and handheld systems costing under EUR 5,000 support this shift, enabling primary-care networks to scan patients on site and avoid capital-budget bottlenecks that delay cart upgrades in public hospitals. Meanwhile, non-invasive applications such as high-intensity focused ultrasound (HIFU) and elastography court private clinics seeking premium procedures, cushioning revenue against maturity in core radiology. Compliance-minded AI inference running directly on probes or carts further differentiates next-generation products in Germany’s stringent data-protection environment.

Key Report Takeaways

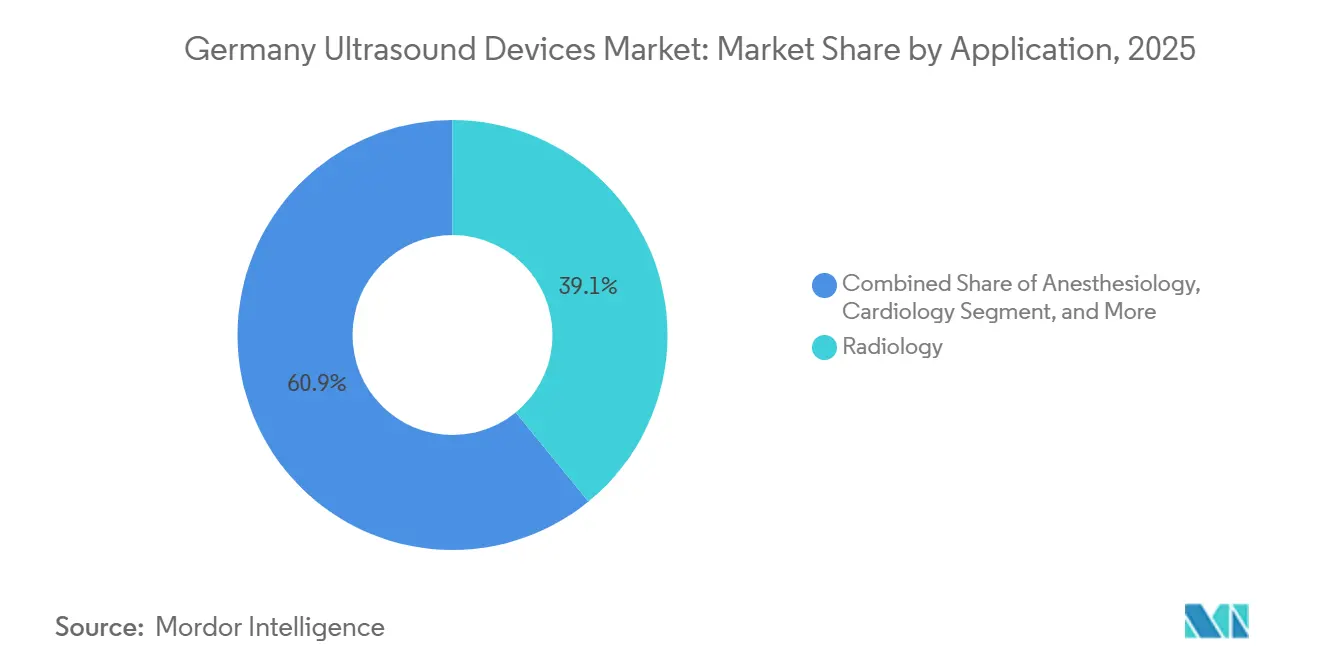

- By application, radiology led with 39.09 % revenue share of the Germany ultrasound devices market size in 2025, while critical care is projected to record a 5.62% CAGR through 2031.

- By technology, 3D & 4D platforms commanded 45.29 % of Germany ultrasound devices market share in 2025, HIFU is forecast to post a 5.13% CAGR over the same period.

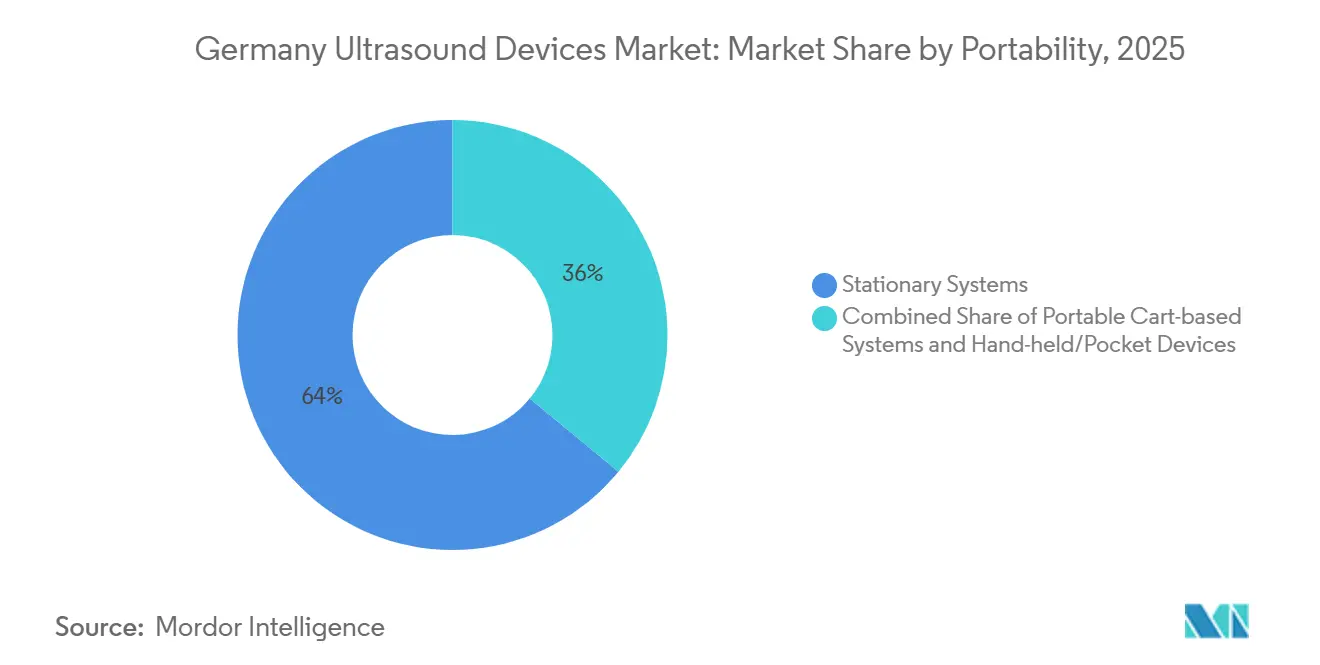

- By portability, stationary consoles held 64.04% of the Germany ultrasound devices market size in 2025, yet handheld devices are set to expand at 6.92% CAGR to 2031.

- By end user, home-healthcare captured 56.01% of spending in 2025, yet is forecast to grow at 6.43 % through 2031 as telehealth monitoring scales.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic Diseases | +0.8 % | National, urban centers | Long term (≥4 yrs) |

| Technological Advancements in Portable Units | +0.9 % | National, rural uptake | Medium term (2-4 yrs) |

| Growing Point-of-Care Adoption | +0.7 % | Emergency, primary care | Medium term (2-4 yrs) |

| Hospital-Reform Outpatient Incentives | +0.6 % | Berlin, NRW, Bavaria | Short term (≤2 yrs) |

| GDPR-Compliant On-Device AI | +0.5 % | University hospitals | Medium term (2-4 yrs) |

| Expanded POCUS Reimbursement | +0.4 % | Statutory insurance | Short term (≤2 yrs) |

| Source: ���ϲ����� | |||

Rising Prevalence of Chronic Diseases

Germany counted 18.7 million residents aged 65+ in 2025, representing 22.4% of the population, and cardiovascular disease prevalence is projected to increase by 12% by 2030.[1]Chronic Disease Report 2025, Robert Koch Institute, rki.de Echocardiography volumes rose 8 % in 2025, while musculoskeletal referrals jumped 15 % as rheumatologists embraced ultrasound-guided biologic injections. Portable scanners allow home-health nurses to check bladder volume and heart function, reducing nursing-home catheterizations by 18% in Bavaria. Reliable reimbursement for chronic-disease imaging insulates providers from budget freezes, keeping the Germany ultrasound devices market on a steady growth track.

Technological Advancements in Portable & Handheld Ultrasound

Handheld systems under 500 g captured 12 % of German unit shipments in 2025, up from 7 % two years earlier, as Butterfly’s iQ3 and Clarius HD3 bundled 5G, wireless charging, and AI auto-measure. Siemens Healthineers’ tablet-sized Sequoia Go streams encrypted DICOM over cellular networks, aiding pre-arrival stroke triage in rural districts.[2]Investor Relations, Siemens Healthineers, siemens-healthineers.com With 4-hour battery life, Philips Lumify overcomes previous endurance limits and satisfies emergency physicians’ shift needs. Performance parity with mid-tier carts closes the quality gap and lowers capital expense per imaging room by up to 40 %, bolstering the Germany ultrasound devices market.

Increasing Adoption in Point-Of-Care Settings

DEGUM reported that 38% of general practitioners owned an ultrasound unit in 2025, up from 22% in 2023.[3]Workforce Report 2025, DEGUM, degum.de Lung ultrasound triage at Charité Berlin reduced chest X-ray orders by 25% and door-to-diagnosis time to 28 minutes. Nerve-block guidance surged 40 % among anesthesiologists, and bedside hemodynamic assessments slashed pneumothorax incidence by 60 % in a multicenter critical-care trial. These gains reallocate scan demand from radiology to frontline clinicians, creating white space for vendors focused on user-friendly probes.

High Cost of Advanced Ultrasound Systems

Premium carts cost between EUR 80,000 and 150,000, straining hospitals whose equipment budgets fell by 6% in real terms during 2023-2025. Saxony tends to favor sub-EUR 50,000 units, allowing Mindray and Samsung to capture an 18% share with discounted 3D platforms. Leasing eases cash flow 35 % of Siemens placements in 2025 were five-year operating leases—but the upfront sticker shock still elongates replacement cycles, tempering Germany ultrasound devices market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Systems | -0.5 % | Municipal hospitals | Medium term (2-4 yrs) |

| Saturated Installed Base in Tertiary Hospitals | -0.4 % | University centers | Long term (≥4 yrs) |

| Stringent EU-MDR Post-Market Surveillance | -0.3 % | EU-wide | Medium term (2-4 yrs) |

| Shortfall of DEGUM-Certified Sonographers in Rural Areas | -0.3 % | Mecklenburg, Brandenburg | Long term (≥4 yrs) |

| Source: ���ϲ����� | |||

High Cost of Advanced Ultrasound Systems

Premium carts cost between EUR 80,000 and 150,000, straining hospitals whose equipment budgets fell by 6% in real terms during 2023-2025. Saxony tends to favor sub-EUR 50,000 units, allowing Mindray and Samsung to capture an 18% share with discounted 3D platforms. Leasing eases cash flow 35 % of Siemens placements in 2025 were five-year operating leases—but the upfront sticker shock still elongates replacement cycles, tempering Germany ultrasound devices market growth.

Saturated Installed Base in Tertiary Hospitals

German hospitals operated 12,000 scanners in 2025, one of Europe’s densest footprints. Two-thirds of 2025 purchases merely replaced eight-year-old units, while MRI and CT upgrades siphoned budgets at university centers like Hamburg UKE, deferring ultrasound refresh. Vendors, therefore, pivot to outpatient clinics and home care for incremental volumes.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Critical Care Accelerates Adoption

Critical care imaging is projected to climb at a 5.62 % CAGR, the swiftest trajectory within the Germany ultrasound devices market, because intensive-care teams require real-time hemodynamic data during resuscitation. Radiology retained 39.09% of 2025 revenue, but portable scanners enable emergency physicians to bypass queues, trimming 32% of radiology referrals for suspected pneumonia at Frankfurt University Hospital. Cardiology echo volumes increased by 9% in 2025 due to wider use of strain imaging in oncology follow-up. Musculoskeletal clinics increasingly perform in-office joint assessments, elevating procedure counts and supporting ancillary probe sales. Urologists exploit sub-EUR 3,000 handheld bladder scanners on geriatric wards, aiding infection-prevention goals.

By Technology: HIFU Broadens Therapeutic Appeal

High-intensity focused ultrasound (HIFU) is expanding at 5.13 % because non-invasive ablation of localized prostate cancer and uterine fibroids commands EUR 3,500 reimbursement per case. Although 3D & 4D retained 45.29% of revenue in 2025, its growth moderated as tertiary penetration peaked. Siemens’ AI 3D rendering now segments cardiac chambers in 10s, trimming cardiologist read times. Canon’s micro-vascular imaging debuted in 2025 and maps capillary perfusion without contrast.

By Portability: Handheld Units Democratize Access

Stationary carts still accounted for 64.04% of portability revenue in 2025, yet their replacement cycle stretched beyond 9 years. Portable carts are prized by emergency and surgical suites for moving devices between beds. Handheld scanners account for only 6.92% of 2025 revenue but grow the fastest, with Butterfly iQ3’s single-probe design eliminating the need to purchase multiple transducers. Paramedic services in Berlin fielded handheld ultrasound in 2025, shaving 18 minutes off trauma triage timelines.

By End User: Tele-Enabled Home Healthcare Surges

Hospitals accounted for 56.01% of 2025 spending, but budget constraints stifle incremental unit growth. Diagnostic centers grew faster, as outpatient reforms paid standalone scan fees. Ambulatory surgical centers are adopting ultrasound for nerve blocks and post-op checks. Home healthcare is growing rapidly, with a 6.43% CAGR, and is expected to continue growing. North-Rhine Westphalia’s pilot cut 30-day heart-failure readmissions 28% via nurse-performed remote scans. Philips’ HealthSuite uploads images to cardiologist dashboards, underpinning insurer reimbursement for 12 annual home scans.

Geography Analysis

Urban tertiary hubs such as Berlin, Munich, and Hamburg demand premium 3D carts, whereas rural hospitals in eastern Länder favor mid-tier portable units to balance cost and utility. Physician density of 4.5 per 1,000 in Baden-Württemberg sustains above-average ultrasound utilization, while Mecklenburg’s 3.0 per 1,000 constrains volumes. Outpatient reimbursement reforms introduced 14 new ultrasound codes that pay EUR 45-65, tilting volumes toward clinics operating extended hours.

Private insurers covering 11% of residents launched supplementary home-scan benefits in October 2025, catalyzing the adoption of handheld devices among nurse-led services. Siemens commands a 25-30% share nationally through legacy contracts, while GE and Philips each hold 15-20%. Mindray and Samsung jointly own 12 % by offering discounted 3D platforms to budget-pressed municipal hospitals. Workforce shortages outside cities hamper the uptake of advanced protocols, but tele-guidance pilots and AI auto-capture buttress quality where DEGUM experts are scarce.

Competitive Landscape

The major players, such as Siemens Healthineers, GE HealthCare, Philips, Canon Medical, and Samsung Medison, are reflecting bundled service contracts and multiyear leases that lock hospitals into proprietary ecosystems. Siemens leverages its home-market advantage and dense service fleet, while GE and Philips court radiology departments with workflow automation and cloud analytics. Mindray, Samsung, and CHISON are undercutting on price, securing municipal hospital tenders as budgets tighten.

Handheld disruptors Butterfly, Clarius, and Exo compete on smartphone connectivity and AI that trims training to hours, unlocking general-practitioner and paramedic niches. Siemens filed 14 GDPR-compliant AI patents in 2025; Philips filed 9 for federated learning. GE’s Caption AI earned CE clearance under the EU AI Act, highlighting incumbents’ pivot toward integrated software value. Mid-size vendors such as Esaote grapple with EU-MDR compliance, which consumes 12-15% of sales, accelerating consolidation or portfolio pruning.

Germany Ultrasound Devices Industry Leaders

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

GE Healthcare

Siemens Healthineers AG

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FUJIFILM Healthcare Europe has officially announced the Europe-wide launch of the EG-740UT, an advanced interventional ultrasonic endoscope engineered for therapeutic applications. This milestone reinforces FUJIFILM’s commitment to delivering cutting-edge endoscopic solutions that elevate clinical precision and patient care.

- April 2024: Butterfly Network Inc., a leading digital health innovator, has announced the commercial launch of its third-generation handheld point-of-care ultrasound (POCUS) system, the Butterfly iQ3, across 17 European countries, effective September 4, 2024. The Butterfly iQ3 is now available in Germany, marking a significant expansion of Butterfly’s footprint in Europe.

Germany Ultrasound Devices Market Report Scope

As per the scope of the report, ultrasonography is an imaging method that creates images of various body structures using high-frequency sound waves. They are used to evaluate a variety of disorders relating to the liver, kidneys, and other abdominal conditions, including usage in pregnancy. As a result, these devices have a variety of uses in the medical area, including diagnostic imaging and therapeutic modality. The Germany ultrasound device market is segmented by application, technology, and type. Based on application the market is segmented as anesthesiology, cardiology, gynecology/obstetrics, musculoskeletal, radiology, critical care, and other applications). Based on technology the market is segmented into 2D ultrasound imaging, 3D and 4D ultrasound imaging, doppler imaging, and high-intensity focused ultrasound. Based on type the market is segmented as stationary ultrasound and portable ultrasound. The report offers the value (in USD) for the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Gynecology / Obstetrics |

| Musculoskeletal |

| Radiology |

| Critical Care |

| Urology |

| Vascular |

| Other Applications |

By Technology

| 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Cart-based Systems |

| Hand-held / Pocket Devices |

By End User

| Hospitals |

| Diagnostic Centers |

| Ambulatory Surgical Centers |

| Home Healthcare Settings |

| Other End Users |

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology / Obstetrics | |

| Musculoskeletal | |

| Radiology | |

| Critical Care | |

| Urology | |

| Vascular | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Cart-based Systems | |

| Hand-held / Pocket Devices | |

| By End User | Hospitals |

| Diagnostic Centers | |

| Ambulatory Surgical Centers | |

| Home Healthcare Settings | |

| Other End Users |

Key Questions Answered in the Report

How large is the Germany ultrasound devices market in 2026?

It stands at USD 752.76 million in 2026, on course to reach USD 899.40 million by 2031.

Which clinical area is expanding fastest for ultrasound use in Germany?

Critical-care imaging grows at a 5.62 % CAGR through 2031 as ICUs and emergency rooms embed lung and cardiac protocols.

What drives handheld ultrasound adoption?

Sub-EUR 5,000 pricing, smartphone integration, and recent reimbursement codes that cut payback periods to about 18 months.

How are German regulations shaping AI in ultrasound?

GDPR strictness favors on-device or federated AI that avoids cloud transfers, accelerating local inference development.

Why is home-healthcare a growth hotspot?

Tele-enabled handheld probes let nurses monitor chronic-disease patients at home, lowering readmissions and now enjoy insurance reimbursement.

Page last updated on: