Geopolymer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

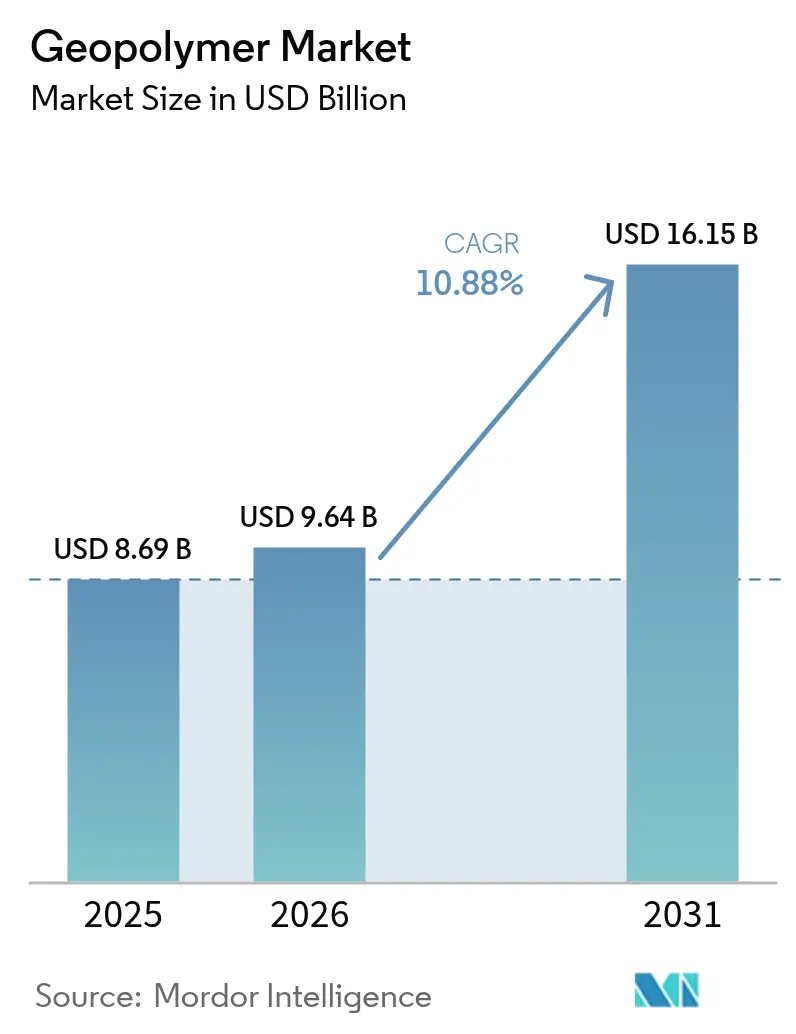

| Market Size (2026) | USD 9.64 Billion |

| Market Size (2031) | USD 16.15 Billion |

| Growth Rate (2026 - 2031) | 10.88% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Geopolymer Market Analysis by ���ϲ�����

The Geopolymer Market size is expected to grow from USD 8.69 billion in 2025 to USD 9.64 billion in 2026 and is forecast to reach USD 16.15 billion by 2031 at 10.88% CAGR over 2026-2031. Declining cost competitiveness of Portland cement under carbon-pricing programs, wider access to industrial by-products such as fly ash and slag, and fast-maturing one-part formulations are steering procurement managers toward aluminosilicate binders. The geopolymer market is also benefiting from green-building mandates in the United States, the European Union, and the Gulf states, each of which embeds embodied-carbon thresholds into public tenders. Ready-mix producers are capitalizing on these policies to widen product portfolios, while deep-sea energy operators now specify geopolymer grouts that tolerate sulfate attack for twice as long as legacy cement systems. Competitive intensity remains moderate because global cement majors still control clinker distribution and therefore the pace at which design codes migrate, yet independent formulators are carving out high-margin niches in waste immobilization and fireproofing.

Key Report Takeaways

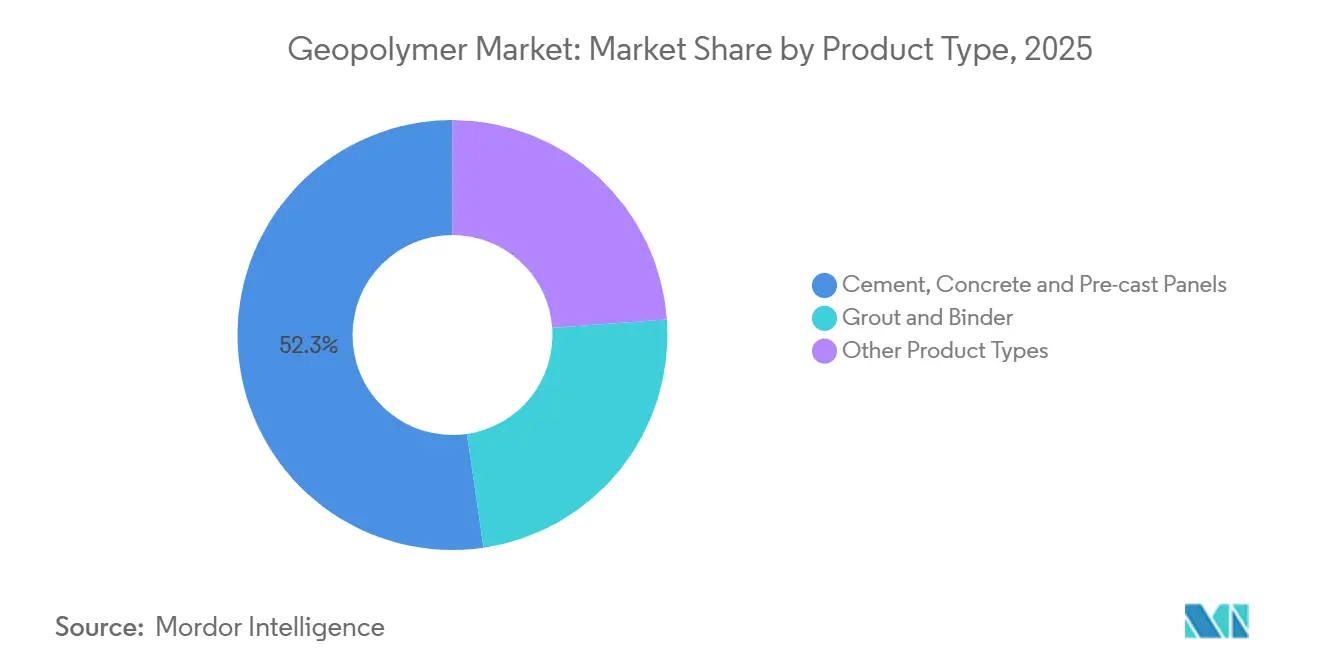

- By product type, cement, concrete, and pre-cast panels held 52.31% of the geopolymer market share in 2025, while grout and binder applications are forecast to expand at an 11.12% CAGR through 2031.

- By application, building construction commanded 34.45% of the geopolymer market size in 2025, whereas nuclear and other toxic-waste immobilization applications are advancing at a 11.25% CAGR to 2031.

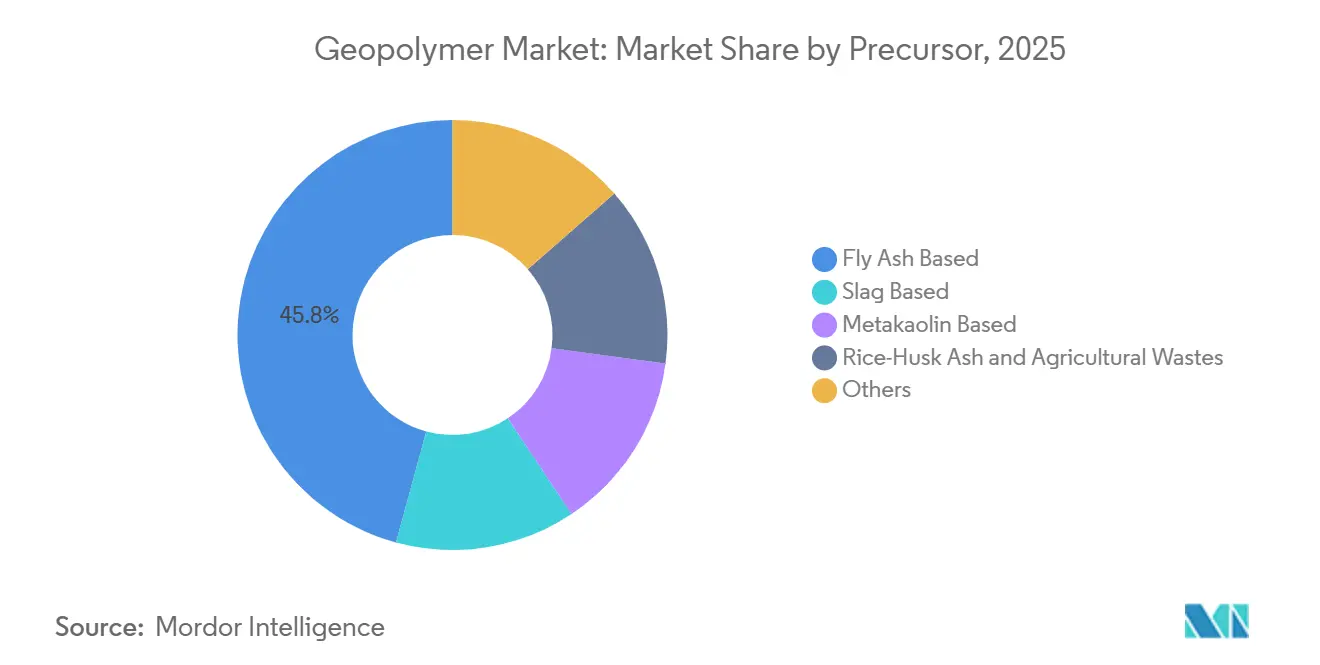

- By precursor, fly-ash-based systems contributed 45.78% of the geopolymer market share in 2025, and metakaolin-based formulations are projected to grow at an 11.67% CAGR during the period.

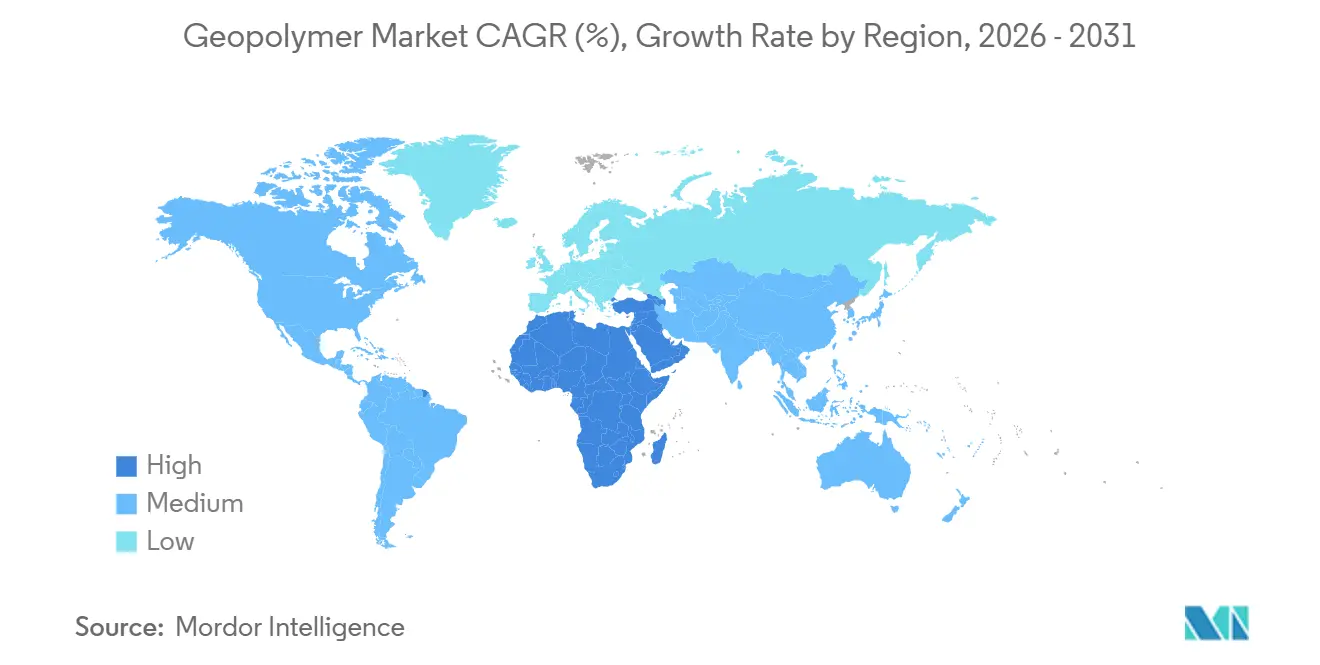

- By geography, Asia-Pacific accounted for 44.31% of the market in 2025, while the Middle East and Africa region is set to record the highest 10.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Geopolymer Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent CO₂-emissions regulations on cement industry | +3.2% | Global, with highest intensity in EU, UK, China, California | Medium term (2-4 years) |

| Growing availability of fly-ash and slag feedstocks | +2.4% | APAC core (China, India, ASEAN), spill-over to North America | Short term (≤ 2 years) |

| Demand for green-building certification materials | +2.1% | North America, EU, Middle East (UAE, Saudi Arabia) | Medium term (2-4 years) |

| Rapid uptake of one-part geopolymer formulations | +1.8% | Global, early gains in Australia, Scandinavia, Japan | Short term (≤ 2 years) |

| Deep-sea energy and mining infrastructure adoption | +1.4% | North Sea, Gulf of Mexico, South China Sea, offshore West Africa | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Stringent CO₂-Emissions Regulations on Cement Industry

Starting in 2026, the Carbon Border Adjustment Mechanism will impose an additional charge on imported clinker. This move is set to widen the cost disparity between Portland and geopolymer binders[1]European Commission, “EU Emissions Trading System,” europa.eu. In China, certain provinces have established a ceiling on CO₂ emissions for every tonne of clinker produced. This regulation has led to winter curtailments, subsequently boosting the attractiveness of supplementary binders. Meanwhile, California's Buy Clean Act mandates a limit on CO₂-equivalent emissions for each unit of compressive strength. Notably, fly-ash geopolymer mixes can achieve this standard without the need for carbon capture. Furthermore, ISO 14067 certification has gained traction among Tier-1 contractors. This endorsement has effectively integrated geopolymer specifications into infrastructure portfolios worth billions. Looking ahead, the International Energy Agency projects that by 2030, carbon pricing will encompass a significant portion of the global cement output, further strengthening the momentum of these regulatory changes.

Growing Availability of Fly-Ash and Slag Feedstocks

In 2025, India produced fly ash, with policy mandates boosting utilization, leading to a year-on-year drop in precursor prices. China's steel sector churned out slag in 2025, resulting in a surplus. This surplus, earmarked for geopolymer applications, is priced lower than imported metakaolin. Vietnam and Indonesia inaugurated beneficiation hubs, achieving a sub-5% loss-on-ignition feedstock. This advancement has reduced compressive-strength variability. In North America, the retirement of coal plants cut the annual fly-ash supply. This shortfall has nudged formulators towards ground glass pozzolan, despite its higher cost. Meanwhile, electric-arc steel mills around the Great Lakes ensure a steady slag supply, maintaining the region's cost advantage.

Demand for Green-Building Certification Materials

LEED v5 awards credits for mixes achieving a significant reduction in embodied carbon. This incentive is projected to boost geopolymer specifications in North American commercial projects. Abu Dhabi's Estidama system mandates ISO 21930 environmental product declarations. Notably, certified geopolymer suppliers are eyeing the lucrative backlog for Expo 2030. Meanwhile, Saudi Arabia's Green Building Code aims for a reduction in embodied carbon for public constructions, spurring demand for geopolymer panels in healthcare facilities. Additionally, both BREEAM International and the European Commission's Level(s) framework incentivize concrete that incorporates industrial waste, aligning seamlessly with geopolymer technology.

Rapid Uptake of One-Part Geopolymer Formulations

One-part systems, which come equipped with dry alkali activators, only need water added on-site and can reduce labor costs. In 2025, CEMEX delivered such concrete to industrial parks in Monterrey. By the end of 2025, Heidelberg Materials will boost a production line in Hanover to churn out such materials monthly. Research published in peer-reviewed journals indicates that sodium-aluminate-activated one-part mixtures offer durability on par with two-part systems in environments with sulfate and chloride exposure. Meanwhile, Japanese patents have taken this innovation further, introducing calcium sulfoaluminate blends that achieve strength in just six hours, even at low temperatures.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of uniform design codes and standards | -1.6% | Global, acute in North America, Middle East, South America | Medium term (2-4 years) |

| Price volatility of alkali activators (NaOH / Na₂SiO₃) | -1.2% | Global, with highest exposure in regions dependent on imported sodium silicate (South America, Africa) | Short term (≤ 2 years) |

| Feedstock chemical variability compromising QC | -0.9% | APAC (China, India, ASEAN), Eastern Europe | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Lack of Uniform Design Codes and Standards

Geopolymer concrete lacks recognition in ASTM C94 and ACI 318, leading engineers to seek project-specific approvals and extending permit cycles[2]American Concrete Institute, “Building Code Requirements,” concrete.org. Australia's AS 3600 performance clauses, updated in 2024, stand as the sole national standard, channeling research and development efforts predominantly in that market. With ISO 19596 not anticipated until 2028, specifiers often revert to Portland cement to mitigate liability risks. British Standards only acknowledge geopolymer mixes post durability trials, hindering adoption in the Middle East. Additionally, conflicting tunnel fire-resistance regulations between Germany and France inflate compliance costs for suppliers catering to both nations.

Price Volatility of Alkali Activators

In late 2024, gas shortages in Europe led to a surge in sodium silicate prices, subsequently raising geopolymer concrete costs. Throughout 2025, sodium hydroxide spot prices in Asia fluctuated, prompting producers to hedge a significant portion of their volumes. Suppliers in South America, dependent on imported activators, faced high landed costs. This situation rendered geopolymer mixes pricier than their local cement counterparts. Dominating the global landscape, three firms command a significant share of the capacity and transfer most energy costs directly to buyers. Meanwhile, projects in Africa grapple with cost fluctuations, a challenge exacerbated by currency depreciation and a complete reliance on imports.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pre-Cast Panels Anchor Volume Growth

In 2025, cement, concrete, and pre-cast panels dominated the geopolymer market, capturing a 52.31% share of the revenue. This surge was largely driven by ready-mix companies adopting one-part systems, streamlining on-site batching. By 2031, this segment is poised to represent a substantial portion of the geopolymer market, buoyed by public projects like low-carbon bridges, schools, and high-rise façades. The quality of these panels is further enhanced through factory-controlled curing. Meanwhile, grout and binder products are witnessing 11.12% growth, fueled by tunnel repairs and subsea cable work, which command premium pricing for their rapid strength gain.

Niche applications of the geopolymer market are emerging in coatings and adhesives, particularly for fireproofing and chemical-resistant linings. However, the higher formulation costs are tempering volume growth. Cold-weather performance, previously a challenge, is now being addressed. Norwegian field trials using calcium sulfoaluminate accelerators demonstrated the ability to achieve 15 MPa within eight hours at 5 °C. With an uptick in product certifications, especially in Europe and Australia, many precast producers are transitioning to ambient-cured mixtures, reaping energy bill savings.

By Application: Waste Immobilization Drives Specialty Demand

Building construction accounted for a 34.45% share of market revenue in 2025, spurred by municipal green-bond financing emphasizing low-carbon concrete. Nuclear and toxic-waste immobilization, although smaller in absolute volume, is forecast to grow fastest at 11.25% CAGR to 2031. Notably, contract awards at Sellafield focused on geopolymer encapsulation for intermediate-level waste. In a significant move, Japanese regulators greenlit this technology for soil stabilization at Fukushima, setting a precedent across regions.

In a bid to enhance road longevity, infrastructure agencies in Australia and India are piloting geopolymer pavements, adept at resisting sulfate attacks in expansive clay soils. Bridge decks, pier jackets, and marine pilings, with chloride diffusion coefficients under 2 × 10⁻¹² m²/s, not only meet the “very low” permeability standard but also enjoy extended maintenance intervals. In petrochemical plants, fireproofing solutions now boast a four-hour integrity at 1,100 °C, surpassing traditional intumescent coatings and tapping into a projected replacement market by 2031.

By Precursor/Raw-Material: Metakaolin Gains on Fly-Ash Scarcity

In 2025, fly-ash systems command a 45.78% share of precursor demand, but their dominance wanes annually as coal plants shutter in OECD markets. By 2031, metakaolin products are set to carve out a notable slice of the geopolymer market, growing at a 11.67% CAGR. Betolar's calcination facility in Lapland underscores the economic viability, especially with an abundance of regional clays. In South Korea, slag-based mixes thrive, bolstered by electric-arc furnaces ensuring consistent feedstock chemistry and government subsidies covering a portion of research and development expenses.

In India and Vietnam, rice-husk ash blends cater to rural-housing initiatives, capitalizing on a zero-cost agricultural waste stream that boasts high silica content post-controlled combustion. While red mud and waste glass offer circular-economy benefits, they necessitate additional steps to counteract alkalinity and alkali-silica reactivity, inflating processing costs. On volcanic islands devoid of fly-ash logistics, basalt powder is gaining traction, achieving strengths apt for non-structural elements. Quality control measures are intensifying: Chinese manufacturers are blending metakaolin into Class F fly ash, slashing batch rejects significantly.

Geography Analysis

In 2025, Asia-Pacific commanded a 44.31% share of the revenue, driven by China's solid-waste utilization quotas and India's ambitious Green Cement Mission. In a notable achievement, Jiangsu and Zhejiang rolled out affordable housing using fly-ash geopolymers, reaping cost savings by sidestepping clinker imports. Thanks to India's IS 18417:2024 standard, placements accelerated on national highways. Japan, prioritizing seismic safety, designated geopolymer grouts for upgrading bridge piers, while South Korea's Green New Deal backed pilot projects at ports and subways.

North America is capitalizing on an allocation for low-carbon concrete under the Infrastructure Investment and Jobs Act. Initial contracts are zeroing in on coastal levee enhancements and mass-timber hybrid towers, where every ounce of weight savings counts. In Europe, Germany invested in geopolymer pilot plants located in North Rhine-Westphalia. Meanwhile, the UK is ambitiously aiming for a reduction in embodied carbon across its public projects by 2030. France's RE2020 regulation has spurred a surge in demand, with Greater Paris housing witnessing installations in 2025.

The Middle-East and Africa are leading the charge with a 10.92% CAGR. NEOM's visionary linear city is mandating low-carbon concrete for all foundation pours, securing long-term contracts with local geopolymer suppliers. In a significant move, Saudi Aramco successfully tested geopolymer well cement in the high-temperature Jafurah shale play, achieving commendable isolation results. The UAE's Masdar City Phase II is integrating geopolymer mixes into its structural concrete. South African school initiatives and the façades of Egypt's New Administrative Capital underscore the continent's growing embrace of these materials, frequently linked to indigenous fly-ash or clay resources.

���ϲ����� provides coverage of the geopolymer market across other key regional markets, including Asia, North America, and Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to China incorporating local coverage and market participation, as required.

Competitive Landscape

The geopolymer market is fragmented. Machine-learning platforms shorten formulation cycles. Feedstock integration is another differentiator: vertically integrated players co-locate plants near consistent ash or slag streams, mitigating quality swings that previously caused rejection rates. Market entry barriers persist where design codes lag, yet pilot approvals under performance-based clauses unlock local monopolies for early movers. Fireproofing for petrochemical tanks, railroad sleepers for high-speed corridors, and subsea grouts for floating wind remain under-penetrated but lucrative. Suppliers that can supply third-party durability data are expected to capture these white-space segments before 2030. Strategic partnerships with steel mills, utilities, and oil-field service firms are forming to secure circular-economy inputs and specialty distribution.

Geopolymer Industry Leaders

Wagners

CEMEX SAB de CV

Schlumberger Limited

PCI Augsburg GmbH

Betolar PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Betolar Plc received the Finnish Chemical Society's 2024 Circular Economy Innovation Award for its geopolymer methods that convert industrial waste into low-carbon building materials, reducing CO2 emissions by up to 80% compared to traditional concrete.

- August 2024: Green 360 Technologies has announced the successful production and delivery of its first low-carbon geopolymer precast product, intended for hardscaping and demonstration purposes in a major government infrastructure project.

Global Geopolymer Market Report Scope

Geopolymers are formed by the reaction between an alkaline solution and an aluminosilicate source or feedstock. Geopolymers are inorganic, two-component, aluminosilicate binders activated by an alkaline activator.

The market is segmented by product type, application, precursor/raw material, and geography. By product type, the market is segmented into cement, concrete, and pre-cast panels, grout and binder, and other product types. By application, the market is segmented into building, road and pavement, runway, pipe and concrete repair, bridge, tunnel lining, railroad sleeper, coating application, fireproofing, nuclear and other toxic waste immobilization, and specific mold products. By precursor/raw material, the market is segmented into fly ash-based, slag-based, metakaolin-based, rice-husk ash and agricultural wastes, and others (including red mud, bauxite residue, waste glass, and basalt powders). The report also covers the market sizes and forecasts for the geopolymer market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Cement, Concrete and Pre-cast Panels |

| Grout and Binder |

| Other Product Types |

| Building |

| Road and Pavement |

| Runway |

| Pipe and Concrete Repair |

| Bridge |

| Tunnel Lining |

| Railroad Sleeper |

| Coating Application |

| Fireproofing |

| Nuclear Other Toxic Waste Immobilization |

| Specific Mold Products |

| Fly Ash Based |

| Slag Based |

| Metakaolin Based |

| Rice-Husk Ash and Agricultural Wastes |

| Others (Red-Mud and Bauxite Residue and Waste Glass and Basalt Powders) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Product Type | Cement, Concrete and Pre-cast Panels | |

| Grout and Binder | ||

| Other Product Types | ||

| By Application | Building | |

| Road and Pavement | ||

| Runway | ||

| Pipe and Concrete Repair | ||

| Bridge | ||

| Tunnel Lining | ||

| Railroad Sleeper | ||

| Coating Application | ||

| Fireproofing | ||

| Nuclear Other Toxic Waste Immobilization | ||

| Specific Mold Products | ||

| By Precursor/Raw-Material | Fly Ash Based | |

| Slag Based | ||

| Metakaolin Based | ||

| Rice-Husk Ash and Agricultural Wastes | ||

| Others (Red-Mud and Bauxite Residue and Waste Glass and Basalt Powders) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the geopolymer market in 2031?

The market is forecast to reach USD 16.15 billion by 2031 under a 10.88% CAGR from USD 9.64 billion in 2026.

How do geopolymers cut embodied carbon compared with Portland cement?

Lifecycle studies show lower CO₂ emissions, which helps public projects meet aggressive carbon thresholds.

Which application is expanding fastest through 2031?

Nuclear and toxic-waste immobilization is expected to grow at an 11.25% CAGR as aging reactors enter decommissioning.

Why is metakaolin becoming a preferred precursor?

Coal-plant closures limit fly-ash supply, and metakaolin enables ambient curing, cutting energy costs in precast operations.

Which region offers the highest growth potential beyond 2026?

The Middle-East and Africa region is poised for a 10.92% CAGR, led by mega-projects like NEOM and offshore retrofits.

What limits the broader adoption of geopolymer concrete in buildings?

A lack of harmonized design standards, particularly in ASTM and ACI codes, adds months to permitting and raises engineering costs.

Page last updated on: