GCC ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

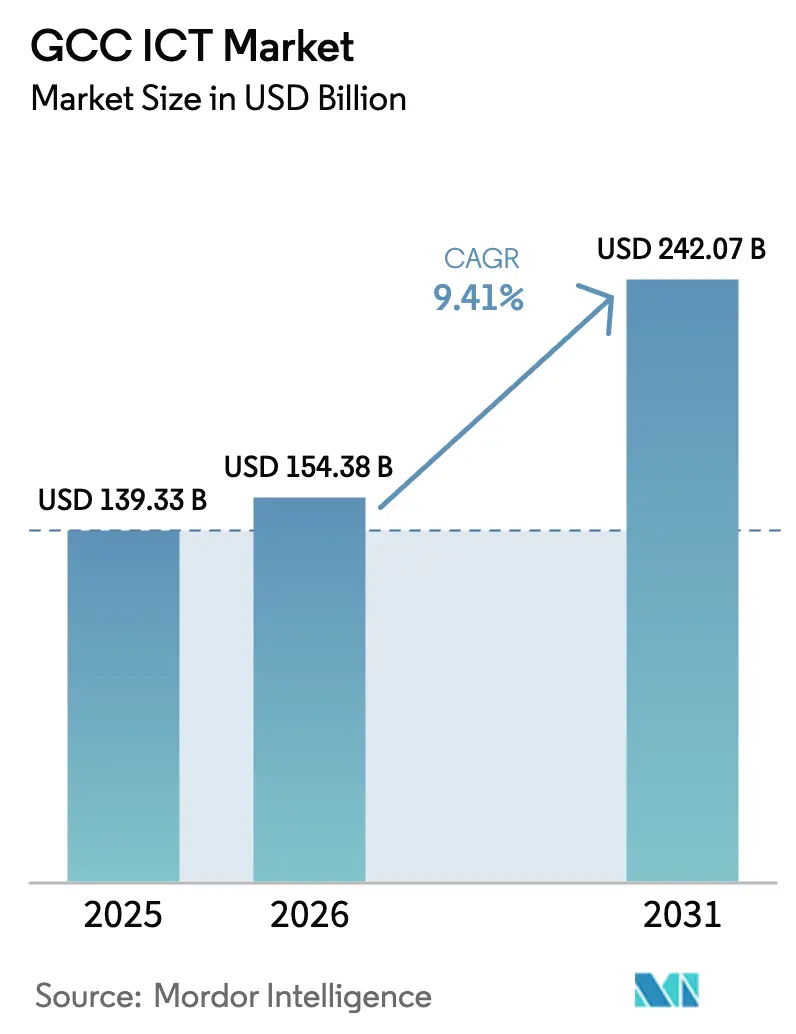

| Base Year Market Size (2025) | USD 139.33 Billion |

| Market Size (2026) | USD 154.38 Billion |

| Market Size (2031) | USD 242.07 Billion |

| Growth Rate (2026 - 2031) | 9.41% CAGR |

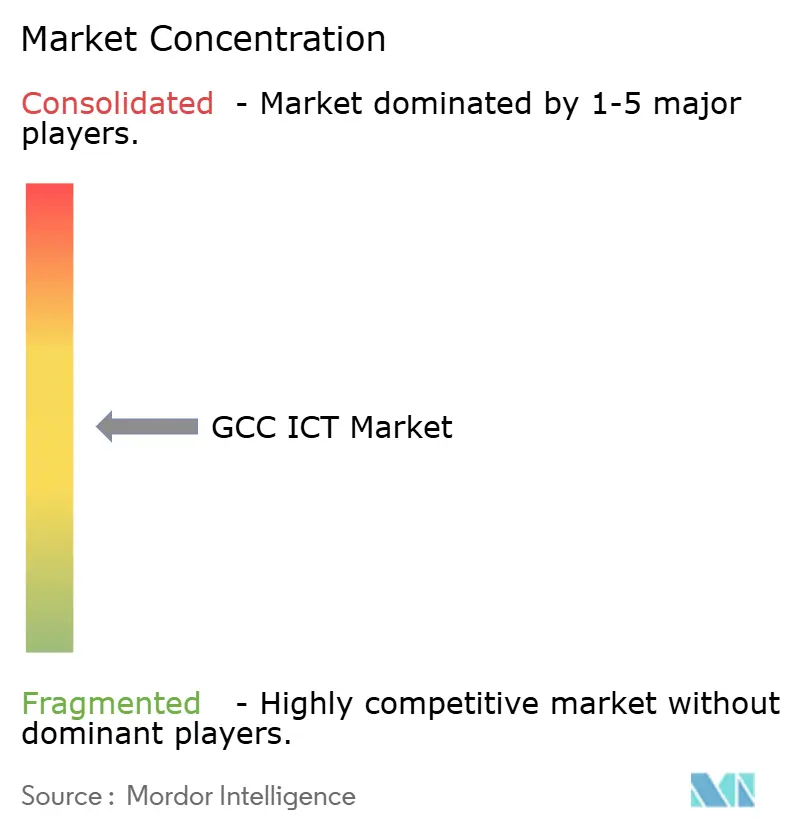

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

GCC ICT Market Analysis by ���ϲ�����

The GCC ICT Market size is expected to grow from USD 139.33 billion in 2025 to USD 154.38 billion in 2026 and is forecast to reach USD 242.07 billion by 2031 at 9.41% CAGR over 2026-2031. This trajectory underscores a structural pivot away from hydrocarbon dependence toward knowledge-based growth, steered by sovereign mandates that prioritize cloud migration, sovereign data centers, and Arabic-language artificial intelligence. Robust fiscal headroom allows governments to pre-fund digital infrastructure, while 5G monetization, smart-city scaling, and mandatory cybersecurity frameworks sustain enterprise spending across verticals. Intensifying localization rules force global vendors to build in-country capacity, thereby lifting the GCC ICT market’s capital intensity but also anchoring long-term service revenues. Inflation-linked tariff reforms for electricity are accelerating investment in renewable power and liquid cooling, compressing margins in the near term yet catalyzing a shift to sustainable operations. Finally, a widening digital-skills gap remains the principal brake on execution timelines, pushing both public and private sectors to ramp up reskilling programs and talent visas.

Key Report Takeaways

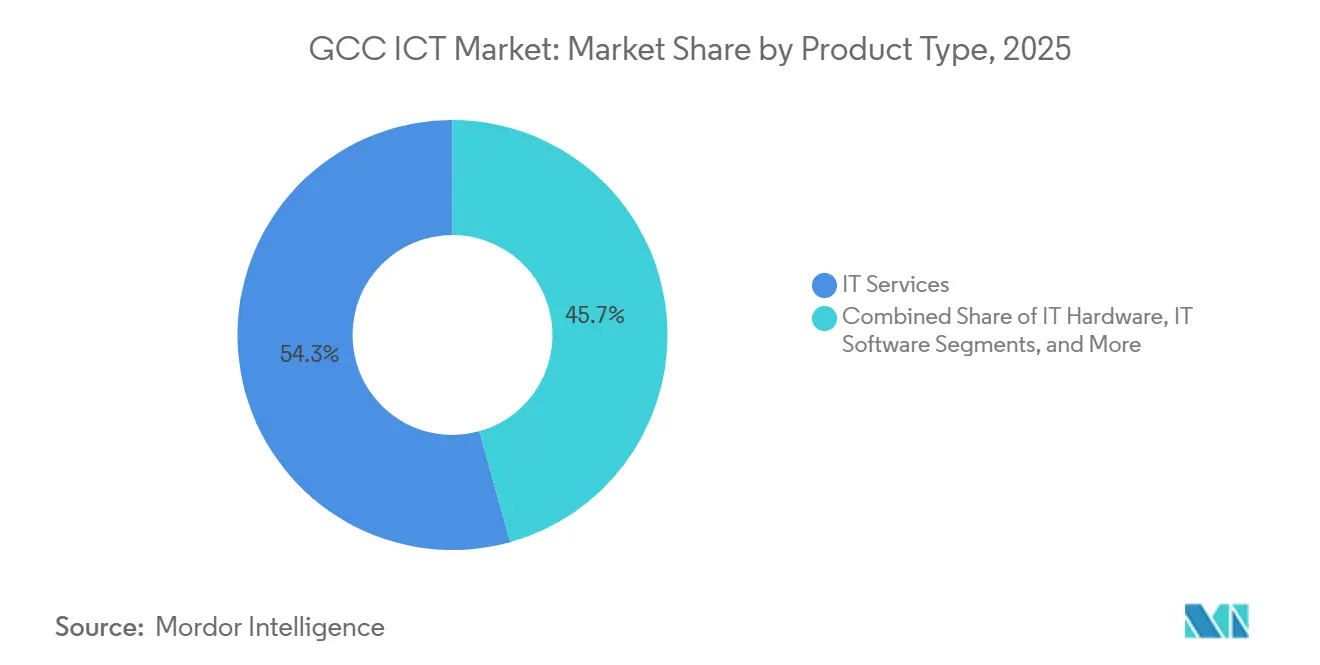

- By product type, IT Services led with 54.32% revenue share in 2025; IT Security and Cybersecurity is projected to expand at a 10.08% CAGR to 2031.

- By enterprise size, large enterprises held 63.14% of the GCC ICT market share in 2025, while SMEs are forecast to grow at a 9.82% CAGR through 2031.

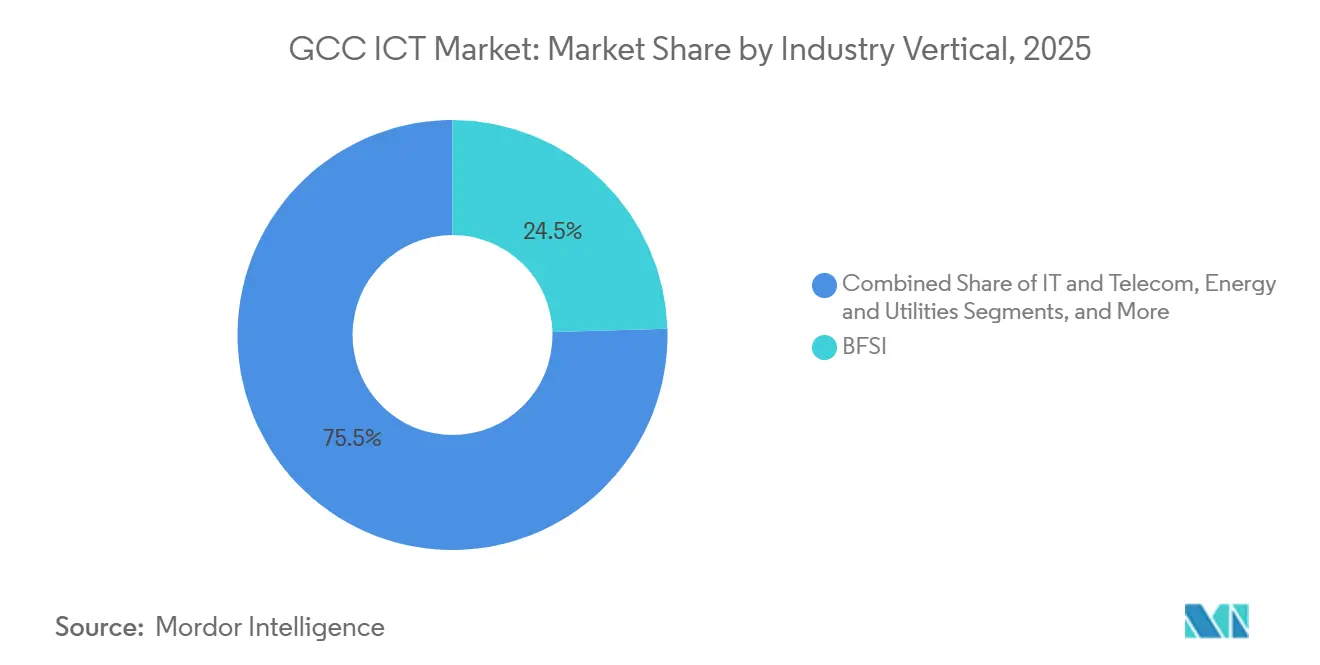

- By vertical, BFSI commanded 24.54% of spending in 2025; Healthcare and Life Sciences is advancing at an 11.19% CAGR to 2031.

- By geography, Saudi Arabia accounted for 55.27% of regional outlays in 2025, whereas Qatar is poised to expand at a 10.26% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC ICT Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Digital Transformation Initiatives | +2.1% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Expanding 5G Network Coverage | +1.8% | Saudi Arabia, UAE, Bahrain, Kuwait | Medium term (2-4 years) |

| Growth of Cloud Adoption Among Enterprises | +1.6% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Increasing Localization of Data Centers | +1.4% | Saudi Arabia, UAE, Qatar, Oman | Long term (≥ 4 years) |

| Rising Adoption of Arabic Language AI | +1.2% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Surge in Smart City Pilot-to-Scale Transitions | +1.0% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Government Digital Transformation Initiatives

Mandatory cloud migration, API-first service delivery, and paperless workflows are now baseline requirements for public entities across the Gulf. Saudi Arabia’s National Digital Transformation Strategy moved 178 agencies onto the Government Cloud Platform by December 2025, unlocking USD 4.2 billion in integration revenues and anchoring the GCC ICT market to multi-year managed-services contracts.[1]Saudi Data and AI Authority, “National Digital Transformation Strategy,” sdaia.gov.sa The UAE reached a 96% digital service delivery rate in 2025 under its Smart Government program, which standardized APIs across 1,200 public services. Qatar’s blockchain customs platform cut port dwell times by 35% in 2024, offering a regional blueprint for trade facilitation. These initiatives lengthen sales cycles but guarantee annuity revenues for vendors that secure compliance credentials.

Expanding 5G Network Coverage

Fifth-generation rollouts enable low-latency use cases in logistics and telehealth but remain capital-intensive outside dense corridors. Saudi Telecom Company raised 5G population coverage to 72% in 2025 and earmarked SAR 15 billion (USD 4 billion) to hit 85% by 2027. Emirates Telecommunications Group achieved 95% coverage in Abu Dhabi and Dubai, supporting autonomous-vehicle pilots and telesurgery. Regulatory pressure is mounting. Bahrain introduced mandatory network slicing in 2025, letting enterprises reserve dedicated bandwidth. Rural gaps in Oman and Kuwait persist because mountainous terrain doubles site costs, underscoring the need for subsidy mechanisms.

Growth of Cloud Adoption Among Enterprises

Data-sovereignty rules have forced enterprises to pivot from Europe-hosted workloads to in-country cloud zones, propelling hyperscaler investment and enlarging the GCC ICT market. AWS’s Dammam region onboarded 340 customers within 90 days of its March 2025 launch, including Saudi Aramco’s digital-twin platform. Azure’s UAE Central processed 18 exabytes in 2025, a 140% jump on the prior year. Google Cloud and Saudi Telecom Company built a sovereign cloud where encryption keys stay with the Saudi regulator, unlocking defense and energy workloads. Hybrid architectures now dominate, with 68% of enterprises retaining latency-sensitive systems on-premises while shifting analytics to public clouds.

Increasing Localization of Data Centers Under GCC Data Sovereignty Rules

Data-sovereignty statutes enacted in Oman, Qatar, and the UAE require citizen data to remain within national borders, stoking demand for local capacity and reshaping capex patterns. Oman’s Personal Data Protection Law sparked Oracle’s USD 400 million Muscat region, slated for Q2 2026. Qatar’s rules drove a 220% surge in colocation demand, lifting Doha rack rates 18% year-over-year. The UAE’s 2024 data-classification code accelerated Khazna’s expansion to 120 MW and attracted USD 2.1 billion from Digital Realty and Equinix. Operators must now replicate facilities in every jurisdiction, increasing capital intensity but also deepening domestic supply chains.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled ICT Professionals | -1.3% | Saudi Arabia, UAE, Qatar, Oman | Long term (≥ 4 years) |

| High Capex for Advanced Infrastructure | -0.9% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Energy Subsidy Reforms Impacting Data Center OpEx | -0.7% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Geopolitical Supply Chain Vulnerabilities | -0.6% | Qatar, Oman, Kuwait, Bahrain | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Shortage of Skilled ICT Professionals

The region faces a structural talent deficit; universities graduated only 22,000 computer science majors in 2024, while the projected demand is for 150,000 additional professionals by 2030. Saudi Arabia earmarked USD 800 million for cloud-and-AI upskilling, yet 35% of trainees relocate abroad within 18 months to chase higher pay.[2]Saudi Ministry of Communications and Information Technology, “National Technology Development Program,” mcit.gov.sa The UAE issued 100,000 “golden visas” to coders, but Arabic fluency and public-sector clearance remain hurdles. Enterprises are establishing captive academies, though the 18-24-month training lead time keeps the labor gap open until at least 2028.

High Capex for Advanced Infrastructure

Operators must outlay unprecedented sums for 5G, hyperscale data centers, and fiber. Saudi Telecom Company’s SAR 15 billion 5G program equaled 28% of revenue. Khazna’s push from 65 MW to 120 MW required USD 1.2 billion, lifting per-MW build costs to USD 12 million, twice the global baseline. Qatar’s fiber rollout demands USD 1.8 billion yet yields a 12-year payback, deterring private capital. Concentrated investment skews toward high-density corridors, leaving rural zones underserved.

Segment Analysis

By Product Type: Services Anchor Spending While Security Surges

IT Services captured 54.32% of 2025 outlays, underlining enterprises’ preference for outsourced migration, integration, and managed operations. The GCC ICT market for IT Services is projected to grow steadily as public entities migrate legacy systems to cloud-native platforms in line with sovereignty rules. Multiyear contracts, such as Accenture’s USD 320 million remit at Saudi Aramco, bundle change management and training into resilient revenue streams. Hardware’s share is easing as enterprises pivot to opex-based models, though edge appliances and ruggedized IoT gateways are pockets of growth in logistics and petrochemicals.

Cybersecurity is the fastest-growing category, advancing at 10.08% annually, fueled by a 340% spike in ransomware attacks and by mandatory frameworks such as Saudi Arabia’s Essential Cybersecurity Controls.[3]National Cybersecurity Authority, “Essential Cybersecurity Controls Framework,” nca.gov.sa Spending is shifting from appliance purchases to managed detection and response, where localized SOCs offering Arabic dashboards differentiate. The GCC ICT market continues to favor vendors that can harmonize zero-trust architectures with data-sovereignty compliance, a combination that global rivals still grapple with.

Note: Segment shares of all individual segments available upon report purchase

By Enterprise Size: SMEs Embrace Cloud While Large Enterprises Retain Hybrid Models

Large enterprises held 63.14% of spending in 2025, reflecting the capital heft behind refinery automation, core-banking upgrades, and nationwide e-health deployments. Core transformations, such as Emirates NBD’s USD 420 million modernization, which processed 2.8 million daily transactions by 2025, validate hybrid architectures that mix on-prem HPC clusters with sovereign cloud zones. The GCC ICT market size for large enterprises is forecast to grow at mid-single-digit rates as megaproject pipelines extend into the next decade.

SMEs, however, are closing the gap at a 9.82% CAGR, buoyed by Kuwait and Bahrain subsidy schemes that reimburse up to 75% of SaaS costs. Low-code platforms are reducing dependence on scarce developers, while regional telcos are bundling connectivity and cloud credits to de-risk adoption. Yet cyber exposure remains acute; 42% of surveyed SMEs reported at least one breach in 2025, reinforcing demand for affordable, managed security services across the broader GCC ICT market.

By Industry Vertical: Healthcare Digitalization Outpaces BFSI Maturity

BFSI accounted for 24.54% of 2025 demand, aided by instant payments and open banking mandates. The GCC ICT market share for BFSI is likely to stabilize as banks pivot from channel digitization to AI-driven risk analytics. Saudi Arabia’s instant payment rails processed 1.2 billion transactions in their first year, forcing real-time fraud detection platforms onto every core-banking road map.

Healthcare and Life Sciences is the breakout vertical, expanding at 11.19% annually through 2031. National EHR platforms such as Saudi Arabia’s Seha and the UAE’s Malaffi are generating massive data lakes for AI-based diagnostics, while telemedicine reimbursement codes ensure provider adoption. Interoperability standards drive spending on API-based integration, solidifying the segment as the fastest contributor to incremental GCC ICT market revenue over the forecast horizon.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Saudi Arabia’s 55.27% spending share stems from megaprojects like NEOM and a USD 40 billion Public Investment Fund earmark for digital infrastructure through 2030, giving the kingdom unmatched scale inside the GCC ICT market. The continuous expansion of sovereign cloud zones and private 5G networks within these projects keeps demand for system integration elevated.

The UAE remains the most digitally mature economy, boasting 95% smartphone penetration and near-universal 4G coverage, yet its growth trajectory moderates as consumer adoption saturates. Enterprise demand now pivots to AI-enabled services and green data-center capacity that mitigates post-subsidy power hikes.

Qatar shows the highest growth path, with a 10.26% CAGR, leveraging the World Cup legacy fiber and IoT networks. Government allocations of QAR 12 billion to extend fiber to 98% coverage by 2027 confirm long-run momentum. Oman, Kuwait, and Bahrain remain niche plays focused on logistics, fintech sandboxes, and hospitality digitization, collectively adding diversification but limited volume to the overall GCC ICT market size.

Competitive Landscape

Incumbent telecom operators, including Saudi Telecom Company, Emirates Telecommunications Group, and Ooredoo, harness nationwide fiber backbones and dense 5G footprints to bundle connectivity with managed cloud, security, and IoT services, making it costly for enterprises to switch providers. The top 10 vendors together captured about 42% of 2025 revenue, with the largest five holding just over 50%, a share that signals moderate consolidation pressure without tipping into oligopoly. Long-term master service agreements often span five to seven years, giving telcos predictable cash flows while locking in customers through escalating bandwidth and cybersecurity requirements. These operators also enjoy preferential access to public-sector tenders because sovereign shareholders view digital infrastructure as a strategic asset. As a result, smaller managed-service providers struggle to win large contracts unless they partner with incumbent carriers.

Hyperscalers are eroding telco dominance by building in-country regions that satisfy data-sovereignty rules, then co-selling services with local partners. Amazon Web Services opened its second Saudi region in Dammam in March 2025, adding 15 MW of compute and luring high-performance oil-and-gas workloads with a 40% latency cut. Oracle joined forces with Emirates Telecommunications Group in October 2025 on an USD 800 million sovereign cloud in Abu Dhabi, restricting administrative access to UAE nationals to accelerate government adoption. Microsoft committed USD 2.1 billion to expand its UAE Azure footprint in November 2025 and embedded Arabic language models directly into Azure AI, turning localization into a product differentiator. System integrators such as Tata Consultancy Services and Accenture ride this wave by stitching multi-cloud, on-premises, and edge environments for ministries and banks, exemplified by TCS’s USD 280 million project to modernize Saudi Arabia’s Ministry of Interior core applications in 2024. Because these projects hinge on regulatory compliance and Arabic-language interfaces, global SIs increasingly staff local delivery centers with bilingual engineers.

Cybersecurity remains the most fragmented battlefield, yet it is also the fastest expanding. Palo Alto Networks, Fortinet, and Check Point grow through hardware refresh cycles, while regional specialists like Elm in Saudi Arabia and DarkMatter in the UAE gain share by offering 24/7 managed detection staffed by Arabic-speaking analysts with security clearances. IBM filed 14 Arabic natural-language-processing patents during 2024-2025, signaling a push to license core AI models that smaller vendors will integrate into chatbots and threat-hunting platforms. G42 is building an integrated stack spanning chips, cloud, and AI, positioning itself as a regional alternative to U.S. hyperscalers for sensitive public-sector workloads. Taken together, these moves show that technology leadership, localization depth, and government relationships outweigh price alone in determining who captures the next wave of GCC ICT spending.

GCC ICT Industry Leaders

Emirates Telecommunications Group Company PJSC (e&)

Saudi Telecom Company

Ooredoo Q.P.S.C.

IBM Corporation

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Saudi Telecom Company and Ericsson signed a USD 1.2 billion deal to deploy 5G standalone core across 14 Saudi cities, targeting sub-5-millisecond latency for NEOM autonomous-vehicle tests.

- November 2025: Microsoft pledged USD 2.1 billion to expand its UAE Azure region, adding 25 MW and embedding Arabic language models in Azure AI to back government digitization.

- October 2025: Emirates Telecommunications Group and Oracle created an USD 800 million sovereign cloud joint venture in Abu Dhabi, restricting admin access to UAE nationals.

- September 2025: Ooredoo launched a private 5G network at Hamad Port with 180 base stations, trimming vessel turnaround by 18%.

GCC ICT Market Report Scope

The GCC ICT market includes the amalgamation and adoption of different Information and Communications Technologies (ICT), such as big data, mobility, storage, outsourcing, and cloud computing in the GCC countries for the purpose of digitization, digital transformation, and tracking the revenue accrued through the sale of technology-related solutions.

The GCC ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security/Cybersecurity, Communication Services), Enterprise Size (Small and Medium-sized Enterprises, Large Enterprises), Industry Vertical (Government and Public Administration, BFSI, IT and Telecom, Energy and Utilities, Retail, E-commerce, and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, Other Industry Verticals), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Oman, Kuwait, Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

| Small and Medium-sized Enterprises |

| Large Enterprises |

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Industry Verticals |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Kuwait |

| Bahrain |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Industry Verticals | ||

| By Geography | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Oman | ||

| Kuwait | ||

| Bahrain | ||

Key Questions Answered in the Report

How fast will cloud spending grow in the GCC ICT market through 2031?

Enterprise cloud outlays are projected to rise at a 1.6 percentage-point premium to the overall market CAGR, driven by sovereign regions launched since 2024 and mandatory data-localization rules.

Which country will see the quickest ICT growth through 2031?

Qatar leads with a forecast 10.26% CAGR, leveraging World Cup legacy fiber, standalone 5G, and USD 3.3 billion earmarked for nationwide IoT coverage.

What is the biggest restraint on digital transformation projects in the Gulf?

A shortage of skilled ICT professionals, estimated at 150,000 by 2030, inflates labor costs and extends project timelines despite ongoing reskilling initiatives.

Why is cybersecurity spending accelerating faster than overall ICT budgets?

Ransomware incidents surged 340% between 2023-2025, and new compliance frameworks mandate real-time monitoring, driving a 10.08% annual rise in IT Security and Cybersecurity outlays.

How are energy subsidy reforms affecting data centers?

Industrial tariff hikes of up to 78% are compressing margins, prompting operators to invest in solar power and liquid cooling that cut electricity use by about 30% over time.

What is the main challenge facing data centers?

Industrial electricity prices averaging EUR 0.25-0.30 per kWh double the EU mean, inflating operating costs and delaying facility expansion.

How large will the GCC ICT market be by 2031?

It is forecast to reach USD 242.07 billion, up from USD 154.38 billion in 2026 under an 9.41% CAGR.